CHAPTER 1 INTRODUCTION 1. CONCEPT OF INSURANCE Life has always been an uncertain thing. To be secure against unpleasant possibilities, always requires the utmost resourcefulness and foresight on the part of man. To pray or to pay for protection is the spirit of the humanity. Man has been accustomed to pray God for protection and security from time immemorial. In modern days Insurance Companies want him to pay for protection and security. The insurance man says "God helps those who help themselves"; probably he is correct. Too many people in this country are not in employment; and work for too many no longer guarantees income security. Several millions are part- time, self employed and low-earning workers living under pitiable circumstances where there is no security cover against risk. Further the inherent changing employment risks, the prospect of continual change in the work place with its attendant threats of unemployment and 1

Transcript

CHAPTER 1

INTRODUCTION

1 CONCEPT OF INSURANCE

Life has always been an uncertain thing To be secure against unpleasant possibilities

always requires the utmost resourcefulness and foresight on the part of man To pray

or to pay for protection is the spirit of the humanity Man has been accustomed to

pray God for protection and security from time immemorial In modern days

Insurance Companies want him to pay for protection and security The insurance man

says God helps those who help themselves probably he is correct

Too many people in this country are not in employment and work for too many no

longer guarantees income security Several millions are part-time self employed and

low-earning workers living under pitiable circumstances where there is no security

cover against risk Further the inherent changing employment risks the prospect of

continual change in the work place with its attendant threats of unemployment and

low pay especially after the adoption of New Economic Policy and the imminent life

cycle risks - a new source of insecurity which includes the changing demands of

family life separation divorce and elderly dependents 1048753 are tormenting the society

Risk has become central to ones life It is within this background life insurance policy

has been introduced by the insurance companies covering risks at various levels Life

insurance coverage is against disablement or in the event of death of the insured

economic support for the dependents It is a measure of social security to livelihood

for the insured or dependents This is to make the right to life meaningful worth

living and right to livelihood a means for sustenance Therefore it goes without

saying that an appropriate life insurance policy within the paying capacity and means

of the insured to pay premium is one of the social security measures envisaged under

the Indian Constitution Hence right to social security protection of the family

economic empowerment to the poor and disadvantaged are integral part of the right to

life and dignity of the person guaranteed in the constitution

Man finds his security in income (money) which enables him to buy food clothing

shelter and other necessities of life A person has to earn income not only for himself

but also for his dependents viz wife and children He has to provide legally for his

1

family needs and so he has to keep aside something regularly for a rainy day and for

his old age This fundamental need for security for self and dependents proved to be

the mother of invention of the institution of life insurance

What is Insurance

The business of insurance is related to the protection of the economic values of assets Every

asset has a value The asset would have been created through the efforts of the owner The

asset is valuable to the owner because he expects to get some benefit from it The benefit

may be an income or some thing else It is a benefit because it meets some of his needs In the

case of a factory or a cow the product generated by is sold and income generated In the case

of a motor car it provides comfort and convenience in transportation There is no direct

income

Every asset is expected to last for a certain period of time during which it will perform After

that the benefit may not be available There is a life-time for a machine in a factory or a cow

or a motor car None of them will last for ever The owner is aware of this and he can so

manage his affairs that by the end of that period or life-time a substitute is made available

Thus he makes sure that the value or income is not lost However the asset may get lost

earlier An accident or some other unfortunate event may destroy it or make it non-functional

In that case the owner and those deriving benefits from there would be deprived of the

benefit and the planned substitute would not have been ready There is an adverse or

unpleasant situation Insurance is a mechanism that helps to reduce the effect of such adverse

situations

Insurance in law and economics is a form of risk management primarily used to hedge

against the risk of a contingent loss Insurance is defined as the equitable transfer of the risk

of a potential loss from one entity to another in exchange for a premium Insurer in

economics is the company that sells the insurance Insurance rate is a factor used to

determine the amount called the premium to be charged for a certain amount of insurance

coverage Risk management the practice of appraising and controlling risk has evolved as a

discrete field of study and practice

2

PROGRESS IN INSURANCE BUSINESS

The growth of Life Insurance in concrete terms could be said to being during the first two

decades of twentieth century when most of the major companies were founded They grew in

terms of rise in the number of companies in terms of number of policies and sum assured as

well as total life fund Indian Insurance Year Book published for the first time in 1914 gives

the figure of the total business-in -force as 2244 crore which grew to Rs 298 crore in 1938

In 1914 there were only 44companies transacting insurance business in India and during the

next 25 years their number rose to 176 The total progress on all the primary heads viz life

fund (Rs 5050 crore) premium income (Rs 1050 crore) and new business (Rs 4330 crore)

indicate that Indian Insurance Business had been making a definite headway during this

years The inter-war -years thus saw rapid growth life insurance in India

The promotion of new life insurance companies continued to be almost a craze and insurance

companies mushroomed In this period 176 insurance companies were formed and many of

them failed Thus unhealthy growth was harmful to the interest of the policy holders and

insurance business in India Feeling concerned about it the All India Life Assurance Offices

Association urged upon the Government in 1932 to undertake the insurance legislation to

(a) Compulsorily register all Life Insurance companies

(b) Secure a deposit of Rs2 lakh from all Life Insurance companies

(c) Compel foreign companies doing business in India to keep sufficient funds in

India securities to meet their liabilities under all policies issued in India

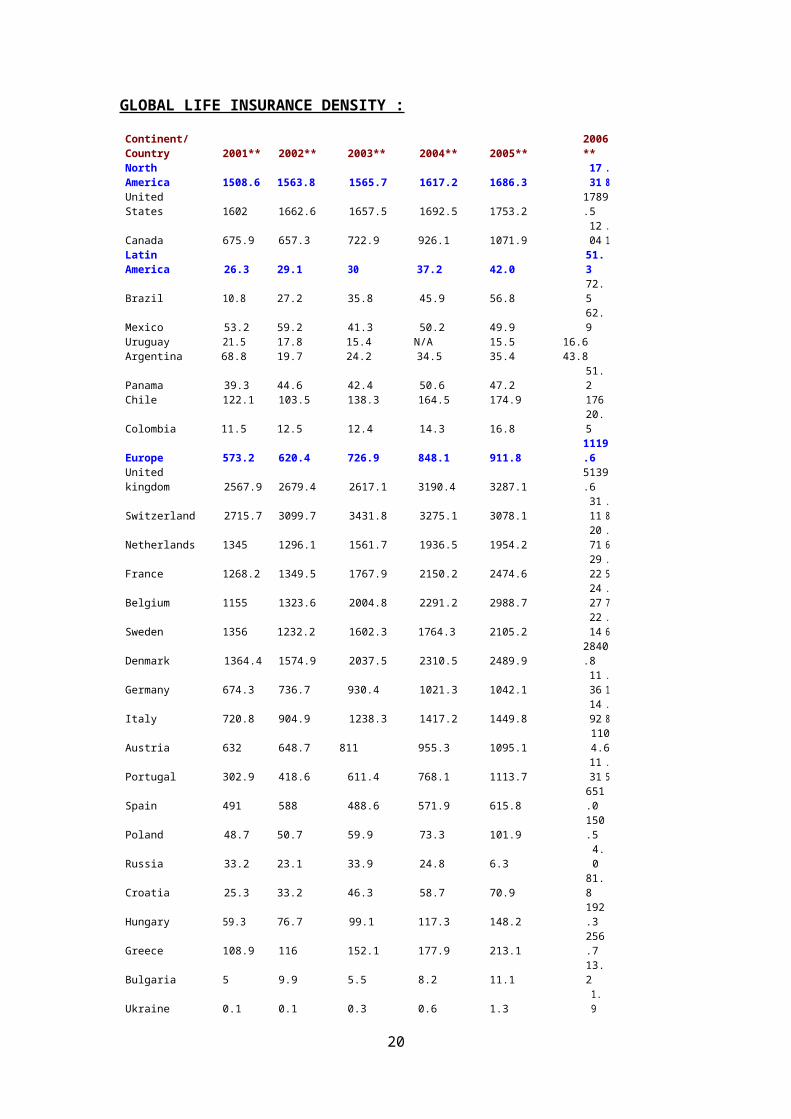

GROWTH OF LIFE BUSINESS IN INDIA 1914-1948

Sr1914 1930 1940 1945 1948

no

1 No of insurers 44 68 195 215 209

(a) Indian 44 68179 200 189(9179) (9302) (9043)

(b) Non-Indian - - 16 15 20

2Total No of

- 748997 1628381 2714000 3016000policies In force

(a) Indian -513925 1371963 2376000 2791000(6861) (8425) (8755) (9015)

Source Swiss Re Sigma volumes Insurance density is measured as ratio of premium to total population Data relates to calenderyears Figure in US$wwwindiainsuranceresearc

12

CHAPTER 2

RESEARCH METHODOLOGY

RESEARCH OBJECTIVES

1 To compare the performance of LIC and private insurance companies in India

2 To find out the performances of LIC and private insurance companies in each

category (size growth productivity and efficiency)

3 To compare grievance management of LIC and private insurance companies

RESEARCH DESIGN

a Type of research design Analytical Research

b Data collection Secondary Sources

c Statistical Tools Ratio Analysis

RESEARCH PROCESS

In this research my research objective was to compare the performance of LIC and Private

insurance companies For this purpose I decided the four broad categories under which I have

compared the LIC and Private insurance companies These are

1 Size

2 Growth

3 Productivity

4 Grievance Handling

Under these Broad Categories I have analyzed 13 factors which are

1 Size

Total Premium

Total Income

Size of Balance Sheet

Total number of Policies

Total number of Branches

2 Growth

Growth in Premium

Growth in Income

13

Growth in number of Policies

Growth in Market share

3 Productivity

Business per Branch

Income per Branch

New Premium per Branch

4 Grievance Handling

I have used the Secondary data of last five financial years I have collected data from the

various balance sheet of LIC and other private insurance companies web sites and in some

cases I personally met some employees of some insurance companies I tried to find out most

of the information required to compare the LIC and private insurance companies

In Analysis I have found all the required data and on the basis of performance gave the rank

to LIC and Private Insurance Companies on each factor and then points Now these Points

have been multiplied with the weightage of that factor And then after the analysis of each

factor a consolidated point table has been prepared to know that which sector is performing

better than other The Weightage for different categories are

Factors WeightageSize 25A Total Premium 5B Total Income 5C Balance Sheet Size 5

D Total No of Policies 5E Total No of Branches 5

Growth 40A First Premium 10B Growth in Income 10C Increase in No of Policies 10

D Growth in Market Share 10Productivity 15A Business per Branch 5B Income Per Branch 5

C First Premium per Branch 5Grievance Handling 20

LIMITATIONS

14

1 Could reach to a limited number of documents of different insurance companies in

regard to the management and other policies and resultant figures so as to identify

the exact cause of their lag in performance

2 Due to the limited time could not study all the insurance companies original

documents individually

3 Non-Proficiency in technical aspects of insurance companies might have hindered the

best analysis of the findings

SIGNIFICANCE OF THE STUDY

The Detailed Study has been done with the purpose of finding out the relative share of LIC

and Private Insurance in India It is useful for the people associated with the Insurance

Industry and the research associates related to the Insurance Sector in India This study will

acquaint them with the data of all the banks complied at one place along with the findings

conclusion and recommendations

15

CHAPTER 3

ANALYSIS AND INTERPRETATION

16

1 SIZE

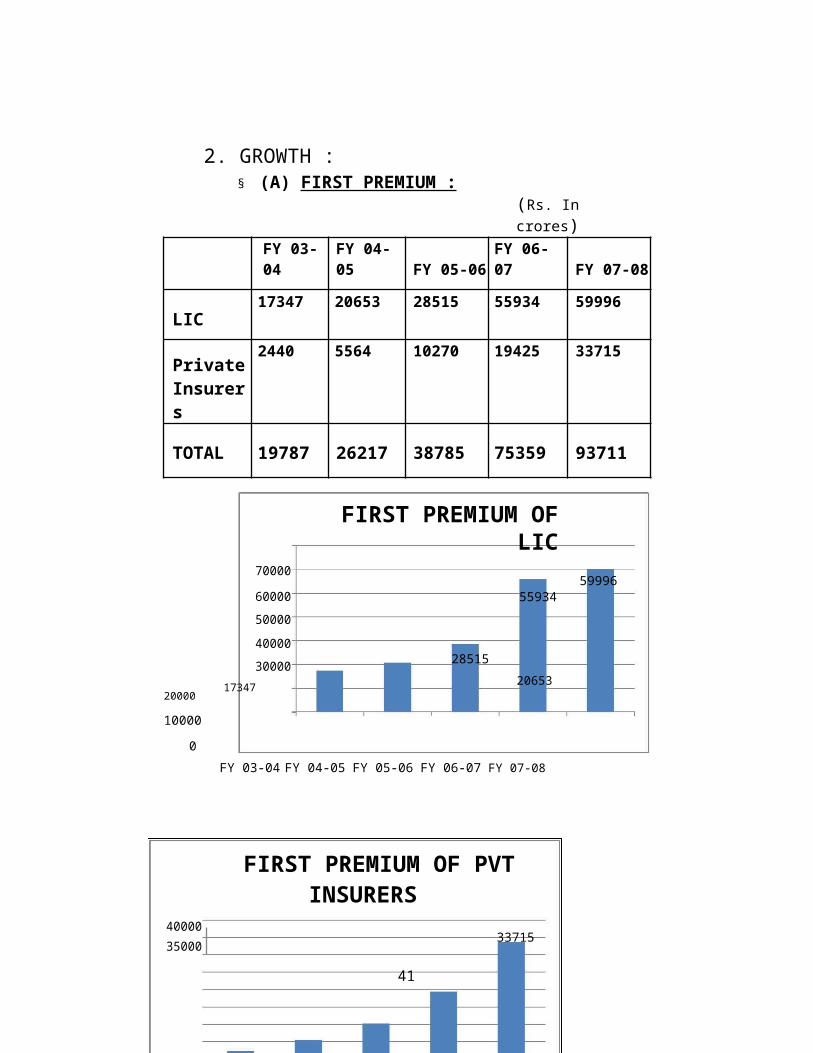

(A) TOTAL PREMIUM (Rs In crores)

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC63533 75127 90792 127822 149789

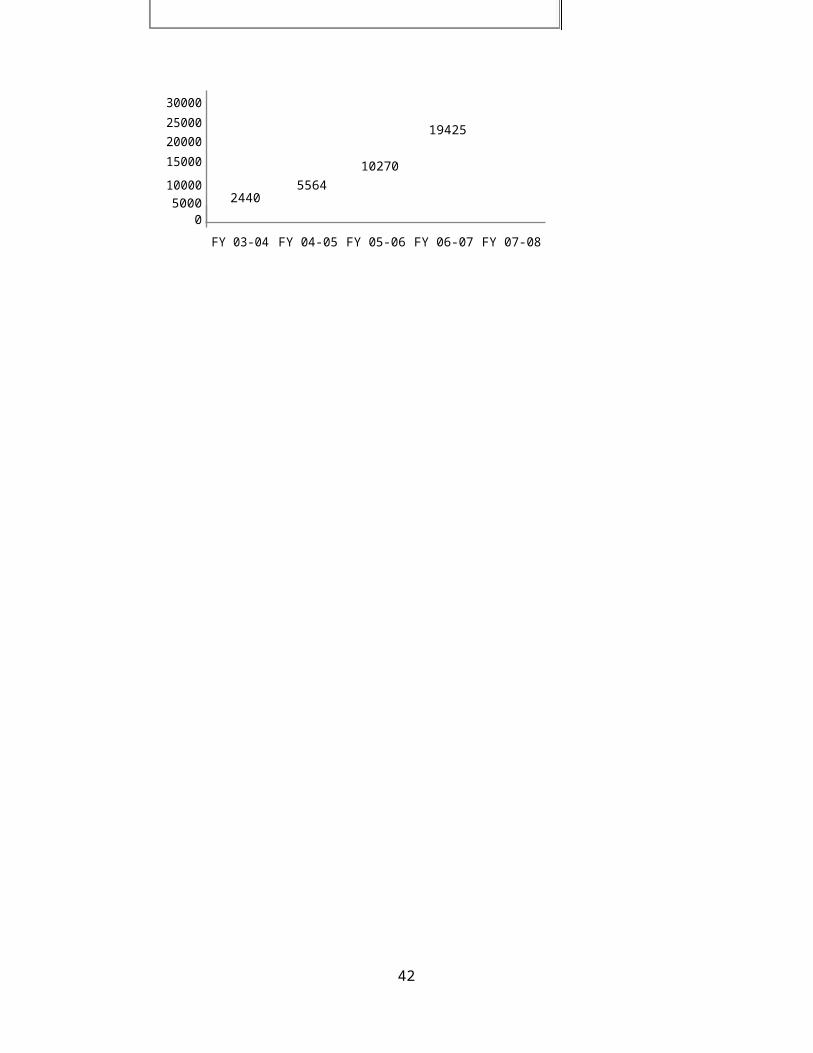

Private3120 7727 15083 28253 51561

Insurers

TOTAL66653 82854 105875 156075 201350

160000PREMIUM OF LIC

149789140000 127822120000100000 90792

7512780000 63533600004000020000

0

FY 03-04FY 04-05FY 05-06FY 06-07FY 07-08

PREMIUM OF PVT INSURERS60000

5156150000

40000

3000028253

20000 15083

10000 31207727

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

17

points after

Avg Premiummultiplying byweightage

( In Crores) Rank points (75)

LIC 101412201 1 75Private Insurance Co 2114880

2 05 375

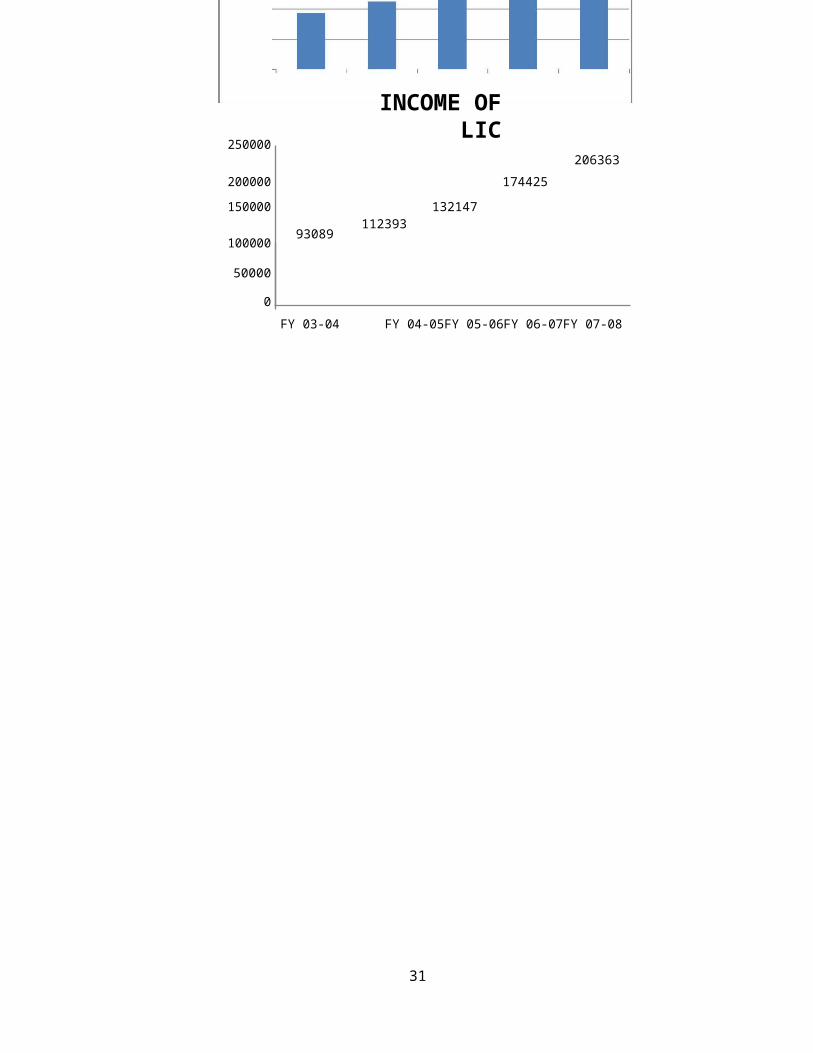

Average premium of LIC is much more than that of all insurance companies altogether LIC s average premium of the last five years is nearly five times the average premium of the all other private insurance companies

It can be said that up to that time their were less number of private players in the field of insurance but then also undoubtedly LIC is the king

All over income of LIC is much more than than of private players It is due to the fact that LIC being a government agency is being trusted by lot of companies and has large number of shares in big corporates

Total average size of balance sheet of LIC in the last five years is certainly higher than that of private insurance companies There is a huge gap in this value It is obvious that LIC has bigger balance sheet as being working in the insurance field for quite large time As compared to average balance sheet size of 40594 crores of private insurance companies LIC s average balance sheet size goes to much high as that of 5394364 crores

(D) TOTAL NUMBER OF POLICIES

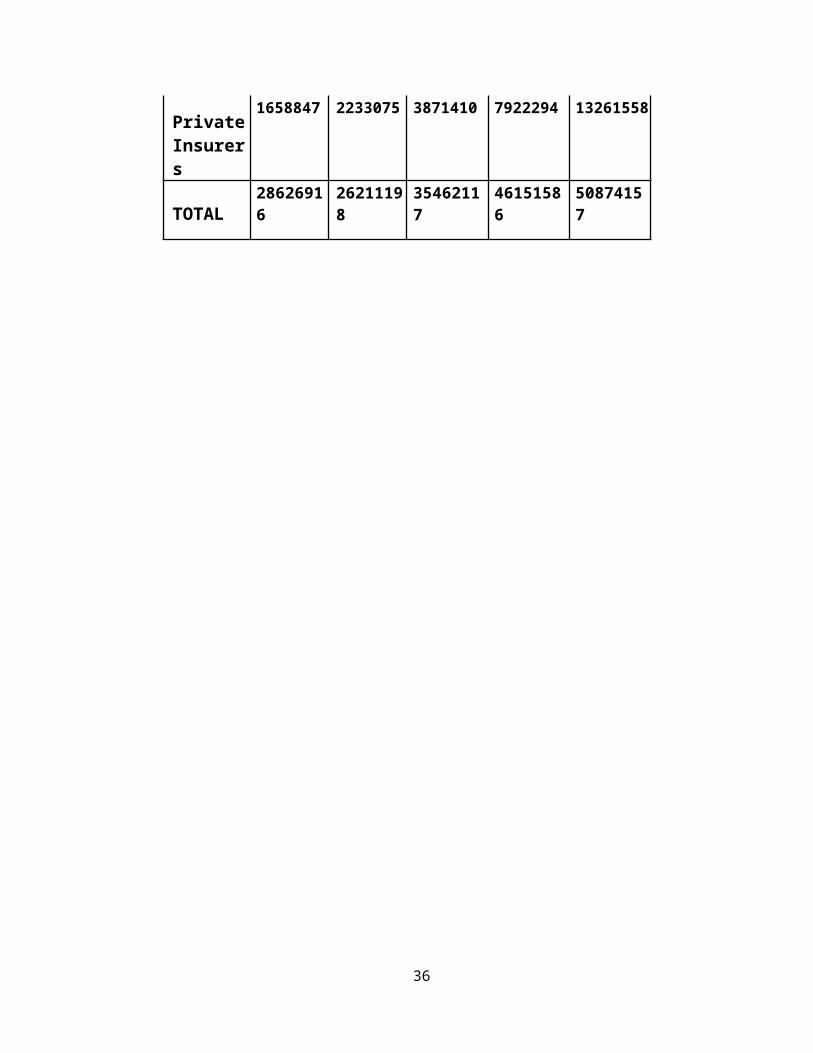

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC26968069 23978123 31590515 38229292 37612599

Private1658847 2233075 3871410 7922294 13261558

Insurers

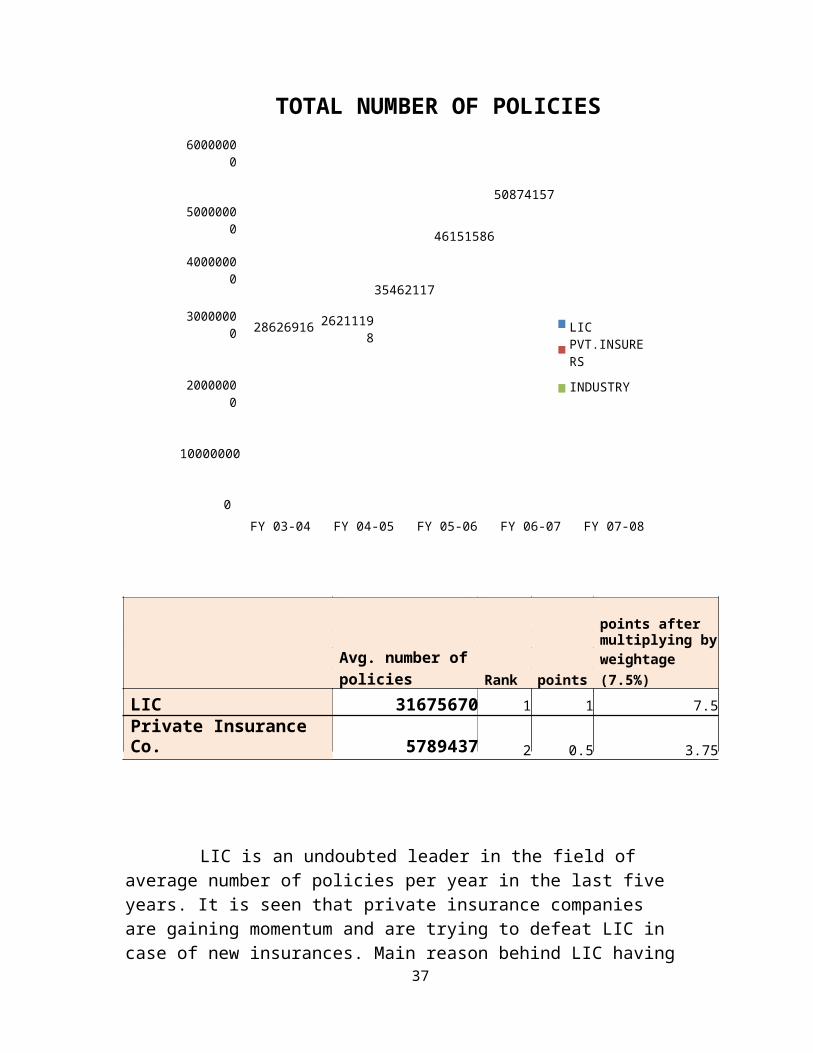

TOTAL 28626916 26211198 35462117 46151586 50874157

21

22

TOTAL NUMBER OF POLICIES60000000

5087415750000000 46151586

4000000035462117

30000000 2862691626211198

LICPVTINSURERS

20000000INDUSTRY

10000000

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

points after

Avg number ofmultiplying byweightage

policies Rank points (75)

LIC 31675670 1 1 75

Private Insurance Co 5789437 2 05 375

LIC is an undoubted leader in the field of average number of policies per year in the last five years It is seen that private insurance companies are gaining momentum and are trying to defeat LIC in case of new insurances Main reason behind LIC having such a large number of policies is the trust of a common man LIC being a government agency has got a faith of indian mass People are not yet prepared to give their savings in the hands of private players

23

24

(E) NUMBER OF BRANCHES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC2196 2197 2220 2301 2522

Private416 804 1645 3072 6391

Insurers

TOTAL 2612 3001 3865 5373 8913

100008913

9000

8000

7000 6391

6000 5373LIC

5000PVT INSURERS

40003865

30723001 INDUSTRY3000 2612 2522

2197 2220 23012196

2000 1645

1000 416804

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

growth inpoints aftermultiplying by

number of weightagebranches Rank points (75)

LIC 148 2 05 375

Private Insurance Co 1436 1 1 75

When the matter of total number of branches comes its very much obvious that LIC being the oldest existing insurance company in India has the large number of offices in the countryby any single insurance company Since the number of private insurance companies is increasing with continuous expansion in their business now the number of branches of all private players has crossed the number of branches of LIC

Growth inGrowth in First points afterPremium multiplying

First Premium (in Absoute by(in Percentage Terms) (in weightageTerms) crores) Rank points (10)

LIC 24585 426492 05 5Private Insurance Co 128176 31275

1 1 10

Though LIC has attained more growth in absolute terms ie Rs42649 crores but private players being so less in number five years back has achieved a dream come true growth of 128176 which is certainly a matter of pride for them

Income (in Absoute by(in Percentage Terms) (in weightageTerms) crores) Rank points (10)

LIC 16434 198872 05 5Private Insurance Co 95520 25714

1 1 10

Here LIC has neither attained more growth in absolute terms ie Rs19887 crores as compared to 25714 crores of private players nor has got more growth in terms of percentagethis shows that private players are doing great job in enhancing their business

(C) INCREASE IN NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC1475992 -2989946 7632584 6638585 -616693

Private804696 574228 1638335 4050884 5339264

Insurers

TOTAL 2280688 - 9270919 10689469 47225712415718

28

INCREASE IN NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC579 -1109 3175 2101 -16

Private9421 3462 7337 10464 674

Insurers

TOTAL 86 -84 353 301 102

GROWTH IN NO OF POLICIES120

10464

100 9421

80 7337674

60 LIC

403462

3175 353

PVT INSURERS

301 INDUSTRY2101

2086

102579

0FY 03-04 FY 04-05 FY 05-06 -16

FY 06-07 FY 07-08

-20 -1109 -84

Growth in Growth in points afternumber of number of multiplyingpolicies policies by(in Percentage (in Absoute weightageTerms) Terms) Rank points (10)

LIC 3947 106445302 05 5Private Insurance Co 69944 11602711

1 1 10

Private players are doing extremely well as they are increasing their customer base rapidly

29

(D) MARKET SHARE

261FY 07-08 739

FY 06-07258

742

FY 05-06265

PVT INSURERS735

LIC

FY 04-05212

788

FY 03-04123

877

0 20 40 60 80 100

LIC is still the market leader in insurance industry with 739 share But we cannot forget that in last five years market share of LIC has decreased It was 877 in year 2003-04 which came down to 739 in 2007-08

Avg business per branch of LIC is much higher than that of whole private insurance companies

32

(B) INCOME PER BRANCH

(Rs In crores)

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC4239 5116 5952 7580 8180

Private1041 1125 1147 789 823

Insurers

INCOME PER BRANCH90

81880 758

70

605952

511650 4239

40LIC

PVT INSURERS30

201041 1125 1147

82310 789

0

FY 03-04 FY 04-05 FY 05-06FY 06-07 FY 07-08

Avg Income Per points afterBranch (In multiplying bycrores) Rank points weightage (5)

LIC 621341 1 5Private Insurance Co 9864

2 05 25

Average income per branch of LIC is much more than that of private insurance companies Its almost six times the total value of all the private companies

Avg NewPremium Per points afterBranch (In multiplying bycrores) Rank points weightage (5)

LIC 156441 1 5Private Insurance Co 61242 05 25

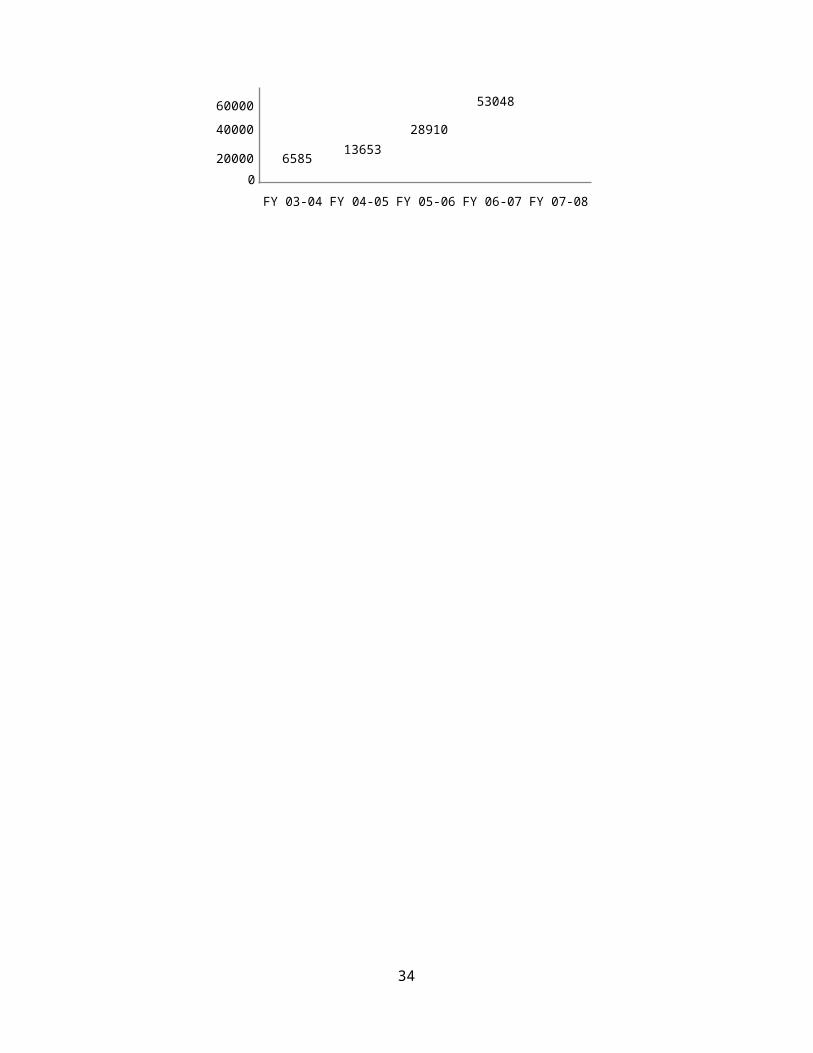

This value tells us about increase in the business of an insurance company in a period Here we see that LIC is ahead of private insurance companies in case of increasing their business

34

4 GRIEVANCE HANDLING

TOTAL NUMBER OF GRIEVANCES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC474 704 851 354 651

Private45 195 540 507 1406

Insurers

NUMBER OF GRIEVANCES RESOLVED

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC39 123 215 313 80

Private26 83 216 450 1103

Insurers

OF GRIEVANCES RESOLVED

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC82 175 253 884 122

Private577 426 400 887 784

Insurers

35

GRIEVANCES IN LIC800 704

651700540600 507

500 474 450

400 TOTAL300 216

RESOLVED200 12380

100 390

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

GRIEVANCES IN PVT COMPANIES1600 14061400

1200 1103

1000

800540 507

TOTAL

600 450 RESOLVED400 195 216200 45

26 83

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

OF GRIEVANCES RESOLVED100

88884790

78480

70

60 577

50 426 40 LIC40

253PVT INSURERS

30

20 175122

8210

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

36

points after

Grievancesmultiplying byweightage

resolved Rank points (75)

LIC 25372 05 375Private Insurance Co 6970

1 1 75

Grievance Handling is one of the major issues in any organization It plays an

important role in Insurance sector People do attract towards companies who

handles their grievances

Here we see that private players are much ahead of LIC when the matter comes to grievance management In the last five years LIC has resolved only 2537 of cases brought in front of them while the percentage of cases resolved in case of private players is 697

This shows that private players are very serious about their image and are

working hard to provide the solution of the problems of the people as early as

possible

37

TOTAL POINTS TABLE

PrivateInsurance

Factors LIC Companies

Size

A Total Premium75 375

75 375B Total Income

75 375C Balance Sheet Size

75 375D Total No of Policies

375 75E Total No of Branches

Growth

A First Premium5 10

5 10B Growth in Income

5 10C Increase in No of Policies

10 5D Market Share

Productivity

A Business per Branch5 25

5 25B Income Per Branch

5 25C First Premium per Branch

Grievance Handling 375 75

Total Score 7775 7275

38

39

CHAPTER 4

FINDINGS amp CONCLUSIONS

LIC is the giant of the insurance sector The overall size of LIC is much more than

that of all private insurance companies Private insurers are in expansion mode and

are increasing their size but are still much behind LIC Total premium deposits in

LIC is much higher than the private insurance companies Total premium of LIC in

FY 07-08 was 149789 crores which three times more than that of private insurance

companies

Income of LIC is much greater than private insurance companies Last year total

income from investments of LIC was 4824414 crores which was nearly equal to the

total income of the all private insurance companies By this we can imagine how big

the LIC is

Size of balance sheet of private insurance companies are lagging much behind LIC

Balance sheet of LIC is seven times bigger than that of private insurance companies

If we see the total number of policies issued by LIC and private insurance companies

we find that there is a huge gap between them No doubt that LIC is a well established

player in the field of insurance and many private companies have just started their

business Hence it is obvious that LIC is having large number of policyholders

Number of branches of private insurance companies is increasing as the new players

are entering in this market Also the established players are in expansion phase and

hence are expanding there business There are many private insurance companies and

hence there total number of branches has gone past LIC in the last financial year But

offices of private insurance companies are mostly in urban areas and still it is LIC

which covers most of the area

Hence we see that LIC is leading when it comes to size It is giant in insurance

sector having huge network and customer base

40

We see that due to excellent service quality and attractive offers private insurance

companies have started getting a number of customers They are growing rapidly

Though LIC is also increasing its customer base but private insurance companies are

moving at a fast pace

Though the income of private insurance companies is negligible when compared with

LIC but then also the pace with which they are increasing their income is tremendous

Private insurance companies are expanding their business and will certainly going to

give a tough competition to LIC in the coming days

LIC is certainly having a large customer base Private insurance companies are not

having that much number of customer base but they are increasing it rapidly They

have registered a decent growth of 10464 in number of new policies in the year

2006-07 Last year also their growth rate was 674

64

LIC being the oldest player in the existing insurance market has the biggest market

share of 739 which was 873 five years earlier We see that private insurance

companies are penetrating in the customer base of LIC

Overall we can see that private insurance companies are giving a tough

competition to the LIC and will certainly create a good business for themselves

in the coming days

There are many new entrants in this sector There are many private insurance

companies who have reported loss in this and previous years This is the main reason

why private insurance companies lag behind LIC in case of business per branch

There is a big difference between them

Same is the case when it comes to income per branch LIC is much ahead of private

insurance companies in this field They are undoubted champions in insurance when it

comes to profit earning

New business is increasingly going towards private insurance companies but still the

customer base of LIC is very strong In issuing new policies per branch also they are

ahead of private insurance companies though not by very large margin

Customer base of LIC is very strong and still business per branch profit per

branch or premium per branch they are leading much ahead of private

insurance companies

41

LIC has not shown their good concern when the matter of grievance handling comes

Private insurance companies are far ahead in this matter LIC has just resolved 25

cases in the last five years while private insurance companies have resolved nearly

70 cases This is a matter from where customer shift starts We have seen the rapid

increase in customer base of private insurance companies which can be very much

affected by this factor

Overall we have seen that still LIC is very famous but private insurance companies are

growing at exceptionally fast pace Private companies show due concern in grievance

management and brings innovative schemes to attract the customers Right now they

are giving good competition to LIC and very soon they will give very tough competition

to Life Corporation of India

42

CHAPTER 3

PREMIUM OF PVT INSURERS

INCOME OF PVT INSURERS

BALANCE SHEET SIZE OF LIC

800000

BALANCE SHEET SIZE OF PVT

INSURERS

TOTAL NUMBER OF POLICIES

FIRST PREMIUM OF PVT

INSURERS

NEW PREMIUM PER BRANCH

TOTAL NUMBER OF GRIEVANCES

NUMBER OF GRIEVANCES RESOLVED

GRIEVANCES IN LIC

GRIEVANCES IN PVT COMPANIES

TOTAL POINTS TABLE

family needs and so he has to keep aside something regularly for a rainy day and for

his old age This fundamental need for security for self and dependents proved to be

the mother of invention of the institution of life insurance

What is Insurance

The business of insurance is related to the protection of the economic values of assets Every

asset has a value The asset would have been created through the efforts of the owner The

asset is valuable to the owner because he expects to get some benefit from it The benefit

may be an income or some thing else It is a benefit because it meets some of his needs In the

case of a factory or a cow the product generated by is sold and income generated In the case

of a motor car it provides comfort and convenience in transportation There is no direct

income

Every asset is expected to last for a certain period of time during which it will perform After

that the benefit may not be available There is a life-time for a machine in a factory or a cow

or a motor car None of them will last for ever The owner is aware of this and he can so

manage his affairs that by the end of that period or life-time a substitute is made available

Thus he makes sure that the value or income is not lost However the asset may get lost

earlier An accident or some other unfortunate event may destroy it or make it non-functional

In that case the owner and those deriving benefits from there would be deprived of the

benefit and the planned substitute would not have been ready There is an adverse or

unpleasant situation Insurance is a mechanism that helps to reduce the effect of such adverse

situations

Insurance in law and economics is a form of risk management primarily used to hedge

against the risk of a contingent loss Insurance is defined as the equitable transfer of the risk

of a potential loss from one entity to another in exchange for a premium Insurer in

economics is the company that sells the insurance Insurance rate is a factor used to

determine the amount called the premium to be charged for a certain amount of insurance

coverage Risk management the practice of appraising and controlling risk has evolved as a

discrete field of study and practice

2

PROGRESS IN INSURANCE BUSINESS

The growth of Life Insurance in concrete terms could be said to being during the first two

decades of twentieth century when most of the major companies were founded They grew in

terms of rise in the number of companies in terms of number of policies and sum assured as

well as total life fund Indian Insurance Year Book published for the first time in 1914 gives

the figure of the total business-in -force as 2244 crore which grew to Rs 298 crore in 1938

In 1914 there were only 44companies transacting insurance business in India and during the

next 25 years their number rose to 176 The total progress on all the primary heads viz life

fund (Rs 5050 crore) premium income (Rs 1050 crore) and new business (Rs 4330 crore)

indicate that Indian Insurance Business had been making a definite headway during this

years The inter-war -years thus saw rapid growth life insurance in India

The promotion of new life insurance companies continued to be almost a craze and insurance

companies mushroomed In this period 176 insurance companies were formed and many of

them failed Thus unhealthy growth was harmful to the interest of the policy holders and

insurance business in India Feeling concerned about it the All India Life Assurance Offices

Association urged upon the Government in 1932 to undertake the insurance legislation to

(a) Compulsorily register all Life Insurance companies

(b) Secure a deposit of Rs2 lakh from all Life Insurance companies

(c) Compel foreign companies doing business in India to keep sufficient funds in

India securities to meet their liabilities under all policies issued in India

GROWTH OF LIFE BUSINESS IN INDIA 1914-1948

Sr1914 1930 1940 1945 1948

no

1 No of insurers 44 68 195 215 209

(a) Indian 44 68179 200 189(9179) (9302) (9043)

(b) Non-Indian - - 16 15 20

2Total No of

- 748997 1628381 2714000 3016000policies In force

(a) Indian -513925 1371963 2376000 2791000(6861) (8425) (8755) (9015)

Source Swiss Re Sigma volumes Insurance density is measured as ratio of premium to total population Data relates to calenderyears Figure in US$wwwindiainsuranceresearc

12

CHAPTER 2

RESEARCH METHODOLOGY

RESEARCH OBJECTIVES

1 To compare the performance of LIC and private insurance companies in India

2 To find out the performances of LIC and private insurance companies in each

category (size growth productivity and efficiency)

3 To compare grievance management of LIC and private insurance companies

RESEARCH DESIGN

a Type of research design Analytical Research

b Data collection Secondary Sources

c Statistical Tools Ratio Analysis

RESEARCH PROCESS

In this research my research objective was to compare the performance of LIC and Private

insurance companies For this purpose I decided the four broad categories under which I have

compared the LIC and Private insurance companies These are

1 Size

2 Growth

3 Productivity

4 Grievance Handling

Under these Broad Categories I have analyzed 13 factors which are

1 Size

Total Premium

Total Income

Size of Balance Sheet

Total number of Policies

Total number of Branches

2 Growth

Growth in Premium

Growth in Income

13

Growth in number of Policies

Growth in Market share

3 Productivity

Business per Branch

Income per Branch

New Premium per Branch

4 Grievance Handling

I have used the Secondary data of last five financial years I have collected data from the

various balance sheet of LIC and other private insurance companies web sites and in some

cases I personally met some employees of some insurance companies I tried to find out most

of the information required to compare the LIC and private insurance companies

In Analysis I have found all the required data and on the basis of performance gave the rank

to LIC and Private Insurance Companies on each factor and then points Now these Points

have been multiplied with the weightage of that factor And then after the analysis of each

factor a consolidated point table has been prepared to know that which sector is performing

better than other The Weightage for different categories are

Factors WeightageSize 25A Total Premium 5B Total Income 5C Balance Sheet Size 5

D Total No of Policies 5E Total No of Branches 5

Growth 40A First Premium 10B Growth in Income 10C Increase in No of Policies 10

D Growth in Market Share 10Productivity 15A Business per Branch 5B Income Per Branch 5

C First Premium per Branch 5Grievance Handling 20

LIMITATIONS

14

1 Could reach to a limited number of documents of different insurance companies in

regard to the management and other policies and resultant figures so as to identify

the exact cause of their lag in performance

2 Due to the limited time could not study all the insurance companies original

documents individually

3 Non-Proficiency in technical aspects of insurance companies might have hindered the

best analysis of the findings

SIGNIFICANCE OF THE STUDY

The Detailed Study has been done with the purpose of finding out the relative share of LIC

and Private Insurance in India It is useful for the people associated with the Insurance

Industry and the research associates related to the Insurance Sector in India This study will

acquaint them with the data of all the banks complied at one place along with the findings

conclusion and recommendations

15

CHAPTER 3

ANALYSIS AND INTERPRETATION

16

1 SIZE

(A) TOTAL PREMIUM (Rs In crores)

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC63533 75127 90792 127822 149789

Private3120 7727 15083 28253 51561

Insurers

TOTAL66653 82854 105875 156075 201350

160000PREMIUM OF LIC

149789140000 127822120000100000 90792

7512780000 63533600004000020000

0

FY 03-04FY 04-05FY 05-06FY 06-07FY 07-08

PREMIUM OF PVT INSURERS60000

5156150000

40000

3000028253

20000 15083

10000 31207727

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

17

points after

Avg Premiummultiplying byweightage

( In Crores) Rank points (75)

LIC 101412201 1 75Private Insurance Co 2114880

2 05 375

Average premium of LIC is much more than that of all insurance companies altogether LIC s average premium of the last five years is nearly five times the average premium of the all other private insurance companies

It can be said that up to that time their were less number of private players in the field of insurance but then also undoubtedly LIC is the king

All over income of LIC is much more than than of private players It is due to the fact that LIC being a government agency is being trusted by lot of companies and has large number of shares in big corporates

Total average size of balance sheet of LIC in the last five years is certainly higher than that of private insurance companies There is a huge gap in this value It is obvious that LIC has bigger balance sheet as being working in the insurance field for quite large time As compared to average balance sheet size of 40594 crores of private insurance companies LIC s average balance sheet size goes to much high as that of 5394364 crores

(D) TOTAL NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC26968069 23978123 31590515 38229292 37612599

Private1658847 2233075 3871410 7922294 13261558

Insurers

TOTAL 28626916 26211198 35462117 46151586 50874157

21

22

TOTAL NUMBER OF POLICIES60000000

5087415750000000 46151586

4000000035462117

30000000 2862691626211198

LICPVTINSURERS

20000000INDUSTRY

10000000

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

points after

Avg number ofmultiplying byweightage

policies Rank points (75)

LIC 31675670 1 1 75

Private Insurance Co 5789437 2 05 375

LIC is an undoubted leader in the field of average number of policies per year in the last five years It is seen that private insurance companies are gaining momentum and are trying to defeat LIC in case of new insurances Main reason behind LIC having such a large number of policies is the trust of a common man LIC being a government agency has got a faith of indian mass People are not yet prepared to give their savings in the hands of private players

23

24

(E) NUMBER OF BRANCHES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC2196 2197 2220 2301 2522

Private416 804 1645 3072 6391

Insurers

TOTAL 2612 3001 3865 5373 8913

100008913

9000

8000

7000 6391

6000 5373LIC

5000PVT INSURERS

40003865

30723001 INDUSTRY3000 2612 2522

2197 2220 23012196

2000 1645

1000 416804

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

growth inpoints aftermultiplying by

number of weightagebranches Rank points (75)

LIC 148 2 05 375

Private Insurance Co 1436 1 1 75

When the matter of total number of branches comes its very much obvious that LIC being the oldest existing insurance company in India has the large number of offices in the countryby any single insurance company Since the number of private insurance companies is increasing with continuous expansion in their business now the number of branches of all private players has crossed the number of branches of LIC

Growth inGrowth in First points afterPremium multiplying

First Premium (in Absoute by(in Percentage Terms) (in weightageTerms) crores) Rank points (10)

LIC 24585 426492 05 5Private Insurance Co 128176 31275

1 1 10

Though LIC has attained more growth in absolute terms ie Rs42649 crores but private players being so less in number five years back has achieved a dream come true growth of 128176 which is certainly a matter of pride for them

Income (in Absoute by(in Percentage Terms) (in weightageTerms) crores) Rank points (10)

LIC 16434 198872 05 5Private Insurance Co 95520 25714

1 1 10

Here LIC has neither attained more growth in absolute terms ie Rs19887 crores as compared to 25714 crores of private players nor has got more growth in terms of percentagethis shows that private players are doing great job in enhancing their business

(C) INCREASE IN NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC1475992 -2989946 7632584 6638585 -616693

Private804696 574228 1638335 4050884 5339264

Insurers

TOTAL 2280688 - 9270919 10689469 47225712415718

28

INCREASE IN NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC579 -1109 3175 2101 -16

Private9421 3462 7337 10464 674

Insurers

TOTAL 86 -84 353 301 102

GROWTH IN NO OF POLICIES120

10464

100 9421

80 7337674

60 LIC

403462

3175 353

PVT INSURERS

301 INDUSTRY2101

2086

102579

0FY 03-04 FY 04-05 FY 05-06 -16

FY 06-07 FY 07-08

-20 -1109 -84

Growth in Growth in points afternumber of number of multiplyingpolicies policies by(in Percentage (in Absoute weightageTerms) Terms) Rank points (10)

LIC 3947 106445302 05 5Private Insurance Co 69944 11602711

1 1 10

Private players are doing extremely well as they are increasing their customer base rapidly

29

(D) MARKET SHARE

261FY 07-08 739

FY 06-07258

742

FY 05-06265

PVT INSURERS735

LIC

FY 04-05212

788

FY 03-04123

877

0 20 40 60 80 100

LIC is still the market leader in insurance industry with 739 share But we cannot forget that in last five years market share of LIC has decreased It was 877 in year 2003-04 which came down to 739 in 2007-08

Avg business per branch of LIC is much higher than that of whole private insurance companies

32

(B) INCOME PER BRANCH

(Rs In crores)

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC4239 5116 5952 7580 8180

Private1041 1125 1147 789 823

Insurers

INCOME PER BRANCH90

81880 758

70

605952

511650 4239

40LIC

PVT INSURERS30

201041 1125 1147

82310 789

0

FY 03-04 FY 04-05 FY 05-06FY 06-07 FY 07-08

Avg Income Per points afterBranch (In multiplying bycrores) Rank points weightage (5)

LIC 621341 1 5Private Insurance Co 9864

2 05 25

Average income per branch of LIC is much more than that of private insurance companies Its almost six times the total value of all the private companies

Avg NewPremium Per points afterBranch (In multiplying bycrores) Rank points weightage (5)

LIC 156441 1 5Private Insurance Co 61242 05 25

This value tells us about increase in the business of an insurance company in a period Here we see that LIC is ahead of private insurance companies in case of increasing their business

34

4 GRIEVANCE HANDLING

TOTAL NUMBER OF GRIEVANCES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC474 704 851 354 651

Private45 195 540 507 1406

Insurers

NUMBER OF GRIEVANCES RESOLVED

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC39 123 215 313 80

Private26 83 216 450 1103

Insurers

OF GRIEVANCES RESOLVED

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC82 175 253 884 122

Private577 426 400 887 784

Insurers

35

GRIEVANCES IN LIC800 704

651700540600 507

500 474 450

400 TOTAL300 216

RESOLVED200 12380

100 390

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

GRIEVANCES IN PVT COMPANIES1600 14061400

1200 1103

1000

800540 507

TOTAL

600 450 RESOLVED400 195 216200 45

26 83

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

OF GRIEVANCES RESOLVED100

88884790

78480

70

60 577

50 426 40 LIC40

253PVT INSURERS

30

20 175122

8210

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

36

points after

Grievancesmultiplying byweightage

resolved Rank points (75)

LIC 25372 05 375Private Insurance Co 6970

1 1 75

Grievance Handling is one of the major issues in any organization It plays an

important role in Insurance sector People do attract towards companies who

handles their grievances

Here we see that private players are much ahead of LIC when the matter comes to grievance management In the last five years LIC has resolved only 2537 of cases brought in front of them while the percentage of cases resolved in case of private players is 697

This shows that private players are very serious about their image and are

working hard to provide the solution of the problems of the people as early as

possible

37

TOTAL POINTS TABLE

PrivateInsurance

Factors LIC Companies

Size

A Total Premium75 375

75 375B Total Income

75 375C Balance Sheet Size

75 375D Total No of Policies

375 75E Total No of Branches

Growth

A First Premium5 10

5 10B Growth in Income

5 10C Increase in No of Policies

10 5D Market Share

Productivity

A Business per Branch5 25

5 25B Income Per Branch

5 25C First Premium per Branch

Grievance Handling 375 75

Total Score 7775 7275

38

39

CHAPTER 4

FINDINGS amp CONCLUSIONS

LIC is the giant of the insurance sector The overall size of LIC is much more than

that of all private insurance companies Private insurers are in expansion mode and

are increasing their size but are still much behind LIC Total premium deposits in

LIC is much higher than the private insurance companies Total premium of LIC in

FY 07-08 was 149789 crores which three times more than that of private insurance

companies

Income of LIC is much greater than private insurance companies Last year total

income from investments of LIC was 4824414 crores which was nearly equal to the

total income of the all private insurance companies By this we can imagine how big

the LIC is

Size of balance sheet of private insurance companies are lagging much behind LIC

Balance sheet of LIC is seven times bigger than that of private insurance companies

If we see the total number of policies issued by LIC and private insurance companies

we find that there is a huge gap between them No doubt that LIC is a well established

player in the field of insurance and many private companies have just started their

business Hence it is obvious that LIC is having large number of policyholders

Number of branches of private insurance companies is increasing as the new players

are entering in this market Also the established players are in expansion phase and

hence are expanding there business There are many private insurance companies and

hence there total number of branches has gone past LIC in the last financial year But

offices of private insurance companies are mostly in urban areas and still it is LIC

which covers most of the area

Hence we see that LIC is leading when it comes to size It is giant in insurance

sector having huge network and customer base

40

We see that due to excellent service quality and attractive offers private insurance

companies have started getting a number of customers They are growing rapidly

Though LIC is also increasing its customer base but private insurance companies are

moving at a fast pace

Though the income of private insurance companies is negligible when compared with

LIC but then also the pace with which they are increasing their income is tremendous

Private insurance companies are expanding their business and will certainly going to

give a tough competition to LIC in the coming days

LIC is certainly having a large customer base Private insurance companies are not

having that much number of customer base but they are increasing it rapidly They

have registered a decent growth of 10464 in number of new policies in the year

2006-07 Last year also their growth rate was 674

64

LIC being the oldest player in the existing insurance market has the biggest market

share of 739 which was 873 five years earlier We see that private insurance

companies are penetrating in the customer base of LIC

Overall we can see that private insurance companies are giving a tough

competition to the LIC and will certainly create a good business for themselves

in the coming days

There are many new entrants in this sector There are many private insurance

companies who have reported loss in this and previous years This is the main reason

why private insurance companies lag behind LIC in case of business per branch

There is a big difference between them

Same is the case when it comes to income per branch LIC is much ahead of private

insurance companies in this field They are undoubted champions in insurance when it

comes to profit earning

New business is increasingly going towards private insurance companies but still the

customer base of LIC is very strong In issuing new policies per branch also they are

ahead of private insurance companies though not by very large margin

Customer base of LIC is very strong and still business per branch profit per

branch or premium per branch they are leading much ahead of private

insurance companies

41

LIC has not shown their good concern when the matter of grievance handling comes

Private insurance companies are far ahead in this matter LIC has just resolved 25

cases in the last five years while private insurance companies have resolved nearly

70 cases This is a matter from where customer shift starts We have seen the rapid

increase in customer base of private insurance companies which can be very much

affected by this factor

Overall we have seen that still LIC is very famous but private insurance companies are

growing at exceptionally fast pace Private companies show due concern in grievance

management and brings innovative schemes to attract the customers Right now they

are giving good competition to LIC and very soon they will give very tough competition

to Life Corporation of India

42

CHAPTER 3

PREMIUM OF PVT INSURERS

INCOME OF PVT INSURERS

BALANCE SHEET SIZE OF LIC

800000

BALANCE SHEET SIZE OF PVT

INSURERS

TOTAL NUMBER OF POLICIES

FIRST PREMIUM OF PVT

INSURERS

NEW PREMIUM PER BRANCH

TOTAL NUMBER OF GRIEVANCES

NUMBER OF GRIEVANCES RESOLVED

GRIEVANCES IN LIC

GRIEVANCES IN PVT COMPANIES

TOTAL POINTS TABLE

PROGRESS IN INSURANCE BUSINESS

The growth of Life Insurance in concrete terms could be said to being during the first two

decades of twentieth century when most of the major companies were founded They grew in

terms of rise in the number of companies in terms of number of policies and sum assured as

well as total life fund Indian Insurance Year Book published for the first time in 1914 gives

the figure of the total business-in -force as 2244 crore which grew to Rs 298 crore in 1938

In 1914 there were only 44companies transacting insurance business in India and during the

next 25 years their number rose to 176 The total progress on all the primary heads viz life

fund (Rs 5050 crore) premium income (Rs 1050 crore) and new business (Rs 4330 crore)

indicate that Indian Insurance Business had been making a definite headway during this

years The inter-war -years thus saw rapid growth life insurance in India

The promotion of new life insurance companies continued to be almost a craze and insurance

companies mushroomed In this period 176 insurance companies were formed and many of

them failed Thus unhealthy growth was harmful to the interest of the policy holders and

insurance business in India Feeling concerned about it the All India Life Assurance Offices

Association urged upon the Government in 1932 to undertake the insurance legislation to

(a) Compulsorily register all Life Insurance companies

(b) Secure a deposit of Rs2 lakh from all Life Insurance companies

(c) Compel foreign companies doing business in India to keep sufficient funds in

India securities to meet their liabilities under all policies issued in India

GROWTH OF LIFE BUSINESS IN INDIA 1914-1948

Sr1914 1930 1940 1945 1948

no

1 No of insurers 44 68 195 215 209

(a) Indian 44 68179 200 189(9179) (9302) (9043)

(b) Non-Indian - - 16 15 20

2Total No of

- 748997 1628381 2714000 3016000policies In force

(a) Indian -513925 1371963 2376000 2791000(6861) (8425) (8755) (9015)

Source Swiss Re Sigma volumes Insurance density is measured as ratio of premium to total population Data relates to calenderyears Figure in US$wwwindiainsuranceresearc

12

CHAPTER 2

RESEARCH METHODOLOGY

RESEARCH OBJECTIVES

1 To compare the performance of LIC and private insurance companies in India

2 To find out the performances of LIC and private insurance companies in each

category (size growth productivity and efficiency)

3 To compare grievance management of LIC and private insurance companies

RESEARCH DESIGN

a Type of research design Analytical Research

b Data collection Secondary Sources

c Statistical Tools Ratio Analysis

RESEARCH PROCESS

In this research my research objective was to compare the performance of LIC and Private

insurance companies For this purpose I decided the four broad categories under which I have

compared the LIC and Private insurance companies These are

1 Size

2 Growth

3 Productivity

4 Grievance Handling

Under these Broad Categories I have analyzed 13 factors which are

1 Size

Total Premium

Total Income

Size of Balance Sheet

Total number of Policies

Total number of Branches

2 Growth

Growth in Premium

Growth in Income

13

Growth in number of Policies

Growth in Market share

3 Productivity

Business per Branch

Income per Branch

New Premium per Branch

4 Grievance Handling

I have used the Secondary data of last five financial years I have collected data from the

various balance sheet of LIC and other private insurance companies web sites and in some

cases I personally met some employees of some insurance companies I tried to find out most

of the information required to compare the LIC and private insurance companies

In Analysis I have found all the required data and on the basis of performance gave the rank

to LIC and Private Insurance Companies on each factor and then points Now these Points

have been multiplied with the weightage of that factor And then after the analysis of each

factor a consolidated point table has been prepared to know that which sector is performing

better than other The Weightage for different categories are

Factors WeightageSize 25A Total Premium 5B Total Income 5C Balance Sheet Size 5

D Total No of Policies 5E Total No of Branches 5

Growth 40A First Premium 10B Growth in Income 10C Increase in No of Policies 10

D Growth in Market Share 10Productivity 15A Business per Branch 5B Income Per Branch 5

C First Premium per Branch 5Grievance Handling 20

LIMITATIONS

14

1 Could reach to a limited number of documents of different insurance companies in

regard to the management and other policies and resultant figures so as to identify

the exact cause of their lag in performance

2 Due to the limited time could not study all the insurance companies original

documents individually

3 Non-Proficiency in technical aspects of insurance companies might have hindered the

best analysis of the findings

SIGNIFICANCE OF THE STUDY

The Detailed Study has been done with the purpose of finding out the relative share of LIC

and Private Insurance in India It is useful for the people associated with the Insurance

Industry and the research associates related to the Insurance Sector in India This study will

acquaint them with the data of all the banks complied at one place along with the findings

conclusion and recommendations

15

CHAPTER 3

ANALYSIS AND INTERPRETATION

16

1 SIZE

(A) TOTAL PREMIUM (Rs In crores)

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC63533 75127 90792 127822 149789

Private3120 7727 15083 28253 51561

Insurers

TOTAL66653 82854 105875 156075 201350

160000PREMIUM OF LIC

149789140000 127822120000100000 90792

7512780000 63533600004000020000

0

FY 03-04FY 04-05FY 05-06FY 06-07FY 07-08

PREMIUM OF PVT INSURERS60000

5156150000

40000

3000028253

20000 15083

10000 31207727

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

17

points after

Avg Premiummultiplying byweightage

( In Crores) Rank points (75)

LIC 101412201 1 75Private Insurance Co 2114880

2 05 375

Average premium of LIC is much more than that of all insurance companies altogether LIC s average premium of the last five years is nearly five times the average premium of the all other private insurance companies

It can be said that up to that time their were less number of private players in the field of insurance but then also undoubtedly LIC is the king

All over income of LIC is much more than than of private players It is due to the fact that LIC being a government agency is being trusted by lot of companies and has large number of shares in big corporates

Total average size of balance sheet of LIC in the last five years is certainly higher than that of private insurance companies There is a huge gap in this value It is obvious that LIC has bigger balance sheet as being working in the insurance field for quite large time As compared to average balance sheet size of 40594 crores of private insurance companies LIC s average balance sheet size goes to much high as that of 5394364 crores

(D) TOTAL NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC26968069 23978123 31590515 38229292 37612599

Private1658847 2233075 3871410 7922294 13261558

Insurers

TOTAL 28626916 26211198 35462117 46151586 50874157

21

22

TOTAL NUMBER OF POLICIES60000000

5087415750000000 46151586

4000000035462117

30000000 2862691626211198

LICPVTINSURERS

20000000INDUSTRY

10000000

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

points after

Avg number ofmultiplying byweightage

policies Rank points (75)

LIC 31675670 1 1 75

Private Insurance Co 5789437 2 05 375

LIC is an undoubted leader in the field of average number of policies per year in the last five years It is seen that private insurance companies are gaining momentum and are trying to defeat LIC in case of new insurances Main reason behind LIC having such a large number of policies is the trust of a common man LIC being a government agency has got a faith of indian mass People are not yet prepared to give their savings in the hands of private players

23

24

(E) NUMBER OF BRANCHES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC2196 2197 2220 2301 2522

Private416 804 1645 3072 6391

Insurers

TOTAL 2612 3001 3865 5373 8913

100008913

9000

8000

7000 6391

6000 5373LIC

5000PVT INSURERS

40003865

30723001 INDUSTRY3000 2612 2522

2197 2220 23012196

2000 1645

1000 416804

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

growth inpoints aftermultiplying by

number of weightagebranches Rank points (75)

LIC 148 2 05 375

Private Insurance Co 1436 1 1 75

When the matter of total number of branches comes its very much obvious that LIC being the oldest existing insurance company in India has the large number of offices in the countryby any single insurance company Since the number of private insurance companies is increasing with continuous expansion in their business now the number of branches of all private players has crossed the number of branches of LIC

Growth inGrowth in First points afterPremium multiplying

First Premium (in Absoute by(in Percentage Terms) (in weightageTerms) crores) Rank points (10)

LIC 24585 426492 05 5Private Insurance Co 128176 31275

1 1 10

Though LIC has attained more growth in absolute terms ie Rs42649 crores but private players being so less in number five years back has achieved a dream come true growth of 128176 which is certainly a matter of pride for them

Income (in Absoute by(in Percentage Terms) (in weightageTerms) crores) Rank points (10)

LIC 16434 198872 05 5Private Insurance Co 95520 25714

1 1 10

Here LIC has neither attained more growth in absolute terms ie Rs19887 crores as compared to 25714 crores of private players nor has got more growth in terms of percentagethis shows that private players are doing great job in enhancing their business

(C) INCREASE IN NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC1475992 -2989946 7632584 6638585 -616693

Private804696 574228 1638335 4050884 5339264

Insurers

TOTAL 2280688 - 9270919 10689469 47225712415718

28

INCREASE IN NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC579 -1109 3175 2101 -16

Private9421 3462 7337 10464 674

Insurers

TOTAL 86 -84 353 301 102

GROWTH IN NO OF POLICIES120

10464

100 9421

80 7337674

60 LIC

403462

3175 353

PVT INSURERS

301 INDUSTRY2101

2086

102579

0FY 03-04 FY 04-05 FY 05-06 -16

FY 06-07 FY 07-08

-20 -1109 -84

Growth in Growth in points afternumber of number of multiplyingpolicies policies by(in Percentage (in Absoute weightageTerms) Terms) Rank points (10)

LIC 3947 106445302 05 5Private Insurance Co 69944 11602711

1 1 10

Private players are doing extremely well as they are increasing their customer base rapidly

29

(D) MARKET SHARE

261FY 07-08 739

FY 06-07258

742

FY 05-06265

PVT INSURERS735

LIC

FY 04-05212

788

FY 03-04123

877

0 20 40 60 80 100

LIC is still the market leader in insurance industry with 739 share But we cannot forget that in last five years market share of LIC has decreased It was 877 in year 2003-04 which came down to 739 in 2007-08

Avg business per branch of LIC is much higher than that of whole private insurance companies

32

(B) INCOME PER BRANCH

(Rs In crores)

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC4239 5116 5952 7580 8180

Private1041 1125 1147 789 823

Insurers

INCOME PER BRANCH90

81880 758

70

605952

511650 4239

40LIC

PVT INSURERS30

201041 1125 1147

82310 789

0

FY 03-04 FY 04-05 FY 05-06FY 06-07 FY 07-08

Avg Income Per points afterBranch (In multiplying bycrores) Rank points weightage (5)

LIC 621341 1 5Private Insurance Co 9864

2 05 25

Average income per branch of LIC is much more than that of private insurance companies Its almost six times the total value of all the private companies

Avg NewPremium Per points afterBranch (In multiplying bycrores) Rank points weightage (5)

LIC 156441 1 5Private Insurance Co 61242 05 25

This value tells us about increase in the business of an insurance company in a period Here we see that LIC is ahead of private insurance companies in case of increasing their business

34

4 GRIEVANCE HANDLING

TOTAL NUMBER OF GRIEVANCES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC474 704 851 354 651

Private45 195 540 507 1406

Insurers

NUMBER OF GRIEVANCES RESOLVED

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC39 123 215 313 80

Private26 83 216 450 1103

Insurers

OF GRIEVANCES RESOLVED

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC82 175 253 884 122

Private577 426 400 887 784

Insurers

35

GRIEVANCES IN LIC800 704

651700540600 507

500 474 450

400 TOTAL300 216

RESOLVED200 12380

100 390

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

GRIEVANCES IN PVT COMPANIES1600 14061400

1200 1103

1000

800540 507

TOTAL

600 450 RESOLVED400 195 216200 45

26 83

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

OF GRIEVANCES RESOLVED100

88884790

78480

70

60 577

50 426 40 LIC40

253PVT INSURERS

30

20 175122

8210

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

36

points after

Grievancesmultiplying byweightage

resolved Rank points (75)

LIC 25372 05 375Private Insurance Co 6970

1 1 75

Grievance Handling is one of the major issues in any organization It plays an

important role in Insurance sector People do attract towards companies who

handles their grievances

Here we see that private players are much ahead of LIC when the matter comes to grievance management In the last five years LIC has resolved only 2537 of cases brought in front of them while the percentage of cases resolved in case of private players is 697

This shows that private players are very serious about their image and are

working hard to provide the solution of the problems of the people as early as

possible

37

TOTAL POINTS TABLE

PrivateInsurance

Factors LIC Companies

Size

A Total Premium75 375

75 375B Total Income

75 375C Balance Sheet Size

75 375D Total No of Policies

375 75E Total No of Branches

Growth

A First Premium5 10

5 10B Growth in Income

5 10C Increase in No of Policies

10 5D Market Share

Productivity

A Business per Branch5 25

5 25B Income Per Branch

5 25C First Premium per Branch

Grievance Handling 375 75

Total Score 7775 7275

38

39

CHAPTER 4

FINDINGS amp CONCLUSIONS

LIC is the giant of the insurance sector The overall size of LIC is much more than

that of all private insurance companies Private insurers are in expansion mode and

are increasing their size but are still much behind LIC Total premium deposits in

LIC is much higher than the private insurance companies Total premium of LIC in

FY 07-08 was 149789 crores which three times more than that of private insurance

companies

Income of LIC is much greater than private insurance companies Last year total

income from investments of LIC was 4824414 crores which was nearly equal to the

total income of the all private insurance companies By this we can imagine how big

the LIC is

Size of balance sheet of private insurance companies are lagging much behind LIC

Balance sheet of LIC is seven times bigger than that of private insurance companies

If we see the total number of policies issued by LIC and private insurance companies

we find that there is a huge gap between them No doubt that LIC is a well established

player in the field of insurance and many private companies have just started their

business Hence it is obvious that LIC is having large number of policyholders

Number of branches of private insurance companies is increasing as the new players

are entering in this market Also the established players are in expansion phase and

hence are expanding there business There are many private insurance companies and

hence there total number of branches has gone past LIC in the last financial year But

offices of private insurance companies are mostly in urban areas and still it is LIC

which covers most of the area

Hence we see that LIC is leading when it comes to size It is giant in insurance

sector having huge network and customer base

40

We see that due to excellent service quality and attractive offers private insurance

companies have started getting a number of customers They are growing rapidly

Though LIC is also increasing its customer base but private insurance companies are

moving at a fast pace

Though the income of private insurance companies is negligible when compared with

LIC but then also the pace with which they are increasing their income is tremendous

Private insurance companies are expanding their business and will certainly going to

give a tough competition to LIC in the coming days

LIC is certainly having a large customer base Private insurance companies are not

having that much number of customer base but they are increasing it rapidly They

have registered a decent growth of 10464 in number of new policies in the year

2006-07 Last year also their growth rate was 674

64

LIC being the oldest player in the existing insurance market has the biggest market

share of 739 which was 873 five years earlier We see that private insurance

companies are penetrating in the customer base of LIC

Overall we can see that private insurance companies are giving a tough

competition to the LIC and will certainly create a good business for themselves

in the coming days

There are many new entrants in this sector There are many private insurance

companies who have reported loss in this and previous years This is the main reason

why private insurance companies lag behind LIC in case of business per branch

There is a big difference between them

Same is the case when it comes to income per branch LIC is much ahead of private

insurance companies in this field They are undoubted champions in insurance when it

comes to profit earning

New business is increasingly going towards private insurance companies but still the

customer base of LIC is very strong In issuing new policies per branch also they are

ahead of private insurance companies though not by very large margin

Customer base of LIC is very strong and still business per branch profit per

branch or premium per branch they are leading much ahead of private

insurance companies

41

LIC has not shown their good concern when the matter of grievance handling comes

Private insurance companies are far ahead in this matter LIC has just resolved 25

cases in the last five years while private insurance companies have resolved nearly

70 cases This is a matter from where customer shift starts We have seen the rapid

increase in customer base of private insurance companies which can be very much

affected by this factor

Overall we have seen that still LIC is very famous but private insurance companies are

growing at exceptionally fast pace Private companies show due concern in grievance

management and brings innovative schemes to attract the customers Right now they

are giving good competition to LIC and very soon they will give very tough competition

Source Swiss Re Sigma volumes Insurance density is measured as ratio of premium to total population Data relates to calenderyears Figure in US$wwwindiainsuranceresearc

12

CHAPTER 2

RESEARCH METHODOLOGY

RESEARCH OBJECTIVES

1 To compare the performance of LIC and private insurance companies in India

2 To find out the performances of LIC and private insurance companies in each

category (size growth productivity and efficiency)

3 To compare grievance management of LIC and private insurance companies

RESEARCH DESIGN

a Type of research design Analytical Research

b Data collection Secondary Sources

c Statistical Tools Ratio Analysis

RESEARCH PROCESS

In this research my research objective was to compare the performance of LIC and Private

insurance companies For this purpose I decided the four broad categories under which I have

compared the LIC and Private insurance companies These are

1 Size

2 Growth

3 Productivity

4 Grievance Handling

Under these Broad Categories I have analyzed 13 factors which are

1 Size

Total Premium

Total Income

Size of Balance Sheet

Total number of Policies

Total number of Branches

2 Growth

Growth in Premium

Growth in Income

13

Growth in number of Policies

Growth in Market share

3 Productivity

Business per Branch

Income per Branch

New Premium per Branch

4 Grievance Handling

I have used the Secondary data of last five financial years I have collected data from the

various balance sheet of LIC and other private insurance companies web sites and in some

cases I personally met some employees of some insurance companies I tried to find out most

of the information required to compare the LIC and private insurance companies

In Analysis I have found all the required data and on the basis of performance gave the rank

to LIC and Private Insurance Companies on each factor and then points Now these Points

have been multiplied with the weightage of that factor And then after the analysis of each

factor a consolidated point table has been prepared to know that which sector is performing

better than other The Weightage for different categories are

Factors WeightageSize 25A Total Premium 5B Total Income 5C Balance Sheet Size 5

D Total No of Policies 5E Total No of Branches 5

Growth 40A First Premium 10B Growth in Income 10C Increase in No of Policies 10

D Growth in Market Share 10Productivity 15A Business per Branch 5B Income Per Branch 5

C First Premium per Branch 5Grievance Handling 20

LIMITATIONS

14

1 Could reach to a limited number of documents of different insurance companies in

regard to the management and other policies and resultant figures so as to identify

the exact cause of their lag in performance

2 Due to the limited time could not study all the insurance companies original

documents individually

3 Non-Proficiency in technical aspects of insurance companies might have hindered the

best analysis of the findings

SIGNIFICANCE OF THE STUDY

The Detailed Study has been done with the purpose of finding out the relative share of LIC

and Private Insurance in India It is useful for the people associated with the Insurance

Industry and the research associates related to the Insurance Sector in India This study will

acquaint them with the data of all the banks complied at one place along with the findings

conclusion and recommendations

15

CHAPTER 3

ANALYSIS AND INTERPRETATION

16

1 SIZE

(A) TOTAL PREMIUM (Rs In crores)

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC63533 75127 90792 127822 149789

Private3120 7727 15083 28253 51561

Insurers

TOTAL66653 82854 105875 156075 201350

160000PREMIUM OF LIC

149789140000 127822120000100000 90792

7512780000 63533600004000020000

0

FY 03-04FY 04-05FY 05-06FY 06-07FY 07-08

PREMIUM OF PVT INSURERS60000

5156150000

40000

3000028253

20000 15083

10000 31207727

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

17

points after

Avg Premiummultiplying byweightage

( In Crores) Rank points (75)

LIC 101412201 1 75Private Insurance Co 2114880

2 05 375

Average premium of LIC is much more than that of all insurance companies altogether LIC s average premium of the last five years is nearly five times the average premium of the all other private insurance companies

It can be said that up to that time their were less number of private players in the field of insurance but then also undoubtedly LIC is the king

All over income of LIC is much more than than of private players It is due to the fact that LIC being a government agency is being trusted by lot of companies and has large number of shares in big corporates

Total average size of balance sheet of LIC in the last five years is certainly higher than that of private insurance companies There is a huge gap in this value It is obvious that LIC has bigger balance sheet as being working in the insurance field for quite large time As compared to average balance sheet size of 40594 crores of private insurance companies LIC s average balance sheet size goes to much high as that of 5394364 crores

(D) TOTAL NUMBER OF POLICIES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC26968069 23978123 31590515 38229292 37612599

Private1658847 2233075 3871410 7922294 13261558

Insurers

TOTAL 28626916 26211198 35462117 46151586 50874157

21

22

TOTAL NUMBER OF POLICIES60000000

5087415750000000 46151586

4000000035462117

30000000 2862691626211198

LICPVTINSURERS

20000000INDUSTRY

10000000

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

points after

Avg number ofmultiplying byweightage

policies Rank points (75)

LIC 31675670 1 1 75

Private Insurance Co 5789437 2 05 375

LIC is an undoubted leader in the field of average number of policies per year in the last five years It is seen that private insurance companies are gaining momentum and are trying to defeat LIC in case of new insurances Main reason behind LIC having such a large number of policies is the trust of a common man LIC being a government agency has got a faith of indian mass People are not yet prepared to give their savings in the hands of private players

23

24

(E) NUMBER OF BRANCHES

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08

LIC2196 2197 2220 2301 2522

Private416 804 1645 3072 6391

Insurers

TOTAL 2612 3001 3865 5373 8913

100008913

9000

8000

7000 6391

6000 5373LIC

5000PVT INSURERS

40003865

30723001 INDUSTRY3000 2612 2522

2197 2220 23012196

2000 1645

1000 416804

0

FY 03-04 FY 04-05 FY 05-06 FY 06-07 FY 07-08