FEDERAL RESERVE ADOPTS RULE REQUIRING GSIBs TO AMEND QFC TRANSACTIONS TO LIMIT TERMINATION RIGHTS OF COUNTERPARTIES By William Shirley and Miki Navazio The authors are lawyers in the Deriva- tives Industry Group of the international law firm Sidley Austin LLP. This article is for informational purposes only and does not constitute legal advice. This information is not intended to create, and the receipt of it does not constitute, a lawyer-client relationship. Readers should not act upon this information without seeking advice from professional advisers. The content of this article does not reflect the views of Sidley Austin LLP. On September 1, 2017, the Board of Governors of the Federal Reserve System (the Federal Reserve) adopted a rule (the Rule) 1 that will require global systemi- cally important U.S. bank holding compa- nies (U.S. GSIBs) 2 and most of their sub- sidiaries to amend a range of derivatives, short-term funding transactions, securities lending transactions and other qualifying financial contracts (QFCs). The required amendments will limit counterparty termi- nation rights related to certain U.S. GSIB resolution and bankruptcy proceedings. Banks and other depository institutions regulated by the Office of the Comptroller of the Currency (OCC) or the Federal De- posit Insurance Corporation (FDIC) are “excluded banks” under the Rule, but they will be subject to “substantively identical” rules adopted by those agencies. 3 Overview of the Rule Entities subject to the Rule’s require- ments are defined as “covered entities.” That term includes all U.S. GSIB parents and subsidiaries other than excluded banks and certain limited categories of other subsidiaries. 4 It also includes the U.S. operations of global systemically important foreign banking organizations (non-U.S. GSIBs). 5 The Rule will require covered entities, when entering into certain QFC transac- tions with buy-side counterparties (as well as with other covered entities and ex- cluded banks), to include specific contract terms in related agreements. Those terms are intended to achieve two distinct regu- latory goals: (i) ensure cross-border en- forcement of the two U.S. special resolu- tion regimes—the orderly liquidation authority under Title II of the Dodd-Frank Act (OLA) and the Federal Deposit Insur- ance Act (FDIA)—as they may apply to covered entities; and (ii) prohibit counter- parties of a covered entity from exercising a range of cross-default rights that are re- lated, directly or indirectly, to an affiliate of the covered entity becoming subject to insolvency proceedings, including under Chapter 11 of the Bankruptcy Code. Reprinted with permission from Futures and Derivatives Law Report, Vol- ume 37, Issue 10, K2017 Thomson Reuters. Further reproduction without permission of the publisher is prohibited. For additional information about this publication, please visit www.legalsolutions.thomsonreuters.com. REPORT The Journal on the Law of Investment & Risk Management Products Futures & Derivatives Law November 2017 ▪ Volume 37 ▪ Issue 10

Transcript

FEDERAL RESERVE

ADOPTS RULE

REQUIRING GSIBs TO

AMEND QFC

TRANSACTIONS TO

LIMIT TERMINATION

RIGHTS OF

COUNTERPARTIES

By William Shirley and Miki Navazio

The authors are lawyers in the Deriva-

tives Industry Group of the international

law firm Sidley Austin LLP. This article

is for informational purposes only and

does not constitute legal advice. This

information is not intended to create,

and the receipt of it does not constitute,

a lawyer-client relationship. Readers

should not act upon this information

without seeking advice from professional

advisers. The content of this article does

not reflect the views of Sidley Austin

LLP.

On September 1, 2017, the Board of

Governors of the Federal Reserve System

(the Federal Reserve) adopted a rule (the

Rule)1 that will require global systemi-

cally important U.S. bank holding compa-

nies (U.S. GSIBs)2 and most of their sub-

sidiaries to amend a range of derivatives,

short-term funding transactions, securities

lending transactions and other qualifying

financial contracts (QFCs). The required

amendments will limit counterparty termi-

nation rights related to certain U.S. GSIB

resolution and bankruptcy proceedings.

Banks and other depository institutions

regulated by the Office of the Comptroller

of the Currency (OCC) or the Federal De-

posit Insurance Corporation (FDIC) are

“excluded banks” under the Rule, but they

will be subject to “substantively identical”

rules adopted by those agencies.3

Overview of the Rule

Entities subject to the Rule’s require-

ments are defined as “covered entities.”

That term includes all U.S. GSIB parents

and subsidiaries other than excluded

banks and certain limited categories of

other subsidiaries.4 It also includes the

U.S. operations of global systemically

important foreign banking organizations

(non-U.S. GSIBs).5

The Rule will require covered entities,

when entering into certain QFC transac-

tions with buy-side counterparties (as well

as with other covered entities and ex-

cluded banks), to include specific contract

terms in related agreements. Those terms

are intended to achieve two distinct regu-

latory goals: (i) ensure cross-border en-

forcement of the two U.S. special resolu-

tion regimes—the orderly liquidation

authority under Title II of the Dodd-Frank

Act (OLA) and the Federal Deposit Insur-

ance Act (FDIA)—as they may apply to

covered entities; and (ii) prohibit counter-

parties of a covered entity from exercising

a range of cross-default rights that are re-

lated, directly or indirectly, to an affiliate

of the covered entity becoming subject to

insolvency proceedings, including under

Chapter 11 of the Bankruptcy Code.

Reprinted with permission from Futures and Derivatives Law Report, Vol-ume 37, Issue 10, K2017 Thomson Reuters. Further reproduction withoutpermission of the publisher is prohibited. For additional information aboutthis publication, please visit www.legalsolutions.thomsonreuters.com.

RE

PO

RT

Th

eJo

urn

alo

nth

eL

awo

fIn

vest

men

t&

Ris

kM

anag

emen

tP

rod

uct

s

Fu

ture

s&

De

riva

tive

sL

aw

November 2017 ▪ Volume 37 ▪ Issue 10

The Rule includes a safe harbor for QFCs that

are amended by a covered entity and a given

counterparty through their adherence to a qualify-

ing protocol published (or to be published) by the

International Swaps and Derivatives Association

Inc. (ISDA). The safe harbor was provided even

though the contract terms resulting from adher-

ence to the qualifying ISDA protocols will differ

in certain important respects from the contract

terms that the Rule otherwise requires. Accord-

ingly, the means by which a covered entity and a

given counterparty choose to comply with the

Rule will involve choosing not only between

contracting mechanisms (protocol adherence

versus bilateral documentation execution) but

also between contractual terms that differ

substantively.

Compliance with the Rule will be phased in

over one year beginning January 1, 2019. How-

ever, as discussed toward the end of this article,

it is likely that covered entities will seek to ensure

Rule compliance with all counterparties by Janu-

ary 1, 2019, including those counterparties for

which the phase-in date is later.

In the balance of this article, we will address

the following topics:

E QFC Transactions Covered by the Rule

E Basic Operation of the Rule

E U.S. Special Resolution Regimes and Re-

quired Opt-In Provisions

E U.S. Bankruptcy Code and Restrictions on

Cross-Defaults

E ISDA Protocols

E Differences Between the Rule’s Stated

Requirements and the ISDA Protocols

E Other Issues

E Observations

QFC Transactions Covered by theRule

The Rule incorporates the Dodd-Frank Act’s

definition of QFC. That definition includes

“swaps, repo and reverse repo transactions, secu-

rities lending and borrowing transactions, com-

modity contracts, and forward agreements.”6 To

narrow the breadth of the Rule’s application, the

Rule applies only to “covered QFCs.” The defi-

nition of covered QFC narrows the Rule’s reach

in two respects. The first considers the terms of a

QFC to determine if it is “in scope” under the

Rule. The second considers the date that the re-

spective covered entity entered into the in-scope

QFC (or certain related QFCs) to determine if it

is a covered QFC (or, alternatively, whether the

QFC, though in scope, is effectively

grandfathered).7

A QFC is in scope if it either

E explicitly restricts transfer of the QFC (or

any interest or obligation in or under, or any

property securing, the QFC) from a covered

entity (whether or not in connection with

any default) or

E explicitly provides one or more “default

rights” with respect to a QFC that may be

exercised against a covered entity.

The Rule defines “default rights” very broadly.

The definition encompasses not only typical

termination and liquidation rights but also rights

to demand additional collateral or margin (other

than where the demand is based solely on mark-

to-market requirements).8 Thus, for example, a

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

2 K 2017 Thomson Reuters

typical credit rating downgrade provision would

be covered.9

Because of the broad definition, most swap,

repurchase and securities lending transactions

that are subject to industry standard master agree-

ments will be in scope. In contrast, spot foreign

exchange transactions, though they are QFCs,

will not be in scope if they are not subject to ex-

plicit terms restricting transfers or providing

default rights. That may be true for many such

transactions,10 but caution is warranted because

trading relationships with covered entities may

be subject to broadly worded master agreements

or other umbrella trading documentation.

An in-scope QFC will be a covered QFC if it

is entered into11 by a covered entity after January

1, 2019 (irrespective of the type of QFC counter-

party or related compliance phase-in date, as

discussed below). In addition, if a covered entity

and a given counterparty enter into a QFC

(whether or not in scope) after January 1, 2019,

then all in-scope QFCs between the two parties

entered into prior to January 1, 2019 will become

covered QFCs automatically. Moreover, the Rule

includes a triggering mechanism for covered

QFCs that is tied to affiliation: If a QFC (whether

or not in scope) is executed on or after January 1,

2019 between (i) a covered entity or any affiliate

that is either a covered entity or an excluded

bank; and (ii) a counterparty or any of its consoli-

dated affiliates, then all in-scope QFCs between

the first covered entity and the counterparty or

any of the counterparty’s consolidated affiliates

will become covered QFCs automatically (re-

gardless of when the in-scope QFCs were

executed).12

In other words, if, after January 1, 2019, any

member of a given consolidated counterparty

group trades with a covered entity or an excluded

bank within a given covered entity group, all in-

scope QFCs between the two groups become

covered QFCs. The interplay between the “cov-

ered QFC” definition and the compliance

phase-in schedule is discussed toward the end of

this article, as are the specifics of the affiliation

triggers (see “Other Issues”).

Basic Operation of the Rule

The Rule operates in two distinct ways:

E In order to ensure cross-border enforcement

of the two U.S. special resolution regimes,

the Rule requires covered entities to include

terms, in certain covered QFCs, pursuant to

which their counterparties “opt in” to the

stay-and-transfer provisions of those

regimes.

E In order to address perceived inadequacies

of Chapter 11 of the Bankruptcy Code (and

other insolvency regimes), the Rule prohib-

its certain covered QFCs from permitting

counterparties to exercise a range of cross-

default rights that are related, directly or

indirectly, to an affiliate of the covered

entity’s becoming subject to proceedings

under the Bankruptcy Code or any other

receivership, insolvency, liquidation, reso-

lution or similar proceedings.13

Analogs for the first requirement (opt in) have

been adopted or are under consideration by

regulators in the United Kingdom, Germany,

France, Switzerland and Japan. The second re-

quirement (cross-default) is unique to the United

States. The two requirements are separately

discussed below.

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

3K 2017 Thomson Reuters

U.S. Special Resolution Regimesand Required Opt-In Provisions

The term “U.S. special resolution regimes”

means the FDIA, which governs the resolution of

FDIC-insured depository institutions, and OLA,

which governs certain resolutions of systemically

important financial institutions. The Federal

Reserve explained that

The [U.S. special resolution regimes] create

special resolution frameworks for failed financial

firms that provide that the rights of a failed firm’s

counterparties to terminate their QFCs are tempo-

rarily stayed when the firm enters a resolution

proceeding to allow for the transfer of the rele-

vant obligations under the QFC to a solvent party.

Such temporary stays generally last until the

end of the business day following the appoint-

ment of the FDIC as receiver.

Subject to certain exceptions (described be-

low), the Rule requires that each covered QFC of

a covered entity “explicitly” provide that in the

event the covered entity becomes subject to a

proceeding under a U.S. special resolution re-

gime,

E the transfer of the covered QFC (and any

interest and obligation in or under, and any

property securing it) from the covered

entity will be effective to the same extent

as the transfer would be effective under the

U.S. special resolution regime if the cov-

ered QFC (and any interest and obligation

in or under, and any property securing it)

were governed by the laws of the United

States or a state of the United States, and

E default rights with respect to the covered

QFC that may be exercised against the

covered entity are permitted to be exercised

to no greater extent than the default rights

could be exercised under the U.S. special

resolution regime if the covered QFC were

governed by the laws of the United States

or a state of the United States.14

The required provisions seek to ensure equiva-

lent treatment, under the U.S. special resolution

regimes, across all jurisdictions for all covered

QFCs.15 Accordingly, the provisions are not

required for a covered QFC if

E the covered QFC “[e]xplicitly provides that

the Covered QFC is governed by the laws

of the United States or a state of the United

States” (and does not carve out application

of the U.S. special resolution regimes), and

E each party to the covered QFC, other than

the covered entity, is (i) an individual domi-

ciled in the United States, (ii) a company

either that is incorporated in or organized

under U.S. law or that has its principal place

of business in the United States or (iii) a

U.S. government branch or U.S. agency.

The Federal Reserve explained the two condi-

tions of the exemption as follows:

It has long been clear that the laws of the United

States and the laws of a state of the United States

both include U.S. federal law, such as the U.S.

Special Resolution Regimes. Therefore, [the

governing law condition] ensures that contracts

that meet this exemption also contain language

that helps ensure that foreign courts will enforce

the stay-and-transfer provisions of the U.S.

Special Resolution Regimes.... [The domicile/

place-of-business condition] helps ensure that the

FDIC will be able to quickly and easily enforce

the stay-and-transfer provisions of the U.S.

Special Resolution Regimes.16

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

4 K 2017 Thomson Reuters

U.S. Bankruptcy Code andRestrictions on Cross-Defaults

The U.S. special resolution regimes do not

include Chapter 11 of the U.S. Bankruptcy Code,

any other chapter of the Bankruptcy Code or any

other U.S. or non-U.S. insolvency regime. For

QFCs, the Bankruptcy Code provides a safe

harbor exemption from the automatic stay that

otherwise generally applies when a debtor files

for relief. Thus, the Bankruptcy Code does not

have the kinds of short-term stay mechanisms ap-

plicable to QFCs that are found in the FDIA and

OLA.

The Rule addresses that difference, in part, by

requiring covered QFCs to limit the exercise of

default rights (and certain restrictions on transfer)

that relate to an affiliate of a direct party to the

QFC becoming subject to a receivership, insol-

vency, liquidation, resolution or similar proceed-

ing (referred to below as an affiliate insolvency).

Of particular relevance are QFCs entered into by

covered entities that are subsidiaries of bank

holding companies (BHCs), particularly where a

BHC guarantees the covered entity’s QFC

obligations.17 QFC agreements for such trading

relationships often include cross-default rights,

permitting a counterparty of a covered entity to

terminate the QFCs where the covered entity’s

BHC parent files for protection under the Bank-

ruptcy Code. Such QFCs permitted counterpar-

ties of Lehman’s subsidiaries to terminate their

transactions when Lehman’s parent filed for

Chapter 11 protection.18

In explaining the Rule’s restrictions on cross-

defaults, the Federal Reserve contrasted OLA and

the Bankruptcy Code as follows:

[OLA]’s stay-and-transfer provisions ... address

both direct default rights and cross-default rights.

But, as explained above, no similar statutory pro-

visions would apply to a resolution under the

U.S. Bankruptcy Code. The final rule attempts to

address these obstacles to orderly resolution by

extending the stay-and-transfer provisions to any

type of resolution of a Covered Entity. Similarly,

the final rule would facilitate a transfer of the

GSIB parent’s interests in its subsidiaries, along

with any credit enhancements it provides for

those subsidiaries, to a solvent financial company

by prohibiting Covered Entities from having

QFCs that would allow the QFC counterparty to

prevent such a transfer or to use it as a ground for

exercising default rights.

Thus, subject to a number of exceptions (dis-

cussed below), a covered QFC

E may not permit the exercise of any default

right with respect to the covered QFC that

is related, directly or indirectly, to an affili-

ate insolvency and

E may not prohibit the transfer of a covered

affiliate credit enhancement (described

below) or certain related rights and obliga-

tions to a transferee upon or following an

affiliate insolvency.19

The Federal Reserve confirmed that a QFC

does not become subject to the Rule’s restrictions

on cross-default because a counterparty has the

right

to terminate the contract on demand or at its op-

tion at a specified time, or from time to time,

without the need to show cause. ... Therefore,

[the cross-default section of the Rule] does not

restrict the ability of QFCs, including overnight

repos, to terminate at the end of the term of the

contract.20

In formulating its restrictions on cross-default

rights, the Rule distinguishes between (i) covered

entities that are “direct parties” to QFCs and thus

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

5K 2017 Thomson Reuters

enter into “covered direct QFCs” and (ii) covered

entities that are credit support providers for their

affiliates’ QFCs (defined as “covered affiliate

support providers”) and thus provide “covered

affiliate credit enhancements.”

The Rule provides certain exceptions to the

mandated contractual restrictions described

above; it refers to the exceptions as “creditor

protections.” The creditor protections allow

covered QFCs to have default provisions that

permit counterparties to terminate a covered QFC

due to the insolvency of the direct party or its fail-

ure to satisfy payment or delivery obligations

pursuant either to the covered QFC or to another

contract between the direct party and the counter-

party; they also allow the exercise of default

rights due to the failure of the covered affiliate

support provider to satisfy a payment or delivery

obligation pursuant to a covered affiliate credit

enhancement.21 Accordingly, in the Adopting

Release, the Federal Reserve emphasized that

“the QFC counterparty would retain its ability

under the U.S. Bankruptcy Code’s safe harbors

to exercise direct default rights.”22

Creditor protections also permit cross-default

terminations after a short “stay period” following

the commencement of affiliate insolvency pro-

ceedings—one business day or 48 hours, which-

ever is longer—if one of four conditions is met.23

If none of those conditions is met, then the re-

striction on the exercise of cross-default rights

will last longer than the short stay period. For

example, if the covered affiliate credit enhance-

ment is not transferred in connection with a

Chapter 11 proceeding, the restriction will con-

tinue beyond the short stay period if the covered

affiliate support provider

E does not become subject to alternative

insolvency proceedings (e.g., Chapter 7

liquidation proceedings) and

E remains obligated to at least a “substantially

similar” extent under (i) the covered affili-

ate credit enhancement and (ii) each other

covered affiliate credit enhancement in re-

spect of other covered direct QFCs with the

supported party and its affiliates—and thus

does not engage in “cherry picking.”24

In that circumstance, a counterparty would

retain its right to terminate covered QFCs for

subsequent payment or delivery defaults (or other

direct defaults, as described above); for example,

termination would be permitted if the direct party

covered entity failed to meet a collateral call. But

the counterparty would not otherwise be able to

terminate the covered QFC even if, for example,

Chapter 11 proceedings were continuing with re-

spect to a covered affiliate support provider that

is a BHC parent guarantor. Moreover, the coun-

terparty would remain obligated to perform its

obligations under the covered QFCs, including

posting additional collateral as and when contrac-

tually required.

If the covered affiliate credit enhancement is

transferred to, for example, a court-approved

transferee, the restriction on the exercise of cross-

default rights will remain in effect if (in addition

to the conditions described above, as they apply

to the transferee) either (i) all of the ownership

interests in the direct party are transferred to the

transferee or (ii) “reasonable assurance” is pro-

vided that all or substantially all of the assets of

the covered affiliate support provider (or net

proceeds therefrom) will be, with limited excep-

tions, transferred or sold to the transferee in a

timely manner.25

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

6 K 2017 Thomson Reuters

As discussed below, the creditor protections

described above are not as protective as those that

are included in analogous provisions of the

International Swaps and Derivatives Association

(ISDA) 2015 Universal Resolution Stay Protocol

(the Universal Protocol). The Universal Protocol

takes greater advantage of the kinds of protec-

tions available to creditors in U.S. bankruptcy

proceedings (e.g., by conditioning continued

restrictions on cross-default rights by reference

to various kinds of court orders).

ISDA Protocols

The Rule provides a safe harbor for certain

ISDA protocols as a means of compliance with

the Rule, despite differences between the kinds

of QFC amendments effected by those protocols

and the Rule’s requirements. This section pro-

vides a brief overview of those protocols; related

differences between the protocols and the re-

quirements of the Rule are discussed in the next

section.

The Rule permits compliance through QFC

amendments that result from adherence to the

Universal Protocol, which ISDA published in

November 2015.26 Like the Rule requirements,

the Universal Protocol addresses two distinct

goals: (i) reinforcing cross-border enforcement

of special resolution regimes and (ii) limiting

cross-defaults in the context of certain U.S.

insolvency proceedings.27 Thus, adherents to the

Universal Protocol achieve contractual ends for

their QFCs that are similar to, though not the

same as, those mandated by the Rule.

The Universal Protocol was developed and

published to enable U.S. and non-U.S. GSIBs to

comply with regulatory requirements in several

FSB jurisdictions, including the United States.

The GSIBs have already adhered to the Univer-

sal Protocol, and thus they will satisfy, with re-

spect to covered QFCs between them, both the

opt-in and the cross-default requirements of the

Rule.

However, the Universal Protocol was not

intended for adherence by buy-side counterpar-

ties of the GSIBs,28 and thus it is not expected to

be a means by which covered entities comply

with the Rule with respect to covered QFCs with

their buy-side counterparties. Accordingly, the

Rule also permits compliance with its require-

ments via adherence to a yet-to-be published

ISDA protocol—defined in the Rule as a U.S.

Protocol. To qualify as a U.S. Protocol for pur-

poses of the Rule, a new protocol must be “the

same as” the Universal Protocol, except in certain

limited respects (described below).29

In May 2016, ISDA published the ISDA Reso-

lution Stay Jurisdictional Modular Protocol (the

JMP) as a complement to the Universal

Protocol.30 The JMP was designed with the ex-

pectation that a separate JMP “module” would be

created for each jurisdiction that required its

banking organizations to amend contracts with

buy-side counterparties. Thus, unlike the Univer-

sal Protocol, which amends QFCs to comply with

the requirements of multiple jurisdictions, the

JMP provides for adherence on a jurisdiction-by-

jurisdiction basis—that is, on a module-by-

module basis. For example, in 2015, ISDA pub-

lished a UK module to the JMP (the JMP UK

Module)31 to permit banking organizations sub-

ject to the UK bank resolution regime to amend

their contracts with buy-side counterparties in

the manner required by UK regulations that were

also published in 2015.32

It is now expected that a U.S. module to the

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

7K 2017 Thomson Reuters

JMP will be published in a form that will qualify

the module as a U.S. Protocol under the Rule. We

refer to the expected module (together with re-

lated terms of the JMP) as the JMP U.S. Module.

Differences Between the Rule’sStated Requirements and theISDA Protocols

As indicated above, neither the Universal

Module nor a U.S. Protocol will result in QFC

amendments that are strictly in accordance with

the Rule’s requirements for (i) opt-in provisions

related to the U.S. special resolution regimes or

(ii) limits on cross-default (and transfer) rights

with respect to other insolvency regimes, includ-

ing Chapter 11 of the Bankruptcy Code. We refer

to those Rule requirements, collectively, as the

stated requirements.

Accordingly, there will be relative advantages

and disadvantages, from the perspective of coun-

terparties to covered entities, to amending cov-

ered QFCs via protocol adherence rather than

amending covered QFCs in accordance with the

stated requirements. That is particularly true for

buy-side counterparties.

In this section, we first discuss the limited dif-

ferences that the Rule permits between a U.S.

Protocol and the Universal Protocol. We then

discuss the key disadvantage and the key advan-

tage, from a buy-side perspective, of amending

QFCs through a U.S. Protocol (such as the ex-

pected JMP U.S. Module) rather than amending

QFCs in accordance with the stated requirements.

Differences Between a U.S.Protocol and the UniversalProtocol

A U.S. Protocol may vary from the Universal

Protocol in only very limited respects. The two

principal permitted variations may be described

as follows:33

E The Universal Protocol restricts rights in a

two-way manner between all adherents

(that is, between all U.S. and non-U.S.

GSIBs). However, the U.S. Protocol may

restrict rights in a one-way manner: As be-

tween a covered entity and a buy-side coun-

terparty that adhere to a U.S. Protocol, the

U.S. Protocol may limit the rights of the

counterparty under the amended covered

QFC (related to the resolution or insolvency

of the covered entity) without limiting the

rights of the covered entity (in connection

with any insolvency of the buy-side

counterparty). As a corollary, the U.S.

Protocol will not amend agreements be-

tween two adherents (in either direction) if

neither adherent is a covered entity (or an

excluded bank).

E The opt-in provisions of the Universal

Protocol apply with respect to a broad range

of national resolution regimes: (i) six “Iden-

tified Regimes” specified in the Universal

Protocol; and (ii) “Protocol-Eligible Re-

gimes,” which the Universal Protocol does

not specify but may subsequently qualify

as such under the Universal Protocol (in-

cluding via publication of new “Country

Annexes”). However, the U.S. Protocol

may limit its application to the six Identi-

fied Regimes.

Thus, despite market expectations that buy-

side counterparties of GSIBs would not adhere to

the Universal Protocol, the Federal Reserve ap-

pears to expect that buy-side participants will ad-

here to a JMP U.S. Module that includes terms

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

8 K 2017 Thomson Reuters

that are, from a U.S. perspective, largely identi-

cal to those in Universal Protocol.

Differences Between a U.S.Protocol and the StatedRequirements

The principal disadvantage to a counterparty

that adheres to a U.S. Protocol (such as the

expected JMP U.S. Protocol), rather than amend-

ing QFCs in accordance with the stated require-

ments, is that adherence is not permitted on a

“dealer-by-dealer” or “static” basis, but is “uni-

versal” and “dynamic.” As discussed below, once

a buy-side market participant adheres to a U.S.

Protocol, it amends its covered QFCs with all

adhering covered entities, including entities that

adhere to the U.S. Protocol as covered entities in

the future.34

The principal advantage to a counterparty that

adheres to a U.S. Protocol (such as the expected

JMP U.S. Protocol), rather than amending QFCs

in accordance with the stated requirements, is

that the amendments that result from adherence,

like those that result from the Universal Protocol,

will provide greater creditor protections to a

counterparty than those permitted by the stated

requirements.

Adherence. The JMP is formulated to permit

dealer-by-dealer adherence through jurisdiction-

specific modules. For example, the JMP UK

Module took advantage of that JMP feature and

permitted buy-side market participants to choose

those JMP UK banking organizations with which

they would amend QFCs through adherence.

However, any JMP U.S. Module that qualifies as

a U.S. Protocol will not permit that flexibility,

but will require adherence on an all-or-none—or

universal—basis.

Moreover, the Rule does not permit “static”

adherence via a U.S. Protocol. In other words,

once a buy-side market participant adheres to a

U.S. Protocol, it adheres in respect of all counter-

parties that are covered entities that adhere to the

U.S. Protocol, whether they are covered entities

on the date of adherence or become covered enti-

ties in the future. In effect, adherence will be

dynamic. Thus, even though the U.S. Protocol

would not initially apply to QFCs between a buy-

side adherent and a banking organization that is a

non-covered entity, if that non-covered entity

were to become a covered entity—for example,

because it was acquired by a U.S. GSIB or be-

cause the Federal Reserve designated it as such—

and were to adhere to the U.S. Protocol, the buy-

side adherent’s existing QFCs with the new

covered entity would be amended automatically

by the U.S. Protocol.35

The Federal Reserve’s approach with respect

to universal adherence was deliberate; indeed, it

was central to the Federal Reserve’s consider-

ation of the ISDA protocols. In the Federal Re-

serve’s proposal of the Rule,36 and in the Adopt-

ing Release, the Federal Reserve emphasized that

it was permitting compliance through use of the

Universal Protocol and a U.S. Protocol—despite

their inconsistencies with the stated requirements

of the Rule—because such compliance would

ensure universal application:

[W]hile the scope of the stay-and-transfer provi-

sions of the Universal Protocol are narrower than

the stay-and-transfer provisions that would have

been required under the proposal and the Univer-

sal Protocol provides a number of creditor protec-

tion provisions that would not otherwise have

been available under the proposal, the Universal

Protocol includes a number of desirable features

that the proposal lacked. The proposal explained

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

9K 2017 Thomson Reuters

that “when an entity (whether or not it is a Cov-

ered Entity) adheres to the [Universal] Protocol,

it necessarily adheres to the [Universal] Protocol

with respect to all Covered Entities that have also

adhered to the Protocol rather than one or a

subset of Covered Entities (as the proposal may

otherwise permit). ... This feature appears to al-

low the [Universal] Protocol to address impedi-

ments to resolution on an industry-wide basis and

increase market certainty, transparency, and eq-

uitable treatment with respect to default rights of

non-defaulting parties.37

Creditor Protections. Like the Universal Proto-

col, a U.S. Protocol will provide greater creditor

protections related to cross-defaults than the

creditor protections permitted by the stated

requirements. Annex A to this article provides a

summary comparison of certain key differences

between creditor protections under a U.S. Proto-

col and those permitted by the stated

requirements. As the comparison table indicates:

E A U.S. Protocol will limit cross-default

rights principally in connection with affili-

ate insolvencies under Chapter 11 of the

Bankruptcy Code and the FDIA.38 In con-

trast, the stated requirements limit cross-

defaults in respect of a broad category of

generically defined types of affiliate

insolvencies.

E A U.S. Protocol will condition any contin-

ued suspension of cross-default rights (be-

yond a one-business day/48-hour stay pe-

riod) on bankruptcy court involvement for

the benefit of creditors. Under the stated

requirements, in contrast, the related credi-

tor protections are neither as specific nor as

robust as those that will be provided for in

a U.S. Protocol.

E A U.S. Protocol’s creditor protections will

be available whether or not the affiliate sup-

port provider is itself a covered entity. In

contrast, creditor protections under the

stated requirements are limited to “covered

affiliate support providers” (that is, affili-

ates that are themselves covered entities).

Thus, for example, if the covered entity is a

U.S. subsidiary of a non-U.S. GSIB, and the

parent of the non-U.S. GSIB (which is not

a covered entity) provides a guarantee sup-

porting the U.S. subsidiary’s QFCs, certain

creditor protections will not be available.39

Other Issues

Practical Considerations Relatedto QFC Amendments

Adherence to a U.S. Protocol may be adminis-

tratively simpler than entering into bilateral

amendment agreements with each covered entity.

For buy-side market participants, that will be

particularly true for those that have trading

relationships with multiple covered entities. All

covered entities, given the likely breadth of their

trading relationships with buy-side counterpar-

ties, are likely to prefer to amend covered QFCs

through adherence to a U.S. Protocol.

Compliance Phase-in Period

As noted above, compliance with the Rule will

be phased in during 2019. A covered entity’s

compliance date for a given covered QFC will be

determined by the regulatory status of the coun-

terparty to the covered QFC, as follows:

Counterparty Compliance Date

Other covered entity or excluded bank January 1, 2019

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

10 K 2017 Thomson Reuters

Counterparty Compliance Date

Financial counterparty40 July 1, 2019

Other counterparties January 1, 2020

However, as noted above (see “QFC Transac-

tions Covered by the Rule”), an in-scope QFC

becomes a covered QFC (and is not grandfa-

thered) if it is executed after January 1, 2019

(notwithstanding a later compliance phase-in

date for the relevant counterparty). Moreover, in-

scope QFCs executed by a covered entity and a

counterparty before January 1, 2019, will become

covered QFCs if they trade any QFC (whether or

not in scope) after January 1, 2019 (even if the

counterparty has a compliance phase-in date that

is later than the trade date). And, as discussed

above, there are knock-on consequences for the

affiliates of a covered entity and a counterparty if

they trade a QFC after January 1, 2019.

Thus, for example: If a covered entity and a

financial counterparty execute a QFC on Febru-

ary 1, 2019, neither that QFC nor any existing

QFC between the two parties must comply with

the Rule on that date, because it is before July 1,

2019 (the phase-in compliance date for financial

counterparties). But if that QFC is an in-scope

QFC, it will be a covered QFC when it is exe-

cuted (regardless of the compliance phase-in

date). Moreover, whether or not it is an in-scope

QFC, the execution of that QFC on February 1

will result in all in-scope QFCs between the

covered entity and the financial counterparty

becoming covered QFCs automatically (and, as

noted above, there are knock-on affects for

affiliates). Thus, when July 1, 2019, arrives, each

of those covered QFCs will be required to comply

with the Rule (e.g., by being amended pursuant

to a U.S. Protocol).

Accordingly, a covered entity will have an

incentive, before trading any QFC (whether or

not in-scope) with any counterparty after January

1, 2019, to know how the covered entity (and its

excluded bank affiliates) will comply with the

Rule when the compliance phase-in date arrives

for the respective counterparty (and its consoli-

dated affiliates). As a consequence, covered enti-

ties may seek to have revised trading documenta-

tion (whether via a U.S. Protocol or otherwise) in

place with each of its QFC counterparties by the

beginning of 2019 even if that documentation

does not take effect until the respective phase-in

date.

“Affiliates”

As noted above (see “QFC Transactions Cov-

ered by the Rule”), an existing in-scope QFC be-

tween a covered entity and a buy-side counter-

party becomes a covered QFC only if a new QFC

is traded between the covered entity or certain of

its affiliates, on the one hand, and the buy-side

counterparty or certain of its affiliates, on the

other. For each side of that trading relationship,

affiliate status is determined differently. On the

covered entity side, “affiliate” is defined by refer-

ence to the “control” definition in the Bank Hold-

ing Company Act of 1956 (the BHCA).41 On the

counterparty side, only “consolidated affiliates,”

as defined in the Rule, must be considered.42 The

BHCA definition of “control” may result in there

being affiliates of a covered entity beyond those

entities that are consolidated with the covered

entity under generally accepted accounting prin-

ciples (GAAP). In contrast, the Rule’s definition

of “consolidated affiliate” is limited to those enti-

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

11K 2017 Thomson Reuters

ties that are consolidated with one another on

financial statements prepared in accordance with

GAAP (or that would have been so consolidated

if GAAP had applied).

Compliance Alternatives

The Rule includes a provision stating,

A covered entity may request that the Board ap-

prove as compliant with the [stated requirements]

proposed provisions of one or more forms of

covered QFCs, or proposed amendments to one

or more forms of covered QFCs, with enhanced

creditor protection conditions.43

However, the provision itself suggests poten-

tial limitations on the practical availability of

“enhanced creditor protection conditions.” The

provision includes detailed “considerations” by

which any request is likely to be evaluated.44 The

considerations include whether the request would

permit adherence “with respect to only one or a

subset of covered entities”—that is, whether

dealer-by-dealer adherence is permitted—and

whether adherence would apply to “existing and

future transactions.”45 Only covered entities are

permitted to submit requests to the Federal Re-

serve under the provision, even though comment-

ers had requested “that counterparties and trade

groups, in addition to covered entities, should be

permitted to make such requests.”46 Moreover,

the provision would require a covered entity to

provide “a written legal opinion verifying that

proposed provisions or amendments would be

valid and enforceable under applicable law of the

relevant jurisdictions, including, in the case of

proposed amendments, the validity and enforce-

ability of the proposal to amend the covered

QFC.”47 Thus there may be meaningful hurdles

to overcome with respect to taking advantage of

any approach to amending covered QFCs that is

not achieved through adherence to the Universal

Protocol or a U.S. Protocol or compliance with

the stated requirements.

Covered Entities Acting asAgents

The Rule states that

(1) A covered entity does not become a party to a

QFC solely by acting as agent with respect to the

QFC; and (2) The exercise of a default right with

respect to a covered QFC includes the automatic

or deemed exercise of the default right pursuant

to the terms of the QFC or other arrangement.48

However, the Federal Reserve cautioned that

where covered entities, acting as agent, also take

on obligations as principal, a different outcome

will be warranted. It stated in the Adopting

Release,

[T]he final rule does not exempt a QFC with re-

spect to which an agent also acts in another capa-

city, such as guarantor. Continuing the example

regarding the covered entity acting as agent with

respect to a master securities lending agreement,

if the covered entity also provided a [securities

lending authorization agreement] that included

the typical indemnification provision discussed

above, the agency exemption of the final rule

would not exclude [that agreement] but would

still exclude the master securities lending

agreement.49

Burden of Proof

The Rule’s cross-default provisions include a

requirement related to the burden of proof and

the standard of proof associated with any exercise

of default rights. It states,

A covered QFC must require, after an affiliate of

the direct party has become subject to a receiver-

ship, insolvency, liquidation, resolution, or simi-

lar proceeding: (1) The party seeking to exercise

a default right to bear the burden of proof that the

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

12 K 2017 Thomson Reuters

exercise is permitted under the covered QFC; and

(2) Clear and convincing evidence or a similar or

higher burden of proof to exercise a default

right.50

The Federal Reserve explained,

The purpose of [burden/standard of proof] re-

quirement is to deter the QFC counterparty of a

covered entity from thwarting the purpose of the

final rule by exercising a default right because of

an affiliate’s entry into resolution under the guise

of other default rights that are unrelated to the af-

filiate’s entry into resolution.... The requirement

[makes] clear that a party that exercises a default

right when an affiliate of its direct party enters

receivership of [sic] insolvency proceedings is

unlikely to prevail in court unless there is clear

and convincing evidence that the exercise of the

default right against a covered entity is not re-

lated to the insolvency or resolution proceeding.51

Similar features are found in the Universal Pro-

tocol52 and thus would be elements of any U.S.

Protocol qualifying for safe harbor treatment

under the Rule.

Observations

The Federal Reserve is not mandating, by rule,

that large U.S. GSIBs trade with buy-side coun-

terparties only if those counterparties agree to

amendments that are consistent with the Univer-

sal Protocol, including universal adherence.

However, the Federal Reserve has ensured that in

the absence of such an agreement, the alternative

for U.S. GSIBs and their counterparties—that is,

compliance with the Rule’s stated require-

ments—will be less attractive from a counter-

party creditor protection perspective. The only

alternative to compliance with the stated require-

ments or through adherence to a U.S. Protocol

requires a covered entity to petition the Federal

Reserve itself, in accordance with the Rule pro-

visions governing “enhanced creditor protection

conditions.” As suggested above, it may be dif-

ficult to take advantage of that alternative.

For investment advisers and asset managers

representing buy-side clients, there will now be

the challenge of communicating the terms and

consequences of the Rule and, perhaps, a U.S.

Protocol, to their clients, investors and accounts.

Investment advisers and asset managers will face

additional challenges because (as discussed

above) triggers for compliance with the Rule are

applied between a covered entity and each coun-

terparty (and the counterparty’s consolidated af-

filiates) without regard to whether the counter-

party (or an affiliate) trades through multiple

advisers and/or managers. Thus, for example, if

an investment adviser trades a QFC with a given

covered entity, the consequences may be

manifold. Of course, one consequence will be

that all covered QFCs the adviser trades (or has

traded) on behalf of the respective client with that

covered entity will become subject to the Rule.

In addition, however, compliance will be required

for covered QFCs that the client has executed

with the covered entity away from the adviser

(e.g., either directly or through another invest-

ment adviser). Moreover, as discussed above, the

adviser’s trade on behalf of the client may trigger

requirements for the QFCs of the client’s

affiliates.

On the sell side, covered entities will need to

monitor for themselves, and disclose to buy-side

counterparties as necessary, the covered entities’

“affiliates” as determined by reference to the

broad BHCA concept of “control.” More gener-

ally, there will be the challenge of educating

counterparties and encouraging them to act be-

fore regulatory deadlines take effect. In some cir-

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

13K 2017 Thomson Reuters

cumstances, the challenges may arise as counter-

parties request alternative (e.g., nonprotocol)

approaches—that is, ad hoc documentation

amendments that meet regulatory requirements

but do not do so solely via a U.S. Protocol such

as the expected JMP U.S. Module and that may,

therefore, attract regulatory attention.

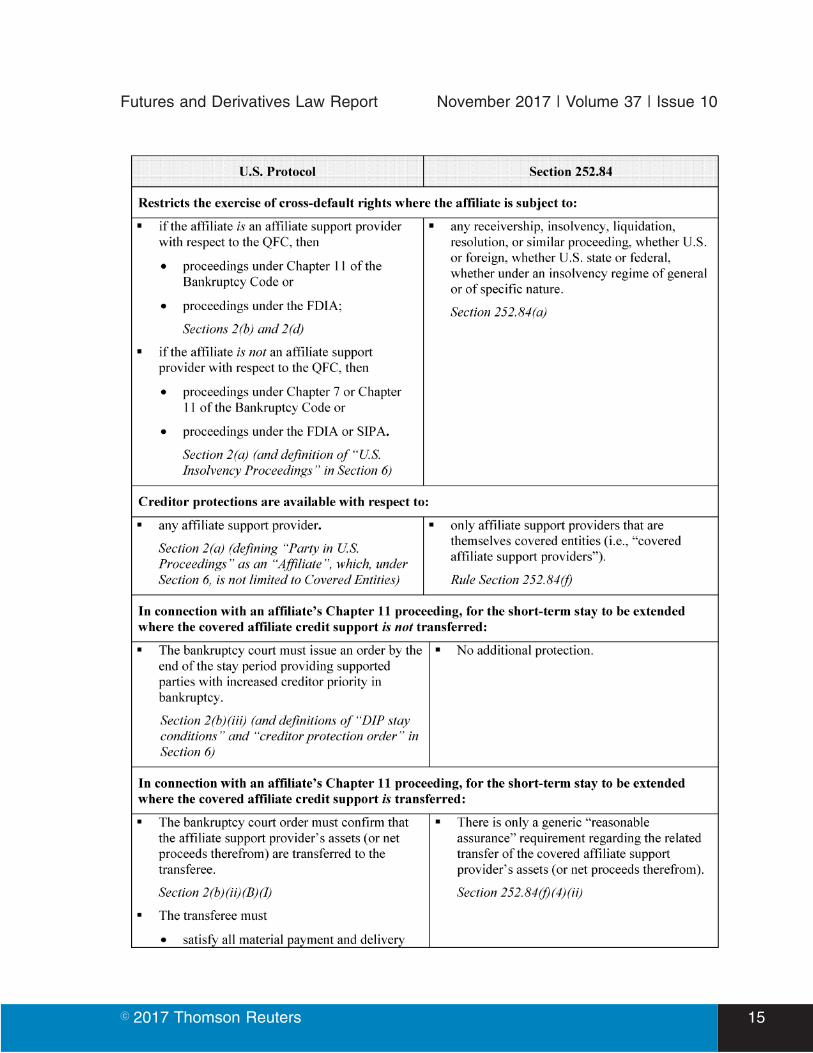

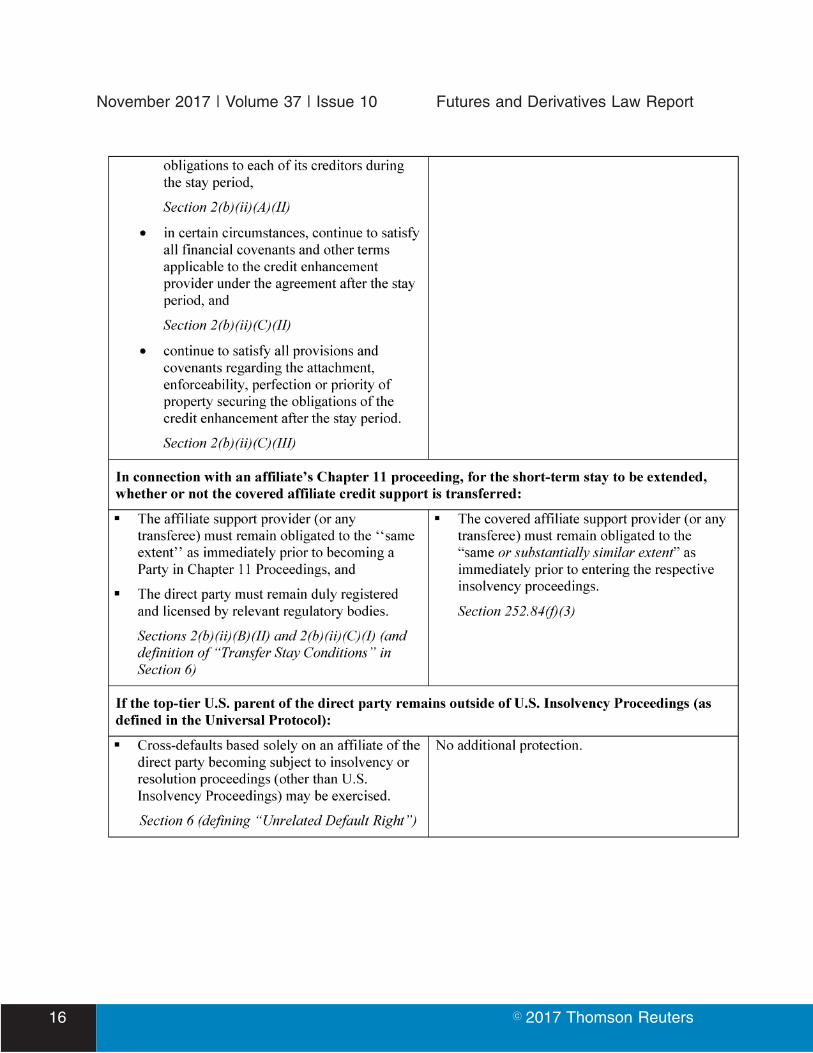

Annex A

Comparison of Certain KeyDifferences Between theCreditor Protections Under aU.S. Protocol and the Rule’sStated Requirements

The table below compares the Universal Proto-

col and the Rule’s stated requirements with re-

spect to their treatment of cross-default

restrictions. More specifically, it compares (i)

certain creditor protections under (and related

aspects of) Section 2 of the Attachment to Uni-

versal Protocol, which would be incorporated in

substance in any U.S. Protocol and (ii) certain

creditor protections under (and related aspects

of) Section 252.84 of the Rule.

As discussed in this article, a U.S. Protocol and

the stated requirements will restrict the cross-

default rights of a counterparty under a covered

QFC with a covered entity—that is, those rights

that are triggered by an affiliate of the covered

entity’s becoming subject to certain insolvency

proceedings. The creditor protections permit

certain exceptions to the otherwise mandated

restrictions.

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

14 K 2017 Thomson Reuters

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

15K 2017 Thomson Reuters

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

16 K 2017 Thomson Reuters

ENDNOTES:

1See Federal Reserve, Restrictions on Quali-fied Financial Contracts of Systemically Impor-tant U.S. Banking Organizations and the U.S.Operations of Systemically Important ForeignBanking Organizations; Revisions to the Defini-tion of Qualifying Master Netting Agreement andRelated Definitions, 82 Fed. Reg. 42882 (Septem-ber 12, 2017) (the Adopting Release), availableat https://www.gpo.gov/fdsys/pkg/FR-2017-09-12/pdf/2017-19053.pdf.

2In this article, “U.S. GSIB” means any U.S.bank holding company (BHC) that is identifiedas a global systemically important BHC pursuantto Federal Reserve rules. See Rule Section252.82(b)(1). There are currently eight U.S.GSIBs: Bank of America Corporation, The Bankof New York Mellon Corporation, Citigroup Inc.,Goldman Sachs Group, Inc., JPMorgan Chase &Co., Morgan Stanley Inc., State Street Corpora-tion and Wells Fargo & Company. See AdoptingRelease at 42892.

3See Adopting Release at 42882. On Septem-ber 27, 2017, the FDIC adopted its rule, which(as expected) is substantively identical to theRule. See FDIC, Restrictions on Qualified Finan-cial Contracts of Certain FDIC-Supervised Insti-tutions; Revisions to the Definition of QualifyingMaster Netting Agreement and Related Defini-tions (Sept. 27, 2017), available at https://www.fdic.gov/news/news/press/2017/pr17072.html.The OCC is expected to adopt its rule shortly.

4The Rule also excludes from its application(i) companies owned in satisfaction of a debtpreviously contacted, (ii) merchant banking andcertain other portfolio companies and (iii) certaincompanies engaged in the business of makingpublic welfare investments. See Rule Section252.82(b)(2).

5In this article, “non-U.S. GSIB” means aglobal systemically important foreign bankingorganization meeting the criteria set forth in theRule. See Rule Section 252.87.

6See Adopting Release at 42894 (citing 12U.S.C. 5390(c)(8)(D)).

7In addition, the Rule excludes (i) covered

QFCs to which a central counterparty clearing-house (CCP) is a party or to which each party(other than the covered entity) is a financial mar-ket utility (FMU) and (ii) certain “types of con-tracts or agreements.” See Rule Sections252.88(a) (referring to CCPs and FMUs) and252.88(c) (referring to certain investment advi-sory contracts and warrants).

8See Rule Section 252.81 (paragraph (1)(ii)of the definition of “default right,” which ex-cludes “a right or operation of a contractual pro-vision arising solely from a change in the valueof collateral or margin or a change in the amountof an economic exposure”).

9See Adopting Release at 42900 (describingpermissible changes in margin due to changes inmarket price, not for “changes due to counter-party credit risk (e.g., credit rating down-grades)”).

10See Adopting Release at 42894 (“[C]om-menters urged the Board to exclude QFCs that donot contain any transfer restrictions or defaultrights ... Commenters named several examples ofcontracts that fall into this category, includingcash market securities transactions, certain spotFX transactions...”).

11The Rule uses the phrase “Enters, executes,or otherwise becomes a party to...” See Rule Sec-tion 252.82(c).

12Rule Section 252.82(c)(1) reads:[A] covered QFC is, ... [w]ith respect to a covered

entity that is a covered entity on November 13,

2017, an in-scope QFC that the covered entity:

(i) Enters, executes, or otherwise becomes a

party to on or after January 1, 2019; or

(ii) Entered, executed, or otherwise became a

party to before January 1, 2019, if the covered

entity or any affiliate that is a covered entity or

excluded bank also enters, executes, or other-

wise becomes a party to a QFC with the same

person or a consolidated affiliate of the same

person on or after January 1, 2019 ...

13The term “cross-default” often connotesdefault rights triggered by defaults under differ-ent agreements between the same two parties,and not only those rights triggered by actions or

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

17K 2017 Thomson Reuters

circumstances of an affiliate of a contractualcounterparty. However, the Adopting Releaseuses the term “cross-default” to refer to defaultrights triggered by the insolvency of an affiliateof a covered entity. Accordingly, we adopt a sim-ilar usage in this article.

14This provision must also apply in circum-stances in which an affiliate of the covered entitybecomes subject to a proceeding under a U.S.special resolution regime.

15The Rule “requires the QFCs of CoveredEntities to contain contractual provisions that optinto the stay-and-transfer treatment of the [U.S.special resolution regimes] to reduce the risk thatthe stay-and-transfer treatment would be chal-lenged by a QFC counterparty or a court in aforeign jurisdiction.” Adopting Release at 42889.

16 Adopting Release at 42901.17The Federal Reserve emphasized that the

cross-default limitations were important in thecontext of a resolution or insolvency proceedingthat is part of a “single point of entry” strategy asapplied to a BHC. See Adopting Release at42885.

18See Adopting Release at 42883.19The Rule includes a carve out from the

transfer limitation where “the transfer wouldresult in the supported party being the beneficiaryof the credit enhancement in violation of any lawapplicable to the supported party.” Rule Section252.84(b)(2).

20 Adopting Release at 42895 note 110; seealso Rule Section 252.81 (paragraph (2) of thedefinition of “default right”).

21See Rule 252.84(d) (“General CreditorProtections” permitting “the exercise of a defaultright that arises as a result of” (1) the direct partybecoming subject to an insolvency proceeding;(2) the direct party not satisfying a payment ordelivery obligation pursuant to the covered QFCor another contract between the same parties thatgives rise to a default right in the covered QFC;or (3) the covered affiliate support provider ortransferee not satisfying a payment or deliveryobligation pursuant to a covered affiliate creditenhancement that supports the covered direct

QFC).22Adopting Release at 42905.23Termination is permitted after the stay pe-

riod if

E the covered affiliate support provider thatremains obligated under the covered affili-ate credit enhancement becomes subject toa receivership, insolvency, liquidation, res-olution or similar proceeding, other than aChapter 11 proceeding,

E the transferee, if any, becomes subject to areceivership, insolvency, liquidation, reso-lution or similar proceeding (subject tocertain exceptions related to resolutionunder the FDIA),

E the covered affiliate support provider doesnot remain, and a transferee does not be-come, obligated to the same, or substan-tially similar, extent as the covered affiliatesupport provider was obligated immedi-ately prior to entering the insolvency pro-ceeding with respect to (i) the covered af-filiate credit enhancement; (ii) all othercovered affiliate credit enhancements pro-vided by the covered affiliate support pro-vider in support of other covered directQFCs between the direct party and the sup-ported party under such covered affiliatecredit enhancement; and (iii) all covered af-filiate credit enhancements provided by thecovered affiliate support provider in sup-port of covered direct QFCs between thedirect party and affiliates of such supportedparty, or

E in the case of a transfer of the covered affil-iate credit enhancement to a transferee, (i)all of the ownership interests of the directparty directly or indirectly held by thecovered affiliate support provider are nottransferred to the transferee, or (ii) reason-able assurance has not been provided thatall or substantially all of the assets of thecovered affiliate support provider (or netproceeds therefrom) will be, with limitedexceptions, transferred or sold to the trans-feree in a timely manner.

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

18 K 2017 Thomson Reuters

See Rule Section 252.84(f).

24The Federal Reserve explained that the“substantially similar” requirement was intended“to prevent the support provider or the transfereefrom ‘cherry picking’ by assuming only thoseQFCs of a given counterparty that are favorableto the support provider or transferee. [OLA andthe FDIA] contain similar provisions to preventcherry picking.” Adopting Release at 42905.

25See Rule Section 252.84(f)(4).

26The Universal Protocol is available at http://assets.isda.org/media/ac6b533f-3/5a7c32f8.pdf/.

27A law firm alert previously written by theauthors described the Universal Protocol and itsbackground. See Sidley Update, New ISDA Reso-lution Stay Protocols: Challenges for Buy-sideand Sell-side Firms Alike (Nov. 19, 2015), avail-able at http://www.sidley.com/news/11-19-2015-derivatives-update.

28When the Universal Protocol was pub-lished, ISDA stated: “While ISDA 2015 Univer-sal Protocol is open to any entity to voluntarilyadhere, it was not developed with the expectationof being used by broader market participants,including buy-side institutions, as a means ofcomplying with regulations applicable to theirdealer counterparties.” ISDA 2015 UniversalResolution Stay Protocol FAQs, available at http://www2.isda.org/functional-areas/protocol-management/faq/22. In the general FAQs publishedwith the JMP, ISDA continued in a similar vein:“It is expected that market participants will uti-lize ISDA Jurisdictional Modular Protocol, ratherthan ISDA 2014 Protocol or the [2015] Protocol,to comply with Stay Regulations.” However, thegeneral FAQs later state: “Section 1 and Section2 of the [2015] Protocol will not form a part ofISDA Jurisdictional Modular Protocol unlessthose amendments are specifically required forcompliance with Stay Regulations.” ISDA Reso-lution Stay Jurisdictional Modular Protocol FAQ,available at http://assets.isda.org/media/f253b540-125/93347b32-pdf/.

29See Rule Section 252.85(a)(3)(ii).

30The JMP is available at http://assets.isda.or

g/media/f253b540-95/83d17e3d-pdf/.31ISDA published the “UK (PRA Rule) Juris-

dictional Module” at the same time as the JMP.The JMP UK Module and related “ModuleFAQs” are available on ISDA’s website: http://www2.isda.org/functional-areas/protocol-management/protocol/25.

32The JMP UK Module relates to final rulespublished by the UK Prudential Regulation Au-thority (PRA). See UK PRA Rulebook: CRRFirms and Non-Authorised Persons: Stay in Res-olution Instrument 2015 (PRA 2015/82), avail-able at http://www.bankofengland.co.uk/pra/Documents/publications/ps/2015/ps2515app1.pdf. Alaw firm alert previously written by the authorsdescribes and compares the Universal Protocoland the JMP and describes the JMP UK Module.See Sidley Update, New ISDA Resolution StayProtocol and UK Module; Federal Reserve RuleProposal (May 13, 2016), available at https://www.sidley.com/en/insights/newsupdates/2016/05/isda-resolution-stay-jurisdictional-modular.

33In addition, notwithstanding the terms ofthe Universal Protocol, a U.S. Protocol

E must apply to the client-facing leg of acleared transaction for which the clearingmember of the central counterparty acts asprincipal, and the clearing mechanism thusinvolves two back-to-back principal-to-principal transactions (as contrasted withcleared transactions for which clearingmembers act as agent, as in the case ofcleared futures and derivatives in the UnitedStates),

E may permit certain “opt outs” in respect ofcovered QFCs only to the extent thosecovered QFCs would, by other means, con-tinue to meet the requirements of the Rule,

E must not include the sunset provision thatwould have applied under the UniversalProtocol if U.S. regulations like the Rulehad not come into effect by January 1,2018, and

E may include “minor and technical differ-ences from the Universal Protocol and dif-

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10

19K 2017 Thomson Reuters

ferences necessary to conform the U.S.protocol to the differences” permitted underthe Rule.

See Rule Section 252.85(a)(3)(ii).34In addition, the stated requirements with re-

spect to “opt in” (as contrasted to cross-defaults)are limited to OLA and the FDIA, whereas adher-ence to a U.S. Protocol (as noted above) wouldeffect an opt-in with respect to each of the sixIdentified Regimes. However, it is not clear howsignificant a consequence that would be because(i) Identified Regimes other that OLA and theFDIA may have limited application with respectto many covered entities (e.g., U.S.-domiciledentities within U.S. GSIB groups), and (ii) wherethey do apply (e.g., where the covered entity isnon-U.S. subsidiary of a U.S. GSIB or is a U.S.subsidiary of non-U.S. GSIB), a non-U.S. Identi-fied Regime may be enforceable against thecounterparty whether or not the counterparty hasopted in through adherence to a U.S. Protocol.

35The Adopting Release states:[T]he final rule does not permit adherence to a

‘‘static list’’ of all current Covered Entities, which

other commenters requested. ... The final rule,

however, does not prohibit the creation of a dy-

namic list identifying of all current ‘‘Covered Par-

ties,’’ as would be defined in the U.S. Protocol, to

facilitate due diligence and provide additional

clarity to the market. See final rule

§ 252.85(a)(2)(ii)(E) (allowing minor and techni-

cal differences from the Universal Protocol).

Adopting Release at 42910 (including footnote

224).

36See Federal Reserve, Notice of ProposedRulemaking, Restrictions on Qualified FinancialContracts of Systemically Important U.S. Bank-ing Organizations and the U.S. Operations ofSystemically Important Foreign Banking Organi-zations; Revisions to the Definition of QualifyingMaster Netting Agreement and Related Defini-tions, 81 Fed. Reg. 29169 (May 11, 2016) (NPR),available at https://www.gpo.gov/fdsys/pkg/FR-2016-05-11/pdf/2016-11209.pdf.

37Adopting Release at 42908-09 (quotingNPR at 29182-83).

38If the affiliate is not a credit enhancement

provider (as defined in the Universal Protocol),the restrictions also apply (and are not subject tocreditor protection exceptions) under Chapter 7of the Bankruptcy Code and proceedings underthe Securities Investor Protection Act (SIPA).

39See Adopting Release at 42906 (discussingthe unavailability of creditor protections with re-spect to “non-U.S. affiliate credit supporter pro-viders”).

40The definition of “financial counterparty”in the Rule is similar to the definition of “financialend user” in the Federal Reserve’s margin rulesfor noncleared swaps. The Rule definition in-cludes (i) bank holding companies or an affiliatethereof; (ii) savings and loan holding companies;(iii) certain U.S. intermediate holding companies;(iv) nonbank financial companies supervised bythe Federal Reserve; (v) certain depository insti-tutions; (vi) certain banking organizations thatare organized under the laws of a foreign country;(vii) certain institutions that function solely in atrust or fiduciary capacity; (viii) certain credit orlending entities; (ix) certain swap dealers and ma-jor swap participants; (x) certain securities hold-ing companies; (xi) certain securities brokers ordealers; (xii) certain investment advisers; (xiii)certain investment companies and entities thatwould be investment companies but for certainexemptions; (xiv) certain private funds; (xv)certain commodity pools, commodity pool opera-tors and commodity trading advisors; (xvi) cer-tain futures commission merchants and othercommodities market professionals; (xvii) certainemployee benefit plans; and (xviii) certain insur-ance companies. See Rule Section 252.81.The definition expressly excludes sovereign enti-ties, multilateral development banks and theBank for International Settlements.

41See Adopting Release at 42892 (“ ‘Subsid-iary’ in the final rule continues to be defined byreference to BHC Act control, as does the defini-tion of ‘affiliate,’ ’’ citing 12 CFR 252.2). Com-menters had raised concerns about whether allaffiliates of a covered entity would be subject tooperational control, given that the BHCA defini-tion of control may result in affiliates that areminority owned. See Adopting Release at 42891.

42See Rule Section 252.81.

Futures and Derivatives Law ReportNovember 2017 | Volume 37 | Issue 10

20 K 2017 Thomson Reuters

43See Rule Section 252.85(b)(1).

44See Rule Section 252.85(d).

45Rule Section 252.85(d), paragraphs (6) and(4).

46Adopting Release at 42911.

47See Rule Section 252.85(b)(3)(ii).

48 Rule Section 252.82(e).

49 Adopting Release at 42908.

50 Rule Section 252.84(i).

51 Adopting Release at 42907.

52See Universal Protocol Attachment Section

2(i) (“Burden of Proof”) and Section 6 (defini-

tion of “Unrelated Default Right” incorporating a

“clear and convincing evidence” standard).

Futures and Derivatives Law Report November 2017 | Volume 37 | Issue 10