34

1 February 4, 2008, www.atlascopco.com Atlas Copco Group Q4 Results February 4, 2008

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | misael-rodgers |

| View: | 220 times |

| Download: | 6 times |

1February 4, 2008, www.atlascopco.com

Atlas Copco Group

Q4 Results

February 4, 2008

2February 4, 2008, www.atlascopco.com

Contents

Q4 Business Highlights

Market Development

Business Areas

Financials

2007 Summary

Outlook

3February 4, 2008, www.atlascopco.com

Q4 - Highlights

Growth accelerated– High organic order growth

– Double-digit in all regions

Strong development for both capital equipment and aftermarket

Excellent performance in all Business areas

Record operating profits

Increased dividend and proposed share buy-back mandate

4February 4, 2008, www.atlascopco.com

Q4 - Figures in summary

Orders up 33%; 20% organic growth

Revenues up 29% to MSEK 17 549; 18% organic growth

Operating profit up 36% to MSEK 3 361– Operating margin at record 19.2% (18.1)

Profit before tax at MSEK 2 134 (2 382)– Includes MSEK 864 write-down of right to notes

Earnings per share for continuing operations SEK 1.83 (1.42), excluding non-recurring write-down

Operating cash flow, continuing operations, MSEK 926 (474)

5February 4, 2008, www.atlascopco.com

Contents

Q4 Business Highlights

Market Development

Business Areas

Financials

2007 Summary

Outlook

6February 4, 2008, www.atlascopco.com

Orders received - Local currencyGroup total +29% YTD, +35% last 3 months(Structural change +11% YTD, +15% last 3 months)

December 2007

7 +34 +10

10 +41 +47

18 +33 +30

5 +33 +45

40 +28 +37

20 +25 +37

A B CA = Portion of sales, Year-to-date, %

B = Year-to-date vs. prev. year, %

C = Last 3 months vs. prev. year, %

7February 4, 2008, www.atlascopco.com

Q4 - The Americas

Good growth in North America– Strong demand from mining customers in

Canada and Mexico

– Demand from the motor vehicle industry and parts of the construction market related to housing still on a weaker level

Positive development within most customer segments in South America

December 2007 A = Portion of sales, Year-to-date, %

B = Year-to-date vs. prev. year, %

C = Last 3 months vs. prev. year, %

A B C

7 +34 +10

20 +25 +37

8February 4, 2008, www.atlascopco.com

Q4 - Europe and Africa/Middle East

Solid organic growth in Europe– Strong demand for compressed air

equipment and industrial tools

– Mining segment strong while construction leveled off in Western Europe

– Very strong growth in Russia

High growth continues in the Africa / Middle East region – Increased demand for industrial and

construction equipment in the Middle East

– Strong development in mining in Southern Africa

December 2007

A B CA = Portion of sales, Year-to-date, %

B = Year-to-date vs. prev. year, %

C = Last 3 months vs. prev. year, %

10 +41 +47

40 +28 +37

9February 4, 2008, www.atlascopco.com

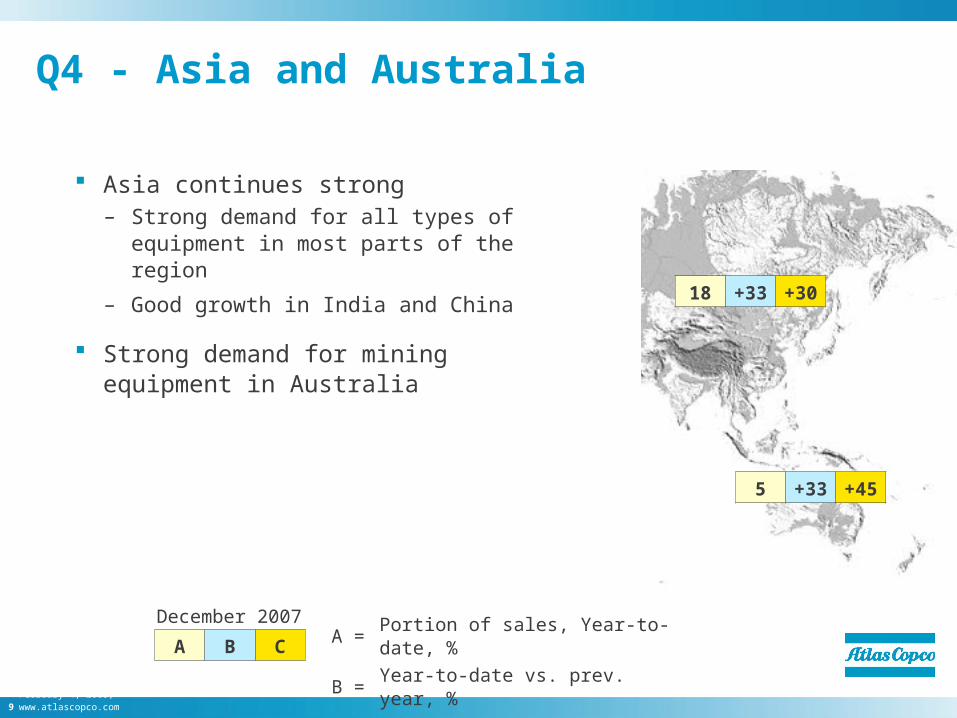

Q4 - Asia and Australia

Asia continues strong– Strong demand for all types of equipment in

most parts of the region

– Good growth in India and China

Strong demand for mining equipment in Australia

December 2007 A = Portion of sales, Year-to-date, %

B = Year-to-date vs. prev. year, %

C = Last 3 months vs. prev. year, %

A B C

18 +33 +30

5 +33 +45

10February 4, 2008, www.atlascopco.com

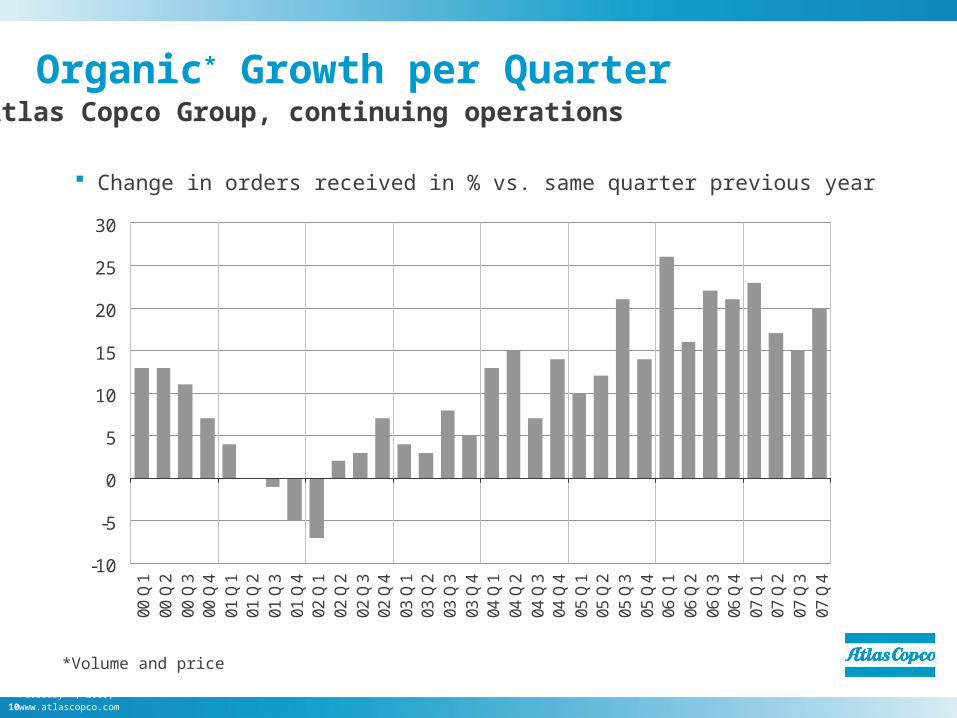

Organic* Growth per Quarter

Change in orders received in % vs. same quarter previous year

Atlas Copco Group, continuing operations

-10

-5

0

5

10

15

20

25

30

00 Q

100

Q2

00 Q

300

Q4

01 Q

101

Q2

01 Q

301

Q4

02 Q

102

Q2

02 Q

302

Q4

03 Q

103

Q2

03 Q

303

Q4

04 Q

104

Q2

04 Q

304

Q4

05 Q

105

Q2

05 Q

305

Q4

06 Q

106

Q2

06 Q

306

Q4

07 Q

107

Q2

07 Q

307

Q4

*Volume and price

11February 4, 2008, www.atlascopco.com

Atlas Copco

15%

21%

0%

10%

20%

30%

2003 2004 2005 2006 2007Organic growth, % Structural changes, %

CAGR, 2003 - 2007, organic growth CAGR, 2003 - 2007, total excl. currency

Growth – Orders receivedContinuing operations (excl. Professional Electric Tools and Rental Service)

12February 4, 2008, www.atlascopco.com

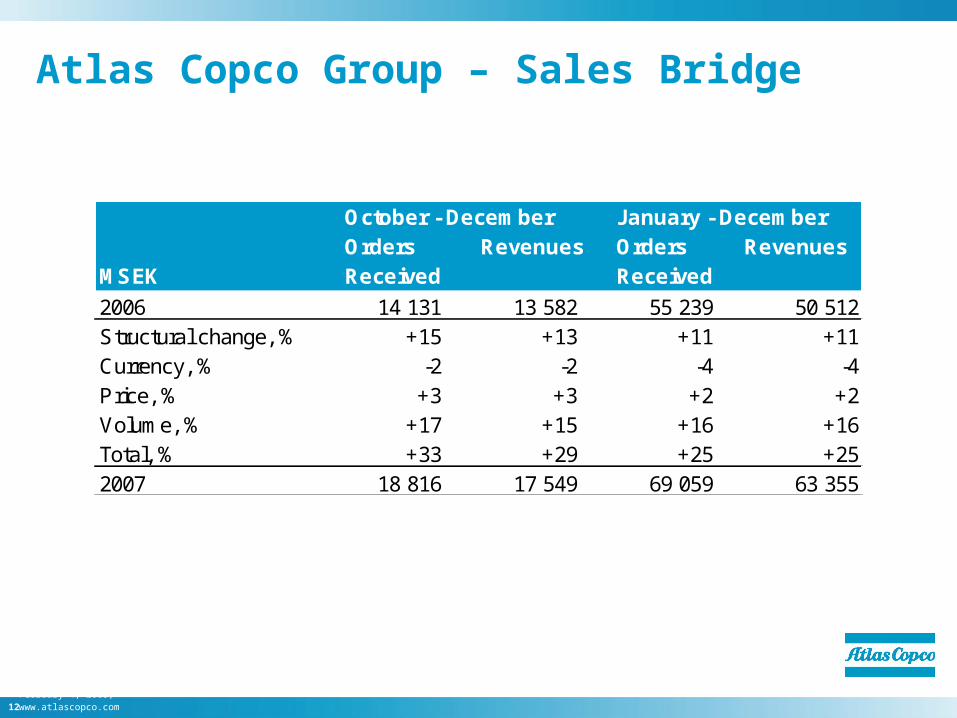

Atlas Copco Group – Sales Bridge

October - December January - DecemberOrders Revenues Orders Revenues

MSEK Received Received

2006 14 131 13 582 55 239 50 512Structural change, % +15 +13 +11 +11Currency, % -2 -2 -4 -4Price, % +3 +3 +2 +2Volume, % +17 +15 +16 +16Total, % +33 +29 +25 +252007 18 816 17 549 69 059 63 355

13February 4, 2008, www.atlascopco.com

Contents

Q4 Business Highlights

Market Development

Business Areas

Financials

2007 Summary

Outlook

14February 4, 2008, www.atlascopco.com

Revenues Operating Operating ROCEMSEK profit margin12 month values, period ending Dec. 2007 Dec. 2007 Dec. 2007 Dec. 2007

Compressor Technique 31 900 6 749 21.2% 65%Construction and Mining Technique 25 140 4 384 17.4% 32%Industrial Technique 6 871 1 539 22.4% 58%Eliminations/Common Group Functions -556 -606Atlas Copco Group 63 355 12 066 19.0% 31%*

Atlas Copco GroupOperating Profit and Return On Capital Employed (ROCE) by Business Area

*excluding non-recurring write-down of RSC notes

15February 4, 2008, www.atlascopco.com

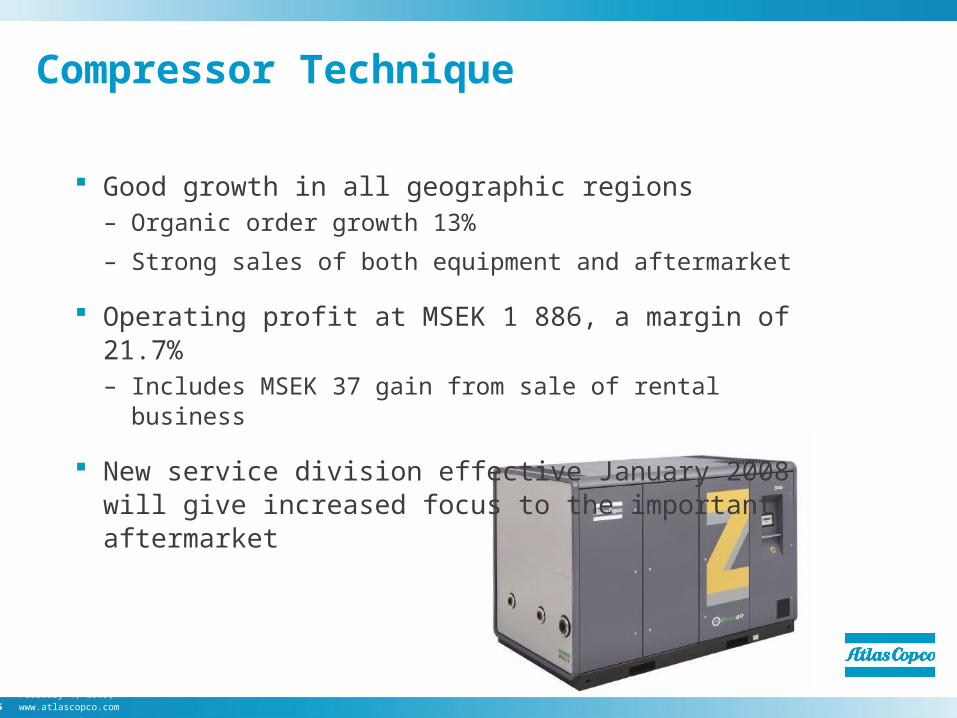

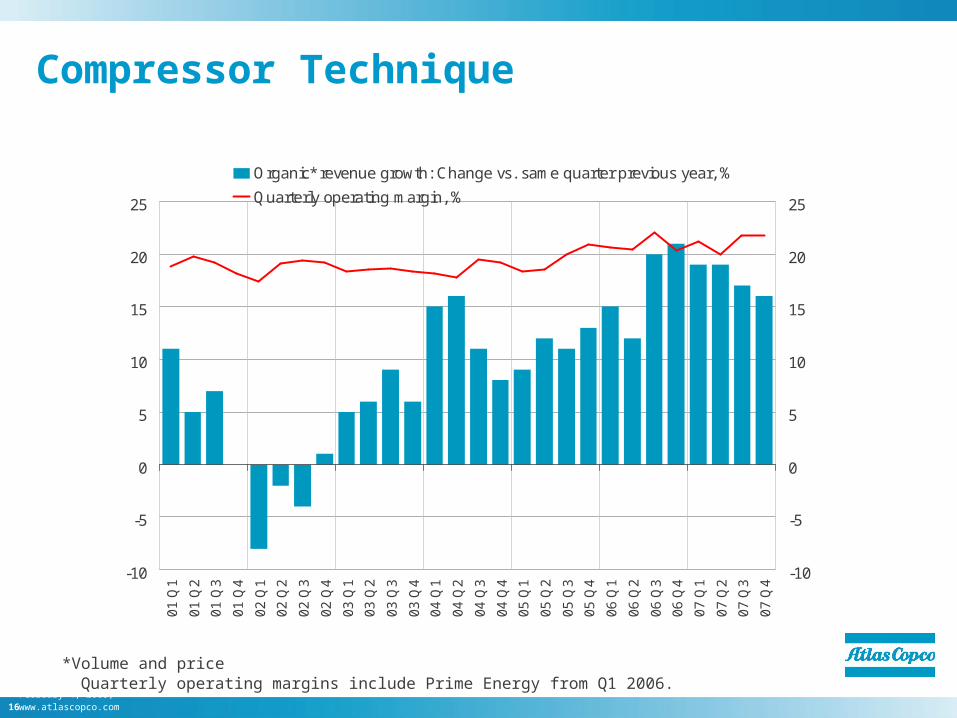

Compressor Technique

Good growth in all geographic regions– Organic order growth 13%

– Strong sales of both equipment and aftermarket

Operating profit at MSEK 1 886, a margin of 21.7%– Includes MSEK 37 gain from sale of rental business

New service division effective January 2008 will give increased focus to the important aftermarket

15February 4, 2008, www.atlascopco.com

16February 4, 2008, www.atlascopco.com

Compressor Technique

-10

-5

0

5

10

15

20

25

-10

-5

0

5

10

15

20

25

01

Q1

01

Q2

01

Q3

01

Q4

02

Q1

02

Q2

02

Q3

02

Q4

03

Q1

03

Q2

03

Q3

03

Q4

04

Q1

04

Q2

04

Q3

04

Q4

05

Q1

05

Q2

05

Q3

05

Q4

06

Q1

06

Q2

06

Q3

06

Q4

07

Q1

07

Q2

07

Q3

07

Q4

Organic* revenue growth: Change vs. same quarter previous year, %

Quarterly operating margin, %

Quarterly operating margins include Prime Energy from Q1 2006.*Volume and price

17February 4, 2008, www.atlascopco.com

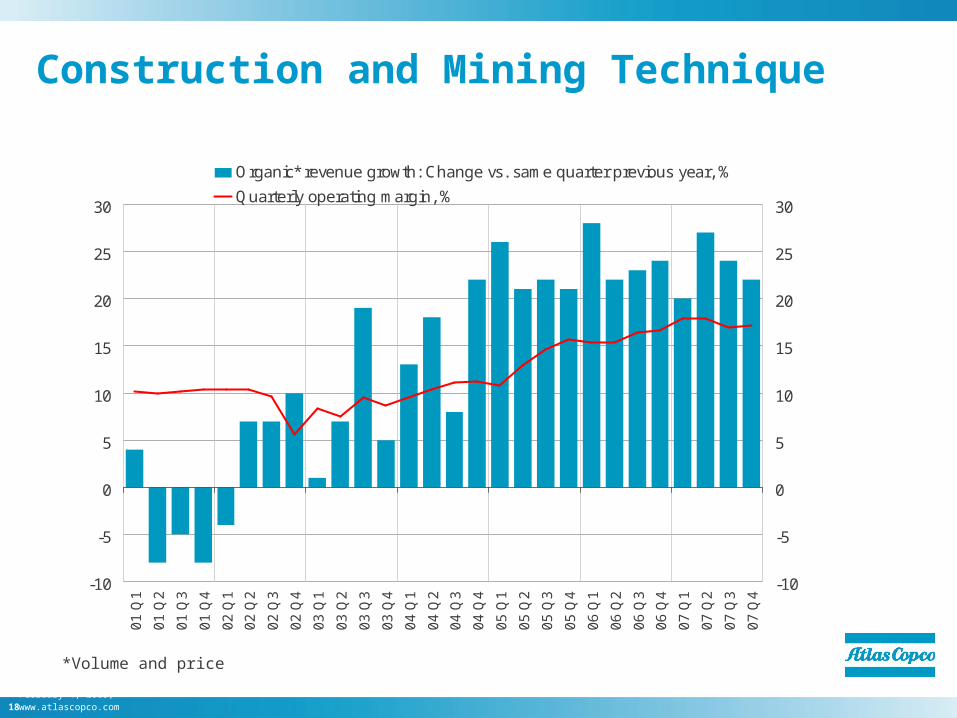

Very strong increase in demand from the mining segment

Organic order growth 30%– 23rd consecutive quarter with volume

growth

Operating profit up 47%, margin at 17.2%– 20% margin for comparable units

Construction and Mining Technique

18February 4, 2008, www.atlascopco.com

-10

-5

0

5

10

15

20

25

30

-10

-5

0

5

10

15

20

25

30

01

Q1

01

Q2

01

Q3

01

Q4

02

Q1

02

Q2

02

Q3

02

Q4

03

Q1

03

Q2

03

Q3

03

Q4

04

Q1

04

Q2

04

Q3

04

Q4

05

Q1

05

Q2

05

Q3

05

Q4

06

Q1

06

Q2

06

Q3

06

Q4

07

Q1

07

Q2

07

Q3

07

Q4

Organic* revenue growth: Change vs. same quarter previous year, %

Quarterly operating margin, %

Construction and Mining Technique

*Volume and price

19February 4, 2008, www.atlascopco.com

Industrial Technique

Volume growth, both in general industry and motor vehicle industry – 11% organic order growth

– North America still slow for motor vehicle industry

Operating profit-margin at 22.2%, including restructuring costs

Acquisition of Japanese air tools manufacturer, strengthening presence in vehicle service market

20February 4, 2008, www.atlascopco.com

Industrial Technique

-5

0

5

10

15

20

25

-5

0

5

10

15

20

25

03

Q1

03

Q2

03

Q3

03

Q4

04

Q1

04

Q2

04

Q3

04

Q4

05

Q1

05

Q2

05

Q3

05

Q4

06

Q1

06

Q2

06

Q3

06

Q4

07

Q1

07

Q2

07

Q3

07

Q4

Organic* revenue growth: Change vs. same quarter previous year, %

Quarterly operating margin, %

*Volume and price

21February 4, 2008, www.atlascopco.com

Contents

Q4 Business Highlights

Market Development

Business Areas

Financials

2007 Summary

Outlook

22February 4, 2008, www.atlascopco.com

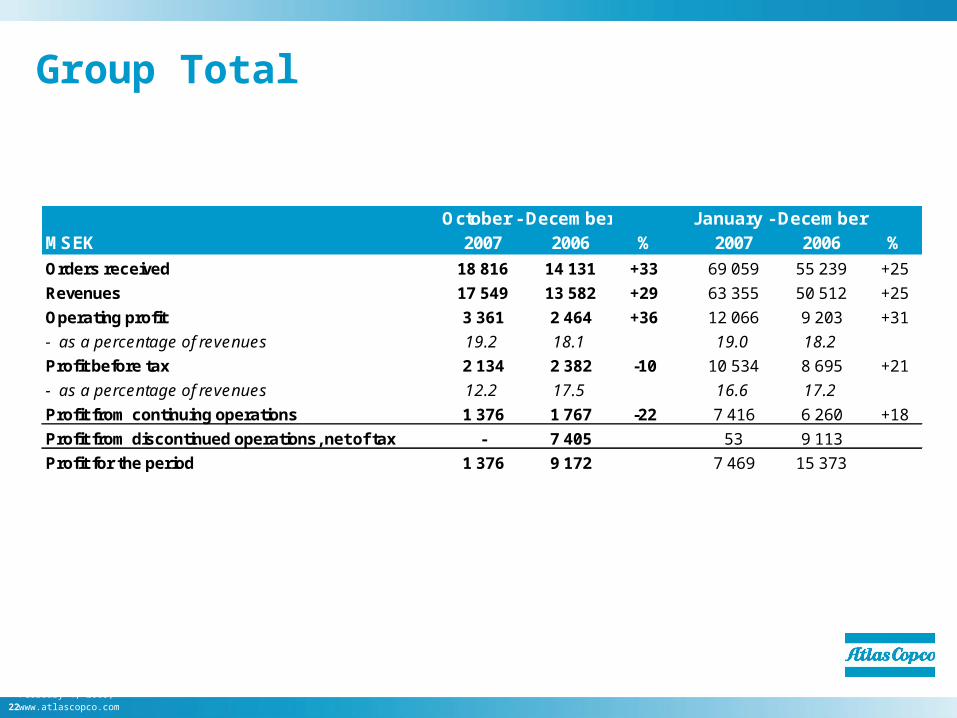

Group Total

October - December January - DecemberMSEK 2007 2006 % 2007 2006 %

Orders received 18 816 14 131 +33 69 059 55 239 +25

Revenues 17 549 13 582 +29 63 355 50 512 +25

Operating profit 3 361 2 464 +36 12 066 9 203 +31

- as a percentage of revenues 19.2 18.1 19.0 18.2

Profit before tax 2 134 2 382 -10 10 534 8 695 +21

- as a percentage of revenues 12.2 17.5 16.6 17.2

Profit from continuing operations 1 376 1 767 -22 7 416 6 260 +18

Profit from discontinued operations, net of tax - 7 405 53 9 113

Profit for the period 1 376 9 172 7 469 15 373

23February 4, 2008, www.atlascopco.com

Profit BridgeOctober – December, 2007 vs 2006

Organic Growth One-time items

MSEK Price/Volume Acq./Div.

Atlas Copco Group

Revenues 17 549 2 427 -270 1 810 13 582

EBIT 3 361 977 -220 140 2 464

% 19.2% 40% - 8% 18.1%

Q4 2007 Currency Q4 2006

One-time items on corporate level include an accounting adjustment related to the personnel stock option program

24February 4, 2008, www.atlascopco.com

Profit Bridge – by Business AreaOctober – December, 2007 vs 2006

Q4 2007 Organic Growth Currency One-time items Q4 2006

MSEK Price/Volume Acq./Div.

Compressor Technique

Revenues 8 676 1 132 -100 700 6 944

EBIT 1 886 430 -130 175 1 411

% 21.7% 38% - 25% 20.3%

Construction & Mining Technique

Revenues 7 121 1 136 -125 1 050 5 060

EBIT 1 228 430 -60 20 838

% 17.2% 38% - 2% 16.6%

Industrial Technique

Revenues 1 920 238 -22 62 1 642

EBIT 426 101 -15 -8 348

% 22.2% 42% - -13% 21.2%

One-time items include a charge related to pension benefits in 2006 and a capital gain for the divestment of a rental company in Compressor Technique and restructuring costs in Industrial Technique

25February 4, 2008, www.atlascopco.com

Balance Sheet

MSEK Dec 31, 2007 Dec 31, 2006

Intangible assets 11 665 21% 4 299 8%

Rental equipment 1 906 3% 1 979 4%

Other property, plant and equipment 4 894 9% 3 777 7%

Other fixed assets 4 245 7% 3 161 6%

Inventories 12 725 22% 8 487 15%

Receivables 16 627 29% 12 401 22%

Current financial assets 1 124 2% 1 016 2%

Cash and cash equivalents 3 473 6% 20 135 36%

TOTAL ASSETS 56 659 55 255

Total equity 14 640 26% 32 708 59%

Interest-bearing liabilities 24 397 43% 8 787 16%

Non-interest-bearing liabilities 17 622 31% 13 760 25%

TOTAL EQUITY AND LIABILITIES 56 659 55 255

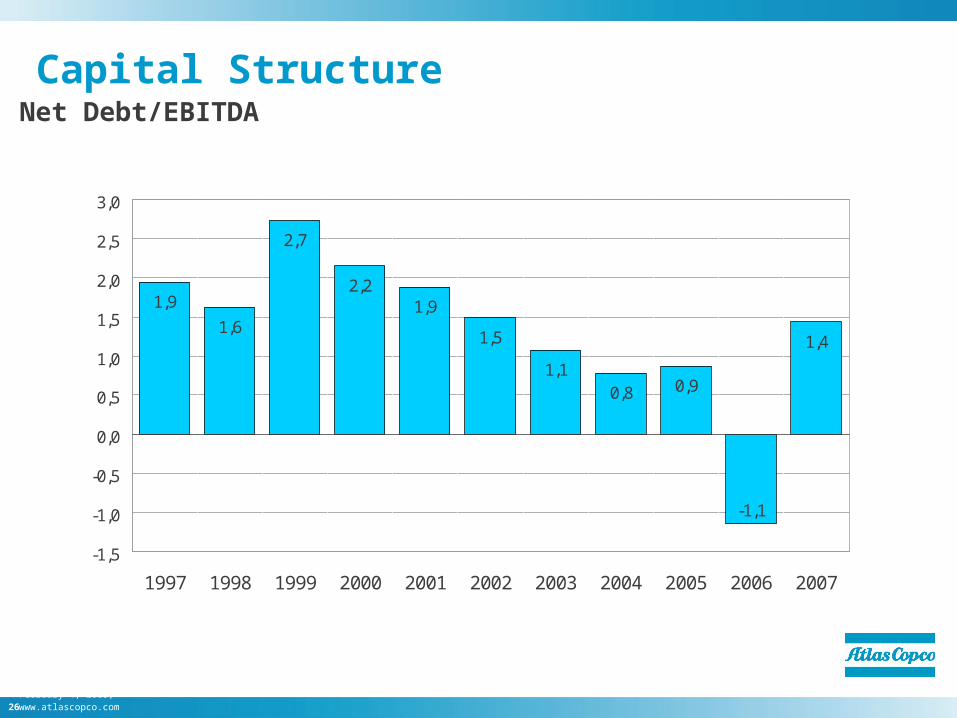

26February 4, 2008, www.atlascopco.com

1,9

1,6

2,7

2,21,9

1,5

1,10,8 0,9

-1,1

1,4

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Capital Structure Net Debt/EBITDA

27February 4, 2008, www.atlascopco.com

Cash FlowContinuing operations

October - December January - DecemberMSEK 2007 2006* 2007 2006*

Operating cash surplus after tax 2 693 1 777 10 005 8 197 of which depreciation added back 498 449 1 800 1 637Change in working capital -865 -462 -2 326 -2 045 Cash flows from operating activities 1 828 1 315 7 679 6 152Investments in tangible fixed assets -652 -543 -2 359 -2 167Sale of tangible fixed assets 180 163 712 586Other investments, net -430 -461 -1 443 -1 506Cash flow from investments -902 -841 -3 090 -3 087 Operating cash flow 926 474 4 589 3 065Company acquisitions/ divestments 32 -282 -5 718 -1 332*Restated, continuing operations

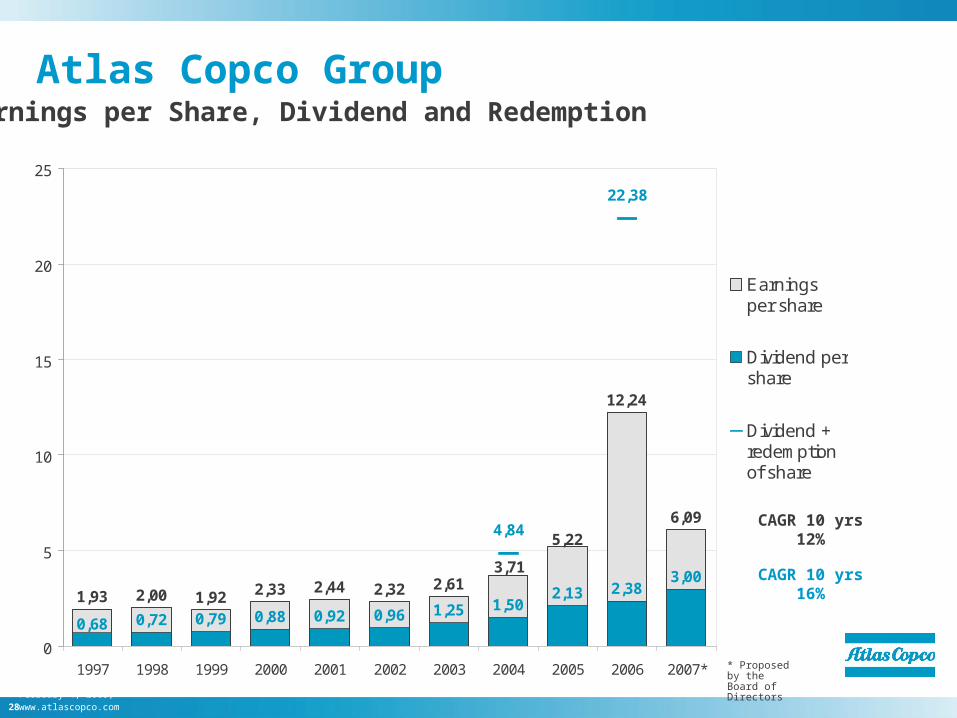

28February 4, 2008, www.atlascopco.com

1,93 2,00 1,92 2,33 2,44 2,32 2,61

12,24

6,09

0,72 0,79 0,88 0,92 0,96 1,25 1,502,13 2,38

3,003,71

5,22

0,68

4,84

22,38

0

5

10

15

20

25

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007*

Earningsper share

Dividend pershare

Dividend +redemptionof share

Atlas Copco GroupEarnings per Share, Dividend and Redemption

* Proposed by the Board of Directors

CAGR 10 yrs 12%

CAGR 10 yrs 16%

29February 4, 2008, www.atlascopco.com

Contents

Q4 Business Highlights

Market Development

Business Areas

Financials

2007 Summary

Outlook

30February 4, 2008, www.atlascopco.com

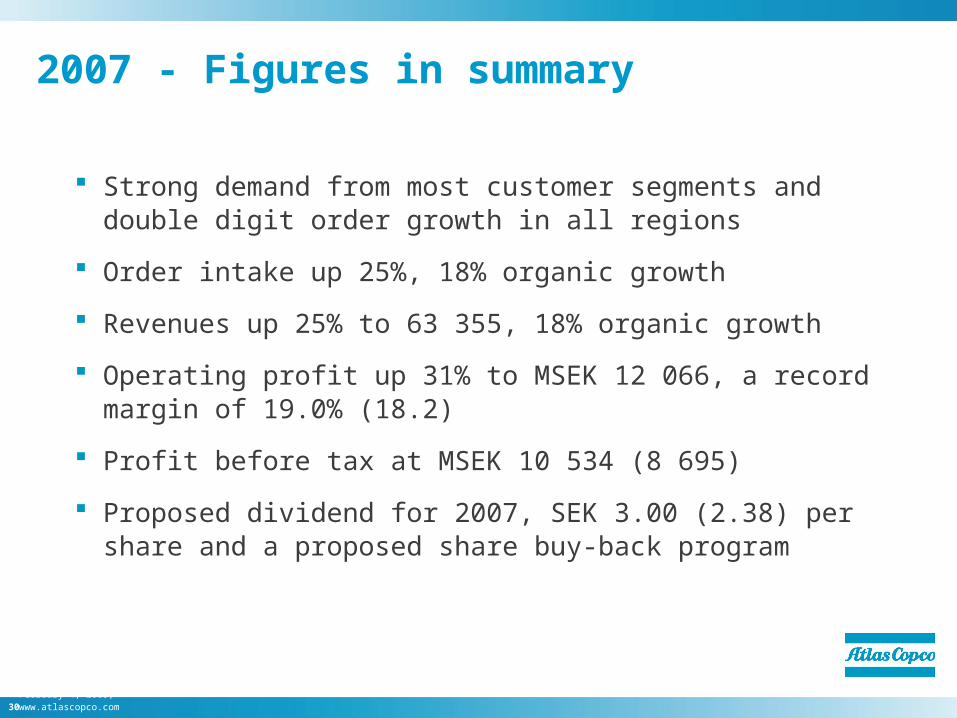

2007 - Figures in summary

Strong demand from most customer segments and double digit order growth in all regions

Order intake up 25%, 18% organic growth

Revenues up 25% to 63 355, 18% organic growth

Operating profit up 31% to MSEK 12 066, a record margin of 19.0% (18.2)

Profit before tax at MSEK 10 534 (8 695)

Proposed dividend for 2007, SEK 3.00 (2.38) per share and a proposed share buy-back program

31February 4, 2008, www.atlascopco.com

Contents

Q4 Business Highlights

Market Development

Business Areas

Financials

2007 Summary

Outlook

32February 4, 2008, www.atlascopco.com

Near-term Outlook

The demand for Atlas Copco’s products and services from most customer segments and regions is expected to remain at the current high level.

The positive outlook includes the main part of the construction segment, while construction related to housing is expected to remain weak, primarily in North America.

33

34February 4, 2008, www.atlascopco.com

Cautionary Statement

“Some statements herein are forward-looking and the actual outcome could be materially different. In addition to the factors explicitly commented upon, the actual outcome could be materially effected by other factors like for example, the effect of economic conditions, exchange-rate and interest-rate movements, political risks, impact of competing products and their pricing, product development, commercialization and technological difficulties, supply disturbances, and major customer credit losses.”