82

FIN. 3403--Corporate Finance INTRODUCTION © R. DIGGLE, CFA University of Central Florida 1999

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | harriet-stone |

| View: | 216 times |

| Download: | 0 times |

FIN. 3403--Corporate Finance INTRODUCTION

© R. DIGGLE, CFA

University of Central Florida

1999

COURSE OBJECTIVES: FIN 3403• To learn to apply the 10 Axioms of Finance in

Ch. 1 of your text.• To learn to APPLY time value of money and

the financial calculator in every day problems.• To understand the basics of Capital Budgeting,

Cost of Capital and Leverage.• To develop an understanding of applied

financial performance and ratio analysis.

FIN 3403 COURSE OBJECTIVES: CONTINUED

• To understand the concepts of risk and return.

• To gain a basic understanding of key financial instruments, markets and institutions.

TOPICS

• WEEK 1-5– TVM – USING FINANCIAL CALCULATOR– USING TABLES IN BACK OF TEXT

• WEEK 6-10– COST OF CAPITAL– LEVERAGE– CAPITAL BUDGETING

TOPICS CONTD.

• WEEK 11-15– FINANCIAL MARKETS, INSTRUMENTS

AND RISK/RETURN– FINANCIAL PERFORMANCE (Financial

ratio analysis --team project)– BOND AND STOCK VALUATION THEORY

FIN 3403: SYLLABUS REVIEW

• OFFICE / HOURS• GRADING

– Drop lowest exam

– Team project

– Homework

– Importance of taking notes in class

• LECTURE NOTES• FINANCIAL CALC.

• Do you need to brush up on accounting?

• My job is to SIMPLIFY concepts in text and problems.

• Ask questions if you are unclear on ANY concept, problem or definition.

WARNING

• This is a quantitative course.

• Homework and class lectures are designed to help you understand the material. You are encouraged to work in a study group to master this material.

• Grades in this course tend to be a bi-modal distribution.

GETTING ORGANIZED

• CLASS ROSTER

• ATTENDANCE POLICY

• TEAM GRADE ON PROJECT

• EXAMS AND MAKE UP POLICY• WALL STREET JOURNAL SIGN UP --

optional but HIGHLY recommended --you may share

• QUESTIONS?

STUDY TIPS TO HELP YOU GET AN “A” IN THIS COURSE• Get into a study group with your team or other

classmates.• Begin NOW by studying the calculator manual.• DO THE HOMEWORK PRIOR TO EACH

CLASS. Exam questions are taken from this material.

• Write out definitions and terms. Do not just use a highlighter. Definitions given in class will be on exams.

STUDY TIPS contd.

• Use the Lecture Notes. They are on my Web Site and were written to help you on exams and to simplify note taking.

• See me during office hours if you are confused or overwshelmed.

• Ask questions until a topic is clear.

• Pay close attention and participate in class. Move to front if you cannot see.

DOWNLOAD LECTURE NOTES AND FILES FROM

WEBSITE• WEB SITE ADDRESS

IS IN SYLLABUS• DOWNLOAD

LECTURE NOTES• DOWNLOAD EXCEL

PROBLEMS• DOWNLOAD PPT

LECTURES FOR REFERENCE

• IF YOU DO NOT KNOW HOW TO DOWNLOAD, GET SOMEONE IN THE COMPUTER LAB TO HELP YOU.

• PRINT LECTURE NOTES AND BRING TO CLASS

My QualificationsR. Diggle, Jr. CFA

• BBA, MBA UNIV. OF MICHIGAN --finance and marketing

• PhD coursework Ohio State University --honors --finance

• 30 years of senior management

• Chartered Financial Analyst

• CEO largest bank --investment sub in the Intermountain West

• Director of Research and member of the management committee --two regional brokers

• BEEN THERE--DONE THAT!!

TEAM COMPANY REPORT

• PLEASE SEE PAGES 5-7 OF LECTURE NOTES DEALING WITH PROJECT.

• PRINT THE STEPS IN THIS PROJECT FROM THE EXCEL FILE I WILL GIVE YOU IN CLASS TODAY.

• I WILL MEET WITH EACH TEAM.

• YOUR IMMEDIATE JOB IS TO GET ORGANIZED AND PICK A COMPANY TO ANALYZE.

• NOTE: SET A TIME FOR REGULAR TEAM MEETINGS.

TEAM PRESENTATIONUSING EXCEL, COMPUSTAT AND POWERPOINT

• Sign up for a team today. Get names and phone number of teammates

• Pick a time when you ALL can meet to work on your project. See lecture notes for details.

• Pick an INDUSTRIAL company. Write for original last annual report ASAP (do not use internet copies)

• I will give each team an Excel disk to use to analyze your company

TEAM REPORT CONTD.

• GO TO MY WEB SITE• CHECK OUT

POSSIBLE COMPANIES ON BIGCHARTS AND NASDAQ DATABASE.

• CHECK EDGAR --SEC DATABASE

• MUST HAVE AT LEAST 5 YEARS OF HISTORY (NO RECENT IPOs) AND SALES OF AT LEAST $500 MILLION.

• MUST BE MAKING A PROFIT

• I WILL HELP YOU.

OBJECTIVES OF THIS TEAM REPORT (15% of grade)

• To become more comfortable making a formal presentation before a group.

• To learn how to use Powerpoint effectively

• To function as a team. This is a skill you will need throughout your career.

• Peer evaluations will be made. I know many of you work. Set team meeting times that work for all members.

THIS IS MS POWERPOINT

• It is EASY to learn• All you need to do is

outline your talk• Pick your slide format

and type slides from your outline. USE LARGE FONTS

• You may add Clip art to jazz up your talk

Be creative!!! It is fun• You can change the

presentation designs. Just make sure text is easily visible in back of room

• Be sure slide 1 lists the names of team members and your topic, class & date

• USE Windows 95 or Windows NT version

POWERPOINT IS POWERFUL

• When you have some slides done you can select the SLIDE SORTER VIEW LIKE THIS…….

• You can use the cut icon to move slides around

• You can insert spreadsheets of photos

• Use the “notes” icon 2nd

from right at bottom to write your “script.”

• Click on the “podium” icon at the lower right when you are ready to test a full page view for your talk.

• Save on a floppy and put on C drive before class.

TEAM MEETINGS --30 MIN

• EXCHANGE NAMES, PHONE NUMBERS AND E MAIL ADDRESSES AND GIVE INSTRUCTOR A COPY

• SET TIME FOR WEEKLY TEAM MEETING AND STUDY GROUP MEETING

• SELECT CANDIDATES FOR COMPANY PRESENTATION

I will spend 5 minutes with each team

Axioms of Finance--TEXT CH 11 Balancing risk and reward is

a key role of a manager. Some risk can be diversified away. Some cannot as we will see.

2 TVM -- our next lecture topic. Money received now is worth more than money received in future.

3 Cash is king!.4 Think incrementally!5 Competition is a great

equalizer. Companies with consistently high margins are rare.

6 Capital markets are “Efficient.” Efficiency is created by free flow of information and capital.

7 Owners and management objectives may not coincide.

8 Taxes affect ALL business decisions.

9 Some risk can be diversified away and some can’t

10 Ethics are important.

GOAL OF THE CORPORATION

• In this course we will focus on PUBLIC CORPORATIONS

• Other forms of organization are discussed on pp 4-6 of your text

• A Public Corporation is responsible to its owners

• The Board of Directors are chosen by the shareowners to oversee management.

• In the U.S. there is no National Corporation Act. Corporations are incorporated in a state.

What is the MOST IMPORTANT goal of the Modern Public Corporation?

• See TEXT P. 2: IT IS NOT profit maximization.

• The goal is “maximization of shareholder wealth” by increasing the price of the common stock over the long term.

There are many ways to accomplish this goal. Let us list a few:

Wealth Maximization is the key!!

• Profit maximization is very important but is only one way to increase shareholder value.– Increasing profits should be an important goal

however.– Wall Street focuses on Earnings per Share (not

net income) in measuring profits.

• Wealth maximization reflects ALL factors that contribute to a higher stock price.

HOW DO WE MEASURE WEALTH MAXIMIZATION?

• Return on Equity (ROE)– Net income / SH equity

OR ROA divided by

Total debt/ total assets

THIS IS CALLED THE DUPONT MODEL

SEE TEXT P. 107

• Increasing ROE– > sales

– > net income

– > net margin

– Make an acquisition where margins are improved

– Make a divestiture where profits >

– Buy back stock

Ways to Maximize S/H Value

• Increasing sales– Internal growth

– Acquisition

• Increasing profit margins– Decreasing costs

– Emphasizing profitable lines or products

• Buying back stock• Using “Financial

Leverage” (Debt) to magnify return to shareowners

• Reducing taxes• Can you think of other

ways?

Maximizing Shareholder ValueBy buying back stock

• RECAP ROE = NET INCOME / TOTAL COMMON EQUITY

• COMMON EQUITY = VALUE OF COMMON STOCK ON BALANCE SHEET

• USING CASH TO BUY BACK COMMON STOCK REDUCES COMMON EQUITY

ACCOUNTING REVIEW

FIN 3403

Has it been more than 2 years since you had basic accounting?

SUGGESTION

Please STUDY ch 3 p. 81-111 NOWWhile this chapter is assigned later to study ratios, it

is important for you to review this material since accounting knowledge is assumed in this course.

Ask questions if you are unclear on any concept in this chapter. I am here to help.

Income statement review: ACCOUNTING PROFIT

SALES (units x price)

less Cost Goods sold =

GROSS INCOME

less SG&A

less depreciation =

OPERATING INCOME

plus other income

less interest expense=

EBIT (Earnings before interest and taxes)

EBIT less interest exp. =

PRETAX INCOME

less FIT paid =

Net Income

less Dividends paid to Common shareholders=

Contribution to Retained Earnings (PLOWBACK)

E.P.S. = Net income /

common shs outstanding

Why does Wall Street Focus on E.P.S.?

• EPS measures the return to the shareowner. Stock prices are usually measured in terms of the PRICE / EARNINGS RATIO which relates S/H value to earnings.

• Many things impact E.P.S. Some are outside control of management such as tax rate or mandated depreciation rules.

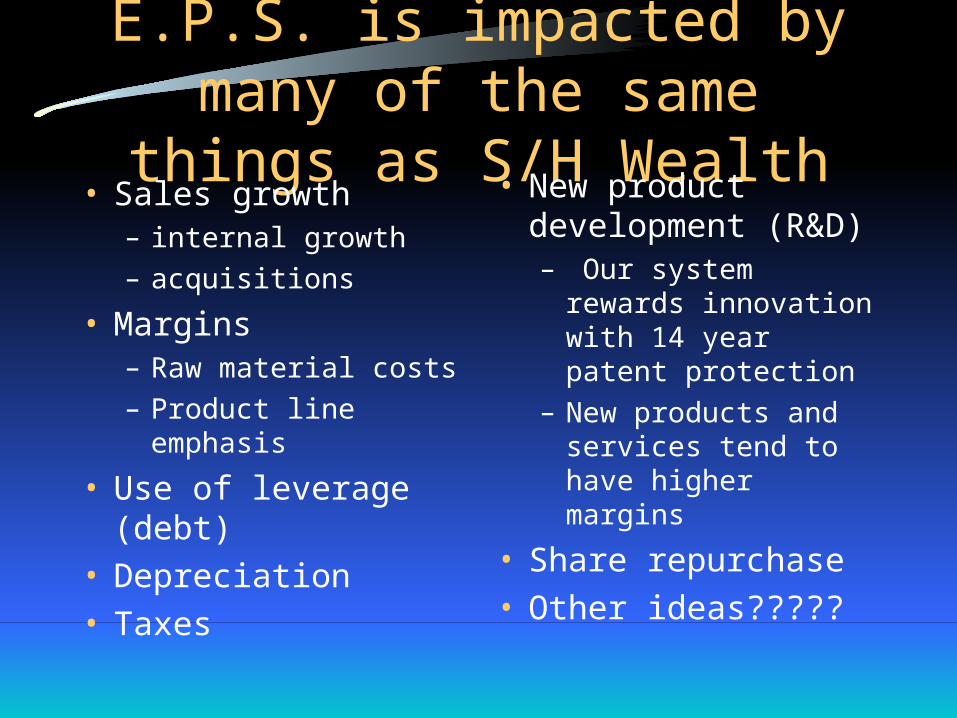

E.P.S. is impacted by many of the same things as S/H Wealth

• Sales growth– internal growth

– acquisitions

• Margins– Raw material costs

– Product line emphasis

• Use of leverage (debt)• Depreciation• Taxes

• New product development (R&D)– Our system rewards

innovation with 14 year patent protection

– New products and services tend to have higher margins

• Share repurchase• Other ideas?????

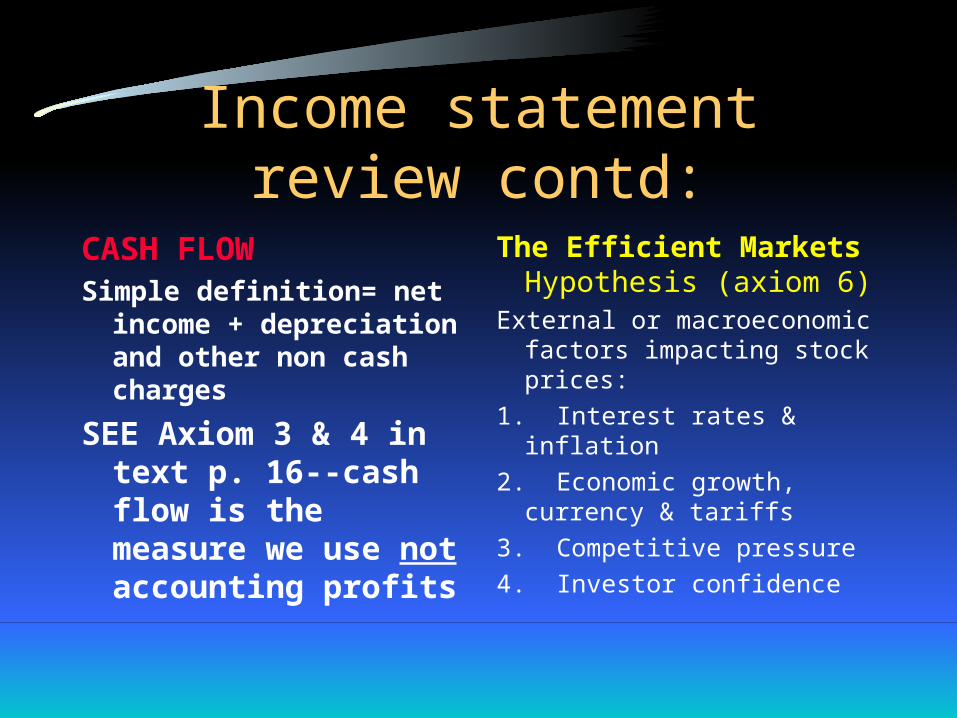

Income statement review contd:

CASH FLOWSimple definition= net

income + depreciation and other non cash charges

SEE Axiom 3 & 4 in text p. 16--cash flow is the measure we use not accounting profits

The Efficient Markets Hypothesis (axiom 6)

External or macroeconomic factors impacting stock prices:

1. Interest rates & inflation

2. Economic growth, currency & tariffs

3. Competitive pressure

4. Investor confidence

Balance Sheet Review

ASSETS• Cash + AR + Inv =

Current AssetsCurrent = less than 1 year

___________________• Long term assets

– Plant & equipment

– “Goodwill”

• TOTAL ASSETS

LIABILITIES AND S/H EQUITY

• Current Liabilities______________________________________________________

• Long term liabilities– LT debt + Pfd stock

• COMMON EQUITY= CS + SURPLUS + RE

“Net worth” or equity capital = TA - TL

TOTAL LIAB + S/H EQ.

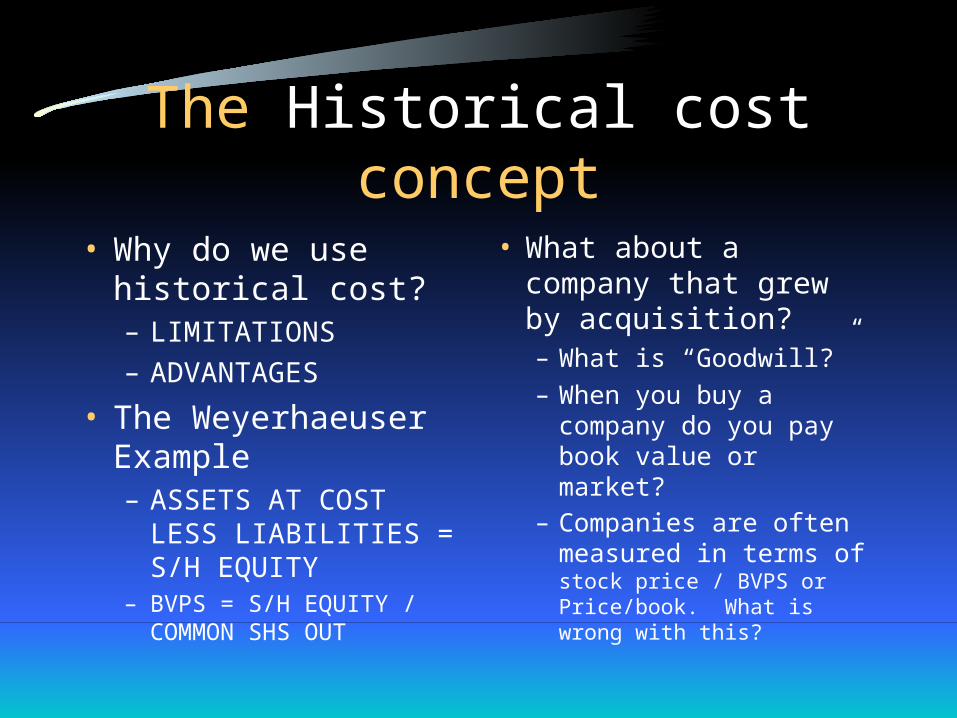

The Historical cost concept

• Why do we use historical cost?– LIMITATIONS– ADVANTAGES

• The Weyerhaeuser Example– ASSETS AT COST

LESS LIABILITIES = S/H EQUITY

– BVPS = S/H EQUITY / COMMON SHS OUT

• What about a company that grew by acquisition?– What is “Goodwill?”– When you buy a

company do you pay book value or market?

– Companies are often measured in terms of stock price / BVPS or Price/book. What is wrong with this?

ASSIGNMENT • SEE SYLLABUS FOR ASSIGNMENTS

• MEET WITH YOUR TEAM OUTSIDE CLASS.

• CHECK OUT WEB SITE

• DOWNLOAD LECTURE NOTES AND OTHER FILES

• READ CH. 1

• STUDY CALCULATOR MANUAL AND GET FAMILIAR WITH KEYS

TVM AND THE USE OF THE TI BA2+ FINANCIAL CALCULATOR

FIN 3403 UCF School of Business

R. DIGGLE, CFA

RECAP OF LAST LECTURE

• We learned about Powerpoint and how you will be using it.

• We examined the concept of Wealth Maximization

• We compared an income statement and a cash flow statement

• We reviewed the 10 axioms of finance summarized on p. 26 of your text.

• If you are rusty on accounting --STUDY chapter 3 ASAP

• Are there questions from last time???

TEAM ORGANIZATION

• ARE YOU SIGNED UP WITH A TEAM?

• HAVE YOU PICKED A COMPANY?

• DO YOU HAVE A REGULAR TIME SET FOR TEAM MEETINGS THAT IS OK WITH ALL?

All teams will meet with

• HAVE YOU CHECKED OUT MY WEB SITE?

• DO YOU ALL HAVE A TIBA2 + CALCULATOR?

• HAVE YOU STUDIED CALC.MANUAL?

me at end of this class

Company Ratio Analysis Project

• Read instructions in Lecture Notes.

• Copy ALL Excel spreadsheets on disk onto blank disks for each team member. Return original disk to instructor. Do NOT write on my disk.

• Print instructions for each team member. Work on assigning tasks for everyone.

• Make a list of questions for instructor.

TVM

• IN ALL TOPICS WE WILL PROCEED AS FOLLOWS:– THEORY– APPLICATIONS– TEXT PROBLEMS– ADDITIONAL PRACTICAL PROBLEMS– QUESTIONS AND REVIEW

• WE WILL REFER TO LECTURE NOTES FIRST AND THEN TO TEXT.

TIME VALUE OF MONEYsee lecture notes p. 8-10

CONCEPT I: The “PRESENT VALUE” of one dollar received in the FUTURE is worth less than a dollar received today.

CONCEPT 2: The further out in the future money is received the less is its “NET PRESENT VALUE”

CONCEPT 3: When we compound money (as in a savings account) the FUTURE VALUE is increased in direct proportion to the rate of interest and the number of compounding periods.

THE FINANCIAL CALCULATOR AND TVM

TABLES HELP YOU MEASURE PV AND FV

PRACTICAL THINGS YOU WILL LEARN IN THIS PART

OF THE COURSE

• Determining how much money you must save for retirement.

• Computing a mortgage payment.

• Determining a lease payment on a car.

• Figuring how much you need to save to put a child through college.

• Measuring return on investment

QUESTION 1:

• ALBERT EINSTEIN WAS ASKED WHAT THE MOST IMPORTANT INVENTION OF MANKIND WAS? WHAT WAS HIS REPLY?

• HINT: HE DID NOT SAY E = MC2

HOW MANY OF YOU BELIEVE YOU WILL BE A

MILLIONAIRE?

• RAISE YOUR HANDS IF YOU FIRMLY BELIEVE YOU CAN DO THIS.

• WHAT IS YOUR ACTION PLAN?

CAN YOU SAVE $300 PER MONTH?

• ASSUME YOU ARE OUT OF UCF AND WORKING.

• UCF FINANCE/ACCTG. MAJORS SHOULD START AT $35K

• RAISE YOU HAND IF YOU THINK YOU CAN SAVE $300 PER MONTH

You can be a Millionaire. I will show you how! Can you Save $300 per month

YEAR FV FVN=P/Y I/Y = 10% I/Y = 15%X YEARS P/Y =12 P/Y =12

PMT = -300 PMT = -300

1 3,801$ 3,906$ 5 23,425$ 26,904$

10 61,966$ 83,597$ 20 229,709$ 454,786$ 30 683,798$ 2,102,946$

ANNUALLY AT 10% AND 15%RULE OF 72 = 72 / I/Y

NUMBER OF YRS FOR A SUM TO DOUBLE

72/10= 7.2 yrs 72/15=4.8 YRS

SEE LECTURE NOTES PP. 8-14

• Turn to page 9 NOW• You may wish to either take notes on Lecture notes

or incorporate class notes in with lecture notes.• All material in the next slides is also discussed in

lecture notes.• THIS MATERIAL IS THE MOST

IMPORTANT MATERIAL IN THE COURSE. REVIEW IT IN YOUR TEAM

FV CONCEPTS

• An INCREASE in I/Y > FV

• AS N increases FV >• The more frequent the

compounding (P/Y) the more FV >.

• FVn= PV (1+r)n

Learn this formula. See lecture notes. Formulas

will be provided in exam

NPV CONCEPTS (See lec notes p 9)• As the interest rate I/Y > the < PV• The longer the time period N, the

more PV <.• The more frequent the

compounding P/Y the more PV <.

• PV = FV n lump sum (1+r)n

Annuity

• PVA = FV + FV + FV

(1+R) (1+R)2 (1+R)n

?

HISTORICAL INVESTMENT RETURNS

Ibbotson Data 1928 to present

NOMINAL

COMMON STOCKS 13%

LONG TERM BONDS 8%

SAVINGS ACCOUNTSAND T BILLS

3%

REAL

COMMON STOCKS 10%

LONG TERM BONDS

5%

SAVINGS ACCOUNTS

AND T-BILLS

0%

Value of $5000 INVESTED ONCE at different rates of returnSET BGN, P/Y =1, PV = -5000 RATE: 3% 5% 8% 12%YRS =N FV FV FV FV

5 5,796$ 6,381$ 7,347$ 8,812$ 10 6,720$ 8,144$ 10,795$ 15,529$ 15 7,790$ 10,395$ 15,861$ 27,368$ 20 9,031$ 13,266$ 23,305$ 48,231$ 25 10,469$ 16,932$ 34,242$ 85,000$ 30 12,136$ 21,610$ 50,313$ 149,800$ 35 14,069$ 27,580$ 73,927$ 263,998$

Value of $300 PER MONTH at different rates of return

SET BGN , P/Y =12 PMT = -300RATE (I/Y): 5% 8% 12%YEARS N FV FV FV

5 60 20,402$ 22,043$ 24,501$ 10 120 46,585$ 54,884$ 69,012$ 15 180 80,187$ 103,811$ 149,874$ 20 240 123,310$ 176,706$ 296,777$ 25 300 178,653$ 285,308$ 563,654$ 30 360 249,678$ 447,108$ 1,048,489$ 35 420 340,828$ 688,165$ 1,929,288$

USING THE TVM TABLES IN THE BACK OF YOUR TEXT

• BACK FLYLEAF– B = FV of A Lump

sum. A lump sum is one payment or receipt.

– D = FV of an “annuity” An annuity is a repetitive payment or income.

– C = PV of a lump sum– E = PV of an annuity

• TEXT PP. 883 TO 890 --more detail

• B = pp. 883 to884• C = pp. 885 to 886• D = pp. 887 to 888• E = pp. 889 to 890

NOTE: TABLES ARE FOR ANNUAL PERIODS ONLY

TABLES APPLICATION• NOTE: Tables will be provided in Exam 1• STEPS:

Must determine WHICH TABLE you must use– COLUMN = interest rate ROW = years– TABLES ARE ANNUAL ONLY

• What is the value of $10,000 compounded at 5% for 15 years?– TABLE B p. 883 value = 2.079– Multiply table value times PV of $10000– Answer is $20,790

TABLES VS. FINANCIAL CALCULATOR

• We will begin using the tables in the back of your text. The tables are ANNUAL. This will help you understand basic concepts.

• You will have problems using tables in EXAM 1.

• We will move from the tables to your Financial Calculator. Bring the calculator to each class and exam. The new calculators are easy to use and prompt you for an answer. Data can be monthly, daily or any other time frame.

Using your Financial Calculator to solve TVM problems

• The calculator provides more

accurate answers than tables• 5 TVM VARIABLES (excluding P/Y)

THE THIRD ROW OF KEYS ON YOUR CALCULATOR

P/Y = Compounding periods per year

I/Y = Annual interest rate

N = (p/y x # of years)

PMT FV PV

• You can enter data in any order. • YOU CAN SOLVE FOR ANY OF THE VARIABLES

CALCULATOR SET UP• Set 4 decimal point accuracy as follows:

– 2nd format– DEC = 4

• Set BGN or END as follows:– 2nd BGN (above PMT key)– To toggle press 2nd ENTER to

change from BGN to END

If BGN is set it appears in upper right of display

• Clear REGISTERS– 2nd CLR TVM, 2nd CLR WORK, 2nd QUIT

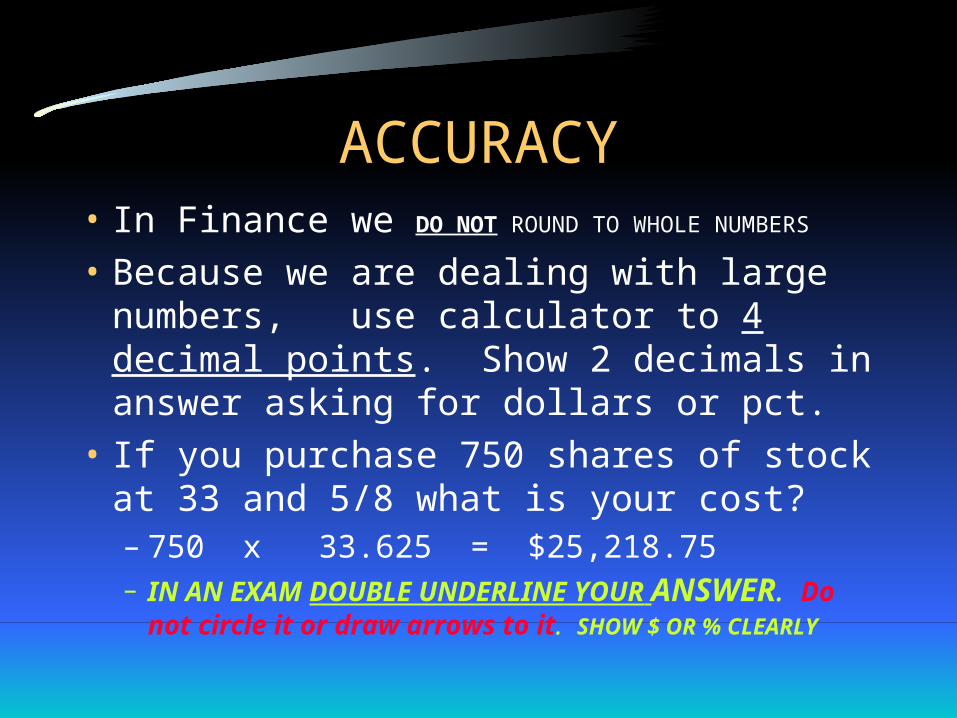

ACCURACY• In Finance we DO NOT ROUND TO WHOLE NUMBERS

• Because we are dealing with large numbers, use calculator to 4 decimal points. Show 2 decimals in answer asking for dollars or pct.

• If you purchase 750 shares of stock at 33 and 5/8 what is your cost?– 750 x 33.625 = $25,218.75– IN AN EXAM DOUBLE UNDERLINE YOUR

ANSWER. Do not circle it or draw arrows to it. SHOW $ OR % CLEARLY

THE 6 TVM KEYS -3rd row• P/Y (2nd P/Y = number of compounding

periods per year)

• N = number of time periods = P/Y times number of years

• I/Y = annual interest rate (8.5% entered 8.5)

• PV = Present value (outflows are entered by entering number and pressing MINUS key in lower right)

• PMT = annuity payment (inflow or outflow)

• FV = Future value

USING YOUR TI BA II + FINANCIAL CALCULATOR TO DO TVM PROBLEMS

• See lecture notes p.11• FOLLOW THESE STEPS

– READ QUESTION

– Clear all registers

– Set BGN or End

– Set P/Y--2nd P/Y--enter number --press ENTER

– Determine what you are solving for

– WRITE INPUTS NEATLY

• STEPS CONTD– Enter 4 TVM inputs on

calculator. I suggest you do it in same order each time.

– Enter data with outflows negative

– enter CPT and TVM key for solution

– Check inputs– Is solution logical?

What do the KEYS mean?

• P/Y must be reset for each problem. P/Y = number of compounding periods per year

• N = years times P/Y. In a 20 year mortgage with monthly payments N = 240.

• I/Y is the stated rate.

• PMT = Regular repetitive payments such as a mortgage or car payment. Enter outflows as a negative number.

• PV = Present value• FV = Future value

Enter data in any order

Calculator keys contd.• BGN vs END

– Set BGN unless otherwise specified in problem.

– BGN means interest accrues from day 1.

– END means interest accrues at end of period.

– ALL EXAM QUESTIONS WILL SPECIFY BGN OR END

• If BGN is set, the letters BGN appear in upper right of your calculator window.

• CLEARING REGISTERS. There are multiple memory registers in the TI BA II +. Clear them ALL.

SELF TEST PROBLEMS

• ANSWERS TO ALL ST PROBLEMS ARE AT END OF CHAPTER.

• PROBLEMS ARE ON P. 193. ANSWERS ARE ON PP. 204-5.

• I recommend you do ST problems FIRST in each chapter to learn how to approach problems. ST problems are NOT in homework assignments.

ST PROBLEMS CH 5 P. 193• ST1 This is the FV of

a lump sum--Table A• This is a 2 step

problem:– A. 8% column, 3 year

line. FACTOR = 1.2597= $31500

– B. 10% column, 3 year line. FACTOR = 1.3310

– answer = $41926

• ST1 on financial calculator:

• Set BGN P/Y = 1• n = 3• i/y = 8• pv = -25000 (OUTFLOW)

• FV (PART A) = $31492--Note that this differs slightly from table amount

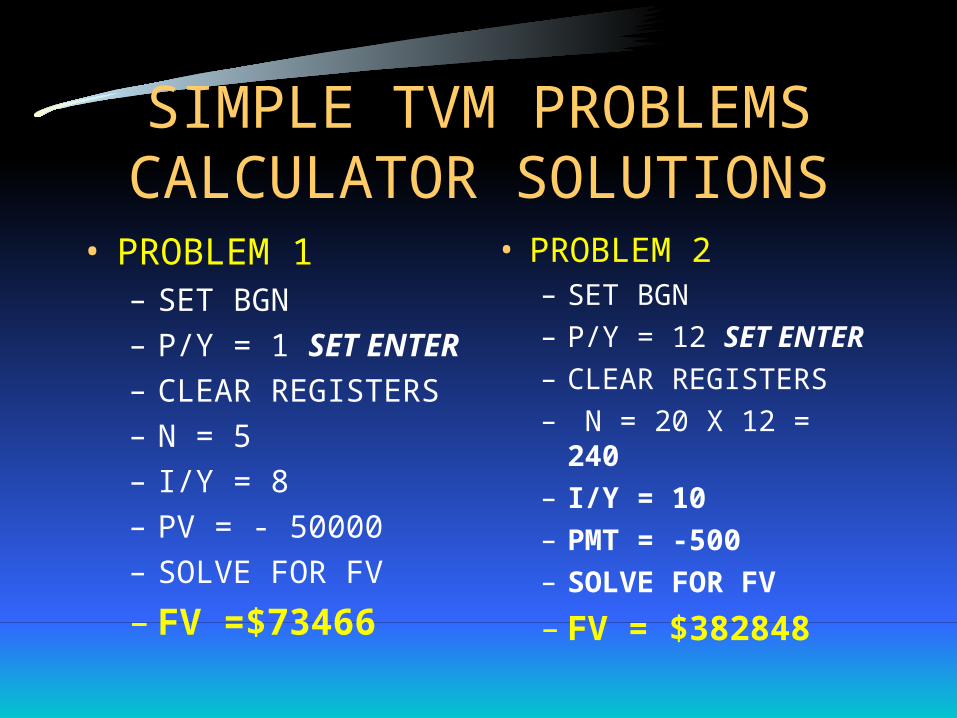

SIMPLE TVM PROBLEMS1. LUMP SUM FV

You inherit $50,000 now. You invest this money at 8% interest. What is this worth in 5 years?

2. ANNUITY FV You save $500 per month at 10% return. What is this worth in 20 years?

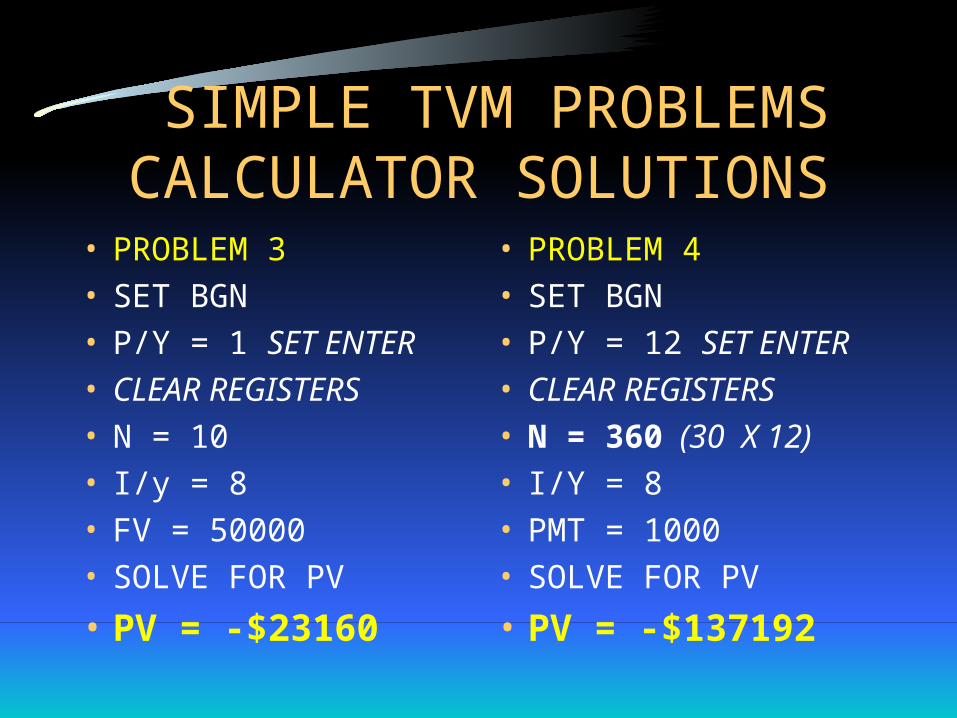

3. LUMP SUM PV You inherit $50000 in 10 years. Assuming an 8% return, what is this worth today?

4. ANNUITY PV You win the lottery. You are paid $1000 per month over 30 years. At an 8% return, what is this worth today?

SIMPLE TVM PROBLEMS CALCULATOR SOLUTIONS

• PROBLEM 1– SET BGN

– P/Y = 1 SET ENTER

– CLEAR REGISTERS

– N = 5

– I/Y = 8

– PV = - 50000

– SOLVE FOR FV

– FV =$73466

• PROBLEM 2– SET BGN

– P/Y = 12 SET ENTER

– CLEAR REGISTERS

– N = 20 X 12 = 240

– I/Y = 10

– PMT = -500

– SOLVE FOR FV

– FV = $382848

SIMPLE TVM PROBLEMS CALCULATOR SOLUTIONS

• PROBLEM 3• SET BGN• P/Y = 1 SET ENTER• CLEAR REGISTERS• N = 10• I/y = 8• FV = 50000• SOLVE FOR PV

• PV = -$23160

• PROBLEM 4• SET BGN• P/Y = 12 SET ENTER• CLEAR REGISTERS• N = 360 (30 X 12)• I/Y = 8• PMT = 1000• SOLVE FOR PV

• PV = -$137192

ASSIGNMENT• COMPLETE SIMPLE TVM PROBLEMS AT

END OF CH. 5. DO THIS WITH YOUR STUDY GROUP. Print your name, date, course and section and problem ch 1 on page one of your assignment. STAPLE.

• I am providing solutions. They are also on web site

• Begin work on PROBLEM HANDOUT IN YOUR STUDY GROUP.

• LIST ANY QUESTIONS YOU MAY ENCOUNTER IN USING YOUR CALCULATOR OR TABLES.

TEAM MEETINGS • Is there anyone not signed up on a team?

• Do you have a meeting time set?

• Pick a company for team analysis projectONE EXCEL DISK GIVEN TO EACH TEAM

FOR NEXT TIME COPY DISK FOR EACH TEAM MEMBER AND RETURN ORIGINAL TO INSTRUCTOR

Do homework problems assigned. Homework must be STAPLED and have name, assignment Fin 3403, section and date on p. 1

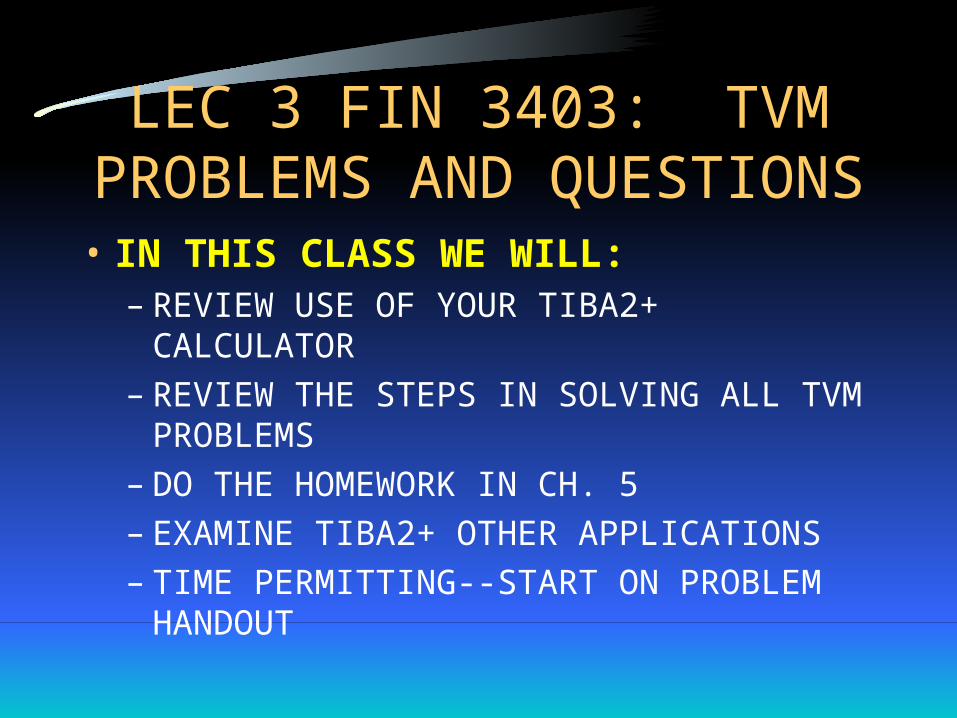

LEC 3 FIN 3403: TVM PROBLEMS AND QUESTIONS• IN THIS CLASS WE WILL:

– REVIEW USE OF YOUR TIBA2+ CALCULATOR

– REVIEW THE STEPS IN SOLVING ALL TVM PROBLEMS

– DO THE HOMEWORK IN CH. 5– EXAMINE TIBA2+ OTHER APPLICATIONS– TIME PERMITTING--START ON PROBLEM

HANDOUT

REVIEW: STEPS IN SOLVING TVM PROBLEMS ON AN EXAM

• See lecture notes p.11• FOLLOW THESE

STEPS– READ QUESTION

– Clear all registers

– Set BGN or End

– Set P/Y--2nd P/Y--enter number --press ENTER

– Determine what you are solving for

– List inputs on TIBA2+

• STEPS CONTD– Enter 4 TVM inputs on

calculator. I suggest you do it in same order each time.

– Enter data with outflows negative

– enter CPT and TVM key for solution

– Check inputs– Is solution logical?

COMMON EXAM MISTAKES

• Failure to clear registers between EACH problem

• Failure to reset P/Y – Default value is 12 since

things like a mortgage or car payment are made monthly

• Failure to set BGN or END--given for each problem

• setting N = yrs x P/Y– YRS 2nd N

– Press N again

• MOST IMPORTANT:

– FAILURE TO NEATLY LIST INPUTS:

– I WILL GIVE PARTIAL CREDIT IF YOU DO THIS

• Failure to check inputs twice. Is answer logical?

HOW TO GET AN “A’ ON EXAM 1• EXAM 1 WILL FOCUS

ON TVM.• WORK PROBLEMS Be

sure you understand each step. Work with classmates.

• ASK QUESTIONS!!! This is confusing at first but you will get the hang of it.

• Read the problem over carefully before starting!

• Always follow the steps I just outlined and draw a time line.

• Write down inputs.• Go through handouts.

Solve them on your calculator.

CH 5 HOMEWORK

• SET A: 5-1 TO 5-15, 5-19 TO 5-21 – SOLUTIONS PROVIDED THROUGH 5-6 A– PARTIAL SOLUTIONS PROVIDED FOR

OTHER PROBLEMS– TABLE SOLUTIONS PROVIDED TO

ANNUAL PROBLEMS ONLY 5-1A TO 5-7A– TIBA2+ SOLUTIONS PROVIDED --answers

in italics

THE TI BA II + FINANCIAL CALCULATOR: ADVANCED FUNCTIONS

• SPREADSHEET REGISTERS– During the term we

will use several built in worksheets. Become familiar with them and read how to use them in the TI manual

• Use the right spreadsheet to check work on TVM keys

• Days between dates– 2nd 1 solve for DBD– DAYS BETWEEN DATES

• Delta % (CHANGE)– 2nd 5

• Cash Flow worksheet– 2nd CF– use in 2nd part of course

• Bond worksheet– 2nd and 9– use in last 3rd. of course

OTHER TVM PROBLEMS

• You want to buy a home. You decide on a 30 year mortgage with an interest rate of 6.75%. The home costs $100,000 and you put 20% down. How much is your monthly payment for P&I (principal & interest)? SET END.

• LIST INPUTS– SET END

– P/Y = 12

– N = 360

– I/Y = 6.75

– PV = - 80000 (MTG)

– FV = 0

– SOLVE FOR PMT

– PMT = 518.87

OTHER TVM PROBLEMS

• You want to retire at age 60. You are 25.

• You figure you need $1 million to retire comfortably.

• You can save $300 per month.

• What return do you need to achieve your goal?

• SET END --THIS WILL ALWAYS BE GIVEN

• P/Y = 12

• n = 420 (35*12)

• PV = 0

• PMT = -300

• FV 1000000

• SOLVE FOR I/Y

• I/Y = 9.49%

OTHER TVM PROBLEMS

• You LEASE a car.• The cost is $20,000 +

6% tax and $300 dealer prep.

• The dealer is offering 0.99% financing.

• The term is 3 years.• The residual is $10000• What is the payment?

• Set BGN.• P/Y = 12• n = 36• I/Y = 0.99• PV = - 21500• FV = 10000• SOLVE FOR PMT

• PMT = 332.31

TVM PROBLEMS: HANDOUT

TVM will be 70-80% of Exam 1 Practice using your calculator to solve

problems in text, workbook and handouts Let us go through a series of real world

applications of TVM that you will use in your own personal finance. PLEASE INTERRUPT AT ANY TIME WITH QUESTIONS. DON’T BE SHY!

RULE OF 72

• WHAT IS IT?

NUMBER OF YEARS FOR A SUM TO DOUBLE

• 72 / STATED INTEREST RATE = YRS TO DOUBLE

• At 10% money doubles in 7.2 years:– 72/ 10 = 7.2

• At 15% money doubles in 4.8 years:– 72/15 = 4.8

• At 5% money takes 14.4 years to double.

CH 1 HOMEWORK TVM

• 5-1A AND 5-2A P. 193

• 5-3A - 5-9A P. 194• 5-10A -5-15A P. 195• 5-19A - 5-21A P. 196• SOLUTION ON

DISK + handout (1 per team please)

• DO PROBLEMS IN YOUR TEAM

• Which table?• Determine table value.• List calculator inputs• Solutions page shows

answer in bold italics.• If unclear, write down

questions for class.