12

European Energy Union Impact on the Refining & Petrochemical Business John Cooper, Director General Budapest, 13th October 2015

European Energy Union

Impact on the Refining & Petrochemical Business

John Cooper, Director General Budapest, 13th October 2015

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

Page 2

FuelsEurope represents 42 Member Companies ≈ 100% of EU Refining

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

• Imports, shutdowns and investments

• EU Refineries: competitive analysis

• Energy Union

• Conclusions

AGENDA

Page 3

“IMPORTANCE AND CHALLENGES OF OIL REFINING IN EUROPE”John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

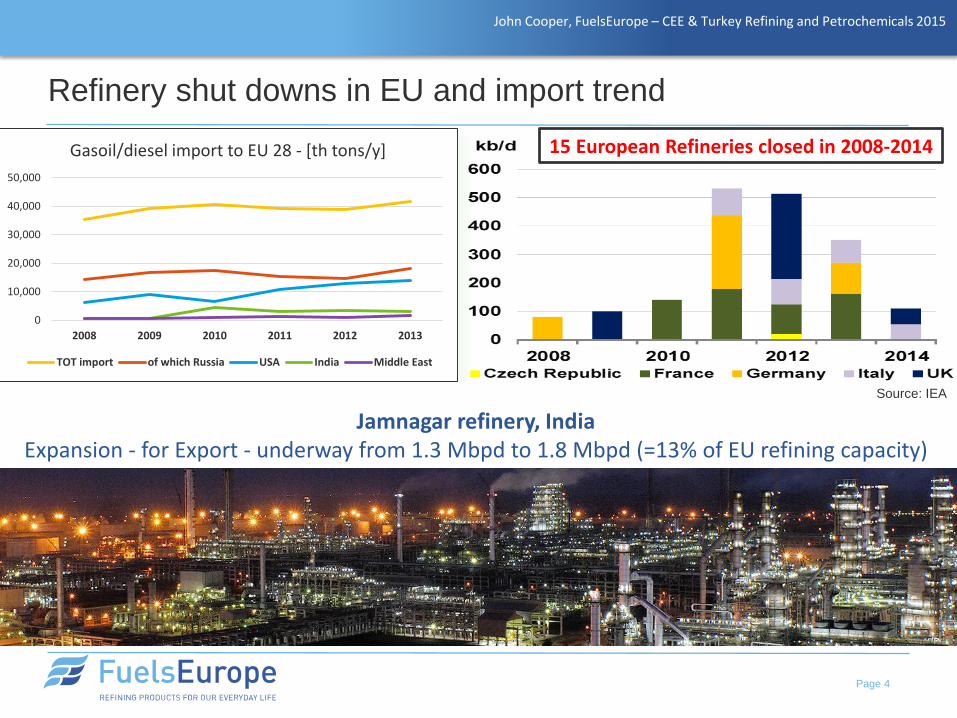

Jamnagar refinery, IndiaExpansion - for Export - underway from 1.3 Mbpd to 1.8 Mbpd (=13% of EU refining capacity)

Refinery shut downs in EU and import trend

Page 4

Source: IEA

0

10,000

20,000

30,000

40,000

50,000

2008 2009 2010 2011 2012 2013

Gasoil/diesel import to EU 28 - [th tons/y]

TOT import of which Russia USA India Middle East

15 European Refineries closed in 2008-2014

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

Page 5

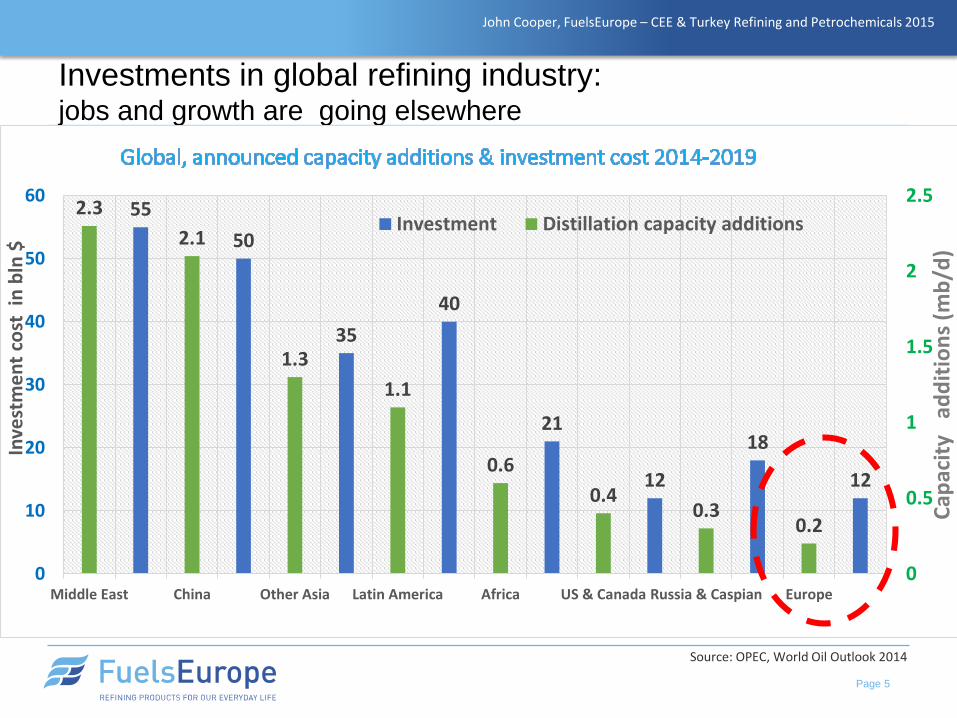

Source: OPEC, World Oil Outlook 2014

Investments in global refining industry: jobs and growth are going elsewhere

55

50

35

40

21

12

18

12

2.3

2.1

1.3

1.1

0.6

0.40.3

0.2

0

0.5

1

1.5

2

2.5

0

10

20

30

40

50

60

Middle East China Other Asia Latin America Africa US & Canada Russia & Caspian Europe

Cap

acit

yad

dit

ion

s (m

b/d

)

Inve

stm

en

t co

st i

n b

ln$

Investment Distillation capacity additions

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

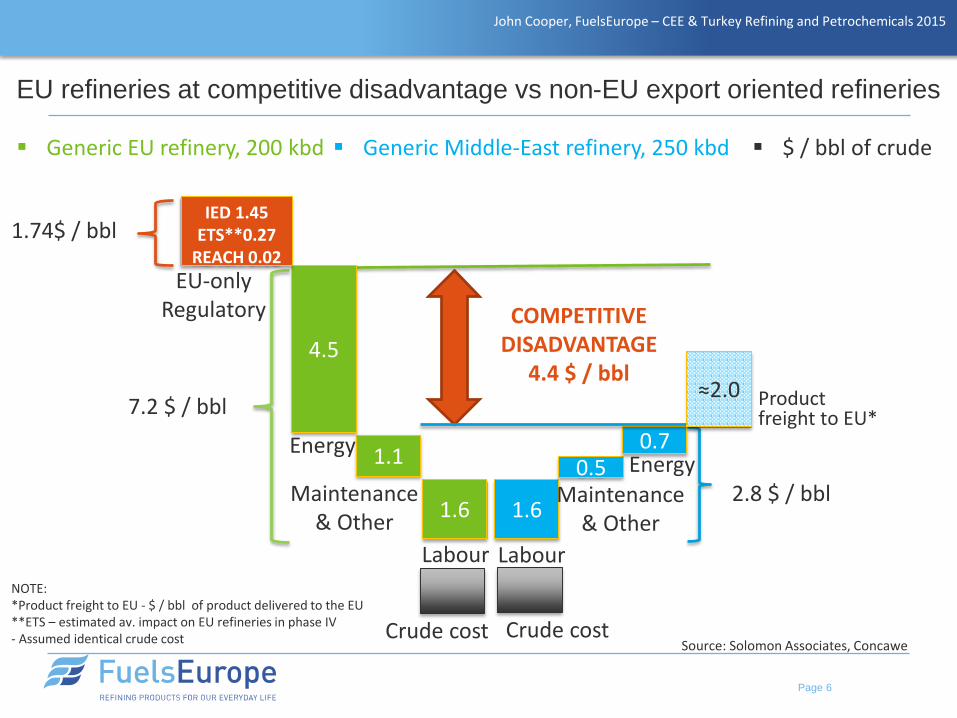

EU refineries at competitive disadvantage vs non-EU export oriented refineries

Page 6

Product freight to EU*

EU-only Regulatory

NOTE:*Product freight to EU - $ / bbl of product delivered to the EU**ETS – estimated av. impact on EU refineries in phase IV- Assumed identical crude cost

7.2 $ / bbl

2.8 $ / bbl

COMPETITIVE DISADVANTAGE

4.4 $ / bbl

Generic Middle-East refinery, 250 kbd $ / bbl of crude Generic EU refinery, 200 kbd

Source: Solomon Associates, Concawe

1.74$ / bbl

1.6

Labour

1.6

Labour

1.1

Maintenance & Other

4.5

Energy0.5

Maintenance& Other

0.7Energy

IED 1.45ETS**0.27

REACH 0.02

Crude cost Crude cost

≈2.0

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

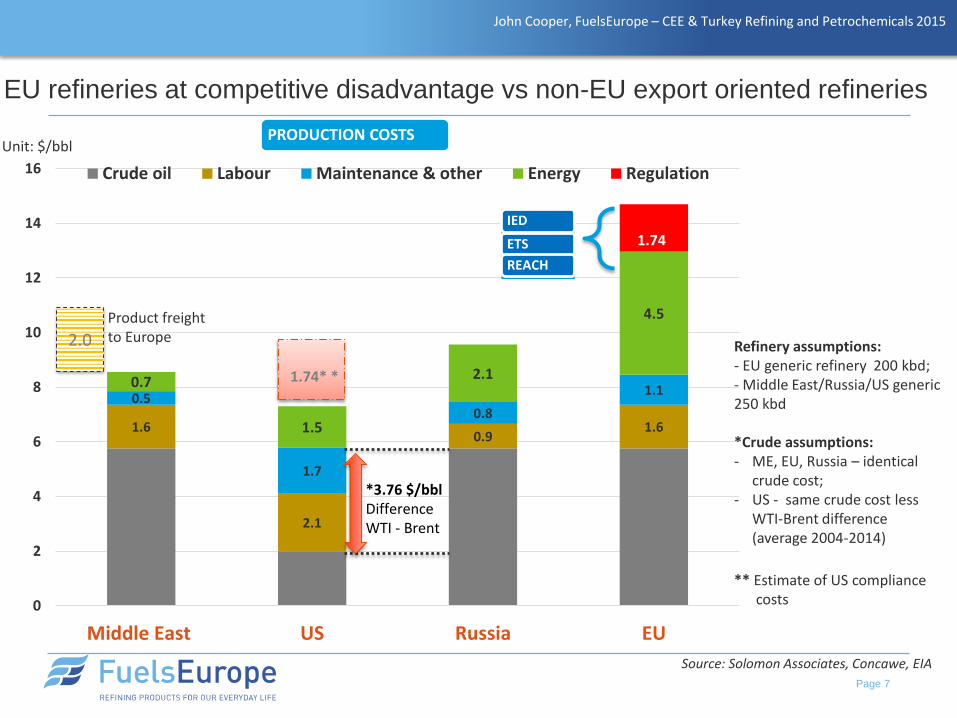

1.6

2.1

0.91.6

0.5

1.7

0.8

1.10.7

1.5

2.1

4.5

0

2

4

6

8

10

12

14

16

Middle East US Russia EU

Crude oil Labour Maintenance & other Energy Regulation

*3.76 $/bblDifference WTI - Brent

EU refineries at competitive disadvantage vs non-EU export oriented refineries

Page 7

Unit: $/bbl

Refinery assumptions: - EU generic refinery 200 kbd;- Middle East/Russia/US generic 250 kbd

*Crude assumptions: - ME, EU, Russia – identical

crude cost;- US - same crude cost less

WTI-Brent difference (average 2004-2014)

IED

ETS

REACH

Source: Solomon Associates, Concawe, EIA

2.0

PRODUCTION COSTS

1.74

1.74* *

** Estimate of US compliance costs

Product freight to Europe

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

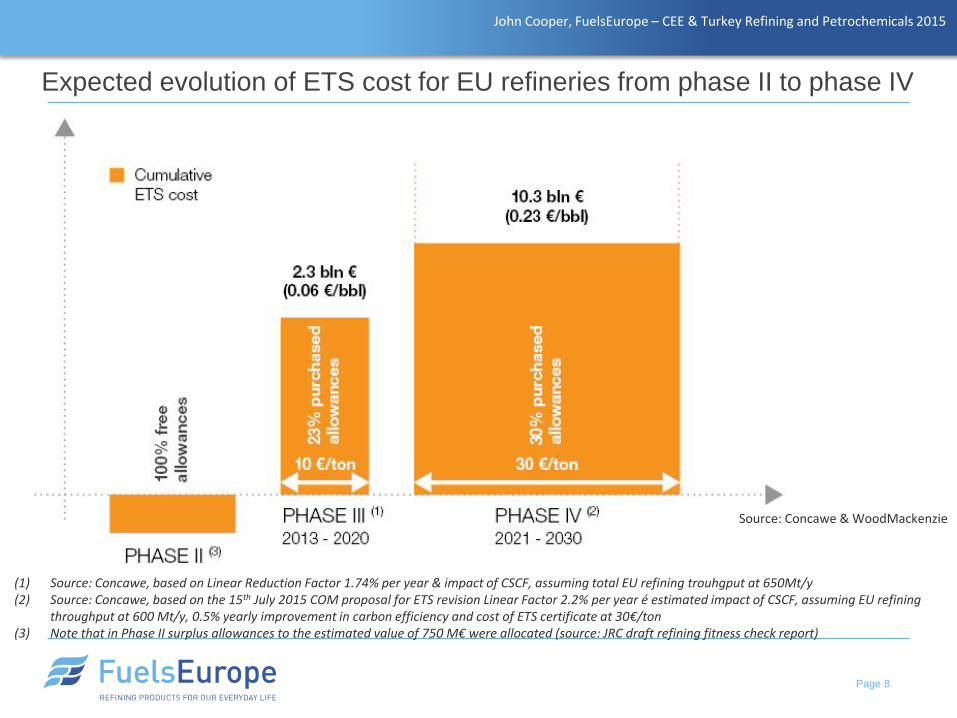

Expected evolution of ETS cost for EU refineries from phase II to phase IV

Page 8

Source: Concawe & WoodMackenzie

(1) Source: Concawe, based on Linear Reduction Factor 1.74% per year & impact of CSCF, assuming total EU refining trouhgput at 650Mt/y(2) Source: Concawe, based on the 15th July 2015 COM proposal for ETS revision Linear Factor 2.2% per year é estimated impact of CSCF, assuming EU refining

throughput at 600 Mt/y, 0.5% yearly improvement in carbon efficiency and cost of ETS certificate at 30€/ton(3) Note that in Phase II surplus allowances to the estimated value of 750 M€ were allocated (source: JRC draft refining fitness check report)

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

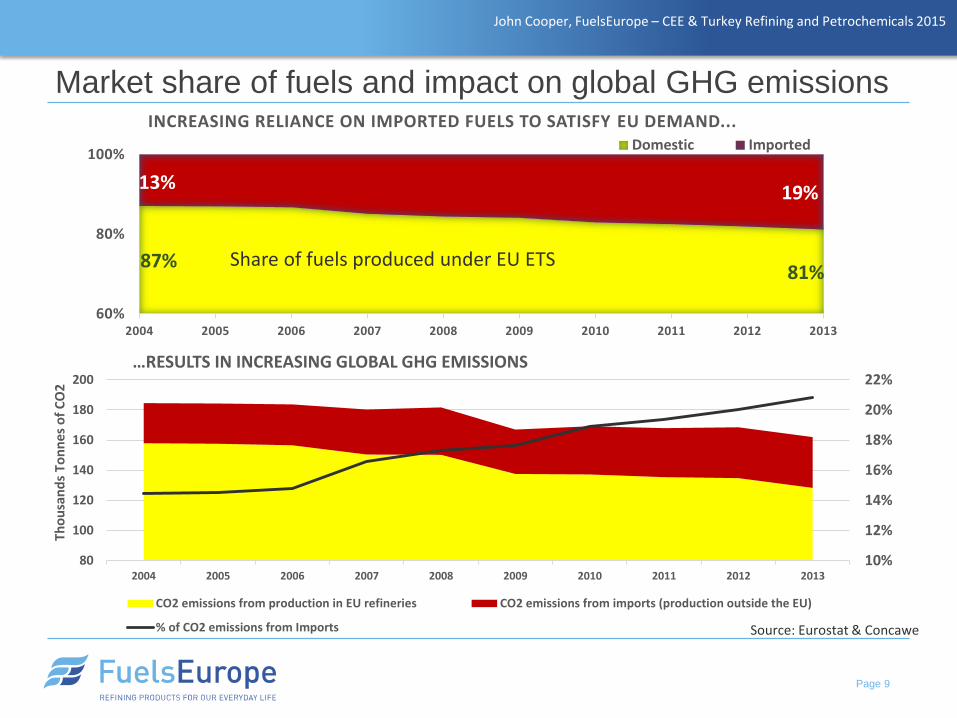

Market share of fuels and impact on global GHG emissions

Page 9

87%81%

13% 19%

60%

80%

100%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

INCREASING RELIANCE ON IMPORTED FUELS TO SATISFY EU DEMAND...Domestic Imported

10%

12%

14%

16%

18%

20%

22%

80

100

120

140

160

180

200

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Tho

usa

nd

s T

on

nes

of

CO

2

…RESULTS IN INCREASING GLOBAL GHG EMISSIONS

CO2 emissions from production in EU refineries CO2 emissions from imports (production outside the EU)

% of CO2 emissions from Imports

Share of fuels produced under EU ETS

Source: Eurostat & Concawe

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

The Energy Union Communication:

• Highlights the importance of open and free energy markets, but…

• Misses an essential focus on how this will deliver competitive energy thus

fostering growth with the ultimate objective of reversing the decline in industrial

value creation in Europe;

• Lacks recognition of the continued need and role of petroleum products in the EU

economy;

• Dismisses petroleum products and refining as involving ‘old technologies’

implying the use of low skilled labour, while the reality is exactly the opposite;

• Does not provide any information on the transition steps towards low carbon

economy. A balanced and economically realistic pathway needs to be developed,

which would provide a clear and consistent steps to bridge the gap between the

vision laid out and the current reality of energy use

Energy Union – an incomplete package?

John Cooper, FuelsEurope – CEE & Turkey Refining and Petrochemicals 2015

• Ambitious regulatory targets for EU refiners create the need for effective carbon leakage measures to prevent an increase in global emissions and the relocation of EU industry and jobs

EU Refining Competitiveness and Impact of Regulation - Conclusions

Page 11

• European refineries compete in a highly competitive global market for refined petroleum products

• High costs for energy & regulatory compliance create a significant

cost disadvantage versus export-oriented refineries outside of EU

• The increasing product import flow to the EU effectively means that

refinery GHG emissions are being exported outside of ETS – “carbon

leakage”

• Moreover, the non-EU refineries exporting to EU are likely to have

relatively higher GHG emissions, causing a net increase in global

emissions

• Current regulatory proposals for ETS Phase IV and Industrial Emissions will

further increase the cost burden on EU refiners

FuelsEurope

165, Boulevard du Souverain

1160 Brussels - Belgium

T: +32 2 566 91 00

www.fuelseurope.eu

This document was presented by

FuelsEurope

Contact:

![RABIGH REFINING AND PETROCHEMICAL ساسϸا ϢاظنϠا ......23/05/2017 10:35 [(1 قفرم).docx] RABIGH REFINING AND PETROCHEMICAL COMPANY (A Saudi Arabian Joint Stock Company)](https://static.documents.pub/doc/80x56/6093ddff78d40270c056c30b/rabigh-refining-and-petrochemical-23052017-1035.jpg)