Assignment Diploma of Finance and Mortgage Broking Management (DIPMB_AS_v1A3) Student identification (student to complete) Please complete the fields shaded grey. Student number 10326305 Assignment result (assessor to complete) Result — first submission (Details for each activity are shown in the table below) Not yet competent Parts that must be resubmitted: 1, 2, 3, 4, 5, 6, 7 Result — resubmission (if applicable) Not yet competent Parts that must be resubmitted 1,2 3,

Transcript

Assignment

Diploma of Finance and Mortgage Broking Management (DIPMB_AS_v1A3)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10326305

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Not yet competent

Parts that must be resubmitted:

1, 2, 3, 4, 5, 6, 7

Result — resubmission (if applicable)

Not yet competent

Parts that must be resubmitted

Parts that must be resubmitted 1,2 3,

Page 2 of 71

Result summary(assessor to complete)

First submission Resubmission (if required) Se

ctio

n 1

Task 1 Not yet demonstrated Not yet demonstrated

Task 2 Not yet demonstrated Not yet demonstrated

Task 3 Not yet demonstrated Not yet demonstrated

Sect

ion

2

Task 4 Not yet demonstrated Demonstrated

Task 5 Not yet demonstrated Demonstrated

Task 6 Not yet demonstrated Demonstrated

Task 7 Not yet demonstrated Demonstrated

Task 8 Demonstrated Demonstrated

Task 9 Demonstrated Demonstrated

Feedback (assessor to complete) A reasonable first attempt at assignment. There are a few questions that require further work. Please be guided by my comments at each task and refer to the self study material for reference.

This is a Diploma level course and expectation is that you are able to follow the instructions to complete each Task. There were occasions where you did not follow all the points and these have been highlighted in my comments. Overall length o your responses was too long and could have been better completed in parts with dot points or tables (e.g. debt serviceability in Task 3 needs to be in table as could the detail of the security that is to be taken and resultant LVR.

Your additional efforts in task 4, 5, 6 and 7 provided sufficient to demonstrate competency. However inn Tasks 1, 2 and 3 your responses do not demonstrate competency in being able to analyse a loan proposal and put together a succinct report to clients with recommendation nor provide appropriate analysis to present a proposal to a lender.

Before attempting again I suggest you review the material more thoroughly, along with any other training materials you have on the subject and draw on knowledge of some experienced brokers/lenders you may work with.

Page 3 of 71

Before you begin Read everything in this document before you start your assignment forDiploma of Finance and Mortgage Broking Management (DIPMB_AS_v1A3).

About this document

This document includes the following parts:

• Instructions for completing and submitting this assignment

• Results and feedback

• Section 1: Complex lending and broking

• Section 2: Business management skills

Instructions for completing and submitting this assignment

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete the assignment within your enrolment period. Your study plan is in the KapLearn Diploma of Finance and Mortgage Broking Management (DIPMB_AS_v1A3) subject room.

Completing the assignment

The assignment

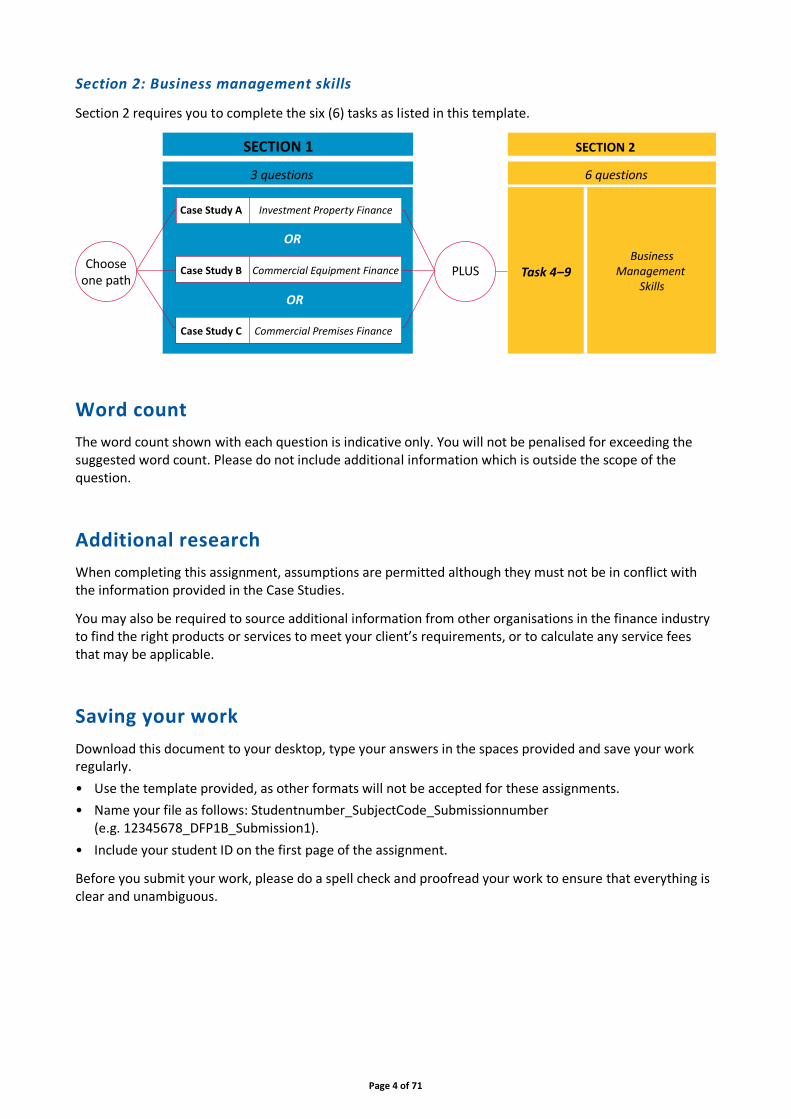

This assignment is split over 2sections. The information and data you need to complete Sections 1 & 2 is presented in case studies at the beginning ofthose sections and each task.

Section 1: Complex Lending and Broking

The first section on complex lending and broking, requires you to answer the questions for one (1) of the three (3)available case studies. Each case study focuses on different lending scenario, (see diagram below).

Page 4 of 71

Section 2: Business management skills

Section 2 requires you to complete the six (6) tasks as listed in this template.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the suggested word count. Please do not include additional information which is outside the scope of the question.

Additional research

When completing this assignment, assumptions are permitted although they must not be in conflict with the information provided in the Case Studies.

You may also be required to source additional information from other organisations in the finance industry to find the right products or services to meet your client’s requirements, or to calculate any service fees that may be applicable.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber (e.g. 12345678_DFP1B_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is clear and unambiguous.

SECTION 1 SECTION 2

3 questions 6 questions

Chooseone path

PLUS

Case Study A

Case Study B

Case Study C

Investment Property Finance

Commercial Equipment Finance

Commercial Premises Finance

OR

OR

Task 4–9Business

ManagementSkills

Page 5 of 71

Submitting the assignment

You must submit your completed assignment in acompatible Microsoft Word document. You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education. Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed all parts and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Diploma of Finance and Mortgage Broking Management (DIPMB_AS_v1A3)subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in your assignment. Failure to do so will mean that your assignment will not be accepted for marking; therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall competence.

Page 6 of 71

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first assessor’s comments in your assignment, so your second assessor can see the instructions that were originally provided for you. Do not change any comments made by a Kaplan assessor.

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in your subject room. You can expect an answer within 24 hours of your posting from one of our technical advisers or student support staff.

Page 7 of 71

Capital City Finance and Mortgage Brokers (CCF & MB) George and Mildred are very happy with the way you service your clients and are sure that you are a good fit for the team. They now want you to turn your focus to your primary task which is to assist in expanding the business by building relationships with selected real estate agents, accountants and legal firms through strategic alliances. They also want you to consider how CCF & MB can consolidate its relationships with its existing strategic partners.

Let’s recap on what you already know about Capital City Finance and Mortgage Brokers (CCF & MB).

It’s a family owned business providing a range of mortgage and finance broking services to the business and private sectors, with experience in all facets of finance and insurance providing expert advice covering a multitude of products and options existing within the market.

CCF & MB specialises in home loans, commercial lending, business lending, personal and motor vehicle finance and insurance (life and general), and focuses on helping clients find the finance service suited to their individual circumstances.

It provides its services through its association with the following partners:

• Australian Aggregators, a rising business in the aggregation business with an extensive panel of residential and commercial lenders, and asset finance.

• ABC General Insurance, a boutique insurance company specialising in a full range of general insurances.

• XYZ Life a small family-owned insurance brokerage specialising in the full range of life insurance products.

Based in the city, CCF & MB has the capacity to service clients from their office or anywhere at their clients’ convenience through its team of mobile brokers.

CCF & MB does not hold a credit license but operates as a credit representative of Australian Aggregators.

Since its inception 13 years ago CCF & MB has built a loan book of almost $1.2 billion and averages over $120 million in new loans annually.

CCF & MB’s vision is to be the mortgage and finance broker of choice in the greater metropolitan area

CCF & MB’s mission statement is to operate professionally in accordance with legislation, our licence and professional standards

CCF & MB’s values are as follows:

• to act with honesty and integrity at all times

• to provide unbiased advice and conduct business, free from any conflict of interest

• to maintain confidentiality in all dealings

• to meet all NCCP regulatory requirements

• to comply with all mortgage industry laws and regulations

• ensure quality and efficiency in its loan processes.

Page 8 of 71

CCF & MB’s people

CCF & MB is owned by husband and wife, George and Mildred Spencer.

With over 35 years’ experience in finance and business ownership, George established and built a successful business dedicated to assisting clients with managing their finances effectively. Starting the business with his wife Mildred 13 years ago, George gained immense satisfaction in seeing it expand to service more and more clients across the city and greater metropolitan area. Although in recent years he has stepped back from dealing directly with clients, he still maintains a small select clientele. He also takes great pride in training and mentoring his team to enhance their performance.

Mildred has over 22 years of lending experience and is qualified not only to assist her clients with their mortgage requirements but also to assist them with their commercial finance requirements. She also holds financial planning qualifications. She specialises in asset finance.

The company has a small team of five additional consultants and two administration staff members. Profiles for the team is as follows:

• Jennifer Dee is recognised as one of the top female brokers in Australia. She has been in the broking industry for over 10 years and has a passion and dedication to assist and accommodate all of her clients’ needs with their financial dreams. Jennifer is an Accredited Mortgage Consultant with the Mortgage and Finance Association of Australia (MFAA).

• Louise Spencer (George and Mildred’s eldest daughter) is an Accredited Mortgage Consultant with the Mortgage and Finance Association of Australia (MFAA) and has been working as a loan consultant for almost two years. Louise started off in the lending industry in the office as an administrator to gain as much experience and knowledge as possible before taking a broking role. Her passion for helping her clients ensures that she is always available to her clients at a time and place convenient for them.

• Michael Spencer is George’s younger brother and is CCF & MB’s equipment finance specialist. He has over 25 years working in the equipment finance industry. He has developed an in depth understanding of the transport and agricultural industries, and also provides finance for general equipment, motor vehicles and computer equipment.

• Martin Longhas specialised in equipment finance for the last three years, but prior to this he spent five years operating his own retail food business. This practical experience allows him to see things from his client’s point of view, including experience with equipment finance. He specialises in plant and equipment in the machinery, woodworking and packaging industries. Examples of some of the equipment he has financed are farm machinery, extrusion lines, plastic injection moulders, commercial catering equipment, woodworking plant, packaging lines, forklifts, office fit-outs and many different motor vehicles.

• Luis Ramirez migrated to Australia in 25 years ago as a young boy with his family. After completing high school he graduated from university with an accounting degree and worked in ANZ in commercial lending. He joined CCF & MB 4 years ago and specialises in vehicle and capital equipment financing. He provides ITC and general equipment lease funding options for clients. By providing better outcomes, both during and at the end of their equipment leases, Luis’ many clients have been able to reduce costs and maximise the value of their available budgets.

CCF & MB is a member of the MFAA as a broking business dealing directly with the public. Both George and Mildred are fellows of the MFAA. CCF & MB is also a corporate member of the FBAA.

All staff members, including consultants, are paid an annual salary plus superannuation. Consultants also receive a car allowance plus a percentage of trail commissions that are paid quarterly based on their performance targets.

Page 9 of 71

CCF & MB’s panelled lenders

With access to an extensive panel of lenders, CCF & MB can meet most clients’ expectations. Residential lenders are listed in the following table.

Adelaide Bank Homeloans Limited Pepper Home Loans

AMP Homeside Phoenix-Circle Credit Union

ANZ ING Direct PLAN Lending

Australian Financial Keystart PN Bank

Australian First Mortgage La Trobe Resi

Bank of Melbourne Liberty Financial St George Bank

BankSA Macquarie Suncorp

Bankwest ME Bank The Rock Building Society

Bluestone Mortgage Mart Westpac

Citibank NAB Wide Bay Australia Ltd

Commonwealth Bank Newcastle Permanent

Heritage Bank Peoples Choice Credit Union

Commercial lenders and asset finance providers are listed in the following table.

Adelaide Bank Commercial Bibby Financial Services Pty Ltd Liberty Financial Commercial

ANZ Commercial Commonwealth Bank Commercial NAB Commercial

Australian First Mortgage Commercial IMB Commercial St George Commercial

Bank SA Commercial ING Direct Commercial Suncorp Commercial

Bankwest Business Banking LaTrobe Commercial Westpac Commercial

Adelaide Bank Commercial Macquarie Leasing Westpac Equipment Finance

ANZ Asset Finance Commonwealth Bank Asset Finance Liberty Asset Finance

Future developments

George and Mildred are very keen to expand and grow their business and are in the process of speaking with a number of real estate agents, accountants and legal firms with a view to forming strategic alliances.

Due to the expected increase in business George and Mildred are seeking to employ another consultant to take on the extra work. This person will be required to:

• build strategic relationships with a number of real estate agents, accountants and legal firmsalready identified

• identify and foster relationships with other real estate agents, accountants and legal firms

• provide finance and mortgage broking services to new clients identified through these strategic alliances.

Page 10 of 71

Section 1: Complex lending and broking

Only complete Tasks 1–3 for one (1) of the case studies in Section 1

Case study A— Tom and Steve Broad

Background

Congratulations, you have just been appointed by George and Mildred as the new consultant to handle the extra work. Whilst your major focus is to build the strategic relationships you are also expected to build your own client base using your own connections and networks.

Two brothers, Tom and Steve Broad have approached you with their desire to jointly purchase two apartments in the same building. They want to purchase them as rental properties. The building has 12 apartments. The units have 80% permanent tenants in place and the remaining 20% are used for holiday rentals. The location is a highly sought after area and all holiday periods are fully booked.

The brothers have invested together before and have experience in buying and selling property. They have sold all their other investment properties and the units will be their only investment until they can identify another opportunity. The cash at bank is mostly from the sales of other investments.

The property

Address: Unit 1, 92 Seaside Lane, Coastville, <Your State> Unit 9, 92 Seaside Lane, Coastville, <Your State>

Purchase price: $350,000 $385,000

Description: 2 bedroom strata title unit on the ground floor 2 bedroom strata title unit on the ground floor

Body corporate fee $2,500 per annum $2,500 per annum

Proposed income Permanent rental at $450 per week Holiday rental at $45,000 per annum

Agent details: Steven Allstone Steven Allstone

Phone: 8282 1113 8282 1113

Mobile: 0412 880 088 0412 880 088

Page 11 of 71

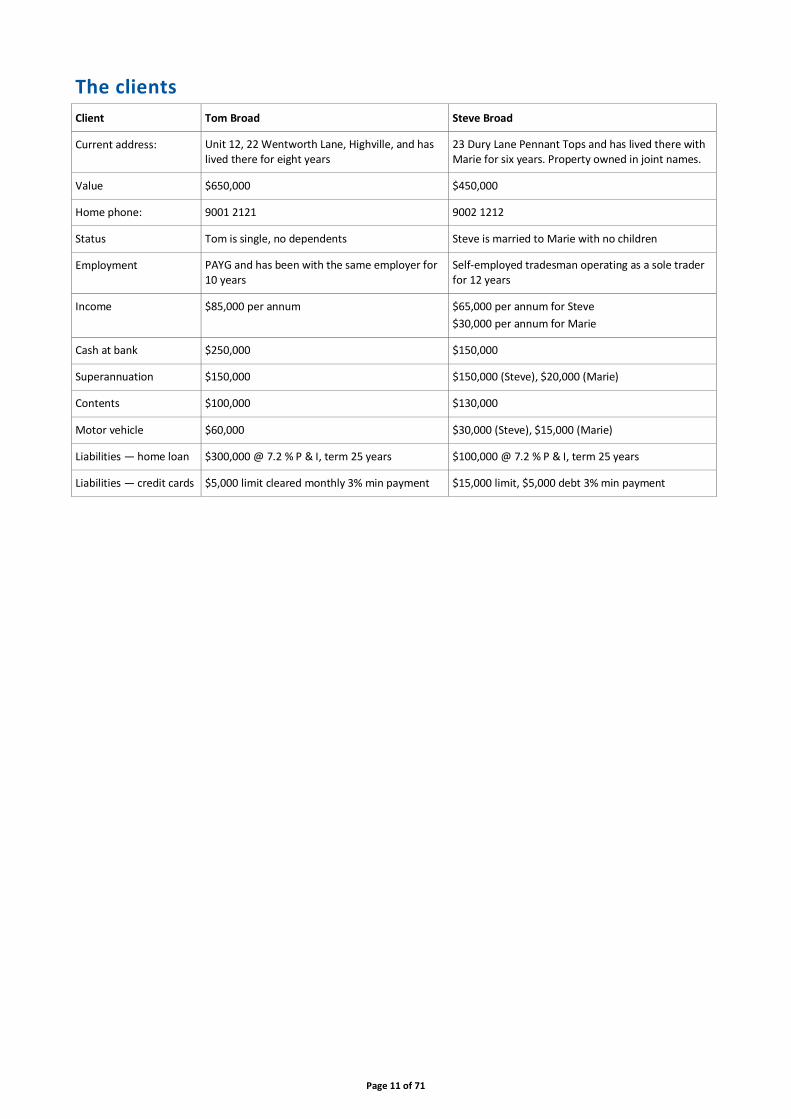

The clients

Client Tom Broad Steve Broad

Current address: Unit 12, 22 Wentworth Lane, Highville, and has lived there for eight years

23 Dury Lane Pennant Tops and has lived there with Marie for six years. Property owned in joint names.

Value $650,000 $450,000

Home phone: 9001 2121 9002 1212

Status Tom is single, no dependents Steve is married to Marie with no children

Employment PAYG and has been with the same employer for 10 years

Self-employed tradesman operating as a sole trader for 12 years

Income $85,000 per annum $65,000 per annum for Steve

Motor vehicle $60,000 $30,000 (Steve), $15,000 (Marie)

Liabilities — home loan $300,000 @ 7.2 % P & I, term 25 years $100,000 @ 7.2 % P & I, term 25 years

Liabilities — credit cards $5,000 limit cleared monthly 3% min payment $15,000 limit, $5,000 debt 3% min payment

Page 12 of 71

Assignment tasks (student to complete)

Task 1a — Identify the clients’ complex broking needs

Prepare a list of questions that you would need to ask Tom and Steve about their history and experience, and the unit purchase.

In preparing your list of questions you should ensure that you cover the following:

• The complex features of Tom’s and Steve’s situation and objectives.

• Potential risks and Tom’s and Steve’s tolerance of risk. In considering risk you should consider:

– how you would identify the risks and the criteria you used to evaluate these risks

– how you would assess their current exposure, the tools you would use in terms of probability, impact and the consequences.

(800 words)

Student response to Task 1a

Tom and Steve Broad are two brothers who want to buy two apartments jointly in a single building.

Their motive is to buy it for renting purposes. Being the financial consultant or adviser for the

brothers on the case, it is my responsibility to know everything about the brothers in a detailed

manner. It include their personal details, financial obligations and position. Also, I would be

required to gain information about their past experiences related to the procurement of the

properties, their loan obligations and all the information related to the property that they propose to

acquire.

I will not be at a position to offer any advice or opinion if it is not known if their proposition is

feasible or not, from a financial standpoint. I need to understand if they would be able to meet the

loan obligations in a timely manner or not. All this information can only be obtained by asking

suitable questions from the two brothers. It will also impart understanding on the degree of risk that

can be endured by them that is their risk tolerance.

The following is the list of questions that would I would ask the clients in regards to the proposed

investment:

I have done basic research on you and I think I have some idea about your background but I’d

Page 13 of 71

like get more understanding on your past investment experiences. Could both of you tell about

the nature of investments you were involved in the past?

What is your experience in the real estate field?

What are your expertise and skills?

What has been the status of your debt obligations and your strategies to meet them in time?

What are the areas of your working and the types of properties you usually work with, cities you

had been employed in and the number of homes that you have bought and sold in the past two

years?

It is important ask background questions first. This way they do not take a defensive positon and

prepares them for upcoming invasive questions. While searching for a new real estate property,

a well-experienced person in this field can help a lot with the help of their experience to search

for real estate. All these questions will also help in assessing their current exposure in the

business. The question about debt obligations would enquire if they are debt-free or not.

Next set of questions would aim to determine their risk-appetite?

Could you please divulge into details about your income and all the income sources?

It is an important determinant to measure the client’s risk tolerance. If the income is high, it is

more likely that the client’s risk tolerance is also high and vice versa. This is due to the fact that

small setbacks would not affect their capability and ability to invest.

What all information can you offer about your expenses and outgoings?

This question aims to determine their expenses that can highly influence their risk appetite. If

their income is high but outgoings are higher relatively, then they would not able to take high

risks. It is important to manage unnecessary expenses.

What can you tell me about financial responsibilities?

This question aims to enquire about all the individual who are financially dependent on them.

The question would probe into their marital status, their children or any other person on entity

Page 14 of 71

that are dependent on the clients.

What amount of liquid cash you have handy at present?

There must always be cash saved as savings in bank for sustaining the lifestyle and for future

financial emergencies. The clients must have sufficient liquidity so that in order to cover any

expenses in future, they don’t have to liquidate their investments.

Are you or your dependents covered under some insurance policy such as Life Insurance Cover

and Health Insurance?

The client’s risk tolerance is highly dependent on the clients’ health and all those dependent on

them. If they do not have any policy that would insure them in illness or accident, they are prone

to have a lower risk appetite.

What amount of loss (in percent) in your investment portfolio would cause personal discomfort

to you such as deprived sleep, despair or anxiety?

In order to know about the probable risks that they may face, I would ask following questions:

What were the challenges that you faced in past or predict facing in future?

What do you deem most difficult while dealing with those challenges?

What strategies you adopt to mitigate the effects of the investment risks?

If you have an investment portfolio of $100,000, and falls down to $80,000 within a month,

what would you do: Sell all the investments, Sell a part of the financial portfolio, sell nothing or

invest larger funds?

How you assume the probability of the risk and what are the impacts of those risks and how you

manage with its consequences?

The company can utilize the technique that Tom and Steve use to tolerate the risks and thus can

work on it to improve it further.

Do you develop an exit strategy for your investments?

Page 15 of 71

Assessor feedback: Resubmission required?

Competency not yet demonstrated. You appear to have misread

part of the case study or perhaps confused it with one of the

others. These are two brothers looking to purchase two residential

investment properties. They don’t need educational qualifications

in this field – they work in different professions. Please re-read

case and amend response.

Competency not yet demonstrated. You have not made sufficient

amendment to the response to demonstrate you have knowledge of

the correct questions to be asked.

No

Page 16 of 71

Task 2a —Develop complex broking options

You are required to prepare a full report for Tom and Steve by outlining the process and the risks (potential and real) of which Tom and Steve should be aware.

In a suitable format, document the process that is required for them to purchase the two units as their investment properties, establishing a joint loan in the brother’s names. You should also include a selection of lenders that will consider this style of borrowing.

In developing your report you should cover the following:

1. The parties to the loan including any opportunities or constraints that could impact on their application

2. The different options available and your recommendation of the best loan structure with the lender — are they using their own property as cross security or the cash at bank as deposit?

3. What various forms of titles could an apartment be registered in

4. A list of the lenders that are able to lend

5. The procedure to commence a loan for a property like this

6. The steps that will need to be in place

7. The client responsibilities, so Tom and Steve fully understand the loan

8. An outline as to the process and what the client needs to arrange

9. The documentation needed to commence the borrowing

10. The name in which the client will sign the contract/purchase/offer and acceptance. If a Family trust is involved what name would the title of the property be registered in, and advise what state you are using to base your answer on

11. The state revenue requirements

12. Which lenders may also require a personal guarantee from Steve’s spouse

13. The maximum LVR to the consumer

14. A summary of all fees and charges — including those for setup and those of the lender.

(800 words)

Student response to Task 2a

With the help of your previous experience, both of you would be able to purchase the two

apartments in the same building while selling off all their investments. You want only these two

apartments as a final investment as these apartments are your only investment. The opportunities

that you have is that both of you already have experience in buying and selling of property and Tom

is with a company from 10 years, whereas Steve is working as a businessman from past 12 years.

Another opportunity for you is that these apartments are in demand.

While I was looking for the ways to increase my client base, I managed to meet you two brothers,

Tom and Steve Broad as you were trying to purchase two apartments in the same building.

Page 17 of 71

However, since the building is in the most sought after area, so you will face trouble acquiring the

proposed two apartments. Another factor that would be an obstruction is the fact that there are only

12 apartments and out of them, 80 percent has permanent tenants and the rest 20 percent are booked

for a holiday rental purposes only. You would be required to send an application to the property

owner who would see that the best application gets the apartments, which is doneby references,

background verification, etc.

In order to make the process easier to understand, let me break it down into parts:

The first step would be to calculate your borrowing capability, i.e. how much can you borrow?

In the next step, all the additional charges will be determined such as deposits, legal costs,

stamp duty and insurance costs.

The best type of loan needs to be determined for your investment.

Getting pre-approval: It means that you get approved and that you fulfil all the lending criteria.

Then the buying process would start that would include making an offer, Contract of Sale,

finalising of loan and settlement. Making an offer includes exchanging contracts, paying

deposits and property valuation. Finalising the loan getting loan approval through Loan

Contracts. The day the ownership of the investment property will be taken by you is the date of

settlement. All the balance payments are required to be done on the day of settlement.

You would be required to apply for loan for the investment in the property wherein you both will be

the borrower party and there will be another lender party. The different forms of titles in which the

apartments can be registered in are freehold, Group title, Company title and Leasehold. It is

recommended that you use the investment property as the security as it is not advised to use your

existing property because the risk involved is higher. If you are not able to meet the debt obligations

or repayments, you may lose your home too. Also in the case of residential loans, you will not be

able to use you contents and motor vehicles as security. The contact/purchase/offer/acceptance will

be signed in the name of Tom and Steve Broad. If there’s a Family Trust involved then the title will

Page 18 of 71

be registered in the name of the Trust. This will protect you and your family if the trust holder dies

and the family would still be able to use the investment property. The risk of high debts would be

reduced. You are advised to open and manage a trust based on proper tax advice. It is also known as

deed of trust. It is just a way of securing the debts and it just imposes lien on a title. This

information is based on the regulations in New South Wales. You need to consider loan fees and

features such as ongoing fees, mortgage offset and home loan rates and decide which type of loan

will be suitable for you. I can help by offering all the important details about the loans so that you

make a wise decision. The process of getting investment loan starts with pre-approval. You will be

required to get a pre-approval from the lender directly. It can be also done through a mortgage

broker. There are several options available for you to take loans and some of the companies that can

provide best suitable loans are ING Direct, NAB, NAB Commercial and IMB Commercial. It

would be better for you to use cash at bank, but since it is not enough to clear your way, so you

have to take a loan from the lenders as mentioned above. Any of these lenders can borrow money

easily and they have very minimum resistance in their procedure to offer the loan. You can easily

take loan following easy steps. The steps that the receiver need to follow are only limited to take

loans following the lender’s terms and conditions and the same goes for apartments.

When you apply for pre-approval, lender makes a check of your credit record. After you get pre-

approval, the buying process will start. Making the offer is the next step. You will be required to

offer the holding deposit. Then the contract of sale will be created by an agent or the lender’s

lawyer. The offer will be outlined, date of settlement and all the conditions before the buying is

settled. At last, the offer will be finalized.

The responsibility of the client is to maintain the privacy and confidentiality. The lender will

mention this before offering the loan to you. The customer has to apply for the loan and then they

have to submit their cash details which include the bank details, details of their property’s value,

etc. After verifying all these necessary details, the lender will then offer the loan. You would be

Page 19 of 71

required to submit your bank details with another source of income and you also need to provide a

document that provides the knowledge about the people dependent on both of you. In the case of

Tom, he is single, so he is independent but in the case of Steve, he is married, but his wife is not

dependent on Steve as she has her income source. The lender has to consider all these elements

before offering the loan.

Almost every lender these days require a guarantor for the person they are offering the loan

so, in the case of Steve, the lender will need his wife who is also an independent woman to make as

a guarantor for Steve to confirm the payback of their loan.Among the earlier mentioned lenders,

NAB can ask for the guarantor. The fees are as:

Application fee of $600, facility fee is $250 pa, loan service fee is $8 pm and application Fee for

existing customers with the newloan is $300. The total cash at bank for both of you is $400,000.

The total worth of the property is $735,000. Therefore, the amount of the loan would be around

$335,000. This way your LVR would be around 45.58%. As your LVR would be less than 60%,

you will be at the minimum risk and you would not be required to pay the Lenders Mortgage

Insurance. The state revenue requirements would include stamp duty and land tax. It is also known

as land transfer duty. The office would require the proof that you are the new owners.

Page 20 of 71

Assessor feedback: Resubmission required?

Competency not fully demonstrated. As per first line of question, this is supposed to be a report from you to Tom and Steve, therefore language has to be in the first party. Please restructure your response and ensure the content covers in detail all the points covered in the question.

Competency not yet demonstrated. You have not fully addressed

the points in the Task as requested.

The report makes no mention of what amount they should borrow,

the deposit they should contribute nor the actual security required

– except a guarantor from Marie which will not be required if

loans are structured correctly.

Why would have superannuation be a constraint to the

application?

No

Page 21 of 71

Task 3a — Implement complex loan structures

Tom and Steve have accepted your recommendations and have given you authority to proceed with their application.

As part of implementing their loan application you are required to prepare a formal written loan submission to the lender for pre-approval. Your loan submission must include the following:

• serviceability calculations

• the proposed structure of the loan given there are two brothers and there is a variance in income

• the loan amount

• the property style, size, use

• any other information that is relevant to the lenders requirements.

In additional to these requirements you should also include:

• your obligations under the NCCP (if any)

• maximum loan amount

• maximum loan terms

• any ATO consideration to be made

• your state legislation and OSR requirements

• your general advice restrictions

• property purchase requirements.

(800 words)

Note: Any assumptions you make should be listed, and not be in conflict with the case study information already provided.

Student response to Task 3a

The objective of this application is to request for a loan for pre-approval. I would request you to

provide a loan amount of $335,000 to purchase two apartments. As this area is in demand and the

apartments are costly, we would require the loan amount. We already have experience in buying

and selling of property, so we had already sold out our all other properties and these apartments are

our only investment as of now. We require this loan under the name of Tom and Steve Broad. The

reason we would like to purchase this property is that it can be used either for permanent residential

purpose or holiday’s purpose. The building policies do not allow any other use of these apartments.

This letter provides the information of the client applying for the loan. The name of the client is

Tom Broad, who with his co-borrower Steve Broad are applying for a loan. Their income source

differs from each other as Tom is with his employer for almost ten years. He is single at present and

has no dependents. His details are as follows:

Page 22 of 71

Income is $85,000 per annum

Cash at the bank is $250,000

Superannuation of $150,000

Contents of $100,000

Motor vehicle $60,000

Liabilities — home loan $300,000 @ 7.2 % P & I, term 25 years

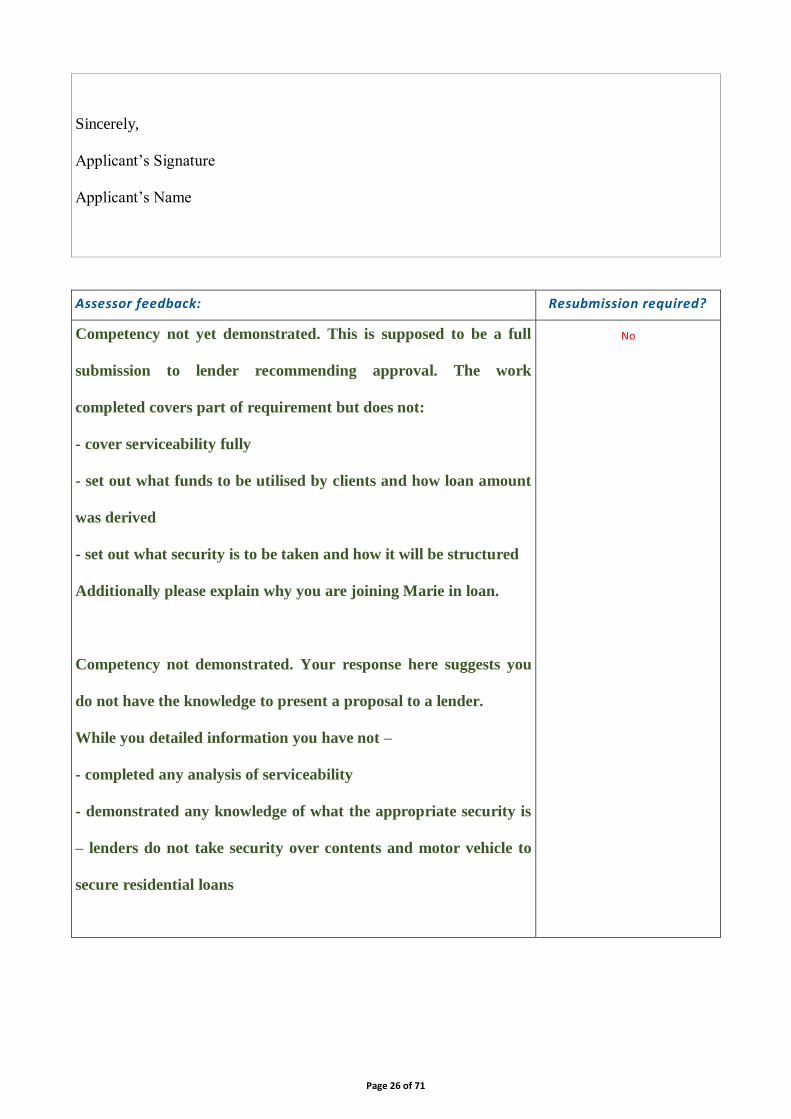

Competency not yet demonstrated. This is supposed to be a full

submission to lender recommending approval. The work

completed covers part of requirement but does not:

- cover serviceability fully

- set out what funds to be utilised by clients and how loan amount

was derived

- set out what security is to be taken and how it will be structured

Additionally please explain why you are joining Marie in loan.

Competency not demonstrated. Your response here suggests you

do not have the knowledge to present a proposal to a lender.

While you detailed information you have not –

- completed any analysis of serviceability

- demonstrated any knowledge of what the appropriate security is

– lenders do not take security over contents and motor vehicle to

secure residential loans

No

Page 27 of 71

Case study B— Ray Murdoch and Steve Brown

Only complete Tasks 1–3 for one (1) of the case studies in Section 1

Background

You have just met with Ray Murdoch and Steve Brown, referred to you by another commercial client.

Ray Murdoch and Steve Brown jointly own a successful and growing business that manufactures metal pallets. They trade under the name Pallets-R-Us Pty Ltd. The pallets are manufactured using material that is lightweight and durable. There has also been a very structured approach to the research and development for the engineering and design of the pallets. The pallets are used in all industry sectors. Part of the process involves powder coating the finished product, which is currently outsourced to a local well-established contractor.

It is critical that Ray and Steve’s product meets market needs. They need to maintain sustainable production and operating costs if they are to forecast their sales and cost of sales.

They have a well-established client database that provides them with repeat ‘business to business’ dealings. Whilst they have only been trading for 26 months they have a solid business plan with written supply contracts with three major business clients and several smaller business clients.

Ray and Steve now require a loan to assist them with the purchase of a sophisticated machine, using the technical platform system CNC. This machine can be programmed to rapidly fabricate multiple components. The machine has an expected commercial lifespan of at least 15 years with operating software to be updated every three years. This software and upgrades is included in the purchase price of $800,000.They need to import the machine from the US. Initial enquiries with the US supplier have indicated that they will require a letter of credit for the import of the machine.

Their business employs five people and, with the expected increase in business through the automation of production, they have forecast that they will need to recruit an additional two staff members in the next 3–6 months to meet sales/production demands.

Steve has been in the metal fabrication field all his working life. He has an MBA and understands financial management. He also has solid engineering skills and developed the majority of the design works for the business. He is married and has no dependants. His wife is a school teacher and she will be retiring at the end of the year.

Ray worked with Steve at ‘Protech’ as a foreman. His skills are in production and managing project/job flow. He has high level technical skills and can complete works to specification at a high standard. Ray is divorced.

Steve and Ray have provided the last two year’s financial accounts for the trading business, as well as interim accounts for the current financial year.

Page 28 of 71

Applicant information

Client Ray Murdoch Steve Brown

Current address: Unit 43, 25 High St Northville, <Your State>and has lived there for six years

23 Desmond Lane Northville, <Your State> and has lived there with Kate for seven years. They own property jointly.

Value $750,000 $900,000

Home phone: 9001 2121 9002 1212

Status Ray is divorced with no dependent age children Steve is married with no dependents

Employment Self-employed business owner Self-employed business owner

Income $100,000 per annum $100,000

Property $750,000 $900,000

Cash at bank $12,500 $9,600

Contents $100,000 $85,000

Superannuation $250,000 Steve $350,000, Kate $60,000

Motor vehicle $40,000 $55,000

Home loan $250,000 @7.2% P & I Term 18 years $350,000 @7.2% P & I Term 22 years

Credit card $25,000 limit with debt of $15,000 payment @3% $10,000 limit with debt of $3,000 payment @3%

Car loan $0 $15,000 payment @ 9% payable 4 years

The business

Year 1 net profit after tax $200,000

Year 2 net profit after tax $220,000

Current year interim profit (10 months trading) $200,000

Wages to partner 1 – years 1 and 2 $100,000

Wages to partner 2 – years 1 and 2 $100,000

Dividend to private investor (flat profit fee) – years 1 and 2 $45,000

Key balance sheet items

Cash $25,000

Debtors $220,000

Creditors $100,000

Notes The business currently meets all creditor payments at 30-day terms.

Debtor collection has been solid. They invoice an upfront payment of 50% of the sale price, which assists in funding their production.

They have orders of $1m over the next 3 months and have made an increase in their gross profit margin.

The orders are from several clients, so their debtors will be well spread.

Page 29 of 71

Task 1b — Identify the clients’ complex broking needs

Prepare a list of questions that you would need to ask Ray and Steve about the proposed transaction.

Calculate the required servicing for the new debt, and the lender comfort surplus.

Outline the process and the risks (potential and real) of which Steve and Ray should be aware.

(800 words)

Student response to Task 1b

Answer here

Assessor feedback: Resubmission required?

No

Page 30 of 71

Task 2b —Develop complex broking options

You are required to prepare a full report for Ray and Steve by outlining the process and the risks (potential and real) of which Ray and Steve should be aware.

In a suitable format, document the process that is required for Steve and Ray to obtain appropriate finance for their equipment and set up the loan.

In developing your report you should cover the following:

1. The parties to the loan

2. The product type you would recommend, including an appropriate term, interest rate and residual (if any)

3. The framework and contents of the letter of credit requirements

4. A list of the lenders that are able to lend

5. The procedure to commence a loan

6. The steps that will need to be in place

7. The client responsibilities, so Steve and Ray fully understand the loan

8. An outline as to the process and what the client needs to arrange

9. The documentation needed to commence the borrowing

10. The name in which the client will sign the contract to purchase

11. A statement of those lenders who may also require a personal guarantee from the borrower’s spouse

12. A summary of all fees and charges — including those for setup and those of the lender.

(800 words)

Student response to Task 2b

Answer here

Assessor feedback: Resubmission required?

No

Page 31 of 71

Task 3b — Implement complex loan structures

Ray and Steve have accepted your recommendations and have given you authority to proceed with their application.

As part of implementing their loan application you are required to prepare a formal written loan submission to the lender for pre-approval. Your loan submission must include the following:

• serviceability calculations, including all borrowing facilities of Directors

• the proposed structure of the loan

• the loan amount

• the property style, size, use

• any other information that is relevant to the lenders requirements.

In additional to these requirements you should also include:

• your obligations under the NCCP (if any)

• maximum loan amount

• maximum loan terms

• any ATO consideration to be made

• your state legislation and OSR requirements

• your general advice restrictions

(800 words)

Note:Any assumptions you make should be listed, and not be in conflict with the case study information already provided.

Student response to Task 3b

Answer here

Assessor feedback: Resubmission required?

No

Page 32 of 71

Case Study C — Bill Smith and John Jones

Only complete Tasks 1–3 for one (1) of the case studies in Section 1

Background

You are meeting with prospective clients, Bill Smith and John Jones. They have been referred to you by their accounting firm, Buckland Accountants.

The prospective clients need assistance with the acquisition of owner-occupied premises to replace their current business premises which is rented and becoming too small for their growing business.

True Blue Pty Ltd trades as True Blue Real Estate and was purchased as an existing real estate business three years ago. Bill Smith and John Jones are the directors.

The shareholders of True Blue Pty Ltd are Bill Smith, John Jones and a private investor, Amanda Williams, who does not work in the business and has no involvement in its day-to-day operation. Each holds an equal one-third share in the company.

Bill and John have each been in real estate for approximately 15 years, focusing on residential sales and leasing. They have gained their work experience in the local area. A wealth of knowledge of the area, coupled with an ever-expanding client base, has resulted in sustained and solid growth for the business.

Details of the property

Sale price of the property is $950,000. (There is no GST requirement as it is being purchased as a going concern.)

A deposit of $95,000 has been paid and is being held in the trust account of the settlement agent/solicitor.

A cash contribution of $233,240 will be made from the general working account of the business.

Property purchase and loan to be in the name of a new entity — True Blue Pty Ltd as trustees for the Smith Jones Unit Trust. There are a total of 99 units in the trust and the unit holdings mirror the shareholding of the trading entity, True Blue Pty Ltd.

The property is situated at 100 Smith St, Yourtown, with contracts exchanged at today’s date and an anticipated settlement date of 90 days.

General observations about the property

The property is in good condition and is well located in the same street as the current rental premises. It is anticipated that the premises will meet the needs of the business for the next 10 years.

Page 33 of 71

Summary of initial client fact find

Bill and John have provided the last two years’ financial accounts for the trading business, as well as interim accounts for 10 months of the current financial year.

True Blue Real Estate’s financial accounts

Year 1 Year 2

Net profit after tax $92,000 $140,060

Current year projected- $175,000

Add back (rent) $47,000 $49,142

Additional superannuation to director $31,400 $34,539

Wages to partner one $70,640 $70,640

Wages to partner two $70,640 $70,640

Payment to private investor (fixed flat profit fee) $45,000 $45,000

Applicant information — Bill Smith

Personal details

Address 26 Nowry Road, Yourtown, 1234

Date of birth 17 February 1958

Phone 7890 1234

Financial details

Gross income $70,640

Owner occupied property valued at $550,000

Outstanding debt on owner-occupied property $210,000 @ 6.2% p.a. on a principal and interest basis

Credit card with limit $15,000 Outstanding debt — $5,000

Superannuation $250,000

Motor vehicle valued at $30,000 (nil debt)

Page 34 of 71

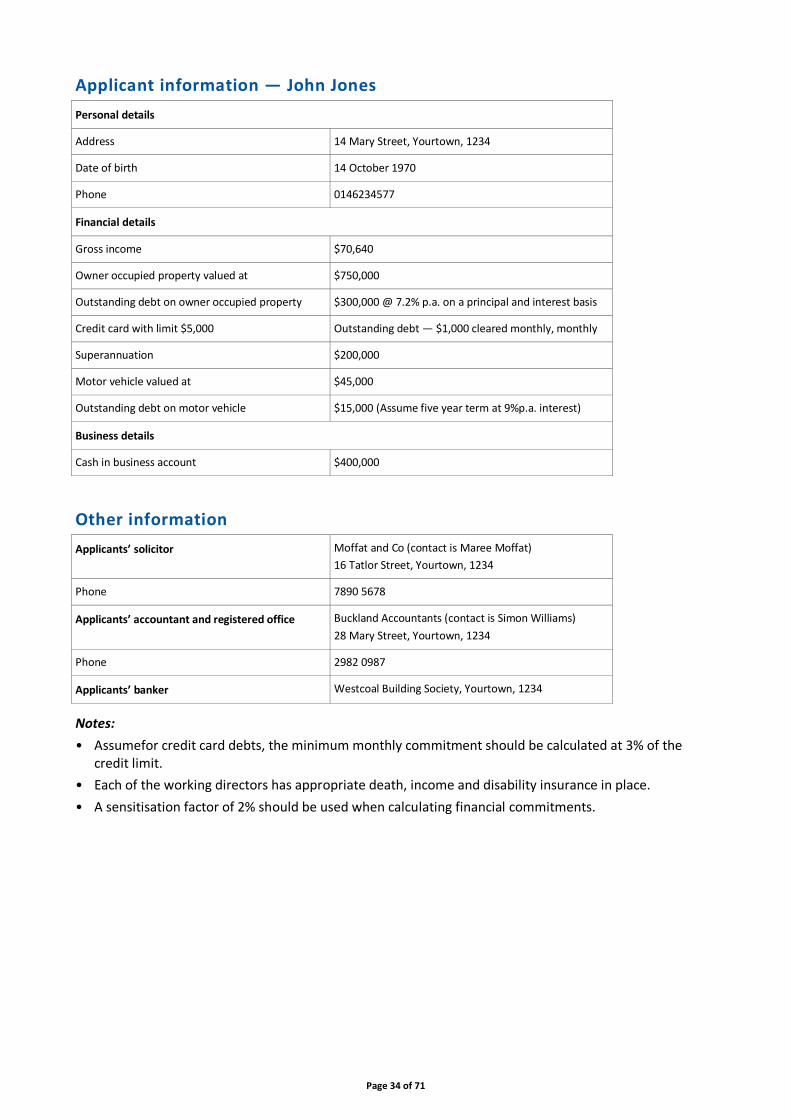

Applicant information — John Jones

Personal details

Address 14 Mary Street, Yourtown, 1234

Date of birth 14 October 1970

Phone 0146234577

Financial details

Gross income $70,640

Owner occupied property valued at $750,000

Outstanding debt on owner occupied property $300,000 @ 7.2% p.a. on a principal and interest basis

Outstanding debt on motor vehicle $15,000 (Assume five year term at 9%p.a. interest)

Business details

Cash in business account $400,000

Other information

Applicants’ solicitor Moffat and Co (contact is Maree Moffat)

16 Tatlor Street, Yourtown, 1234

Phone 7890 5678

Applicants’ accountant and registered office Buckland Accountants (contact is Simon Williams)

28 Mary Street, Yourtown, 1234

Phone 2982 0987

Applicants’ banker Westcoal Building Society, Yourtown, 1234

Notes:

• Assumefor credit card debts, the minimum monthly commitment should be calculated at 3% of the credit limit.

• Each of the working directors has appropriate death, income and disability insurance in place.

• A sensitisation factor of 2% should be used when calculating financial commitments.

Page 35 of 71

Assignment tasks (student to complete)

Task 1c — Identify the clients’ complex broking needs

Prepare a list of questions that you would need to ask Bill and John about their history, experience, business performance and the property purchase.

In preparing your list of questions you should ensure that you cover the following:

• The complex features of Bill’s and John’s situation and objectives.

• Potential risks and Bill’s and John’s tolerance of risk. In considering risk you should consider:

– How you would identify the risks and the criteria you used to evaluate these risks

– How you would assess their current exposure, the tools you would use in terms of probability, impact and the consequences.

(800 words)

Student response to Task 1c

Assessor feedback: Resubmission required?

Yes

Page 36 of 71

Task 2c — Prepare complex broking options

You are required to prepare a full report for Bill and John by outlining the process and the risks (potential and real) of which Bill and John should be aware.

In a suitable format, document the process that is required for them purchase the new property and establishing the loan.

In developing your report you should cover the following:

1. The parties to the loan

2. The best physical set up with the lender — are they using their own property as cross security or the investment property?

3. What name should the title be registered in given there is a Trust involved and advise what state you are basing your answer in

4. The procedure to commence a loan for a property like this

5. The steps that will need to be in place

6. The client responsibilities (Bill and John should fully understand the loan that is proposed)

7. An outline as to the lending process and what the client needs to arrange

8. The documentation needed to commence the borrowing

9. The name in which the client will sign the contract to purchase

10. The state revenue requirements

11. A statement as to whether guarantees from spouse’s or any other security will be required and why this is/is not the case

12. The maximum LVR

13. Suggest three (3) lenders to client’s that would be likely to consider this request

14. A summary of fees and charges — including those for setup and those of the lender.

Note: You may make any reasonable assumptions necessary in order to complete the proposal.

(800 words)

Student response to Task 2c

Assessor feedback: Resubmission required?

Yes

Page 37 of 71

Task 3c — Implement complex loan structures

Bill and John have accepted your recommendations and have given you authority to proceed with their application.

As part of implementing their loan application you are required to prepare a formal written loan submission to the lender for pre-

• the proposed structure of the loan given the purchases is in the name of a new Unit Trust entity

• the loan amount

• the property style, size, use

• proposed security

• any other information that is relevant to the lenders requirements.

In additional to these requirements you should also include:

• your obligations under the NCCP (if any)

• maximum loan amount

• maximum loan terms

• any ATO consideration to be made

• your state legislation and OSR requirements

• restrictions on overseas purchase, if any

• your general advice restrictions

• property purchase requirements.

Notes:

• Any assumptions you make should be listed, and not be in conflict with the case study information already provided.

• You will need to calculate and include your workings of the required servicing and debt service cover ratio for the new debt and existing borrowings of Directors. Comment on the DSCR comfort level for lender.

• You may make any reasonable assumptions necessary in order to complete the proposal.

Student response to Task 3c

Assessor feedback: Resubmission required?

Yes

Page 38 of 71

Section 2: Business management skills

Task4 — Developing and nurturing relationships with clients, other professionals and third party referrers

George and Mildred now require you to write a plan to assist in developing and nurturing relationships with clients, other professionals and third party referrers.

Your plan should address the following:

1. How CCF & MB’s policies and procedures and legislative, regulatory and professional codes of practice impact on developing and nurturing relationships

2. How you would use CCF & MB’s social, business and ethical standards to develop and maintain positive relationships

3. The importance of confidentiality and how you would maintain it in your dealings with colleagues, clients and other parties

4. How you would adjust your Interpersonal style to the needs and situation of other parties

5. How you would go about developing and maintaining business and professional networks and other relationships to benefit the organisation, and how you would use them to identify and cultivate relationships in order to promote and market the organisation

6. How you could use and cooperate with other professionals and third parties to expand and enhance the reputation of the organisation, and to identify new and improved business practices

7. How you would build referral business through appropriate communication channels to find and secure new business relationships

8. How you would identify referral needs and provide information p about CCF & MB’s relevant products and services

9. How you would secure interviews with referral business so that then needs of clients can be met.

(1,000 words)

You may use any format for your plan but it must address each of the points above. If you are unsure as to how to write a plan, you can refer to the Business Growth and Marketing topic and use the suggested SMEAC format outlined in Part 5, Section 12.

When completing this task, assumptions are permitted although they must not be in conflict with the information provided in the background information.

Student response to Task 4

Task 4 — developing and nurturing relationships with clients, other professionals and third

party referrers

The quality of client relationship plays a major role in making any business successful. It is like the

good friendship which builds understating and rapport between parties. It takes regular and clear

communication to the clients to achieve such effective relationship. Building such clear

relationships with clients involves investing effort and time into understanding or accepting the

Page 39 of 71

client’s business and condition. However it is a time taking process. Establishing and then retaining

such client relationship is simply a cost-effective practice which contributes in improving efficiency

and productivity. A plan is required to develop and nurture relationship with clients or other

professional in order to take the business to new heights.

The plan mainly focuses on building and sustaining rewarding and effective relationship with all

the professionals related to this industry. There are certain official or legal requirements under CCF

and MB’s policies which are included in the plan of building good client relationship. The legal

procedure requires clear documentation which reduces the chance of any misunderstanding between

people of the company and clients. The documentation has significant role in building and

maintaining a healthy relationship. We, through letter of acceptance, intend to sign enforceable

contract with clients so they that they can come to know about the company’s terms and policies

and feel secure about any deception. The policies of CCF and MB help the client. We provide the

range of solutions for their queries.

We will strive for deal with our client with full of integrity, professionalism and competency.

Providing unbiased advice to the client is one of the business ethical behaviour of CCF and MB

thereby we will provide the best possible suggestions regarding the business. Focusing on meeting

the expectations of the client would be the fundamental agenda under the plan of building an

effective relationship with client. Every business dealing with the client would be free from conflict

of interest. The opinions of the clients will be listened carefully. With every new client, we will take

the session to educate them about all mortgage sector regulations. CCF and MB’s fundamental

values like honesty and integrity would surely encourage the client to engage with the company.

This is kind of business which requires confidentiality. As this industry is highly competitive,

the role of confidentiality is very essential. If, any organization is failed to properly protect and

secure business information then it can affect business and client relationship adversely.

Every business dealings require confidentiality. Here, also, there are certain information which

Page 40 of 71

are needed to keep confidential if not or in wrong hands then these information or data can be

misrepresented or misused in illegal activities such as fraud and discrimination. Lack of

confidentially in the business may lead to undesirable outcomes of the business. The disclosure of

information of company or its clients which are sensitive or should not be opened may result in loss

of client trust, loyalty and confidence. This always ended up as loss of efficiency and productivity.

Therefore, our plan fully focuses on the best practices of strengthen the confidentiality in dealing

with the clients. In the official manner, we will share the legal agreement with client in which both

will give the assurance of live up on the words that each other’s sensitive information would not be

disclosed in any circumstances. Also in other way, through casual meeting, we will share our past

experience and show our responsibility and integrity towards confidentiality. We would not talk

about the sensitive information about client and their cases in front of other people. In the same way

the company’s confidentiality can be maintained. We will keep the company’s and clients file in the

safe which could be accessible for some selected people in of the company. In the official meetings

with the clients, we will demand and share relevant files and documents only so that the risk of

disclosure of sensitive information can be minimized. The information either of company or client

would not be told to anyone has nothing to do with the business. We will avoid any risk which can

turn into loss of trust and loyalty from clients. As protecting confidential data of information of

company and their clients is core component of company’s ethical behaviour, we would keep it

confidential and maintain healthy relationship of trust and loyalty with clients.

We believe in adjusting to the needs and the situations of the clients. If the client is not

comfortable discussing deals through telephonic conversations, we would set personal meeting with

the clients. As we said our plan is totally focused on fulfilling client’s expectations and

requirements so we would not take a step back when there will need to adjust our workflow.

However, we would never hamper the company’s policies in the sake of client’s satisfactions.

Clients comes with lots of hope, so it is our responsibly to live on their expectations. For this, we

Page 41 of 71

will ask the client about him/her time and place in which he/she is comfortable to sign a deal. We

will also consider clients’ opinions and according to it will make changes in the work schedule if

needed. Our interpersonal styles and techniques involve:

Appropriate methods for communicating information and ideas to the clients.

Seeking response from the internal and external sources for developing and refining

approaches and ideas.

Treating clients’ empathy, respect and integrity.

Soft-sell methods

Hard-sell methods

Education and information

Negotiation and persuasion

Our professional and business network may connect with:

Land title offices, construction and building professionals

Planning consultants, quantity surveyors and surveyors

Our referral network can include:

Relatives and friends

Past clients

Recommendations from the clients

Franchise referrals and recommendations

Developed networks

Page 42 of 71

In order to develop and maintain business and professional networks, we would make use of

appropriate channels for communications. These channels include advertisements, community

events, seminars, face-to-face meetings, mail drops and electronic technology. Business and

professional networking is one of the effective and cost efficient marketing procedures to expand

business. Building professional networks provides the opportunities to make profits. We would go

for contacting the people through referrals and convert them into clients in order to save time and

money. We would also go for other traditional methods of approaching people such as email,

phone, email, social media and business websites. We will optimize company’s promotional

activities in order to company visible to people. We will attend various business events in order to

get noticed by people in the industry which helps the company in building professional network and

increasing opportunities.

In order to enhance the reputation of the company, firstly, we will get the opportunities such as

client’s leads and joint ventures and involve them in company’s vision and mission. The

accumulated knowledge from the professionals and the third parties would lead to satisfied

customers which would definitely enhance the company’s reputation. It would also us to expand

and explore the markets and increase our popularity with new services. Our cooperation and

relationship would be based on self-analysis, chemistry and compatibility.

We would set the target of referrals and with the help of old clients and through social media or

email referral strategies we would be able to secure new business relationship. Whenever there will

be need of professional network or expanding business through internal workforce in the company

then we would go for referrals. We will take the referrals from the old clients. We will provide the

company’s information through those old clients only because they can easily educate their

colleagues about company’s policies and procedures.

We will identify the vacancies and would select best of referred people for interview. Initially we

will inform our referring clients about company’s need so that they can refer such people from

Page 43 of 71

whom the needs of the clients can be met.

Assessor feedback: Resubmission required?

Competency not yet demonstrated. You have covered off some of

the points in Task but you have not really addressed which other

professional people you would like to network with for mutual

business development. Think of a referral network as not just

coming from existing clients but those other professionals you deal

with. Your further comments should focus on points 4, 5, 6

highlighted above. You might also refer to the SMEAC example

for guidance as to how this response should be presented.

Competency now demonstrated.

No

Page 44 of 71

Task5 —Growing the business

Having considered how you would go about building and nurturing relationships, George and Mildred now require you to turn your attention to marketing and promoting CCF & MB’s business. This requires you to develop a marketing plan for the business.

In developing your marketing plan you should consider the following:

1. Your plan should be developed in line with CCF & MB’s vision statement

2. The identification of target markets using a combination of research and your own personal experience

3. The identification of your major competitors (at least two) with a competitor analysis developed for each competitor

4. The identification of CCF & MB’s market position based on your research findings and analysis

5. How you would promote CCF & MB’s brand and the tools you would use to achieve this

6. The provision of options for increasing yield per existing client

7. How you would implement your plan and monitor it to ensure objectives/goals/performance indicators are being met

8. How you would adjust your plan if required.

(1,000 words)

You may use any format for your plan but it must address each of the points above. If you are unsure as to how to write a plan, you can refer to the Business Growth and Marketing topic and use the suggested SMEAC format outlined in Part 5, Section 12.

When completing this task, assumptions are permitted although they must not be in conflict with the information provided in the background information.

Student response to Task 5

Task 5 — growing the business

Developing a plan for marketing is the fundamental requirement of every small, middle and large

business organization. A marketing plan in the form of a business document outlines the company’s

marketing strategy. Marketing plan static process it keeps on changing according to the demand of

the company. Like every other company, we will make a marketing plan for CCF and MB in order

to increase brand awareness among people.

Our marketing plan consists of several components. The first component of our market plan is

‘understand the customers’. First, the company will have to identify the customers or the people

who are looking for the services we provide. The vision statement of CCF and MB is to be the

mortgage and finance broker of choice in the greater metropolitan area. The vision statement

indicates the objective of the company. So the company will has to promote themselves in

Page 45 of 71

metropolitan area where the scope of getting clients is very high. The company will has to evaluate

demand from the customers.

This marketing plan will allow company to target services to the ideal customers who most

likely to avail the services. The ideal customers of this company are person seeking loan, individual

requiring finance for business start-up, person who have personal finance requirement. And the

scope of getting these kinds of customers is very high in the metropolitan cities.

After understanding the customers, the plan involves analysing the market in terms of scope of

this business in that particular area. The analysis will involve researching on past data about how

much persons look for mortgage and finance every year, how many new start-ups have opened in

last few years with help of mortgage age and finance broker. This will help company in evaluating

the scope of the business in that particular metropolitan area.

The next in the marketing plan is to analyse the competition in the market. Identification of the

competitors is very important to make any business sustainable in the market because every new

company that comes in the market have to analyse the approaches and tactics of other company

present in the market. Australian finance group is one of the major competitors of CCF & MB in

mortgage and finance broking market. AFG is one of the leading firms in the mortgage and finance

broking market which have been offered home loans to thousands of their customers. AFG offers its

finance services at reasonable price. AFG has built a healthy relationship with their clients. It now

provides insurance products, commercial finance, and securitised products of AFG. In order to give

tough completion to AFG, CCF & MB will have to offer services at low price and with more

authenticity. The second name in this competition could be Mortgage Choice which is also a well-

known mortgage broker. However, it is not too old firm but CCF and MB will have to analyse the

marketing tactics that Mortgage choice implements.

The market plan is also involves determining the market position of the company. As CCF and

Page 46 of 71

MB is a new company in this market so it is too early to say about its market position. The market

plan that we have set is expected help CCF & MB in reaching good position in the market.

We will use content marketing to promote CCF and MB. Content marketing involves

encouraging customers to avail the services through slogans showing company’s quality of services.

We will also use social media to promote brand. By generating referrals we would be able to get

visible by people. With the typical mortgage and fiancé services we will provide the educational

structure which will help the company in making reputation in the market. There are various other

tools which we would use to promote brand such as testimonials, email marketing, digital

marketing and promotional programs and events. We will set the budget in which all the

promotional activities would be covered.

Implementation of the plan starts with the reviewing the all the steps involves in the marketing

plan. Execution of market planning requires team of experts and adequate resources which CCF and

MB already has. A session with the marketing will be held in order to readdress them about

objective and goals which the company is trying to achieve. A separate team would be assigned for

each component of the marketing plan. For example, one team will analyse the market situation,

one team will analyse the competitors activities and so on. Simultaneously, one team will be

focusing on building relationship with clients, agents and professionals and also generating

referrals.

Once the plan is implemented next is to monitor the same. In monitoring the plan, we will track

the advertising campaign and other promotional activities associated with marketing plan. We

would be focusing on determining whether the plan is on target or not. We would be tracking how

many new clients we are approaching in every week or month or how many real estate agents we

have approached since the plan started. We would also check whether our marketing budget on

track or not. We would be monitoring the best practices we have implemented to analyse market

situation and activities of competitors. We would also be checking for any failure of the market

Page 47 of 71

strategy.

We would make adjustments in the marketing plan when needed. By staying beware of changes in

market condition, technology, competition, clients, customers, and other factors, we would easily

be able to adjust our plan. We would refine the marketing objectives. However, the vision statement

will be remained same. Either by increasing or decreasing time and budget for the plan, we would

make adjustments in the making plan.

Action Plan for the company:

Month Activities Deadline Responsible

January Understanding customer base 31/1 Senior manager

(Marketing

Department)

January Analysis of the market to find out the

scope of the business

31/1 Product Manager

February Analysis of the competition in the market

and the market position of the company

15/2 Sales manager

March Content marketing to promote CCF and

MB

30/3 Head of Marketing &

Distribution

April Implementation of the plan 30/4 Marketing team

May Monitoring the progress and the

effectiveness of the plan

Continuous

process

Head of Marketing &

Distribution

Assessor feedback: Resubmission required?

Competency not yet demonstrated. Some good work but you need

to actually develop an Action Plan for all to follow. Please take the

points you have made above and produce a short Action Plan

covering ―the activity‖, ―By who‖ and By when‖.

Competency now demonstrated.

No

Page 48 of 71

Task6 — Identifying risk and applying risk management processes

George and Mildred have become very concerned about the potential risks that could jeopardise CCF & MB’s business operations. They were very impressed with your growth and marketing plans for CCF & MB so they have now moved you into more of a general manager’s role with expanded responsibilities, including managing CCF & MB’s risk. As part of your new responsibilities you are required to develop a risk management plan.

In producing this plan you are required to:

1. Establish the context for CCF & MB’s risk management plan

2. List and explain the tools you will use in assessing the risks you identify

3. Identify the stakeholders you would consult in establishing context and the tools you would use in identifying CCF & MB’s risks

4. Identify at least two risks that CCF & MB could face for each of the six categories of business risk including strategic risks, compliance risks, financial risk, operational risks, market and environmental risks and reputational risks with an appropriate risk statement for each identified risk

5. Conduct a risk analysis and risk evaluation for the risks you have identified

6. Identify treatments for them

7. How you will monitor and review them in your risk management plan.