104

Exchange Rate Determination

| Date post: | 10-Dec-2015 |

| Category: |

Documents |

| Upload: | charles-burns |

| View: | 228 times |

| Download: | 2 times |

Exchange Rate Determination

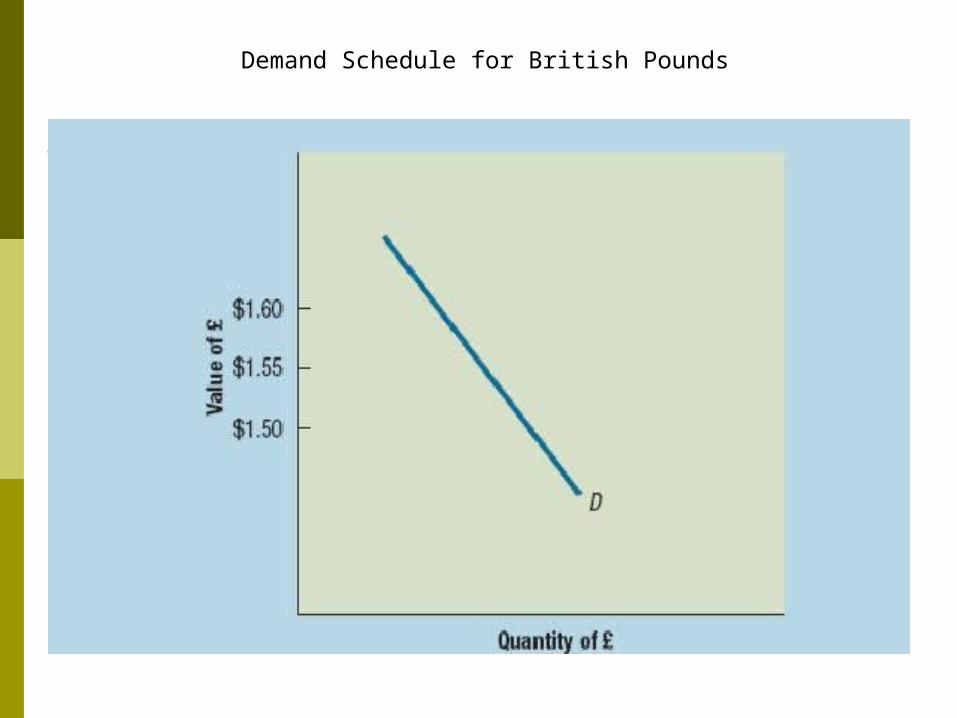

B. Exchange Rate EquilibriumHow exchange rates reach equilibrium?1. Demand for a Currency

a. derived from the local buyers who are willing and able to purchase foreign goods but who must convert their

local currencies.

b. An indirect relationship exists between the cost of foreign currency and amount demanded.

c. Graphically, a downward-sloping demand curve

The reason for the downward –sloping demand schedule is that the US corporation would be encouraged to purchase more British goods when the pound was worth less, because it would take fewer dollars to obtain the desired amount of pounds.

Exhibit 4.2 page 87

Demand Schedule for British Pounds

B. Exchange Rate Equilibrium2. Supply of a Currency for Sale

a. derived from the foreigners who are willing and able to supply foreign currency that must be converted first in order to purchase local goods.

b. A direct relationship exists between cost of the foreign currency and the amount supplied.

c. Graphically, an upward-sloping supply curve

When the pounds for the sale British consumers and firms are more likely to purchase U.S. goods. Thus, they supply a greater number of pounds to the market, to be exchanged for dollars.

conversely when the pound is valued low, the supply of pounds for sale is valued less, reflecting less British desire to obtain U.S. goods.

Exhibit 4.3 page 88

Supply Schedule of British Pounds for Sale

Exhibit 4.4 page 89

Equilibrium Exchange Rate Determination

Factors That Influence Exchange Rates1. Relative Inflation Rates2. Relative Interest Rates

a. Real Interest Rates3. Relative Income Levels

Relative Inflation Rates

The sudden jump in U.S. inflation should cause an increase in the U.S. demand for British goods and therefore also cause an increase in the U.S. demand for British pounds.

In addition, the jump in U.S. inflation should reduce the British desire for U.S. goods and therefore reduce the supply of pounds for sale.

At the previous equilibrium exchange rate of $ 1.55, there would be a shortage of pounds in the foreign exchange market.

The increased U.S. demand for pounds and the reduce supply of pounds for sale place upward pressure on the value of the pound. The new equilibrium value is $1.57.

Relative Interest Rates

U.S. interest rates rise while British interest rates remain constant.

In this case ,U.S. investors will likely reduce their demand for pounds, since the U.S. rates are now more attractive relative to British rates ,and there is less desire for British bank deposits.

U.S. rates will now look more attractive to British investors with excess cash, the supply of pounds for sale British investors should increase as they establish more bank deposits in the United States.

Due to an inward shift in the demand for pounds and an outward shift in the supply of pounds for sale, the equilibrium exchange rate should decrease.

Relative Income Levels

The U.S. income level rises substantially while the British income level remains unchanged.

Consider the impact of this scenario on (1) the demand schedule for pounds, (2) the supply schedule of pounds for sale, and (3) the equilibrium exchange rate.

First the demand schedule for pounds will shift outward, reflecting the increase in U.S. income and therefore increased demand for British goods.

Second, the supply schedule of pounds for sale is not expected to change. Therefore the equilibrium exchange rate of the pound is expected to rise.

Government ControlsGovernments influence the equilibrium exchange rate in many ways, including

1. imposing foreign exchange barriers,

2. imposing foreign trade barriers,

3. intervening (buying and selling currencies) in the foreign exchange markets,

4. affecting macro variables such as inflation, interest rates, and income levels.

E. Expectations1. The Role of Information

a. Impact of Signals on Currency Speculation

1.) commonly driven by signals of future interest rate movements

2.) by other factors such as signals of the future economic

conditions that affect exchange rates

Interaction of Factor An increase in income levels sometimes cause

expectations of higher interest rates.

So even though a higher income level can result in more imports, it may also indirectly attract more financial inflows (assuming interest rates increase).

Because the favorable financial flows may overwhelm the unfavorable trade flows, an increase in income levels is frequently expected to strength the local currency.

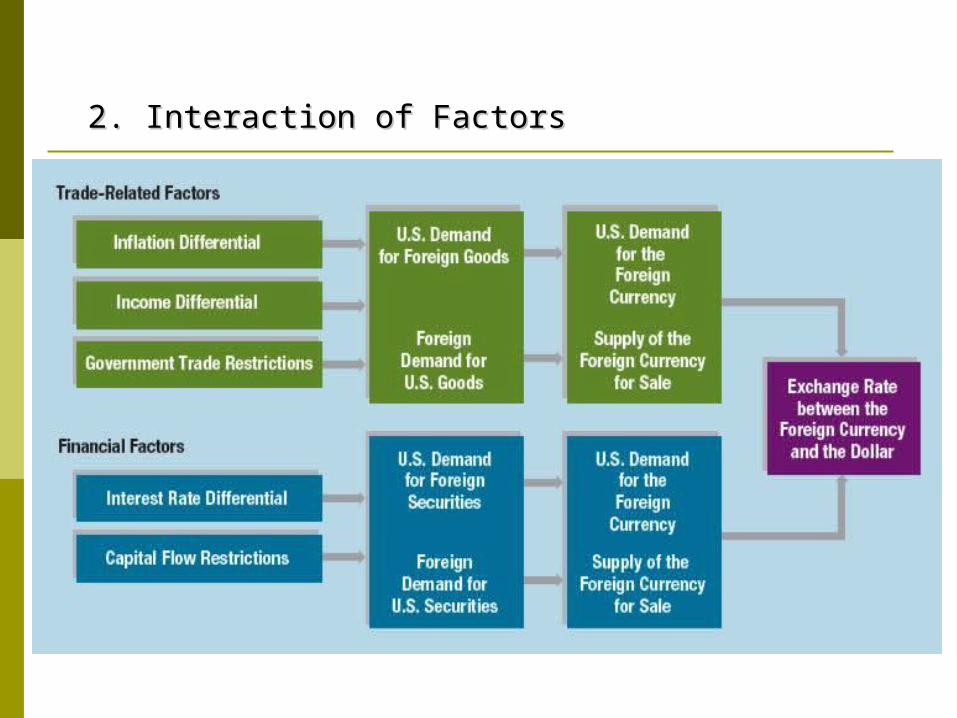

Interaction of factorsAssume the simultaneous existence of

(1) a sudden increase in U.S. inflation (2) a sudden increase in U.S. interest

rates.

If the British economy is relatively unchanged, the increase in U.S. inflation will place upward pressure on the pound’s value while the increase in U.S. interest rates place downward pressure on the pound’s value.

Interaction of factors The sensitivity of an exchange rate to these

factors is dependent on the volume of international transactions between the two countries.

If the two countries engage in a large volume of international trade but very small international capital flows, the relative inflation rates will likely be more influential.

If the two countries engage in a large volume of capital flows, however, interest rate fluctuations may be most influential.

2. Interaction of Factors2. Interaction of Factors

ARBITRAGE AND THE LAW OF ONE PRICE

I. THE LAW OF ONE PRICE Law states: Identical goods sell for the same

price worldwide.

If the price after exchange-rate adjustment

were not equal, arbitrage in the goods

worldwide ensures eventually it will.

The Three Theories of Exchange Rate determination

Purchasing Power Parity (PPP), which links spot exchange rates to nations’ price levels.

The Interest Rate Parity (IRP), which links spot exchange rates, forward exchange rates and nominal interest rates.

The International Fisher Effect (IFE) which links exchange rates to nations’ nominal interest rate levels.

Purchasing Power Parity (PPP)

The PPP theory focuses on the inflation-exchange rate relationships.

If the law of one price were true for all goods and services, we could obtain the theory of PPP.

There are two forms of the PPP theory.

Interpretations of PPP

The absolute form of PPP is an extension of the law of one price.

It suggests that the prices of the same products in different countries should be equal when measured in a common currency.

Absolute From of PPP The absolute from of PPP, also called the “law of one price,” suggests that prices of similar products of two different countries should be equal when measured in a common currency.

E=Pa/PbE= Ex ratePa and Pb are the purchasing power of two

currencies.

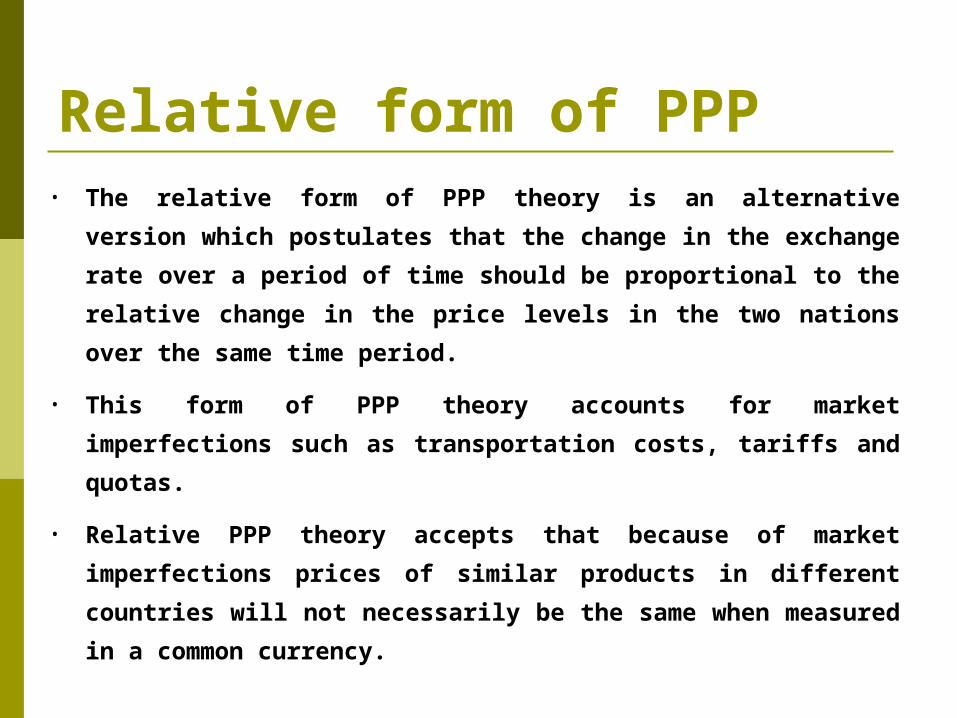

Relative form of PPP• The relative form of PPP theory is an alternative version

which postulates that the change in the exchange rate over

a period of time should be proportional to the relative

change in the price levels in the two nations over the same

time period.

• This form of PPP theory accounts for market imperfections

such as transportation costs, tariffs and quotas.

• Relative PPP theory accepts that because of market

imperfections prices of similar products in different

countries will not necessarily be the same when measured

in a common currency.

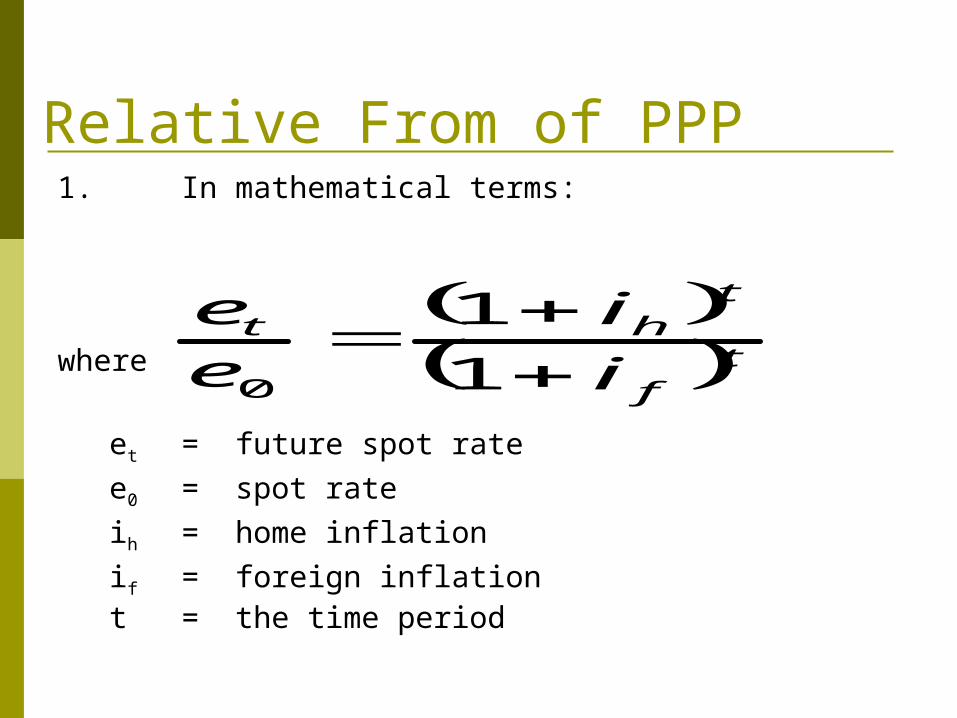

Relative From of PPP1. In mathematical terms:

where

et = future spot rate

e0 = spot rate

ih = home inflation

if = foreign inflation t = the time period

tf

tht

i

i

e

e

1

1

0

Relative From of PPPIf purchasing power parity is expected to hold, then the bestprediction for the one-periodspot rate should be

tf

th

ti

iee

1

10

Relative From of PPP For example, inflation rate in India is 5 per

cent and that in USA 3 per cent, an if the initial exchange rate is Rs. 40/US $, the value of the rupee in a two-year period will be

e2 = 40(1.05/1.03)2orRs. 41.57/US $

Relative From of PPP Such an inflation-adjusted rate is known as

the real exchange rate.

This means that if the real exchange rate is constant, currency gains or losses from nominal exchange rate changes will be offset by the difference in relative rates of inflation.

Rationale behind PPP Theory

Suppose U.S. inflation > U.K. inflation. U.S. imports from U.K. and

U.S. exports to U.K. Upward pressure is placed on the £ .

This shift in consumption and the £’s appreciation will continue until in the U.S.: priceU.K. goods priceU.S. goods

in the U.K.: priceU.S. goods priceU.K. goods

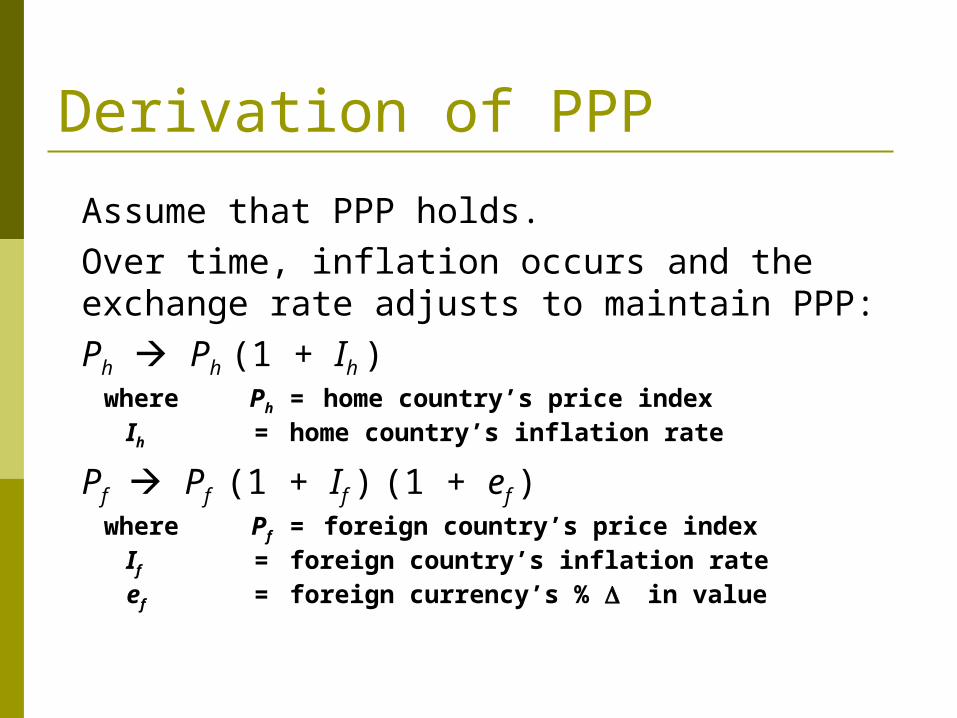

Derivation of PPP

Assume that PPP holds. Over time, inflation occurs and the exchange rate adjusts to maintain PPP:Ph Ph (1 + Ih )

where Ph = home country’s price indexIh = home country’s inflation rate

Pf Pf (1 + If ) (1 + ef )where Pf = foreign country’s price index

If = foreign country’s inflation rateef = foreign currency’s % in value

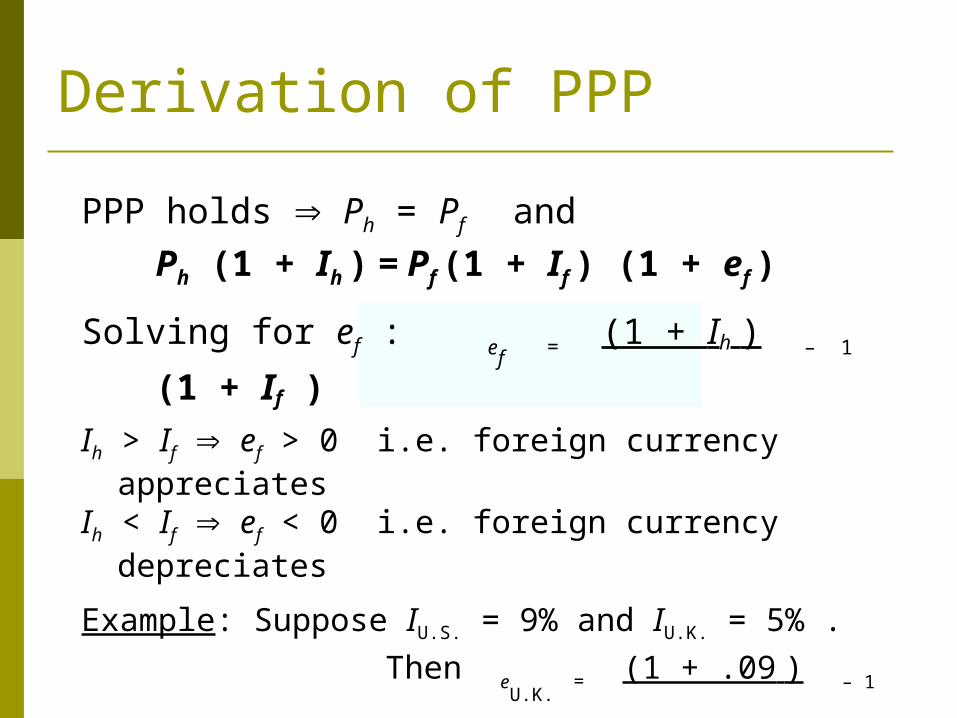

Derivation of PPP

Ih > If ef > 0 i.e. foreign currency appreciatesIh < If ef < 0 i.e. foreign currency depreciates

Example: Suppose IU.S. = 9% and IU.K. = 5% .

Then eU.K.

= (1 + .09 ) – 1 = 3.81%

(1 + .05 )

PPP holds Ph = Pf and

Ph (1 + Ih ) = Pf (1 + If ) (1 + ef )

Solving for ef : ef = (1 + Ih ) – 1

(1 + If )

Simplified PPP Relationship

When the inflation differential is small, the PPP relationship can be simplified as

ef Ih – If

Example:Suppose IU.S. = 9% and IU.K. = 5% . Then eU.K. 9 – 5 = 4%

Relative From of PPP When a government sticks to a particular

exchange rate without caring prevailing inflation, a gap emerges- between the real and the nominal exchange rates which results in lowering of export competitiveness and in turn, the trade deficit.

This is why, this theory suggests that a country with high rate of inflation should devalue its currency relative to the currency of the countries with lower inflation rates.

Again, it is the real exchange rate, and not the nominal exchange rate, that has a bearing on the performance of the economy

The Theory holds good only Relative price structure remains stable in

different sectors; since changes in the relative prices of various goods and services may lead to differently constructed indices to deviate from each other, and

There is no structural change in the economy, such as changes in tariff, in technology, and in autonomous capital flow.

EVIDENCE FOR THE THEORY The absolute version has been tested by Isard (1977) and

McKinnon (1979). Both of them find violation of the theory in the short run, but in the long run, they find the theory holding good to some extent.

As regards the relative version, the studies made till the early 1980s found normally relationship existing between rate of inflation and exchange rate, especially in the long run (Aliber and Stickney, 1975;Dornbusch, 1976; Mussa, 1982).

Subsequent studies find clear-cut violation of the theory also in the long run (Adler and Lehmann, 1983; Edison, 1985), Taylor (1988) finds very little evidence for PPP to hold good, In a review of 14 cases, MacDonald (1988) finds that in 10 cases, the theory is not applicable even in the long run, but in four cases it holds good.

PPP theory does not hold good in real life. Firstly, the assumptions of this theory do not hold good in

real life.

Secondly extraneous factors such as interest rates, governmental interference, etc. influence the exchange rate.

The early 1990s for instance, some of the European countries experienced higher inflation rates than the USA, but their currencies did not depreciate against the dollar because their high interest rates attracted capital from the USA.

Thirdly, when no domestic substitute to an import is available, the material is imported even after the prices go higher in the exporting countries.

Testing the Purchasing Power Parity Theory

Conceptual Tests of PPP1.) Choose two countries (say, India and a foreign country United States)

2.) Compare the differential in their inflation rates to the percentage change in the foreign Currency’s value during several time periods.

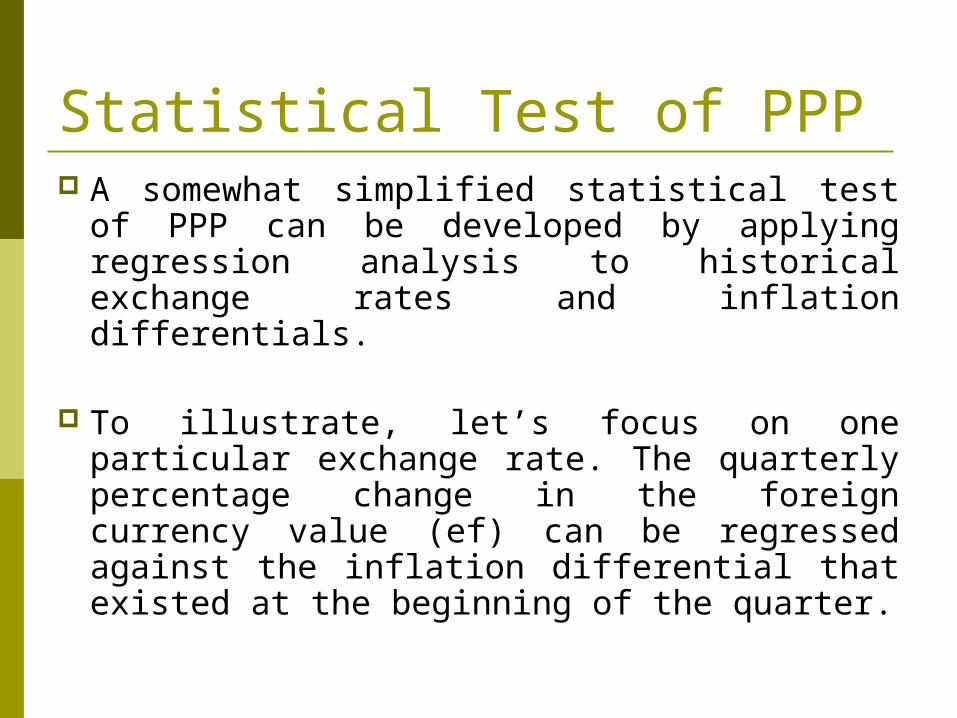

Statistical Test of PPP A somewhat simplified statistical test of

PPP can be developed by applying regression analysis to historical exchange rates and inflation differentials.

To illustrate, let’s focus on one particular exchange rate. The quarterly percentage change in the foreign currency value (ef) can be regressed against the inflation differential that existed at the beginning of the quarter.

Statistical Test of PPP

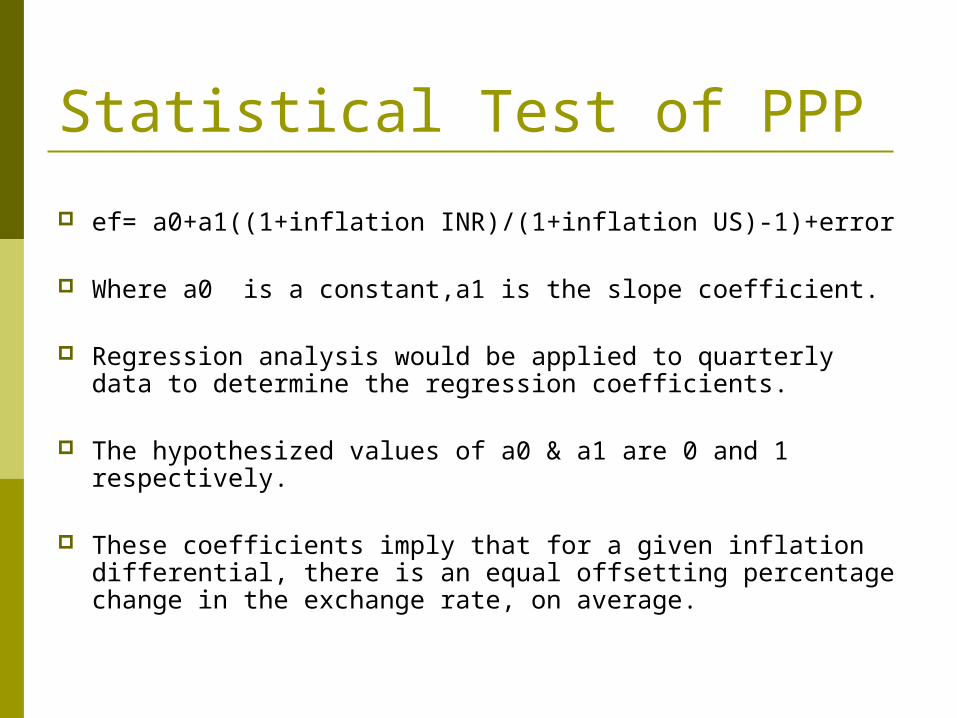

ef= a0+a1((1+inflation INR)/(1+inflation US)-1)+error

Where a0 is a constant,a1 is the slope coefficient.

Regression analysis would be applied to quarterly data to determine the regression coefficients.

The hypothesized values of a0 & a1 are 0 and 1 respectively.

These coefficients imply that for a given inflation differential, there is an equal offsetting percentage change in the exchange rate, on average.

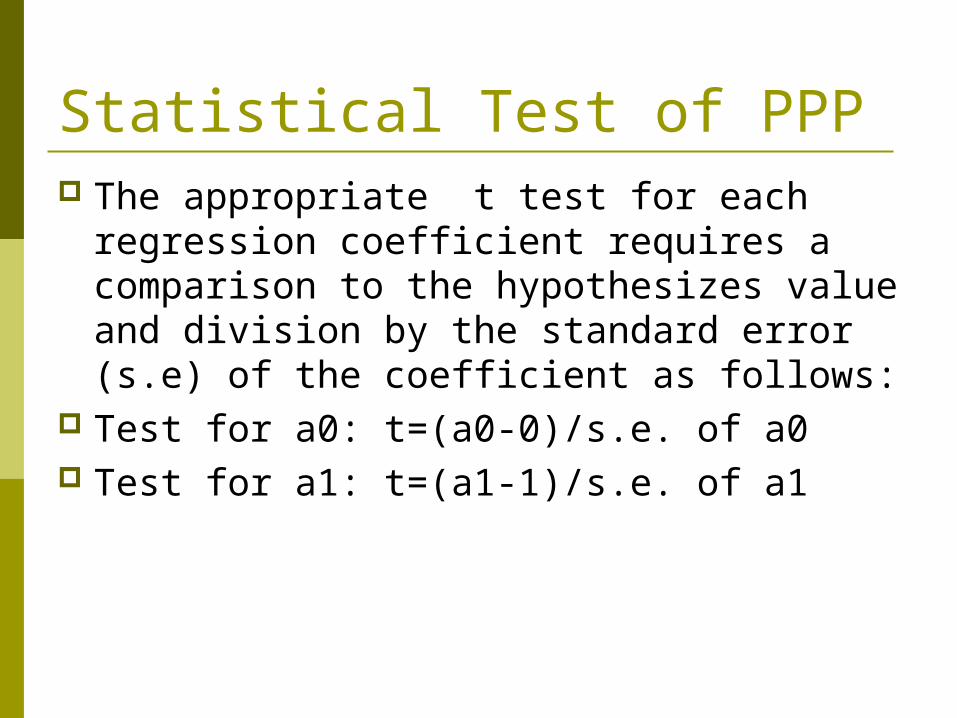

Statistical Test of PPP The appropriate t test for each regression

coefficient requires a comparison to the hypothesizes value and division by the standard error (s.e) of the coefficient as follows:

Test for a0: t=(a0-0)/s.e. of a0 Test for a1: t=(a1-1)/s.e. of a1

Statistical Test of PPP Then the t-table is used to find the critical t-value.

If either t-test finds that the coefficients differ significantly from what is expected, the relationship between the inflation differential and the exchange rate differ from that stated by PPP theory.

It should be mentioned that the appropriate lag time between the inflation differential and the exchange rate is subject to controversy.

Empirical studies indicate that the relationship between inflation differentials and exchange rates is not perfect even in the long run.

However, the use of inflation differentials to forecast long-run movements in exchange rates is supported.

A limitation in the tests is that the choice of the base period will affect the result.

Testing the PPP Theory

PPP in the Long Run

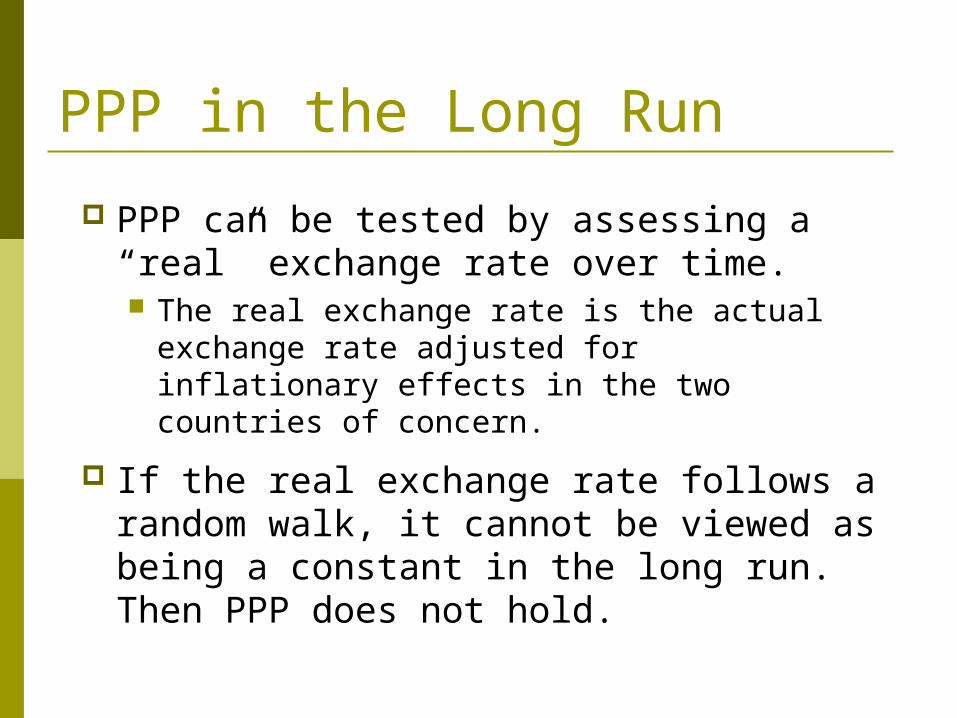

PPP can be tested by assessing a “real” exchange rate over time. The real exchange rate is the actual

exchange rate adjusted for inflationary effects in the two countries of concern.

If the real exchange rate follows a random walk, it cannot be viewed as being a constant in the long run. Then PPP does not hold.

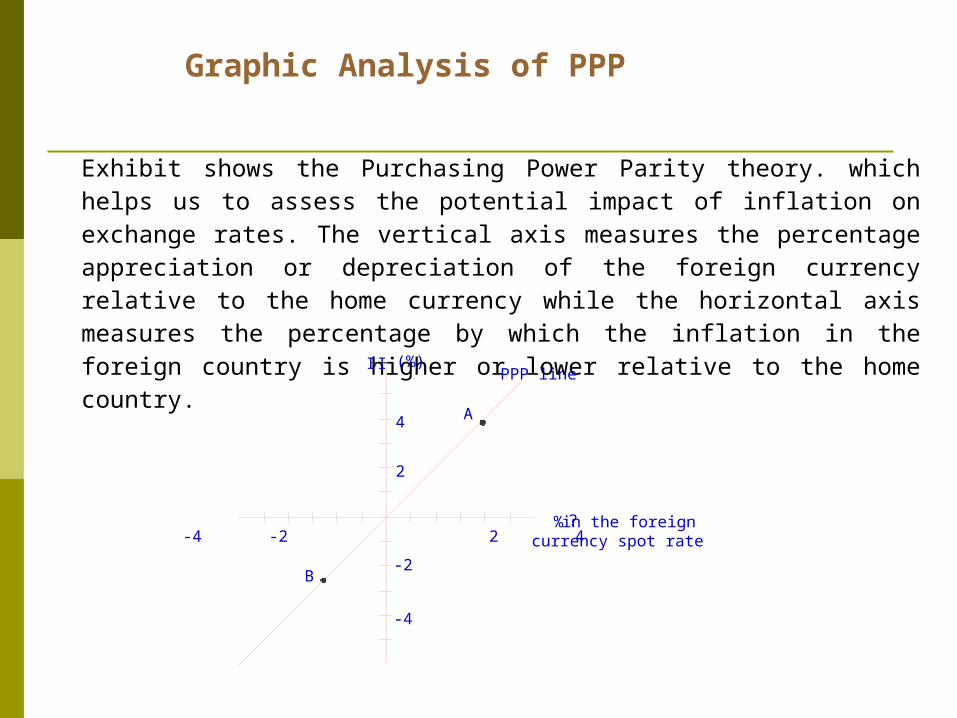

Exhibit shows the Purchasing Power Parity theory. which helps us to assess the potential impact of inflation on exchange rates. The vertical axis measures the percentage appreciation or depreciation of the foreign currency relative to the home currency while the horizontal axis measures the percentage by which the inflation in the foreign country is higher or lower relative to the home country.

I -I (%)

4

2

-2

-4

-4 -2 2 4% ? in the foreigncurrency spot rate

PPP line

A

B

Graphic Analysis of PPP

Fisher Effect-Interest Rate The Fisher effect states that whenever an investor

thinks of an investment, he is interested in a particular nominal interest rate which covers both the expected inflation and the required real interest rate Mathemetically, it can be expressed as

1 + r = (1 + a)(1 + I) where

r = nominal interest rate,a = real interest rate, and

I = expected rate of inflation.

Fisher Effect-Interest Rate Suppose the required real interest rate is 4 per

cent and the expected rate of inflation is 10 per cent, the required nominal interest rate will be:

1.04 x 1.10 - 1 = 14.4%

Suppose, the interest rate in the USA is 4 per cent and the inflation rate in India is 10 per cent higher than in the USA. A US investor will be tempted to invest in India only when the nominal interest in India is more than 14.4 per cent.

Fisher Effect-Interest Rate The concept of real interest rate applies to

all investment-domestic and foreign.

An Investor invests in a foreign country if the real interest rate differential is likely to be in his favor, but when such a differential exists, arbitrage begins in the form of international capital flow that ultimately equals the real interest rate across countries.

Fisher effect-Interest Rate For this type of arbitrage, it is necessary

that the capital market be homogeneous throughout the world so that the investors do not differentiate between the domestic capital market and the foreign capital markets.

Fisher effect-Interest Rate In real life, such homogeneous capital market is not found

in view of government restrictions and varying economic policies in different countries.

As a result, interest rates vary among countries. Mishkin (1984) confirms this view and finds that investors have a strong liking for the domestic capital market in order to insulate themselves from foreign exchange risk; and so, there will be no arbitrage even if real interest rate on foreign securities is higher.

The Fisher effect holds good normally in case of short-maturity government securities and very seldom in other cases.

Interest Rate Parity A theory that the interest rate differential

between two countries is equal to the differential between the forward exchange rate and the spot exchange rate.

Interest rate parity plays an essential role in foreign exchange markets, connecting interest rates, spot exchange rates and foreign exchange rates

Interest Rate Parity Formula

(Forward rate / spot rate) = (1 + interest rate A) / (1 + interest rate B)

Calculating the Forward Exchange Rate

The future value of a currency is the present value of the currency + the interest that it earns over time in the country of issue.

Future Value of Currency (FV)

FV=P(1+r)n

FV = Future Value of CurrencyP = Principalr = interest rate per yearn = number of years

Calculating the Forward Exchange Rate

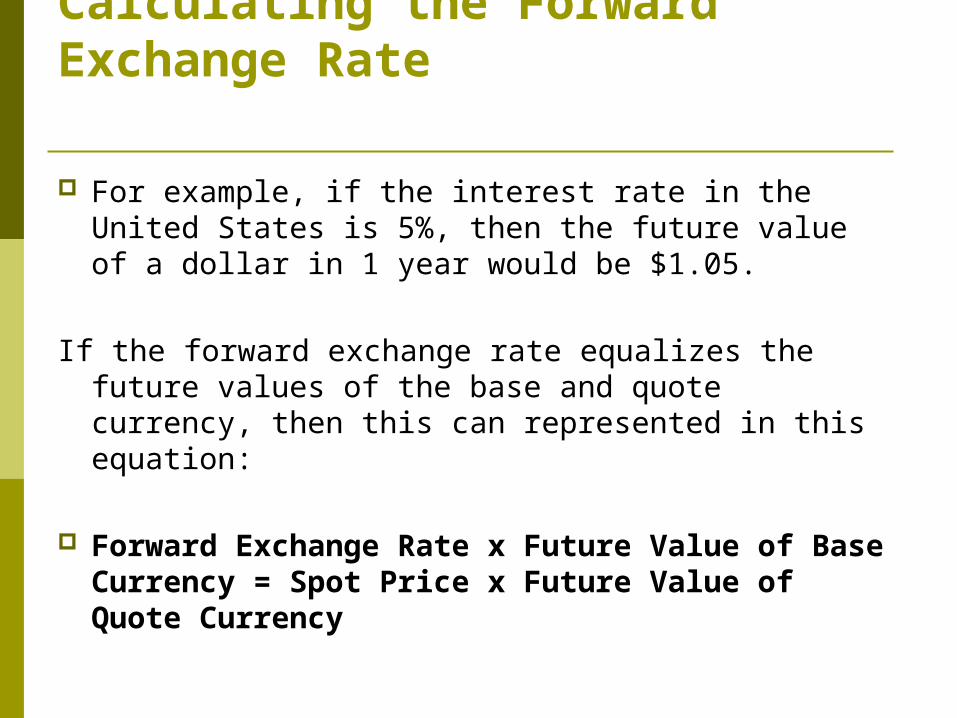

For example, if the interest rate in the United States is 5%, then the future value of a dollar in 1 year would be $1.05.

If the forward exchange rate equalizes the future values of the base and quote currency, then this can represented in this equation:

Forward Exchange Rate x Future Value of Base Currency = Spot Price x Future Value of Quote Currency

Calculating the Forward Exchange Rate

Forward Exchange Rate

ForwardExchange

Rate

= Spot Price x

Future Value ofQuote

Currency────────────

Future Value ofBase Currency

=S(1+rq)n

───────(1+rb)n

S = Spot Pricerq = Interest Rate of Quote Currencyrb = Interest Rate of Base Currencyn = Number of Compounding Periods

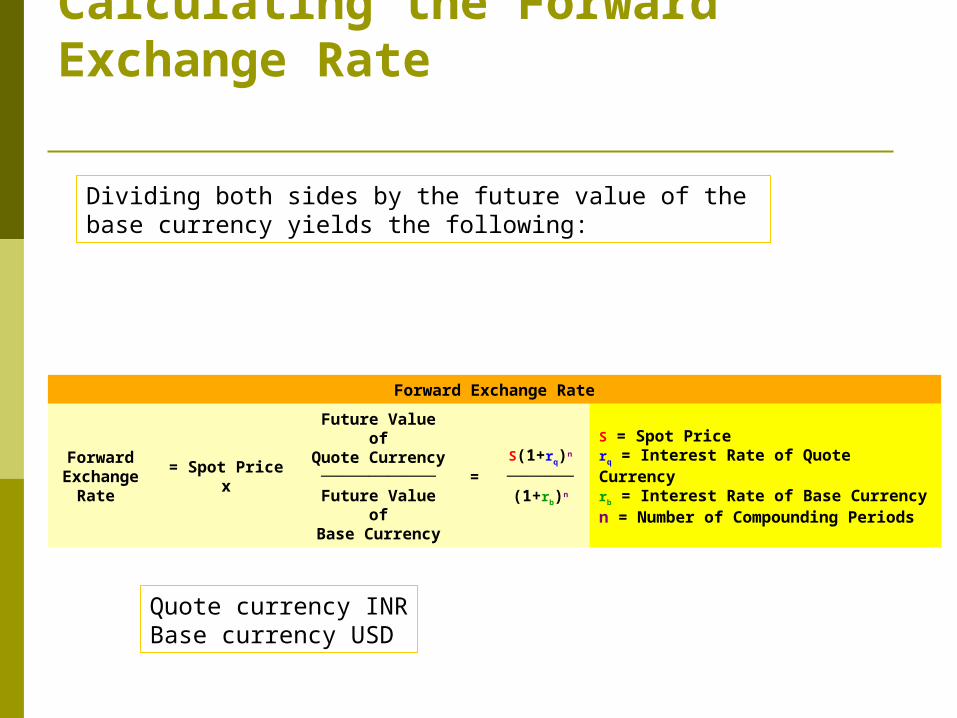

Dividing both sides by the future value of the base currency yields the following:

Quote currency INRBase currency USD

Example — Calculating the Forward Exchange Rate For instance, if the spot price for USD/EUR = 0.7395, then

this means that 1 USD = .7395 EUR.(USD- base currency, EURO-Quote currency )

The interest rate in Europe is 3.75%, and the interest rate in the United States is 5.25%.

In 1 year, 1 dollar earning United States interest will be worth $1.0525 and 0.7395 Euro earning the European interest rate of 3.75% will be worth 0.7672 Euro.

Thus, the forward spot rate 1 year from now is equal to 0.7672/1.0525,

Example — Calculating the Forward Exchange Rate

ForwardExchange

Rate =

S(1+rq)n

──────(1+rb)

n

=─ 0.7395(1+0.0375)1

───────────(1+0.0525)1

=0.7395 *1.0375──────────

1.0525= 0.7290

Thus, the forward exchange rate is 1 USD = 0.7290 (rounded) Euro, or simply, the forward rate.

methods of calculating the forward rate results in slight differences):

Euro has appreciated

Interest Rate Parity

The reason why the forward exchange rate is different from the current exchange rate is because the interest rates in the countries of the respective currencies is usually different, thus, the future value of an equivalent amount of 2 currencies will grow at different rates in their country of issue.

The forward exchange rate equalizes the difference in interest rates of the 2 countries. Thus, the forward exchange rate maintains interest rate parity.

A corollary is that if the interest rates of the 2 countries are the same, then the forward exchange rate is simply equal to the current exchange rate.

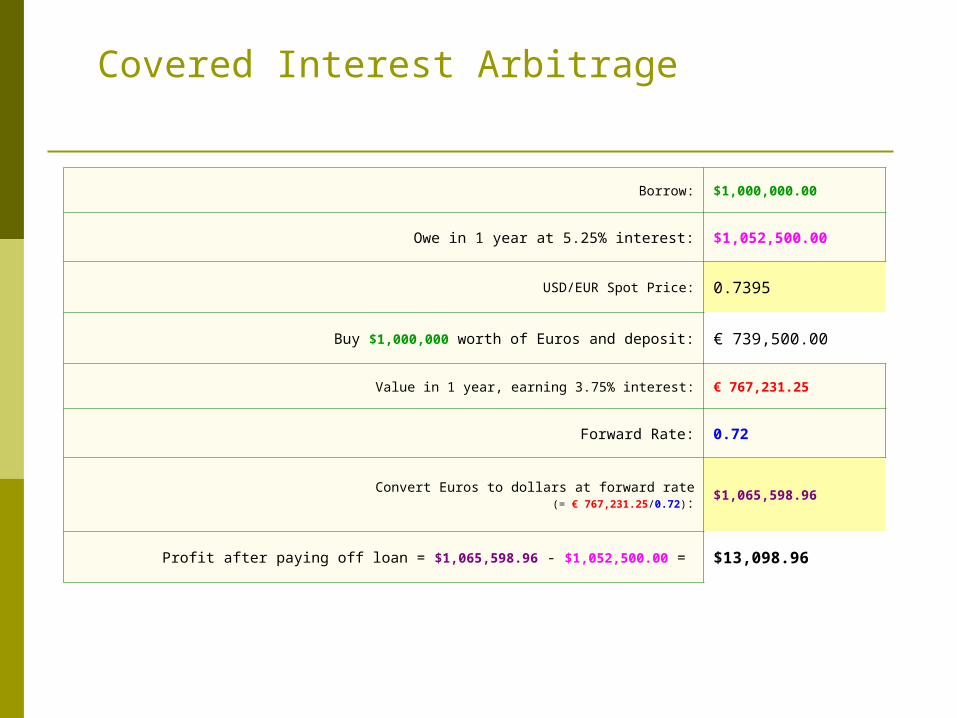

FX Spot — Forward Arbitrage (Covered Interest Arbitrage)

If the future values of the currencies are not equalized, then an arbitrage opportunity will exist, allowing an arbitrageur to earn a riskless profit.

Taking the above example of dollars and Euros, we found the forward rate to be 0.7289. But what if the forward rate were only 0.72?

Then we can borrow, let's say, $1,000,000 to buy Euros, deposit the Euros in a bank account, earn interest on it for 1 year, then convert the Euros back to dollars, then pay off the loan.

Invest in a currency which is appreciating.

The rest is risk-free profit. This is known as FX spot-forward arbitrage or covered interest arbitrage.

Borrow: $1,000,000.00

Owe in 1 year at 5.25% interest: $1,052,500.00

USD/EUR Spot Price: 0.7395

Buy $1,000,000 worth of Euros and deposit: € 739,500.00

Value in 1 year, earning 3.75% interest: € 767,231.25

Forward Rate: 0.72

Convert Euros to dollars at forward rate(= € 767,231.25/0.72):

$1,065,598.96

Profit after paying off loan = $1,065,598.96 - $1,052,500.00 = $13,098.96

Covered Interest Arbitrage

FX Forward Price Quotes Are Expressed in Forward Points

Because exchange rates change by the minute, forward prices are usually quoted as the difference in pips—forward points—from the current exchange rate.

Since currency in the country with the higher interest rate will grow faster and because interest rate parity must be maintained, it follows that the currency with a higher interest rate will trade at a discount in the FX forward market, and vice versa.

So if the currency is at a discount in the forward market, then you subtract the quoted forward points in pips; otherwise the currency is trading at a premium in the forward market, so you add them.

FX Forward Price Quotes Are Expressed in Forward Points

In our above example of trading dollars for Euros, the United States has the higher interest rate, so the dollar will be trading at a discount in the forward market.

With a current exchange rate of EUR/USD = 0.7395 and a forward rate of 0.7289, the forward points is equal to 106 pips, which in this case would be subtracted.

Practical Considerations

Interest rate parity assumes that there will be no transaction fees and that neither party will default on the transaction.

In actual practice, currency prices quoted by banks to customers often include a risk premium.

Deviations from IRP

Why might actual deviations from IRP occur?

transactions costs capital controls political risk

Spurious deviations from IRP could be due to:

taxes timing noncomparableasset

Covered Interest Arbitrage If the forward rate differential is not equal to the interest

rate differential, covered interest arbitrage will begin and it will continue till the two differentials become approximately equal.

In other words, a positive interest rate differential in a country is offset by annualized forward discount.

A negative interest rate differential is offset by an annualized forward premium.

Finally, the two differentials will be equal. In fact, this is the point where the forward rate is determined.

Covered Interest Arbitrage… Another example To explain the process of covered interest

arbitrage, suppose the spot rate is Rs. 40/US $ and the three-month forward rate is Rs. 40.28/ US $ involving a forward differential of 2.8 per cent. [(40.28-40)/40]*100

The interest rate is 18 per cent in India and 12 per cent in the USA involving interest rate differential of 5.37 per cent.[(1.18-1.12)/1.12]*100

Since the two differentials are not equal, covered interest arbitrage will begin.

Covered Interest Arbitrage.. STEPS Borrowing in the USA, say, US $ 1,000 at 12 per cent

interest Converting the US dollar into the rupee at spot rate to get

Rs. 40,000/ Investing Rs. 40,000 in India at 18 per cent interest Selling the rupee 90-day forward at Rs. 40.28/$ After three months, liquidating the Rs. 40,000 investment

which would fetch Rs. 41,800 Selling Rs. 41,800 for US dollars at the rate of Rs. 40.28/US

$ to get US $ 1,038 Repaying loan in the USA which amounts to US $ 1,030 Reaping profit: US $ 1,038 - 1,030 = US $ 38.

Covered Interest Arbitrage So long as inequality continues between the forward rate

differential and the interest rate differential, arbitrageurs will profit and the process of arbitrage will go on.

The differential will be wiped out for the following reasons:

1.Borrowing in the USA will raise the interest rate there. 2. Investing in India would increase the invested funds and

thereby lower the interest rate there. 3. Buying rupees at spot rate will increase spot rate of the

rupee. 4. Selling rupees forward will depress the forward rate of the

rupee.

Covered Interest Arbitrage The first two actions narrow the interest rate

differential, while 3 and 4 widen the forward rate differential.

However, the real life experience shows that the two differentials-interest rate and forward rate-are equal only approximately and not precisely.

It is because the interest rate parity theorem assumes no transaction cost, no tax rate.

Covered Interest Arbitrage First of all, there is always transaction cost

involved in selling a currency spot and buying it forward.

The transaction cost, which is manifest in the bid-ask spread, forces forward rate differential to deviate from the expected one.

The transaction cost, which is involved also in borrowing and investing, influences the effective interest rate and thereby the interest rate differential.

Covered Interest Arbitrage Secondly, there is disparity in the tax rate

on interest income in different countries. Such a disparity allows the interest rate differential to deviate from the expected one.

Last but not least, if there is political unrest in the country where the funds are invested, the cost of investment will be greater and this will influence the interest rate differential.

Uncovered Interest Arbitrage In an uncovered interest arbitrage, the

arbitrageur does not take advantage of the forward market and does not go for any forward contract for reaping profit.

Rather the decision behind profit-making depends upon the expectation about the future spot rate, inasmuch as the interest rate differential between two countries leads to changes in future spot rate.

Uncovered Interest Arbitrage If interest-rate differential is not equal to

changes in the future spot rate, uncovered interest parity will exist. This can be represented in the form of an equation:(1 + RA)/(1 + RB) = (Se+l - S)/Swhere Se+l is the expected future spot rate, RA and RB are the interest rates in Country A and Country B.

Uncovered Interest Arbitrage So long as equality is not reached, the arbitrageurs will go

for uncovered interest arbitrage and reap profits.

Suppose the interest rate on the Indian treasury bill is 7.0 per cent and that on the UK treasury bill is 4.0 per cent and so the interest rate differential is 2.88 per cent.

[(1.07-1.04/1.04)*100] If the investor expects a depreciation of 4.0 per cent in the

future spot rate of Indian rupee he/she will invest in the UK treasury bill because a fixed amount of British pound will fetch greater amount of Indian rupee at a future date.

This will go on till the two differentials are equal. This is uncovered interest arbitrage.

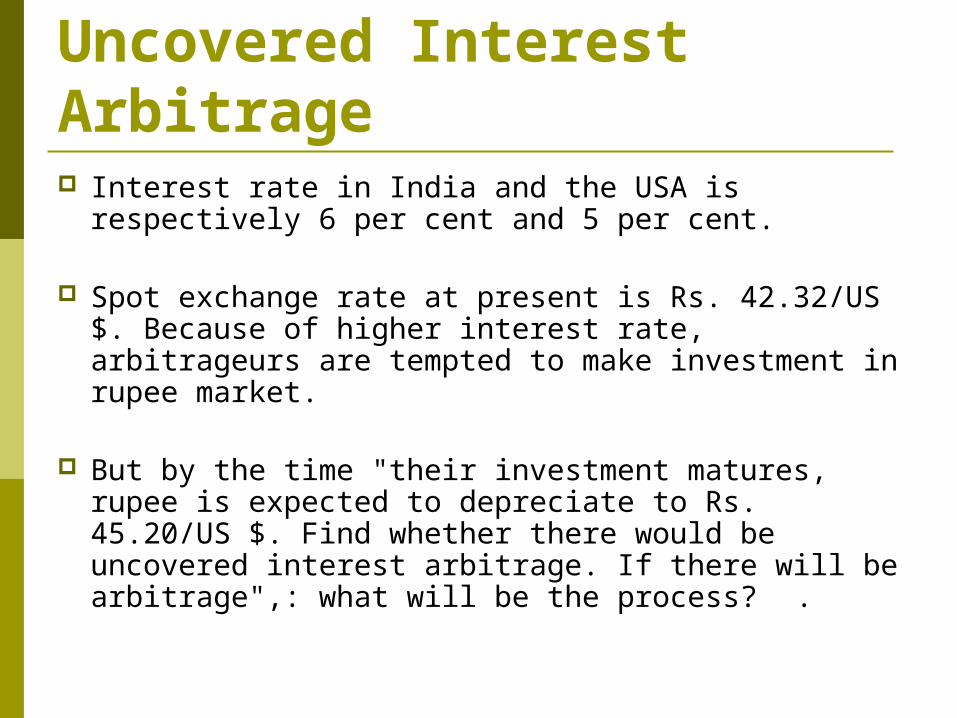

Uncovered Interest Arbitrage Interest rate in India and the USA is respectively 6

per cent and 5 per cent.

Spot exchange rate at present is Rs. 42.32/US $. Because of higher interest rate, arbitrageurs are tempted to make investment in rupee market.

But by the time "their investment matures, rupee is expected to depreciate to Rs. 45.20/US $. Find whether there would be uncovered interest arbitrage. If there will be arbitrage",: what will be the process? .

Uncovered Interest Arbitrage Interest rate differential = 1.06/1.05 – 1 = 0.95 per cent

Future spot rate differential = (45.20 – 42.32)/42.32 = 6.81 percent

Since these two differentials are not equal, uncovered parity does not exist. As a result, there will be uncovered interest arbitrage.

Again, under this type of situation, arbitrageurs will take back their investment out of rupees market for fear of lower return in terms of US dollar. As a result of lower supply of money there, Indian interest rate will ascend to achieve uncovered parity.

Evaluating IRP Theorem

The study of Marston (1976) shows that the IRP theorem held good with greater accuracy in the Euro-currency market in view of the complete freedom from controls and restrictions.

Similar findings emerge from the work of Giddy and Duffey (1975).

However, there are studies that identify deviation from the theorem (Officer and Willet, 1970; Aliber, 1973; Frenkel and Levich, 1975).

Evaluating IRP Theorem

The reasons for derivations are:(i) Since different rates prevail on bank deposits,

loans, treasury bills, etc., short-term interest rate cannot be specific and the chosen rate can hardly be the definitive rate of the formula.

(ii) The marginal interest rate applicable to borrowers and lenders differs from the average interest rate because interest rate changes with successive amount of borrowing.

Evaluating IRP Theorem

(iii) The investment in foreign assets is more risky than that in domestic assets. If greater diversification is applied to foreign investment in order to lower the risk element, the law of diminishing returns may apply; and as a result, the arbitrageurs may not respond to the interest rate differential as envisaged by the IRP theorem.

(iv) There are also cases when interest rate parity is disturbed owing to the play of extraordinary forces leading to speculation. It is basically the market expectation of future spot rates that influences the forward rate.

If market expectations are strong enough, they can push forward rates beyond the point which interest rate parity would dictate.

Evaluating IRP Theorem

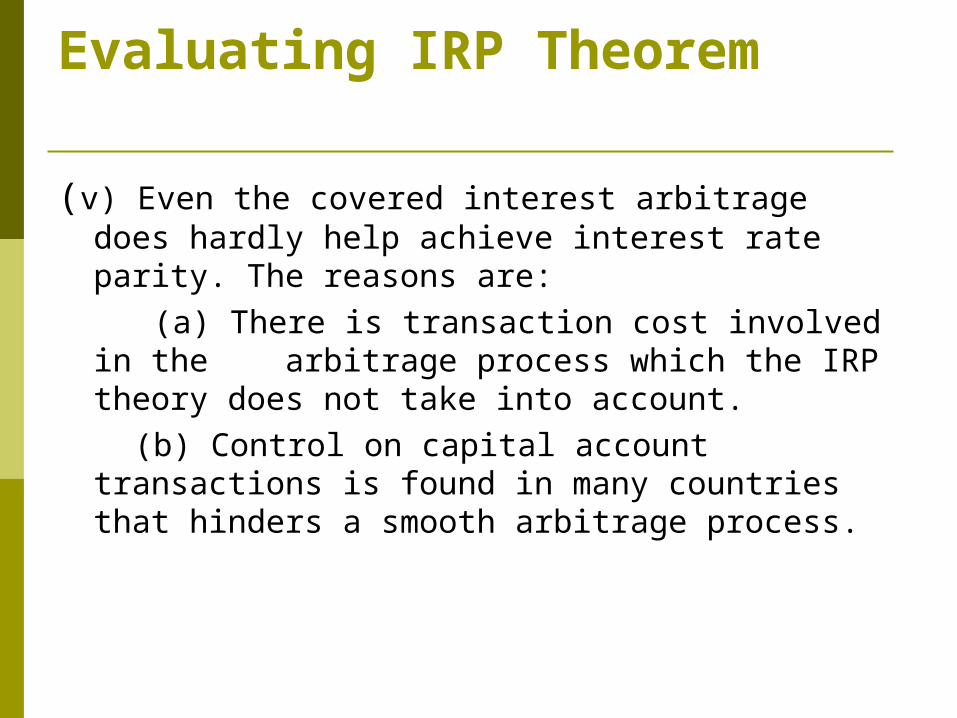

(v) Even the covered interest arbitrage does hardly help achieve interest rate parity. The reasons are:

(a) There is transaction cost involved in the arbitrage process which the IRP theory does not take into account.

(b) Control on capital account transactions is found in many countries that hinders a smooth arbitrage process.

Combined Effect of Interest Rate and Inflation- Fisher’s open proposition, known as the

International Fisher Effect or generalized version of the Fisher effect.

It is a combination of the conditions of the PPP theory and Fisher's closed proposition.

PPP theory suggests that exchange rate is determined by the inflation rate differentials, while the latter states that the nominal interest rate is higher in a country with higher inflation rate .

Combined Effect of Interest Rate and Inflation-

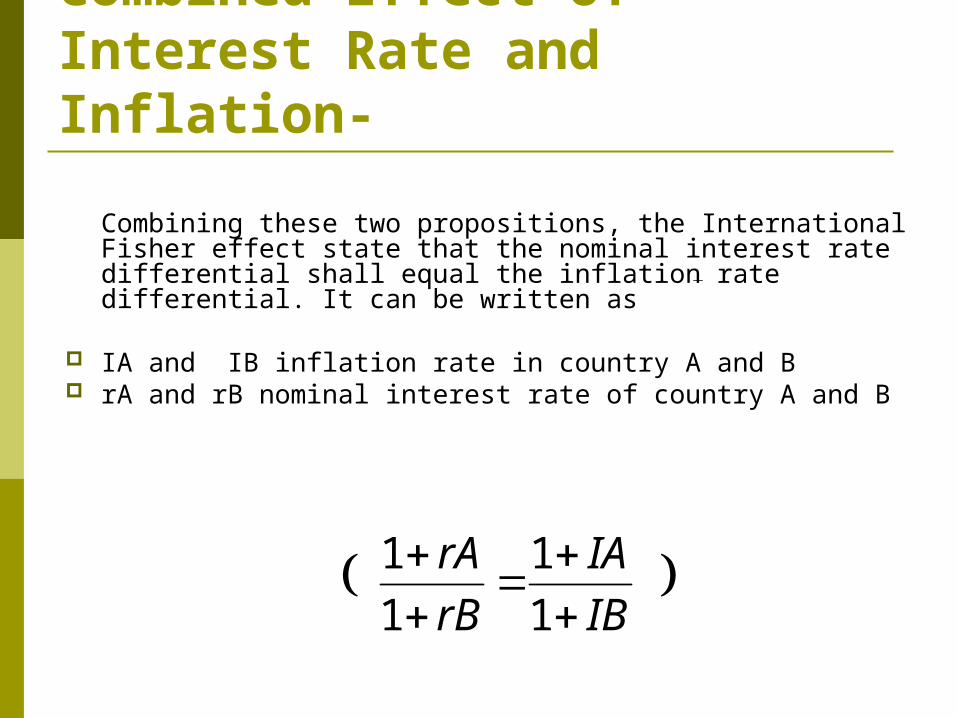

Combining these two propositions, the International Fisher effect state that the nominal interest rate differential shall equal the inflation rate differential. It can be written as

IA and IB inflation rate in country A and B rA and rB nominal interest rate of country A and B

IB

IA

rB

rA

1

1

1

1

Combined Effect of Interest Rate and Inflation- The rationale behind this proposition is that an

investor likes to hold assets denominated in currencies expected to depreciate only when the interest rate on those assets is high enough to compensate the loss on account of depreciating exchange rate.

As a corollary, an investor holds assets denominated in currencies expected to appreciate even at a lower rate of interest because the expected capital gain on account of exchange rate appreciation will make up the loss on yield on account of low interest.

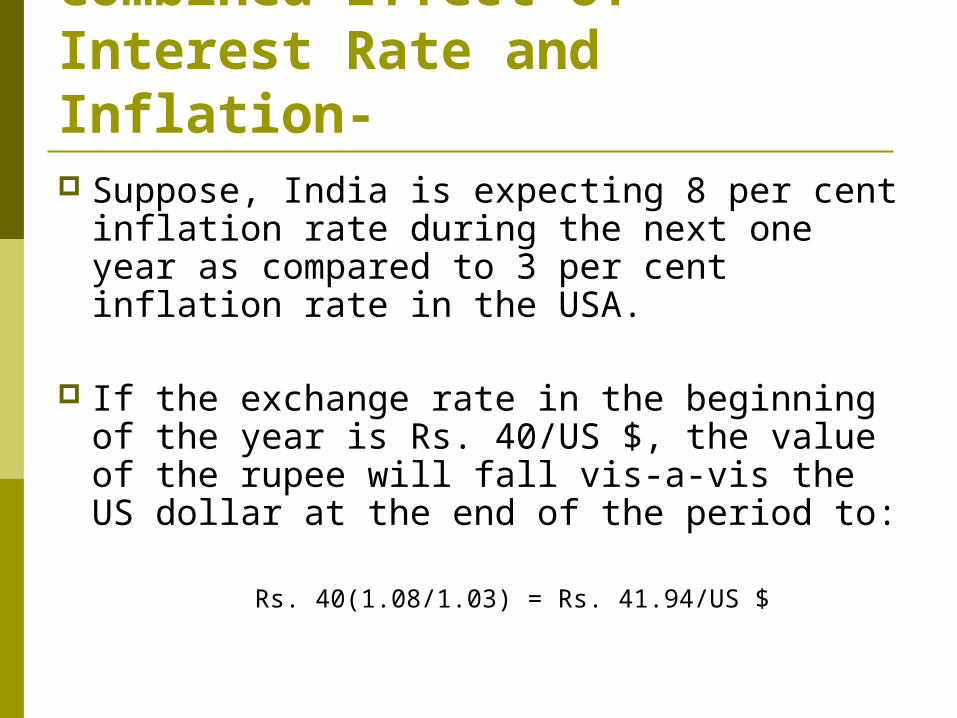

Combined Effect of Interest Rate and Inflation- Suppose, India is expecting 8 per cent

inflation rate during the next one year as compared to 3 per cent inflation rate in the USA.

If the exchange rate in the beginning of the year is Rs. 40/US $, the value of the rupee will fall vis-a-vis the US dollar at the end of the period to:

Rs. 40(1.08/1.03) = Rs. 41.94/US $

Combined Effect of Interest Rate and Inflation- Suppose further that at the beginning of the period, interest

rate in India is 7 per cent as against 4 per cent in the USA. At the end of the period, interest rate in India will rise to an

extent that will equate approximately the inflation rate differential.

In order to find out the change in interest rate, the following equation may be applied:

et/eo = (1 + rIND)l(1 + rUsA) Basing on the above equation, we have

41.94/40 = (1 + rIND)/1.04

Or 1 + rIND = 1.09 Or rIND = 0.09 or 9%

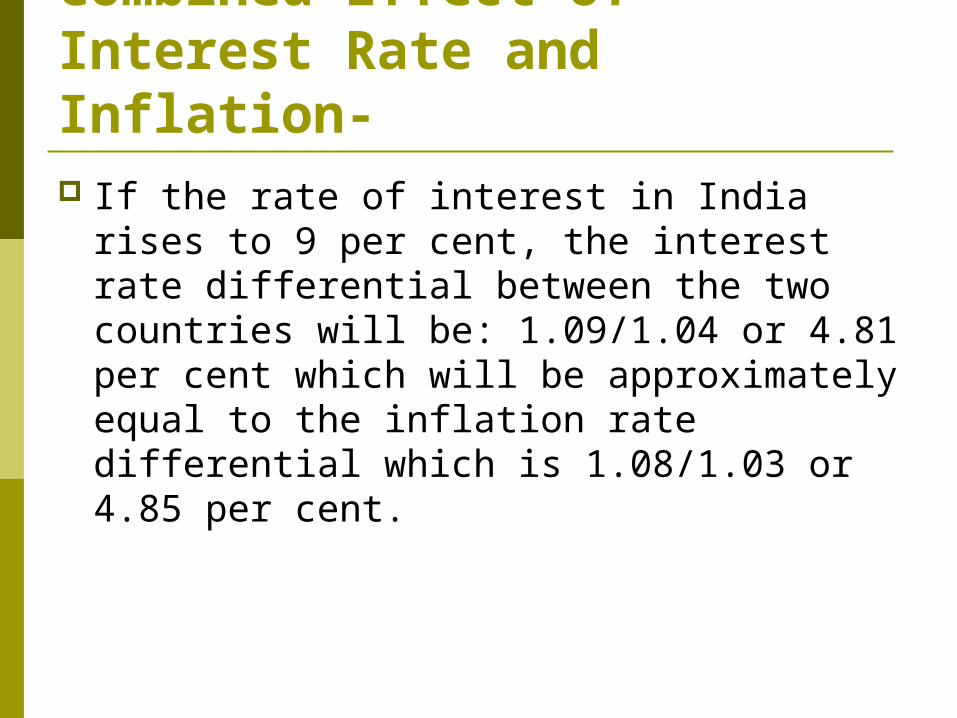

Combined Effect of Interest Rate and Inflation- If the rate of interest in India rises to 9 per

cent, the interest rate differential between the two countries will be: 1.09/1.04 or 4.81 per cent which will be approximately equal to the inflation rate differential which is 1.08/1.03 or 4.85 per cent.

International Fisher Effect (IFE)

According to the Fisher effect, nominal risk-free interest rates contain a real rate of return and anticipated inflation.

If all investors require the same real return, differentials in interest rates may be due to differentials in expected inflation.

International Fisher Effect (IFE)

The international Fisher effect (IFE) theory suggests that currencies with higher interest rates will depreciate because the higher nominal rates reflect higher expected inflation.

Investors hoping to capitalize on a higher foreign interest rate should earn a return no higher than what they would have earned domestically.

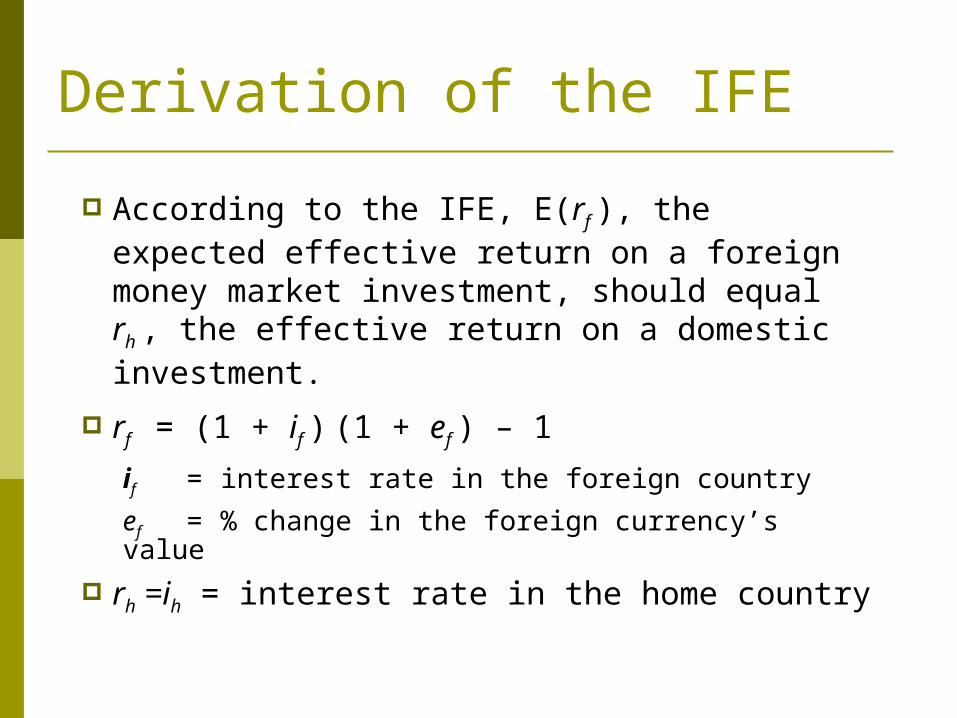

According to the IFE, E(rf ), the expected effective return on a foreign money market investment, should equal rh , the effective return on a domestic investment.

rf = (1 + if ) (1 + ef ) – 1

if = interest rate in the foreign country

ef = % change in the foreign currency’s value

rh =ih = interest rate in the home country

Derivation of the IFE

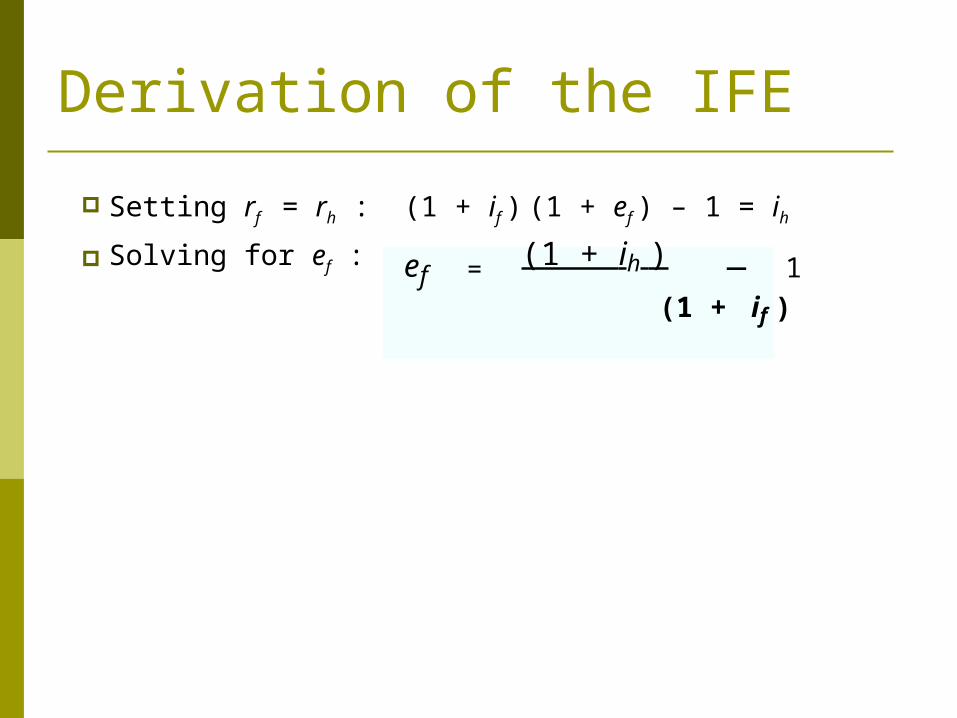

Setting rf = rh : (1 + if ) (1 + ef ) – 1 = ih

Solving for ef : ef = (1 + ih ) _ 1

(1 + if )

Derivation of the IFE

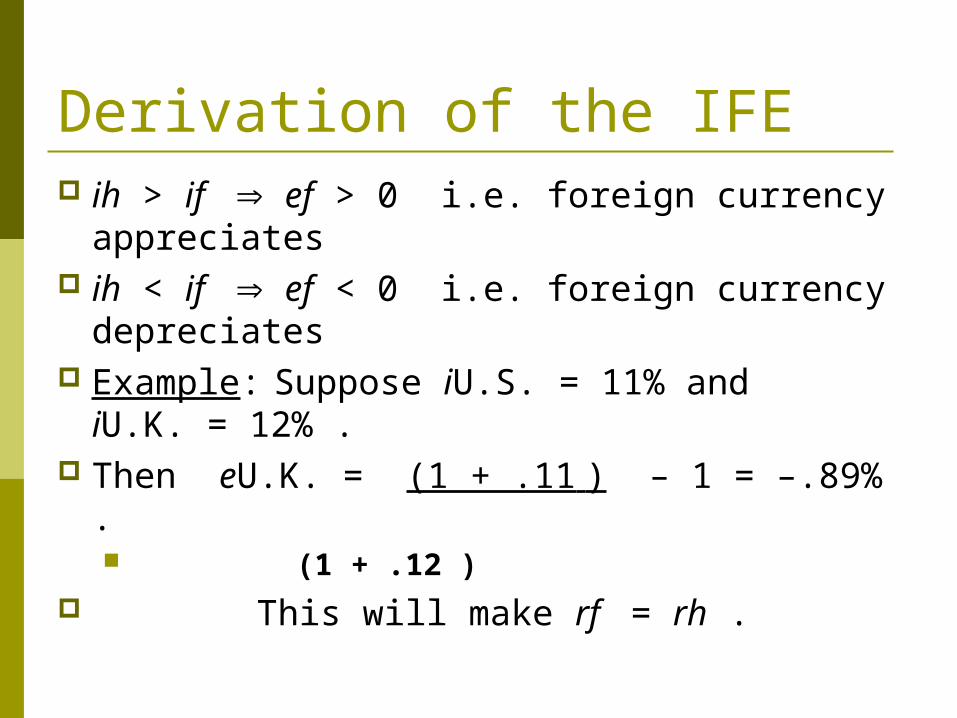

Derivation of the IFE ih > if ef > 0 i.e. foreign currency

appreciates ih < if ef < 0 i.e. foreign currency

depreciates Example: Suppose iU.S. = 11% and

iU.K. = 12% . Then eU.K. = (1 + .11 ) – 1 = –.89% .

(1 + .12 ) This will make rf = rh .

When the interest rate differential is small, the IFE relationship can be simplified as ef ih _ if

Derivation of the IFE

If the British rate on 6-month deposits were 2% above the U.S. interest rate, the £ should depreciate by approximately 2% over 6 months. Then U.S. investors would earn about the same return on British deposits as they would on U.S. deposits.

International Fisher Effect - IFE

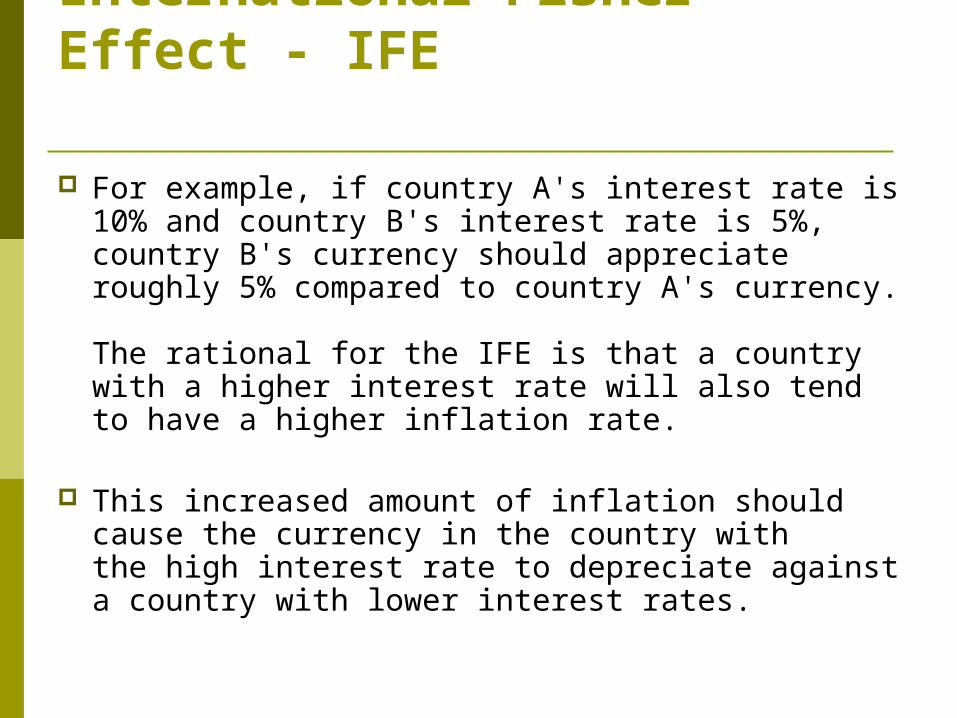

For example, if country A's interest rate is 10% and country B's interest rate is 5%, country B's currency should appreciate roughly 5% compared to country A's currency.

The rational for the IFE is that a country with a higher interest rate will also tend to have a higher inflation rate.

This increased amount of inflation should cause the currency in the country with the high interest rate to depreciate against a country with lower interest rates.

Tests of the IFE

If actual interest rates and exchange rate changes are plotted over time on a graph, we can see whether the points are evenly scattered on both sides of the IFE line.

Empirical studies indicate that the IFE theory holds during some time frames. However, there is also evidence that it does not hold consistently.

Why the IFE Does Not Occur Since the IFE is based on PPP, it will not

hold when PPP does not hold. In particular, if there are factors other than

inflation that affect exchange rates, exchange rates may not adjust in accordance with the inflation differential.

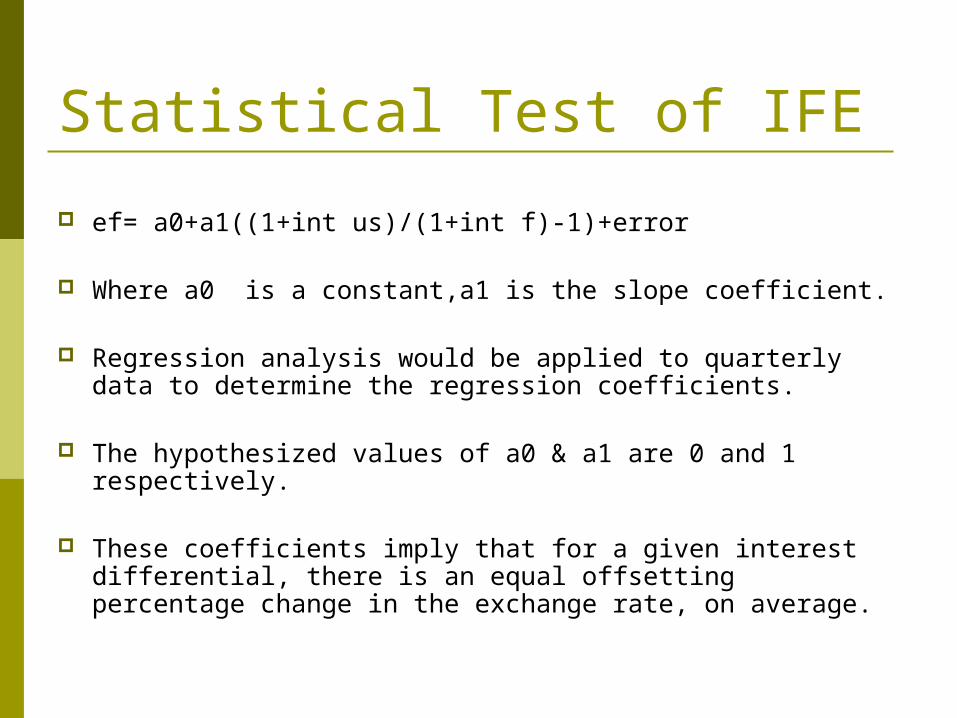

International Fisher EffectStatistical Test of the IFE. A somewhat simplified statistical test of the IFE can be developed by applying regression analysis to historical exchange rates and the nominal interest rate differential.

Statistical Test of IFE

ef= a0+a1((1+int us)/(1+int f)-1)+error

Where a0 is a constant,a1 is the slope coefficient.

Regression analysis would be applied to quarterly data to determine the regression coefficients.

The hypothesized values of a0 & a1 are 0 and 1 respectively.

These coefficients imply that for a given interest differential, there is an equal offsetting percentage change in the exchange rate, on average.

Statistical Test of IFE The appropriate t test for each regression

coefficient requires a comparison to the hypothesizes value and division by the standard error (s.e) of the coefficient as follows:

Test for a0: t=(a0-0)/s.e. of a0 Test for a1: t=(a1-1)/s.e. of a1

Statistical Test of IFE

The t-table is then used to find the critical t- value.

If either t-test finds that the coefficients differ significantly from what was hypothesized, the IFE is refuted

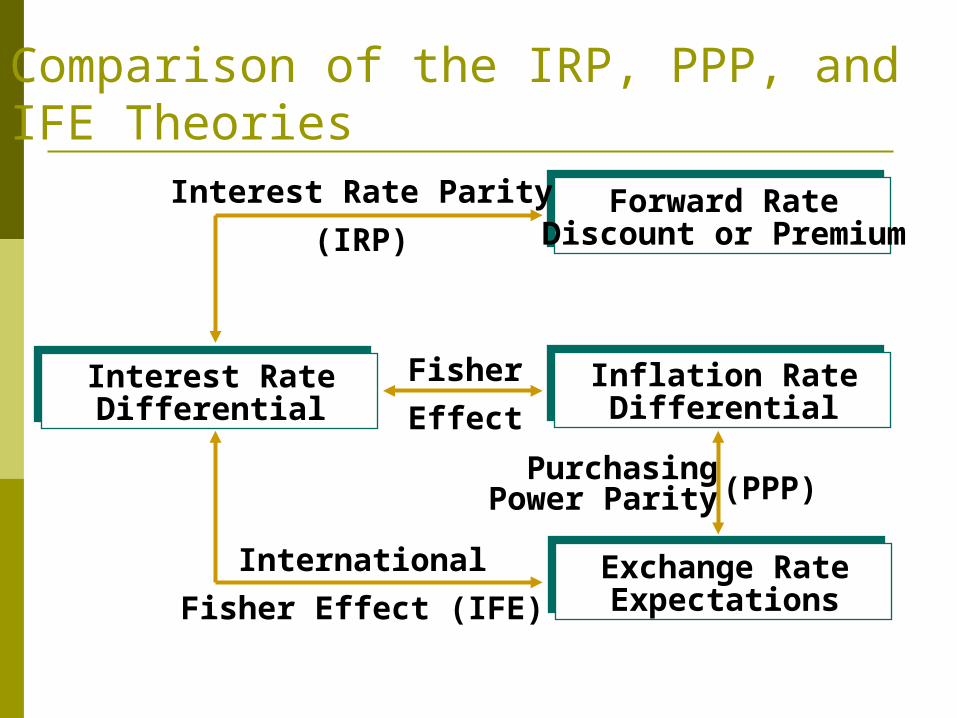

Comparison of the IRP, PPP, and IFE Theories

Exchange RateExpectations

Inflation RateDifferential

Forward RateDiscount or Premium

Interest RateDifferential

PurchasingPower Parity (PPP)

Interest Rate Parity

(IRP)

Fisher

Effect

International

Fisher Effect (IFE)

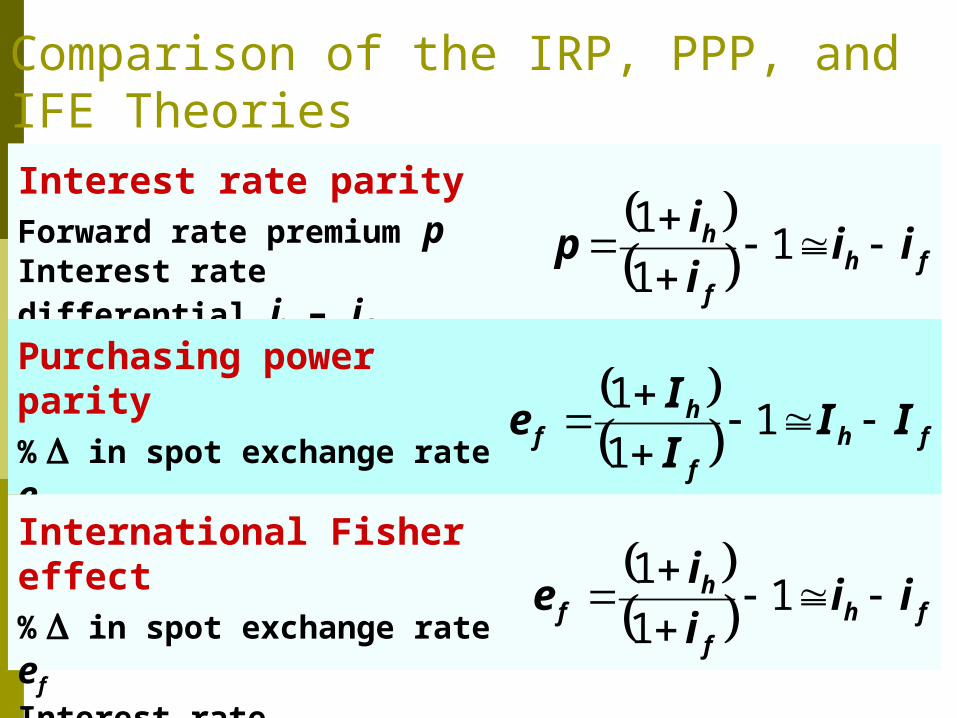

Comparison of the IRP, PPP, and IFE TheoriesInterest rate parityForward rate premium pInterest rate differential ih – if

fh

f

h iii

ip

11

1

Purchasing power parity% in spot exchange rate efInflation rate differential Ih – If

fh

f

hf II

I

Ie

11

1

International Fisher effect% in spot exchange rate efInterest rate differential ih – if

fh

f

hf ii

i

ie

11

1

Comparison of PPP, IFE and IRP Theories

Theory Key Variables of Theory Summary of Theory

Interest rate party (IRP)

Forward rate premium (or discount)

Interest differential The forward rate of one currency with respect to another will contain a premium (or discount) that is determined by the differential in interest rates between the two countries. As a result, covered interest arbitrage will provide a return that is no higher than a domestic return.

Purchasing Power Parity (PPP)

Percentage change in spot exchange rate

Inflation rate differential

The spot rate of one currency with respect to another will change in reaction to the differential in inflation rates between the two countries. Consequently, the purchasing power for consumers when purchasing goods in their own country will be similar to their purchasing power when importing goods from the foreign country.

International Fisher Effect (IFE)

Percentage change in spot exchange rate

Interest rate differential

The spot rate of one currency with respect to another will change in accordance with the differential in interest rates between the two countries. Consequently, the return on uncovered foreign money market securities will, on an average, be no higher than the return on domestic money market securities from the perspective of investors in the home country.