148

EXIM DOCUMENTATION & PROCEDURE By Eknath Birari

| Date post: | 21-Nov-2014 |

| Category: |

Documents |

| Upload: | nitesh-agarwal |

| View: | 520 times |

| Download: | 1 times |

EXIM DOCUMENTATION & PROCEDURE

By Eknath Birari

Agenda

q How to set up Export Companiesq Export Sales Contract q Terms of Shipments [INCOTERMS]q Processing of Export Orderq Documentation: Overview q Understanding Documents – Proforma Invoice,

Commercial Invoice, Packing List, Inspection Certificate, Certificate of Origin, GSP Certificate, Shipping Bill, ARE-1, Mate Receipt, GR/SDF, Marine Insurance Policy, ECGC Policy, Bill of Exchange, Bank Realisation Certificate, Bill of Lading and Airway Bill, Special Consular Invoice, etc.

q Pre-shipment Inspection

How to set up Export Companies

Preliminaries for starting export Business

q Setting up of an appropriate form of business organisation - What should be the form of business organisation?

q Choosing appropriate mode of operation – How one wants to enter into the business?

q How to select name, design stationary including catalogue?

qWhen and where to open a Bank Account?

Preliminaries for starting export Business

q How to obtain mandatory registration? a.PANb.IECc.Registration for Digital Signatured.RCMCe.Registration with various agencies

q How to quickly respond to overseas enquiries and how to project image?

q Electronic Data Interchange (EDI)

Setting up of an appropriate form of business organisation

q What should be the form of business organisation?

§ Main types of business organisations prevailing in India are: • Sole proprietorship, • Partnership firm, • Private limited company, • Public limited company, • Co-operative society, • Trust, etc.

Choosing appropriate mode of operation

qHow one wants to enter into the business?Export business is mainly classified in three broad categories:

• Merchant exporters, • Manufacturer exporters and • Service exporters.

How to select name, design stationery including catalogue?

q Selection of Name: § SIMPLE § It may signify PRODUCT/ACTIVITY/ SPECIALITY

q Designing of Stationery [Letterheads, envelopes, visiting cards etc.]§ Same colour combinations§ Logo § Quality§ Size§ Appearance

How to select name, design stationery including catalogue?

q Preparing of Product Catalogue/Literature/CD§ Colour combination§ Avoid over crowded literature§ Gives information about products/services offered § Technical details, if necessary

q Creating Website (Online Home Page) § Vision of the company§ List of Products/services. In case of products, display clips of

the same.§ List of Group Companies, branches etc.

Preliminary Registrations

q When and where to open a Bank Account? An exporter/importer should have a current account with an bank having a foreign exchange department [Authorised Dealer].

q How to obtain mandatory registrations?a. Permanent Account Number (PAN):

Exporter should make an application to the Income – Tax Authorities to allot a Permanent Account Number (PAN).

b. Importer-Exporter Code Number (IEC):• FTP lays down IEC number as basic eligibility criteria to

become Exporter/Importer. • It is allotted by Regional Authority i.e. Joint Director

General of Foreign Trade.

Importer-Exporter Code

§ An application for grant of IEC number shall be made by Registered/ Head Office of applicant, except EOUs and SEZ units to concerned RA in ANF 2A with documents prescribed therein.

§ As per Policy Circular No. 15/2006 Dtd. 27.07.2006 an applicant (exporter/importer) may now choose one of the two options for application submission:

• File an online application and submit a physical copy of the application by taking a printout of the online application.

• Submit a physical copy of the application directly at the regional DGFT office.

Importer-Exporter Code

q Check sheet for application for issue of IEC no. § Application in ANF 2A § Declarations in Part D of Aayaat Niryaat Form in duplicate on

letterhead.§ One copy of the application must be submitted.§ Each individual page of the application has to be signed by the

applicant.§ Demand Draft of Rs.1000 evidencing payment of application fee

in favour of the concerned regional office of DGFT. Money can also be paid through Electronic Fund Transfer (EFT) and TR 6A challan by cash.

§ Certificate from the Banker of the applicant firm in the specified format as given in Part B (Appendix 18 A) of ANF 2A

Importer-Exporter Code

q Check sheet for application for issue of IEC no. § Self certified copy of Permanent Account Number (PAN) issued

by Income Tax Authorities.§ Two copies of passport size photographs of the applicant.§ Photograph on the banker’s certificate should be attested by

the banker of the applicant.§ Self addressed envelope and stamp of Rs.30.§ Envelope mentioning name and address of the Bank with stamp

of Rs.30.§ Self certified copy of Partnership Deed/ Memorandum and

Article of association, if any.§ Self certified copy of RBI approval in cases where non resident

interest/holding in the firm/company exists with repatriation benefits.

§ EXPORTER’S / IMPORTER’S PROFILE• Each importer/exporter is required to file

importer/exporter profile once with the Regional Authority in ‘ANF 1’ (Aayaat Niryaat Form).

• RA shall enter the information in database so as to dispense with the need for asking the repetitive information.

§ IDENTITY CARDS• To facilitate collection of Authorisation and other

documents from DGFT Head Quarters and RA, identity cards (as in Appendix 20B, valid for 3 years) are issued by the concerned Regional Authorities to the proprietor/ partners/ directors and the authorised employees (not more than three), of the importers and exporters, upon application as in Appendix 20A of HBP Vol. I.

Registration for Digital Signature

§ A Digital Signature is the electronic equivalent of a physical signature and can be used to electronically sign any document or transaction. One needs to have a valid digital certificate tocreate a digital signature.

§ DGFT has authorised various agencies to issue a Digital Signature Certificate with a validity of one or two years. [SafeExim, Tech Options, etc.]

§ With a Digital Signature one can apply for licenses electronically with the DGFT and digitally sign his online license application.

Registration for Digital Signature

§ Digital Signatures are legally admissible in a Court of Law, as provided under the provisions of it.

§ W.e.f. 01.04.2004, no on-line application is possible if an IEC holder does not opt for a digital signature. Application fee is also to be paid through the Electronic Fund Transfer. Moreover, 50% reduction in application fees is granted to only those who are using both Digital Signatures as well as EFT route.

Registration-Cum-Membership Certificate (RCMC)§ RCMC means the certificate of registration and membership

granted by an Export Promotion Council/ Commodity Board/ Development Authority or other competent authority as prescribed in the Foreign Trade Policy or Handbook (Vol.1).

§ An exporter desiring to obtain a Registration-cum-Membership Certificate shall declare his main line of business in the application, which shall be made to the Export Promotion Council (EPC) relating to that line of business.

§ However, a status holder has the option to obtain RCMC from Federation of Indian Exporters Organization (FIEO). The service exporters (except software service exporters) shall be required to obtain RCMC from FIEO.

List of few EPCs/Commodity Boards

q Agricultural and Processed Food Products Export Development Authority (APEDA)

q Basic Chemicals, Pharmaceuticals & Cosmetics Export Promotion Council

q Chemicals and Allied Products Export Promotion Council (CAPEXIL)

q Coffee Board

q Coir Board

q Electronics and Computer Software Export Promotion Council (ESC)

q Engineering Export Promotion Council

q Export Promotion Council for EOUs and SEZ Units

q Federation of Indian Export Organisations (FIEO)

List of few EPCs/Commodity Boards

q The Gem & Jewellery Export Promotion Council

q Export Promotion Council for Handicrafts

q The Handloom Export Promotion Council

q The Indian Silk Export Promotion Council

q Pharmaceutical Export Promotion Council

q The Rubber Board

q Spices Board

q Tea Board

q Tobacco Board

q Wool & Woollens Export Promotion Council

Registration with various Agencies

i. Registration for legal identity :-Exporter has to get his organization registered under respective acts/authorities such as:-• A sole proprietor - The Shops and Establishments Act or

take permission from local authorities, such as Municipal Corporation, if required.

• A partnership firm - Indian Partnership Act, 1932.• A Joint stock company - Indian Companies Act, 1956• A Co-operative Society - The Co-operative Societies Act,

1912.• A Trust - Indian Trust Act, 1882

ii. Registration for manufacturing activities a. Small Scale Industryb. Industrial Licensingc. Tiny Sector/Enterprisesd. Khadi Village Industries Commission

Registration with various Agencies

iii. Registration with Central Excise Authorities:-Goods meant for exports are exempt from Central Excise duty. To avail exemption from payment of excise duty on export goods, exporter has to obtain C.ExciseRegistration. There are two options to avail such benefit:a. Export under Rebate claim - Exporter has to pay excise duty at the time of clearance and on exportation can claim rebate of excise duty paid.b. Export under Bond - In this case goods are cleared under Bond and there is no need of payment of excise duty.

Registration with various Agencies

iv. Registration with the Customs Authorities (BIN)§ Exporters have to obtain PAN based Business

Identification Number (BIN) from the DGFT prior to filing of shipping bill for clearance of export goods.

§ Under the EDI System, PAN based BIN is received by the Customs System from the DGFT online.

v. Registration with VAT AuthoritiesGoods which are to be shipped out of the country for export are eligible for exemption from both VAT and Central Sales Tax for this registration with VAT Authorities is required.

Registration with various Agencies

vi. Registration with Service Tax Authorities§ Service tax is an indirect tax levied under the Finance Act,

1994.§ At present, there are approximately 96 categories of

services taxable under the service tax net. § Service Tax is levied at a uniform rate of 12% + 2%

Education Cess + 1% Secondary and Higher Education Cesson services liable to service tax under Finance Bill 2007.

Registration with various Agencies

vi. How to quickly respond to overseas enquiries and how to project image?• Strategy in Export and Import Correspondence• When to reply• Means of reply

vii. Electronic Data Interchange (EDI)• EDI is the modern mode of transfer of documents. • It is direct electronic transmission, computer to

computer of standard business forms such as purchase order, advance, shipping notices, invoices and the like between two organizations.

Contd…….

• The five key elements of EDI are 1. Electronic Transmission, 2. Standards Business Documents, 3. Predefined format, 4. Business application and 5. Trading partner.

• It increases the profits by lowering the cost of the business process and increases the marketing share by providing an improved service to customers.

• The Indian Government has also fallen in line with the requirements of International Trade and has introduced computerized processing of documents in various matters relating to international trade.

Contd…….

• EDI applications can help with their wide range of business application systems for different industries, which include:

» Application for trade permits from government agencies.

» Bidding for export quotas from regulatory bodies.» Filing of corporate returns with relevant

authorities.» Submission of claims to insurance companies.» Bill payment and collection with banks and

financial institutions.» Order placement and invoicing with trading

partners.

Export Sales Contract

Export Sales Contract

qWhat is Export Sales Contract?§ Agreement between buyer and seller, stipulating

each and every details of the transaction.

§ Legally binding document.

§ It reduces the probabilities of disputes & differences as it fixes the role and responsibilities of each party.

Export Sales Contract

q Terms and Conditions:§ While drafting the sales contract one must ensure the

following:-1. Coverage is complete.2. Maximum clarity.3. Future probability to be provided.4. Trade practices.5. Law of both countries6. Need of both parties.

§ There should not be any ambiguity regarding the exact specifications of goods and terms of sale including export price, mode of payment, storage and distribution methods, type of packaging, port of shipment, delivery schedule etc.

Export Sales Contract

§ Following standard terms and conditions are covered in an Export Sales contract: -

• Name & address of both the parties.• Contract Number & Date, place• Description of goods, quantity and quantity• Product Standards and Technical Specifications of goods.• Inspection/certification• Total Value of Contract• Terms of delivery (F.O.B./C.F.R./C.I.F. etc.), • Period of Delivery/Shipment, part shipment, Trans-

shipment.• Terms of payment:- L/C, D/A, D/P, advance payment,

Amount/Mode & Currency

Contd…..

Export Sales Contract

• Taxes, Duties and charges • Packing, Labeling, Marking, etc.• Brokerage/commissions and discounts• Licences and Permits • Insurance Requirements, Certificates of Insurance• Documentary Requirements• Performance guarantee• Signature by all parties to the contract.• Force Majeure of Excuse for Non-performance of contract• Remedies • Arbitration.

§ Standard Export Sales Contract forms are also available. These can be used as it is or with some modification as per individualneed.

Terms of Shipment [INCOTERMS]

INCOTERMS 2000

q INTRODUCTION

In their sales contract buyer and seller agree on the conditions of sale : payment on the one hand and delivery on the other. These terms determine at what precise location the ownership of the goods is transferred from seller to buyer and when/how payment will be done. In international trade a universal set of rules on delivery has been developed over the years. It is called INCOTEMRS.

q

Incoterms 2000

Group E Departure

EXW Ex Works

Group F Main carriage unpaid

FCAFASFOB

Free Carrier Free alongside shipFree on board

Group C Main carriage paid

CFRCIFCPTCIP

Cost and FreightCost, Insurance, FreightCarriage Paid toCarriage and Insurance Paid to

Group DArrival

DAFDESDEQDDUDDP

Delivered at FrontierDelivered Ex ShipDelivered Ex QuayDelivered Duty UnpaidDelivered Duty Paid

(Note, that when the Incoterms indicate a certain Point or “…..,” the point of destination or origin must be mentioned)

INCOTERMS 2000

q The Incoterms divide costs and risksThe Incoterms of trade have been designed to clarify obligations of both parties, the buyer and the seller. Principally, these are:

The seller must: The buyer must:Provide the goods according to the contract

Pay the price as agreed upon

Contd….

INCOTERMS 2000

In order to finalise the transaction, both parties will have to perform certain tasks, like:

Arrange for licences, Arrange for licences,

Authorisation and formalities Authorisation and formalities

Arrange for shipment Arrange for shipment

Arrange for delivery Accept delivery

Bear the risks for his activities Bear the risks involved in his contractual activities.

Source: Guide to Incoterms, ICC Paris

INCOTERMS 2000q EXW = EX WORKS (… named place)

Cost of Goods plus cost of Export packing and markingIn this term the seller delivers the goods by keeping it ready in deliverable state at the seller's place or another named place. This named place can be factory/godown or manufacturing unit. In this term seller does not clear the goods for exports nor goods are loaded on vehicle.

q FCA = FREE CARRIER (… named place) Cost of Goods plus cost of Getting goods to railway station or truck for transportation to portThis term refers to seller's responsibility to deliver the goods, cleared for export, to the carrier appointed by the buyer at the named place. In this term the place of delivery is very important. If the delivery is at sellers place's then he is responsible for loading. If the delivery occurred at any other place, the seller is not responsible for unloading. This term can be used for all modes of transport as well as multimodal.

INCOTERMS 2000

q FAS = FREE ALONGSIDE SHIP (…named port of shipment)Cost of Goods plus cost of Transport to port and getting goods alongside shipIn this term when the goods are placed alongside the vessel at the named port of shipment it will be considered that the seller has completed the delivery. The buyer has to bear all risks of loss or damage to the goods and all costs from this point of time. However the seller must clear the goods for the purpose of export. This term can be used only for inland waterway transport or shipment by sea. It is not used when it is air shipment.

INCOTERMS 2000

q FOB = FREE ON BOARD (… named port of shipment)Cost of Goods plus cost of Getting goods on board and preparing shipping documentsThis is the most popular term and is widely in use. FOB means that the seller delivers when the goods pass the ship's rail at the named port of shipment. Under this term the buyer has to bear all costs and risk of loss of damage to the goods from that point. This term requires the seller to clear the goods for exports. This term is used only for sea or inland waterway transport. It is not suitable for shipment by air.

INCOTERMS 2000

q CFR = COST AND FREIGHT (… named port of destination)Cost of Goods plus cost of Freight cost (port to port)Earlier this term was popularly known as C&F or CNF. CFR means the seller must pay the cost and the freight necessary for the goods to reach at the named destination. However, the risks of loss or damage to the goods after the time of the delivery is on buyers account. The seller is required to clear the goods for exports. This term can be used only for sea and inland waterway transport.

INCOTERMS 2000q CIF = COST INSURANCE AND FREIGHT (… named port of

destination)Cost of Goods plus cost of Marine Insurance“Cost, Insurance and Freight” means that the seller, delivers when the goods pass the ship’s rail in the port of shipment. The CIF price refers that it covers the cost of the goods, freight necessary to bring the goods to the named port of destination and also marine insurance. Compared to the previous term, CFR the seller contracts for the insurance and pay the insurance premium. It will be essential for the buyer to know that under the CIF term the seller is required to obtain the insurance only on minimum cover. If the buyer wishes to have more protection then he should make his own insurance arrangement extra or should specify to the seller at the time ofcontract.In this term the seller must clear the goods for exports and the buyer must arrange necessary clearance for import. This term can be used only for sea and inland water transport.

INCOTERMS 2000

q CPT = CARRIAGE PAID TO (… named place destination)“Carriage Paid To” means the seller delivers the goods to the carrier nominated by him but the seller must in addition pay the cost ofcarriage necessary to bring the goods to the named destination. This refers to the fact that all the risks and any other cost occurring after the goods have been delivered will be on buyer’s account. This term is used for all modes of transport including multimodal transport.

q CIP = CARRIAGE AND INSURANCE PAID TO (…named place of destination)“Carriage and Insurance Paid To” means that the seller delivers the goods to the carrier nominated by him, but the seller must in addition pay the cost of carriage necessary to bring the goods to the named destination. This means that the buyer bears all risks and any additional costs occurring after the goods have been so delivered. However, in CIP the seller also has to procure insurance against the buyer's risk of loss of or damage to the goods during the carriage.

INCOTERMS 2000

q DAF = DELIVERD AT FRONTIER (… named place)This term is used when goods are to be delivered at land frontier, irrespective of the mode of transport. "Delivered At Frontier" means the seller delivers when the goods are placed at the disposal of the buyer on the arriving means of transport not unloaded, cleared for exports but not cleared for import at the named point and place at the frontier, but before the customs border of the adjoining country.

q DES = DELIVERD EX SHIPCost of Goods plus cost of Putting goods at disposal of customer on board vessel at port of destination“Delivered Ex Ship” means that the seller delivers when goods are place at the disposal of the buyer on board ship not cleared for import at the named port of destination. In this term all the cost and risk in bringing the goods to the named port of destination before discharge is on seller. This term can be used only when the shipment is by sea or inland waterway or multimodal transport in the vessel at the port of destination.

INCOTERMS 2000

q DEQ = DELIVERED EX QUAY (… named port of destination)Cost of Goods plus cost of Unloading charges at port of destination “Delivered Ex Quay” means that the seller delivers when the goods are placed at the disposal of the buyer not cleared for, import on the quay (wharf) at the named port of destination. The seller has to bear costs and risks involved in bringing the goods to the named port of destination and discharging the goods on the quay (wharf). The DEQ term requires the buyer to clear the goods for import and to pay for all formalities, duties, taxes and other charges upon import.

INCOTERMS 2000

q DDU = DELIVERED DUTY UNPAID“Delivered Duty Unpaid” means that the seller delivers the goods to the buyer, not cleared for import, and not unloaded from any arriving means of transport at the named place of destination. The seller has to bear the costs and risks involved in bringing the goods thereto other than where applicable any duty for import in the country of destination. Such duty has to be borne by the buyer as well as any costs and risks caused by his failure to clear the goods for import in time.

INCOTERMS 2000

q DDP = DELIVERED DUTY PAID (…named place of destination)Cost of Goods plus cost of Payment of duties and transport to customer“Delivered Duty Paid" means that the seller delivers the goods to the buyer, cleared for import, and not unloaded from any arriving means of transport at the named place of destination. The seller has to bear all the costs and risks involved in bringing the goods thereto including, where applicable, any duty for import in the country of destination.

INCOTERMS 2000-Chart of Responsibility

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

?

INCOTERMS 2000

q Incoterms 2000 – an exampleA customer in Hanover, Germany, asks for a quotation for 3000 pairs of shoes, to be delivered DDP at his warehouse. You have decided on a unit selling price of $2, giving a total nominal price of $ 6000 for the goods when sold domestically. For export you will have to calculate with an additional set of costs which are involved in making them physically available to your customer.

What are the additional costs of getting the goods from your factory in (e.g.) Agra, India, to the customer? How (*) is your quotation affected by the terms of delivery?

(*) In this calculation example, all costs are hypothetical.

INCOTERMS 2000

q Incoterms 2000 – an example

If you quote:

Your price should include:

Additional costs:

Your total price is:

EXW Ex-works AgraExport packing, marking crates with shipping marks

300 6300

FCA Free on Carrier at Agra station. Carriage and insurance for delivery to railway station by road transport including insurance

100 6400

INCOTERMS 2000

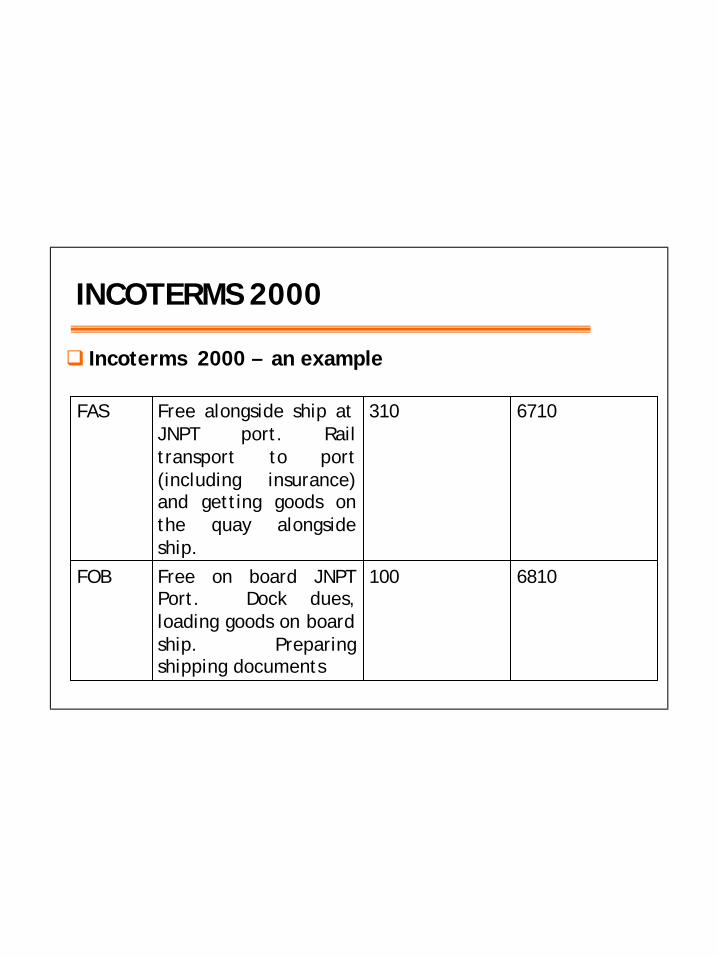

q Incoterms 2000 – an example

FAS Free alongside ship at JNPT port. Rail transport to port (including insurance) and getting goods on the quay alongside ship.

310 6710

FOB Free on board JNPT Port. Dock dues, loading goods on board ship. Preparing shipping documents

100 6810

INCOTERMS 2000

q Incoterms 2000 – an example

CFR Cost and Freight.Sea Freight to Hamburg (nearest port to Hanover)

875 7685

CIF Cost, insurance, freight. Sea freight + marine insurance (port to port)

100 7785

DES Delivered ex ship at Hamburg. Landing charges at Hamburg port.

90 7875

INCOTERMS 2000

q Incoterms 2000 – an example

DDP Delivery duty Paid at customer’s warehouse in Hanover. Import duties for 3000 pairs of shoes

1200 9075

Transport by rail Hamburg to Hanover

150 9225

The buyer actually pays **

1350 9225

(**) = ‘availability price’.

Processing of an Export Order

Processing of an export order

Pre-shipmentStage

Preliminary Stage

Shipment Stage

Post-shipmentStage

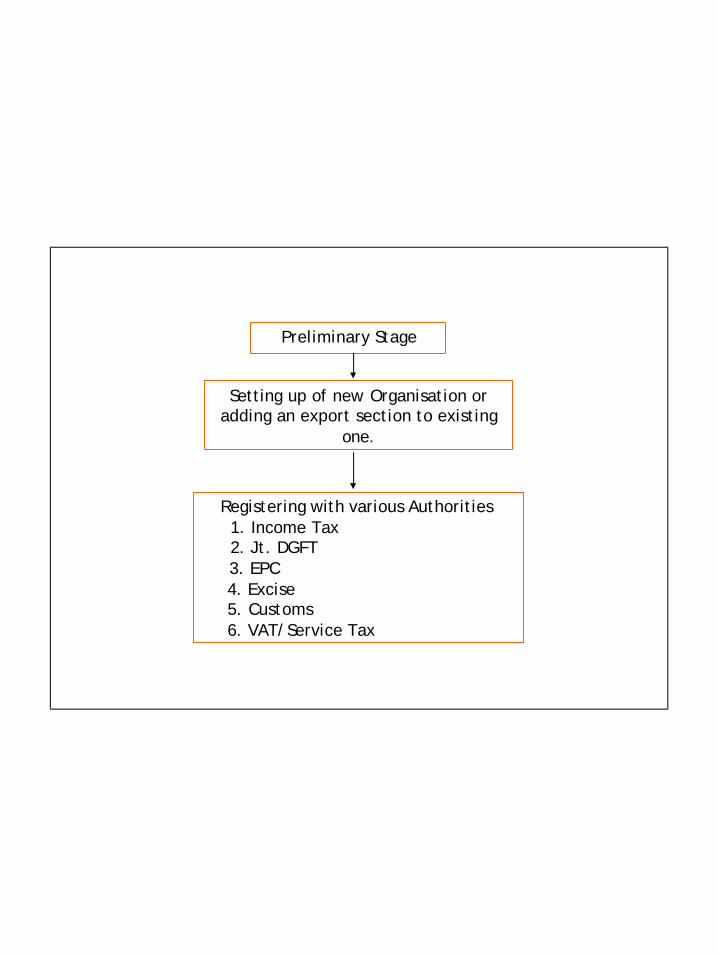

Preliminary Stage

Setting up of new Organisation or adding an export section to existing

one.

Registering with various Authorities1. Income Tax 2. Jt. DGFT 3. EPC 4. Excise 5. Customs 6. VAT/Service Tax

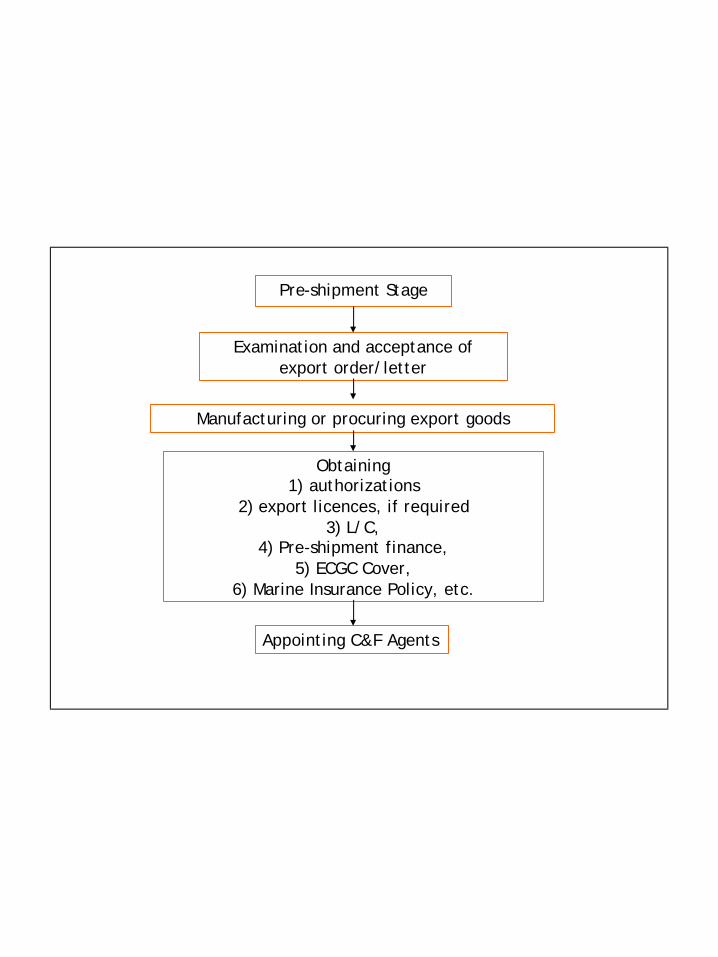

Pre-shipment Stage

Examination and acceptance of export order/letter

Obtaining 1) authorizations

2) export licences, if required3) L/C,

4) Pre-shipment finance, 5) ECGC Cover,

6) Marine Insurance Policy, etc.

Manufacturing or procuring export goods

Appointing C&F Agents

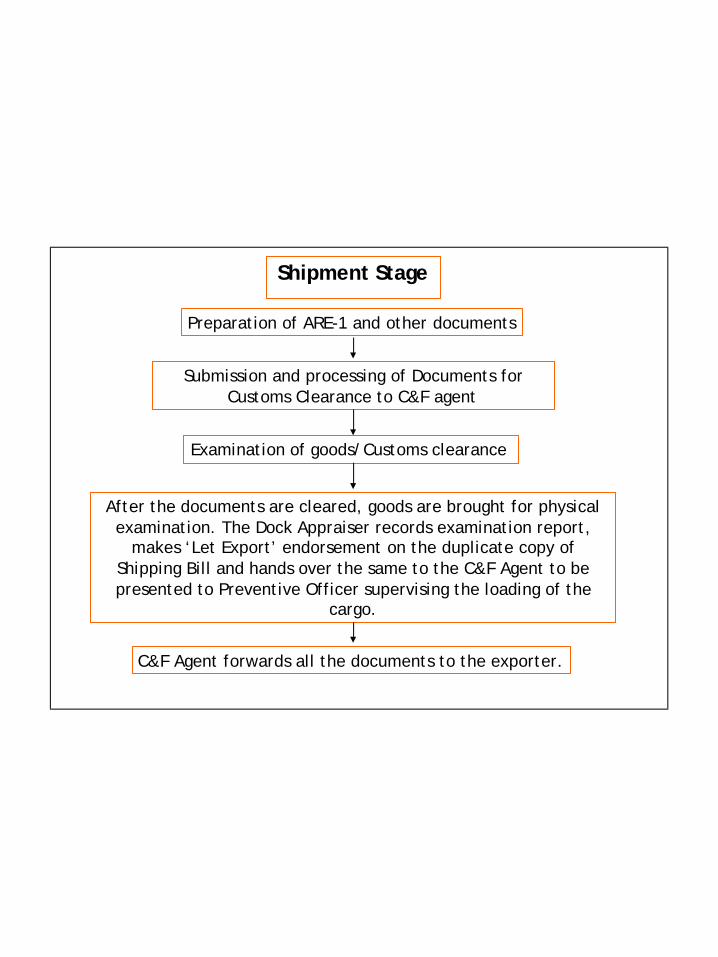

Shipment Stage

Submission and processing of Documents for Customs Clearance to C&F agent

Examination of goods/Customs clearance

After the documents are cleared, goods are brought for physical examination. The Dock Appraiser records examination report,

makes ‘Let Export’ endorsement on the duplicate copy of Shipping Bill and hands over the same to the C&F Agent to be presented to Preventive Officer supervising the loading of the

cargo.

C&F Agent forwards all the documents to the exporter.

Preparation of ARE-1 and other documents

Post-shipment

Shipment Advice is sent to Importer.

Export Documents are presented to Bank for negotiation.

Export documents are scrutinized, and if found in order are negotiated or sent for collection. Exporter receives payment

through Banking channel and upon realisation Bank issues Bank Realisation Certificate to Exporter.

Exporter claims rebate of central excise duty or submits proof of export if goods are cleared under bond

Exporter initiates action for claiming export benefits.

Overview of Documentation

Significance of Documentation

q Documents are important for the following reasons:

(a) as an evidence of shipment and title of goods;

(b) for obtaining payment;

(c) to provide a specific and complete description of the goods;

(d) for assessment of correct Duty for clearance purpose;

(e) for obtaining Export Licences;

(f) for obtaining export finance;

(g) for completing Pre-shipment Inspection;

(h) for claiming export benefits like Duty Drawback, etc.

Commercial / Regulatory Documentsq Commercial set of documents are mainly used for

Commerce. In other words these are documents normally exchanged between buyer and seller.

q Regulatory documents are required in dealing with various regulatory authorities such as customs, RBI, Excise, Licencing authorities Inspection and other Export Promotion bodies for availing incentives etc.

Commercial / Regulatory Documentsq Documents are categorized into two categories, namely

Commercial Documents and Regulatory Documents.

Commercial RegulatoryCommercial Invoice Shipping Bill

Inspection Certificate ARE1 from (Excise)

Insurance Certificate RBI Declaration Forms (GR/PP)Bill of Lading / AWB Application for remittance of

currencyCertificate of Origin Various LicencesBill of Exchange Bill of EntryShipment Advice

Packing List

Commercial / Regulatory Documents

q Referring to the Commercial set of documents, it may please be observed that these set of documents are prepared from other set of documents (some of these only). These are known as auxiliary documents.

q These documents may not be required by the foreign buyer, but these are must for preparation of main export documents, known as Principle Commercial Documents.

Commercial Documents

8. Letter to Bank for negotiation of documents

8. Bill of Exchange

7. Shipping Instructions7. Packing List

6. Shipping order6. Shipment Advice5. Mate Receipt5. Bill of Lading

4. Application for Certificate of Origin

4. Certificate of Origin3. Declaration for Insurance 3. Insurance Certificate

2. Intimation for Inspection2. Inspection Certificate1. Proforma Invoice1. Commercial Invoice

AuxiliaryPrincipal

Export Documentation

qPre-shipment Documents qPost-shipment Documents

Pre-shipment Documents

q Documents at pre-shipment stage are those documents, which are required to be made, till the consignment is presented to the customs department for clearance.

q The following documents can, therefore, be treated as pre-shipment documents:-§ Proforma Invoice§ Confirmed order or contract§ Letter of Credit§ Pre-shipment Inspection Certificate§ Packing list§ Shipping Bill§ Export Declaration Forms (GR/SDF)§ ARE

Post-shipment Documents

q Documents at Post-shipment stage are naturally those which are prepared after the shipment.

q These documents include the following:-§ Mate Receipt § Bill of Lading § Airway Bill§ Roadway/Railway Bill§ Post Parcel/ Courier Receipt§ Invoices (including consular invoice) § Certificate of Origin§ Insurance Certificate or Policy § Bill of Exchange§ BRC

Documents for availing various Export Benefits

q Documents are also divided, depending upon, whether the benefit has to be claimed prior to exports or after the exports.

q For claiming benefits one has to make different applications with various government authorities.

Contd….

Documents for availing various Export Benefits

q At the pre-shipment stage the following documents are note-worthy. § Application for pre-shipment finance from the bank.§ Application of Advance Authorization or Duty Free Import

Authorisation with DGFT. § Application for execution of Bond with Central Excise

authorities.§ Application for obtaining CT-1 in case of a Merchant Exporter

Documents for availing various Export Benefits

q At the post shipment stage, the following documents are note-worthy.§ Application of Duty Entitlement Pass Book.§ Application for Focus Market or Focus Product Scheme. § Application for fixation of Brand rate of Drawback

Import Documentation

Important Documents–Imports

q Invoiceq Packing listq Bill of Lading or Delivery Order/Airway Bill q GATT declaration form duly filled in q Importers/CHA’s declaration q Licence/Authorisations in original wherever necessaryq Letter of Credit/Bank Draft/wherever necessary q Insurance document q Import license q Industrial License, if required q Test report in case of chemicals q Catalogue, Technical write up, Literature in case of machineries,

spares or chemicals as may be applicable q Separately split up value of spares, components, machineries q Certificate of Origin, if preferential rate of duty is claimed under

PTAs/FTAs etc.q No Commission declaration

Understanding Documents

Understanding Documents

q All documents whether it is for export or import transaction generally contain following information§ Name and address of the exporter and importer§ Document No. and date.§ Order No. and date§ Port of discharge§ Port of destination § Country of origin§ Description of Goods§ Marks and nos., model nos. [if any]§ Weight§ ITC HS Code No. § Value § Currency§ Terms of payment § Terms of shipment etc.

Understanding Documents

q However, depending upon the nature of the document, specific information is to be mentioned.

q For e.g. apart from the above details, Shipping Bill will include what export benefit is being claimed against that particular shipment, etc. Similarly, Packing List will give information about how goods are packed.

q Let us now study each document in depth.

Invoice

q It is itemized statement prepared and issued by a seller at the time of dispatching the goods to the buyer.

q It helps the Customs Authorities to:§ ensure that goods shipped are permitted by the export policy.§ compute the customs duty, if any, payable on the export or the

import.§ check the quantity of goods. They generally open a few

packages at random and check the veracity of details in the invoice.

§ check if there is any over-invoicing or under-invoicing (that may be resorted to by the importer to reduce the import duty payable).

Invoice

q Invoices are often called bills.

q Various types of invoices used in International Trade are

• Proforma Invoice• Commercial Invoice• Consular Invoice or Leagalized Invoice• Customs Invoice

PROFORMA INVOICE

q When negotiation is finalised and buyer intends to place an order he normally requests the exporter to send proforma invoice incorporating all details of proposed transaction.

q It is useful to buyer/importer in different ways:-§ It helps to eliminate common error of wrong description, spelling and

technical specifications.

§ Letter of Credit can be established as per proforma invoice. Many times in L/C, reference of proforma invoice is also given. In that case it becomes an important document while negotiation.

§ Sometimes an importer needs proforma invoice to enable him to obtain an import license from his government, & for foreign exchange authorities etc.

§ In some countries, proforma invoice is required for customs clearance.

COMMERCIAL INVOICE

q Commercial Invoice is a fundamental commercial document of prime importance in any trade transaction.

q It is a bill for the goods/ of merchandise from the seller to the buyer.

q It is a prima facie evidence of the contract of sale and purchase.

q There is a Special provision under Uniform Customs & Practice for Documentary Credits UCP – 600 for Commercial Invoice.

COMMERCIAL INVOICE

q There is no standard format for a commercial invoice, it generally contains the following details:§ Name & Address of the Shipper/Exporter and Importer/Consignee§ Commercial Invoice number & date§ Reference, order of acceptance or contract number & date

§ Description of goods consigned in full (No short cut), Quantity§ Shipment details – vessel name/voyage – port of loading / discharge § Net Weight / Gross weight

§ Terms and conditions of the Sale (Incoterms 2000)§ Terms of payment

§ Shipping marks and number of packages, special markings, if any§ Country of origin§ Import-Export licence number

§ Signature by authorised person

CONSULAR INVOICE or LEGALISED INVOICE

q Post shipment document.

q Consular invoice is a certificate issued by Trade Consular of importer’s country stationed in the exporter’s country.

q This invoice is required mainly by the African Countries like Kenya, Uganda, Tanzania, Mauritius, Nigeria, Ghana, Zanzibar, etc.

q This invoice is most important document which needs to be submitted for certification to the embassy of the importing country located in the country of exports.

CONSULAR INVOICE or LEGALISED INVOICE

q Consular invoice is an invoice which is sworn to as being correct in all particulars before the Consul of the country to which the goods are destined.

q It facilitates the clearing of goods through customs of the importing country.

q Consular invoices provide the importing country with a means of: § Checking prices of goods § Determining the origin of goods § Calculating import duties § Checking over- and under invoicing

CUSTOMS INVOICE

q The customs invoice is used in lieu of the commercial invoice in few importing countries for customs purposes, but the importer often needs a commercial invoice too.

q The customs invoice can be in a form called the certificate of value.

q The invoices vary in format but they contain essentially the same data as in the commercial invoice and packing list.

Packing List

q It is a consolidated statement in a prescribed format detailing how goods are packed, marked and numbered including weight and dimensions of each package.

q It is useful for customs at the time of examination and warehouse keeper of buyer to maintain inventory record and to effect delivery.

q It have many details common from invoice but it does not indicate unit rate value of goods.

q The exporter or his/her agent, the customs broker or the freightforwarder, reserves the shipping space based on the gross weightor the measurement shown in the packing list.

Packing List

q Customs uses it as a check-list to verify: § the outgoing cargo (in exporting) and § the incoming cargo (in importing).

q Basic functions of Packing List are: § To confirm the contents of a shipment as it left the exporter’s

premises. § To indicate weights, measures and the piece count (i.e. the

number of cartons or cases) in that shipment.

q It is prepared in 7-10 copies or as per the requirement.

Inspection Certificate

q “Certificate of Inspection” is issued by the Inspection Agency concerned certifying that the consignment has been inspected before shipment as per the requirements of the Exports (Quality Control and Inspection) Act, 1963.

q It satisfies the conditions relating to quality control and inspection as applicable to it and is certified export worthy.

q This certificate is required:§ by customs before allowing shipment of goods or § by a banker to negotiate the documents.

q This certificate bears cross references of invoice or contract number.

Inspection Certificate

q Inspection can be done by § Inspection Agency appointed by the Government of India, i.e.

Export Inspection Agency, Textile Committee, Central Silk Board etc.

§ Inspection Agency may also be nominated by importing countries’ Government i.e. SGS and OMIC by some African Countries.

§ Sometimes buyer himself appoints an independent private inspector to inspect the goods.

q If an inspection is a part of transaction, then exporter is required to arrange for necessary inspection.

q It can be a certificate of quality, weight, analysis, or the like.

Certificate of Origin [COO]

q It is a certificate indicating the fact that the goods which have been exported have originated or manufactured in a particular country. So it is a sort of declaration testifying the origin ofexport.

q It is normally required by an importer to clear goods from the customs.

q For political and social reasons, it is insisted by Customs Authority of importing country before goods are allowed to enter in the country.

q It helps the importer to take an advantage in duty concession, if any. For e.g. goods imported under Free Trade Agreement.

Certificate of Origin [COO]

q On the basis of COO, Customs can ensure that certain prohibited goods of particular countries are not imported.

q It also ensures that goods have not been reshipped by a seller who has brought them into his own country from some other place of origin.

q It is sent to the importer by the exporter.

q It is issued or signed by an independent official organization, such as a Chamber of Commerce, on prescribed form.

Certificate of Origin

q These are often required:§ to meet Customs requirements in the importing state § to comply with Banking requirements § for other official and commercial reasons.

q There are two categories of Certificate of Origin :1. Preferential Certificate of Origin and 2. Non-preferential Certificate of Origin

Preferential Certificate of Origin

q It entitles preferential treatment in duty in the importing country.

q These certificates are governed by rules of origin which are always part of Preferential Trading Agreements entered into between two or more countries.

q As far as India is concerned the following agreements are noteworthy:

• Generalised System of Preferences (GSP)• SAARC Preferential Trading Agreement (SAPTA)• Asia- Pacific Trade Agreement (APTA)• India-Sri Lanka Free Trade Agreement (ISLFTA)

Preferential Certificate of Origin

q Some of the agencies which are authorised to issue PCOO are:

• Export Inspection Agencies – All products.• Directorate General of Foreign Trade & its regional offices -

All products.• Spices Board, Ministry of Commerce & Industry - Spices and

Cashewnuts• Central Silk Board through 8 regional offices all over India -

Silk Products.• Coir Board – Coir and Coir Products.• Textile Committee - Textiles and madeups

Non-preferential Certificate of Origin

q It evidences the origin of goods and do not bestow any right to preferential tariffs.

q The Government has also nominated certain authorisedagencies to issue Non Preferential Certificate of Origin in accordance with Article II of International Convention Relating to Simplification of Customs formalities.

Shipping bill

q Shipping Bill is an important document required to seek permission of customs to export goods by Sea/Air. It is prepared by the exporter and submitted to the Customs.

q The exporter of any goods has to file a “SHIPPING BILL” as an entry for the purpose of export by air or sea and a “BILL OF EXPORT” in respect of export by land.

q Cargo will be allowed to be carted to Dock/Port sheds only afterstamping and passing of the shipping bill by customs authorities.

q The exporter has to sign a declaration in the Shipping Bill regarding the truth of its contents.

Shipping bill

q Shipping Bill normally contains: • the name and address of the importer/consignee and

exporter, • invoice number and date, • name of vessel carrying the goods, • name of master or agents, • port at which goods are to be discharged, • country of final destination, • description of goods, quantity details of each case,• value of the goods as defined in the Sea Customs Act, • number of packages with total weight, • marks and numbers, etc.

Shipping bill

q Types of Shipping Bills: § FREE SHIPPING BILL: Used for export of goods which neither

attract any Export duty/cess nor entitled to any Duty Drawback

§ DUTIABLE SHIPPING BILL: Used when export goods are subject to Export Duty/Cess. Duty is charged either on quantity basis (Fixed amount per kg. or per Metric tonne) or on certain percentage of assessable value.

§ DRAWBACK SHIPPING BILL: Used when Duty Drawback is to be claimed.

§ SHIPPING BILL FOR SHIPMENT EX-BOND: Used when the goods are to be exported which have been imported earlier and kept in bond prior to re-export.

Shipping bill

q Types of Shipping Bills: § DEPB SHIPPING BILL: When DEPB benefit is to be claimed.

§ DEEC SHIPPING BILL: This shipping bill is used for export of goods under Advance Authorisation (Duty exemption scheme).

§ DEEC CUM DRAWBACK SHIPPING BILL: This shipping bill is used for export of goods where both the schemes Duty Exemption as well as Drawback are to be taken into account.

Shipping bill

q Shipping bill is required to be submitted in quadruplicate. If Drawback/DEPB claim is to be made, one additional copy should be submitted.

q Copies of Shipping Bill are as under:§ Customs Copy: For record of Customs§ Exporter’s Copy: For record of Exporters/ Exporter may forward it

to shipping company. § Export Promotion Copy: For office of DGFT. This copy is the most

important document for claiming duty Neutralisation/Exemption benefits plus export incentives wherever applicable.

§ Exchange Control Copy: For negotiating the export documents in bank. It is Proof of export for exchange purposes.

§ DEPB Copy: For use in the import cell of customs for registration of licence.

ARE

q ARE stands for application for removal of excisable goods for exports by Air/Sea/ Post/Land.

q Goods which are sold overseas are exempted from payment of excise duty or entitled for Rebate of Excise Duty, if excise paid goods are exported. Under both these circumstances, the document to be used is ARE.

qWhen goods are removed without payment of duty for the purpose of export, they will get covered under the provisions of Rule 19 of the Central Excise Rules.

ARE

qWhen excise paid goods are exported and rebate of Excise Duty is to be claimed, they will get covered under Rule 18 of Central Excise Rules.

q ARE is prepared before clearance of goods from the factory gate.

q ARE will specify whether goods are exported under Rule 19 or under Rule 18.

ARE

q There are three types of ARE:

a) ARE 1: is used for physical export of goods.

b) ARE 2: is used when goods are removed for manufacture and packing of the goods to be exported.

c) ARE 3: is used when goods are supplied as deemed exports.

Mate Receipt

q Mate’s receipt is a receipt issued by the Master or Mate of the vessel stating that certain goods have been received on board his vessel.

q It is prima-facie evidence that the goods are loaded in the vessel.

q It contains:the name of shipping line and vessel, port of loading, port of discharge and place of delivery, marks and numbers, number and kind of packages, gross weight,description of goods, container status/seal number, shipping bill number and date andcondition of cargo at the time of its receipt on board the vessel.

q It is serially numbered.

Mate Receipt

q Port authorities recover port dues from exporter on production of this receipt.

q On payment of Dock dues, the exporter or his agent collects the receipt from the Port-Trust authorities and hands over to shipping company for preparing Bill of Lading.

q Bill of Lading is prepared on the basis of Mate’s Receipt.

q It is of a transferable nature.

q In case of ascertaining the exact date of shipment, the mate’s receipt date is also very important.

q Normally, the date of Export is regarded as “the date of Mate Receipt or the date of Bill of Lading, whichever is later”.

Export Declaration Forms (GR/SDF)

q As per the exchange regulations, exporters, wishing to ship goods abroad, are required to submit Export Declaration Forms to the Customs authorities (whenever the value of the shipment exceeds US $ 25,000) before any export of goods from India is made.

q It is to be filed by exporter stating that export proceeds would be realized within 180 days for non-status holder exporters and 360 days for status holder exporters.

Export Declaration Forms (GR/SDF)

GR Form

: Used for exports to all countries made other than by post including export of software in physical form i.e. magnetic tapes/discs and paper media - When S/B is filed manually. [prepared in duplicate]

SDF Form

: Appended to the shipping bill, for exports declared to Customs Offices notified by the Central Government which have introduced Electronic Data Interchange (EDI) system for processing shipping bills notified by the Central Government. [prepared in duplicate]

Relevant Declaration Forms, as prescribed by RBI under Foreign Exchange Management (Export of Goods and Services) Regulations, 2000.

Export Declaration Forms (GR/SDF)

q These forms normally contain:§ Name and address of exporter, IEC code number and description of

goods.§ Name and address of authorised dealer through whom the proceeds of

the exports have been, or will be, realised.§ Details of commission due to foreign agent or buyer should be

correctly declared. Otherwise, difficulties may arise at the time of remittances of such commission/ payment. An exporter should notethis point very carefully.

§ It should be clearly indicated whether the export is on “Outright Sale Basis” or “On Consignment Basis”

§ An exporter is required to give analysis of full export value, a break-up of FOB value, freight, insurance, discount, commission, etc.

§ An exporter has to mention the period within which he will realise full export value of transaction. If the shipment is on DA terms, then an exporter has to bring forex within that period. However, normally maximum period allowed is 180 days.

Statutory Declaration Form [SDF]

q Procedure for Distribution / disposal of copies of SDF

§ The SDF form should be submitted in duplicate (to be annexed to the relative shipping bill) to the Commissioner of Customs concerned.

§ After verifying and authenticating the declaration in form SDF, the Commissioner of Customs will hand over to the exporter, one copy of the shipping bill marked ‘Exchange Control Copy’ in which form SDF has been appended for being submitted to the bank within 21 days from the date of export.

Statutory Declaration Form [SDF]

§ Banks should accept the Exchange Control (EC) copy of the shipping bill and form SDF appended thereto, submitted by the exporter for collection/negotiation of shipping documents.

§ The manner of disposal of EC copy of shipping Bill (and form SDF appended thereto) is the same as that for GR forms.

MARINE INSURANCE POLICY

qMarine insurance policy is a contract whereby the insurer (insurance company) in consideration of a payment or premium by the insured agrees to indemnify the latter against loss incurred by him in respect of goods exposed to perils of the sea.

q It should normally: a. cover to the extent of 110% of CIF value b. express in the same currency of Letter of Credit and c. cover risk from the date of shipment.

MARINE INSURANCE POLICY

q The policy should specify different kinds of risks covered for example:

• ‘All Risk’, • ‘Warehouse to Warehouse’ and • ‘Clause A’

q The claim of insurance can be made payable at destination, if so desired.

q The amount paid to insurance company as consideration is known as ‘Premium’. It is a factor of cost and calculated roughly at 1%.

Bill of Exchange

q Bill of Exchange [BE] is a document drawn and is an order by the exporter to the buyer to pay the money in specified exchange.

q It is also known as a draft.

q A bill of exchange is accompanied by commercial documents which are presented by a bank and released to the buyer either against payment (at sight) or against a signature for payment on a specified future date.

q It is an unconditional written order.

Bill of Exchange

qWhen a BE is drawn on foreign firm it is termed as a foreign draft or bill of exchange.

q It is prepared either in an international currency or Indian rupees depending on the terms of the contract.

q Accordingly, the bill is known by the name of currency in which it is drawn. e.g. a bill drawn in US dollars is known as a “Dollar Bill” and when drawn in Rupees, it is termed as “Rupees Bill”.

Bill of Exchange

q The most common versions of a bill of exchange are:

A) Sight Draft –§ When the drawer (exporter) expects the drawee

(importer) to make payment immediately upon the draft being presented to him.

§ Unless and until the Draft is received, the Negotiating/ Collecting Bank does not hand over the Shipping documents and the buyer cannot take delivery of goods.

Bill of Exchange

B) Usance Draft –§ When draft is drawn for payment at a date later

than the date of presentation. § It may be a fixed future (specific) date or

determinable date according to the period of credit viz. 30 days, 60 days or 90 days etc. § It is presented to the drawee (importer) who will

retire the documents by accepting the draft by putting his signature and date.

Bill of Exchange

qWhen the payment is received in advance no Bill of Exchange is required to be drawn.

q Parties to a bill of exchangei. Drawer – who makes the order for making

payment. ii. Drawee – whom the order to pay is made. iii. Payee – whom the payment is to be made.

Bill of Exchange

q Features of a Bill of Exchange:§ A bill must be in writing, duly signed by its drawer,

accepted by its drawee and properly stamped.

§ It must contain an order to pay. Words like ‘please pay US $ 5,000 on demand and oblige’ are not used.

§ The order must be unconditional.

§ The sum payable mentioned must be certain or capable of being made certain.

§ The parties to a bill must be certain.

Bank Realisation Certificate

q Once the export proceeds are realised, the exporter has to prepare Bank Certificate of Export and Realisation for the purpose of claiming export benefits, incentives, etc.

q It is prepared as per Form No.1, given in Appendix 22A of Handbook of procedures 2004-09 (Vol. I).

q To prepare this certificate, the date of realisation is most essential, as the exporters have to apply for the export benefits, incentives, etc. within six months following the month/quarter of the realization month.

Bank Realisation Certificate

q It is signed by the authorized signatory of the firm/company with full name in block letters with designation, full official and residential addresses.

q Bankers attest this certificate as true and correct after verifying the particulars, including the date of mate receipt. This date is the most important, as this is the actual date of export.

Bank Realisation Certificate

q It is signed by an authorized signatory of the bank with his name and designation.

q Bankers affix certificate number and date and also mention the Authorized Foreign Exchange Dealer's Code number allotted to Bank by Reserve bank of India.

q For this purpose, this certificate must be accompanied with the following documents:-§ A copy of invoice, § A copy of customs attested export promotion copy of the

shipping bill, § A copy of Bill of Lading/ PP receipt/ Airway bill, § A copy of the insurance certificate/Insurance policy/cover.

Bill of Lading (B/L)

q Bill of Lading is the transport document associated with Sea freight.

q It is issued by the Shipping Company or its agent or master of a ship acknowledging that specified goods have been received on board as cargo for conveyance to a named place for delivery to the consignee who is usually identified.

q It is a document of title to the goods and, as such, is freely transferable by endorsement and delivery.

Bill of Lading (B/L)

q Bill of Lading serves three purposes as: § Receipt given by Shipping Company as goods described on

document has been received by it/carrier.§ Evidence of the contract of carriage by sea between the

shipping company and the shipper (exporter or importer). § Document of title to the goods and can be used to obtain

payment or a written promise before the merchandise is released to the importer.

q For the bill of lading to be negotiable it must be: 1. made out to the order to the shipper. 2. signed by the steamship company. 3. endorsed in blank by the shipper.

Bill of Lading (B/L)

q It is the only evidence to file a claim against the shipping company in the event of non-delivery, defective delivery or short-delivery of the cargo at the destination.

q For preparation of B/L the exporter should submit the complete set of B/L together with mate receipt to the shipping company which will calculate the freight amount on the basis of measurement or weight.

q On payment of freight, the shipping company returns the B/L duly signed and supported by requisite adhesive stamps.

Bill of Lading (B/L)

q Generally made out in the sets of two or three originals duly signed by the master of the ship or the agent of the steamship company.

q All the originals are equally valid for taking the delivery of the goods. Once one original is utilised the other originals become null and void.

qMarked as ‘Non-negotiable copy’ cannot be utilised for taking the delivery of goods.

Bill of Lading (B/L)

q Bill of Lading contains the following information: § Shipping company’s name and address.§ Consignee’s name and address.§ Notify party§ Name of the vessel, § Port of loading/Shipment and port of discharge.§ Shipping marks and Numbers, Cubic measurements, weights§ Description of the goods § Number of packages.§ Shipped on board with date-rubber stamp.§ Gross weight and net weight.§ Freight details § Signature of the shipping company’s agent.§ Container number if any.§ Shipper’s name and address.§ B/L Number and Date§ Originals§ Terms (on reverse)

Bill of Lading (B/L)

q Bill of Lading can be further described as under:-§ Shipped on Board :- When goods are actually shipped on

board.

§ Received for shipment :- When goods have been handed over to agent for shipment.

§ Through B/L:- When two or more carriers/ different modes of transport form i.e. road, rail, air, and sea employed to reach goods to their final destination.

Bill of Lading (B/L)

§ Transhipment B/L:- When there is no direct service between the two ports and ship-owner is prepared to tranship the goods at an intermediate port.

§ Stale B/L:- i.e. a late B/L that has been held too long before it is passed on to a bank for negotiation or to the consignee.

§ Clean B/L:- Where the carrier has noted that the goods have been received or loaded in ‘apparent good condition’ (no apparent damage, loss, etc.).

Bill of Lading (B/L)

§ Claused B/L:- Which contains additional clauses/notations limiting the responsibility of the shipping company which specify deficient condition(s) of the goods and/or packaging.

§ Combined Transport B/L:- When different modes of transport are used; usually issued when goods stuffed at shipper’s premises and delivered at consignee’s premises.

Bill of Lading (B/L)

§ Charter Party B/L:- Where a shipper has contracted with a shipping line to charter a vessel for the movement of cargo. It is issued by the carrier or its agent in the charter shipping. Unless otherwise authorized in the letter of credit (L/C), the charter party B/L is not acceptable in the L/C negotiation.

§ Freight Paid B/L:- When freight is paid at the time of shipment or in advance, the B/L is marked, freight paid.

§ Freight Collect B/L:- When the freight is not paid and is to be collected from the consignee on the arrival of the goods, the B/L is marked, freight collect.

Bill of Lading (B/L)

§ Negotiable B/L:- It is a title document to the goods, issued “to the order of” a party, usually the shipper, whose endorsement is required to effect it’s negotiation. Thus, a shipper's order (negotiable) B/L can be bought, sold, or traded while goods are in transit and is commonly used for letter of credit transactions.

Airway Bill (AWB)

q Airway Bill is a transport document associated with Airfreight.

q It serves as a receipt for goods and an evidence of the contract of carriage, but it is not a document of title to the goods. Hence,the AWB is non-negotiable.

q It contains the following details:§ number of packages § dimensions or volume § gross weight § shipping marks

q The goods in the air consignment are consigned directly to the consignee.

Airway Bill (AWB)

q On the reverse side of the airway bill are the airline’s terms and conditions of carriage whereby an airline is obligated to transport a consignment to its final destination once it has confirmed receipt of the shipper’s consignment.

q Airway bill can be comprised in two parts:§ MAWB (Master Airway bill) – shipments sent on a direct basis,

not consolidated.

§ HAWB (House Airway bill) – shipments sent on a consolidation basis whereby grouping together various clients consignments under one MAWB being issued by the freight forwarder.

ECGC COVER

q Export Credit Guarantee Corporation of India (ECGC) is an institution, which plays vital role in the promotion of exports.

q How does ECGC help Exporters?§ offers insurance protection to exporters against payment risk, § provides guidance in export related activities, § makes available information on different countries with its own

credit ratings, § makes it easy to obtain export finance from banks/ financial

institutions, § assists exporters in recovering bad debits, § information on credit - worthiness of overseas buyers.

ECGC COVER

q Main activities of the ECGC: § ECGC provides a wide range of credit risk insurance covers to

exporters against loss in export of goods and services and issues policies.

§ The ECGC covers can be divided broadly into four groups:1. Standard Policies issued to:

a) exporters to protect them against payment risks involved in exports on short-term credit; and

b) small exporters’ policy to protect them against payment risks involved in exports on short-term credit.

ECGC COVER

2. Specific policies designed to protect Indian firms against payment risks involved in: a) exports on deferred terms of payment; b) services rendered to foreign parties; & c) construction works and turnkey projects undertaken abroad.

3. Financial guarantees: ECGC offers guarantees to banks and financial institutions in India to protect them from risks of loss involved in extending their financial support to exporters at the pre-shipment as well as post-shipment stages;

ECGC COVER

4. Special schemes:ECGC also provides guarantee to bank under special schemes viz. § Transfer Guarantee [meant to protect banks which add

confirmation to Letters of Credit opened by foreign banks], § Insurance cover [for Buyer’s Credit], § Line of Credit, § Overseas Investment Insurance to Indian companies investing in

joint ventures abroad in the form of equity or loan § Exchange Fluctuation Risk Insurance.

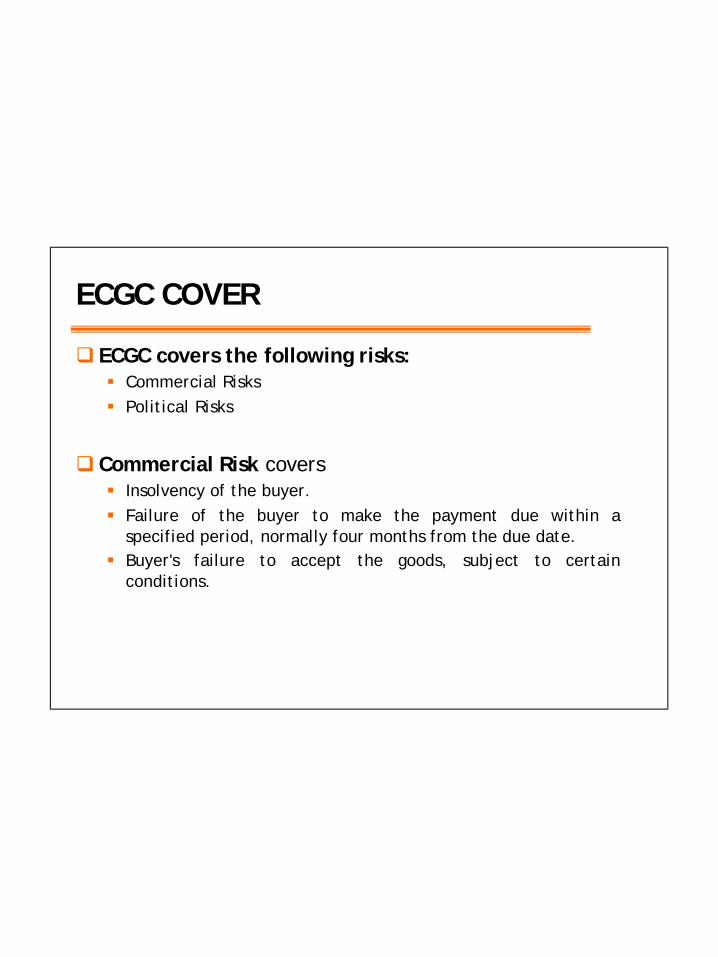

ECGC COVER

q ECGC covers the following risks: § Commercial Risks§ Political Risks

q Commercial Risk covers § Insolvency of the buyer.§ Failure of the buyer to make the payment due within a

specified period, normally four months from the due date.§ Buyer's failure to accept the goods, subject to certain

conditions.

ECGC COVER

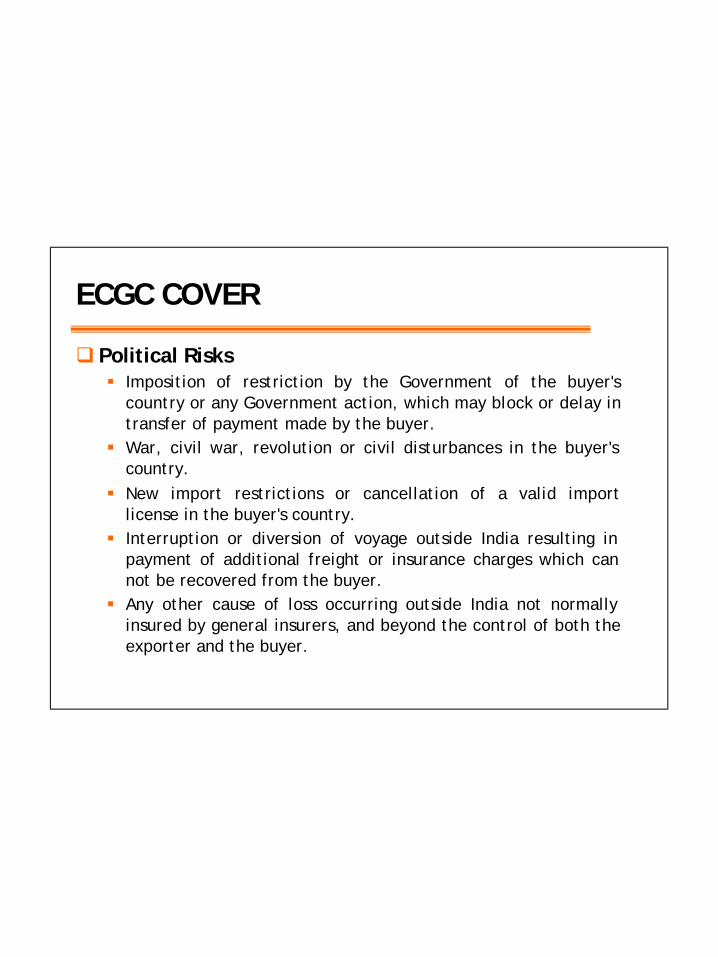

q Political Risks§ Imposition of restriction by the Government of the buyer's

country or any Government action, which may block or delay in transfer of payment made by the buyer.

§ War, civil war, revolution or civil disturbances in the buyer's country.

§ New import restrictions or cancellation of a valid import license in the buyer's country.

§ Interruption or diversion of voyage outside India resulting in payment of additional freight or insurance charges which can not be recovered from the buyer.

§ Any other cause of loss occurring outside India not normally insured by general insurers, and beyond the control of both the exporter and the buyer.

ECGC COVER

q Risks not covered by ECGC § Commercial disputes including quality disputes raised by the

buyer, unless the exporter obtains a decree from a competent court of law in the buyer's country in his favor.

§ Causes inherent in the nature of goods.§ Buyers’ failure to obtain necessary import or exchange

authorization from authorities in his country. § Default or insolvency of any agent of exporter or collecting

bank. § Loss or damage to goods which can be covered by general

insurance. § Exchange rate fluctuation.§ Failure or negligence on the part of the exporter to fulfill the

terms of the export contract.

Tips for Proper Documentation

q Implications of all Regulatory documents must be studied carefully. For example; declaration on ARE1 forms.

q Filing of Shipping Bill electronically requires correct entries including HS code for the product. Many times, small mistakes are extremely difficult to correct later on.

q Shipping bills must be filed according to the scheme the exporter wants to avail . For example; DEPB /DFIA/Drawback etc.

q Extra care should be taken when combination of schemes is intended to be used. For example; DEEC – Drawback.

q Co-relation between customs, excise and DGFT is extremely important. Many times documents do not match with each other, which results in delay or denying of some benefit under one or the other scheme.

Tips for Proper Documentation

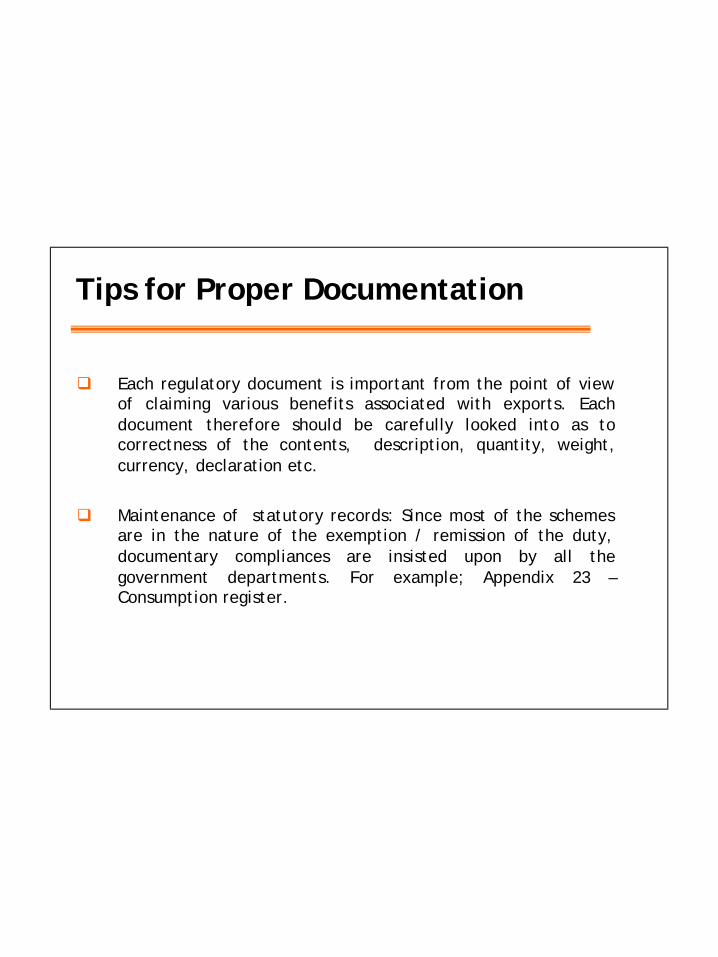

q Each regulatory document is important from the point of view of claiming various benefits associated with exports. Each document therefore should be carefully looked into as to correctness of the contents, description, quantity, weight, currency, declaration etc.

q Maintenance of statutory records: Since most of the schemes are in the nature of the exemption / remission of the duty, documentary compliances are insisted upon by all the government departments. For example; Appendix 23 –Consumption register.

PRE-SHIPMENT INSPECTION FORMALITIES q Quality is an important element of export marketing. q Exporters must export goods of international standards. q In India, the Quality Control and Inspection Act provides for

compulsory quality control and pre-shipment inspection. q The Export Inspection Council [EIC] was set up by the Government

of India under Section 3 of the Export (Quality Control and Inspection) Act, 1963 (22 of 1963), in order to ensure sound development of export trade of India through Quality Control andInspection and for matters connected thereof.

q EIC and its agencies are involved in maintaining the quality andproviding inspection certificate to the exporters.

q The inspection certificate is required by the customs authority for the shipment of the goods.

PRE-SHIPMENT INSPECTION FORMALITIESq ISI and AGMARK are recognized as a mark of adequate quality for

export purpose.

q The customs authorities allow the export of products marked ISI and AGMARK without any pre-shipment inspection certificate, as such product’s quality is guaranteed.

q TYPES OF PRE-SHIPMENT INSPECTION, SYSTEMS OF QUALITY CONTROL/ INSPECTION :

a. Consignment-wise inspection (CWI)b. In-process Quality Control (IPQC)c. Self-certification scheme d. Food Safety Management System based Certificatione. Fumigation of consignment

Procedure for pre-shipment inspection

Inspection

A Units with adequate In-process quality

control

BUnits not approved with In-process quality control

Units with adequate In-process quality control

q Certificate of inspection given on the basis of the unit’s performance report submitted by the inspectors during the checks at all levels of production.

q They have to submit their applications in the prescribed ‘Intimation for Inspection’ form to the Export Inspection Agency.

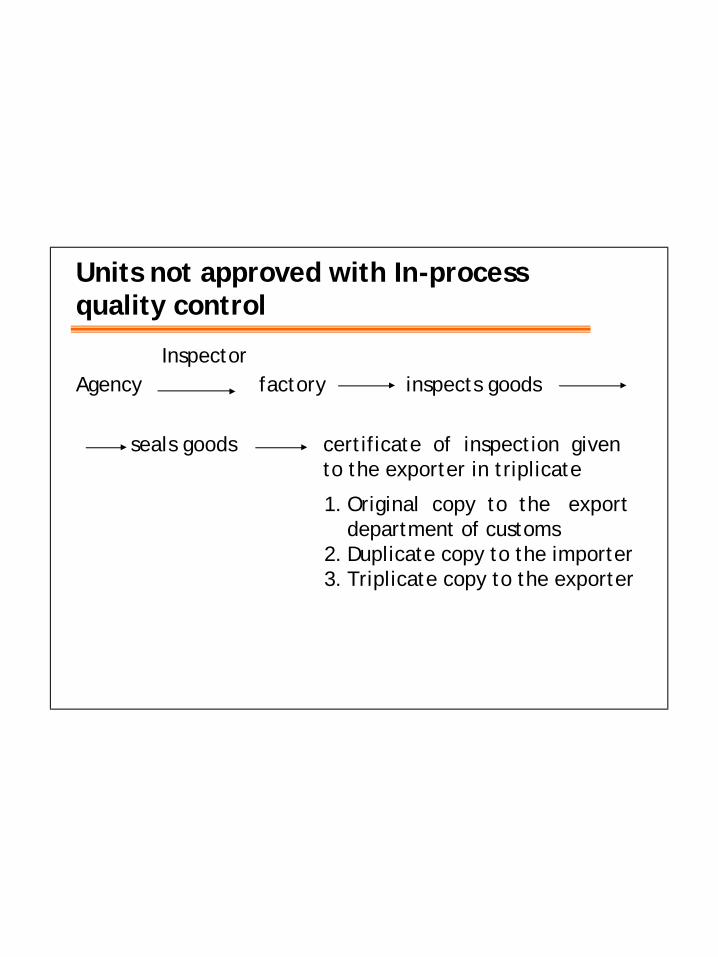

Units not approved with In-process quality control

Application for inspection Agency1. In the prescribed format2. 7 days prior to the date of shipment3. Documents required

• Copy of the export contract• Copy of letter of credit• Details of packing specification• Invoice giving evidence of FOB value of export

consignment• Crossed cheque for the amount of inspection

fees, and• Declaration regarding importer’s technical

specification, if any.

Units not approved with In-process quality control

InspectorAgency factory inspects goods

seals goods certificate of inspection given to the exporter in triplicate

1. Original copy to the export department of customs

2. Duplicate copy to the importer3. Triplicate copy to the exporter

Thank You

Sudhakar Kasture

Exim Institute

Mumbai: A-203, Everest Chambers,

Next to Star TV Office,Near Marol Naka,

Andheri-Kurla Road,Andheri (East), Mumbai – 400 059.

Tel: 28507615/28507329/65769126Fax: 28506419

Pune:EPI Centre, Opp. Indsearch,

Law College Road, Pune 411004.Tel:(+91) 020 65246159 Fax: (+91) 020 25465195

E-mail: [email protected]