94

Export Opportunities for the U.S. Wind Energy Industry Brian O’Hanlon: Moderator

Export Opportunities for the U.S. Wind Energy Industry

Brian O’Hanlon: Moderator

Beijing | Brussels | London

Emerging wind power marketsKlaus Rave, Chairman, Global Wind Energy Council

WINDPOWER Anaheim, 24 May 2011

Beijing | Brussels | London

Outline

1.2010 market growth2.China3.Latin America

1. Brazil2. Mexico3. Chile4. Argentina5. Other interesting markets6. Scenarios up to 2030

Beijing | Brussels | London

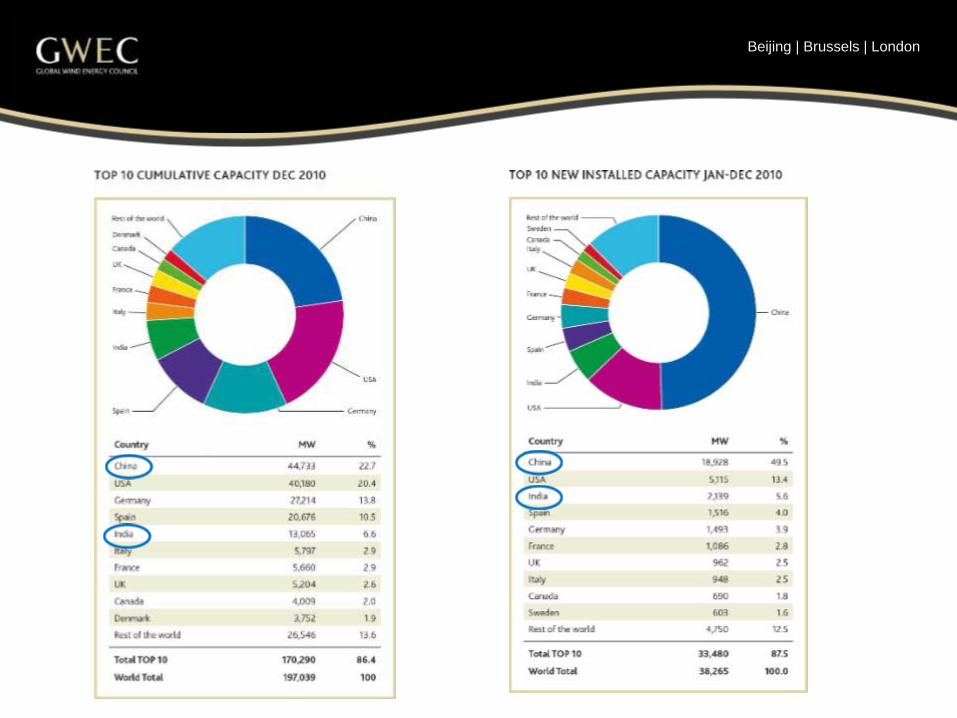

Chapter 1 | 2010 market growth

Beijing | Brussels | London

Beijing | Brussels | London

Beijing | Brussels | London

Beijing | Brussels | London

Beijing | Brussels | London

Chapter 2 | China

Beijing | Brussels | London

Drivers for wind power in China

• Strong political commitment to RE developmento RE law enacted in 2006o Feed-in tariff since 2009o Mandatory share of 1% non–hydro RE in 2010 and

3% in 2020o Unofficial target of 200 GW of wind by 2020

• Clean Development Mechanism (CDM)o 869 projects approved for CDM (39% of all projects

registered)o Important contribution on ROI

Beijing | Brussels | London

Wind Base Programme

Beijing | Brussels | London

Grid connection

• Infrastructure struggles to keep up with wind power additions; biggest problem for future development

• Recent agreement by Chinese grid companies to connect 80 GW by 2015 and 150 GW by 2020

• $6.1bn have been invested by end of 2010 to facilitate wind integration

• Investments of $600bn planned between 2009-2020 in super grid

Beijing | Brussels | London

Market share – Foreign vs domestic

Beijing | Brussels | London

Chapter 2 | Latin America

Beijing | Brussels | London

Strong growth in Latin America

Beijing | Brussels | London

Strong growth in Latin America

• Installed capacity quadrupled in three years

• 700 MW added in 2010 to reach 2,000 MW – 50% growth

• Leading markets: Brazil (931 MW), Mexico (519 MW), Chile (172 MW)

• Other interesting markets: Argentina, Chile, Uruguay, Costa Rica, Peru, Venezuela

Beijing | Brussels | London

Brazil - Potential

• Wind potential of 350 GW (at heights of 80-100 m)

• Large unpopulated areas

• 9,600 km of coastline

• Main regions for development:o North/North-East (Rio Grande do Norte, Ceará,

Pernambuco and Bahia)o South/South-East (Rio Grande do Sul, Santa Catarina)

Beijing | Brussels | London

Brazil – Other benefits

• Currently 70% hydro in power mix

• Problem: water shortages, especially during dry season, when winds are strongest

• Good compatibility hydro/wind thanks to flexibility

• Well developed grid, windiest areas close to grid and demand centers

Beijing | Brussels | London

Brazil - Market

• Market grew by 326 MW in 2010, reaching 931 MW (+50%)

• PROINFA (2002): target of 1,400 MW, last projects under construction

• 2009 auction: 71 wind projects, 1,800 MW- price: Rs 148/MWh (113 USD)

• 2 auctions in 2010: 1,500 MW & 500 MW wind- price: Rs 134/MWh and Rs 123/MWh

Beijing | Brussels | London

Beijing | Brussels | London

Brazil - Players

• First market entrant: Wobben Enercon (Germany)

• More recently: Impsa (Argentina); Suzlon (India); Vestas (Denmark)o all involved in Proinfa projects

• New entrants in 2009/2010 auctions: Alstom, Gamesa, GE Wind, Siemens

- eligible for BNES financing due to local manufacturing

• Target: local content share of 60%

Beijing | Brussels | London

Brazil - Outlook

• 1,000 MW threshold reached very soon

• Total project pipeline up to 2013: more than 4,000 MW • 2 more auctions announced for June 2011

• Long-term outlook more unclear

Beijing | Brussels | London

Mexico - Potential

• 316 MW installed in 2010, total capacity 519 MW

• Potential estimated at around 71 GW

• Most promising regions:

1. Isthmus of Tehuantepec, State of Oaxaca (508 MW operating now – potential: 10 GW)

2. La Rumorosa, State of Baja California (potential: 5 GW)3. Northern coast on the Gulf of Mexico4. Yucatán Peninsula

Beijing | Brussels | London

Mexico - Policy

• Since 1992, private sector can participate through:o Self-generationo Independent Power Producers (IPP) (PPAs with CFE)o Export to other countries

• 2008: Energy Reform Bill, including legislation on RE (LAERFTE):o Target to increase non-hydro RE capacity from 3.3%

(1,900 MW) to 7.6% (4,500 MW) by 2012o SENER in charge of developing RE strategyo Creation of RE Fund (USD 220 mil/year)

Beijing | Brussels | London

Mexico – Market players

• Acciona, Iberdrola and EDF with an important share of the market.

• Gamesa, Acciona, Clipper and Vestas Wind turbines have been installed.

• Blades, towers and turbine parts are manufactured domestically, but the indigenous capacity is still marginal.

Beijing | Brussels | London

Mexico - Outlook

• 717 MW to be installed during 2011

• Brings capacity up to 1,200 MW

• Pipeline: 3,500 MW for the next 3-4 years

• Main regions: Oaxaca, Baja California, Tamaulipas

Beijing | Brussels | London

Argentina - Potential & Policy

• 60 MW installed at the end of 2010

• A huge wind power potential with Patagonia resource (said to be capable of powering the whole continent 7 times over)

• The province of Buenos Aires also with good resources and closer to transmission grid

• GENREN, an auction program has awarded 754 MW•• Lack of financial certainty main barrier for wind development

Beijing | Brussels | London

Argentina – Benefits & Obstacles

• A well developed manufacturing industry already in the country. IMPSA and NRG Patagonia already manufacturing.

• Investments in transmission infrastructure is needed to develop the Patagonian potential.

• Strong drive to diversify the power matrix in order to reach energy independence

Beijing | Brussels | London

Chile - Potential & Policy

• 170 MW of wind power installed.

• A huge wind power potential mainly at the south of the country.

• Problem: main wind resource generally at a long distance from key demand centers

• Target: 10% of Renewable Energy to 2024

Beijing | Brussels | London

Chile - Market players & Outlook

• No wind manufacturing capacity currently in Chile

• Urgent need for new power generation investments:- Hydroelectric capacity threatened by severe drought in

recent years- Increasing demand to fuel economic growth

• Price of energy on spot market important driver for wind development, but long-term investor certainty even more essential

Beijing | Brussels | London

Other promising markets

Uruguay: - 150 MW already awarded in first auction (2010); second auction for 150 MW in process- Target: 500 MW of wind by 2015.

Peru: - A first auction awarded 142 MW; second RE auction in process.

Central America and Caribbean: - Wind Energy can be highly competitive, but regulatory frameworks and investment confidence need to be improved.

Beijing | Brussels | London

Beijing | Brussels | London

Thank you.

THE INTERNATIONAL TRADE ADMINISTRATION: HELPING U.S. WIND COMPANIES COMPETE GLOBALLY

Brian O’HanlonOffice of Energy and Environmental Industries

WINDPOWER 2011May 24, 2011

Topics Covered

International Trade Administration U.S. Department of Commerce

Federal Programs Supporting U.S. Exports

What is the International Trade Administration?

Renewable Energy and Energy Efficiency Export Initiative

Opportunities to Work With ITA and the U.S. Government

International Buyers Program at WINDPOWER 2011!

Contact Information

International Trade Administration U.S. Department of Commerce

International Trade Administration

• Manufacturing and ServicesCompetitiveness

• U.S. and Foreign Commercial ServiceTrade Promotion

• Market Access and ComplianceNegotiation

• Import AdministrationAnti-Dumping

The Department of Commerce’s International Trade Administration (ITA) is the lead trade promotion agency of the

United States Government

Manufacturing and Services (MAS)

Industry Expertise

Aerospace Automotive Building Products and Construction Chemicals Consumer Goods Electronic Commerce Energy Environmental Technologies Forest Products Health Information and Telecommunications Technologies Manufacturing Machinery Metals Textiles and Apparel

Promote U.S. Industry Competitiveness

Eliminate Trade Barriers

Evaluate Regulation and Policy

Support Trade Promotion

Provide Market Research and Analysis

Organize Trade Promotion Events

Advocate for Policy in Foreign Markets

Matchmaker for U.S. Government Programs

International Trade Administration U.S. Department of Commerce

International Trade Administration U.S. Department of Commerce

U.S. Foreign and Commercial Service

Access Export Readiness

Identify Key Markets

Determine Sales Potential

Implement Export Plan

Overcome Challenges

U.S. Commercial Service Business Approach

Trade Counseling. Get the information and advice you need to succeed

Market Intelligence. Target the best trade opportunities.

Business Matchmaking. Connect with the right partners and prospects.

Commercial Diplomacy. Ensure your products and services have the best possible prospects for success in international markets.

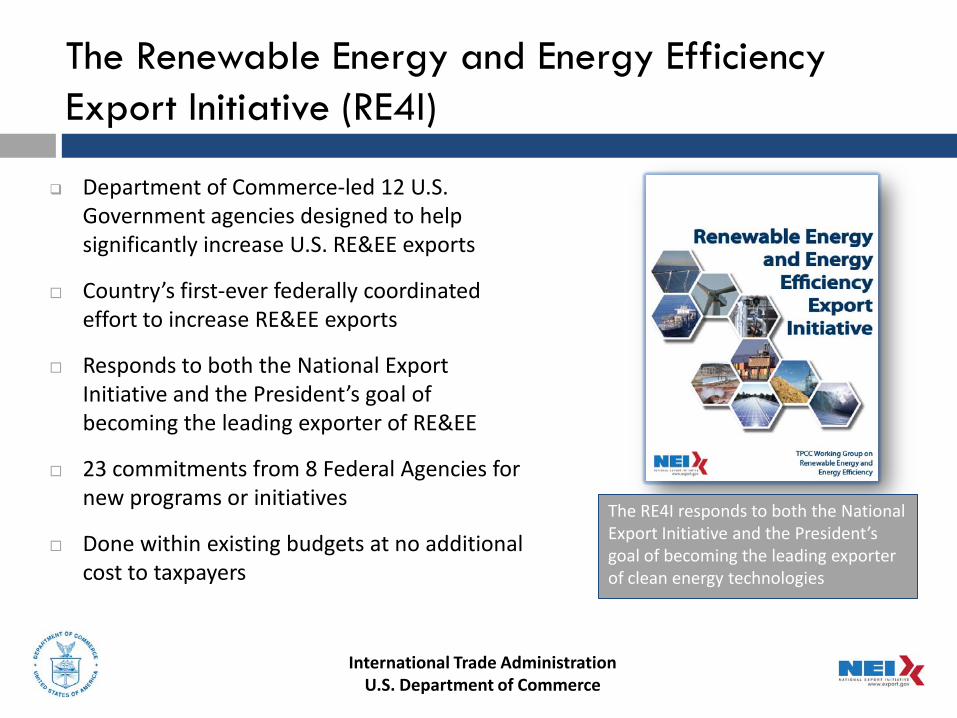

Department of Commerce-led 12 U.S. Government agencies designed to help significantly increase U.S. RE&EE exports

Country’s first-ever federally coordinated effort to increase RE&EE exports

Responds to both the National Export Initiative and the President’s goal of becoming the leading exporter of RE&EE

23 commitments from 8 Federal Agencies for new programs or initiatives

Done within existing budgets at no additional cost to taxpayers

The RE4I responds to both the National Export Initiative and the President’s goal of becoming the leading exporter of clean energy technologies

The Renewable Energy and Energy Efficiency Export Initiative (RE4I)

International Trade AdministrationU.S. Department of Commerce

• Export Express Program• Export Working Capital Loan Program• International Trade Loan Program

Federal Programs to Facilitate Wind Exports

International Trade Administration U.S. Department of Commerce

• Political Risk Insurance• Renewable Energy Finance Team• Renewable Energy Investment Funds

• Feasibility studies• Overseas Grants• Contracts with U.S. Firms

U.S. Trade and Development Agency

Overseas Private Investment Corporation

Small Business Administration

• U.S. Agency for International Development• State Department EcoPartnerships Program• Energy and Climate Partnership of the Americas

Additional Federal Programs

• Carbon Policy• Pre-Export Financing• Export Credit Insurance

• U.S. Foreign and Commercial Service• Market Development Cooperator Program• Trade Missions

U.S. Export-Import Bank

Department of Commerce

International Trade Administration U.S. Department of Commerce

Maintaining Competitiveness

Created in 2007

Primary U.S. Government mechanism to manage foreign investment promotion

What we do:

Facilitate investment inquiries

Act as ombudsman

Connect investors with U.S. states

Provide policy guidance

Educate investors

Other Opportunities

League of Green Embassies advance the presidential mandate to reduce greenhouse gas emissions in USG

buildings;

demonstrate the capabilities of U.S. products and technologies to the worldmarket;

increase the exports of U.S. products and services in line with the NationalExport Initiative.

ContactKeith Curtis, [email protected]

International Trade Administration U.S. Department of Commerce

Intl. Buyers Program at WindPower 2011

Buyer delegations from fourteen countries

Trade Counseling

Market Intelligence

Business Matchmaking

Exhibitor Promotion

Free guide to exporting

International Trade Administration U.S. Department of Commerce

Contact Information

Brian O’HanlonOffice of Energy and Environmental Industries

(202) 482-3492

[email protected]/reee

Financing Wind Energy Exports: The Role of Ex-Im Bank

Craig O’Connor, DirectorOffice of Renewable Energy & Environmental Exports

WINDPOWER 2011

U.S. Ex-Im Bank

Export Credit Insurance

Case Study:

Direct Loan

• made by Ex-Im Bank to a foreign buyer

• Fixed interest rates based on a 1% spread over Treasury notes

– Interest rate for an 18-year Direct Loan is 4.78% (as of April 14, 2011)

• The international borrower submits the Direct Loan application.

• Ex-Im Bank requires the buyer to make a cash payment to the exporter equal to at least 15% of the U.S. supply contract.

– 15% cash payment can either be borrowed from a lender or the exporter, or be from the buyer’s own funds.

• Exporter paid with disbursement L/C or buyer is reimbursed

• A negotiated credit agreement required for a Direct Loan

• Shipping must be made on U.S.-flag vessel (except air shipments)

Case Study: Clipper Windpower

Case Study: Gamesa – Cerro de Hula, Honduras

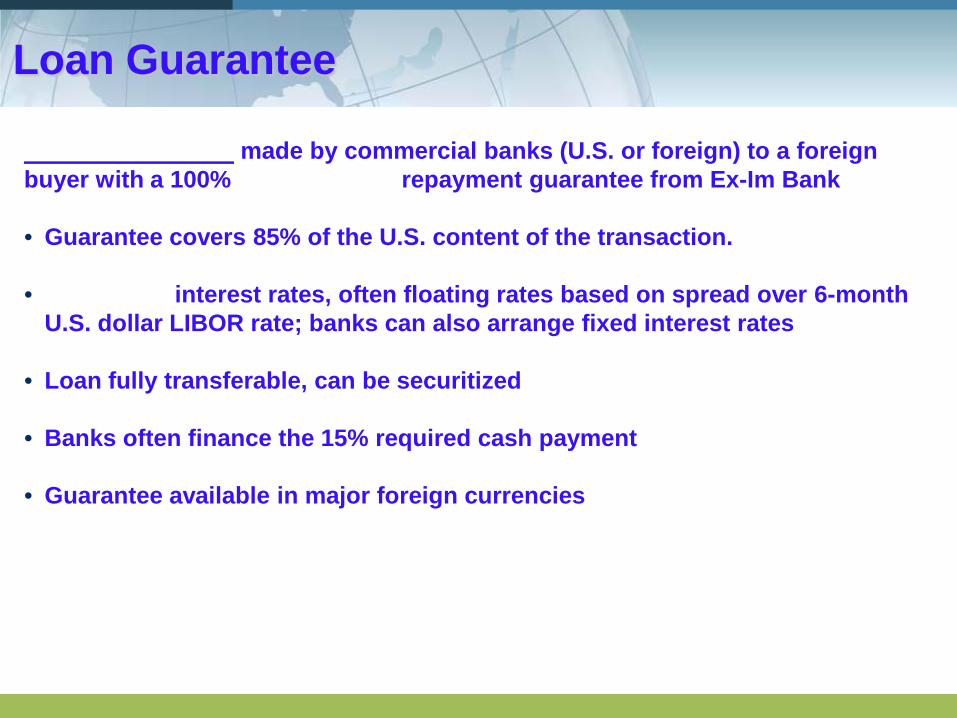

Loan Guarantee

made by commercial banks (U.S. or foreign) to a foreign buyer with a 100% repayment guarantee from Ex-Im Bank

• Guarantee covers 85% of the U.S. content of the transaction.

• interest rates, often floating rates based on spread over 6-month U.S. dollar LIBOR rate; banks can also arrange fixed interest rates

• Loan fully transferable, can be securitized

• Banks often finance the 15% required cash payment

• Guarantee available in major foreign currencies

Northern Power – Italy Community Wind

Northern Power – Italy Community Wind

Largest Private Renewable Energy Project in Honduras

Largest Private Renewable Energy Project in Honduras

Financing Approach

Turnkey Approach

Driving US Exports

Exporting Case Studies

Patrick K. StromSales Account Manager, International MarketsNRG Systems

WINDPOWER 2011 Conference & Exhibition May 24, 2011

Overview

• About NRG Systems and our products

• There is a world of opportunity. Good news!

• 3 ways to optimize international success

• 2 case studies

About NRG Systems • Founded 1982

• 114 employees

• 144 countries

• Lean manufacturing

• Niche business

• Met towers, data loggers, sensors, LIDAR, turbine control sensors, software

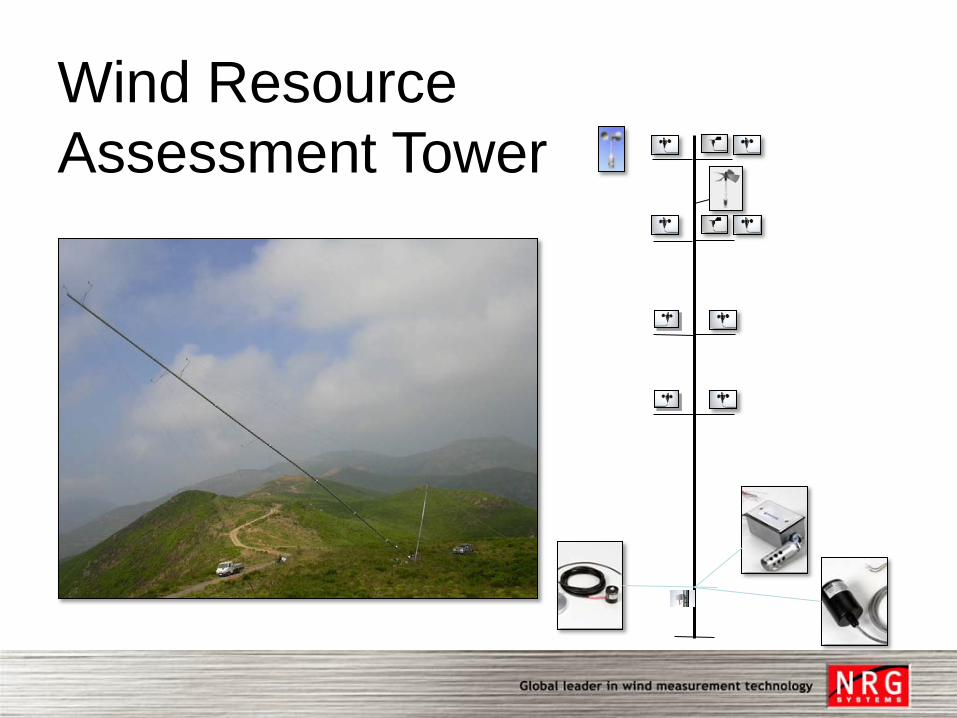

Wind Resource Assessment Tower

Optimizing Success: Globalization

The Puzzle…

Optimizing Success: Sea Freight

Comparison

Truck• Vermont to Los Angeles: 3000 miles• Greater carbon footprint, handling• Cost: $5000-$10,000; 30% fuel surcharge

Sea Freight • Vermont to Port of Shanghai: 8000 miles• Sealed 20 ft container, few restrictions• Cost: $3500

Optimizing Success: Smart Packaging

EnviroCrate60m Tower System

Optimizing Success: Smart Packaging

EnviroCrate60m Tower System

Delivery

The value of a Freight Forwarder

• Long term relationship

• Invaluable in case of trouble

• Ally for getting payment safely

• Navigate complex letters of credit

The value of an International Partner

• Finding clients, targeted marketing

• Navigating customs, local regulations

• Long term cooperation

• Mutual success

Case Study 1:Kiribati

• 2 x 34m complete systems

• NGO funding, Japanese partner

• Free sea/surface shipping to Hawaii, weekly flight to Kiritimati Island

• High reliance on fossil fuels

• Climate change (43 ft highest point)

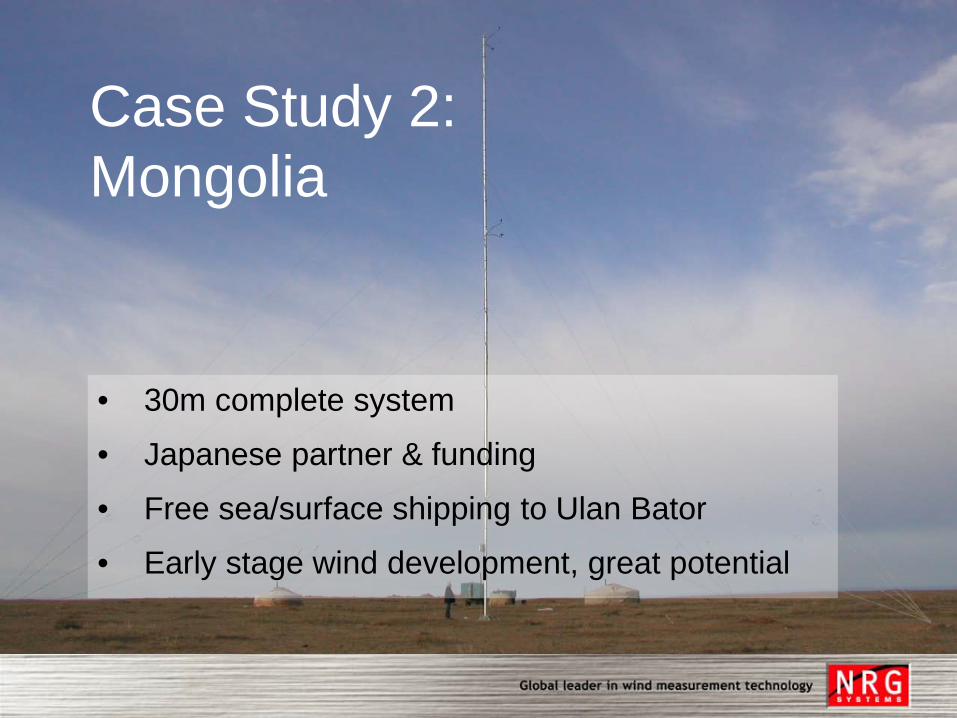

Case Study 2:Mongolia

• 30m complete system

• Japanese partner & funding

• Free sea/surface shipping to Ulan Bator

• Early stage wind development, great potential

Conclusion

• Being in the U.S. has advantages

• Think about the whole product lifecycle

• Avoid commoditization

• Use resources available to you: government programs, forwarders, partners

Now go close the trade deficit!

Patrick Strom

1-802-482-2255

www.nrgsystems.com

Questions and Answers

Part 1

Questions and Answers

Part 2

Questions and Answers

Part 3

Questions and Answers

Part 4