27

Fixed Income Presentation March 2017

Fixed Income Presentation March 2017

2

Legal Disclaimers

Forward Looking Statements. This presentation may contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. The words “believe,” “expect,” “project,” “will,” “should,” “could” and similar expressions are intended to identify such forward-looking statements. These forward-looking statements reflect the Company’s best judgment based on current information, and although we base these statements on circumstances that we believe to be reasonable when made, there can be no assurance that future events will not affect the accuracy of such forward-looking information. As such, the forward-looking statements are not guarantees of future performance, and actual results may vary materially from the projected results and expectations discussed in this report. Factors that might cause the Company’s actual results to differ materially from those anticipated in forward-looking statements include, but are not limited to: (1) competitive pressure on sales and pricing, including pressure from imports and substitute materials; (2) U.S. and foreign trade policies affecting steel imports or exports; (3) the sensitivity of the results of our operations to prevailing steel prices and changes in the supply and cost of raw materials, including pig iron, iron ore and scrap steel; (4) availability and cost of electricity and natural gas which could negatively affect our cost of steel production or could result in a delay or cancelation of existing or future drilling within our natural gas working interest drilling programs; (5) critical equipment failures and business interruptions; (6) market demand for steel products, which, in the case of many of our products, is driven by the level of nonresidential construction activity in the U.S.; (7) impairment in the recorded value of inventory, equity investments, fixed assets, goodwill or other long-lived assets; (8) uncertainties surrounding the global economy, including the severe economic downturn in construction markets and excess world capacity for steel production; (9) fluctuations in currency conversion rates; (10) significant changes in laws or government regulations affecting environmental compliance, including legislation and regulations that result in greater regulation of greenhouse gas emissions that could increase our energy costs and our capital expenditures and operating costs or cause one or more of our permits to be revoked or make it more difficult to obtain permit modifications; (11) the cyclical nature of the steel industry; (12) capital investments and their impact on our performance; and (13) our safety performance. These and other factors are discussed in Nucor's regulatory filings with the Securities and Exchange Commission, including those in Nucor's fiscal 2016 Annual Report on Form 10-K, Item 1A. Risk Factors. We do not undertake any obligation to update or publicly release any revisions to our forward-looking statements to reflect subsequent events, changed circumstances or changes in our expectations after the date of a particular forward-looking statement, except as required by applicable law.

Non-GAAP Financial Information. This presentation includes financial measures that do not conform to U.S. generally accepted accounting principles (“GAAP”). Non-GAAP financial measures are defined and reconciled to the most comparable GAAP financial measures at the end of this presentation. These measures are provided as a supplement to, and not as a substitute for, GAAP measures of performance. Furthermore, these measures may not be consistent with similar measures provided by other companies.

No Offer or Solicitation. This document is not a prospectus or a prospectus equivalent document. This document is not intended to and does not constitute, or form part of, any offer, invitation to the solicitation of any offer to purchase, acquire, subscribe for, sell or otherwise dispose of any securities, or the solicitation of any vote or approval in any jurisdiction, issuance or transfer of securities of Nucor.

Disclaimer. Nucor believes the information contained in this material to be reliable but does not warrant its accuracy or completeness. Data and information provided by the unaffiliated third parties has not been independently verified.

Fixed Income Presentation | March 2017

3

Table of Contents

Business Overview & Investment Highlights

Financial Results II.

I.

Fixed Income Presentation | March 2017

4

I. Business Overview & Investment Highlights

5

Nucor Business Overview

• North America’s most diversified steel and steel products company

• Nucor (Baa1/A-) is the largest steel producer in the United States, operating 24 scrap-based steel mills that have an annual production capacity of approximately 26.7 million tons. Nucor is North America’s largest recycler.

• Market Capitalization of ~$20bn

• Primary business segments: Steel mills, Steel products, Raw Materials

• Operations throughout the value chain, supported by a sustainable raw materials division

• Nucor, through The David J. Joseph Company, also brokers ferrous and nonferrous metals, pig iron and HBI/DRI; supplies ferro-alloys; and processes ferrous and nonferrous scrap

• Products produced include:

• Carbon and alloy steel; steel piling; hollow structural section (HSS) tubing; electrical conduit; steel joists and joist girders; steel deck; fabricated concrete reinforcing steel; cold finished steel; steel fasteners; metal building systems; steel grating and expanded metal; and wire and wire mesh

• Key Acquisitions include:

• Tubular Acquisitions: Independence Tube: 2016 - $430mm (HSS), Southland Tube: 2017 - $130mm (HSS), Republic Conduit: 2017 - $335mm (electrical conduit)

• Gallatin Steel: 2014, $770mm (flat-rolled steel mill)

• Skyline Steel: 2012, $675mm (steel piling distribution)

• David J. Joseph: 2008, $1.44bn (scrap processing & brokerage)

• Harris Steel: 2007, $1.1bn (rebar fabrication, cold-finish steel, steel trading & distribution)

Steel Mills Production 21.3 million tons

Facilities Over 200 locations

2016 Net Sales $16.2 billion

2016 Net Earnings $796 million

2016 Cash, Cash Equivalents & Short-Term Investments

$2.2 billion

2016 Fortune 500 Rank 170

Employees 23,900

2016 Net Sales Per Employee US$678k

Source: Company filings; Fortune 500 website and Bloomberg as of March 1, 2017

Fixed Income Presentation | March 2017

6

Key Nucor Highlights

Nucor’s Culture and Management Team Drive Strategy for Profitable Growth

Most Diversified US Producer of Steel and Steel Products

Sustainable Profitability and Highly Variable Cost Structure Protects Margin Spread

Recent Strategic Investments Yielding Higher and Less Volatile Returns

Market Leadership in North America with Leverage to Growing End Markets

1

2

6

7

3

Consistent Cash Flow Generation and Strong Liquidity Position 4

Long Term Commitment to Investment Grade rating and Lowest Sector leverage 5

Fixed Income Presentation | March 2017

7

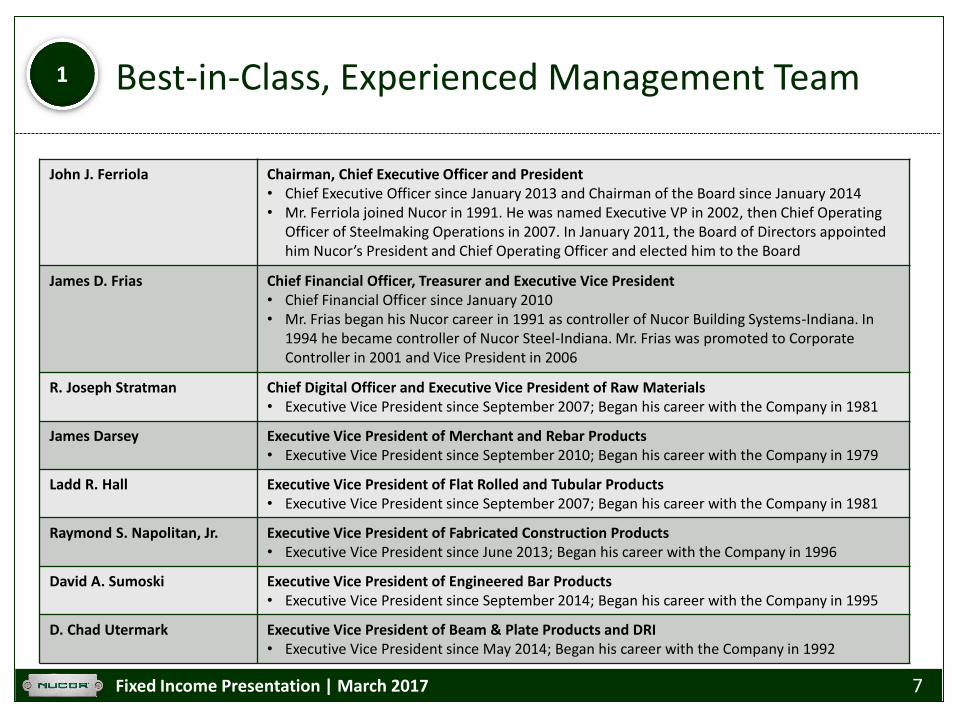

Best-in-Class, Experienced Management Team

John J. Ferriola Chairman, Chief Executive Officer and President • Chief Executive Officer since January 2013 and Chairman of the Board since January 2014 • Mr. Ferriola joined Nucor in 1991. He was named Executive VP in 2002, then Chief Operating

Officer of Steelmaking Operations in 2007. In January 2011, the Board of Directors appointed him Nucor’s President and Chief Operating Officer and elected him to the Board

James D. Frias Chief Financial Officer, Treasurer and Executive Vice President • Chief Financial Officer since January 2010 • Mr. Frias began his Nucor career in 1991 as controller of Nucor Building Systems-Indiana. In

1994 he became controller of Nucor Steel-Indiana. Mr. Frias was promoted to Corporate Controller in 2001 and Vice President in 2006

R. Joseph Stratman Chief Digital Officer and Executive Vice President of Raw Materials • Executive Vice President since September 2007; Began his career with the Company in 1981

James Darsey Executive Vice President of Merchant and Rebar Products • Executive Vice President since September 2010; Began his career with the Company in 1979

Ladd R. Hall Executive Vice President of Flat Rolled and Tubular Products • Executive Vice President since September 2007; Began his career with the Company in 1981

Raymond S. Napolitan, Jr. Executive Vice President of Fabricated Construction Products • Executive Vice President since June 2013; Began his career with the Company in 1996

David A. Sumoski Executive Vice President of Engineered Bar Products • Executive Vice President since September 2014; Began his career with the Company in 1995

D. Chad Utermark Executive Vice President of Beam & Plate Products and DRI • Executive Vice President since May 2014; Began his career with the Company in 1992

Fixed Income Presentation | March 2017

1

8

Nucor’s People & Culture

Fixed Income Presentation | March 2017

1

9

Five Drivers to Profitable Growth

1. Low Cost Producer

2. Market Leadership

3. Move Up The Value Chain

4. Expand Channels To Market

5. Commercial Excellence

Fixed Income Presentation | March 2017

1

10

Sheet37%

Bar22%

Structural10%

Plate8%

Finished products(1)

11%

Other12%

Sheet58%

Bars and Structure

21%

Finished Products(1)

9%

Other12%

Sheet72%

Bars and Structure

28%

Sheet67%

U.S.Steel Europe30%

Tubular3%

Most Diversified U.S. Producer of Steel and Steel Products

Source: Company Filings. 2016 data except for ArcelorMittal’s breakout by product type (2015)

Nucor Volumes Sold to External Customers ArcelorMittal

U.S. Steel

Steel Dynamics

2

(1) Finished products consist of Steel Joists, Steel Deck, Cold finished Steel and Rebar Fabrication Products for Nucor. Sections and Semis for ArcelorMittal

Total Tons Sold in 2016: 24,309kt

Total Tons Sold in 2016: 76,144kt

Total Tons Sold in 2016: 14,990kt

Total Tons Sold in 2016: 9,246kt

Fixed Income Presentation | March 2017

11

Market Leadership in North America

Source: SEC Filings, Industry Data, First River Consulting

Structural Steel

Rebar Steel

Merchant Bar Steel

Cold Finished Bar Steel

Sheet Steel (hot + cold + galvanized)

Plate Steel

SBQ Bar Steel

#1 North American

Market Leader

Steel Joist & Deck

Rebar Fab & Distribution

Steel Piling Distribution

Metal Buildings

#2 North American

Market Leader

#3 North American

Market Leader

Hollow Structural Section (HSS) Steel Tubing

Steel Electrical Conduit Pipe

Fixed Income Presentation | March 2017

3

12

North American Footprint Levered to Strong End Markets

9

11

13

15

17

19

2013 2014 2015 2016 2017P 2018P

Nu

mb

er o

f V

ehic

les

Bu

ilds

(in

mill

ion

s)

Non-Residential Construction

45%

Heavy Equipment / Ag / Transportation /

Industrial Goods 25%

Auto / Consumer Durables

12%

Power & Energy 10%

Other 8%

N.A. Light Vehicle Production

Nucor’s Operating Footprint

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

2013 2014 2015 2016 2017P 2018P

An

nu

al V

alu

e o

f C

on

stru

ctio

n (

in m

illio

ns)

U.S. Non-Residential Construction Put in Place

Steel Mills

Steel Products

Raw Materials

Steel Products Joint Ventures

Approx. Shipments by End Market

Source: U.S. Census, Dodge Analytics AIA

Source: Bloomberg, Ward’s AutoInfoBank, LMC Automotive, IHS Automotive, CAAM, AutoData, ACEA,

Fixed Income Presentation | March 2017

3

13

Consistent Cash Flow Generation

Source: Company Filings

$-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(in

bill

ion

s o

f d

olla

rs)

$495 Million Average ‘01-‘03

$1.3 Billion Average ‘09-‘16

Cyclical Trough to Cyclical Trough

Fixed Income Presentation | March 2017

4

14

• Only North American steel producer with an investment grade credit rating; Baa1/A- (Stable Outlook)

• Weighted Average Fixed Coupon: 5.3%; Weighted Average Time to Maturity: 12.6 years

• Strong liquidity position of ~$3.7bn supported by $1.5bn revolving credit facility (undrawn); target liquidity of $2.5bn

• Operated with average cash balance of $1.5bn (2000-2016); YE 2016 ~$2.2bn

$500

5.20% Senior Note due

8/1/43

4.125% Senior Note due 9/15/22

6.40% Senior Note due 12/1/37

5.85% Senior Note due

6/1/18

5.75% Senior Note due 12/1/17 4.00% Senior

Note due 8/1/23

IRB Debt

Strong Liquidity Position

$20 $1

$337

$28 $25

$600 $600

$500

$600

$500

$650

$500

2017 2018 2019 2020 2021 2022 2023 2037 2038 2040 2043

Fixed Income Presentation | March 2017

Source: Company Filings

4

15

Long Term Commitment to IG Rating

Nucor’s Net Debt, EBITDA and Leverage since 2009

Note: EBITDA calculated as Earnings before Income Taxes and Noncontrolling Interests plus Net Interest Expense plus Depreciation and Amortization. Net debt calculated as Short Term Debt plus Long Term Debt minus Cash, Cash Equivalents, Restricted Cash, and Short Term Investments. See Appendix for Reconciliation Source: Company Filings

Fixed Income Presentation | March 2017

5

846

1,216 1,133

2,205

2,869

3,434

2,349 2,161

-

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2009 2010 2011 2012 2013 2014 2015 2016

Net D

ebt / E

BIT

DA

(x)

US

$m

m

Net Debt EBITDA Net Debt / EBITDA

Successful deleveraging

16

3.6x 3.2x 3.1x

2.2x 1.6x

1.3x 1.0x

-

1.0x

2.0x

3.0x

4.0x

5.0x

AK Steel US Steel Gerdau CommercialMetals

Company

ArcelorMittal

SteelDynamics

Nucor

Net Debt 2016A / EBITDA 2016A

Lowest Sector Leverage

Note: EBITDA calculated as Earnings before Income Taxes and Noncontrolling Interests plus Net Interest Expense plus Depreciation and Amortization adjusted for Impairment and restructuring charges. Net debt calculated as Short Term Debt plus Long Term Debt minus Cash, Cash Equivalents, Restricted Cash, and Short Term Investments. See Appendix for Reconciliation Source: Company Filings

Fixed Income Presentation | March 2017

5

17

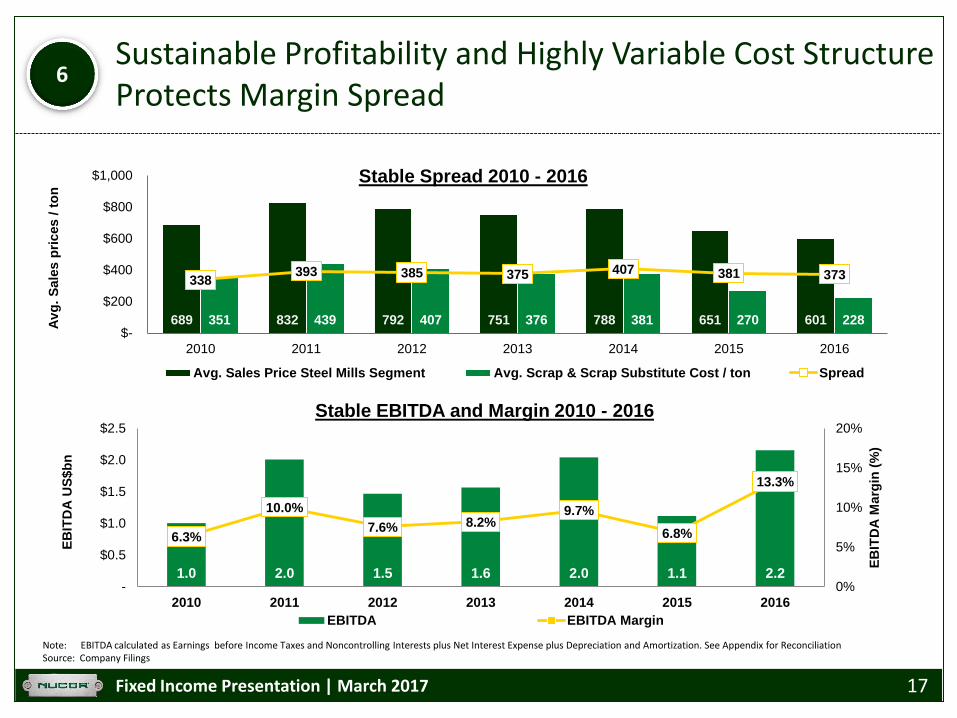

Sustainable Profitability and Highly Variable Cost Structure Protects Margin Spread

Note: EBITDA calculated as Earnings before Income Taxes and Noncontrolling Interests plus Net Interest Expense plus Depreciation and Amortization. See Appendix for Reconciliation Source: Company Filings

1.0 2.0 1.5 1.6 2.0 1.1 2.2

6.3%

10.0%

7.6% 8.2% 9.7%

6.8%

13.3%

0%

5%

10%

15%

20%

-

$0.5

$1.0

$1.5

$2.0

$2.5

2010 2011 2012 2013 2014 2015 2016

EB

ITD

A M

arg

in (

%)

EB

ITD

A U

S$b

n

Stable EBITDA and Margin 2010 - 2016

EBITDA EBITDA Margin

689 832 792 751 788 651 601 351 439 407 376 381 270 228

338 393 385 375 407 381 373

$-

$200

$400

$600

$800

$1,000

2010 2011 2012 2013 2014 2015 2016

Av

g.

Sale

s p

rices /

to

n Stable Spread 2010 - 2016

Avg. Sales Price Steel Mills Segment Avg. Scrap & Scrap Substitute Cost / ton Spread

Fixed Income Presentation | March 2017

6

18

Recent Strategic Investments

Strategic Investments Completion/ Startup

$ Spent (millions)

Nucor Steel Berkeley sheet mill adding 7th mill to produce wider and lighter hot rolled

Q1 2014 $98

Gallatin Steel acquisition adds ~1.6 million tons of flat-rolled capacity and increases Nucor’s total flat-rolled capacity to ~12 million tons annually

Q4 2014 $770

Nucor-Yamato expansion of sheet piling product to wider sizes 2014 $115

SBQ & Wire Rod expansion into higher value-added product at Tennessee, Nebraska & South Carolina mills (Combined annual capacity increase of 1 million tons)

2015 $290

Nucor-Yamato Quench & Self-Temper (QST) process for high-strength, low-alloy beams

Q3 2016 $75

Longview, TX plate mill acquisition adds 125,000 tons of higher value-added carbon and alloy plate products

Q3 2016 $29

Tubular Products acquisitions adds ~1 million tons of tubular product shipments (hollow structural section tubing and electrical conduit)

Q4 2016 / Q1 2017 $900

Nucor Steel Arkansas Cold Mill Complex expansion adds 500,000 tons capacity to produce advanced high-strength, high strength low-alloy, and motor lamination steel products

Q1 2019 $230

Low Risk & High Return

Fixed Income Presentation | March 2017

7

19

Expanding Channels to Market

8%

16%

20%

0%

5%

10%

15%

20%

25%

2006 2016 2017 pro forma

Downstream Steel Usage

Fixed Income Presentation | March 2017

7

20

27.0% 26.6%32.3%

22.5%18.5%

(1.7%)

2.4%7.8%

4.8% 5.0% 6.9%2.3%

7.8%

(5%)

5%

15%

25%

35%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

RO

IC

Return on Invested Capital Performance

Source: Company Filings; ROIC = EBIT(1-.35)/(Total Debt + Equity). See Appendix for Reconciliation

Up-Cycle

“Great Recession”

2.3% 4.2%

7.2% 7.2% 7.9% 10.4%

12.5%

-

5%

10%

15%

AK Steel U.S. Steel Gerdau Arcelor Mittal CMC Steel Dynamics Nucor

RO

IC

Average ROIC 2004 - 2016

Fixed Income Presentation | March 2017

7

21

II. Financial Results

22

Fiscal Year Results Summary

Note: EBITDA calculated as Earnings before Income Taxes and Noncontrolling Interests plus Net Interest Expense plus Depreciation and Amortization. Net debt calculated as Short Term Debt plus Long Term Debt minus Cash, Cash Equivalents, Restricted Cash, and Short Term Investments. See Appendix for Reconciliation Source: Company Filings

Fixed Income Presentation | March 2017

Key Metric Units 2012 2013 2014 2015 2016

Volume Sold Million tons 23.1 23.7 25.4 22.7 24.3

Sales US$ billion $19.4 $19.1 $21.1 $16.4 $16.2

EBITDA US$ billion $1.5 $1.6 $2.0 $1.1 $2.2

EBITDA Margin % 7.6% 8.2% 9.7% 6.8% 13.3%

Cash from Operations US$ billion $1.2 $1.1 $1.3 $2.2 $1.7

Net Debt US$ billion $2.2 $2.9 $3.4 $2.3 $2.2

Net Debt / EBITDA (x) 1.5x 1.8x 1.7x 2.1x 1.0x

23

Financial History

Source: Company Filings Note: EBITDA calculated as Earnings before Income Taxes and Noncontrolling Interests plus Net Interest Expense plus Depreciation and Amortization. Net debt calculated as Short Term Debt plus Long Term Debt minus Cash, Cash Equivalents, Restricted Cash, and Short Term Investments. See Appendix for Reconciliation

Sales (US$ billion) Net Debt / EBITDA

Cash from Operations (US$ billion) Debt to Capital

4.6 4.3 4.8 6.3

11.4 12.7

14.8 16.6

23.7

11.2

15.8

20.0 19.4 19.1 21.1

16.4 16.2

$-

$5

$10

$15

$20

$25

$30

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

0.8

0.5 0.5 0.5

1.0

2.1 2.3

1.9

2.5

1.2

0.9 1.0 1.2 1.1

1.3

2.2

1.7

-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

16% 16%

26% 26% 20%

17% 15%

30% 28% 29%

37% 36% 30%

34% 34% 36% 35%

0%

10%

20%

30%

40%

50%

60%

70%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Debt / Capital Debt / Capital Limit

Fixed Income Presentation | March 2017

0.0

0.0

1.2 1.2

0.1

-0.4 -0.4

0.3 0.3

3.7

1.2

0.6

1.5 1.8 1.7

2.1

1.0

(1.00)x

-

1.00x

2.00x

3.00x

4.00x

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Questions

24

Appendix

25

26

EBITDA and Net Debt Reconciliation

Note: EBITDA calculated as Earnings before income taxes and non-controlling interests plus Net interest expense plus Depreciation and Amortization. Net debt calculated as Short Term Debt plus Long Term Debt minus Cash, Cash Equivalents, Restricted Cash, and Short Term Investments. Source: Company Filings

Fixed Income Presentation | March 2017

$ in millions 2010 2011 2012 2013 2014 2015 2016

Earnings Before Taxes and

Noncontrolling Interests 267$ 1,252$ 697$ 809$ 1,147$ 242$ 1,299$

Net Interest 153 166 162 147 169 174 169

Depreciation 512 523 534 536 652 626 613

Amortization 70 68 73 74 72 74 74

EBITDA 1,003$ 2,008$ 1,466$ 1,566$ 2,041$ 1,115$ 2,155$

$ in millions 2010 2011 2012 2013 2014 2015 2016

Short Term Debt 13$ 2$ 30$ 29$ 207$ 51$ 18$

Long Term Debt (incl. current maturities) 4,280 4,280 3,607 4,351 4,351 4,337 4,339

Total Debt 4,294 4,282 3,637 4,380 4,558 4,388 4,357

Less: Cash & ST Investments 2,479 2,563 1,157 1,511 1,124 2,039 2,196

Less: Restricted Cash 599 586 275 - - - -

Net Debt 1,216$ 1,133$ 2,205$ 2,869$ 3,434$ 2,349$ 2,161$

Fiscal Year Ended December 31,

27

Nucor ROIC Reconciliation

Note: ROIC Calculated as EBIT (1-.35) / (Total Debt + Equity) Source: Company Filings

Fixed Income Presentation | March 2017

Nucor 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2004-

2016

AVG

EBIT 1,829,083 2,141,934 2,874,191 2,552,285 3,194,874 (279,226) 420,208 1,417,906 859,379 955,463 1,316,544 415,397 1,467,903

NOPAT 1,188,904 1,392,257 1,868,224 1,658,985 2,076,668 (181,497) 273,135 921,639 558,596 621,051 855,754 270,008 954,137

Total Debt 923,550 923,550 922,300 2,250,300 3,266,600 3,086,200 4,280,200 4,280,200 3,607,156 4,350,902 4,350,558 4,337,145 4,357,100

Equity 3,481,281 4,312,049 4,857,351 5,112,917 7,929,204 7,390,526 7,120,070 7,474,885 8,002,692 8,018,250 8,110,342 7,477,816 7,879,865

Total Capital 4,404,831 5,235,599 5,779,651 7,363,217 11,195,804 10,476,726 11,400,270 11,755,085 11,609,848 12,369,152 12,460,900 11,814,961 12,236,965

ROIC 27.0% 26.6% 32.3% 22.5% 18.5% -1.7% 2.4% 7.8% 4.8% 5.0% 6.9% 2.3% 7.8% 12.5%