115

CENTRE FOR THE PROMOTION OF IMPORTS FROM DEVELOPING COUNTRIES FOOD INGREDIENTS FOR INDUSTRIAL USE EU MARKET SURVEY 2002 VOLUME II VOLUME II

Mailing address: P.O. Box 30009, 3001 DA Rotterdam, The NetherlandsPhone: +31 10 201 34 34 Fax: +31 10 411 40 81E-mail: [email protected] Internet: http://www.cbi.nl

Office and showroom: WTC-Beursbuilding, 5th floor37 Beursplein, Rotterdam, The Netherlands

CENTRE FOR THE PROMOTION OF IMPORTS FROM DEVELOPING COUNTRIES

FOOD INGREDIENTS FOR INDUSTRIAL USE

FOO

D IN

GR

ED

IEN

TS

FOR

IND

US

TR

IAL U

SE

EU MARKET SURVEY 2002

EU

MA

RK

ET

SU

RV

EY

2002V

OLU

ME

II VOLUME II

EU MARKET SURVEY 2002

FOOD INGREDIENTS FOR INDUSTRIAL USE

Compiled for CBI by:

ProFoundADVISERS IN DEVELOPMENT

in collaboration withIr. A.F. Eshuis

July 2002

DISCLAIMERThe information provided in this survey is believed to be accurate at the time of writing. It is, however, passed on to the reader without any responsibility on the part of CBI or the authors and it does not release the reader from theobligation to comply with all applicable legislation.

Neither CBI nor the authors of this publication make any warranty, expressed or implied, concerning the accuracy of the information presented, and will not be liable for injury or claims pertaining to the use of this publication or the information contained therein.

No obligation is assumed for updating or amending this publication for any reason, be it new or contrary informationor changes in legislation, regulations or jurisdiction.

New CBI Publication with new format and contents, partly replacing CBI market surveys:• Grains and Pulses, April 1998• Natural Gums and Resins, March 1999• Essential Oils and Oleoresins, January 1999• Natural Food Colours and Flavours, May 1999• Dried Fruit and Edible Nuts, May 1999• Oil Seeds, April 1998

Photo courtesy:

Catz International BVThe Netherlands

CONTENTS

REPORT SUMMARY 6

1 PRODUCT CHARACTERISTICS 81.1 Product groups 81.2 Customs/statistical product classification 11

2 INTRODUCTION TO THE EU MARKET 13

3 CONSUMPTION 153.1 Market size 153.2 Market segmentation 223.3 Consumption patterns and trends 25

4 PRODUCTION 28

5 IMPORTS 325.1 Total imports 325.2 Imports by product group 385.3 The role of the developing countries 52

6 EXPORTS 54

7 TRADE STRUCTURE 577.1 EU trade channels 577.2 Distribution channels for developing country exporters 61

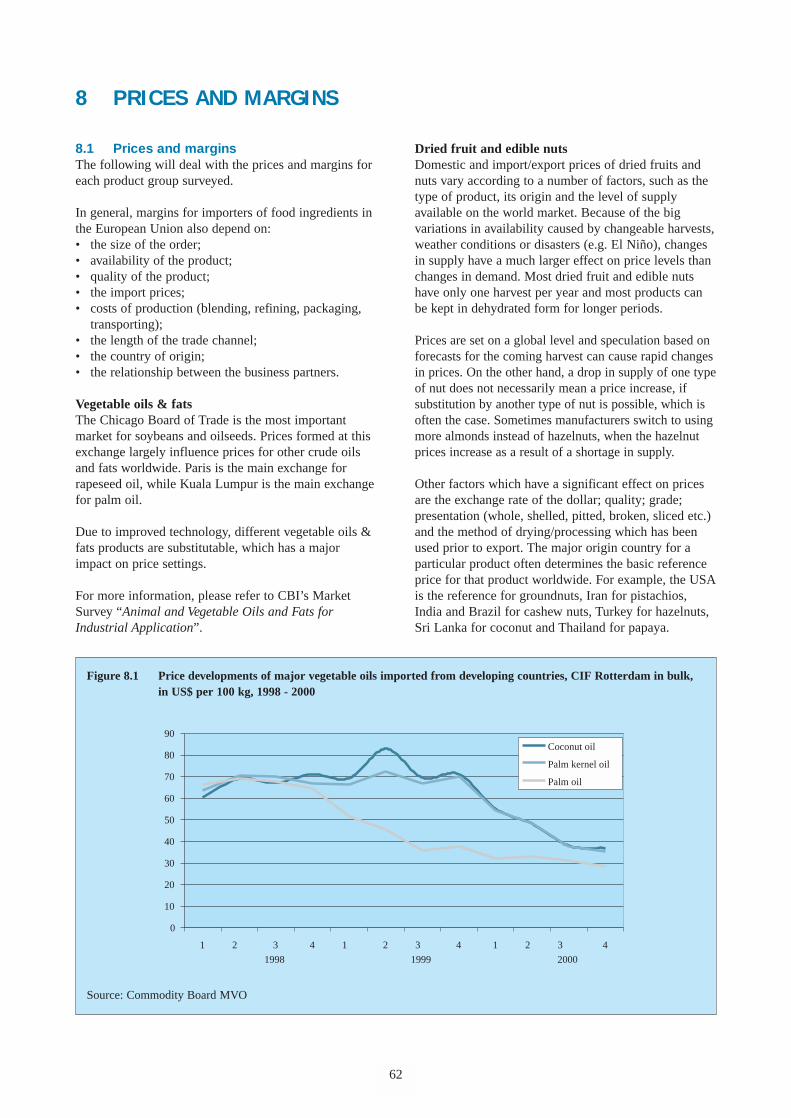

8 PRICES AND MARGINS 628.1 Prices and margins 628.2 Sources of price information 70

9 OPPORTUNITIES FOR EXPORTERS 73

APPENDICES 761 HS code classification of food ingredients for industrial use 762 Detailed import/export statistics 793 Standards organisations 914 Sources of price information 935 Trade associations 946 Trade fair organisers 987 Trade press 998 Trade promotion organisations 1009 Other useful addresses 10110 List of developing countries 10311 List of Netherlands importers and most important EU importers 10412 Useful Internet sites 111

5

REPORT SUMMARY

This EU market survey profiles the EU market for foodingredients for industrial use. The emphasis of thesurvey lies on those products which are of importanceto developing country suppliers. The major nationalmarkets within the EU for those products arehighlighted. The survey includes contact details ofimporters, trade associations, and other relevantorganisations. Furthermore, statistical marketinformation on consumption, production and trade,and information on trade structure and prices andmargins is provided.

As an exporter you need this information in order toformulate your own market and product strategies.To assist you with this, CBI has developed a matchingEU Strategic Marketing Guide “Food Ingredients forIndustrial Use”. It offers a practical handbook forexporters engaged, or wishing to engage, in exportingfood ingredients for industrial use to the EuropeanUnion. It aims to facilitate exporters in formulatingtheir own market and product strategies, through theprovision of practical information and a methodologyof analysis and ready-to-fill-in frameworks.

As mentioned above, statistical market information onconsumption, production and trade, and informationon trade structure and prices and margins, which isrequired for the ready-to-fill-in frameworks, can befound in this EU Market Survey.

Market researchThis EU Market Survey and the EU StrategicMarketing Guide serve as a basis for further marketresearch: after you have read this survey and thenfilled in the frameworks in the strategic marketingguide, it is important to further research your targetmarkets, sales channels and potential customers.

Market research depends on secondary data (data thathave been compiled and published earlier) and primarydata (information that you collect yourself). An exampleof secondary data is this EU Market Survey.Primary data are needed when secondary data fall shortof your needs, for example when researching yourspecific type of consumer about the acceptance of yourspecific product. Sources of information are, amongothers, (statistical) databanks, newspapers andmagazines, market reports, (annual) reports from branchassociations, but also shops in target countries, productsor catalogues from your competitors, and conversationswith suppliers, specialists, colleagues and evencompetitors. After you have received/collected yourinformation, you should analyse it. In order to judge theattractiveness of the market, sales channel or customer,you should use/develop a classification or score system.

6

For more detailed information on market research,reference is made to CBI’s Export Planner (2000).

ConsumptionThanks to increased prosperity in the EU, eatingbehaviour is related to income and life style. Despitethis increase in prosperity, the food market in the EU ishighly competitive, since consumers are not going toeat more, but will only, at the very most, switch to otherproducts.

Recent research into EU consumer behaviour showsthat today’s consumer has the following preferencesconcerning food and nutrition:• Safe food• Healthy food• Organic food• Fruit and vegetables• Environment-consciousness• Convenience• Variety• ‘Grazing’: smaller bites in between meals• Internationalisation: increased demand for ethnic and

exotic ingredients

Distribution structureThe food ingredient channel embraces business-to-business transactions involving sales of ingredients forfurther manufacturing. Changes in the foodmanufacturing/ingredients industry are reflected inconcentration, globalisation and partnerships.Technical innovation, necessitating a high level ofspending on R&D, is seen as critical to competesuccessfully in the marketplace. Companies need tocontinually originate, formulate and bring newingredients to the market quickly, while focusing oncustomers’ applications and processes, investing inmanufacturing capability, culinary resources, technicaladvances and sensory services to meet the demands ofthe market.

These changes in food manufacturing have importantimplications for suppliers such as:• Size of manufacturing plants. • Fulfil and/or complement customers’ R&D function.• Partnership arrangements with key customers.• Develop added value products.• Innovation as a key to competitive advantage. • Tracking and tracing: introduction of chain

management and labelling systems, through whichproducts can be traced back to the producer.

• The emphasis on food safety requires continuingdevelopments in the areas of traceability, food safetyassurance schemes, hygiene and training initiatives.

ImportsThe leading EU importers for food ingredients forindustrial use are Germany, France, the UnitedKingdom, The Netherlands and Italy. At the level ofproduct groups, however, there can be other countries,which are important markets. Spain, for example, is animportant market for pulses, while Portugal representsthe second leading EU importer of sugars.

Although vegetable oils & fats imports from developingcountries decreased considerably between 1998 and2000, it remained the leading product group suppliedby developing countries in absolute terms. During thesame period, only the values of spices & herbs,pulses, seeds and vegetable saps & extracts increased.

If we look at the shares of developing countries in EUimports, developing countries were particularly strongin sugars, seeds, spices & herbs, natural gums & resinsand honey. In 2000, developing countries supplied over50 percent of the imports (in value) by EU membercountries of these products. China, Indonesia, India,Argentina, Iran, and Turkey are among the leadingdeveloping countries supplying the EU with foodingredients for industrial use.

OpportunitiesIf the food-processing has taught the ingredientsuppliers anything in the past years, it is that there isonly enough room for a limited number of suppliersand, to succeed, one needs to be a technicallyknowledgeable partner. It is to be expected that the highinvestments in research and development of newproducts could constitute a problem for a developingcountry.

7

The advice that we can give in order to be successful inthe competitive food market is:• Offer a ‘concept’: a product should include complete

product specifications, suggestions for application,instructions on how to store and to process,proposals for product presentation, information onquality assurance (e.g. HACCP) or even ISOcertification.

• Go ‘organic’: healthy, natural and organic productsare occupying an increasingly stronger position inthe EU. This applies to the consumer market aswell as to the food industry. Organic production isparticularly attractive for growers in developingcountries, since much of their food production isalready organic or can be changed to organic.

For more information, please refer to CBI’s EUMarket Survey “Organic Food Products”.

• Adopt HACCP: adopting a system of quality control,will be a very positive argument in export business.

• Adopt standards for Good Agricultural Practice.

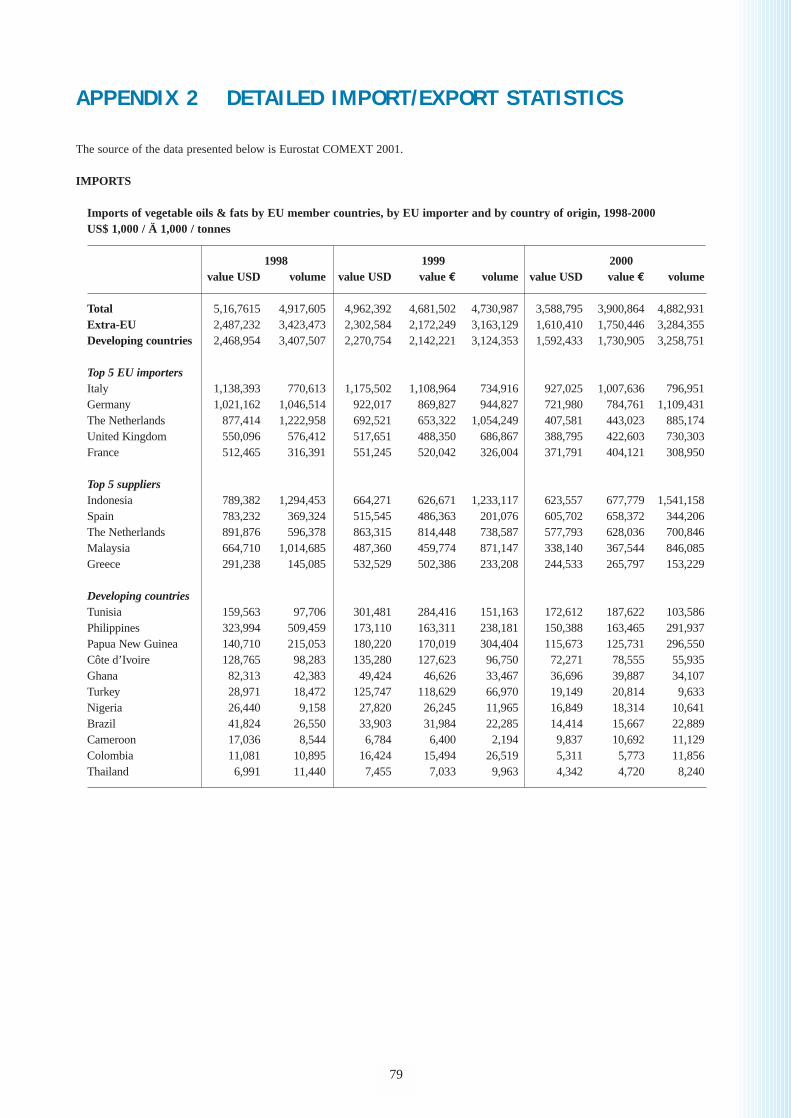

EU imports of food ingredients originating in developing countries, 2000,US$ 1,000,000 / € 1,000,000 / 1,000 tonnes

value US$ value € volume

Vegetable oils & fats 1,592 1,731 3,259Dried fruit & edible nuts 1,572 1,709 965Sugars 908 987 3,831Spices & herbs 461 502 148Natural gums & resins 315 342 314Pulses 196 214 294Essential oils & oleoresins 193 210 27Dried vegetables 137 148 58Honey 117 128 118Seeds 83 90 118Natural colours & flavours 77 84 9Vegetable saps & extracts 13 14 4

1 PRODUCT CHARACTERISTICS

1.1 Product groups Food ingredients for industrial use encompass anenormous diversity of product groups. In this survey wewill focus on a limited number of product groups whichare interesting for exporters in developing countries.The ingredients discussed in this survey fall in thefollowing groups, ranking in order of importance:• Vegetable oils and fats • Dried fruit and edible nuts • Sugars (exotic)• Spices and herbs• Natural gums and resins• Essential oils and oleoresins • Pulses• Dried vegetables• Natural colours and flavours• Honey • Seeds • Vegetable saps and extracts

It is important to note, however, that some of theingredients are not only traded for the food industry,but also find their way to the cosmetic andpharmaceutical industries. A number of the aboveproduct groups are dealt with in more detail in thefollowing CBI’s surveys:

The above product groups, concerning organicproducts, are also dealt with in CBI’s EU MarketSurvey “Organic Food Products”.

Characteristics of products groups discussed in thissurvey are described below briefly.

Vegetable oils & fatsOil seeds are mainly processed, by crushing or solventextraction, into vegetable oil. Groundnuts form themajor exception. The kernels are mainly used in snacks

and confectionery, or used as bird feed and forprocessing into peanut butter, while the remainder isused for processing into arachide oil.

Vegetable oils and fats constitute about 80% of totaledible oils and fats production. They form majorconstituents of the food chain. Performance and useof vegetable oils are determined by the fatty-acidcomposition.

It should be noted that this market survey only dealswith a selected group of vegetable oils, while CBI’s EUMarket Survey “Animal and Vegetable Oils and Fats forIndustrial Use” covers a wider range of oils and fats.For more information, please refer to the surveymentioned earlier.

Dried fruit and edible nutsDried fruit can be divided into vine fruit and tree fruit.The best-known vine fruit species are raisins, sultanasand currants, whereas apples, apricots, bananas, dates,figs, papayas, peaches, pears and prunes are the mostimportant tree fruits. Dried fruit is mainly used as asnack or a constituent for breakfast cereals, muesli,bakery products, dairy products and desserts.

There are two segments for edible nuts: groundnuts(peanuts) and luxury (tree) nuts. The most importanttypes of the latter for the European trade are almonds,hazelnuts, pistachios, coconuts, cashew nuts, walnutsand para- or Brazil nuts. Information on the relatedproducts may be found in the following CBI’s EUMarket Surveys:• “Fresh Fruit and Vegetables”• “Preserved Fruit and Vegetables for Industrial Use”

8

For more detailed information on spices and herbs, please refer to: EU Market Survey “Spices and Herbs”

For more detailed information on vegetable oils and fats, please refer to: EU Market Survey “Animal and Vegetable Oils andFats for Industrial Application”

For more detailed information honey, please refer to: EU Market Survey “Honey and Beeswax”

For more detailed information on dried fruit and vegetables, please refer to: EU Market Survey “Preserved Fruit and Vegetablefor Industrial Use”

For more detailed information on essential oils and oleoresins, EU Market Survey “Natural Ingredients forand vegetable saps and extracts, please refer to: Pharmaceuticals”

EU Market Survey “Natural Ingredients forCosmetics”

SugarsSugars are important ingredients in our food supply.While all fruits and vegetables produce sugar, the sugarcane and sugar beet plants contain the most accessiblestores of sucrose.

The sugar that results from sugar cane and sugar beetprocessing is the same sucrose that is found naturally inthe original plants and in fruits and vegetables. The rawsugar colour is removed by physical separation of plantmaterials and by carbon filters which absorb colouredimpurities. Since the pure sugar crystals are naturallycolourless, no bleaching or whitening is necessary.

A by-product of the cane and beet sugar refiningprocess is molasses, which has a multitude of uses.Molasses is important as a raw material for theproduction of antibiotics, bakers yeast, rum and alcohol,as well as an animal feed supplement.

Sugars have many different functions in foods. Forexample:• They provide sweetness to some foods. • They serve as preservatives in jams and jellies. • Sugar increases the boiling point or reduces the

freezing point of foods. • They are also essential for proper fermentation by

yeast. • Sugars react with amino acids to produce colour and

flavour compounds important to the taste and goldenbrown colour of baked goods.

• Sugars make foods, that have limited moisturecontent, crisp.

Spices and herbsThe main international trade for spices and herbs is indried and in crude form, cleaned but not furtherprocessed. It is estimated that about 85 precent of thetrade is in this form. The remaining trade concernscrushed or ground spices, essential oils or oleoresins.

For more detailed description of each major spice/herband its use, please refer to CBI’s EU Market Survey“Spices and Herbs”.

9

Natural gums and resinsAs far as gums are concerned, the survey only dealswith natural gums because most modified gums andsynthetic gums generally do not come from developingcountries. The product group of natural gums includesstrongly related products, such as seaweed extracts,pectin and starches, based on the fact that these are ofmuch relevance to developing countries.

Gums can be defined as polymeric material (generallycarbohydrates) which can be dissolved or dispersed inwater to give a thickening and/or gelling effect. Sincethese materials are collodial in nature, they are alsoreferred to as hydrophilic colloids or hydrocolloids inmore scientific terms. Hydrocolloids are mostly used inprocessed foods to provide texture, body and mouthfeel and to make it more difficult for dispersedmaterials to separate (i.e. to improve stability).

Of the natural gums mentioned in Table 1.1, gum larch,psyllium seed and quince seed are not discussed in thisreport, because these gums are very rarely used in theEuropean food industry. Gelatin is excluded because itis an animal product, while all others are of vegetableorigin.The group of starches is reduced to tapioca, sago andarrowroot starch, since these are the products importedfrom developing countries.

Resins are solid or semi-solid materials, usually acomplex mixture of organic compounds called terpenes,which are insoluble in water but soluble in certainorganic solvents. Resins are very widely distributed inthe plant kingdom although a few families are notablein accounting for a large proportion of the resins whichare traded (e.g. Leguminosae, Burseraceae andPinaceae). Most resins traded are obtained as exudatesby tapping. Resins are essential elements in themanufacturing of paints. They are also used in balms,natural coatings, cosmetics and glue products.This survey deals only with a particular kind of resins,the rosins. Rosin products find applications in many(often unrelated) industries, for a variety of purposes.Examples are the food industry, the paper industry,the pharmaceutical industry, the paint and ink industry.

Table 1.1 Classification of natural gums

Tree exudates and extracts Seed or root gums Seaweed extracts Others

Arabic Locust bean Agar-agar PectinTragacanth Guar Alginate GelatinKaraya Psyllium seed Carrageenan StarchesLarch Quince seed FurcellaranGhatti

Essential oils and oleoresinsEssential oils are aromatic, or odorous, oily liquids(sometimes semi-liquid or solid) obtained from plantmaterial, for example flowers, buds, seeds, leaves,twigs, bark, herbs, woods, fruits and roots.

The oils are volatile, i.e. they evaporate from thebotanical (plant) material upon heating. It is this highvolatility that distinguishes essential oils from fatty oils.They are usually soluble in alcohol or ether, but areonly slightly soluble in water. Essential oils, the mosthighly flavoured part of many spices and herbs, are ofhigher value than the spice itself. Essential oils areprobably the most important and largest single categoryof flavouring substances currently available to theflavourist.

Oleoresins are liquid preparations which are made bypercolating a volatile solvent through a ground spice orherb and subsequent elimination of the solvent by(vacuum-)evaporation.

Essential oils do not contain the non-volatilecomponent of the spice, therefore, the flavour profile isincomplete. Oleoresins consist of essential oils, resinsand the components that provide pungency in a spice.Oleoresins are total extracts of the natural spice or herb,representing the volatile and the non-volatilecomponents of the spice or herb. Compared to essentialoils, the oleoresins display greater stability towardshigh-heat applications and have flavour characteristicsmore like the natural dry spice than the correspondingessential oils. Therefore, oleoresins are used where afull range of flavour is required, such as in producingprocessed meats.

For more information, please refer to CBI’s MarketSurvey “Natural Ingredients for Cosmetics”.

Pulsesthe focus within this product group will be on kidneybeans, chickpeas and broad & horse beans. The groupsare small, however, they are important for exporters indeveloping countries.

Dried vegetablesVegetables, consisting of more than 80 percent of water,are dried in order to stop disintegration and spoilagethrough physical processes and the multiplication ofmicro-organisms. These organisms obtain the water andnutrients they need for growth from the vegetable inwhich they grow. By drying or dehydrating vegetables,the water is removed from the food and from thebacterial cell, thus ending its multiplication. The driedvegetables described in this survey can be whole, cut,sliced, broken or powdered, but not further prepared.

10

Although some vegetables are sun-dried or field-dried,most vegetables are dehydrated industrially. The maindehydrated vegetables are onions, tomatoes, garlic,carrots and olives. The Netherlands HorticultureCommodity Board’s definition of dried vegetables isused in this survey, resulting in the exclusion of driedleguminous vegetables (for example, dried peas andbeans; these belong to the special category of pulses).The sauce, soup and ready-meal processors are themain consumers of dried vegetables.

Natural food colours and flavoursThe natural colours can be divided into two categories:• those derived from natural foods by physical

processes, e.g. beetroot red;• those derived by various processes from natural

sources which are not normally consumed as food,e.g. cochineal;

Colours which can be used in food are available in thefollowing different forms:• powder: a dried substance on a neutral carrier. It has

a high percentage of colour substance. Powder is themost common form of dye found in the marketplace.It is easy to dissolve in food products. However,it can expose handlers’ dust and cause cross-contamination between product lines;

• blended powders: the advantage of a blendedpowder is that it negates the need for operatives tocharge individual primary colours;

• solutions in water, oil, alcohol or other permittedorganic solvents;

• emulsions: ground suspensions of a pigment in acarrier in which the pigment is not soluble.The emulsion is already dispersible in aqueoussystems, has improved stability to oxidation, pH,heat and light, and is suitable for use in manydifferent applications;

• granulars: granulated dye blends provide acontrolled product in a dust-free formulation.

Flavours in food play an important role in theacceptance and consumption of products and in thequality of life in general. Food acceptance by humans isdetermined mainly by appearance and texture, butflavour is also very important. For example, spices areadded to food not for their nutritional value, but fortheir taste and flavour. Furthermore, aromas thatdevelop during frying and baking enhance theenjoyment of food.

A great variety of flavourings is needed to impart flavour,and people differ in their appreciation of flavour.Aromatic compounds are found in nature, but have alsobeen synthetically manufactured.The use of flavours is necessitated for several reasons:• to create a totally new taste;• to enhance, extend, round out or increase the potency

of flavours already present;• to mask other undesirable flavours (as in

pharmaceuticals);• to donate flavour to food which is otherwise

flavourless (e.g. boiled sweets; soft drinks, edible ices,milk desserts etc.);

• flavour ingredients can stimulate other moreexpensive flavours or replace unavailable flavours;

• to reinforce aromatics which are lost in the processingof foods (like concentrated citrus fruit juices,pasteurised foods, syrups, etc.).

Flavours are presented to the market place in threeprimary forms, i.e., liquids, powders, and pastes.There are several subforms within the three primaryforms. The subgroups can be called flavour forms.Examples of the various forms include:1 Liquids: water-soluble, oil-soluble, and emulsions;2 Powders: spray dried and extended (plated);3 Pastes: fat-based, starch, carbohydrate-based,

and protein-based.

HoneyHoney is the sweet substance produced by the honeybee from the nectar of blossoms or secretions of or onliving parts of plants, and which the bees collect,transform and combine with specific substances of theirown and store and leave to mature in honey combs.

Honey is primarily composed of fructose, glucose andwater. It contains other sugars, as well as traceenzymes, minerals, vitamins and amino acids.Honey may include small traces of sucrose, maltose,melitose and other oligosaccarides (including dextrins),as well as traces of fungi, algea, yeast and other solidparticles resulting from the process of obtaining honey.The flavour, aroma and colour of honey differdepending on the nectar sources (the blossoms) visitedby the honey bees. The colour of honey ranges fromnearly colourless to dark brown, and the flavour variesfrom delectably mild to distinctively bold, dependingon where the honey bees buzzed.

For more detailed information, please refer to CBI’s EUMarket Survey “Honey and Beeswax”.

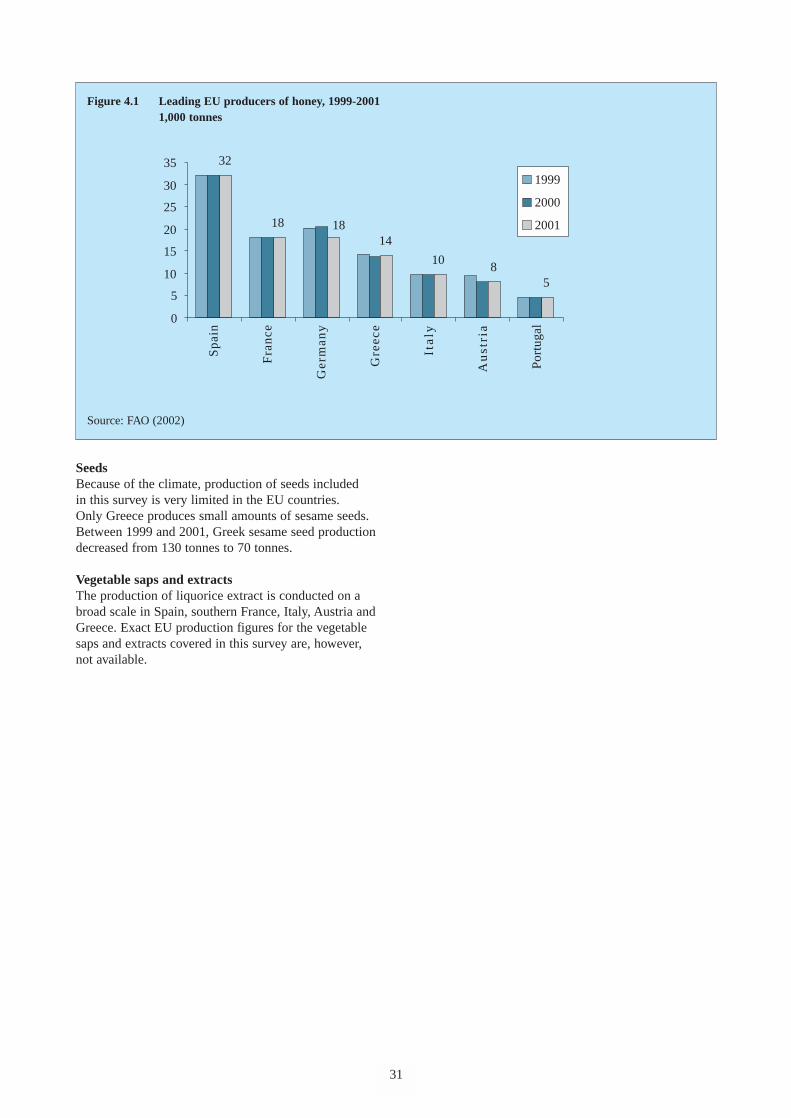

SeedsThe EU countries import relatively minor commodities,such as sesame seeds and hemp seeds, for furtherprocessing. Sesame seeds (Sesamum indicum), also

11

known as benniseed, gingelly, sim sim, and til, aresupplied to markets in North America, Europe, andEast Asia by countries in Africa, Latin America, andSouth Asia. Cooking oil can be extracted from sesameseeds, and this is their main use, especially in Asia.In North America and Europe, raw sesame seeds aregenerally used for toppings on breads such ashamburger buns, bagels, bread sticks, and other bakedgoods. Restaurants and natural food store customerspurchase sesame seeds for use in ethnic dishes.Middle Eastern countries use sesame seeds for tahinipaste and halvah, as well as for oil.

There are different types and qualities of sesame seeds.White seeds are a white-to-golden colour and receive ahigher market price than mixed seeds, which rangefrom yellow to dark brown. White seeds are usedprimarily in raw form because of their aesthetic value,whereas mixed seeds are generally crushed to oil.

The value of sesame seeds depends on their purity,expressed as a percentage, and oil content, whichshould exceed 50 percent. Hulling seeds, or removingtheir thin husk, increases their value as does bleachinghulled seeds. Moisture content and free fatty acidcontent are also important in assessing value.The highest-quality sesame seeds are found in CentralAmerica, primarily in Guatemala.

Vegetable saps and extractsVegetables saps and extracts are also used as flavoursand colours in food products. Therefore, one is referredto information on natural colours and flavours fordetailed information. It should be noted that a largenumber of this product group is used by themedical/pharmaceutical industry, and therefore,specific information is not available.

For more information on vegetable aps and extracts,please refer to CBI’s EU Market Survey “NaturalIngredients for Pharmaceuticals”.

1.2 Customs/statistical productclassification

On January 1, 1988, a unified coding system wasintroduced to harmonise the trading classificationsystems used world-wide. This system is called theHarmonised Commodity Description System (HS) andwas developed by the World Customs Organisation(WCO). The system comprises about 5,000 commoditygroups, each identified by a six digit code, arranged in alegal and logical structure and is supported by well-defined rules to achieve uniform classification.The system is used by more than 177 countries andeconomies as a basis for their Customs tariffs and forthe collection of international trade statistics. After thesix-digit code, countries are free to use furthersubheadings. In the trade data of Eurostat, an 8 digit

system is used. Most codes, however, end with twozeros, i.e. effectively only using 6 digits. In somecountries, even 10 digits are sometimes used.

Appendix 1 gives the four-to-eight-digit list of the mainHS codes for food ingredients for industrial use.

12

2 INTRODUCTION TO THE EU MARKET

The European Union (EU) is the current name for theformer European Community. Since 1 January 1995,the EU has consisted of 15 member states.Negotiations are in progress with a number of candidatemember states, many of which already have extensivetrade and co-operation agreements with the EU.It is envisaged that five of these countries will becomemembers in 2004.

According to the first demographic estimates for 2001,published on January 11, 2002 by Eurostat, thepopulation of the EU on 1 January 2001 was expectedto total 379.4 million. While the pace of populationgrowth in the EU has slowed greatly in the last 30years, the increase of 0.4% in 2001 was slightly higherthan the figure in recent years. Total GDP in 2000equalled US$ 7,856.6 billion at current prices, while theaverage GDP per capita (at current exchange rates)amounted to US$ 20,759 in 2000 (OECD, 2002).

The most important aspect of the process of unification(of the former EC countries) which affects trade is theharmonisation of rules in the EU countries. As theunification allows free movement of capital, goods,services and people, the internal borders have beenremoved. Goods produced or imported into onemember state can be moved around between the othermember states without restrictions. A precondition forthis free movement is uniformity in the rules andregulations concerning locally produced or importedproducts. Although the European Union is already afact, the regulations have not yet all been harmonised.Work is in progress on uniform regulations in the fieldsof environmental pollution, health, safety, quality andeducation.On January 1, 2002 the euro (€) became the legalcurrency used in 12 EU member states. It had alreadybeen in use since 1 January 1999, by banks as legalcurrency in eleven EU member states: Austria,Belgium, Finland, France, Germany, Italy, Ireland,

13

Exchange rates of EU currencies in US$

Country Currency 1997 1998 1999 2000 2001 June 2002

European Union ECU 1.13 1.12 - - - -€ - - 1.06 0.92 0.89 0.95

Denmark DKr 0.15 0.15 0.13 0.12 0.12 0.13Sweden SKr 0.13 0.13 0.12 0.11 0.10 0.10United Kingdom GB£ 1.64 1.66 1.62 1.51 1.45 1.48

Source: CBS Statline (July 2002)

Luxembourg, The Netherlands, Spain, and Portugal.Greece joined the Economic and Monetary Union(EMU) on 1 January 2001.

The most recent Eurostat trade statistics quoted in thissurvey are from the year 2000. In 1998, the EuropeanCurrency Unit (ECU) was still used as a monetaryinstrument by financial institutions to simplify financialprocedures. On 1 January 1999, statistical andcontractual values in ECU were converted into euroson a 1:1 exchange rate. The € / US$ exchange ratecurrently (June 2002) stands at around US$ 0.95 forone euro.

The US$ is the basic currency unit used to indicatevalue in this market survey. The Eurostat trade statisticsare based on the € values and transferred into US$ withthe exchange rates presented below.

Trade figures quoted in this survey must be interpretedand used with extreme caution. The collection of dataregarding trade flows has become more difficult sincethe establishment of the single market on 1 January1993. Until that date, trade was registered by means ofcompulsory Customs procedures at border crossings,but, since the removal of the intra-EU borders, this isno longer the case. Statistical bodies like Eurostatcannot now depend on the automatic generation of tradefigures. In the case of intra-EU trade, statisticalreporting is only compulsory for exporting andimporting firms whose trade exceeds a certain annualvalue. The threshold varies considerably from countryto country, but it is typically about € 100,000. As aconsequence, although figures for trade between theEU and the rest of the world are accurately represented,trade within the EU is generally underestimated.

This survey focuses on the five major EU markets forfood ingredients for industrial use. These are Germany,France, the United Kingdom, The Netherlands and

Italy. These EU member countries will be highlighted,because of their relative importance in terms ofconsumption, production, imports and exports.

14

3 CONSUMPTION

3.1 Market sizeUnderstandably, no detailed consumption figures areavailable for the overall group natural food ingredients.Ingredients are supplied to, and further processed by,the food industry. As the trade in these products isbusiness to business trade, there are no directconsumption figures available. Therefore, developmentsin the food retail market are first described below.Then the different product groups falling under foodingredients for industrial use will be discussed.

Overview of packaged foods marketThe global packaged foods market is forecast to growby 12 percent in real terms between 2000 and2004, or at just under 3 percent per annum. The threelargest sectors are bakery products, chilled food anddairy products. These three are forecast to account foralmost 50 of sales in 2004. The four smallest sectorsare baby food, spreads, fruit/nut/cereal bars and mealreplacement drinks, which are forecast to account foralmost 3 percent of total packaged grocery sales.

Oils/fats, canned food and frozen food are forecast to bethe fastest growing sectors at 29 percent, 23 percent and19 percent respectively. Sectors forecast to grow more

slowly than the global average are dairy products (10%),spreads (9%), confectionery (9%), bakery products (8%),chilled food (8%) and fruit/nut/cereal bars (3%).

Euromonitor data show that Germany is the largest foodmarket in Europe, followed by France and Italy.

Table 3.2 Consumer expenditure on food, 1997-1999US$ 1,000,000 / € 1,000,000

1997 1998 1999 1999US$ US$ US$ €

Germany 148,299 150,437 146,952 153,075France 115,314 116,175 112,900 117,604Italy 101,650 100,892 98,908 103,029UK 80,102 81,918 90,293 94,055The Netherlands 22,324 22,553 23,116 24,079

Source: Euromonitor (2001)

The Economic Research Service of the USDA operatesa per capita food consumption data system at

15

Table 3.1 World packaged foods markets, 2001-2004

2001 2002 2003 2004 2004 US$ € US$ € US$ € US$ € % of total

Bakery products 238.1 267.5 242.8 272.8 247.8 278.4 253 284.3 17.1Chilled food 221.7 249.1 225.4 253.3 230.3 258.8 235.3 264.4 15.9Dairy products 206.7 232.2 211.6 237.8 217.1 243.9 223 250.6 15.1Dried food 102.5 115.2 106.1 119.2 110.2 123.8 114.9 129.1 7.8Confectionery 107.9 121.2 110.2 123.8 112.7 126.6 115.3 129.6 7.8Ice cream/ yoghurts/ chilled desserts 102.2 114.8 105.5 118.5 108.8 122.2 112.2 126.1 7.6Frozen food 92.3 103.7 96.4 108.3 101 113.5 105.8 118.9 7.2Canned food 74.9 84.2 77.4 87.0 81 91.0 84.7 95.2 5.7Oils/fats 63.2 71.0 66.1 74.3 69.6 78.2 73.4 82.5 5Sauces/dressings/ condiments 60.3 67.8 62.6 70.3 65.2 73.3 68.1 76.5 4.6Savoury snacks 47.9 53.8 49.4 55.5 51 57.3 52.7 59.2 3.6Baby food 17.8 20.0 18.4 20.7 19.1 21.5 19.9 22.4 1.3Spreads 13.3 14.9 13.5 15.2 13.9 15.6 14.2 16.0 1Fruit/nut/cereal bars 3.1 3.5 3.2 3.6 3.4 3.8 3.5 3.9 0.2Meat replacement drinks 1.7 1.9 1.8 2.0 1.9 2.1 2 2.2 0.1

Total 1,353.50 1,390.60 1,432.80 1,478.00 100

Source: Euromonitor (2001)Note: Totals may not be the exact sum due to rounding off

www.ers.usda.gov/Data/FoodConsumption/index.htm.The European Commission also registers humanconsumption of certain agricultural products. The rangeof registration is, however, much more detailed thanthat of the USDA.

To gain a clear overview of the significance of the EUmarket for food ingredients, it is important to analysethe size and development of EU demand. Unfortunately,in practice, it is not possible to collect information withrespect to the demand for these product groups. This ismainly because the major products covered by thissurvey are used in various industries (cosmetic industry,divergent sectors of food industry, pharmaceuticalindustry). It is not possible from the statisticalinformation available to distinguish the food ingredientsused by these industries separately. It is, however,possible to give a general indication of the size andtrends of the EU market for the surveyed productgroups in general.

Below, the focus will be on the food market of theselected EU countries. Then, the market for each foodingredient surveyed will be dealt with.

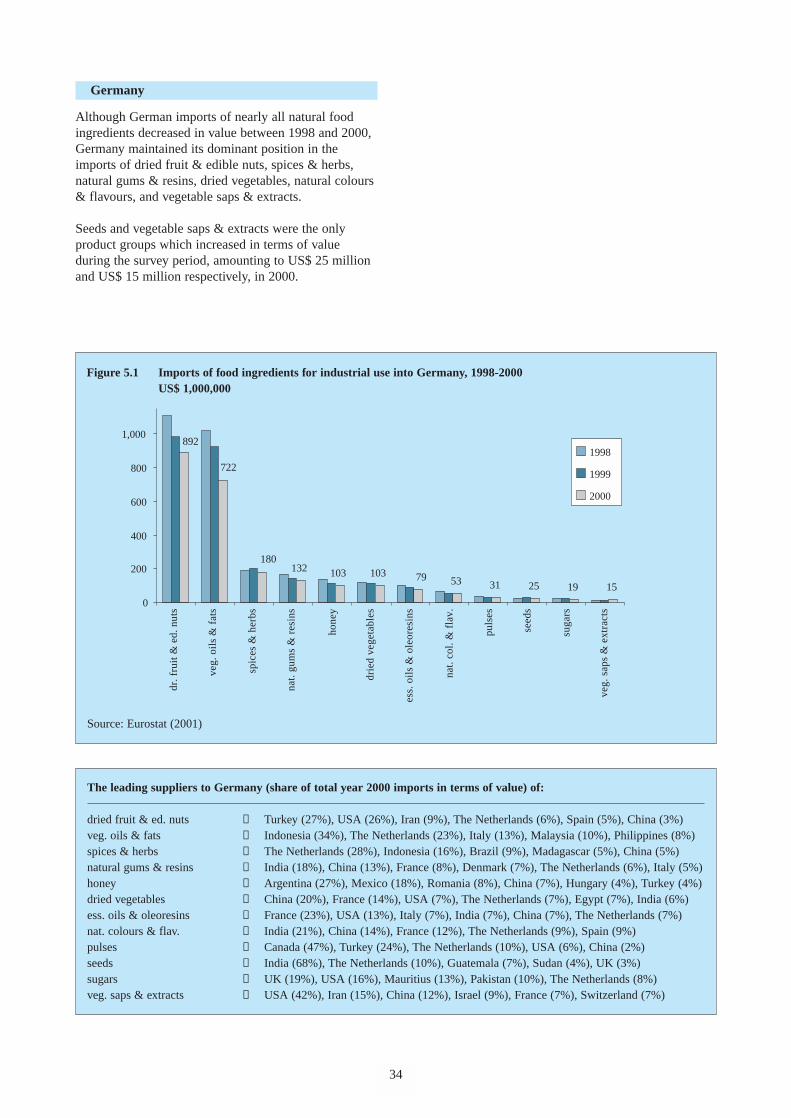

Germany

Germany’s consumers spend about US$ 196 billionannually on food and beverages. Of this amount, aboutone-third is spent in restaurants, canteens and otherplaces where food and beverages are served.The remaining two-thirds is spent in retail food andbeverage outlets, e.g., supermarkets. In 1998, Germany’sfood and beverage retailers registered annual sales ofabout US$ 135 billion. The country represents the largestretail food market in Europe. Nominal growth in salesremains relatively flat, with food/beverage sales growingonly about 2 percent annually over the 1993-98 period.Taking into account retail price inflation, real growth insales over this period was about zero.

The German market for most nuts and dried fruit isfairly stable throughout the year but sales generallypeak during the run up to the Christmas season. Importsare generally in-bulk and often used as ingredients bythe German food-processing industry. Germany is alsoa leading important importer of spices and herbs andhoney.

United Kingdom

The grocery trade is the largest sector in the UK foodretailing industry. In 1998, large businesses involvedpredominantly in food retail (including supermarketsand superstores) accounted for almost 80 percent of thefood market, with sales of US$ 114 billion (€ 102billion). In 1999, it was estimated that the largebusinesses saw grocery sales of US$ 121 billion (€ 114billion), with total grocery sales reaching US$ 149billion (€ 141 billion).

16

The leading players operating in the food ingredientsindustry in the UK have been experiencing a sharpdecline in profits following a moderate fall in salesduring the last full accounting years, 1998-2001.During the three-year financial period, the averageleading food ingredients company saw an average salesresult of minus 5 percent and an average profit result ofminus 19 percent.

The UK market has a relatively large interest in ethnicproducts due to the large Indian/Pakistani population.

France

Foreign cuisine and food products are booming inFrance’s dynamic market for consumer-ready and highvalue foods. Potentially lucrative opportunities exist fora number of niche products. Products with the bestprospects include fish and seafood; tropical fruits andnuts; beverages, including wines and spirits; innovativedietetic/health and organic foods; and any prepared ornon-prepared ethnic foods with a regional image.Hyper/supermarkets and city centre stores account for75 percent of total food retail sales in France.

Table 3.3 Total retail food and beverage sales inFrance, 1997-1999 (in billion $)

1997 1998 1999 1999US$ US$ US$ €

Food and beverages 103.4 106.3 107.5 101.4Of which food 96.1 98.8 100.0 94.3

Source: INSEE (National Institute for Statistics andEconomic Studies)

The Netherlands

Like in other EU countries, Netherlands eating habitsare changing. Consumers are demanding more safe andhealthy foods, more convenience, more fresh foods,a greater variety and more specialty food items.

The private label market in The Netherlands showssignificant signs of growth in the future, withconsumers asking supermarkets to provide a widervariety of private label products, to introduce higherquality goods into the market and offer more value formoney. Private labels are especially high in milk, meals,eggs and biscuits.

Italy

Consumers now pay more attention to spot sales(such as “two for the price of one”) and they are alsoturning their attention toward more healthy eating.For example, poultry consumption is gaining over beef;frozen foods are advancing in popularity more thancanned; mineral water and juices are more popularthan hard liquors; etc.. New or ongoing trends in Italianfood consumption include:• a desire for genuine, natural and fresh products; • growing demand for light or dietetic products; • increased importance of breakfast and snacking in

people’s diet; • increasing emphasis on time-saving meals, although

not to the extent that quality is sacrificed; • emergence of a new, educated consumer who wants

more nutritional information and more services, etc.

The success of snack foods in Italy is due to moderndistribution and marketing strategies. Teenagers are stillfairly health conscious or at least under the influence ofthe traditional Italian diet. However, the mass media hashad a tremendous impact on snack food consumption inItaly and products such as popcorn, soft drinks, sportsdrinks, single serving ice cream bars, etc. areincreasingly popular.

Despite a growing number of working women, Italy isbehind its EU counterparts in demand for conveniencefoods. Again, the strong influence of the traditionalMediterranean diet allows for marginal changes fromfresh to convenience foods, i.e. frozen vegetables andlasagne may be accepted, but a line of fully preparedmicrowave meals is still not found in Italian

17

supermarkets. Italian consumers are spending more toeat out, despite the difficult domestic economy.This is no doubt a “hard” trend that will consolidateand perhaps accelerate. For example, average annualgrowth in turnover for the hotel, restaurant andinstitutional sectors is forecast at 6 percent annuallyby FEDERALIMENTARE. The driving forces behindthe growth in this sector include modern life-styles(more working women, higher per capita incomes,increasing single member households, increasing urbanpopulation, etc.). In addition, the HRI sector itself haschanged and adapted to meet the needs of a broad crosssection of consumers.

After focussing on the food market in the selected EUcountries, the market for food ingredients in the EUcountries is also dealt with, and follows below.

Vegetable oils & fatsAs the trade in these products is business-to-businesstrade, there are no direct consumption figures availablefor these products. FAO, however, providesconsumption figures based on production + imports - exports + stock changes.

In 2000, EU vegetable oil consumption amounted tosome 13.8 million tonnes. The leading oils consumedinclude rape and mustard oil (22% of consumption),palm oil (18%), sunflower seed oil (15%), soyabean oil(12%). Industries use vegetable oils and fats asingredients for a whole variety of food and non-foodproducts, compound feed and industrial applications.To illustrate this, deliveries in The Netherlands to theprocessing industry (food, compound feed and industrial)show the following figures for 2000 (x 1,000 tons):

Table 3.4 Gainers in private label market share in the Netherlands, 1999 in percent of total volume

Product Volume Share Product Value Share

Sweeteners 9.1 Sweeteners 6,4Fruit drinks 6.6 Vegetables, herbs 3.1Snack bases 4.1 Chilled ready meals 2.5Milk/Buttermilk 2.8 Oils 2.5Chilled ready meals 2.6 Pasta 2.3Peanuts, nuts etc. 2.5 Peanuts, nuts etc. 2.1Dutch packaged cheese 2.5

Source: PMLA (2000)

Human consumption Compound feed Industrial

Volume 684 488 178% 50 40 10

In The Netherlands, eleven companies refine vegetableoils. The main end products are soy oil, palm oil, cocoafat and sunflower oil. Lecithin is an important semi-processed product. In 2000, 1.4 million tonnes ofvegetable and animal fats and oils were put on themarket. More than 80 percent is destined for humanconsumption. The market for these commodities is verycompetitive and large scale. Small and mediumexporters in developing countries will find moreopportunities in specialty vegetable oils (e.g.macadamia nut oil, brazil nut oil).

For more detailed information on the market forvegetable oils and fats, please refer to CBI’s EU MarketSurvey “Animal and Vegetable Oils and Fats forIndustrial Application”.

Dried fruits and edible nutsThe EU market for edible nuts increased, from 1.7million tonnes in 1998 to 1.8 million tonnes in 2000.Most EU countries increased their nut consumption andGermany and Italy were the leading treenut consumingcountries in 2000. EU consumption of groundnuts(peanuts) was some 450 thousand tonnes in 2000.The leading peanut consumers UK, Germany andThe Netherlands account for about two-thirds of EUconsumption.

Relatively cheap almond prices are favouring domesticconsumption, and, are, in some cases, causing substitutionfor other, more expensive nuts. Imported almonds aremostly consumed in northern Italy, while local almondsare more popular in the south, where Italian production is

18

concentrated. Walnut consumption (mainly in shell) istraditionally concentrated during the Christmas season,although sales of shelled walnuts, consumed either assnacks or as ingredients for the confectionery industry,have increased sharply in recent years.

At http://inc.treenuts.org one can find a global statisticalreview for a number of nuts.

SugarsThe exact consumption of sugar by the industries is notavailable. Therefore, the following is an attempt todescribe the end-user market for sugar in order to givethe reader a picture of the market.More than 100 countries produce sugar, approximately 72percent of which is produced from sugar cane growthprimarily in the tropical and sub-tropical zones of thesouthern hemisphere, with the balance produced from sugarbeet which is grown in the temperate zones of the northernhemisphere. Around 73 percent of the world’s sugar isconsumed in the country of origin while the balance istraded on world markets. Global sugar production for the2000-2001 season is estimated at 128 million tonnes withconsumption expected to be 130 million tons. The EU, withconsumption of 35 kg per capita, ranked fourth on the listof world consumers of sugar.

For more statistic information, please refer tohttp://www.illovo.co.za/default1.htm.

Spices and herbsThe EU market for spices and herbs increased from161 thousand tonnes in 1998 to 165 thousand tonnes

Table 3.5 Consumption of treenuts by EU member states, 1998-2000 in tonnes

1998 1999 2000

European Union 1,671,651 1,707,106 1,751,434Germany 357,418 360,000 382,861Italy 370,573 375,172 376,429Spain 257,045 291,012 275,533France 234,898 225,424 232,955Greece 99,266 105,098 106,435United Kingdom 84,317 89,753 95,960The Netherlands 83,691 65,255 80,047Belgium-Luxembourg 49,446 45,119 55,446Austria 48,581 48,584 49,885Portugal 35,188 51,858 46,200Denmark 19,991 19,502 23,083Sweden 22,898 21,855 17,186Finland 5,224 5,683 5,725Ireland 3,116 2,792 3,688

Source: FAO (2002)

in 2000, indicating an increase of almost 3 percent.The leading consuming country is Germany, closelyfollowed by the UK.

In almost all EU countries the largest proportion, being55-60 per cent of the total usage of spices and herbs,was consumed by the industrial sector. The retail sectorconsumed 35-40 per cent and the catering sector 10-15 per cent. In Sweden, The Netherlands and Italy

19

these proportions were respectively 55 per cent, 35 percent and around 10 per cent. In most markets, the ratiois moving towards higher relative usage by theindustrial sector, reflecting the growing popularity ofready-to-use spice mixtures. Another reason is theincreasing consumption of processed foods, which oftenrely on spices and herbs to retain and enhance the foodflavour.

Table 3.6 Consumption of sugar by EU countries, 1998-2000 tonnes

1998 1999 2000

European Union 14,499,983 14,504,843 14,362,443Germany 3,408,702 3,429,362 3,454,982France 2,386,671 2,423,950 2,388,986United Kingdom 2,285,974 2,184,541 2,106,348Italy 1,830,223 1,830,101 1,757,798Spain 1,213,450 1,236,749 1,242,996Netherlands 735,347 741,256 727,058Belgium-Luxembourg 552,973 536,499 556,746Sweden 412,441 411,353 412,701Austria 376,190 375,971 377,113Greece 346,343 344,325 345,005Portugal 325,558 344,431 342,816Denmark 267,892 263,407 265,139Finland 198,050 205,654 204,106Ireland 160,167 177,244 180,650

Source: FAO (2002)

Table 3.7 Consumption of spices by EU countries, 1998-2000 tonnes

1998 1999 2000

European Union 161,399 162,664 164,671Germany 38,310 42,101 44,174United Kingdom 32,372 32,647 34,655The Netherlands 20,801 20,113 25,013France 17,306 17,620 14,212Austria 7,019 5,921 6,870Belgium-Luxembourg 4,804 4,340 6,799Italy 5,459 6,627 6,528Spain 17,924 15,987 6,459Greece 3,399 4,050 5,535Sweden 4,337 4,503 4,873Denmark 4,803 4,296 3,295Ireland 1,288 2,093 2,325Portugal 2,015 1,604 2,132Finland 1,562 1,551 1,801

Source: FAO (2002)

For more detailed information on the market for spicesand herbs, please refer to CBI’s EU Market Survey“Spices and Herbs”.

Natural gums and resinsAccording to IMR International, the leading researchcentre in the food hydrocolloid industry, the recentglobal market for hydrocolloids values between US$ 3-3.5 billion (€ 3.3-3.8 billion). Included in thiscategory are seaweed extracts such as agar andcarrageenan; exudate gums such as gum arabic,tragacanth and karaya; seed gums including guar, locustbean and tara gum; fermentation gums such as xanthan;plant extracts and pectin; the synthetic hydrocolloids(carboxymethyl cellulose (CMC) and microcrystallinecellulose (MCC); the soluble hydrocolloidsmethylcellulose / hydroxypropylmethylcellulose(MC/HPMC)); modified starches; and animal proteinssuch as gelatine.

Hydrocolloids are used in the beverage, jam,confectionery, bakery and dairy industries where they actas emulsifiers, stabilisers, suspending agents,gelling agents, thickeners and mouth feel improvers.The ability to perform in this wide range of functions hasmade them particularly good in fat-replacement systems.There is no single “magic” ingredient/fat replacementproduct, and this has given way to a systems approach inwhich each ingredient supplier has its own products.Many food companies also experiment withcombinations of various hydrocolloids in their products.

The USA and the EU are the largest regional markets,each accounting for a little less than one-third(US$ 900-950 million, € 978-1,032 million) of theglobal market. Asia and Latin America are growingfaster than the USA and the EU. In general, the largestmarkets in Europe are, in order of importance,Germany, the United Kingdom, France and Italy.The total market in the rest of the EU is about as largeas the market in the United Kingdom. According toIMR International, the leading food hydrocolloids in theglobal market account for the shares presented below:

Starch is the leading food hydrocolloid, followed bygelatine. Market growth of starch is very low.Gelatine is the most popular animal-derived foodingredient available. However, awareness over healthissues related to meat and animal-derived products andalso genetically modified foods (GM), have led to anincreased demand for alternatives. Besides, gelatinereplacement is also desirable in order to meet Kosherand Halal food standards. Hydrocolloids which aresuitable for replacement are gelling and non-gellinggums like modified starches, carrageenans, pectin, agar-agar, alginates, guar gum, locust bean gum and xanthangum. The leading suppliers of most of these replacersare western countries. However, there are also minor

20

developing country producers which may takeadvantage of the change in the market.

Hydrocolloids coming primarily from developingcountries are gum arabic, guar gum, agar-agar.Occasional production ‘on the spot’ of carageenan canalso be found.

Essential oils and oleoresinsThe food industry has steadily increased its consumptionof essential oils over the past few years and this appearsto be the most promising sector for demand growth. Themain essential oils used are citrus fruit, mint and clove.The leading import markets for these products are TheNetherlands, the UK and France respectively. New foodand beverage products require strong flavour demand, forinstance in fashionable drinks.

There are varying estimates on the fragrance andflavour industry. According to the Dutch Association offragrance and flavour producers, global sales in 2000accounted for some US$ 7.5 billion, while Euromonitorvalues the market at US$ 11 billion. The leadingimporter of citrus fruit oil is The Netherlands as itcontrols the EU import through the ports of Rotterdamand Amsterdam.

PulsesThe most interesting product group for suppliers fromdeveloping countries concern speciality beans. Due tofood crises in Europe, people are eating less meat.Hence, people are looking for non-animal foods thatcan provide necessary proteins. Soybean is often usedas protein provider, but kidney beans, lima beans andchickpeas can also be used as replacers of meat.Often the beans are sold in preserved forms, in cans ordried. However, they are also used in ready chilli andTex Mex meals and by the feed and pet food industry.

In 2000, all EU countries together consumed about1.8 million tonnes of pulses. Italy accounted for27 percent of the total EU consumption, closelyfollowed by Spain with 23 percent market share.

Dried vegetablesDried vegetables are mainly consumed by the driedsoup industry. It uses most types of dried vegetables,especially potatoes, onions, tomatoes, leek, carrots andpeas. The soup industry in the EU is dominated by afew large multinational companies. These are UnileverBestfoods (Knorr, Unox), and Nestlé (Maggi).

There are no consumption data available for driedvegetables.

Please also refer to CBI’s EU Market Survey“Preserved Fruit and Vegetables for Industrial Use” formore information.

Natural colours and flavoursChr. Hansen, one of the leading food ingredientmanufacturers, estimates the European market fornatural colours in 2001 at US$ 350 million. This isabout a third of the total global colour market of US$ 1billion.

Consumers look for foodstuffs with a fresh andappealing colour, but fewer people want to eat or drinksomething which is coloured synthetically. The marketfor natural food colours has been steadily growing overrecent years.

Some natural food colours are being manufactured inpart from substances of natural origin which would notbe normally eaten. Annatto, for example, is an extractfrom the seeds of the Bixa orellana L. bush. Theseseeds, however, are not edible and the colour isextracted with organic solvents. Carmine is an extractobtained from the cochineal insect, precipitated withaluminium salts.

Because of this situation, there is a clear tendencytowards more genuine natural food colours andflavours. Manufacturers of genuine natural food coloursand flavours only use edible fruits, vegetables andplants as basic raw materials and they try to utilisemanufacturing processes that are as close to nature astechnically possible. Traditional raw materials used forproducing natural food colours are blue grapes,elderberries, hibiscus fruits or red cabbage. A broadvariety of raw materials is available for natural foodflavours; e.g. a natural strawberry flavour is notproduced from strawberries, but can be composed from

21

flavour components produced from various natural rawmaterials.

Recent years have seen a dramatic improvement instability and price-performance ratio. Even experts aresurprised at today’s favourable prices for natural foodcolours, although they are still more expensive thansynthetic ones.

In view of the favourable development of prices and thevisible trend towards natural raw materials andprocesses, it can be safely assumed that the market share“foods having colouring and flavouring properties” willincrease even further in the coming years.

HoneyTotal consumption of honey in the EU was estimated atabout 274 thousand tonnes in 2000. The average annualconsumption of honey per capita in the EU amounts toabout 0.7 kg. Consumption differs greatly between EUcountries. Per capita consumption in Austria is 1.8 kgand in Ireland 0.3 kg.

Table 3.8 Consumption of pulses by EU member states, 1998-2000 tonnes

1998 1999 2000

European Union 1,814,215 1,822,080 1,746,499Italy 478,748 467,620 478,019Spain 399,562 360,428 398,243United Kingdom 347,629 411,044 349,916France 155,182 166,241 164,671Germany 196,967 174,446 129,031Greece 66,931 71,109 72,624Portugal 55,442 49,168 50,696The Netherlands 48,714 49,600 31,702Belgium-Luxembourg 25,562 27,590 24,784Sweden 15,166 14,415 14,123Ireland 8,337 9,591 11,300Austria 4,163 8,369 7,884Finland 6,390 6,437 7,369Denmark 5,420 6,022 6,137

Source: FAO (2002)

Table 3.9 Honey consumption by EU countries, 20001,000 tonnes

consumption consumptionper capita

EU 274.3 0.7Germany 89.0 1.1France 40.0 0.7Spain 38.0 1.0UK 25.0 0.4Italy 21.0 0.4Greece 15.0 1.4Austria 14.4 1.8Portugal 11.9 1.2Belgium & Luxembourg 8.0 0.7The Netherlands 7.1 0.4Denmark 4.0 0.8Sweden 4.0 0.4Finland 2.9 0.6Ireland 1.2 0.3

Source: Apiservices (2002)

The honey market has two major sectors: one is honeyfor household consumption and the other is honey forindustrial use as a natural sweetener of bakery products,sweets etc.. While the market share of these two sectorsdiffers somewhat per EU country, it can be stated that,on average, 80 percent of honey is sold directly toconsumers, while about 20 percent goes to the industrialuser. The industrial market is sensitive to honey prices.The major substitutes for industrial honey are sugar,invert sugar syrup, corn syrup and high fructose cornsyrup (a cheap and versatile substitute for honey,

22

especially in products in which flavour is unimportant).

For more detailed information on the market for honey,please refer to CBI’s EU Market Survey “Honey andBeeswax”.

SeedsNo consumption figures are available for the productgroups included under seeds. Seeds are supplied to, andfurther processed by, the food industry. As the trade inthese products is business-to-business trade, there areno direct consumption figures available for theseproducts. However, FAO has published consumptionfigures for sesame seed, which are shown in Table 3.10.

EU consumption of sesame seeds showed an increasebetween 1998 and 2000, amounting to almost72 thousand tonnes in 2000. Greece, The Netherlandsand Germany are the leading consuming countries.

Vegetable saps and extractsNo consumption figures are available for the product groupsincluded under vegetable saps and extracts. The market forvegetable saps and extract overlaps the market for flavoursand colours. Therefore, one should refer to the text onflavours and colours for extra information.

3.2 Market segmentationThe market for natural food ingredients can generallybe segmented according to:

Major end-users• Beverage industry. The beverage industry is a major

user of flavours and colours. • Ready-meals industry. The ready-meals industry is a

significant end-user of ingredients.

Table 3.10 Consumption of sesame seeds by EU countries, 1998-2000 thousand tonnes

1998 1999 2000

Greece 20 12 19The Netherlands 9 10 16Germany 14 13 14UK 5 5 6Italy 4 4 5France 4 4 4Austria 1 1 2Spain 1 1 2Sweden 1 1 2Belgium/Luxembourg 1 1 1Denmark 2 2 1EU 62 54 72

Source: FAO (2002)

• Soup industry. The soup industry is the largest end-user of dried vegetables. Preserved mushrooms arealso used by this industry. The main products arepacket soups (dried) including soup bases, instantsoups (dried), canned soups and, to some extent,frozen soups.

• Breakfast cereal industry. The breakfast cerealindustry uses nuts and dried fruits in its productionof cereals, and muesli.

• Other food industries. Several other food industriesutilise ingredients in one way or another.These include the pet food, confectionery (candy andcereal bars), bakery and baby food industries.

Vegetable oils & fatsThe following table gives a short description of theapplication of selected vegetable oils in the food industry.

Product Application

Palm oil Margarine, ice-cream, confectionery,filled milk, salad oil, cooking, frying

Palm kernel oil Confectionery, bakery, imitation dairyproducts

Olive oil salad oil, cooking, dietetic food, healthfood

Coconut oil Cooking, margarine, shorteningsconfectionery, bakery, filled milk,coatings

Groundnut oil Deep frying, pan frying, margarine,shortenings, salad oil, salad dressing

Cocoa butter Chocolate industry, confectionery,bakery, dairy products, coatings

For more detailed information, please refer to CBI’s EUMarket Survey “Animal and Vegetable Oils and Fats forIndustrial Application”.

Dried fruits and nutsDried fruits are relevant to the following industries:• Confectionery and chocolate industry: chocolate

bars, health and fruit/nut/cereal bars, nougat• Breakfast cereal industry: varied dried fruit are used

in muesli, cereal bars. New variations of muesli, liketropical or exotic muesli and muesli snacks and thecontinuing development of new mixes, crunches andhealthy snacks are increasing the usage of apple,banana chips/flakes, dates, papaya, mango, guavaand a variety of nuts as ingredients.

Luxury nuts have grown in popularity in all sectors and,in the consumer market, nut packers have successfullymarketed newly developed mixtures. These are enjoyedas luxury snacks and are increasingly used as aningredient in exotic French or Chinese dishes (e.g.Chinese chicken with cashew nuts). Luxury nuts are

23

also becoming popular as a tasty and healthy substitutefor meat. Nuts are also used in recipes for salads,especially combined with pine nuts, walnuts, almonds,pepitas, and other seeds or with croutons (small piecesof toast). New varieties of salad dressings used inFrench, Italian, Asian and Mexican cuisine are enjoyed.This has given the grinder and processor an opportunityto introduce ready-to-use “salad kits” consisting of nuts,seeds and dried fruit. These ready-to-use kits and nutoils used for stir-fry meals have become very popular.Luxury nuts are also eaten with cheese after a specialdinner. More consumers also recognise the health valueof luxury nuts, with their high nutrition and proteinlevels another factor, which is expected to increase thedemand for luxury nuts. Macadamia nuts, for example,contain 11 minerals, including magnesium, and arecholesterol-free.

SugarsSugars are used in the manufacture of soft drinks,bakery products, confections and ice cream. Sugars areconsidered an essential ingredient of most of theproducts of the fruit canning industry. They act aspreservatives and maintain desirable appearance,flavour, colour and body in the products.

Spices and herbsSpices are used particularly in the processing of meat,fish, canned products, sauces, soups, bakery goods andother prepared and convenience food. In most cases, themeat industry is by far the largest user of a wide rangeof spices. Other sectors, like the drink industry, useanise, badian and juniper in alcoholic drinks andliqueurs and use ginger in soft drinks. Ginger is alsoused in biscuits and pickles. Pepper and mustard areused in most savoury products and sauces, while mint isused in confectionery and tooth paste.

Industrial food processing also includes spice mixingfor meat factories, butchers, bakers and packers for thecatering sector. Grinders and blenders tend to makemore multifunctional mixes, to be used especially in thebaking and meat processing industries.

For more detailed information, please refer to CBI’s EUMarket Survey “Spices and Herbs”.

Natural gums and resinsGums and resins are used in the beverages, jam,confectionery, bakery and dairy industries where they actas emulsifiers, stabilisers, suspending agents,gelling agents, thickeners and mouth feel improvers. Theability to perform in this wide range of functions hadmade them particularly good in fat-replacement systems.

Essential oils and oleoresinsThe kind of oil and the quality of the oil determine inwhat kind of final product essential oils and oleoresins

are processed. Essential oils and oleoresins are used asbasic raw materials in flavouring. They are used in thepreparation of food products and beverages,pharmaceutical/medicinal preparations, as well aspersonal care and household products (such ascosmetics, toiletries, and cleaning preparations).They are used in medicinal products to add taste orsmell or to suppress the less desirable medicatedflavour. The table below gives an overview of theutilisation of essential oils by the food industry.

Food industry Essential oils and oleoresins

Soft drink • CitrusConfectionery • Spice oleoresinsTobacco • VanillaCandy • Flavour and floral oilsProcessed and canned food products • Oleoresins

Oleoresins are also used for colouring purposes, e.g.paprika, turmeric. Although oleoresins are normallythick, viscous and sometimes highly coloured products,they generally give less colour to the finished productthan the corresponding spices, because they are used insuch small quantities. The flavour of oleoresins may notbe fully equivalent to their corresponding essential oils.The normal use range of oleoresins in food is 1/5 to1/20 of their corresponding dry spices. In general, theoleoresins offer the flavourist many advantages.

PulsesPulses are a relatively new source for food ingredients.Dried beans and peas (legumes) are very valuable andinexpensive sources of food. They are rich in proteinand in complex carbohydrate with various types ofdietary fibre as well as lots of vitamins and minerals.They are easily stored and retain nutritional valuethrough storage and cooking. Beans and pulses are usedto make many dishes varying from hummus (Middle-East chickpeas soup) to minestrone soup.

Dried vegetablesAs mentioned earlier, dried vegetables are mainlyconsumed by the dried soup industry. This industry inthe EU is dominated by a few large multinationalcompanies. These are Unilever Bestfood (Knorr, Unox),and Nestlé (Maggi). The ready-meals industry is also asignificant end-user of dried vegetables (mainly forpizzas and pasta dishes).

For more information please refer to CBI’s EU MarketSurvey “Preserved Fruit and Vegetable for IndustrialUse”.

24

Food colours and flavouringNatural food colours have many different applications.The main product sectors, in order of importance are:• dairy• savoury/bakery• soft drinks• confectionery• beverages

Natural food flavours also have many different sectorsof application including, in order of importance:• soft drinks• dairy• savoury/bakery• confectionery• beverages

HoneyIndustrial honey is mainly used in the bakery,confectionery and cereal industries. Other industriesusing this honey include manufacturers of baby food,sauces, tobacco and pharmaceutical products. It is alsoused for curing meat and in the production of honey-roasted nuts.

Table honey is used mainly as spread on bread, andsome is used as a natural sweetener for drinks such astea or milk. Consumers of organic and health foods,who are generally customers of the specialist healthfood stores, mainly use honey as a natural nutritiousalternative to sugar and for the flavouring of cooking.It goes with nearly all foods, from salad dressings tovegetable and meat glazes to casserole dishes.It is especially good in desserts and baked goods.The moisture-absorbing quality of honey helps breads,cakes, cookies and candies stay fresh longer.Honey wine can be served with or following dinner,and several after-dinner liqueurs include honey.

Honey remains a popular ingredient in both theindustrial and food service sectors. It is positioned as anatural and healthy extra, for example, in breakfastcereals. As consumer interest in health foods increases,light, low-fat and vitamin-enriched products arefeaturing in markets for natural products containinghealth food. For more information, please refer to CBI’sEU Market Survey “Honey and Beeswax”.

SeedsThe market can be divided into segments according tothe type of destination and consumer of the seeds:• processing industry / crushers• animal feed industry• human consumption• oil seeds used for sowing

The major part of the seeds is processed for oil, and themeal produced is utilised in animal feedstuff

compounds. The major exception is palm nuts, wherekernels in food snacks and confectionery account forthe major part of the market.

Sesame seeds are supplied to markets in NorthAmerica, Europe, and East Asia by countries in Africa,Latin America, and South Asia. Cooking oil can beextracted from sesame seeds, and this is their main use,especially in Asia. In North America and Europe,raw sesame seeds are generally used for toppings onbreads such as hamburger buns, bagels, bread sticks,and other baked goods. Restaurants and natural foodstore customers purchase sesame seeds for use in ethnicdishes. Middle Eastern countries use sesame seeds fortahini paste and halvah, as well as for oil.

Shea nut products, the solid fat (butter or stearin) andthe liquid oil (olein), are ideal for use as raw materialsin cooking oil, margarine, cosmetics, soap, detergentsand candles, but it has found its primary market nicheas a substitute for cocoa butter in the chocolate andconfectionery industry.

Vegetable saps and extractsVegetable saps and extracts can be used as colours andflavours in beverages and candies, as a raw material forthe flavour industry, and for medical and health foodsupplements. For more applications please also refer tothe text on flavours and colours.

Organic and conventional productionThe market for food ingredients for industrial use can alsobe segmented according to whether the products aregrown by organic1 farming or by conventional farming.This is particularly important, since the demand fororganic food is booming in several EU member countriesand these can offer interesting market opportunities fordeveloping countries exporters. Organic products stillaccount for a small share of the total food consumption,varying from approx. 1% in France, Sweden, Italy,Belgium, The Netherlands up to 2.7% in Denmark,although the market for organic products experiencesstrong growth rates. Sweden, The Netherlands and theUnited Kingdom are the major growth markets, withexpected annual growth rates of over 20 percent. Becauseof its nature, organic production is highly suitable forsmall and medium-sized farmers working in areas whichmay not be suitable for large-scale food production. Driedfruits like apricots, bananas and pineapple are importantorganic products within the segment dried fruits and nuts.For more information on organic production and itscertification, please contact SKAL, Ecocert, SoilAssociation and other EU inspection organisations orconsultancy organisations like Agro Eco. Please refer toAppendix 9 for contact details of these organisations.Please also refer to CBI’s EU Market Survey “OrganicFood Products” for more detailed information.

25

3.3 Consumption patterns and trendsThe population in Western Europe is still growing andwill continue to grow until about 20 years from now.It is estimated that thereafter, Western Europe will startto show a declining population size. However, alreadynow the composition of the population is changing.It shows a rapidly growing proportion of elderly peoplecombined with a decreasing proportion of youngpeople. We also see a family ‘dilution’; familyhouseholds are getting smaller because people arehaving fewer children. Moreover, the number of singlehouseholds in Western Europe is substantial and stillincreasing, making these people a highly significantconsumer group for food suppliers.

Thanks to increased prosperity in the EU, eatingbehaviour is related to income and life style. Despitethis increase in prosperity, the food market in the EU ishighly competitive, since consumers are not going toeat more, but will only, at the very most, switch to otherproducts.

Recent research into consumer behaviour shows thattoday’s consumer has the following preferencesconcerning food and nutrition:

Safe foodFood products should be safe to human helth and eatingthem should not result in any danger or risk.

Healthy foodHealthy food refers to food products which are low infat and have limited sugar and salt content; this includesfunctional foods, which have specific health-promotingproperties and food products with added vitamins andminerals or bacteria supporting the intestinal function.

Organic foodSince European consumers have recently experiencedseveral food scares, many people are concerned aboutthe safety of food, as well as the effects of intensive

1 The Basic Standards of IFOAM (InternationalFederation of Organic Agriculture Movements)represent the world-wide consensus of what isorganic. The EU Regulation for organic food isbased on the IFOAM standards. Uniform standardsfor organic food production and labellingthroughout the EU were established by the passingof Council Regulation (EEC) 2092/91.This regulation and subsequent amendmentsestablish the main principles for organic productionat farm level and the rules that must be followed forthe processing, sale and import of organic productsfrom third (non-EU) countries (see also Section1.1.3 of the EU Strategic Marketing Guides“Preserved Fruit and Vegetables for IndustrialUse” and “Organic Food Products”).

farming on the countryside and on the environment ingeneral. These factors, combined with the increasingawareness of the importance of diet and nutrition, haveintensified interest in organic foods, which are grownaccording to principles laid down in Directive EC2092/91 (see Section 1.1.1) of the EU StrategicMarketing Guide “Food ingredients for industrial use”).Simply said, it means that products are grown withoutthe use of artificial (chemical) fertilisers and pesticides.The demand for organic food is booming in several EUmember countries. This can offer interesting marketopportunities for exporters in developing countries,where often the major part of agricultural produce isanyway organic although not certified (‘organic bydefault’). Certification by a EU accredited certifyingbody (including regular inspections) is necessary.Organic products still only account for a small share ofthe total food consumption, although the market fororganic products experiences strong growth rates.Sweden, The Netherlands and the United Kingdom arethe major growth markets, with expected annual growthrates of over 20 percent.

More information on the above can be found in CBI’sEU Market Survey “Organic Food Products”.

Fruit and vegetablesThere is a growing interest in the consumption of fruitand vegetables in the West European food market.This is caused by the fact that fruit and vegetablescontain vitamins and natural antioxidants, which aresupposed to have properties preventive to heart diseasesand cancer.

Environment-consciousnessFood production, especially primary growing, should beenvironment-friendly (organic, see above). Waste,including packaging waste, should be avoided or atleast reduced. In the scope of the increasingenvironment-consciousness in the EU, a group ofleading European food retailers launched the EurepGapProtocol in 1999. For more information on the EurepGroup and EurepGap Protocol, please refer towww.eurep.org.

ConvenienceEuropean people (including women) are working moreand more in jobs outside their home and have busysocial lives. Moreover, the number of single householdsincreases. As a result, less time is left for thepreparation of a full meal. Therefore, West Europeanconsumers have a growing need for convenience meals,spurring the demand for peeled potatoes, canned soup,preserved vegetables, prefried fries, fish sticks, pizza,frozen pastry, ready meals (frozen, chilled or shelf-stable).

26

VarietyVariety in food consumption has increased as a result ofthe promotion by the food industry of ingredientmixtures (spices) and sauce mixes with distinctiveethnic flavours. Due to the sales of ingredient mixtures,consumers do not have to purchase or be familiar withthe individual spices required for a particular dish,nor is lengthy preparation time involved. Ethnic cuisineis becoming more mainstream and increasinglyfragmented into more regional variants.

‘Grazing’The modern consumer does not confine himself to thetraditional three meals a day (breakfast, lunch anddinner), but is eating smaller bites at more frequentintervals: ready-to-eat products or products requiringvery little ultimate preparation: take-out foods,hamburgers, mini-pizzas, instant soups, filledcroissants, candy bars, muesli bars, cheese sticks andfruit yoghurts. Restaurant quality is becoming thebenchmark for the growing ranges of added-valueprepared food offerings.

Tracking and tracingAs a result of several food scares (BSE, dioxine)consumers increasingly pose questions on theproduction process and demand open, honest, andinformative labelling. This has resulted in a discussionin the fruit and vegetable processing industry about“tracking and tracing”. With the help of good chainmanagement and control within the chain, retail outletsare able to supervise all kinds of aspects of fresh fruitand vegetables and products derived from them, such asplant material, growth, harvest, storage, distribution andprocessing. The fruit and vegetable processing industryis increasingly paying attention to chain managementand labelling systems, through which products can betraced back to the producer.

Tracking and tracing will become obligatory in the EU,as well as for all exporters to the EU in the near future,according to the EU Regulation (EC) 178/2002, alsocalled ‘General Food Law’.

InternationalisationAs the world is increasingly turning into a globalvillage, culinary traditions from other continents tend tobe more widely accepted by European consumers,thereby increasing the demand for ethnic and exoticingredients. This development is also stimulated by thesteady population growth of ethnic minority groupswhich have significantly increased their purchasingpower over the last years. Many products containingexotic fruits (like fruit juice drinks, jams, ice cream) aremanufactured by European food industries fromingredients that are imported as semi-manufacturedproducts (fruit juice concentrate).