Flood Insurance in The Netherlands Ministerie van Verkeer en Waterstaat Dutch Ministry of Transport, Public Works and Water Management Directorate General Water drs. Martijn van de Groep Projectmanager Flood Insurance ECWATECH 4 june 2008

Transcript

Flood Insurance in

The Netherlands

Ministerie van Verkeer en Waterstaat

Dutch Ministry of Transport, Public Works and Water Management

Directorate General Water

drs. Martijn van de Groep

Projectmanager Flood Insurance

ECWATECH 4 june 2008

Contents

Background (1953 – 2005)

Recent developments (1990 – 2008)

Flood Insurance project (2006 – 2008)

Questions and discussion

1953

1835 casulaties; 72.000 people evacuated;financial losses approx. € 6 billion;

flooded area approx. 2000 km2

Flood insurance after the 1953 flood disaster

After 1953 floodings, damage as a result of flood perils was excluded from regular insurance policies:

- since 1956 ‘Obligatory Decree on Floodings’

- since abolishment of exclusion in 1990, no private insurance solution was developed for the Dutch market

Ministerie van Verkeer en Waterstaat

Cabinet proposal 1995 after floodings Rine (1993) and Meuse (1995) and earthquake Roermond (1992)

Cabinet proposal (1995): ‘Compensation Act for floodings (rivers only) and earthquakes’

Council of State negative recommendations lead to withdrawal of proposal main arguments:

- Constitutional state responsibility to provide for compensation (art 21)

- Solidarity

- Flood protection measures (structural works along rivers) will increase chances of private flood insurance initiatives

Ministerie van Verkeer en Waterstaat

State Compensation Act (1998)

Loss compensation for flood disasters Event-based limitation (2008: max € 500 mln)

Ministerie van Verkeer en Waterstaat

Assessment by independent review committee (2005)

Third party liability is primary mechanism for loss compensation In case of natural disaster (no provoker):

- citizenz are responsible for private insurance (when available)- government role to enhance insurability (if not available)

State Compensation Act remains safety net

Advisory Committee Water (2005/2006)

Chairman: His Royal Highness Prince of Orange expert debate in november 2005

conclusion: all involved parties affirmative on shared responsibility with regard to disaster losses due to floodings

recommendation to set up a hybrid private-public partnership in whichcitizens, business, regional governments/water communities, (re)insurers, capital market parties and state government each provide for a substantial contribution to loss compensation in case of severe floodings

Ministerie van Verkeer en Waterstaat

Cabinet proposal (june 2006)

Basic assumptions: Stimulate private initiatives Enhance own responsibility of citizens

Cornerstones: Third party liability Insurance

- draft of step-by-step plan to set-up private-public partnership- focus on social, political and economical endurance

- challenging and complex (2-5 years for implementation) Compensation Act as safety net of last resort

Ministerie van Verkeer en Waterstaat

Project Flood Insurance (start june 2006)

Pilotproject resulting from ACW recommendations and cabinet proposal

Task Force coördinated by ministry of Finance:

Ministerie van Verkeer en Waterstaat

- Ministery of Finance- Ministery of Transport, Public Works and Water Management- Ministery of Interior and Kingdom Relations- Dutch Association of Insurers

Association of Water Boards :

- executive management decision not to participate in Task Force- positive attitude towards introduction of flood insurance- available for expert consultation

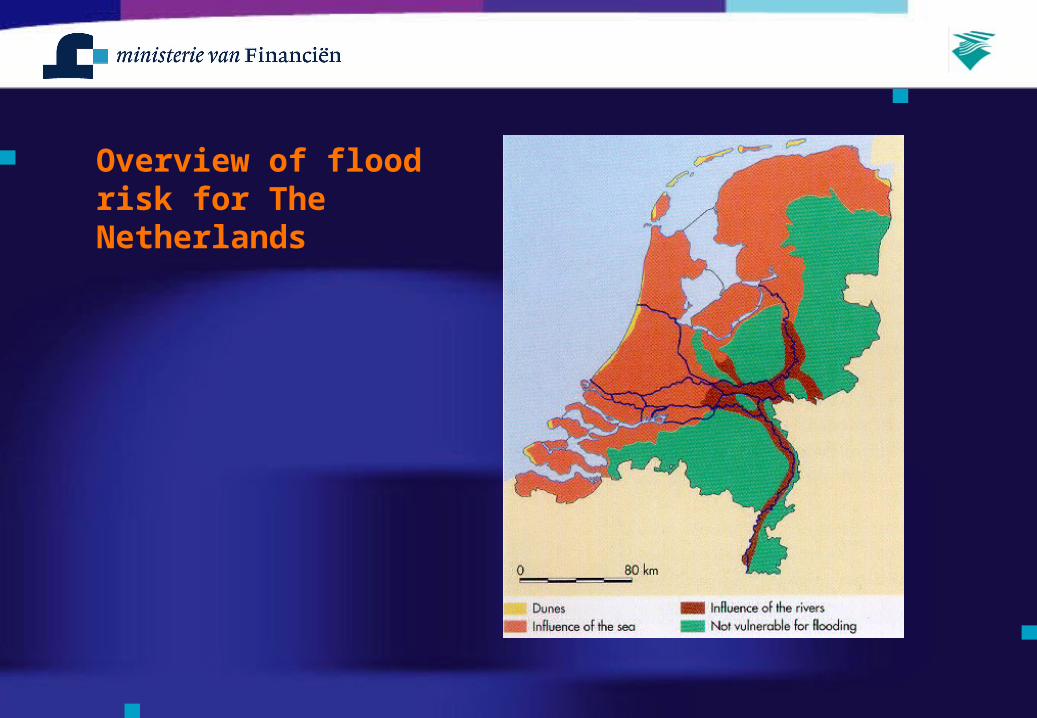

Overview of flood risk for The Netherlands

Objectives and scope:

Objectives:

The project’s primairy objective is to enhance the private insurability of the flood risk in The Netherlands

Ministerie van Verkeer en Waterstaat

Scope: 4, 5, 6, 7

Flood insurance: overview of possible bottlenecks

the volume of the risk collective for the flood peril (antiselection)

the ability to assess risks within a reasonable accuracy (information/risk modelling)

the high maximum possible loss (insurers market solvabilitity)

reinsurance capacity

economic viability (adequate premiums)

Ministerie van Verkeer en Waterstaat

Until recently, the Dutch Association of Insurers valued the flood risk as a “low probability, high consequences” risk, which is technically not insurable due to the following characteristics:

Flood insurance: technical solution

Ministerie van Verkeer en Waterstaat

Retention by individual insurance companies

Insurance pool

Re-insurance

Government layer(directorate general water)

Government (ministry of finance)

20%

€ 300 million

€ 300 million

€ 500 million

€ 400 million

Deductibles by individual household and private companies

Flood insurance: technical solution

Legal obligation for insurers to offer flood loss compensation in household policies (fire insurance policy).

‘Hybrid’ structure: private sector based model with government participation only where necessary to complement the construction;

Layerstructure with loss compensation limit set to € 1,5 billion per event with re-instatement for 2nd event within 1 year. No guarantee for state compensation beyond limit. Vertical government layer 20% to reduce moral political risk

Risk related premium accounting with estimated average premium < € 15 (annually) for individual household

For discussion: possibility of fiscal reserve for national insurance companies combined with gradual raise in compensation limit.

Ministerie van Verkeer en Waterstaat

Flood insurance versus State Compensation Act:

Advantages:- legal right to loss compensation (security)- reduction of indirect losses (payment procedure)- ‘consumption smoothing’ (risk premium spreading)- premium based on economical value and exposed actual risks

Disadvantages:- premium based on costs + shareholder profit target (price)- possibility of liability conflict between government and insurers- failing willingness to pay due to low risk perception

Flood insurance: further procedure

Mid 2008: decision making within Dutch cabinet

If Dutch cabinet decides for pubic-private insurance solution:- implementation (adjustment of household policies) per 1 january 2010