42

Forms of Business Organization

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | jaysonfredmarin |

| View: | 3 times |

| Download: | 1 times |

Forms of Business Organization

Sole Proprietorship

Its owner operates it for his or her own profit

Must apply for a Business Name and be registered with the Department of Trade and Industry (DTI)

Sole Proprietorship

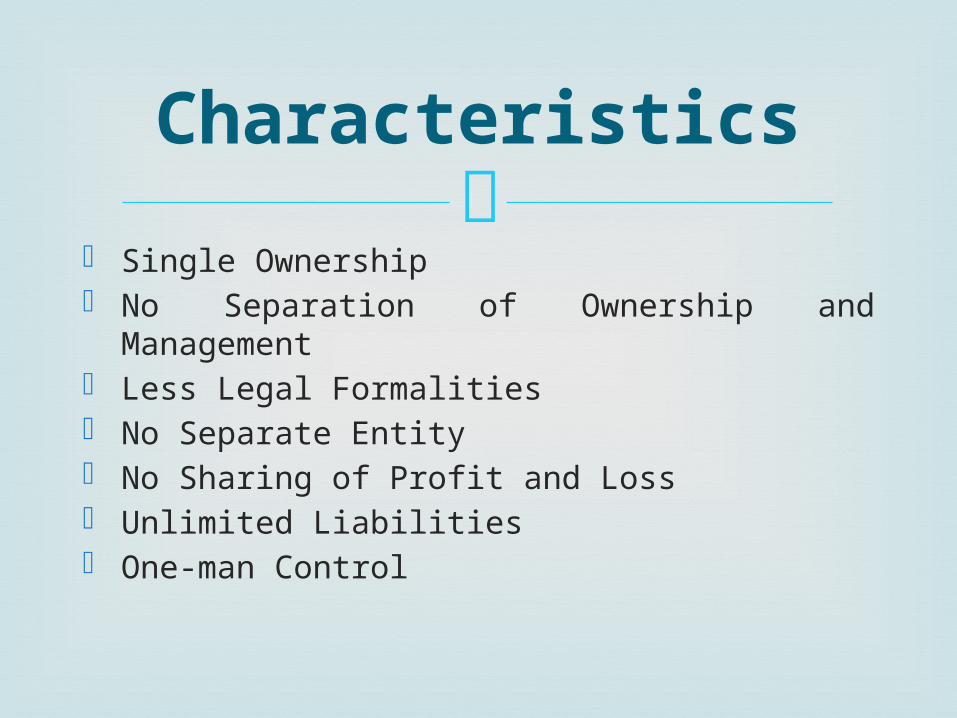

Single Ownership No Separation of Ownership and Management Less Legal Formalities No Separate Entity No Sharing of Profit and Loss Unlimited Liabilities One-man Control

Characteristics

Owner receives all profits Low organizational costs Income included and taxed on proprietor’s

personal tax return Independence Ease of Dissolution

Strengths

Owner has unlimited liability Limited fund-raising power tends to inhibit

growth Proprietor must be a jack-of-all-trades Difficult to give employees long-run career

opportunities Lack of continuity when proprietor dies

Weaknesses

Partnership

Under the Civil Code of the Philippines, by the

contract of partnership, two or more person bind themselves to contribute money, property or industry to a common fun, with the intention of dividing the profits among themselves

A contract of partnership having a capital of three thousand pesos (Php 3,000.00) or more, in money or property, must register with the Securities and Exchange Commission (SEC)

Partnership

Two or More Persons Contractual Relationship Sharing of profits of business Existence of Lawful Business Participant Agent Relationship Unlimited Liabilities

Characteristics

Can raise more funds than sole proprietorship Borrowing power enhanced by more owners More available brain power and managerial

skill Income included and taxed on partner’s tax

return

Strengths

Owners have unlimited liabilities Partnership is dissolved when a partner dies Difficult to liquidate or transfer partnership

Weaknesses

Kinds of Partners

Capitalist Partner Industrial Partner General Partner Limited Partner Managing Partner Liquidating Partner Partners by Estoppel

Continuing Partner Surviving Partner Sub partner Ostensible Partner Secret Partner Silent Partner Dormant Partner

Partnership at will

Indefinite Period Existence after Completion of Venture Existence after Expiry Period

Particular Partnership Limited Partnership

Kinds of Partnership

Without violating the agreement Violation of the agreement Loss Death of any partners Insolvency of any partner or of the partnership Civil Interdiction of any partner By the decree of court under Art. 1831, NCC

Causes of Dissolution

Partnership is not terminated Partnership continues for a limited purposes Transaction of a new business is prohibited

Effects of Dissolution

Time of Termination No part of any business, financial operation

or venture is carried on by the partners in a partnership, or

Within 12 months period, there are sales or exchange of 50 percent or more of the total interest in both capital and profits

Termination of Partnership

If the business requires winding up, the

partnership does not terminate when it dissolves. It continues until the liquidation is completed and he proceeds are distributed.

The partnership become a sole proprietorship when a partner buys out all the interests of the other partners, the partnership terminates at the time of the transactions.

Winding Up the Business

Sale or Exchange of a 50 Percent Interest Terminates the Partnership A partnership terminates if there is a sale or exchange of at

least a 50 percent interest in the partnership over a 12-month period.

Example: A-B-C and its partners report on a calendar year basis. On November 30, A sells a 25 percent interest to D. On the following March 1, B sells a 25 percent interest to E. The partnership terminates on the sale to E. However, if D would have resold his interest to E, the partnership would not have terminated because only a 25 percent interest was sold.

Termination of Partnership

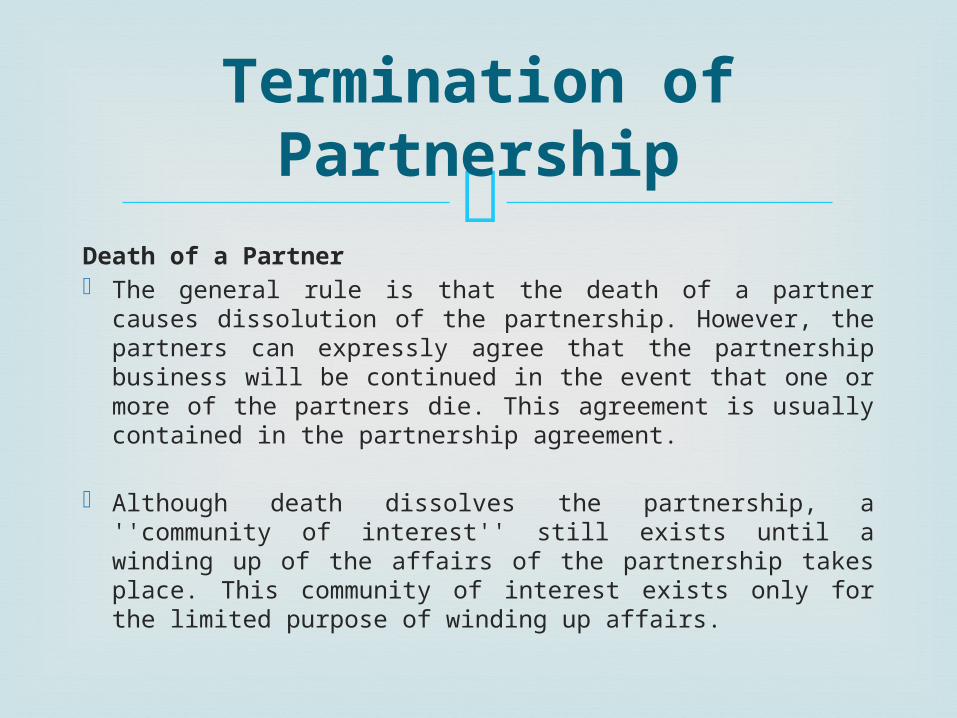

Death of a Partner The general rule is that the death of a partner causes

dissolution of the partnership. However, the partners can expressly agree that the partnership business will be continued in the event that one or more of the partners die. This agreement is usually contained in the partnership agreement.

Although death dissolves the partnership, a ''community of interest'' still exists until a winding up of the affairs of the partnership takes place. This community of interest exists only for the limited purpose of winding up affairs.

Termination of Partnership

After dissolution, Each partner has an equal right to

possess the firm assets, to participate in winding up process, and dispose of the firm assets for the purpose of liquidating and winding up the firm affairs. If dissolution occurs because of the death of one partner, the surviving partners ordinarily have full power to control and dispose of the assets in order to terminate partnership business. The partners may, however, agree among themselves that one or more of them shall have exclusive authority to possess, control and dispose of the assets.

Winding Up the Business

Even after Dissolution, no one is entitled to exclusive possession for his own use of specific partnership property until:

The partnership has been liquidated An Accounting has been made The property has been applied to the payments of debts

Some partners do not have the authority to wind up the partnership, including:

Bankrupt or insolvent partners Partners who have wrongfully dissolved the

partnership

Winding Up the Business

Corporation

“A corporation is an artificial being created by operation of law, having the right of succession and the powers, attributes, and properties expressly authorized by law or incident to its existence.”

Sec. 2, Title I of Batas Pambansa Blg. 68

Corporation

It is an artificial being It is created by operation of law It has the right of succession It has only the powers, attributes, and

properties expressly authorized by law or incident to its existence

Characteristics

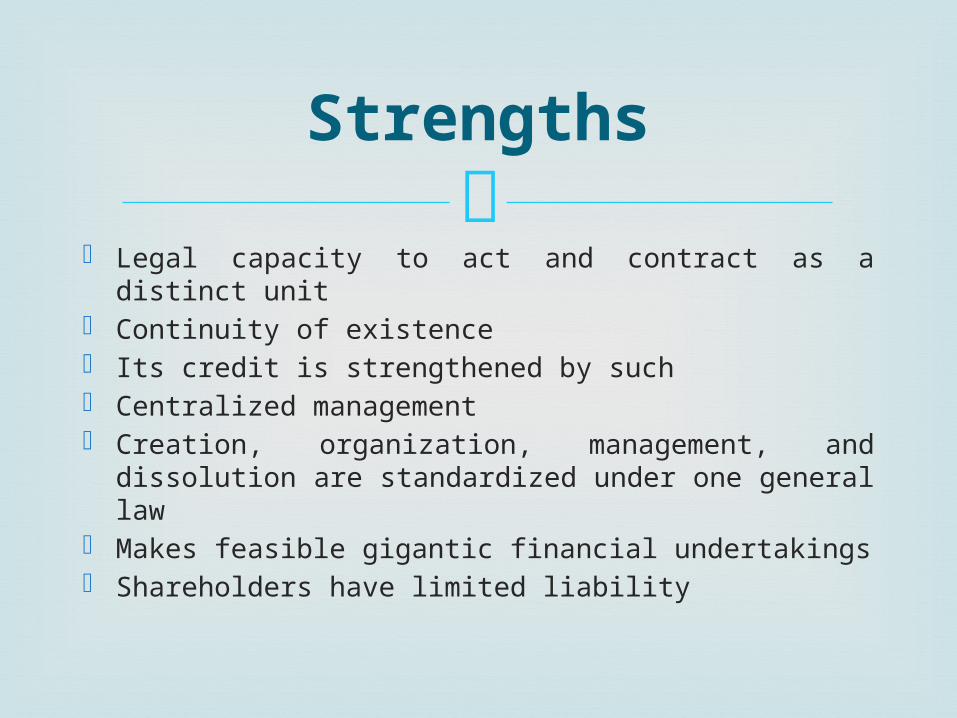

Legal capacity to act and contract as a distinct

unit Continuity of existence Its credit is strengthened by such Centralized management Creation, organization, management, and

dissolution are standardized under one general law

Makes feasible gigantic financial undertakings Shareholders have limited liability

Strengths

Relatively complicated Entails relatively high cost of formation and

operations Greater degree of governmental control and

supervision In large corporations, management and

control are separated from ownership Stockholders have little voice in the conduct of

the business

Weaknesses

Stock corporation Created and operated for the purpose of

making a profit which may be distributed in the form of dividends to stockholders

Non-stock corporation Created not for profit but for the public good

and welfare (e.g. charitable, religious, social, civic, political organizations)

Classes of Corporations

Public corporation Formed for the government of a portion of the

State for the general good and welfare

Private corporation Formed for some private purpose, benefit, or

end

Classes of Corporations

Private corporations also include:

Government-owned or controlled corporations (GOCCs)

Quasi-public corporations

Classes of Corporations

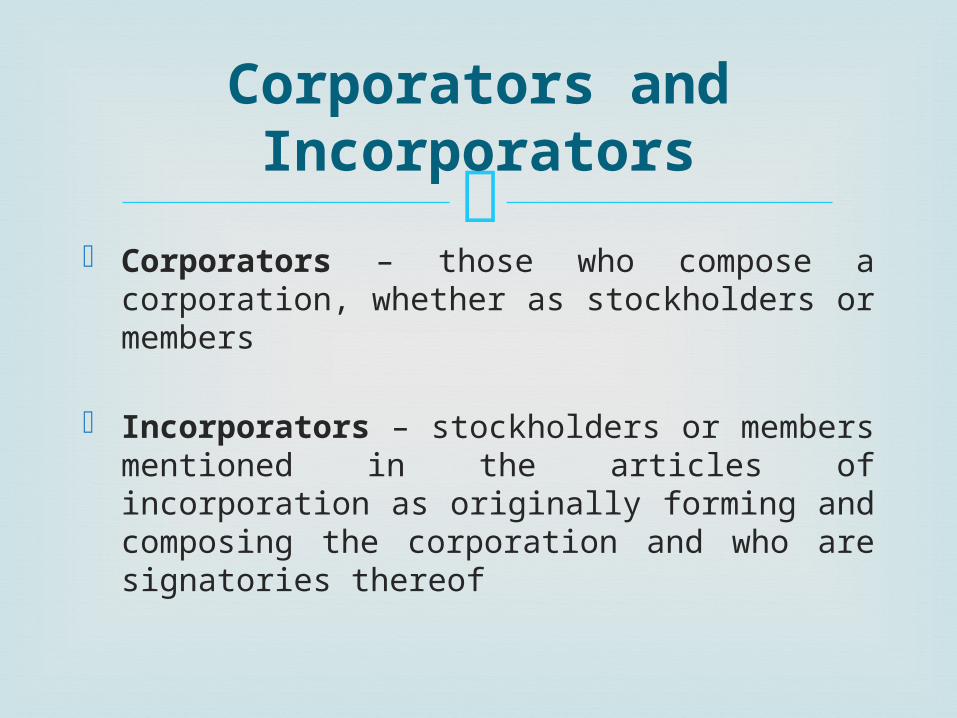

Corporators – those who compose a

corporation, whether as stockholders or members

Incorporators – stockholders or members mentioned in the articles of incorporation as originally forming and composing the corporation and who are signatories thereof

Corporators and Incorporators

5-15 natural persons Of legal age Majority should be residents of the Philippines Must own or be a subscriber to at least 1 share

Number and Qualifications of

Incorporators

Drafting and execution of articles of

incorporation Filing with the Securities and Exchange

Commission (SEC) of the articles of incorporation along with the treasurer’s affidavit

Payment of the filing and publication fees Issuance by SEC of certificate of incorporate

Steps in Incorporation

Stock – one of the units into which the capital

stock is divided

(Authorized) capital stock – amount fixed in the articles of incorporation, to be subscribed and paid in or agreed to be paid in by the stockholders of a corporation

(Share of) Stock

Par value share One with a specific money value fixed in the

articles of incorporation

No par value share Does not state how much money it represents

Par v. No Par Value

Common shares Its holders stand upon an equal footing,

without extraordinary rights or privileges

Preferred shares One with a stated par value which entitles the

holder thereof to certain preferences over the holders of common stock

General Classes of Shares

Founders’ shares Issued to the originators of a firm, these shares

are entitled to all of the remaining (after tax) profits, no matter how much

Redeemable shares These are shares, usually preferred, which by

their terms are redeemable at a fixed date or at the option of either the issuing corporation or the stockholder or both at a certain redemption price

General Classes of Shares

Treasury shares Shares which are lawfully issued by the

corporation and fully paid for and later reacquired by it either by purchase, redemption, donation, forfeiture or other lawful means.

General Classes of Shares

It involves two legal steps:

Termination of the corporate existence at least as far as the right to go on doing ordinary business is concerned; and

The winding up of its affairs, the payment of its debts, and the distribution of its assets among the shareholders or members and other persons interested.

Dissolution

Voluntary By vote of the board of directors/trustees and

the stockholders/members where no creditors are affected

By judgment of the SEC after due process where creditors are affected

Amendment of articles of incorporation By submitting to the SEC a verified declaration

of dissolution for approval

Dissolution

Involuntary By expiration of the term provided for in the

original articles of incorporation By legislative enactment By failure to formally organize and commence

the transaction of its business within 2 years from date of incorporation

By order of the SEC

Dissolution

Manner of creation Number of incorporators Commencement of juridical personality Powers Management Effect of mismanagement Right of succession Term of existence Firm name Dissolution Governing laws

Corporation v. Partnership

It is important to know what structure one will

select for his or her business, as this will not only have an impact on how much you pay in taxes, but will also affect the amount of paperwork you are required to do, as well as the liability you face and your ability to raise money.

Conclusion