40

Factoring Factoring Reimbursement Reimbursement Into the Deal Into the Deal May 2, 2005 May 2, 2005

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | thaddeus-patton |

| View: | 26 times |

| Download: | 0 times |

Factoring Reimbursement Factoring Reimbursement

Into the Deal Into the DealMay 2, 2005May 2, 2005

AgendaAgenda

• Tag overview

• Who pays for health care

• What is reimbursement

• How reimbursement affects deal’s value

• Developments and trends

• How Medicare is changing biotech market

• Building reimbursement analysis into deal process

• U.S. reimbursement planning and problem solving since 1998

• Former owner S&FA; Exec VP PAREXEL

• Payer research; strategic planning

• Reimbursement forecasting

• Competitive analysis

• Advocacy with major payers

Tag Client MixTag Client Mix

Pharmaceuti-cals20%

Biotech/ Biologicals

40%

Investors/ Advisors

15%

Ad/ PR/ PA Agencies

10%

Devices/ Diagnostics

15%

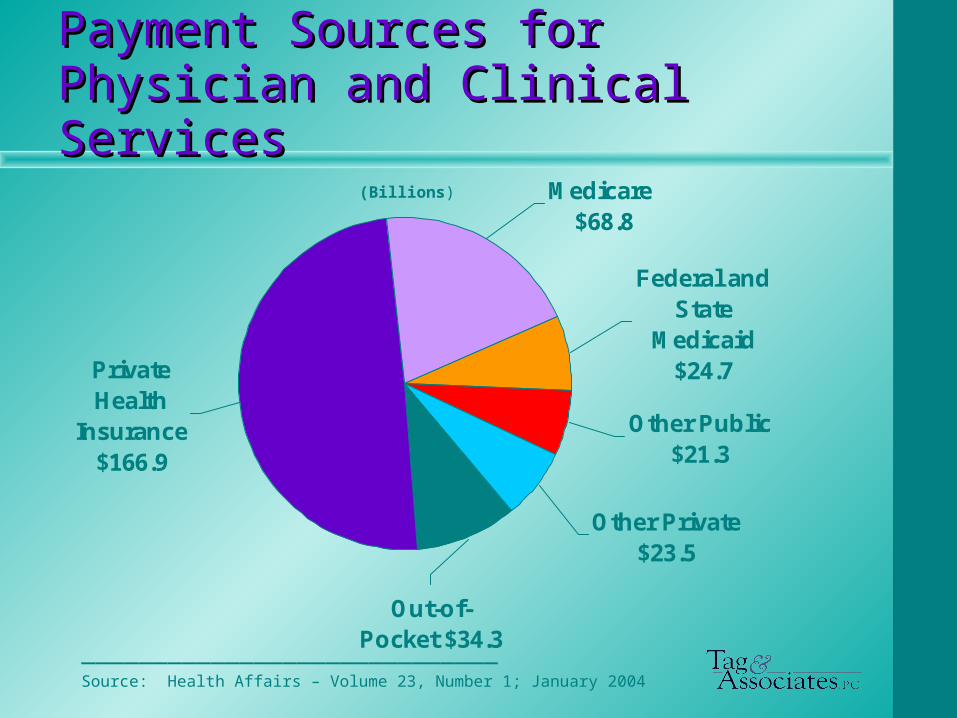

Who Pays for Health CareWho Pays for Health Care

Payment Sources forPayment Sources forPhysician and Clinical ServicesPhysician and Clinical Services

Other Private $23.5

Medicare $68.8

Other Public $21.3

Private Health

Insurance $166.9

Federal and State

Medicaid $24.7

Out-of-Pocket $34.3

_____________________________Source: Health Affairs – Volume 23, Number 1; January 2004

(Billions)

Payment Sources for Prescription Payment Sources for Prescription DrugsDrugs

Federal and State

Medicaid $28.6

Medicare $2.6

Private Health

Insurance $77.6

Out-of-Pocket $48.6

Other Public $5.0

_____________________________Source: Health Affairs – Volume 23, Number 1; January 2004

(Billions)

Reimbursement andReimbursement andHow It Affects Deal’s Value How It Affects Deal’s Value

Know Whether “Reimbursement” Know Whether “Reimbursement” Means Coverage or PaymentMeans Coverage or Payment

Coverage

• Is the product or related service an insured benefit?

– Under what circumstances?

Payment

• How much will the insurer reimburse?

– To whom?

Many Factors Affect Many Factors Affect ReimbursementReimbursement

• Tech category (e.g. Rx, OTC, DME, supply, diagnostic, screen)

• Payer• Tx setting• Dosage form• Admin method• Labeling (on/off)• Diagnosis• Safety & efficacy

• Product cost (price)• Related costs (e.g. lab)• Uniqueness• Alternative cost• Cost offsets• Prescribing Dr.• Abuse potential• Political/social• Evidence-based

outcomes

Reimbursement Winners Reimbursement Winners

• Norplant – Medicaid; not an OC

• Lupron depot – Clinician administered

• EPO – Cover as sub Q or we do trials as IV only

• Drug eluting stents – Showed payers cost impact, good and bad

… … And LosersAnd Losers

• tPA – Great science, no payment

• Lupron daily injection – No coverage for self-admin

• Gliadel wafers – Part of DRG, no payment

• Rocephin (otitis media) – Pediatricians were capitated

Take AwayTake Away

• Great medicine (tPA) will trump poor reimbursement …

• But not every good technology is great medicine

Case Study: Same Technology, Case Study: Same Technology, Different ReimbursementDifferent Reimbursement

• QLT’s Photofrin (porfimer sodium) photodynamic therapy

• Sanofi-Winthrop: esophageal and lung cancer

• Novartis: macular degeneration

Poor Return for Sanofi-Poor Return for Sanofi-WinthropWinthrop

• Hospital O/P procedure in era of poor hospital reimbursement

• Endoscope/bronchoscope procedures under-reimbursed based on simple tech

• 2 year wait for drug reimbursement code

Because of reimbursement, procedure viewed as last resort despite good clinical outcomes

Winner For Novartis Winner For Novartis

• Decent reimbursement for physician office single eye procedure– Strategy developed to deal with subpar

reimbursement of 2nd eye procedure

• Good drug reimbursement year 1

• No therapeutic alternative Robust uptake, despite mediocre

clinical results

Developments and TrendsDevelopments and Trends

OverviewOverview

• Evolving payer objectives: Cost avoidance > Cost benefit > Value > Affordability

• Utilization control via patient cost sharing

• Federal government becoming largest customer for Rx drugs

• Medicare evolving: payer > national heath policy and treatment manager

OverviewOverview – cont’d– cont’d

• Elimination of provider profit on drugs

• Power shift: Provider > Distributor

• Coverage policy linked to outcomes data

• Health econ and off-label requirements changing scope of registration studies

Evolving Payer ObjectivesEvolving Payer Objectives

• 1980’s – Cost avoidance (managed care)

• 1990’s – Cost benefit (outcomes analysis)

• 2000’s – Value - money for quality (evidence based medicine)

• On The Horizon – Affordability - Employers (declining profits) and governments (increasing deficits) not willing to absorb cost of every medical breakthrough

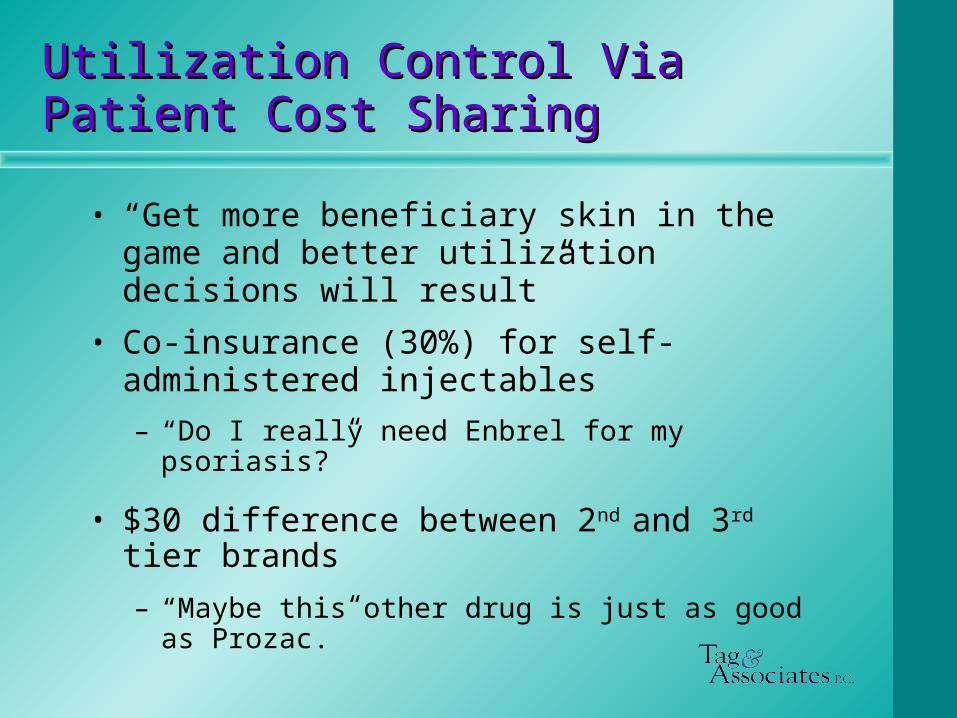

Utilization Control ViaUtilization Control ViaPatient Cost SharingPatient Cost Sharing

• “Get more beneficiary skin in the game and better utilization decisions will result”

• Co-insurance (30%) for self-administered injectables

– “Do I really need Enbrel for my psoriasis?”

• $30 difference between 2nd and 3rd tier brands

– “Maybe this other drug is just as good as Prozac.”

Federal Government Will Control Federal Government Will Control 40% of Rx Market40% of Rx Market (White Dots)(White Dots)

Medicaid$30

Out of Pocket

$60

Other Public $10

Medicare $65

Private Ins $95

2002 Rx Payment Sources (bil)2002 Rx Payment Sources (bil) 2008 Projected (bil)2008 Projected (bil)

Other Public $5.0

Private Ins

$77.6

Medicaid $28.6 Out of

Pocket $48.6

Medicare $2.6

___________________________Source: 2002 data: Health Affairs Volume 23, Number 1; January 2004. 2008 data: Tag & Associates estimate.

Total = $162.4 Total = $260

Medicare Evolving to Be NationalMedicare Evolving to Be NationalTreatment Policy ManagerTreatment Policy Manager

• CMS process for evaluating new technology is rigorous and willing to embrace new costs– Implanted automatic defibrillators

– Drug eluting stents

• Adverse Medicare coverage policy decision is routinely followed by private payers

Elimination of Provider Profit on Elimination of Provider Profit on Clinician-Administered DrugsClinician-Administered Drugs

• Medicare: AWP > ASP; CAP

• Medicaid: National “reform” on the horizon

Elimination of Provider Profit on Elimination of Provider Profit on Clinician-Administered DrugsClinician-Administered Drugs – – cont’d.cont’d.

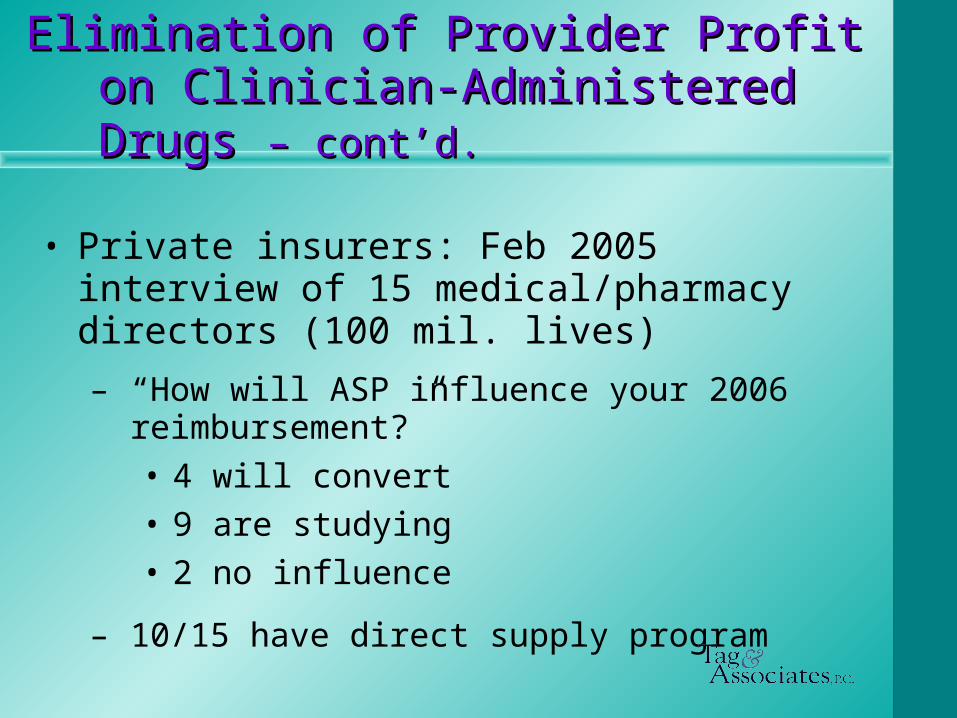

• Private insurers: Feb 2005 interview of 15 medical/pharmacy directors (100 mil. lives)

– “How will ASP influence your 2006 reimbursement?”• 4 will convert• 9 are studying• 2 no influence

– 10/15 have direct supply program

Power Shift to DistributorsPower Shift to Distributors

• CAP, direct supply shifts power to distributor

– Ability to control access via formulary

– Reflected in M&A activity

• Medco/Accredo

• AmeriSource Bergen/US BioServices

• Caremark/Advance PCS

Coverage Policy linked to Coverage Policy linked to Outcomes DataOutcomes Data

• New in 2005: Medicare expands coverage for selected technologies only if manufacturer agrees to data collection per CMS spec

– Implanted defibrillators

– Off label use of 4 new Ca drugs

Coverage Policy Linked to Coverage Policy Linked to Outcomes Data Outcomes Data – cont’d.– cont’d.

• Since late 1990s: Private tech evaluators become more influential each year– BC/BS TEC

– Wilkerson Group

• Globalization: UK NICE influence spreads across EU

Broad Registration Studies Needed Broad Registration Studies Needed to Support Reimbursementto Support Reimbursement

• Traditional FDA strategy of “path of least resistance” still OK for FDA but no longer viable for payer success

– Payers demanding health econ data for coverage

– Clamping down on off label uses not supported by scientifically rigorous data

How Medicare Is Changing How Medicare Is Changing the Biotech Marketthe Biotech Market

Clinician-Administered Clinician-Administered DrugsDrugs

• Physician office and hospital O/P drugs are a pass-through expense rather than a profit center

• First time ever formulary as a result of CAP

– Some categories need only 1 drug

Clinician-Administered Drugs Clinician-Administered Drugs – – cont’d.cont’d.

• Coverage of new tech will require 1 of the following:

– Lower price

– Impressive safety or efficacy

– Favorable outcomes data

– Widespread socio-political demand

Self-Administered DrugsSelf-Administered Drugs

• Part D establishes a de facto national baseline formulary of ~250 drugs

• Beneficiaries have strong $ incentive to keep total Rx spending <$2,250

– Between $2,250 and $5,100, patient pays 100%

Building Reimbursement Into Building Reimbursement Into Deal Process Deal Process

Make It Fundamental to the Make It Fundamental to the Go/No Go DecisionGo/No Go Decision

• Immediately identify reimbursement issues

• Can development decisions be used to fix problem or gain advantage?

• If problem can’t be fixed, how will it impact the value of the technology?

Take the Payers’ Take the Payers’ PerspectivePerspective

• Which payer has the biggest stake?

• To whom are they beholden?

• What/who influences their decision making?

• How will technology impact them?

• What happens if they say “No?”

Do Not Rely On the Downstream Do Not Rely On the Downstream PartnerPartner

• Regardless of size and general competence, they are wrong as often as they are right

• They will under-value the technology b/c of easily manageable reimbursement problem

• To the person you are dealing with, it always looks “just like this other product we had 2 years ago in this other category ….”

Teach Your ClientTeach Your Client

• Most technology developers are unaware of reimbursement issues or have the wrong information

• Help them understand why payers are as much a customer as clinicians

Bring a Reimbursement POA Bring a Reimbursement POA to the Discussion Tableto the Discussion Table

• Show prospective partners that you

– Expect them to invest at an appropriate level to conquer or capitalize on the reimbursement issues

– Will not allow reimbursement to be a red herring that distracts from other more significant issues