Capstone Project Foreign Direct Investment in Indian Retail Sector and Its Implications In partial fulfillment ofPost Graduate Diploma in Industrial Engineering (PGDIE) National Institute of Industrial Engineering Certificate Capstone Project: FDI in Indian Retail Sector and Its Implication Page 1 By Santosh Kumar Roll NO: 75 PGDIE-41 NITIE, Mumbai Under Guidance ofProf. S. B. Hiremath ProfessorNITIE Mumbai

Transcript

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

Foreign direct investment (FDI) plays an important role in India’s growth dynamics. Evidently,

there is no national consensus on allowing FDI in retail. Advocates tout it as the much-needed

major policy push that could arrest the economic downturn, bring in not only foreign funds but

advanced technology and expertise, create infrastructure, offer better prices to farmers,

generate ancillary industries and create millions of jobs. However, sceptics present a doomsday

scenario: it will wipe out small farmers and traders, result in job losses and open the floodgates

for cheap goods from countries like China, adversely impacting Indian industry. While both

arguments have some validity, the two sides err on the side of extremes. This paper focuses that

FDI in retail is not an unmitigated disaster as projected by some, nor a magic wand leading to

instant economic growth. If allowed with professional circumspection and safeguards and

viewed dispassionately, it is in the country's national interest to allow FDI in retail.

METHODOLOGY:

Analytical, descriptive and comparative methodology has been adopted for this report; reliance

has been placed on books, journals, newspapers and online databases and on the views of

writers in the respective discipline.

LITERATURE REVIEW:

The advantages of allowing FDI in the retail sector evidently outweigh the disadvantages

attached to it and the same can be deduced from the examples of successful experiments in

countries like Thailand and China; where too the issue of allowing FDI in the retail sector wasfirst met with incessant protests, but later turned out to be one of the most promising political

and economical decisions of their governments and led not only to the commendable rise in the

level of employment but also led to the enormous development of their country’s GDP. Thus, as

a matter of fact FDI in the buzzing Indian retail sector should not just be freely allowed but per

contra should be significantly encouraged (Amisha Gupta, IJMMR Dec 2010). FDI is really

important for the Indian Economy and definitely FDI in the retail sector too. The government is

considering a proposal to bring uniformity to the level of foreign direct investment allowed in

various business segments within a particular sector. At present, varied levels of FDI are

permitted in different business segments in at least half a dozen areas including petroleum,

aviation, media, retail, telecom and the financial sector. For instance in telecom, basic and

cellular services are allowed 74% FDI, ISPs without gateway 100%, and equipment

manufacturing 100%. Similarly, in the financial sector, NBFCs can have 100% FDI, private

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 4

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

sector banks 74%, and asset reconstruction companies 49%.Government officials also agreed

that the proposal, at initial stages now, could find its way into the national foreign investment

policy. A Uniform sectoral FDI may be one of the ways to consolation of FDI. But until then

FDI in retail trade should be allowed and the extent of it should not be minimized. (Tanay

Kumar & Ritanker Sahu, Emerald 2007) Potential benefits from allowing large retailers to enter

the Indian retail market may outweigh the costs. Evidence from the United States suggests that

FDI in organised retail could help tackle inflation, particularly with wholesale prices. It is also

expected that technical know-how from foreign firms, such as warehousing technologies and

distribution systems, for example, will lend itself to improving the supply chain in India,

especially for agricultural produce. Creating better linkages between demand and supply also

has the potential to improve the price signals that farmers receive. By eliminating both waste

and middlemen also increase the fraction of the final sales prices that is paid to farmers. An

added benefit of improved distribution and warehousing channels may also come from

enhanced exports (Anshu Chari & TCA Madav, the word economy 2012).

The low penetration of organized retailing in India means retailers still do not have the volume

that can influence discounts from big FMCG brands. A large percentage of market share in

FMCG is dominated by three or four strong players. Exposure to international retailers will

accelerate the rate of Indian retailing change. (Chitra Sriwastava & Brenda, Emerald 2012)

Almost every two months we see big corporations who had previously shied away from theretail industry, announcing huge investments into the sector. Companies already in the market

are coming up with new formats almost every quarter. Coupled with the economy growing in

leaps and bounds and the government at the center obliging with favorable policies, the retail

sector is a bus no one wants to miss in India. (STPV-2007-2002, June 12, 2007)

But on other hand Rajat & Abhisek say that the lure of FDI in retail is based on the Wal-Mart

story in China. That was when China had become the hub for exporting cheap goods into the

U.S. Many U.S. corporations exploited the opportunity. That story has outlived its purpose. The

yuan debate has undone it. The U.S. cannot afford to live with a hollowed manufacturing base;

nor can China live with an exports-only strategy and has to turn inward. The moral is that there

is no global model of retail which can be replicated elsewhere. (Rajat Kesari & abhishek kumar,

Zenith Oct 2011)

DEFINITION OF FOREIGN DIRECT INVESTMENT:

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 5

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

FDI is the process whereby residents of one country (the home country) acquire ownership of

assets for the purpose of controlling the production, distribution and other activities of a firm in

another country (the host country). IMF Definition: “ Foreign direct investment is the category

of international investment that reflects the objective of obtaining a lasting interest by a resident

entity in one economy in an enterprise resident in another economy. The lasting interest implies

the existence of a long-term relationship between the direct investor and the enterprise and a

significant degree of influence by the investor on the management of the enterprise.”

One of the most striking developments during the last two decades is the spectacular growth of

FDI in the global economic landscape. This unprecedented growth of global FDI in 1990 around

the world make FDI an important and vital component of development strategy in both

developed and developing nations and policies are designed in order to stimulate inward flows.

In fact, FDI provides a win – win situation to the host and the home countries. Both countries

are directly interested in inviting FDI, because they benefit a lot from such type of investment.

The ‘home’ countries want to take the advantage of the vast markets opened by industrial

growth. On the other hand the ‘host’ countries want to acquire technological and managerial

skills and supplement domestic savings and foreign exchange. Moreover, the paucity of all types

of resources viz. financial, capital, entrepreneurship, technological know- how, skills and

practices, access to markets- abroad- in their economic development, developing nations

accepted FDI as a sole visible panacea for all their scarcities. Further, the integration of globalfinancial markets paves ways to this explosive growth of FDI around the globe.

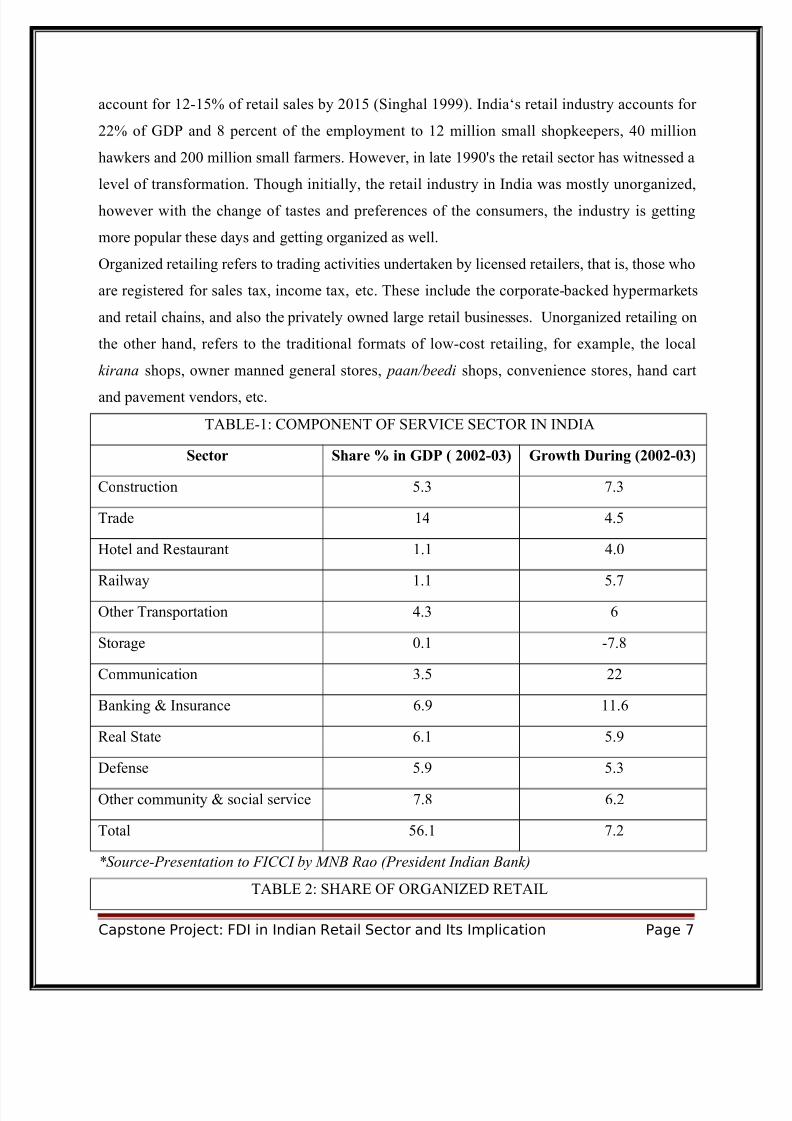

BACKGROUND OF INDIAN RETAIL SECTOR:

The Indian retail industry has experienced high growth over the last decade with a noticeable

shift towards organized retailing formats. The industry is moving towards a modern concept of

retailing. The size of India's retail market was estimated at US$ 435 billion in 2010. Of this,

US$ 414 billion (95% of the market) was traditional retail and US$ 21 billion (5% of the

market) was organized retail. India's retail market is expected to grow at 7% over the next 10

years, reaching a size of US$ 850 billion by 2020. Traditional retail is expected to grow at 5%

and reach a size of US$ 650 billion (76%), while organized retail is expected to grow at 25%

and reach a size of US$ 200 billion by 2020. According to the Investment Commission of India,

the retail sector is expected to grow by $660 billion by 2015 and also expected that India will be

among the top 5 retail markets then. The organized sector is expected to grow to $100 bn and

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 6

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

Some of the key players in the Indian retail market, with a dominant share are:

Pantaloon Retail Ltd, a Future group ventures

Shoppers Stop Ltd

Spencer’s Retail, RPG Enterprises

Lifestyle Retail, Landmark group venture

Other major domestic players in India are Bharti Retail, Tata Trent, Globus, Aditya Birla

‘More’, and Reliance retail. Some of the major foreign players who have entered the segment in

India are

Carrefour which opened its first cash-and-carry store in India in New Delhi.

Germany-based Metro Cash & Carry which opened six wholesale centers in the country.

Walmart in a JV with Bharti Retail, owner of Easy Day store—plans to invest about US$

2.5 billionover the next five years to add about 10 million sq ft of retail space in the

country.

British retailer Tesco Plc (TSCO) in 2008, signed an agreement with Trent Ltd.

(TRENT), the retail arm of India’s Tata Group, to set up cash-and-carry stores.

Marks & Spencers have a JV with Reliance retail.

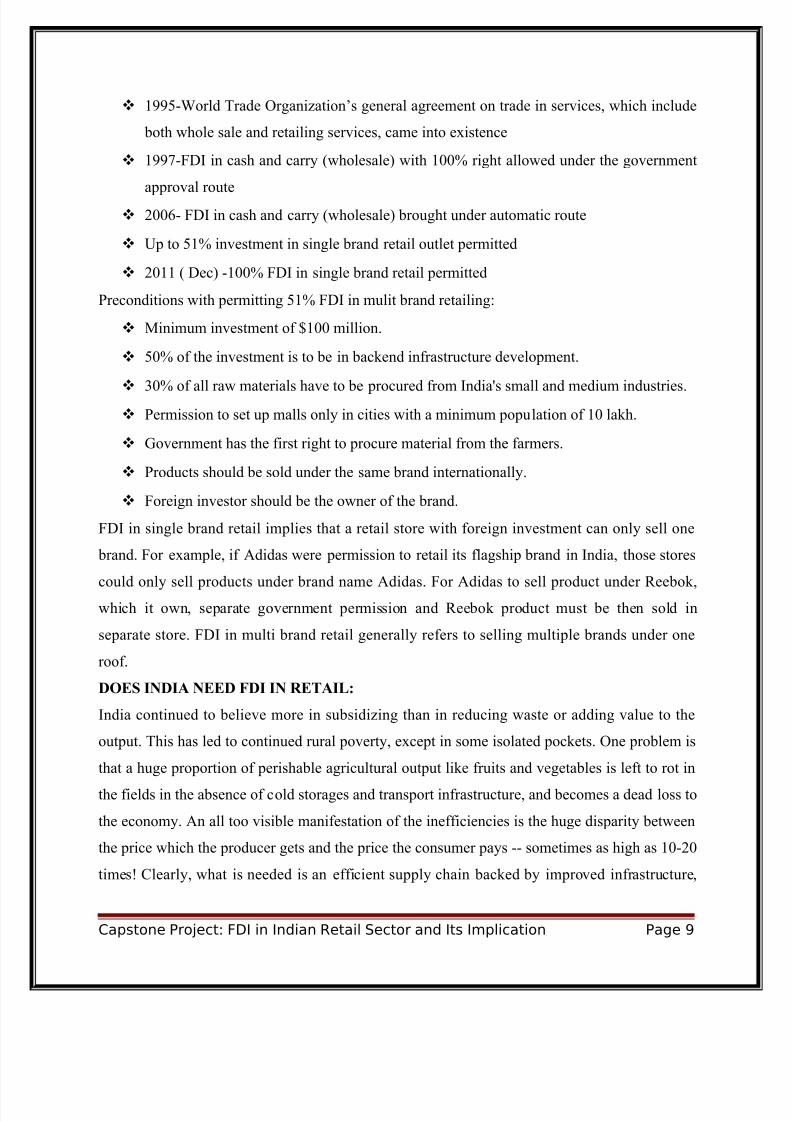

GOVERNMENT POLICIES:

Till now FDI up to 100 per cent was allowed for cash and carry wholesale trading and export

trading under the automatic route, and FDI up to 51 per cent was allowed in single-brand

products, with prior government approvals. However, the Government recently passed a cabinetnote and permitted FDI up to 51% in multi brand retailing with prior Government approval and

100% in single brand retailing thus further liberalizing the sector. This policy initiative is

expected to provide further fillip to the growth of the sector.

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 8

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

1995-World Trade Organization’s general agreement on trade in services, which include

both whole sale and retailing services, came into existence

1997-FDI in cash and carry (wholesale) with 100% right allowed under the government

approval route

2006- FDI in cash and carry (wholesale) brought under automatic route

Up to 51% investment in single brand retail outlet permitted

2011 ( Dec) -100% FDI in single brand retail permitted

Preconditions with permitting 51% FDI in mulit brand retailing:

Minimum investment of $100 million.

50% of the investment is to be in backend infrastructure development.

30% of all raw materials have to be procured from India's small and medium industries.

Permission to set up malls only in cities with a minimum population of 10 lakh.

Government has the first right to procure material from the farmers.

Products should be sold under the same brand internationally.

Foreign investor should be the owner of the brand.

FDI in single brand retail implies that a retail store with foreign investment can only sell one

brand. For example, if Adidas were permission to retail its flagship brand in India, those stores

could only sell products under brand name Adidas. For Adidas to sell product under Reebok,which it own, separate government permission and Reebok product must be then sold in

separate store. FDI in multi brand retail generally refers to selling multiple brands under one

roof.

DOES INDIA NEED FDI IN RETAIL:

India continued to believe more in subsidizing than in reducing waste or adding value to the

output. This has led to continued rural poverty, except in some isolated pockets. One problem is

that a huge proportion of perishable agricultural output like fruits and vegetables is left to rot in

the fields in the absence of cold storages and transport infrastructure, and becomes a dead loss to

the economy. An all too visible manifestation of the inefficiencies is the huge disparity between

the price which the producer gets and the price the consumer pays -- sometimes as high as 10-20

times! Clearly, what is needed is an efficient supply chain backed by improved infrastructure,

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 9

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

cold storages, packing and transportation. And, the traditional system of distribution, ending

with the mom and pop shops or the street-side vegetable seller, is just not capable of creating it.

This brings us to the third blind spot: distribution and retailing. First, umpteen indirect taxes

hamper a smooth chain. Again, for decades, financing of manufacturing was considered virtuous

while finance for trade or consumption was discouraged. The middlemen were, broadly

speaking, thought to be parasites standing between the producer and the consumer, contributing

little to economic growth or output. The fact is that the circle of economic activity cannot be

completed until what is produced reaches the consumer and, therefore, efficient distribution and

retailing are very important. To quote just one example, can India imagine a vibrant automobile

sector without an efficient distributor and service network and, indeed, vehicle finance? Or a

fast growing and needed housing sector without availability of housing finance?

The entry of the organised sector in retail trade is capable of mitigating, if not solving, the huge

waste involved in the current system, simultaneously paying better prices to the producer and

lower prices for the consumer. This is manifest to anybody visiting some of the newer

supermarkets in urban/metropolitan India: the produce is cleaner, fresher, well-packed, and

often cheaper than the vegetable seller on the street. This is possible because of the far more

efficient distribution system which organised retail chains are employing, by cutting layers of

middlemen. One very positive sign is that a way seems to have been found for the corporate

sector to enter the rural economy through contract farming -- almost every day one sees major corporate names making forays in the area. If the huge margin between producer and consumer

prices is one attraction, they are also perhaps inspired by what Pepsi succeeded in doing for the

potato farmer in Punjab, partly to fulfil the export obligations imposed on it when it entered

India.

Recent indications that the government is considering foreign direct investment in retail trade

have sparked off a debate on the advisability and consequence of this policy. Retail trade takes

place through five types of outlets -- kirana shops, more modern retail shops, departmental

stores, supermarkets, and hypermarkets. Kirana shops and retail shops are a feature of our

landscape. Every village and town has them. They are usually family-owned and managed.

Most kirana shops store goods unpacked in bulk containers, from which they are measured or

weighed out in paper packets by the owner. When towns become cities, departmental stores

appear. Supermarkets are the next stage in the evolution of retailing. They are viable only in the

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 10

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

bigger cities. The fear expressed by some people is that allowing FDI in retail trade and the

entry of international retailers could lead to a diminution of kirana shops and retail stores. It is

worthwhile analyzing the advantages and disadvantages of the proposed policy of allowing FDI

in retail trade.

One key point is that Indian government must differentiate between the interests of consumers,

who constitute our population of nearly 1,100 million , from the interests of retailers, who may

number over one million . It is obvious that the interests of the consumer should take precedence

over those of the retailer. FDI in retail and the development of larger stores and supermarkets

have the following advantages from the point of view of consumers:

FDI will provide access to larger financial resources for investment in the retail sector

and that can lead to several of the other advantages that follow;

The larger supermarkets, which tend to become regional and national chains, can

negotiate prices more aggressively with manufacturers of consumer goods and pass on

the benefit to consumers. They can lay down better and tighter quality standards and

ensure that

With the availability of finance, the supermarkets can invest in much better infrastructure

facilities like parking lots, coffee shops, ATM machines, etc. All this will make shopping a

pleasant experience. The supermarkets offer a wide range of products and services, so the

consumer can enjoy single-point shopping. The argument that the advent of FDI andsupermarkets will displace a large number of kirana shops is similar to the argument used

during the era of industrial licensing, which was meant to protect small-scale industries. But

eventually the inefficiencies and quality standards of the protected small-scale companies

become apparent even to socialist politicians and licensing was abolished. Small-scale industries

have not died. Instead, they have learnt to co-exist as suppliers to large-scale industries.

In the case of retail trade, the kirana shops in large parts of the country will enjoy built-in

protection from supermarkets because the latter can only exist in large cities. On the other hand,

the ability of supermarkets to demand pricing and quality standards from manufacturers will

benefit even kirana shops, who can even buy from the supermarkets to sell the same products in

smaller towns and villages. It can be argued that since the advantages cited above are due to the

scale of operations rather than the involvement of foreign capital, why should India allow FDI

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 11

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

in retail trade? The case for FDI has more to do with the confidence and willingness to invest

large amounts in a short period as well as the expertise based on experience.

Even a modest chain of 200 supermarkets, to be set up all over India in selected towns and cities

in the next three years, will require an investment of about Rs 2,000 crore (Rs 20 billion), at the

rate of Rs 10 crore (Rs 100 million) per supermarket to cover the infrastructure and working

capital. Each supermarket may take 2 or 3 years before it becomes profitable. There is a risk that

a few of them may even fail. How many Indian entrepreneurs will be willing and able to commit

this level of investment and undertake the risks involved? That is where the international

experience and skills that may come with FDI would provide the confidence and capital. Apart

from this, by allowing FDI in retail trade, India will become more integrated with regional and

global economies in terms of quality standards and consumer expectations. Supermarkets could

source several consumer goods from India for wider international markets. India certainly has

an advantage of being able to produce several categories of consumer goods, viz. fruits and

vegetables, beverages, textiles and garments, gems and jewellery, and leather goods. The advent

of FDI in retail sector is bound to pull up the quality standards and cost-competitiveness of

Indian producers in all these segments. That will benefit not only the Indian consumer but also

open the door for Indian products to enter the wider global market. It is therefore obvious that

India should not only permit but encourage FDI in retail trade. Just as in the case of most

products, the brand name of the supermarket chain is a strong element in its growth and success.People have confidence in names like Sainsbury, Asda, Marks & Spencer, etc. just as they have

confidence in Indian brands like the Tatas and Godrej. A possible outcome can be that Indian

groups with strong local brand quality like the Tatas will collaborate with international

supermarket chains like Sainsbury, to set up supermarket chains in India. It will be unwise for a

government to interfere in this process.

CASE STUDY OF WALL MART:

I take the case of Wal-Mart’s model of retailing as the bench mark for the possible effects of

allowing entry of large foreign retail firms into India. What are the advantages of Wal-Mart in

the U. S., and other countries, whether these advantages can be translated into India and if so

what are the possible effects in terms of net benefit or losses on different stakeholders?

Wal-Mart is the largest retail corporation in the world with $ 400 million annual turnover and

about two million employees. Wal-Mart discount store was first established in a small town

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 12

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

Rogers in Arkansas by Sam Walton in 1962. The basic strategy was to enter small towns with

population of 5000 to 25000 which were not served by large retailers and derive scale advantage

in relation to the size of small town markets and eliminate small players. This is similar to a

natural monopoly where, given the size of the market, one large player with global economies of

scale can serve the market more efficiently than large number of small players. The outcome of

this strategy is illustrated with a simple partial equilibrium theory.

In Figure, D is demand curve of a small town. The linear addition of ‘ U ’ shaped cost curves of

small firms is represented by LACs and LMCs, the long run average cost and long run marginal

cost respectively. With these costs, the equilibrium market price is P and quantity served is OQ.

Let us take that a large player with global economies of scale enters the market and the cost

curves of the large firm are LACl and LMCl . The large firm charges a market price P1 that is

equal to long run average cost. The supply increases from Q to Q1.The decline in the market

price causes exit of small firms. Will it result in unemployment as small firms employ more

labor per unit of output produced than the large firm with economies of scale? Increase in output

supplied from Q to Q1 can absorb some of the labor released by the exit of small firms. Given

the fixed costs of the supply chain infrastructure, the constant and positive marginal cost could

be treated as goods turnover and labor costs. Apart from this, decline in price from P to P1

increases consumer surplus to the extent of PabP1 and real incomes. Increase in real incomes

increases expenditure and savings and could generate employment in other activities. After realizing the cost advantage in its expansion in small towns, Wal-Mart translated this into its

operations in large cities with aggressive cost and price cutting and grew at a rapid pace.

One could argue that the large firm could act as a monopolist after it drives out the small firms

and produce at a point where the marginal revenue for D intersects LMC1, which may imply a

price higher than the small firms’ P . However, Wal-Mart has not done this and that it is against

its whole pricing strategy- keeping costs and prices as low as possible and realize high turnover

with thin margins. The following provides the different processes of the cost advantage.

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 13

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

within two days against at least five days for competitors and shipping costs on average turn out

to be 3 percent as against 5 percent for competitors.

As far as employment effect of Wal-Mart is concerned, Basker (2005) found that “…

immediately after entry, retail employment in the country increases by approximately 100 jobs;

this figure declines by half over the next five years as some small and medium size retail

establishments close. Wholesale employment declines by approximately 20 jobs over five

years.”

On the other hand, Ghemawat and Mark (2006) argue that Wal-Mart has grown the economic

pie available to be divided among its various stakeholders instead of slicing up a fixed pie in a

way that favors one group over another. They cite the McKinsey Global Institute’s study of the

U.S. labor productivity growth between 1995 and 2000 (by Robert Solow) which shows that

Wal-Mart contributed significantly for its growth. Given that Wal-Mart’s prices are 8 percent

lower than competitors, the U.S. consumers save on the order of $ 18 billion per year. For each

job lost through Wal-Mart effect, consumers saved more than $ 7 million per year. This would

imply that in terms of net effects more jobs were created through increase in incomes and

expenditure than those of direct losses.

The above discussion shows that Wal-Mart derived a sustainable advantage with respect to

competitors in the U.S. with net positive effects on the economy as a whole. The following issue

is whether it has been able to translate it to foreign country operations. The theory of multinational firms shows that a firm becomes a multinational if it has intangible asset

advantage in technology, brand name and organization otherwise local firms can produce the

product more efficiently than a foreign firm (Hymer, 1960). For example, when Wal-Mart

entered Canada and the U.K. it has been successful. However, it failed in South Korea and

Germany and struggles in countries such as Japan and Russia.

The operation of Wal-Mart in Mexico is shown to have resulted in $ 60,000 in savings to

customers for each $ 10,000 in wages paid to employees (Das and Pramanik, 2011). Wal-Mart

grew very rapidly in Mexico. By 2012, it has become the largest private employer with 209000

employees. Wal-Mart entered China in 1996 and now it operates 352 stores in 130 cities. Wal-

Mart has been able to cater to the rapidly growing Chinese market at around 18 percent

annually. About 20,000 Chinese suppliers provide Wal-Mart with 70 percent of its global sales.

Thirty percent of Chinese exports are accounted by Wal-Mart. Schell (2011) observes “Just as

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 15

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

China is providing Walmart with the lifeblood of its commercial growth, Walmart is helping the

Chinese state not just to satisfy the escalating demands of its consumers but to extend Beijing’s

regulatory writ. Together, they are engaging in a bold experiment in consumer behavior

modification, market economies, and environmental stewardship.

IMPLICATIONS OF FDI IN INDIAN RETAIL INDUSTRY:

Before going into the possible effect of FDI on different stakeholders, I would like to discuss the

effect of the entry and expansion of large organized Indian retailers such as the Reliance fresh in

Bangalore, Hyderabad and a small town Guntur in the state of Andhra Pradesh. The

observations are based on visits ( Murali Patibandla ) to the Reliance stores and field interview

of small vendors located within five kilometer radius of the location of the Reliance store. The

Reliance fresh stores operate both large stores and relatively small ones depending on the real

estate available in the areas populated with middle income and richer consumers. They stack up

with food grains both in large quantity and smaller quantity packets, processed foods of all

kinds, fresh vegetables and fruits and some stores have fresh meat and fish set up separately

from the main store. Vegetables, fruits and meat products are brought in everyday while the

processed foods and food grains are stacked up in relation to turnover. They ensure the products

meet the grading and quality requirements both at the procurement and final sale stages. The

prices in the Reliance stores on average are cheaper by about 5 to 10 percent compared to

nearby Kirana stores and fruit and vegetable vendors in Bangalore. Apart from this, consumer’shave wider choice of products than those available in Kirana stores. The entry of the Reliance

stores led to closure of middle scale grocery stores, which are relatively modern compared to

Kirana stores, located in the radius both in the metros and the small town. Kirana stores and

vegetable and fruit vendors observed that their business dropped by 20 percent with the advent

of the Reliance fresh stores within the radius.

Textbook economics shows that a monopolist could undertake price discrimination to maximize

producer’s surplus: perfect price discrimination of charging a different price from different

consumers depending on their willingness to pay; second order price discrimination of charging

different prices depending on the quantity of purchase and third degree price discrimination of

charging different prices from segmented markets depending on price elasticity of demand. 13

However, as I observed in Bangalore, small and medium scale vendors are able to exercise a

certain form of perfect price discrimination of quoting higher price to a customer who looks rich

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 16

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

(with cars) and lower price from a customer who appears poorer. Secondly, they could exercise

third degree price discrimination of charging higher prices in the rich localities and lower prices

in the poorer areas. The ability of small vendors to exercise perfect price discrimination has

declined with the entry of the large organized retailers as the richer consumers with cars and

refrigerators prefer to buy from the large players with diverse product choices. The main market

that remained with the small vendors is the daily income earners who buy small quantities for

their everyday needs. The Reliance fresh stores sell both large quantity packages at discount and

also small quantity items of say rice, wheat powder, lentils and vegetables at a cheaper rate than

the small vendors. However, poor consumers’ inability to incur costs of going to the Reliance

fresh makes them to buy from the small vendors. A few small Kirana stores in the Bannerghatta

road of Bangalore procure large quantities of food grains and dry foods from the Reliance stores

on a weekly basis and sell to costumers with a mark-up of 5 to 10 percent. Apart from this, the

small Kirana stores which are densely located with each other have developed cooperative

agreements with each other and avoid price competition. The following issue is how does the

entry of foreign players effects the market dynamics? The possible effect of allowing FDI is

improvements in supply chain technologies, technological and informational externalities to

local players and competitive dynamics that could benefit consumers and suppliers. The press

reports show that in the year 2011 the Pantaloon Retail’s net profits increased 69 percent to Rs

1.42 billion on net sales of Rs 122.1 billion which means the company was able to makesupernormal profits at the cost of consumers and suppliers. A study of the Indian retail chain

Spencer (Singh 2010) shows that lower procurement prices are not passed onto consumers and

most supermarkets maintain high margins on perishable items. This is where competition from

foreign firms will drive the industry to be contestable.

Assuming Wall-Marts Entry in India:

the first issue would be Wal-Mart’s ability to adapt its low cost and price model to India’s

institutional and infrastructure conditions and overtime how its’ operations change the landscape

of the retail industry in India. Wal-Mart has to modify the U.S model of establishing large stores

outside the cities. Furthermore, at present there are large barriers for trade within the country-

different tax regime of the states and infrastructure conditions. Just to give an example, it is

easier to bring apples from Australia to Bangalore than getting them from the Himachal Pradesh

state. This means Wal-Mart has to adopt the supply chain for the different regions of the country

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 17

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

than for the whole country. In other words, certain elements of the supply chain could be

standardized at the national level and others have to be adapted to regional requirements

As mentioned earlier, Wal-Mart’s supply chain is highly efficient in terms of linking sales

pattern at the front end to its warehouses and the producers. One of the important issues is 18

creating linkages with large number of Indian manufacturers and farmers spread across the

country which poses difficulties in inventory management if it faces problems of high

transaction costs of contracts, delivery time, and quality control. Wal-Mart has to invest

significant amount of resources in cultivating long term relationship with the suppliers and

helping them in quality and delivery control mechanism.

Wal-Mart’s practices is that it drives supplier firms to be cost-effective especially if the

suppliers become dependent on the large buyer. On the other hand, if supplier firms in India

learn from Wal-Mart in improving production and delivery practices, they could improve their

bargaining by diversifying their sales to other large retailers or even by selling in the

international markets. If Wal-Mart is able to adapt its supply chain to Indian conditions, it could

benefit both large and relatively small Indian retailers by expanding the market through

improving know-how of large number of vendors in the country. This was what happened in the

auto-component industry in India especially in regard to the first-tier producers as a result of

entry of TNCs in the automobile industry (Patibandla, 2006, Okada, 2009).

Macroeconomic policies aimed at curbing food inflation result in perverse outcomes. If we takethe example that the Reserve Bank of India increases interest rates to curb economic activity

that is expected to curb food inflation, this results in unemployment so that demand for food

from the poor goes down. This is a perverse outcome. The main way to reduce food inflation is

to reduce the supply inelasticity- increase in agricultural productivity, allowing free trade across

the country and adoption of efficient supply chain that reduces the wastage. To cater to the

growing demand for food, large retailers have to invest significant amount of resources in

building backend infrastructure- warehouses, cold storages and linkages with large number of

farmers. If India’s policy makers fail to facilitate this, food inflation will keep increasing.

On the employment side, modernization of the retail sector through the entry of large retailers

will have some disruptive effects in the short run that there will be some direct job losses

especially unskilled labor and generation of jobs for semi-skilled labor. Most of the jobs that are

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 18

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

created in the large retailers such as the Reliance are workers with basic computer and English

language skills

Turnover per employee for the retail sector in India is about Rs. 340,000 per annum. The

turnover per employee for Wal-Mart International is about Rs. 9,971,057 which is 29 times that

of the unorganized sector in India. If foreign players capture 10 per cent share by 2015, that will

turn out to be Rs. 189660 million with employment of 19000 employees replacing about 0.55

million in the unorganized sector (Ray et al, 2012). A study by Price Water Cooper (2011)

shows every 50,000 square feet of development creates direct employment for 200 people.

Based on these estimates 1.5 million jobs will be created in the frontend retail activities by

2015. Apart from this, 10-20% more jobs will be for backend activities. The direct employment

will be close to 1.8 million. This does not take into account of net effect of employment through

expansion of markets, and incomes. If output expands through modernization of the retail, it will

increase real incomes (and savings) and generates employment in other sectors. In the case of

wage levels, the 20 organized retail sector has to adhere to the labor market regulations which

means workers will be better off than being employed in the unorganized.

As mentioned earlier, close to 30 per cent of manufacturing exports of China are accounted by

Wal-Mart. If Wal-Mart is able to replicate its global supply chain practice in India it can source

manufacturing exports from India which will generate employment. China is transforming into a

middle-income country with a per capital income of about $ 5000. This will increase wage costsin the manufacturing. This is where India can take advantage by letting the manufacturing

industry to move to India by improving infrastructure, literacy rates and reducing transaction

costs of business

CONCLUSION:

Evidently, there is no national consensus on allowing FDI in retail. Advocates tout it as the

much-needed major policy push that could arrest the economic downturn, bring in not only

foreign funds but advanced technology and expertise, create infrastructure, offer better prices to

farmers, generate ancillary industries and create millions of jobs. However, sceptics present a

doomsday scenario: it will wipe out small farmers and traders result in job losses and open the

floodgates for cheap goods from countries like China, adversely impacting Indian industry.

While both arguments have some validity, the two sides err on the side of extremes. FDI in

retail is not an unmitigated disaster as projected by some, nor a magic wand leading to instant

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 19

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar

economic growth. If allowed with professional circumspection and safeguards and viewed

dispassionately, it is in the country's national interest to allow FDI in retail. Opening up the

telecom sector to foreign investment worked by bringing a communication revolution that

embraces everyone. Similarly, foreign investment in the automobile industry ended the long

wait for outdated scooters and cars and led to leading global companies vying to sell the latest

models in India. When Pizza Hut, Domino's, McDonald's, Wimpy, Burger King, KFC and other

such international brands were allowed, there were orchestrated demonstration in many cities;

they were painted as anti-people and anti-Indian enterprises. We were told Haldirams,

Bikanerwalas, Nirulas, Nathus and their ilk will vanish. All these Indian chains have multiplied

their outlets, diversified their production line, upgraded their packing and presentation, and are

doing roaring business. In fact, some of the largest MNCs like McDonald's, Pizza Hut and

Domino's have been forced to Indianise their offerings. Where else in the world would you find

a McDonald burger with paneer and potato patties and coriander sauce? While many starve,

millions of tonnes of grain rot for want of adequate storage facilities. Ask how farmers in

Punjab feel when their produce is not picked up and lies unsold. Can they negotiate higher

prices? When the mercury rises, fruit don't last more than two days. TV channels often show

how adulterated ghee, milk made out of detergent, mangoes and papayas ripened with masala,

vegetables and fruit injected with dangerous concoctions are flooding the market. Who is to

blame? FDI in retail? No one should underestimate the ingenuity of ordinary hawkers and smallgrocery owners. They know how to reach out to their potential customers. Today, in many areas

of Delhi, vegetable vendors present their carts, laden with fresh stuff straight from the farm, as

early as 6:00 am. Many joggers and walkers find it convenient to pick up their daily requirement

of vegetables from these vendors. In the evening, they move near temples where devotees find it

a blessing to shop for fruit and vegetables at the temple gates. Small grocery shops realise the

value of home delivery, small stores also reduce a rupee or two on most items. This demand-

and-supply relationship will remain unchanged notwithstanding the entry of bigwigs like Tesco,

Carrefour and Wal-Mart.

REFERENCES:

1- Murali Patibandla, FDI in Retail Sector: Some Issue, Working Paper No: 366

2- Amisha Gupta, FDI in Retail Sector: Strategic Issue and Publications, IJMMR, Volume

1 Dec, 2010

Capstone Project: FDI in Indian Retail Sector and Its Implication Page 20

7/29/2019 FDI in Indian Retail Sector_Santosh Kumar