51

Australian Worldwide Exploration www.awexp.com.au August/September 2007 For personal use only

Australian Worldwide Exploration

www.awexp.com.au

August/September 2007

For

per

sona

l use

onl

y

overviewfinancial summarycornerstone projects a year of deliveryfuture outlook

For

per

sona

l use

onl

y

Overview

For

per

sona

l use

onl

y

Overview of AWE ASX200 E&P operating company

market cap. = A$1,410m (@ $3.15 per share)

reserves = 56 mmboe (2P)

strong financial position

4 cornerstone projects in production

captured growth potential

exploration :- NZ, Indonesia and Australia

future growth options

For

per

sona

l use

onl

y

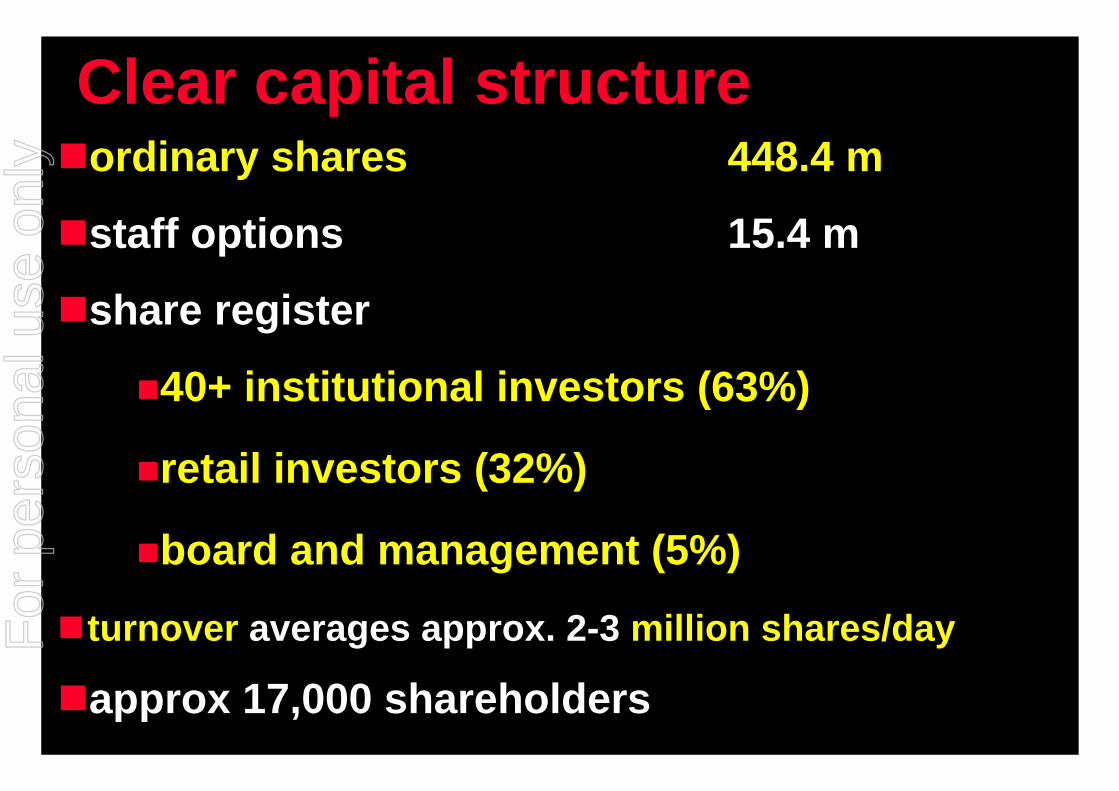

Clear capital structureordinary shares 448.4 m

staff options 15.4 m

share register

40+ institutional investors (63%)

retail investors (32%)

board and management (5%)

turnover averages approx. 2-3 million shares/day

approx 17,000 shareholders

For

per

sona

l use

onl

y

Bruce Wood Managing Director (32 years experience)

Leigh Brooks Exploration Manager (33 years)

Rick Frith Engineering & Prod Manager (33 years)

Neville Kelly CFO and Co. Sec (25 years)

Garry Marsden Corporate Development (25 years)

Ian Palmer NZ Development Manager (26 years)

Eric Matthews NZ Exploration Manager (33 years)

Elliot Yearsley Indonesian Country Manager (25 years)

Dennis Washer NZ Country Manager (28 years)

strong background in global oil & gas operations :-

exploration, development, production and acquisitions.

Experienced management teamF

or p

erso

nal u

se o

nly

...... but E&P is a global game. AWE will grow globally in the medium term, but this will be done with rigor & focus

To date AWE has grown with a strong Australasian focusF

or p

erso

nal u

se o

nly

10 years of growth

Since IPO: Grown business >50 fold; Increased share price >6 fold; 20% annualised TSR since listing

For

per

sona

l use

onl

y

2006-07

a year of delivery

For

per

sona

l use

onl

y

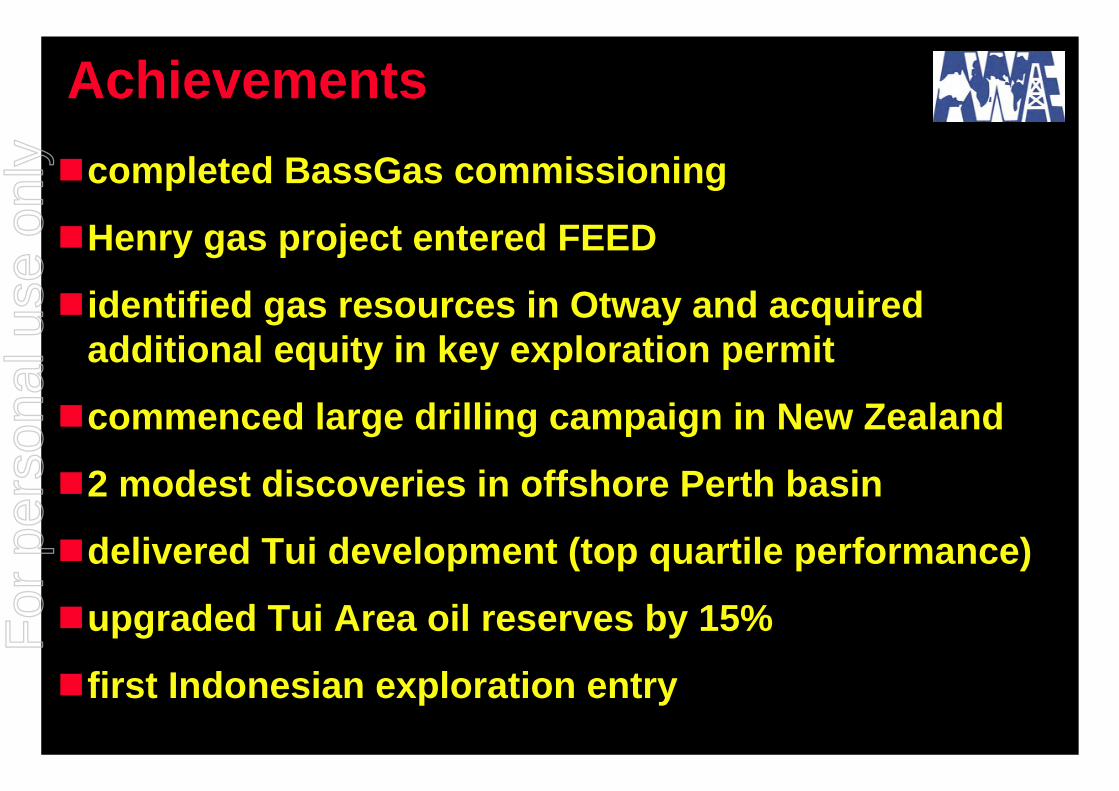

Achievementscompleted BassGas commissioning

Henry gas project entered FEED

identified gas resources in Otway and acquired additional equity in key exploration permit

commenced large drilling campaign in New Zealand

2 modest discoveries in offshore Perth basin

delivered Tui development (top quartile performance)

upgraded Tui Area oil reserves by 15%

first Indonesian exploration entry

For

per

sona

l use

onl

y

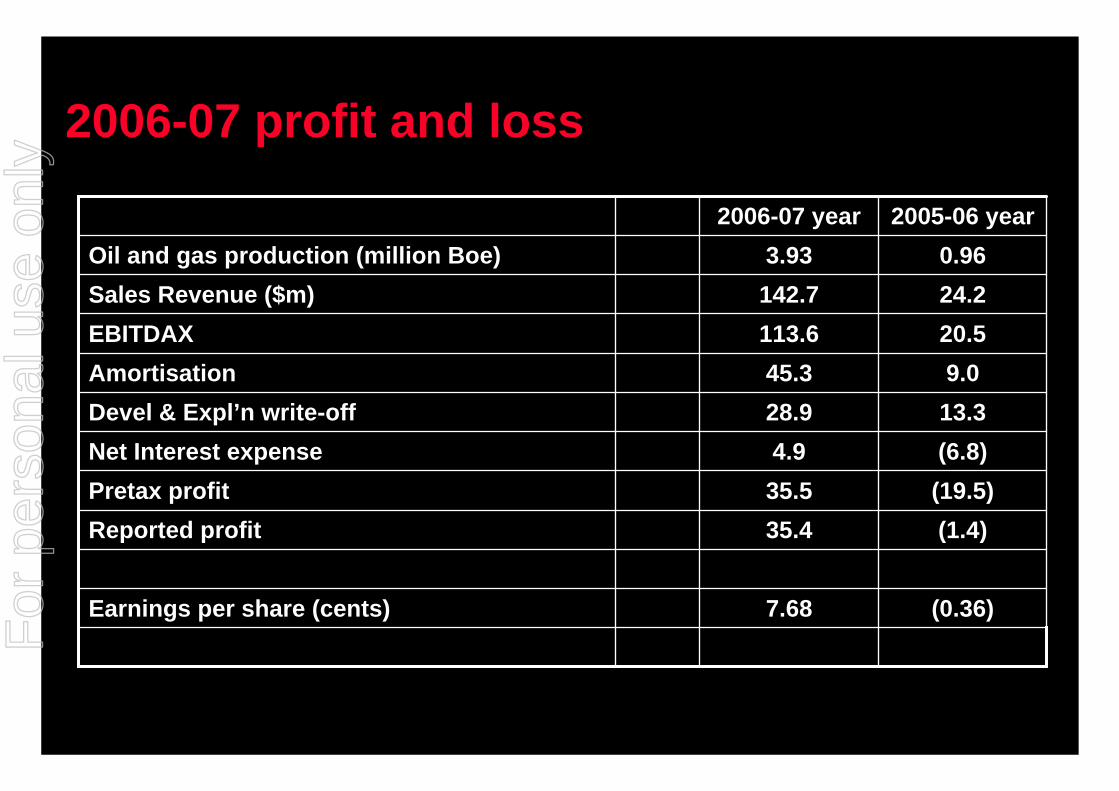

2006-07 profit and loss

(0.36)7.68Earnings per share (cents)

(1.4)35.4Reported profit(19.5)35.5Pretax profit(6.8)4.9Net Interest expense13.328.9Devel & Expl’n write-off9.045.3Amortisation

20.5113.6EBITDAX24.2142.7Sales Revenue ($m)0.963.93Oil and gas production (million Boe)

2005-06 year2006-07 year

For

per

sona

l use

onl

y

Production TargetF

or p

erso

nal u

se o

nly

Numbers may not add due to rounding

2006-07 net profit components

Numbers may not add due to rounding

For

per

sona

l use

onl

y

Numbers may not add due to rounding

2006-07 cash flow summary

Numbers may not add due to rounding

Numbers may not add due to rounding

For

per

sona

l use

onl

y

Cornerstoneprojects

For

per

sona

l use

onl

y

Yolla field performing at design capacity

2007/8 EBITDAX target A$35 million (WTI @ US$60/Bbl)

growth potential (Oil price; Reserve additions at Yolla; Trefoil field tie-in; Expl’n success)

Trefoil and Rockhopper/Gentoo projects under commercial studies

BassGas project (AWE 30%)F

or p

erso

nal u

se o

nly

BassGas Project (AWE 30%) F

or p

erso

nal u

se o

nly

Casino project (AWE 25%)

initial contract 96 TJ/day (additional 44 TJ/day contracted until Q3, 2007)

successful development and strong field performance

Henry Feed nearing completion

Casino 2007/8 EBITDAX target = A$29 million

Pecten East-1 and Netherby-1 planned for early 2008F

or p

erso

nal u

se o

nly

otway basin Vic P44 (AWE 25%)..excellent exploration

Henry 160 PJ

Casino 285 PJ

Pecten East

MarthaNetherby

For

per

sona

l use

onl

y

Perth Basin (AWE 27.5%)F

or p

erso

nal u

se o

nly

Cliff Head project (AWE 27.5%)field performing well, oil production now >10,000 bopdpump and scaling problems solved 4 million barrels of oil produced to date2007/8 EBITDAX target = $48 million (WTI @ US$60/Bbl)2 modest discoveries in 2007. Both under commercial review

For

per

sona

l use

onl

y

Tui Area oil project,

DELIVERED

20 months from FID to first oil

For

per

sona

l use

onl

y

AWE’s Taranaki Basin Acreage F

or p

erso

nal u

se o

nly

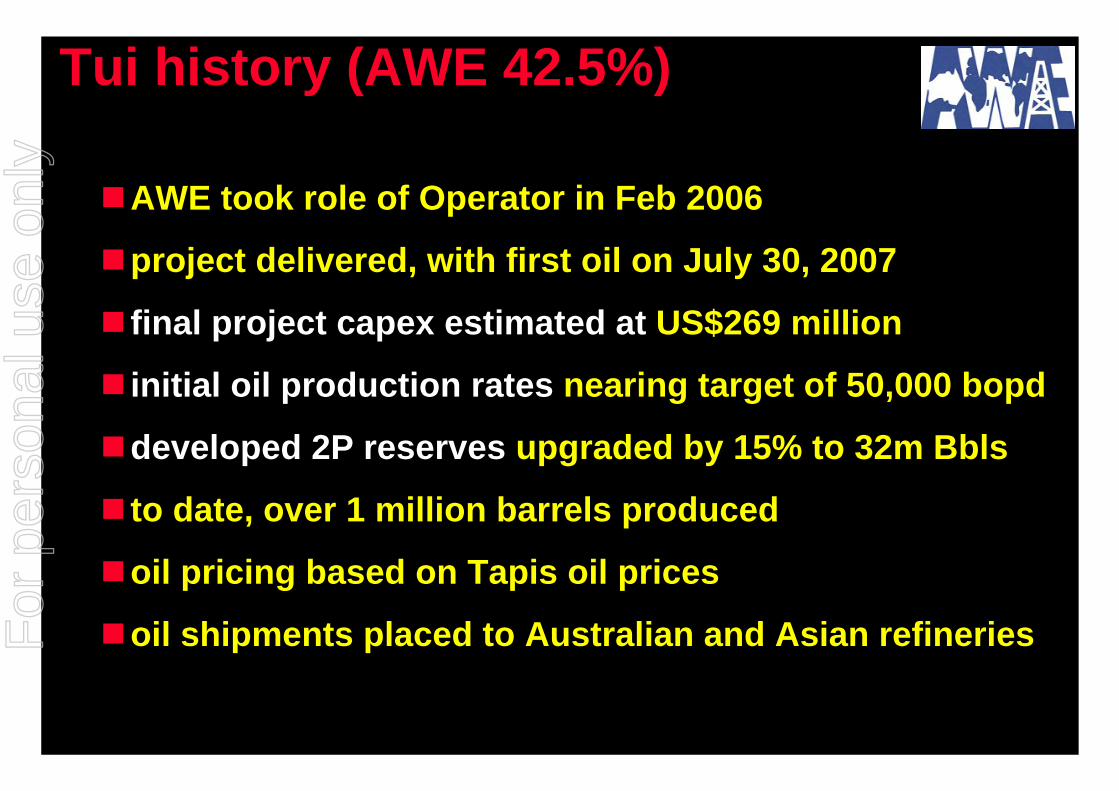

Tui history (AWE 42.5%)

AWE took role of Operator in Feb 2006

project delivered, with first oil on July 30, 2007

final project capex estimated at US$269 million

initial oil production rates nearing target of 50,000 bopd

developed 2P reserves upgraded by 15% to 32m Bbls

to date, over 1 million barrels produced

oil pricing based on Tapis oil prices

oil shipments placed to Australian and Asian refineriesFor

per

sona

l use

onl

y

Mid water arches

FPSO Umuroa

Sub sea well head and tree

Flowlines and Umbilicals

Mooring lines

Tui development

For

per

sona

l use

onl

y

FPSO in SingaporeF

or p

erso

nal u

se o

nly

Normand Installer vesselF

or p

erso

nal u

se o

nly

Installation of mid water arches F

or p

erso

nal u

se o

nly

FPSO in New PlymouthF

or p

erso

nal u

se o

nly

FPSO mooring at TuiF

or p

erso

nal u

se o

nly

First oil transfer from FPSO to AkamaF

or p

erso

nal u

se o

nly

Akama discharging in SydneyF

or p

erso

nal u

se o

nly

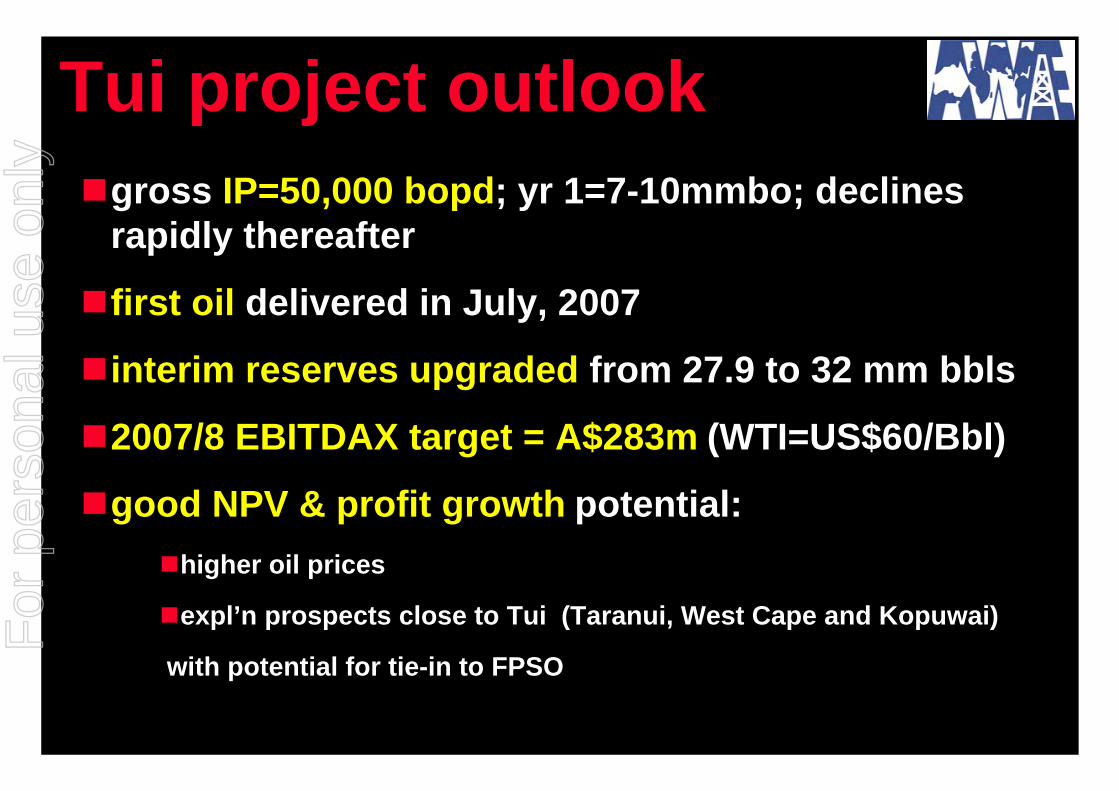

Tui project outlookgross IP=50,000 bopd; yr 1=7-10mmbo; declines rapidly thereafter

first oil delivered in July, 2007

interim reserves upgraded from 27.9 to 32 mm bbls

2007/8 EBITDAX target = A$283m (WTI=US$60/Bbl)

good NPV & profit growth potential:higher oil prices

expl’n prospects close to Tui (Taranui, West Cape and Kopuwai)

with potential for tie-in to FPSO

For

per

sona

l use

onl

y

How we do itretain the best people

provide a great work environment

stay nimble (no paralysis by analysis)

AWE as the JV partner of choice

team focus with single point accountability

positive board and management interaction

transparent communications with shareholders & broader community e.g. unaudited resultsF

or p

erso

nal u

se o

nly

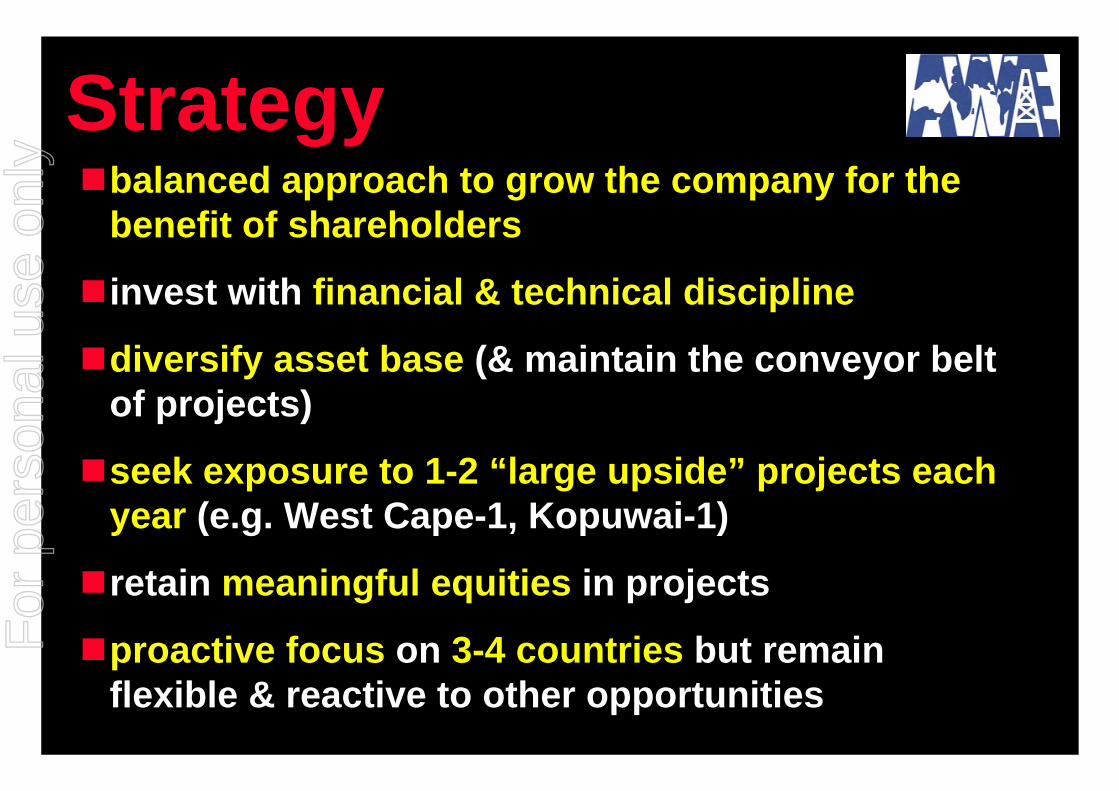

Strategybalanced approach to grow the company for the benefit of shareholders

invest with financial & technical discipline

diversify asset base (& maintain the conveyor belt of projects)

seek exposure to 1-2 “large upside” projects each year (e.g. West Cape-1, Kopuwai-1)

retain meaningful equities in projects

proactive focus on 3-4 countries but remain flexible & reactive to other opportunities

For

per

sona

l use

onl

y

FutureOutlook

For

per

sona

l use

onl

y

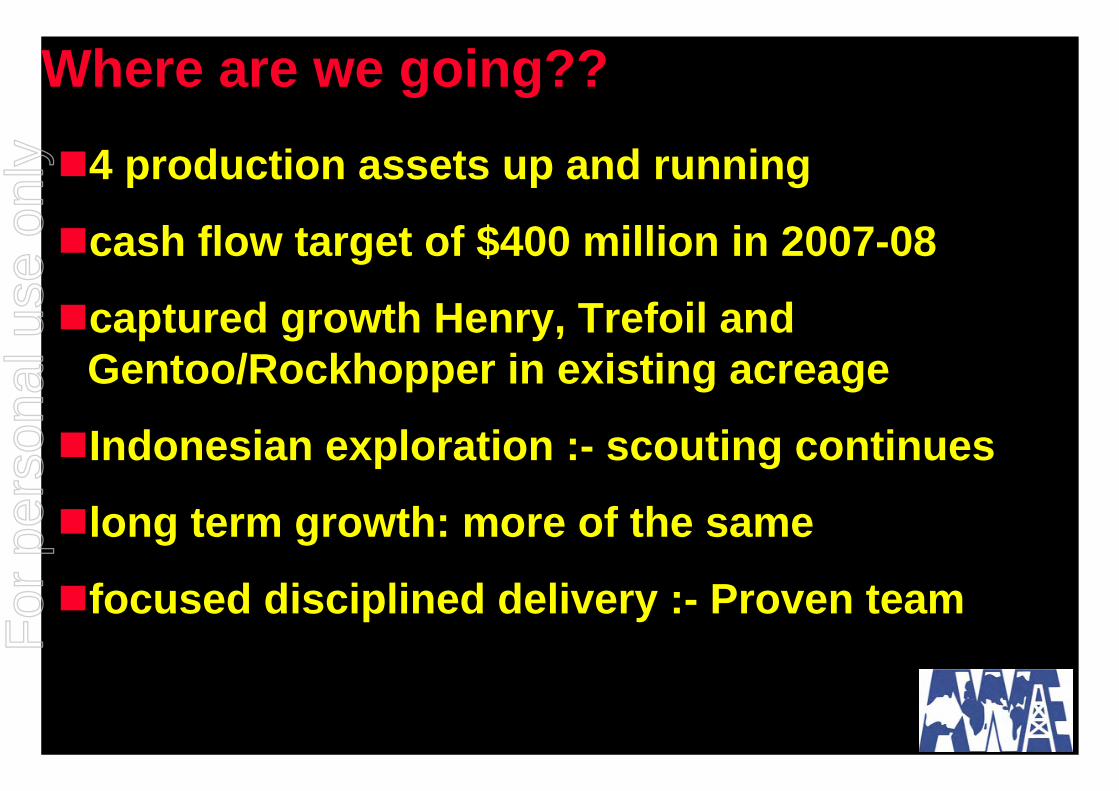

Where are we going??

4 production assets up and running

cash flow target of $400 million in 2007-08

captured growth Henry, Trefoil and Gentoo/Rockhopper in existing acreage

Indonesian exploration :- scouting continues

long term growth: more of the same

focused disciplined delivery :- Proven team

For

per

sona

l use

onl

y

ExplorationOutlook

For

per

sona

l use

onl

y

Prospect Permit Equity Size AWE Cost Timing

(%) (gross) (A$mm)

Taranui-1 PMP 38158 42.5 5-15 mmbo 8.0 currentLisah-1 Bulu PSC 42.5 7.0 Q3-07Lengo-1 Bulu PSC 42.5 7.0 Q3-07West Cape-1 PEP 38481 40.0 >100 mmbo 11.0 Q3-07Kopuwai-1 PEP38482 50.0 >100 mmbo nil Q4-07Henry-2 VIC/P 44 25.0 dev’t early 2008Netherby-1 VIC/P 44 25.0 110 bcf 4.5 early 2008Pecten East-1 VIC/P 44 25.0 160 bcf 4.5 early 2008

A$42m

Upcoming drilling programSeptember 2007

Forward exploration drilling cost is approx. 10cps, but exposing shareholders to dollars per share upside

AWE’s historical commercial success rate is >20%

For

per

sona

l use

onl

y

Good follow-up potential for large prospects (20 to >100 mmb oil)

Update on Taranaki explorationF

or p

erso

nal u

se o

nly

18 km

Tui area FieldsTaranui

Prospect

OiProspect

For

per

sona

l use

onl

y

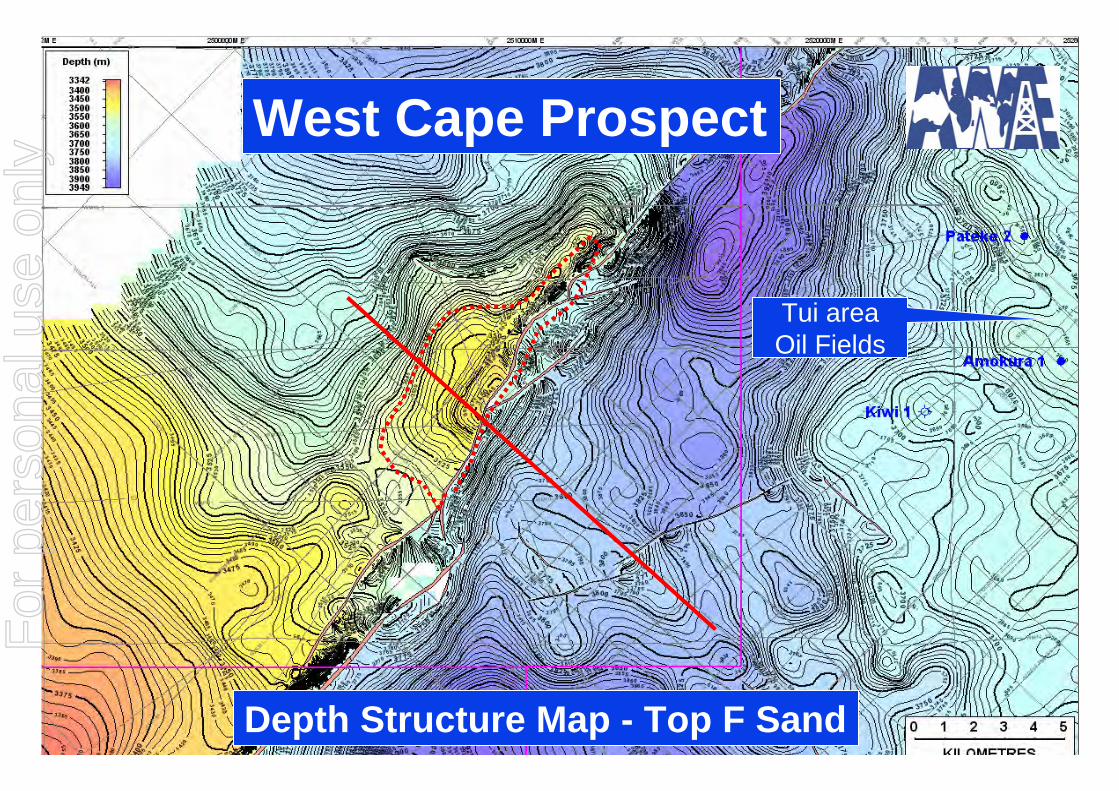

Depth Structure Map - Top F Sand

West Cape Prospect

Tui area Oil Fields

For

per

sona

l use

onl

y

F Sand

West Cape prospect – dip line3 km

For

per

sona

l use

onl

y

Indonesian area of explorationF

or p

erso

nal u

se o

nly

Netherby & Pecten East prospects, Otway basin (AWE 25%)

Henry 160 PJ

Casino 285 PJ

Pecten East

MarthaNetherby

For

per

sona

l use

onl

y

Targets

For

per

sona

l use

onl

y

Production growth targetF

or p

erso

nal u

se o

nly

Cashflow growth target

Long term cashflow target > $130 million per annum

For

per

sona

l use

onl

y

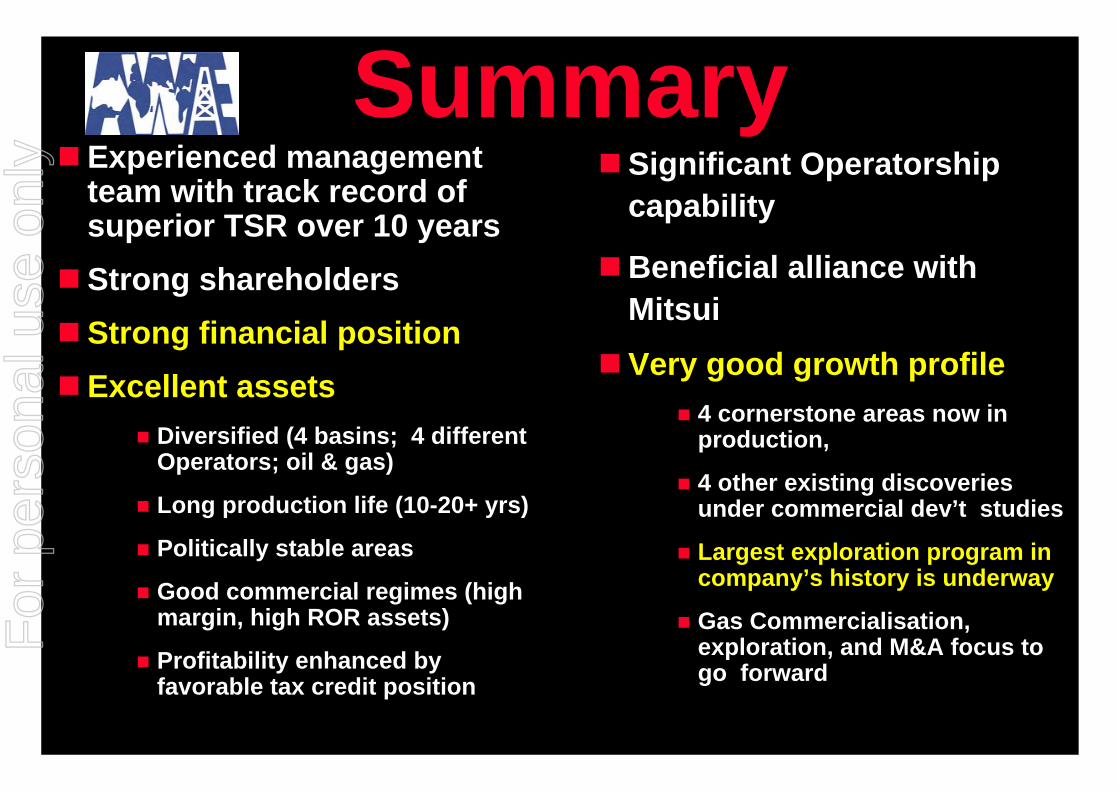

SummaryExperienced management team with track record of superior TSR over 10 yearsStrong shareholdersStrong financial positionExcellent assets

Diversified (4 basins; 4 different Operators; oil & gas)

Long production life (10-20+ yrs)

Politically stable areas

Good commercial regimes (high margin, high ROR assets)

Profitability enhanced by favorable tax credit position

Significant Operatorship capability

Beneficial alliance with MitsuiVery good growth profile

4 cornerstone areas now in production,

4 other existing discoveries under commercial dev’t studies

Largest exploration program in company’s history is underway

Gas Commercialisation, exploration, and M&A focus to go forward

For

per

sona

l use

onl

y

Disclaimer

This presentation may contain forward looking statements that are subject to risk factors associated with oil and gas businesses. It is believed that the expectations reflected in these statements arereasonable but they may be affected by a variety of variables and changes in underlying assumptions which could cause actual results or trends to differ materially, including but not limited to: price fluctuations, actual demand, currency fluctuations, drilling andproduction results, reserve estimates, loss of market, industry competition, environmental risks, physical risks, legislative, fiscal and regulatory developments, economic and financial market conditions in various countries and regions, political risks, project delay or advancement, approvals and cost estimates.

All references to dollars, cents or $ in this presentation are to Australian currency, unless otherwise stated.

For

per

sona

l use

onl

y

Australian Worldwide Exploration

www.awexp.com.au

August/September 2007

For

per

sona

l use

onl

y