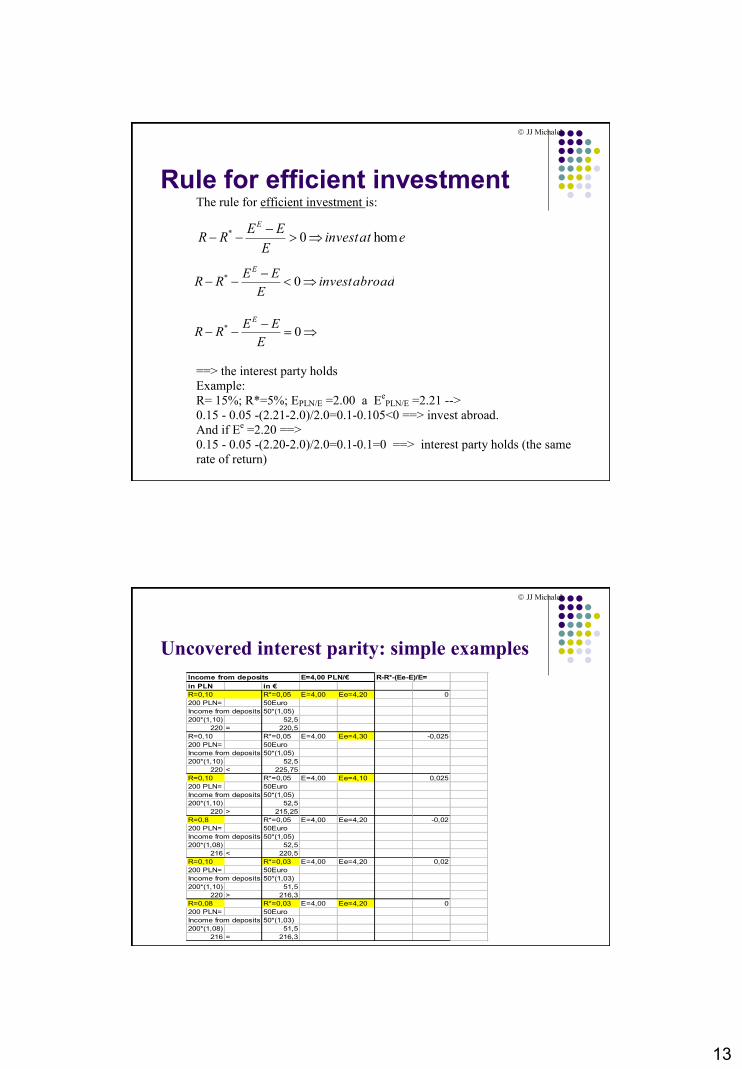

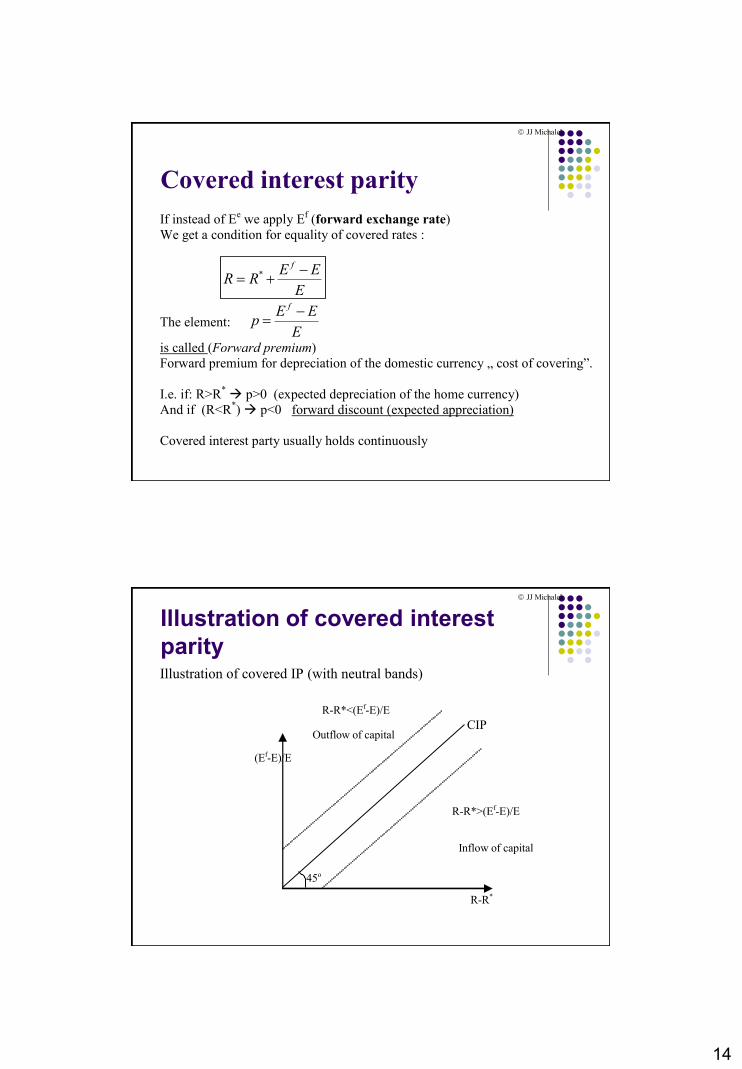

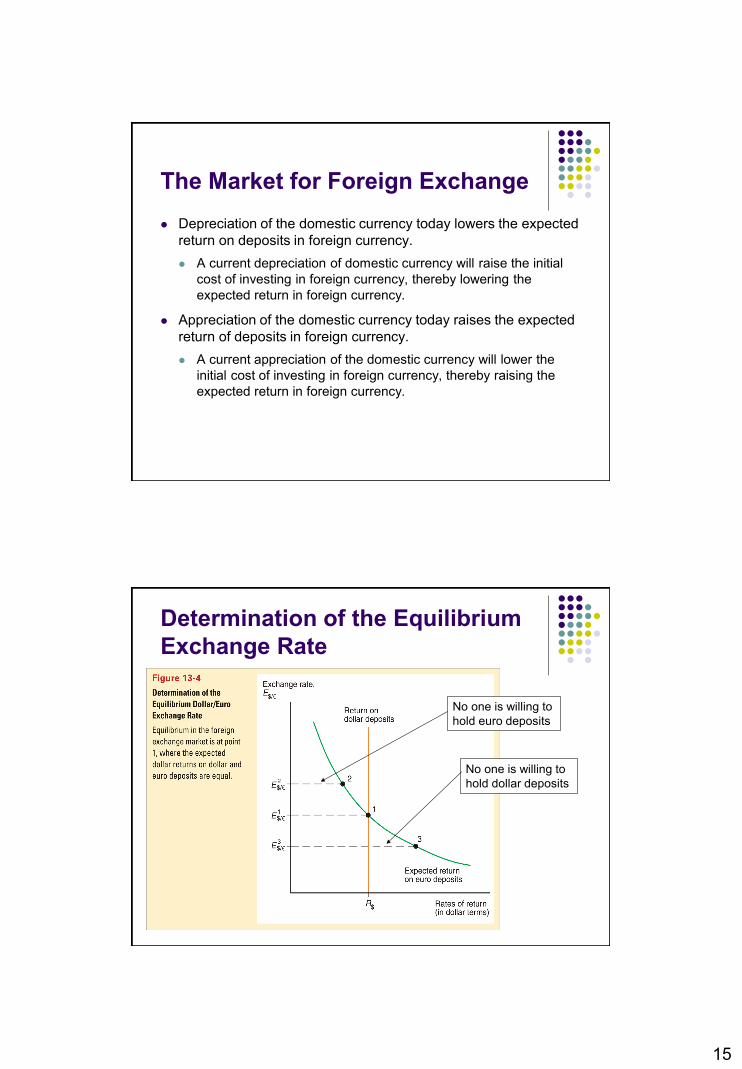

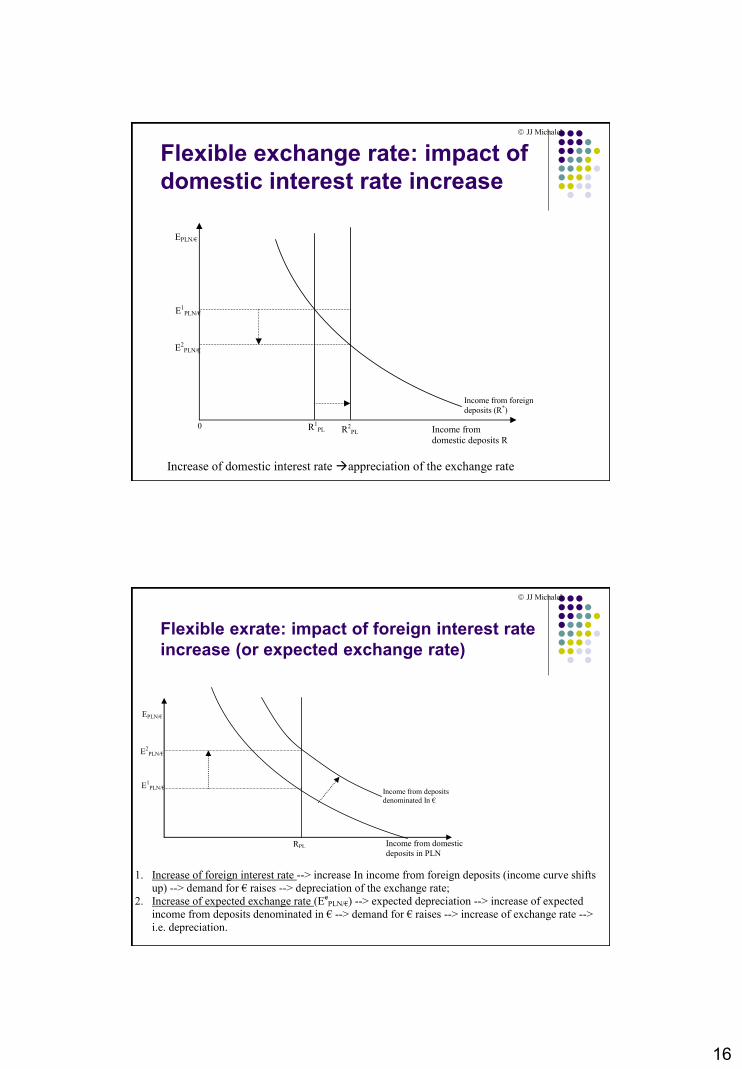

1 Exchange rate and interest parity Jan J. Michalek Exchange rate Exchange rate: the price of one currency expressed in another currency Definition: how many units of domestic currency are needed to buy one unit of foreign currency: e.g. 3,9 PLN/$ Changes in exchange rates: Fixed exchange rate: devaluation and revaluation Flexible exchange rates: depreciation and appreciation. JJ Michalek

Transcript

1

Exchange rate

and interest parity

Jan J. Michalek

Exchange rate

Exchange rate: the price of one currency expressed in another currency

Definition: how many units of domestic currency are needed to buy one unit of foreign currency: e.g. 3,9PLN/$

Changes in exchange rates:

Fixed exchange rate: devaluation and revaluation

Flexible exchange rates: depreciation and appreciation.

JJ Michalek

2

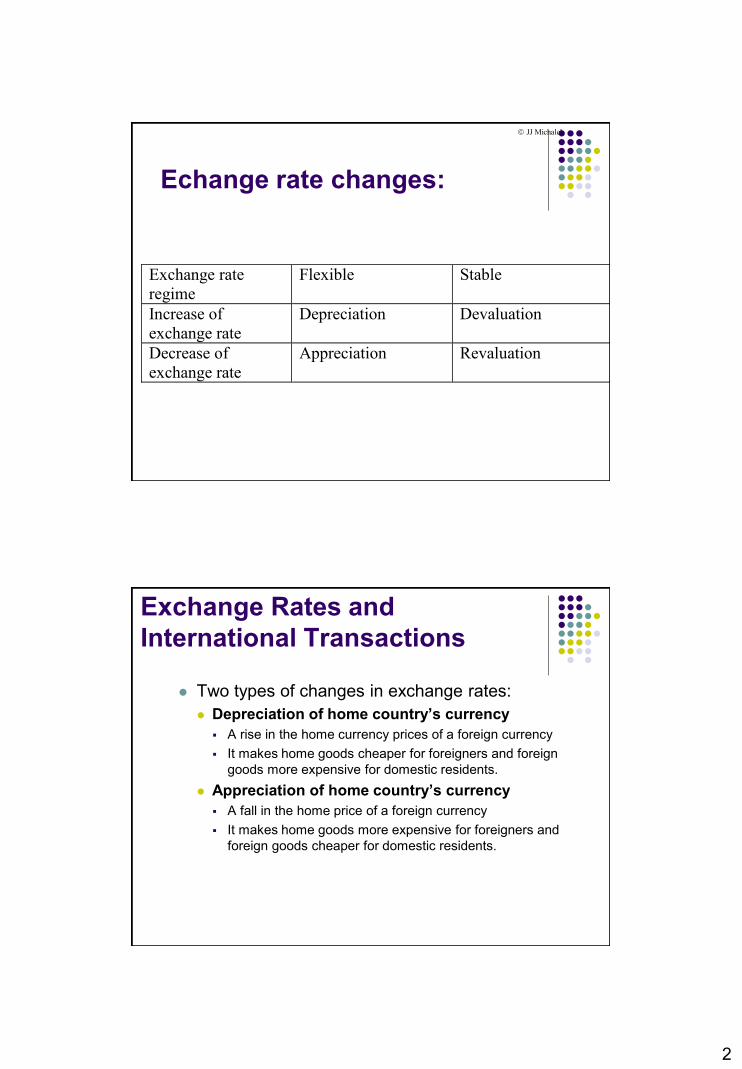

Echange rate changes:

Exchange rate

regime

Flexible Stable

Increase of

exchange rate

Depreciation Devaluation

Decrease of

exchange rate

Appreciation Revaluation

JJ Michalek

Two types of changes in exchange rates:

Depreciation of home country’s currency

A rise in the home currency prices of a foreign currency

It makes home goods cheaper for foreigners and foreign

goods more expensive for domestic residents.

Appreciation of home country’s currency

A fall in the home price of a foreign currency

It makes home goods more expensive for foreigners and

foreign goods cheaper for domestic residents.

Exchange Rates and

International Transactions

3

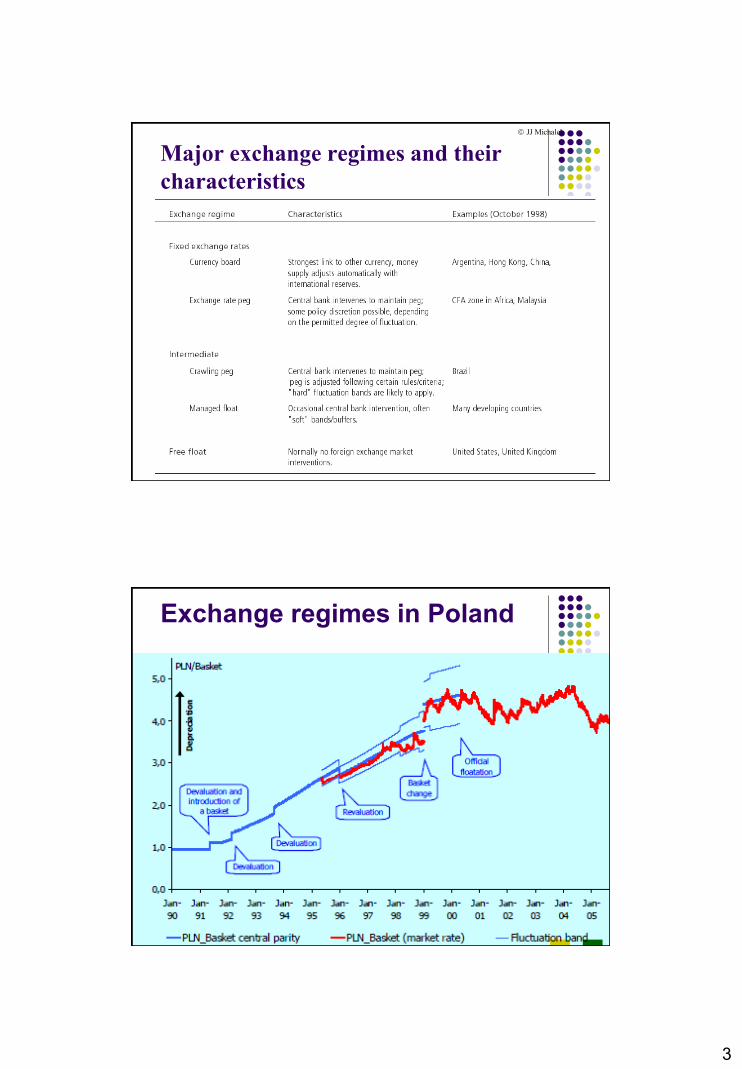

Major exchange regimes and their

characteristics

JJ Michalek

Exchange regimes in Poland

4

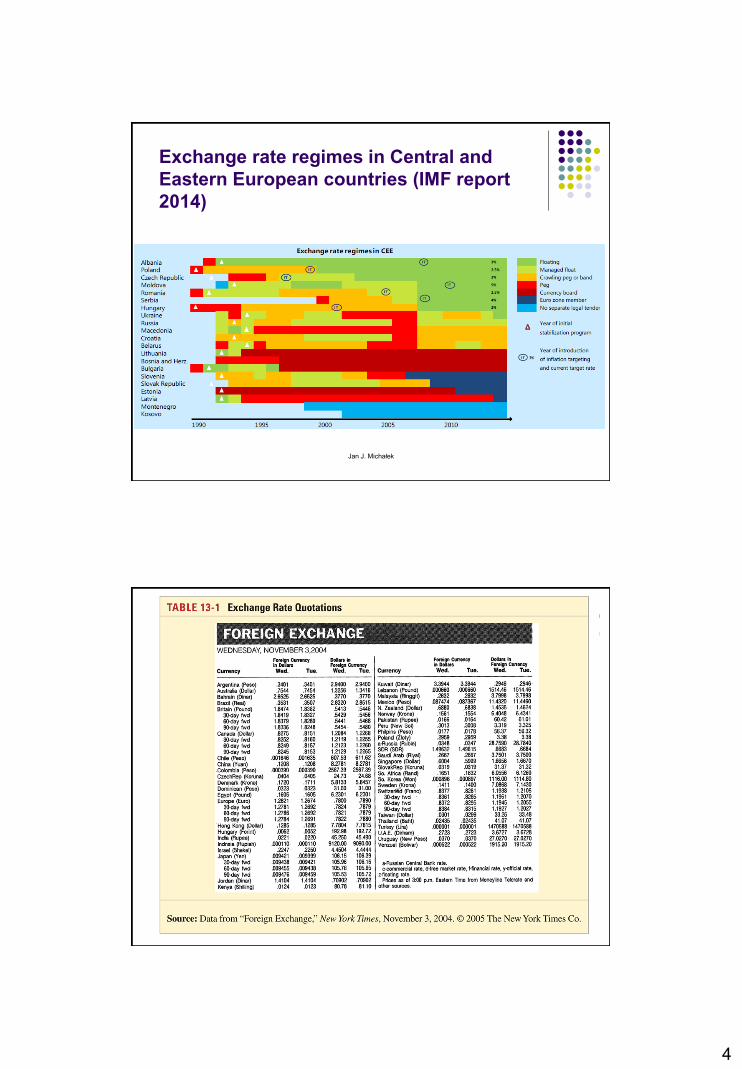

Exchange rate regimes in Central and

Eastern European countries (IMF report

2014)

Jan J. Michałek

5

Domestic and Foreign Prices

If we know the exchange rate between two

countries’ currencies, we can compute the price of

one country’s exports in terms of the other

country’s money.

Example: The dollar price of a £50 sweater with a

dollar exchange rate of $1.50 per pound is (1.50 $/£) x

(£50) = $75.

Exchange Rates and

International Transactions

Exchange rate: major world

actors

Size of the market:

For example: 1999:$1,7 trillion per day: $637 billion in London, $350 in New York, $150 billion in Tokyo.

Major actors and foreign exchange markets:

Commercial banks (interbank trading: retail operations less than $1 million, wholesale: above $1 million: more favorable rates: 90 percent of all foreign exchange rate transactions)

Multinational corporations;

Non bank financial institutions;

Central banks

Foreign exchange brokers.

JJ Michalek

6

Foreign exchange arbitrage

When banks or economic agents seek to earn benefit from discrepancies among exchange

rates prevailing simultaneously in different markets.

Example: the Exchange rate of dollar to pound sterling ES/Ł equals:

00,2NYE 20,2LE

With 100$

We can buy 50Ł in NY in exchange for $100

And sell 50Ł In London for: 50*2,20= $110

Immediate profit of 10 $ or 10% (very profitable)

Many transactions of this sort are done

Price of Ł raises (increased demand) in NY e.g. to 2,09

Price of Ł decreases (increased supply) In London e.g. to 2,11

A very small difference In Exchange rates between different foreign exchange markets

JJ Michalek

Spot Rates and Forward Rates

Spot rates are exchange rates for currency exchanges “on the spot”, or when trading is executed in the present.

Forward rates are exchange rates for currency exchanges that will occur at a future (“forward”) date.

forward dates are typically 30, 90, 180 or 360 days in the future.

rates are negotiated between individual institutions in the present, but the exchange occurs in the future.

7

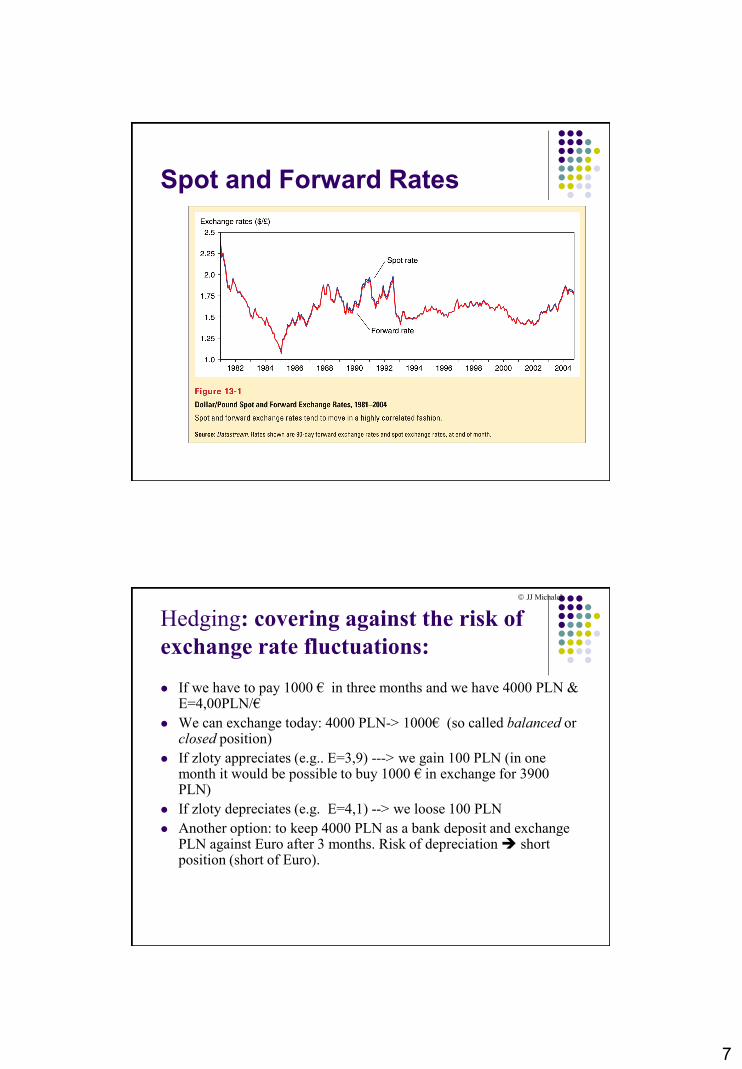

Spot and Forward Rates

Hedging: covering against the risk of

exchange rate fluctuations:

If we have to pay 1000 € in three months and we have 4000 PLN & E=4,00PLN/€

We can exchange today: 4000 PLN-> 1000€ (so called balanced or closed position)

If zloty appreciates (e.g.. E=3,9) ---> we gain 100 PLN (in one month it would be possible to buy 1000 € in exchange for 3900 PLN)

If zloty depreciates (e.g. E=4,1) --> we loose 100 PLN

Another option: to keep 4000 PLN as a bank deposit and exchange PLN against Euro after 3 months. Risk of depreciation short position (short of Euro).

JJ Michalek

8

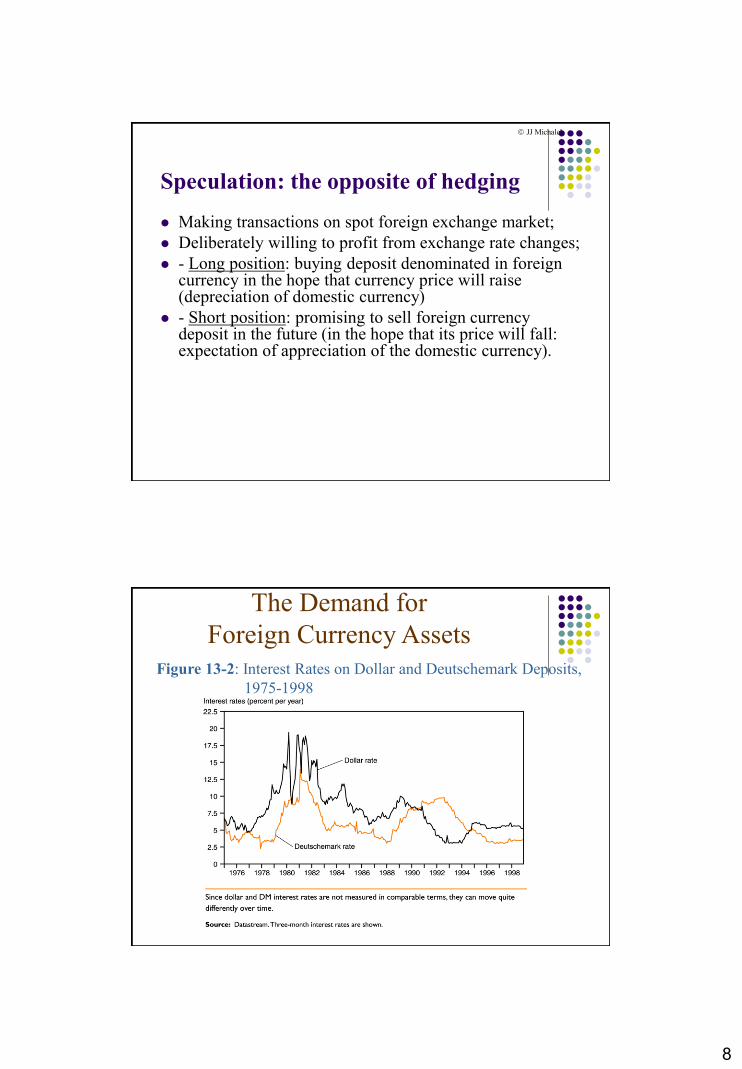

Speculation: the opposite of hedging

Making transactions on spot foreign exchange market;

Deliberately willing to profit from exchange rate changes;

- Long position: buying deposit denominated in foreign currency in the hope that currency price will raise (depreciation of domestic currency)

- Short position: promising to sell foreign currency deposit in the future (in the hope that its price will fall: expectation of appreciation of the domestic currency).

JJ Michalek

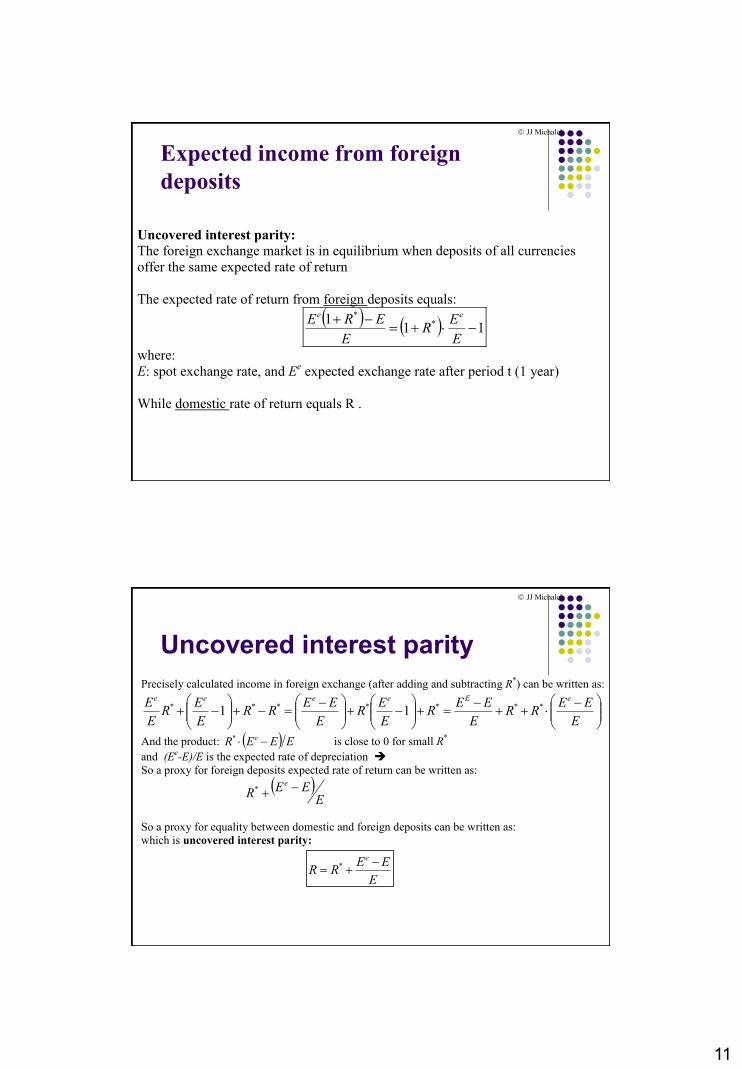

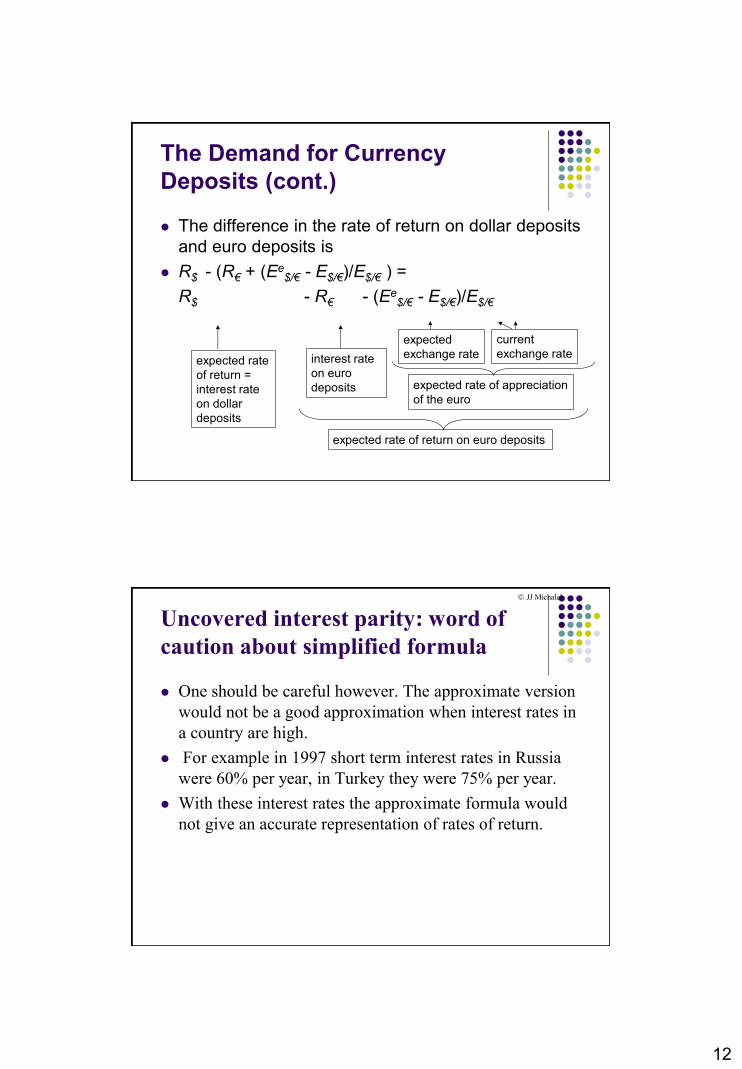

Figure 13-2: Interest Rates on Dollar and Deutschemark Deposits,

1975-1998

The Demand for

Foreign Currency Assets

9

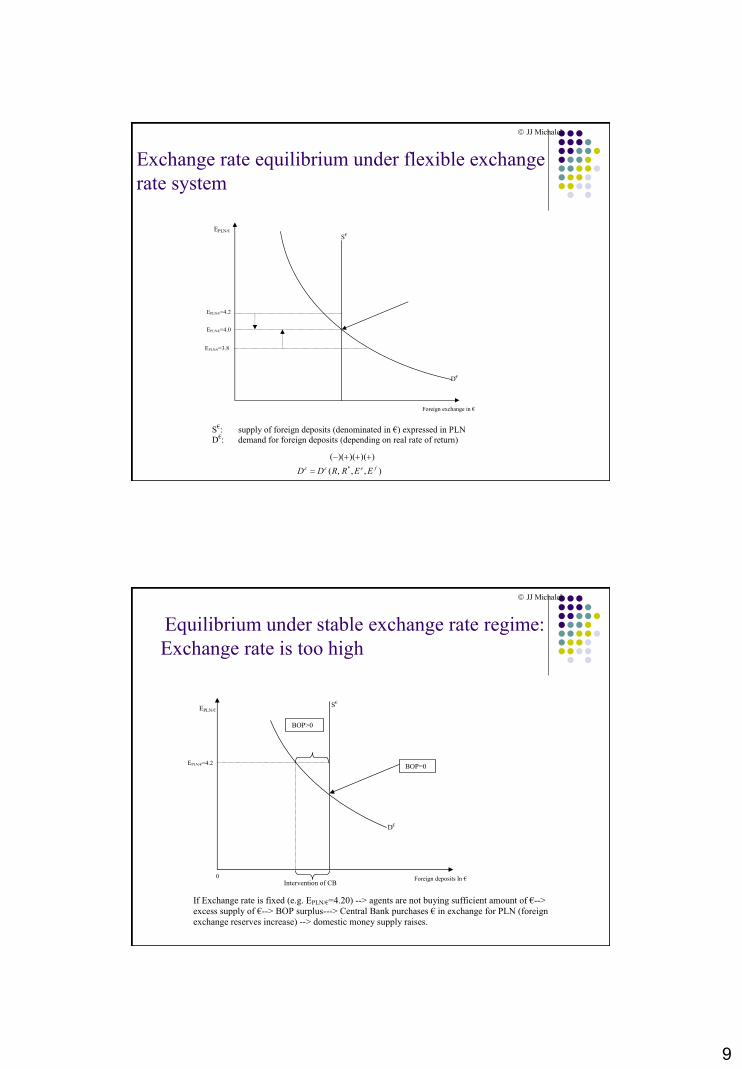

Exchange rate equilibrium under flexible exchange

rate system

S€: supply of foreign deposits (denominated in €) expressed in PLN

D€: demand for foreign deposits (depending on real rate of return)

EPLN/€=3.8

EPLN/€=4.2

EPLN/€=4.0

EPLN/€

S€

D€

Foreign exchange in €

),,,(

))()()((

* fe EERRDD

JJ Michalek

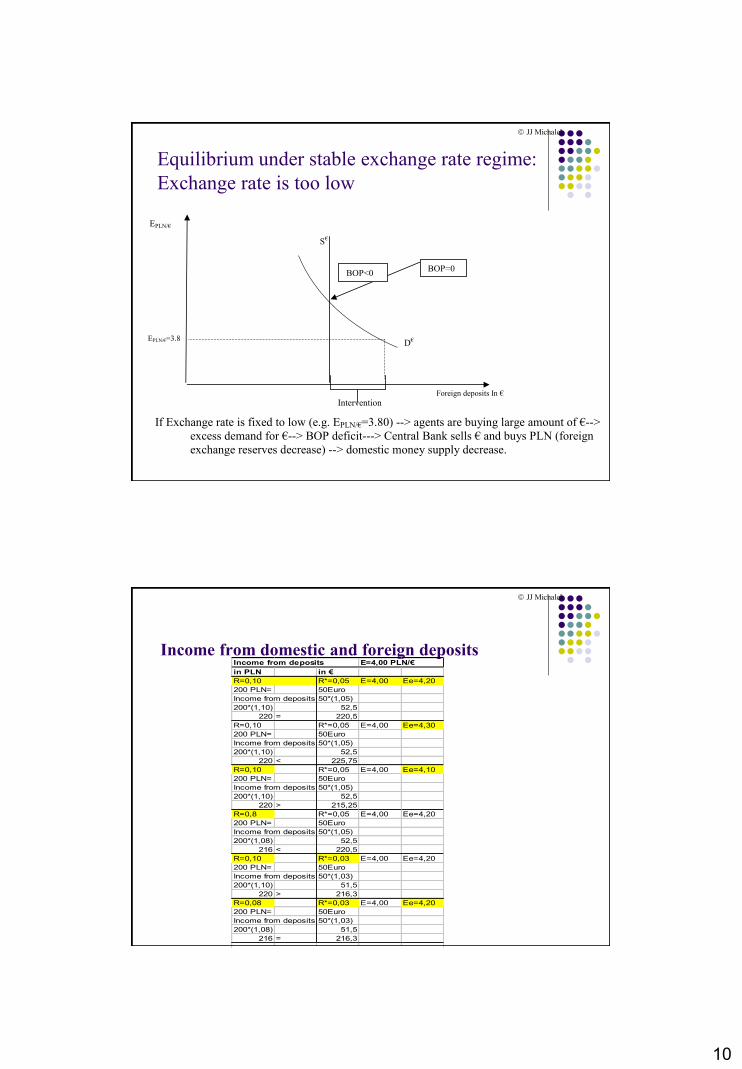

Equilibrium under stable exchange rate regime:

Exchange rate is too high

If Exchange rate is fixed (e.g. EPLN/€=4.20) --> agents are not buying sufficient amount of €-->

excess supply of €--> BOP surplus---> Central Bank purchases € in exchange for PLN (foreign