78

Foundations of Risk Management FRM 2012 Study Notes – Part 1.Topic 1 By David Harper, CFA FRM CIPM www.bionicturtle.com

| Date post: | 25-Oct-2015 |

| Category: |

Documents |

| Upload: | sadiakhn03 |

| View: | 202 times |

| Download: | 47 times |

Foundations of Risk Management FRM 2012 Study Notes – Part 1.Topic 1

By David Harper, CFA FRM CIPM

www.bionicturtle.com

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 1 www.bionicturtle.com

Table of Contents

Jorion, Chapter 1: The Need for Risk Management ............................................. 2

Stulz Chapter 3: Creating Value with Risk Management ...................................... 17

Elton, Chapter 5: Delineating Efficient Portfolios .............................................. 24

Elton, Chapter 13: The Standard Capital Asset Pricing Model ............................... 31

Elton, Chapter 14: Nonstandard Forms of Capital Asset Pricing Models ................... 37

Elton, Chapter 16: Arbitrage Pricing Model (APT) .............................................. 42

Amenc, Chapter 4 (4.2 only): Applying CAPM to Performance Measurement ............. 46

CAS, Overview of Enterprise Risk Management ................................................. 53

Allen, Chapter 4: Financial Disasters ............................................................ 61

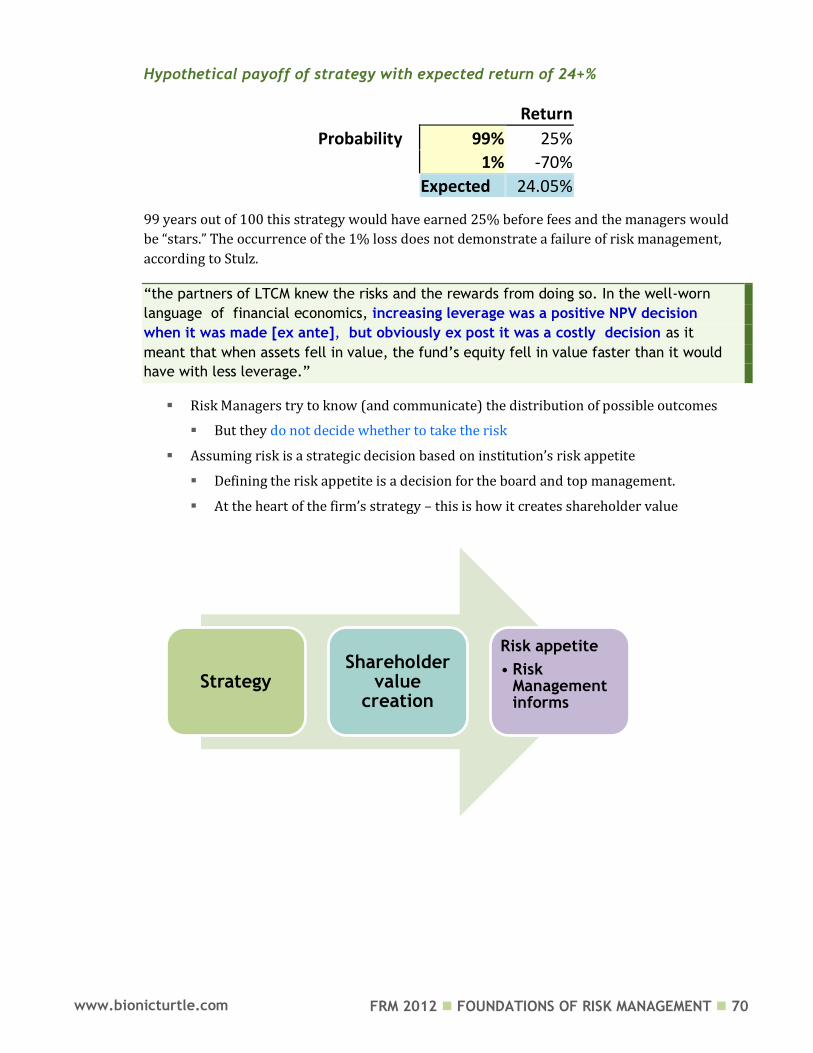

René Stulz,” Risk Management Failures What and When .................................... 69

GARP Code of Conduct ............................................................................... 74

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 2 www.bionicturtle.com

Jorion, Chapter 1:

The Need for Risk

Management

In this chapter…

Define risk and describe some of the major sources of risk. Differentiate between business and financial risks and give examples of each. Relate significant market events of the past several decades to the growth of

the risk management industry. Describe the functions and purposes of financial institutions as they relate to

financial risk management. Define what a derivative contract is and how it differs from a security. Define financial risk management. Define value-at-risk (VaR) and describe how it is used in risk management. Describe the advantages and disadvantages of VaR relative to other risk

management tools such as stop-loss, limits, notional limits, and exposure limits. Compare and contrast valuation and risk management, using VaR as an example. Define and describe the four major types of financial risks: market, liquidity,

credit, and operational; and their forms.

Define risk and describe some of the major sources of risk.

Risk is volatility of unexpected outcomes (value of assets, equity, or earnings). Some authors

distinguish between risk and uncertainty:

Risk: when the outcome is random but the probability distribution is known or can be estimated or approximated. e.g., a six-sided die (we know the distribution is uniform). Much of our FRM study concerns the traditional attempt to parameterize (or otherwise estimate, even if empirically) the approximately distribution of possible losses.

Uncertainty: the probability distribution is itself unknown. Example: a terrorist attack. This is when the distribution itself eludes us.

The major sources of risk include:

Human (Accident) including regulatory policy (and unintended consequence

Human (Deliberate) including terrorism and war

Natural disaster including earthquakes and hurricanes

Economic growth including the creative “disruption” caused by technological innovation

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 3 www.bionicturtle.com

Differentiate between business & financial risks & give examples of each.

Business risks are risks that the corporation assumes willingly. They may do this to create a competitive edge or to add shareholder value.

Financial risks are losses due to financial market activities. Examples of financial risk include losses due to interest-rate movements or defaults on financial obligations.

Deliberate, necessary

Competitive advantage

To create Shareholder value

For example

Business decisions (investments, products) & environment (competition & economy)

Shareholders pay for and expect firms to assume business risk!

Losses due to financial market activities

For example

Interest rate exposure

Defaults on financial obligations

Accounts receivables

To a non-financial firm, not core & firm should (probably) hedge

Banks & financial services are in the business of managing financial risk; managing

financial risk is (should be) a core strategic activity. However, industrial (non-financial)

companies typically want to hedge financial risks; i.e., the assumption of financial risk is

often non-strategic to non-financial companies.

Human (Accident)

• Regulatory policy: unintended consequence

Human (Deliberate)

• Terrorism

• War

Natural disaster

• Earthquake

• Hurricane

Economic Growth

• Technological innovation

Business Risks Financial Risks

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 4 www.bionicturtle.com

Relate significant market events of past several decades to growth of the

risk management industry.

Fixed exchange rate system broke down 1971 1

Oil price shocks High inflation 1973 2

Black Monday. US stocks drop 23%

10/19/87 3

Bond debacle (Fed hikes rates 6 times) 1994 4

Deflation of Japanese stock price bubble 1989 5

Asian turmoil 1997 6

Russian default Global crisis (LTCM) Aug 1998 7

Terrorist attack on New York 9/11/01 8

Visible subprime crisis Aug 2007 9

Fed takeover Fannie Mae & Freddie Mac; Merrill Lynch sold; Lehman bankruptcy; AIG Sep 2008 10

Bretton

Woods

Black

Monday

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 5 www.bionicturtle.com

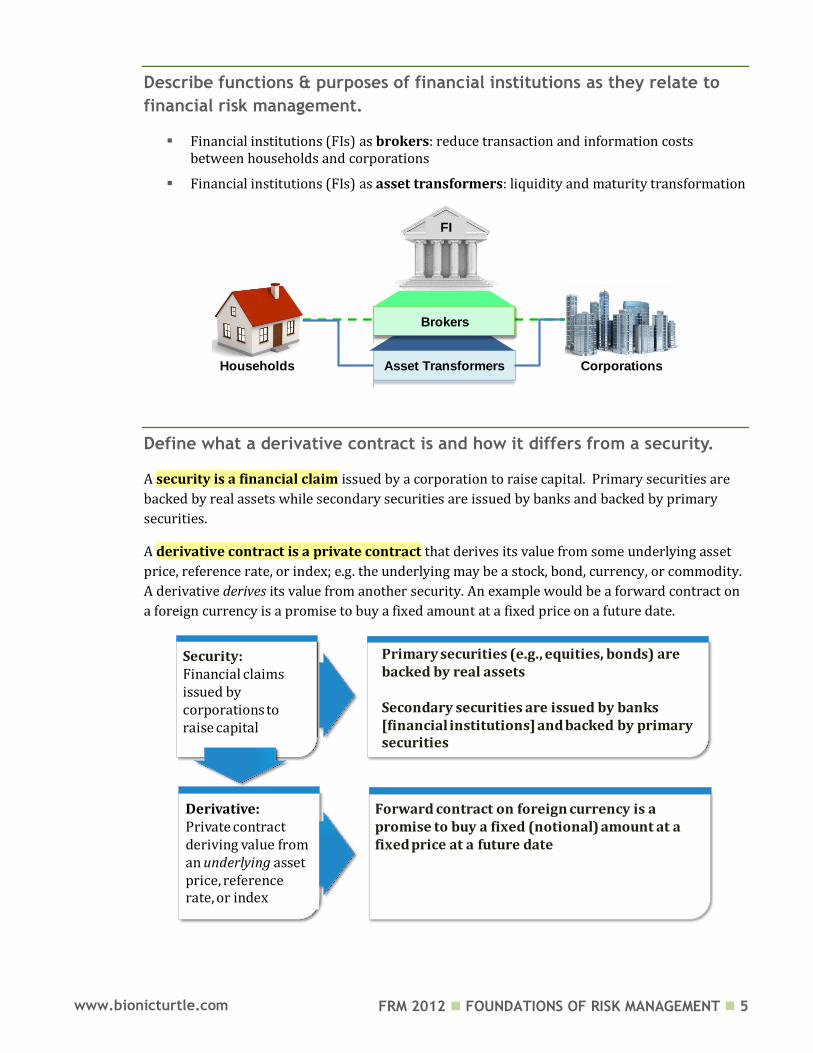

Describe functions & purposes of financial institutions as they relate to

financial risk management.

Financial institutions (FIs) as brokers: reduce transaction and information costs between households and corporations

Financial institutions (FIs) as asset transformers: liquidity and maturity transformation

Define what a derivative contract is and how it differs from a security.

A security is a financial claim issued by a corporation to raise capital. Primary securities are

backed by real assets while secondary securities are issued by banks and backed by primary

securities.

A derivative contract is a private contract that derives its value from some underlying asset

price, reference rate, or index; e.g. the underlying may be a stock, bond, currency, or commodity.

A derivative derives its value from another security. An example would be a forward contract on

a foreign currency is a promise to buy a fixed amount at a fixed price on a future date.

Asset Transformers

Brokers

Corporations

FI

Households

Security:Financial claims issued by corporations to raise capital

Primary securities (e.g., equities, bonds) are backed by real assets

Secondary securities are issued by banks [financial institutions] and backed by primary securities

Derivative:Private contract deriving value from an underlying asset price, reference rate, or index

Forward contract on foreign currency is a promise to buy a fixed (notional) amount at a fixed price at a future date

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 6 www.bionicturtle.com

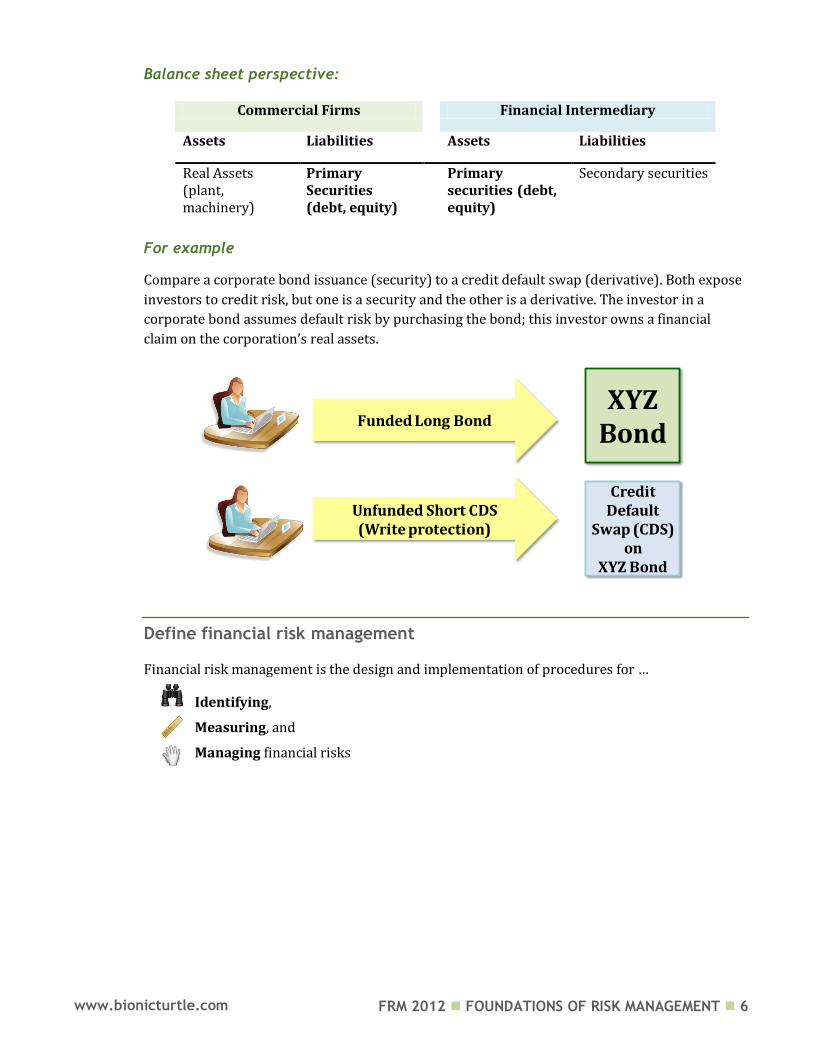

Balance sheet perspective:

Commercial Firms

Financial Intermediary

Assets Liabilities

Assets Liabilities

Real Assets

(plant, machinery)

Primary Securities (debt, equity)

Primary securities (debt, equity)

Secondary securities

For example

Compare a corporate bond issuance (security) to a credit default swap (derivative). Both expose

investors to credit risk, but one is a security and the other is a derivative. The investor in a

corporate bond assumes default risk by purchasing the bond; this investor owns a financial

claim on the corporation’s real assets.

Define financial risk management

Financial risk management is the design and implementation of procedures for …

Identifying,

Measuring, and

Managing financial risks

XYZBond

Credit Default

Swap (CDS) on

XYZ Bond

Unfunded Short CDS (Write protection)

Funded Long Bond

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 7 www.bionicturtle.com

0

20

40

60

80

100

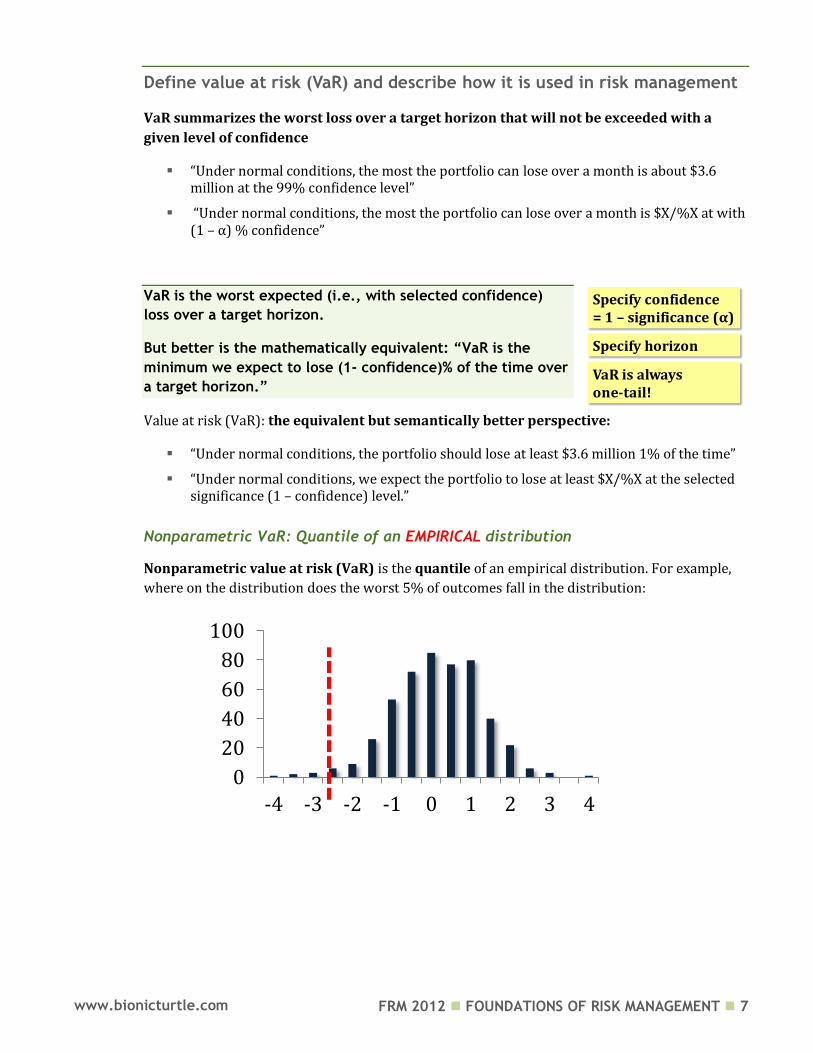

-4 -3 -2 -1 0 1 2 3 4

Specify confidence = 1 – significance (α)

Specify horizon

VaR is always one-tail!

Define value at risk (VaR) and describe how it is used in risk management

VaR summarizes the worst loss over a target horizon that will not be exceeded with a

given level of confidence

“Under normal conditions, the most the portfolio can lose over a month is about $3.6 million at the 99% confidence level”

“Under normal conditions, the most the portfolio can lose over a month is $X/%X at with (1 – α) % confidence”

VaR is the worst expected (i.e., with selected confidence)

loss over a target horizon.

But better is the mathematically equivalent: “VaR is the

minimum we expect to lose (1- confidence)% of the time over

a target horizon.”

Value at risk (VaR): the equivalent but semantically better perspective:

“Under normal conditions, the portfolio should lose at least $3.6 million 1% of the time”

“Under normal conditions, we expect the portfolio to lose at least $X/%X at the selected significance (1 – confidence) level.”

Nonparametric VaR: Quantile of an EMPIRICAL distribution

Nonparametric value at risk (VaR) is the quantile of an empirical distribution. For example,

where on the distribution does the worst 5% of outcomes fall in the distribution:

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 8 www.bionicturtle.com

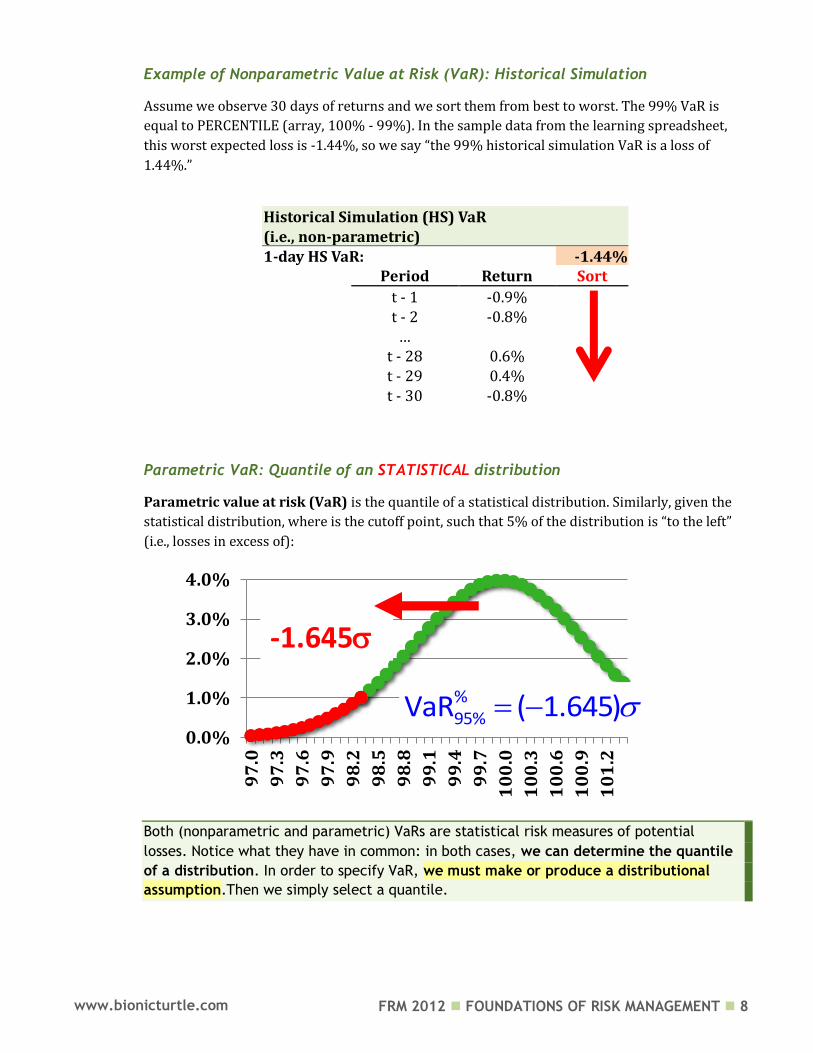

Example of Nonparametric Value at Risk (VaR): Historical Simulation

Assume we observe 30 days of returns and we sort them from best to worst. The 99% VaR is

equal to PERCENTILE (array, 100% - 99%). In the sample data from the learning spreadsheet,

this worst expected loss is -1.44%, so we say “the 99% historical simulation VaR is a loss of

1.44%.”

Historical Simulation (HS) VaR (i.e., non-parametric) 1-day HS VaR:

-1.44%

Period Return Sort

t - 1 -0.9%

t - 2 -0.8%

…

t - 28 0.6%

t - 29 0.4%

t - 30 -0.8%

Parametric VaR: Quantile of an STATISTICAL distribution

Parametric value at risk (VaR) is the quantile of a statistical distribution. Similarly, given the

statistical distribution, where is the cutoff point, such that 5% of the distribution is “to the left”

(i.e., losses in excess of):

Both (nonparametric and parametric) VaRs are statistical risk measures of potential

losses. Notice what they have in common: in both cases, we can determine the quantile

of a distribution. In order to specify VaR, we must make or produce a distributional

assumption.Then we simply select a quantile.

0.0%

1.0%

2.0%

3.0%

4.0%

97

.0

97

.3

97

.6

97

.9

98

.2

98

.5

98

.8

99

.1

99

.4

99

.7

10

0.0

10

0.3

10

0.6

10

0.9

10

1.2

%95%VaR ( 1.645)

-1.645

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 9 www.bionicturtle.com

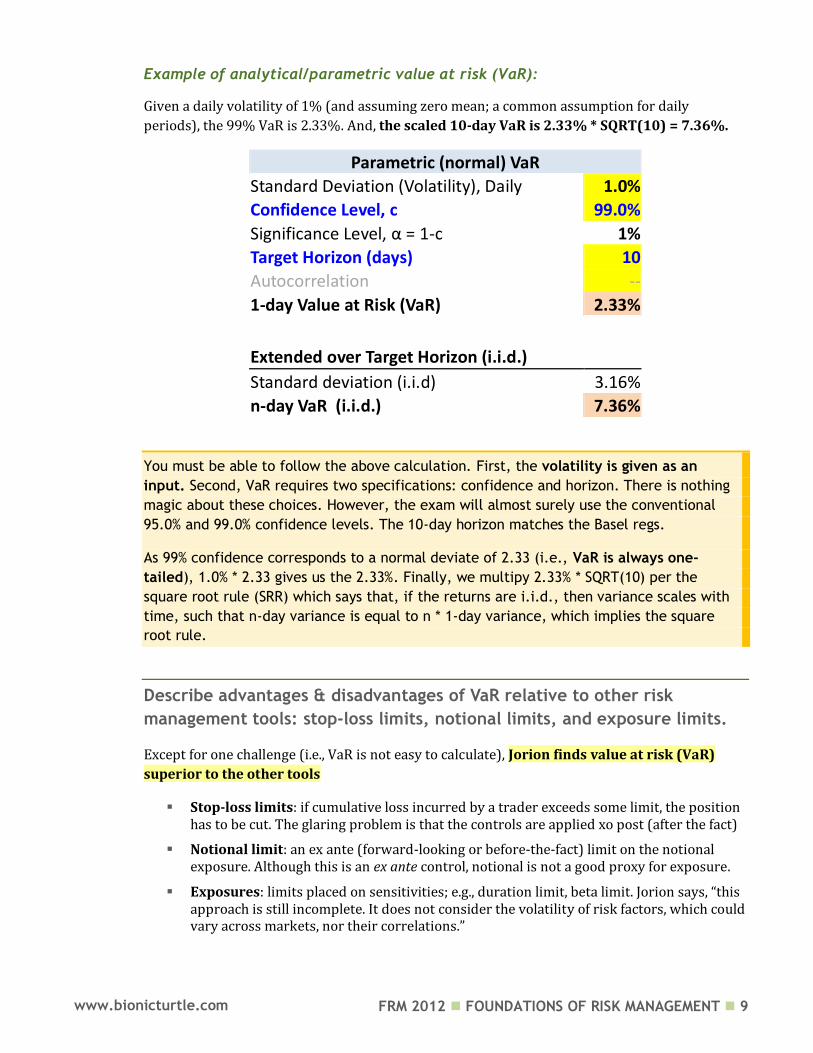

Example of analytical/parametric value at risk (VaR):

Given a daily volatility of 1% (and assuming zero mean; a common assumption for daily

periods), the 99% VaR is 2.33%. And, the scaled 10-day VaR is 2.33% * SQRT(10) = 7.36%.

Parametric (normal) VaR

Standard Deviation (Volatility), Daily 1.0%

Confidence Level, c 99.0%

Significance Level, α = 1-c 1%

Target Horizon (days) 10

Autocorrelation --

1-day Value at Risk (VaR) 2.33%

Extended over Target Horizon (i.i.d.) Standard deviation (i.i.d) 3.16%

n-day VaR (i.i.d.) 7.36%

You must be able to follow the above calculation. First, the volatility is given as an

input. Second, VaR requires two specifications: confidence and horizon. There is nothing

magic about these choices. However, the exam will almost surely use the conventional

95.0% and 99.0% confidence levels. The 10-day horizon matches the Basel regs.

As 99% confidence corresponds to a normal deviate of 2.33 (i.e., VaR is always one-

tailed), 1.0% * 2.33 gives us the 2.33%. Finally, we multipy 2.33% * SQRT(10) per the

square root rule (SRR) which says that, if the returns are i.i.d., then variance scales with

time, such that n-day variance is equal to n * 1-day variance, which implies the square

root rule.

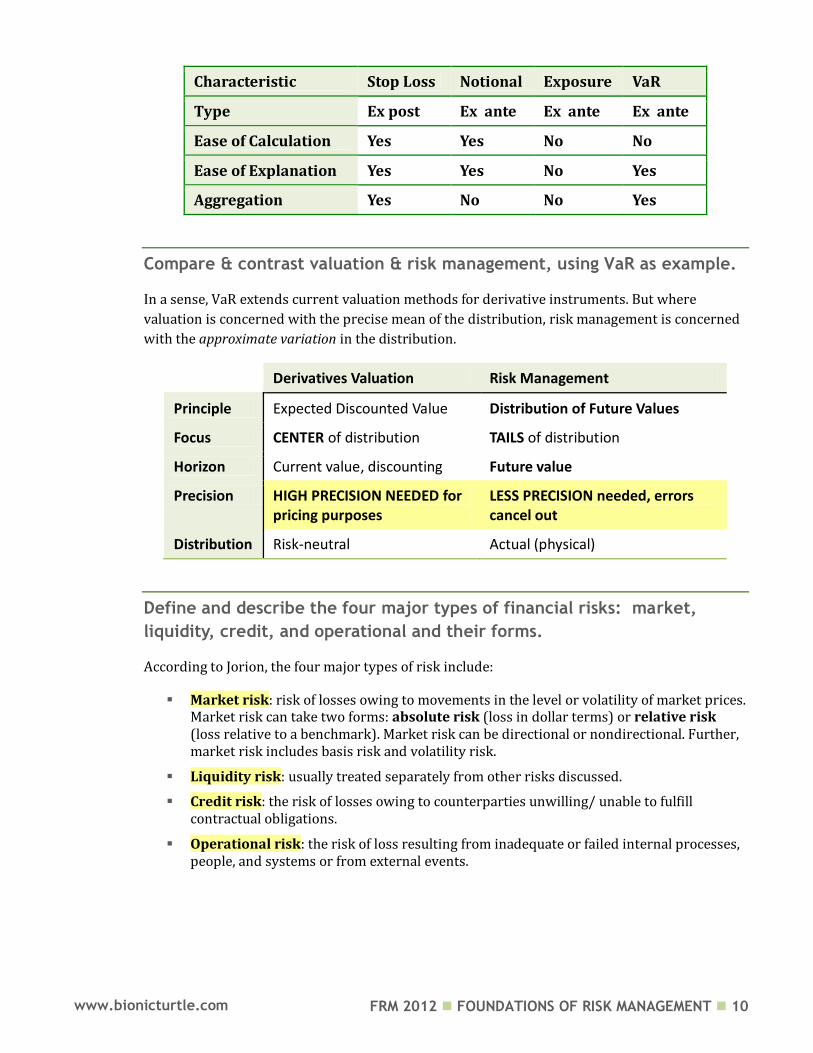

Describe advantages & disadvantages of VaR relative to other risk

management tools: stop-loss limits, notional limits, and exposure limits.

Except for one challenge (i.e., VaR is not easy to calculate), Jorion finds value at risk (VaR)

superior to the other tools

Stop-loss limits: if cumulative loss incurred by a trader exceeds some limit, the position has to be cut. The glaring problem is that the controls are applied xo post (after the fact)

Notional limit: an ex ante (forward-looking or before-the-fact) limit on the notional exposure. Although this is an ex ante control, notional is not a good proxy for exposure.

Exposures: limits placed on sensitivities; e.g., duration limit, beta limit. Jorion says, “this approach is still incomplete. It does not consider the volatility of risk factors, which could vary across markets, nor their correlations.”

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 10 www.bionicturtle.com

Characteristic Stop Loss Notional Exposure VaR

Type Ex post Ex ante Ex ante Ex ante

Ease of Calculation Yes Yes No No

Ease of Explanation Yes Yes No Yes

Aggregation Yes No No Yes

Compare & contrast valuation & risk management, using VaR as example.

In a sense, VaR extends current valuation methods for derivative instruments. But where

valuation is concerned with the precise mean of the distribution, risk management is concerned

with the approximate variation in the distribution.

Derivatives Valuation Risk Management

Principle Expected Discounted Value Distribution of Future Values

Focus CENTER of distribution TAILS of distribution

Horizon Current value, discounting Future value

Precision HIGH PRECISION NEEDED for pricing purposes

LESS PRECISION needed, errors cancel out

Distribution Risk-neutral Actual (physical)

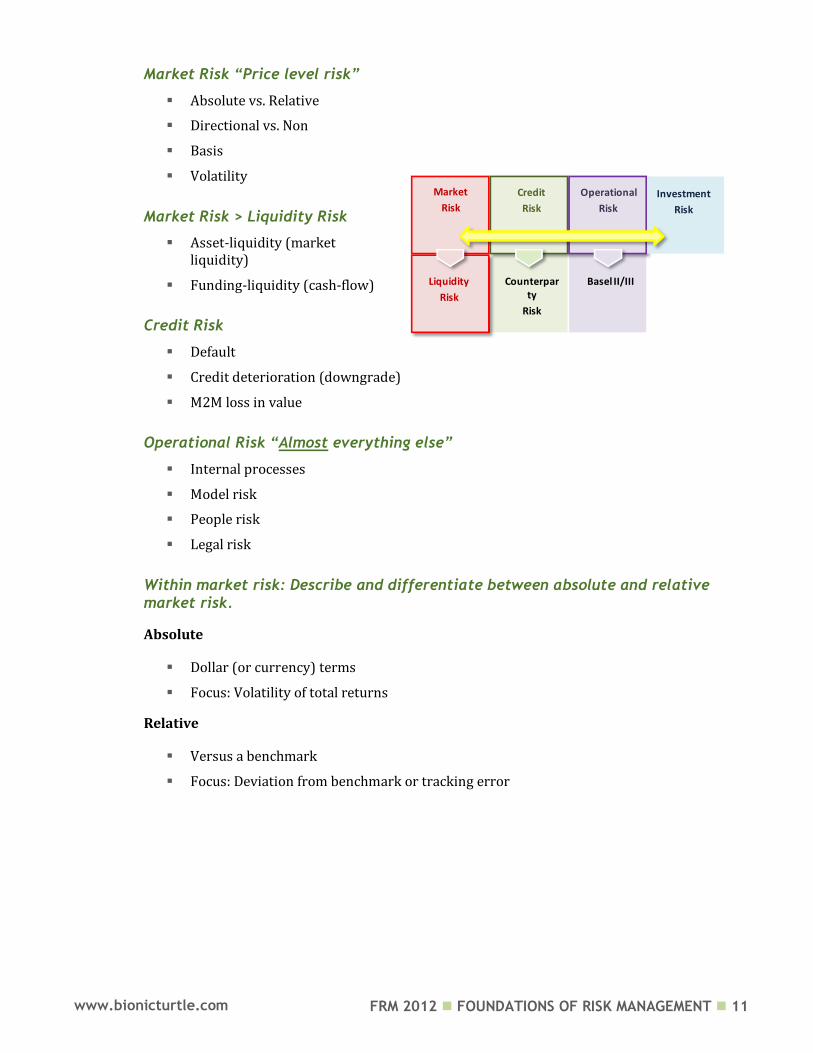

Define and describe the four major types of financial risks: market,

liquidity, credit, and operational and their forms.

According to Jorion, the four major types of risk include:

Market risk: risk of losses owing to movements in the level or volatility of market prices. Market risk can take two forms: absolute risk (loss in dollar terms) or relative risk (loss relative to a benchmark). Market risk can be directional or nondirectional. Further, market risk includes basis risk and volatility risk.

Liquidity risk: usually treated separately from other risks discussed.

Credit risk: the risk of losses owing to counterparties unwilling/ unable to fulfill contractual obligations.

Operational risk: the risk of loss resulting from inadequate or failed internal processes, people, and systems or from external events.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 11 www.bionicturtle.com

Operational

Risk

Credit

Risk

Basel II/IIICounterparty

Risk

Liquidity

Risk

Market

Risk

Investment

Risk

Market Risk “Price level risk”

Absolute vs. Relative

Directional vs. Non

Basis

Volatility

Market Risk > Liquidity Risk

Asset-liquidity (market liquidity)

Funding-liquidity (cash-flow)

Credit Risk

Default

Credit deterioration (downgrade)

M2M loss in value

Operational Risk “Almost everything else”

Internal processes

Model risk

People risk

Legal risk

Within market risk: Describe and differentiate between absolute and relative market risk.

Absolute

Dollar (or currency) terms

Focus: Volatility of total returns

Relative

Versus a benchmark

Focus: Deviation from benchmark or tracking error

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 12 www.bionicturtle.com

Within market risk: Describe and differentiate between directional and non-directional market risk.

Directional

Movements in financial variables. For example:

Stock price moves down,

Interest rates drop,

Commodity prices change

Non-directional

The risks that remain, including hedged positions

Nonlinear exposures,

Basis risk

Volatilities

Within market risk: Describe basis risk and its sources.

Basis risk refers to unanticipated movements in relative prices of assets in a hedged

position, such as cash and futures or interest-rate spreads are considered basis risk. In the case

of a forward contract, the basis is the difference between the forward price (F) and the spot

price (S). In theory, the forward and spot prices should converge, such that the basis should

approach zero as the contract approaches maturity. But this is only theoretical and depends on

an exact match in the commodity, perfect timing, other key assumptions (e.g., perfect liquidity)

and the absence of other frictions. A hedge is constructed based on an anticipation of the basis

(e.g., that the basis will converge to zero). Basis risk, then, is the risk that the hedge will not

perform as expected; i.e., that the hedge will not offset the loss in the primary position.

Time (T)S0

F0

ST-1

FT-1 F0ST

ST=FT

All hedges imply (at least some) basis risk: the risk the hedge will not exactly offset

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 13 www.bionicturtle.com

Basis risk is often underestimated but it is arguably one of the most important risks. All

hedges imply (at least some) basis risk: the risk the hedge will not exactly offset.

Recently in “Lessons from the Financial Crisis,” Goldman’s CEO said, “a lot of risk models

incorrectly assumed that positions could be fully hedged. After LTCM and the crisis in

emerging markets in 1998, new products like basket indices and credit default swaps

were created to help offset a number of risks. However, we didn’t, as an industry,

consider carefully enough the possibility that liquidity would dry up, making it difficult to

apply effective hedges.”

Within market risk: Describe volatility risk & sources.

Unanticipated movements in relative prices of assets in a hedged position, such as cash and

futures or interest-rate spreads

The classic instrument that represents a trade on volatility risk is a stock option. In fact,

options are motivated as instruments of volatility. Salih Neftci writes (in Principles of

Financial Engineering, 2nd Ed), “an option exposure, when fully put in place, is an impure

position on the way volatility is expected to change. A market maker with a net long

position in options is someone who is “expecting” the volatility to increase. A market

maker who is short the option is someone who thinks that the volatility of the underlying

is going to decrease.”

Within liquidity risk: Asset vs. funding liquidity risk.

Liquidity risk is typically divided into two different, but related, types: asset-liquidity risk (a.k.a.,

market/product-liquidity risk) and funding-liquidity risk (a.k.a., cash-flow risk). Both concern

the dilemma of not having enough time: liquidity risk implies that time can eventually solve the

problem. Funding liquidity risk refers to the inability to meet payment obligations or to fund

ongoing operations. “This is especially a problem for portfolios that are leveraged and subject to

margin calls from the lender.” Asset-liquidity risk refers to a transaction that cannot be

conducted at prevailing market prices “owing to the size of the position relative to normal

trading lots.” This is also simply when the position cannot be exited without steep discounting

(or, in the extreme case, a “fire sale”)

Asset-liquidity risk (market/product liquidity risk)

Cannot exit position at prevailing market prices due to size of the position

Varies by…

Asset class

Prevailing market conditions

Funding-liquidity risk (cash-flow risk)

Cannot meet payment obligations

Balance sheet issue, typically concern of CFO

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 14 www.bionicturtle.com

In the context of the credit crisis, much attention has been focused on the interrelationship

between asset and funding liquidity risk. Specifically, for example, the lack of asset liquidity can

trigger margin calls that create funding liquidity risk.

Within credit risk: Describe and differentiate between exposure and recovery rate.

Exposure (a.k.a., amount at risk) is the potential amount that can be lost. For example, if a bond

buyer invests $10 million dollars, then the investor’s exposure is $10 million. However, upon

default, the investor expects at least some partial recovery. The recovery rate (1 – loss given

default) is the proportion recovered. Recovery is also referred to as “cents on the dollar;” e.g.,

40% recovery is “40 cents on the dollar.”

Exposure (EAD)

Amount at risk

Recovery Rate

Proportion paid back to lender (cents on the dollar)

Asset-liquidity risk (market/product liquidity risk)

• Transaction cannot be conducted at prevailing market prices owing to size of the position

• Varies by…

• Asset class

• Prevailing market conditions

Funding-liquidity risk (cash-flow risk)

• Inability to meet payment obligations, which may force liquidation, transforming paper losses into realized losses

Crisis Lesson: Inter-

related

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 15 www.bionicturtle.com

C

M

Within credit risk: Describe credit event and how it may relate to market risk.

A credit event occurs when there is a change in the counterparty’s ability to perform its

obligations. According to Jorion, credit risk should be defined as the potential loss in mark-to-

market value incurred owing to a credit event.

Please pay careful attention: credit risk is not limited to default. Consistent with the

broad here definition in Jorion, De Servigny includes three sub-classes of credit risk in his

overview of credit risk models: default; rating migration; and change in spread.

Therefore, credit risk include both default risk and risk of credit deterioration.

Within credit risk: Describe sovereign risk and its sources.

Sovereign risk

Country-specific (unlike default risk which is generally company-specific)

Sources

Countries impose foreign-exchange controls that make it impossible for counterparties to honor their obligations

Within credit risk: Describe settlement risk and its sources

Settlement risk: when two payments are exchanged the same day. Risk that counterparty may

default after the institution already made its payment

Pre-settlement exposure: only netted value

On settlement day: full value of payments due

Jorion: Settlement risk is acute for foreign-exchange transactions

Within operational risk: Describe relationships between operational, market & credit risk

Operational risks can lead to market or credit risks

A settlement fail can create market risk because cost may depend on movement in market prices

Again important is the theme of the interdependence of risks. Although operational

risks are defined separately, the point is that operational losses cannot necessarily be

analyzed in isolation of market and credit risks.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 16 www.bionicturtle.com

Within operational risk: Describe model risk and its sources

Operational risk > Model risk

Model risk is risk of losses owing to the fact that valuation models may be flawed

“Very insidious” and requires intimate knowledge of modeling process

Model risk is “the risk of error in our estimated risk measures due to inadequacies (or

deficiencies) in our models. (Kevin Dowd)” Models are by definition quantitative but

this chapter largely concerns the qualitative conundrums posed by reliance on models.

Within operational risk: Describe people risk

Operational risk > People risk

People risk includes internal or external fraud

For example:

Rogue traders

Within operational risk: Describe legal risk and its sources

Operational risk > Legal risk

Legal risk arises from exposure to fines, penalties or punitive damages resulting from supervisory actions, as well as private settlements

Examples:

Counterparties sue to invalidate credit losses [related to credit risk]

Shareholders lawsuits against corporations

What is excluded from operational risk?

Strategic risk

Business risk

Reputational risk (controversial)

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 17 www.bionicturtle.com

Stulz Chapter 3:

Creating Value with

Risk Management

In this chapter…

Explain how risk management can create value by handling bankruptcy costs. Explain how risk management can create value moving income across time and

reducing taxes. Describe how risk reduction benefiting a large shareholder may increase or

decrease firm value. Explain the relationship between risk management, managerial incentives, and

the structure of management compensation, and its effect on firm value. Describe debt overhang, and explain how risk management can increase firm

value by reducing the probability of debt overhang. Explain how risk management can reduce the problem of information

asymmetry and increase firm value.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 18 www.bionicturtle.com

Stulz Chapter 3 realizes imperfect markets and concludes risk management can add value

Perfect financial markets risk management cannot create value

Markets are not perfect! Imperfections (and frictions) imply risk management can create value

Capital structure (financial distress)

Taxes

Agency and information asymmetries

Explain how risk management can create value by handling bankruptcy

costs.

Debt is cheaper than equity. In theory, then, firm value increases as the firm increases its financial

leverage (ratio of debt/equity or debt/total assets). However, higher leverage also increases the

probability of bankruptcy (and default) and incurs a “cost of financial distress.”

In summary:

Equity is more expensive than debt due to (i) subordinate claim and (ii) tax shield on debt

Ceteris paribus, the firm would prefer to increase leverage to lower its weighted average cost of capital (WACC)

However, the “friction” is the cost of financial distress: as leverage increases, beyond some point, the cost of equity and debt both increase due to the threat of default and bankruptcy

NoFriction

PerfectCompetition

PerfectInformation

Cost ofFinancialDistress

InformationAsymmetry

Taxest(friction!)

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 19 www.bionicturtle.com

Generally, interest paid by a company is tax-deductible. The tax savings achieved by the use of

debt is called the tax shield. All other things being equal, a firm that uses debt saves cash taxes

and decreases its weighted average cost of capital.

However, at a certain point, using more debt becomes counterproductive because debt carries a

fixed obligation and increases the risk of default. This is the essential trade-off: as they increase

their leverage (i.e., ratio of debt-to-equity), firms increase their tax shield but also increase the

present value of costs of financial distress. The optimal capital structure of a firm balances the

tax benefits of debt against the costs of financial distress.

A firm can reduce the present value of the costs of financial distress through risk management

by making financial distress less likely. As a result, it can take on more debt. Risk management

enables the firm to have a higher debt level, and hence a greater tax shield from debt, for any

likelihood of financial distress.

If a firm carries a risk of bankruptcy, then it incurs bankruptcy costs (e.g., as reflected in higher

interest expense). In this case, the irrelevance theorem does not hold. The present value of this

firm can be reduced by the present value of the bankruptcy costs, as follows:

Value of firm = PV(Cash flow) – PV (bankruptcy costs)

If the cost to hedge bankruptcy risk is zero (or even if it is merely less than the bankruptcy

costs), risk management creates value because the market will bear the diversifiable risk. In fact,

if the risk is diversifiable (i.e., non-systematic), the capital markets should be able to bear the

risk with zero cost. In this case, gains from risk management equal present value of the

bankruptcy costs:

Gain from risk mgmt = Value of hedged firm − Value of un-hedged firm = Present Value (bankruptcy costs)

- 2,000 4,000 6,000 8,000

10,000 12,000 14,000

0.13 0.36 0.55 0.70 0.84 0.95

Firm value(FCF/WACC)

Firm value - PV(cost of financialdistress)

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 20 www.bionicturtle.com

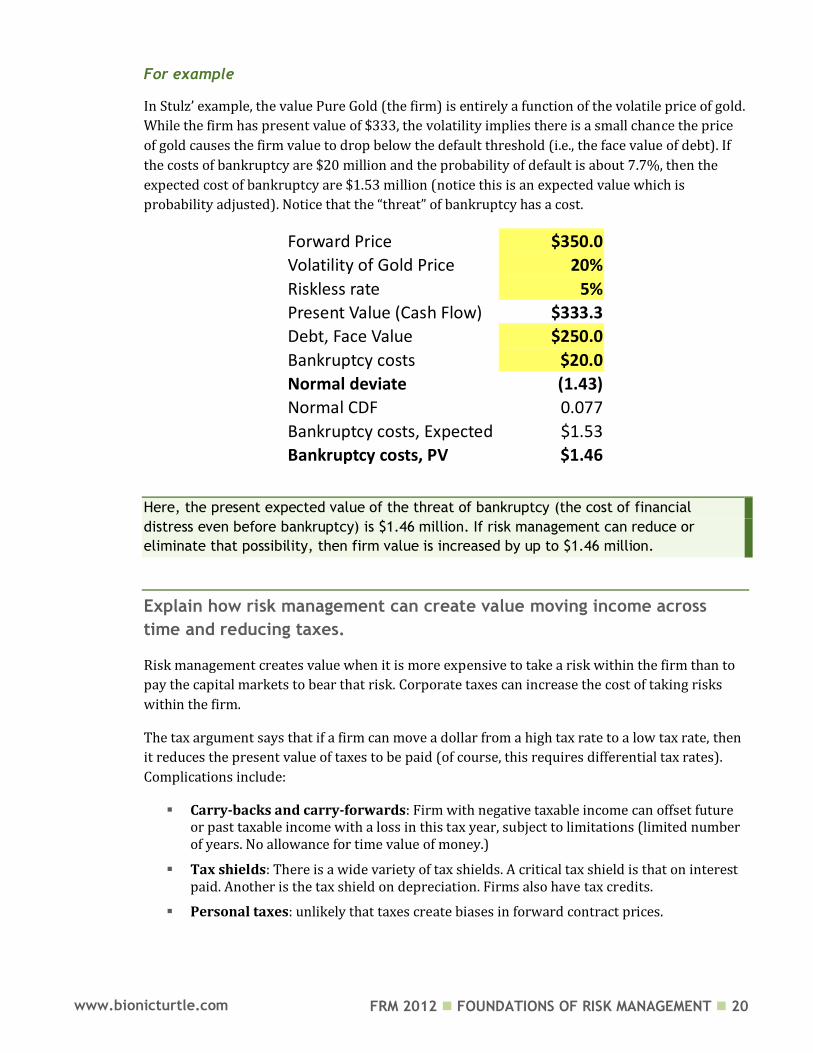

For example

In Stulz’ example, the value Pure Gold (the firm) is entirely a function of the volatile price of gold.

While the firm has present value of $333, the volatility implies there is a small chance the price

of gold causes the firm value to drop below the default threshold (i.e., the face value of debt). If

the costs of bankruptcy are $20 million and the probability of default is about 7.7%, then the

expected cost of bankruptcy are $1.53 million (notice this is an expected value which is

probability adjusted). Notice that the “threat” of bankruptcy has a cost.

Forward Price $350.0

Volatility of Gold Price 20%

Riskless rate 5%

Present Value (Cash Flow) $333.3

Debt, Face Value $250.0

Bankruptcy costs $20.0

Normal deviate (1.43) Normal CDF 0.077

Bankruptcy costs, Expected $1.53

Bankruptcy costs, PV $1.46

Here, the present expected value of the threat of bankruptcy (the cost of financial

distress even before bankruptcy) is $1.46 million. If risk management can reduce or

eliminate that possibility, then firm value is increased by up to $1.46 million.

Explain how risk management can create value moving income across

time and reducing taxes.

Risk management creates value when it is more expensive to take a risk within the firm than to

pay the capital markets to bear that risk. Corporate taxes can increase the cost of taking risks

within the firm.

The tax argument says that if a firm can move a dollar from a high tax rate to a low tax rate, then

it reduces the present value of taxes to be paid (of course, this requires differential tax rates).

Complications include:

Carry-backs and carry-forwards: Firm with negative taxable income can offset future or past taxable income with a loss in this tax year, subject to limitations (limited number of years. No allowance for time value of money.)

Tax shields: There is a wide variety of tax shields. A critical tax shield is that on interest paid. Another is the tax shield on depreciation. Firms also have tax credits.

Personal taxes: unlikely that taxes create biases in forward contract prices.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 21 www.bionicturtle.com

For example

Pure Gold (the firm) will achieve pre-tax profit of either $250 million (50% probability) or $450

million (50% probability). The simplified tax schedule is such that 50% taxes are paid only if the

pre-tax cash flow exceeds $300 million; no taxes otherwise. Alternatively, Pure Gold can sell its

gold forward at $350; note this is the same as the expected (average) value of the future spot

price. After-tax cash flow is higher for the hedged firm:

Tax Schedule

RF Rate 5%

Cash Flow < $299.0 0%

Cash Flow > $300.0 50%

Future

After-tax

Spot (S1) Tax FV PV

Probability 50% $250.0 $0.0 $250.0 Probability 50% $450.0 $75.0 $375.0 Expected

$350.0 $37.5 $312.5 $297.6

Forward

After-tax

(F0)

FV PV

$350.0 $25.0 $325.0 $309.5

If a firm can move a dollar from a high tax rate to a low tax rate, then it reduces the

present value of taxes to be paid

Describe how risk reduction benefiting a large shareholder or stakeholder

may increase or decrease firm value.

A large shareholder can engage in monitoring.

Evaluate management actions

Influence incentives (e.g., bonus plans, stock options)

Explain the relationship between risk management, managerial

incentives, and management compensation, and its effect on firm value.

Agency problem

Management acts in their own interest instead of shareholders’ interests (e.g., “empire building”)

How to solve? Incentives (e.g., stock options) try to provide alignment between management actions (and decisions) with shareholder welfare.

But practice is more difficult

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 22 www.bionicturtle.com

Authors argue for:

Tying compensation to some measure of value

creation

Share ownership

Describe debt overhang and explain how risk management can increase

firm value by reducing the probability of debt overhang.

Debt overhang is too much debt: To increase shareholder value may not increase firm value!

Induces shareholders seek negative NPV projects, and/or

Avoid investing in valuable projects because they dilute

Consequently, risk management that reduces this probability increases firm value today.

Rate 5% Gold $5 Invest,

HLG Debt $400.0 Price Payoff of:

$10

Probability 50% $250.0 $260.0

Probability 50% $450.0 $460.0

Value of Debt:

50% $250.0 $260.0

50% $400.0 $400.0

FV $325.0 $330.0

PV $309.5 $314.3

Value of Equity:

50% $0.0 $0.0

50% $50.0 $60.0

FV $25.0 $30.0

PV $23.81 $28.6

Value of Firm (D+E) $333.3 $342.9

Increase in Equity Value $4.8

Existing Equity DILUTED to: $23.571

Principal-Agent (Agency) is a key friction in Subprime Crisis

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 23 www.bionicturtle.com

Explain how risk management can reduce the problem of information

asymmetry and increase firm value.

Information asymmetry: one party (management) knows more than the other (outside investor)

Problem for management raising funds managers know more about firms’ projects than outsiders

Ways to reduce the costs of managerial discretion (and therefore reduce the costs of the funds)

Sit large shareholder on board; e.g., private equity fund

Borrow against assets rather than against future project.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 24 www.bionicturtle.com

Elton, Chapter 5:

Delineating

Efficient Portfolios

In this chapter…

Calculate the expected return and volatility of a portfolio of risky assets. Explain how covariance and correlation affect the expected return and volatility

of a portfolio of risky assets. Describe the shape of the portfolio possibilities curve. Define the minimum variance portfolio. Define the efficient frontier and describe the impact on it of various

assumptions concerning short sales and borrowing.

Calculate the expected return and volatility of a portfolio of risky assets.

Expected return

The expected return on a portfolio of two assets is given by

P A A B BR X R X R , fraction of portfolio held in asset A, asset B

, , expected return on asset A, asset B, portfolio

A B

A B P

X X

R R R

Volatility of a portfolio of risky assets The expected return on a portfolio of two assets is given by

1 22 2 2 2(1 ) 2 (1 )P A A A B A A ABX X X X

Please note we can replace the covariance with the product of the correlations and the standard

deviations:

1 22 2 2 2(1 ) 2 (1 )P A A A B A A AB A BX X X X

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 25 www.bionicturtle.com

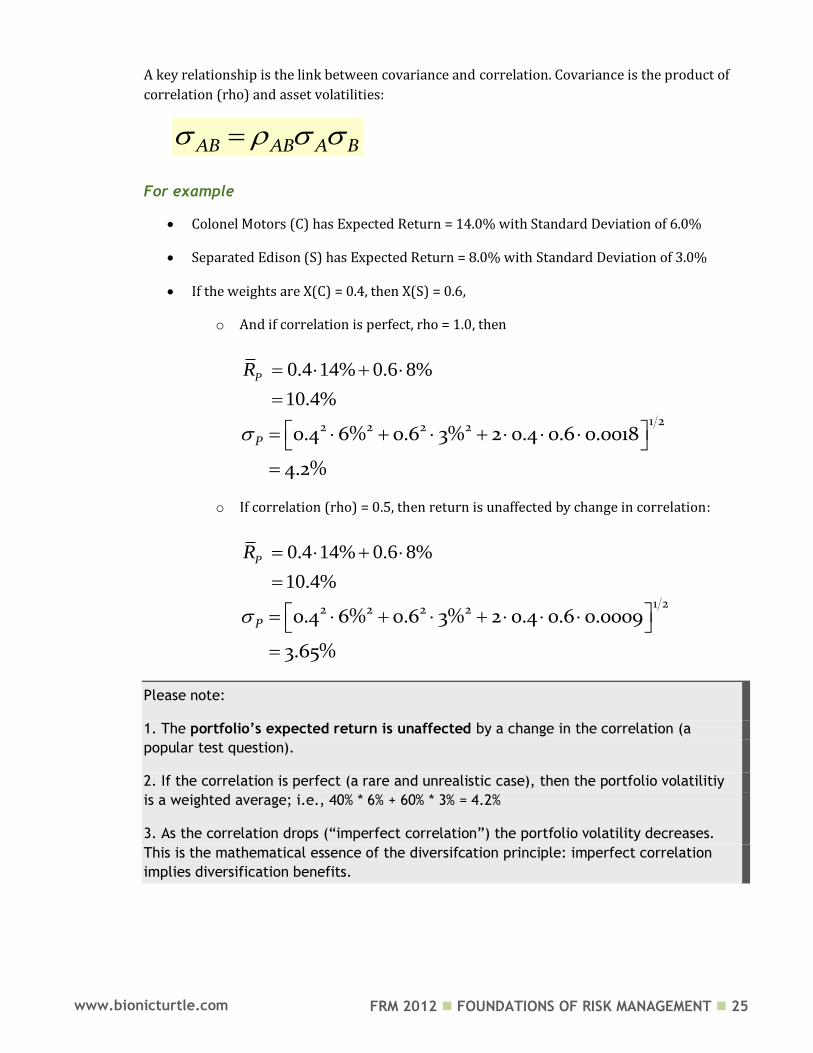

A key relationship is the link between covariance and correlation. Covariance is the product of

correlation (rho) and asset volatilities:

AB AB A B

For example

Colonel Motors (C) has Expected Return = 14.0% with Standard Deviation of 6.0%

Separated Edison (S) has Expected Return = 8.0% with Standard Deviation of 3.0%

If the weights are X(C) = 0.4, then X(S) = 0.6,

o And if correlation is perfect, rho = 1.0, then

0.4 14% 0.6 8%

10.4%

PR

1 22 2 2 20.4 6% 0.6 3% 2 0.4 0.6 0.0018

4.2%

P

o If correlation (rho) = 0.5, then return is unaffected by change in correlation:

0.4 14% 0.6 8%

10.4%

PR

1 22 2 2 20.4 6% 0.6 3% 2 0.4 0.6 0.0009

3.65%

P

Please note:

1. The portfolio’s expected return is unaffected by a change in the correlation (a

popular test question).

2. If the correlation is perfect (a rare and unrealistic case), then the portfolio volatilitiy

is a weighted average; i.e., 40% * 6% + 60% * 3% = 4.2%

3. As the correlation drops (“imperfect correlation”) the portfolio volatility decreases.

This is the mathematical essence of the diversifcation principle: imperfect correlation

implies diversification benefits.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 26 www.bionicturtle.com

Explain how covariance & correlation affect the expected return and

volatility of a portfolio of risky assets.

Assume two assets with expected returns and standard deviations. The riskless rate is 4.0%.

Riskless rate 4.00%

Asset A

Expected Return 14.00%

Standard Deviation 20.00%

Variance 0.0400

Asset B

Expected Return 4.00%

Standard Deviation 10.00%

Variance 0.0100

The portfolio that includes these two assets has a risk/return profile that varies according to the

correlation (different weights between the assets will “move you along a line.”)

According to Stock & Watson

The lower (closer to -1.0) the correlation coefficient between assets, all other attributes

held constant, the higher the payoff from diversification.

The combinations of two assets can never have more risk than that found on a straight

line connecting the two assets in expected return standard deviation space.

0.0%

5.0%

10.0%

15.0%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Exp

ect

ed

Re

turn

Standard Deviation

Portfolio Possibilities Curve Given Various Correlation Assuptions

From -1.0 to +1.0

-1.00

-0.50

0.00

0.50

1.00

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 27 www.bionicturtle.com

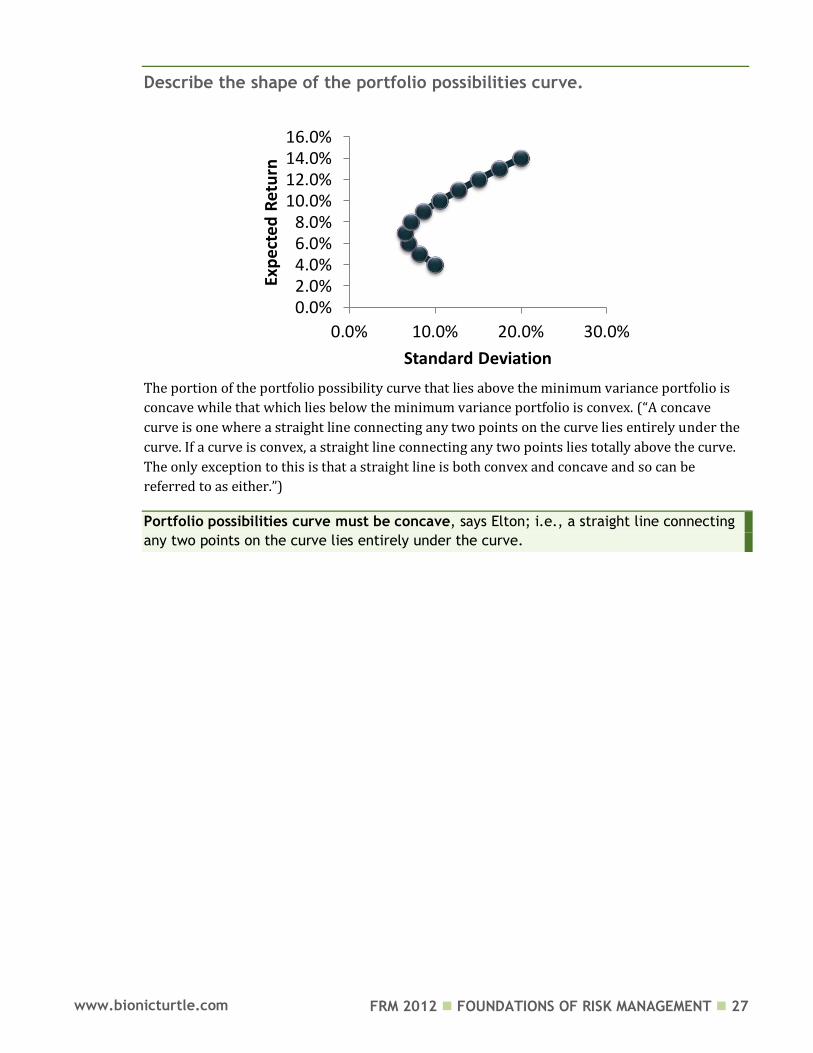

Describe the shape of the portfolio possibilities curve.

The portion of the portfolio possibility curve that lies above the minimum variance portfolio is

concave while that which lies below the minimum variance portfolio is convex. (“A concave

curve is one where a straight line connecting any two points on the curve lies entirely under the

curve. If a curve is convex, a straight line connecting any two points lies totally above the curve.

The only exception to this is that a straight line is both convex and concave and so can be

referred to as either.”)

Portfolio possibilities curve must be concave, says Elton; i.e., a straight line connecting

any two points on the curve lies entirely under the curve.

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%

0.0% 10.0% 20.0% 30.0%

Exp

ecte

d R

etu

rn

Standard Deviation

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 28 www.bionicturtle.com

Define the (global) minimum variance portfolio.

The (global) minimum variance portfolio is not the “best” portfolio; i.e., it is not the

portfolio with the highest Sharpe ratio.

Although not assigned, we can solve for the minimum variance portfolio. We can solve by setting

first partial derivative equal to zero (i.e., where slope of tangent is flat):

mvp

2

mvp 2 2

0

2

PA

A

B AB A BA

A B AB A B

XX

X

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0.0% 10.0% 20.0% 30.0%

Exp

ecte

d R

etu

rn

Standard Deviation

Minimum variance

Most efficient

(highest excess

return/volatility)

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 29 www.bionicturtle.com

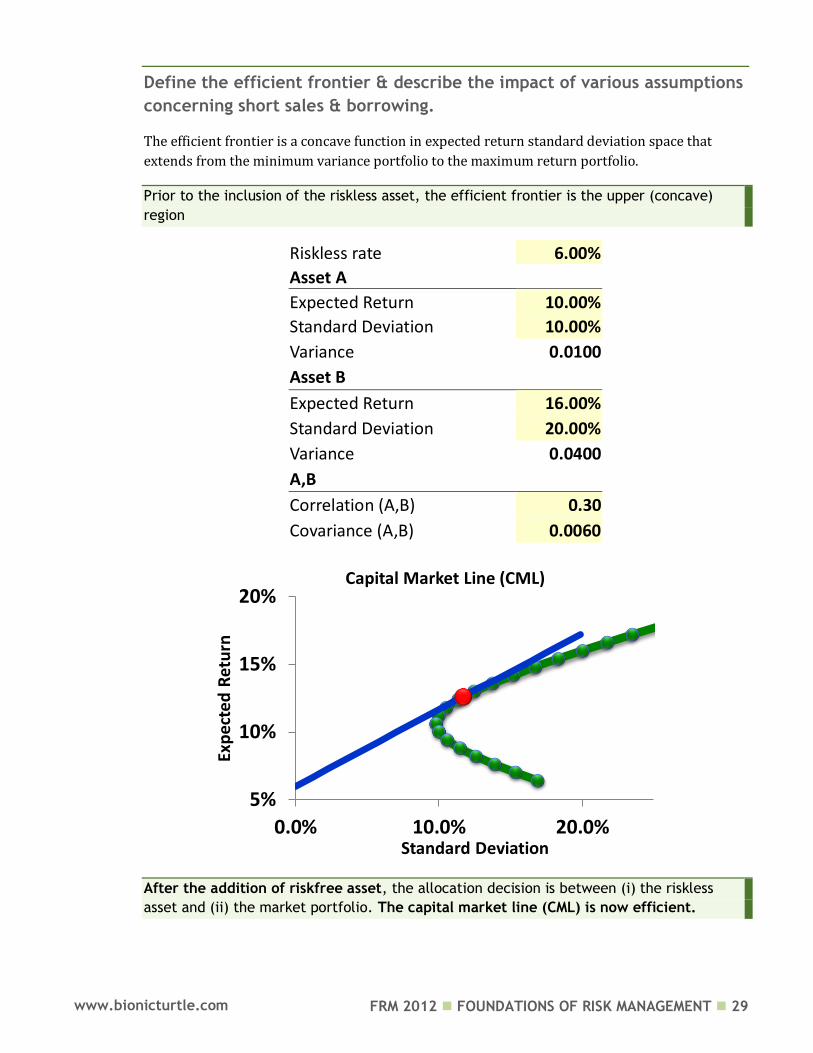

Define the efficient frontier & describe the impact of various assumptions

concerning short sales & borrowing.

The efficient frontier is a concave function in expected return standard deviation space that

extends from the minimum variance portfolio to the maximum return portfolio.

Prior to the inclusion of the riskless asset, the efficient frontier is the upper (concave)

region

Riskless rate 6.00%

Asset A

Expected Return 10.00%

Standard Deviation 10.00%

Variance 0.0100

Asset B

Expected Return 16.00%

Standard Deviation 20.00%

Variance 0.0400

A,B

Correlation (A,B) 0.30

Covariance (A,B) 0.0060

After the addition of riskfree asset, the allocation decision is between (i) the riskless

asset and (ii) the market portfolio. The capital market line (CML) is now efficient.

5%

10%

15%

20%

0.0% 10.0% 20.0%

Exp

ecte

d R

etu

rn

Standard Deviation

Capital Market Line (CML)

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 30 www.bionicturtle.com

With short sales

With short sales, portfolios exist that give infinite expected rates of return.

With the introduction of the riskfree borrowing and lending

Before the introduction of riskfree borrowing and lending, the efficient frontier is the non-

linear segment starting at the global minimum variance portfolio and extending up (superior

portfolios dominate) throughout the market portfolio. But these portfolios, which lie on the non-

linear curve, are risky portfolios with—as we progress up and to the right—higher risk and

higher return. (Elton: “Up to this point we have been dealing with portfolios of risky assets.”)

Then the riskless asset is introduced: “We can consider lending at a riskless rate as investing in

an asset with a certain outcome (e. g., a short- term government bill or savings account).

Borrowing can be considered as selling such a security short; thus borrowing can take place at

the riskless rate.”

Combinations of any security or portfolio and riskless lending and borrowing lie along a

straight line in expected return standard deviation of return space.

A FC F C

A

R RR R

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 31 www.bionicturtle.com

Elton, Chapter 13:

The Standard Capital

Asset Pricing Model

In this chapter …

Understand the derivation and components of the CAPM. Describe the assumptions underlying the CAPM. Describe the capital market line. Use the CAPM to calculate the expected return on an asset.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 32 www.bionicturtle.com

Understand the derivation and components of the CAPM.

CAPM says that expected return is a linear function of systemic risk (beta)

Expected excess return = (price of risk) * (quantity of risk)

i F i M FR R R R

Equivalent formulation for CAPM:

Since beta is equal to covariance [security return, market return] / market return variance, an

equivalent expression is given by:

2

2

iMi

M

M F iMi F

M M

M FF iM

M

R RR R

R RR

Price of risk (MRP, ERP)

Quantity of risk

0%

5%

10%

15%

20%

25%

0.00 1.00 2.00 3.00

Exp

ecte

d R

etu

rn

Beta (quantity of systemic risk]

Security Market Line (SML)

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 33 www.bionicturtle.com

Describe the assumptions underlying the CAPM.

No transaction costs.

There is no cost (no friction) to buy or sell any asset. To include transaction costs in the model

adds much complexity. Whether it is worthwhile introducing this complexity depends on the

importance of transaction costs to investors’ decisions. Given the size of transaction costs, they

are probably of minor importance.

Assets are infinitely divisible.

Investors could take any position in an investment, regardless of the size of their wealth. For

example, they can buy one dollar’s worth of IBM stock.

Absence of personal income tax.

Implies investor (individual) is indifferent to dividends versus capital gains.

Perfect competition (individuals are “price-takers”)

An individual cannot affect the price of a stock by his/her buying or selling action. This is

analogous to the assumption of perfect competition. While no single investor can affect prices by

an individual action, investors in total determine prices by their actions.

Mean-variance framework.

Investors are make decisions solely in terms of expected values and standard deviations. of the

returns on their portfolios.

First (mean) and second (variance or standard deviation) moments only

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 34 www.bionicturtle.com

Unlimited short sales allowed.

Individual investor can sell short any amount of any shares.

Unlimited lending and borrowing at the riskless rate.

Investor can lend or borrow any amount of funds desired at a rate of interest equal to the rate

for riskless securities.

Homogeneity of expectations: single period

All investors are assumed to define the relevant period in exactly the same manner.

Investors are concerned with the mean and variance of returns (or prices over a single period)

and all investors are assumed to define the relevant period in exactly the same manner.

Homogeneity of expectations: identical expectations.

All investors are assumed to have identical expectations with respect to the necessary inputs to

the portfolio decision: expected returns, variance of returns, and the (pairwise) correlation

matrix.

All assets are marketable.

All assets, including human capital, can be sold and bought on the market.

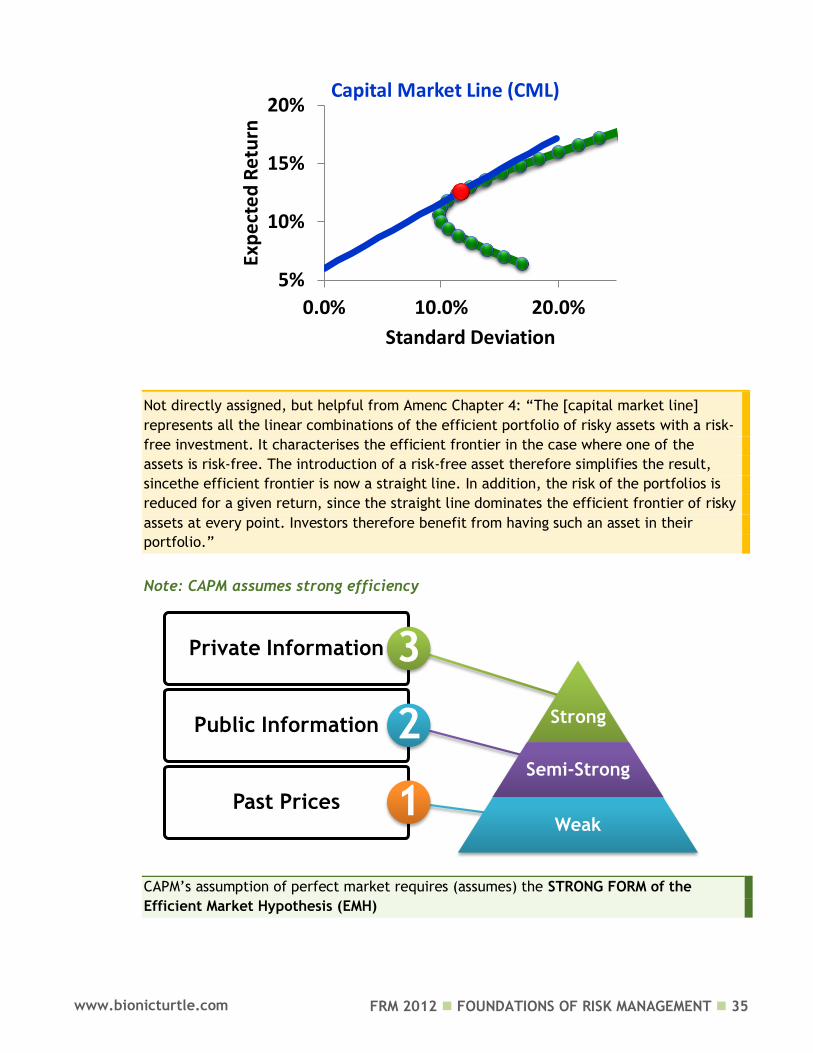

Describe the capital market line.

The capital market line (CML) is the set of optimal portfolios: a linear combination of (i) the

market portfolio and (ii) the risk-free asset

From Elton’s Conclusion: “We have discussed the Sharpe– Lintner– Mossin form of a

general equilibrium relationship in the capital markets. This model, usually referred to as

the capital asset pricing model or standard CAPM … we have shown that, under the

assumptions of the CAPM, the only portfolio of risky assets that any investor will own is

the market portfolio. Recall that the market portfolio is a portfolio in which the fraction

invested in any asset is equal to the market value of that asset divided by the market

value of all risky assets. Each investor will adjust the risk of the market portfolio to his or

her preferred risk- return combination by combining the market portfolio with lending or

borrowing at the riskless rate. This leads directly to the two mutual fund theorem. The

two mutual fund theorem states that all investors can construct an optimum portfolio by

combining a market fund with the riskless asset. Thus, all investors will hold a portfolio

along the [straight] line connecting [the riskfree rate] with the [market portfolio] in

expected return, standard deviation of return space.”

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 35 www.bionicturtle.com

Not directly assigned, but helpful from Amenc Chapter 4: “The [capital market line]

represents all the linear combinations of the efficient portfolio of risky assets with a risk-

free investment. It characterises the efficient frontier in the case where one of the

assets is risk-free. The introduction of a risk-free asset therefore simplifies the result,

sincethe efficient frontier is now a straight line. In addition, the risk of the portfolios is

reduced for a given return, since the straight line dominates the efficient frontier of risky

assets at every point. Investors therefore benefit from having such an asset in their

portfolio.”

Note: CAPM assumes strong efficiency

CAPM’s assumption of perfect market requires (assumes) the STRONG FORM of the

Efficient Market Hypothesis (EMH)

Private Information

Strong Public Information

3

Semi-Strong

Past Prices

2

Weak 1

5%

10%

15%

20%

0.0% 10.0% 20.0%

Exp

ect

ed

Re

turn

Standard Deviation

Capital Market Line (CML)

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 36 www.bionicturtle.com

Use the CAPM to calculate the expected return on an asset.

Assume that the following assets are correctly priced according to the security market line.

Derive the security market line.

What is the expected return on an asset with a Beta of 2.0 (Elton Question 13.1)?

1 1

2 2

6% 0.5

12% 1.5

R

R

Answer:

12% 1.5

6% 0.5

6% 3%

F

F

F

R MRP

R MRP

MRP R

2.0

3% 6%

3% 6% 2 15%

R

R

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 37 www.bionicturtle.com

Elton, Chapter 14:

Nonstandard Forms of Capital

Asset Pricing Models

In this chapter…

Describe the impact on the CAPM of the following: Short sales disallowed Riskless lending and borrowing Personal taxes Nonmarketable assets Heterogeneous expectations Non-price-taking behavior

Describe the following multi-period versions of CAPM: Consumption-oriented CAPM CAPM including inflation Multi-beta CAPM

Describe the impact on the CAPM of the following:

In this reading, unrealistic assumptions in the CAPM (on the left, below) are variously replaced

by more realistic assumptions (on the right, below):

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 38 www.bionicturtle.com

Describe the impact on the CAPM of the following: Short sales disallowed The allowance of short-sales is a convenient assumption that simplifies the derivation math, but

it is not a necessary assumption: if short sales are disallowed, exactly the same CAPM result

is obtained.

Elton: “Short sales were defined in the broadest sense of the term in that the investor

was allowed to sell any security (whether owned or not) and to use the proceeds to buy

any other security. This was a convenient assumption and it simplified the mathematics

of the derivation, but it was not a necessary assumption. Exactly the same result would

have been obtained had short sales been disallowed. The economic intuition behind this

is quite simple. In the CAPM framework all investors hold the market portfolio in

equilibrium. Since in equilibrium no investor sells any security short, prohibiting short

selling cannot change the equilibrium. Thus, the same CAPM relationship would be

derived irrespective of whether short sales are allowed or prohibited.”

Describe the impact on the CAPM of the following: No Riskless lending and

borrowing

If we assume there is neither riskless lending nor borrowing, CAPM still applies except

borrowing (lending) at the riskfree asset is replaced by shorting (going long) the zero-

beta portfolio. This is the zero-beta CAPM; also referred to as the two-factor model:

( )

expected return on zero-beta portfolio

i Z M Z i

Z

R R R R

R

No riskless lending/borrowing leads to Zero-beta CAPM

Elton: “Under the zero-beta CAPM (i.e., no riskless lending and borrowing), all investors

no longer hold the same portfolio in equilibrium. This is comforting for it is more

consistent with observed behavior. Of less comfort is that investors still hold most

securities (either long or short) and hold many securities short. In the case where neither

lending nor borrowing is allowed, we have a two mutual fund theorem. In the case where

riskless lending is allowed, we have a three mutual fund theorem. As in the case of the

simple CAPM, we still get a security market line. In addition, many of the implications

of this relationship are the same. For risky assets or portfolios, expected return is still a

linearly increasing function of risk as measured by Beta. It is only market risk that affects

the return on individual risky securities and portfolios of risky securities. On these

securities the investor gains no extra return from bearing diversifiable risk. In fact, the

only difference lies in the intercept and slope of the security market line.”

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 39 www.bionicturtle.com

Describe the impact on the CAPM of the following: Personal taxes

The simple form of the CAPM ignores taxes, which therefore assumes that investors are

indifferent between capital gain and dividend income; and that all investors hold the same

portfolio of risky assets.

If we introduce taxes, including the assumption that capital gains are taxed, in general, at a

lower rate than dividends, the equilibrium prices should change. Investors will evaluate after-

tax risk and return. This implies that, even with homogeneous expectations about the before-tax

return on a portfolio, the relevant (after-tax) efficient frontier faced by each investor will be

different. However, a general equilibrium relationship should still exist since, in the

aggregate, markets must clear.

( )

dividend yield of market portfolio

dividend yield for stock i

tax factor

i F i M F M F i F

M

i

E R R E R R R R

After the more realistic introduction of personal taxes: although each investor new looks

at a different efficient frontier, markets still clear to (more complex) general

equilibrium

Describe the impact on the CAPM of the following: Nonmarketable assets

Human capital is an example of a nonmarketable asset

Adding nonmarketable assets leads to a general equilibrium relationship of the same

form as the simple model that excluded nonmarketable assets. However, the market trade-

off between return and risk is different, as is the measure of risk for any asset.

The equilibrium return for an asset can be either higher or lower than it is under the standard form of the CAPM

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 40 www.bionicturtle.com

Describe the impact on the CAPM of the following: Heterogeneous

expectations

CAPM assumes homogenous expectations: all investors have the same inputs (expected

returns, variances [of returns], and covariance/correlation matrix)

If we relax this assumption to allow for the (certainly!) more realistic assumption that investors

have heterogeneous expectations, equilibrium can still be expressed in terms of expected

returns, covariances, and variance, but now these returns, covariances, and variances are

complex weighted averages of the estimates held by different individuals

Describe the impact on the CAPM of the following: Non-price-taking

behavior

Elton: “Lindenberg finds the price affector will hold less of the riskless asset (will be less of a risk

avoider) than [otherwise]. By doing so the price affector increases utility. “

Because the price affector still holds a combination of the riskless asset and the market portfolio,

we still get the simple form of the CAPM, but the market price of risk is lower than it

would be if all investors were price takers.

One of the CAPM assumptions is that markets are perfectly compeitive; that is, the

individuals are price-takers. Relaxing this assumption implies the idea that some investors

(e.g., large mutual or pension funds) believe their trades impact price.

Describe the following multi-period versions of CAPM: Consumption-

oriented CAPM

A number of authors have taken a different approach to defining equilibrium in the capital

markets. They start with a set of assumptions:

Investors maximize a multiperiod utility function for lifetime consumption;

Investors have homogeneous beliefs concerning return characteristics of assets;

There is an infinitely lived fixed population;

There is a single consumption good; and

There exists a capital market that allows investors to reach a consumption pattern such that they cannot jointly fare better by additional trades.

The authors are able to show, under these assumptions, that return on assets should be

linearly related to the growth rate in aggregate consumption if the parameters of the linear

relationship can be assumed constant over time.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 41 www.bionicturtle.com

This model is directly analogous to the simple form of the CAPM, except the growth rate of per

capita consumption replaces the rate of return on the market portfolio.

1

1 market price of the consumption beta

expected return on portfolio with

zero consumption beta

i Z i

i

R R

Describe the following multi-period versions of CAPM: CAPM including

[uncertain] inflation

Equilibrium is similar to the simple form of the CAPM, but both the definition of the market price

of risk and the risk on an asset are modified.

As long as the correlation between the rate of return on the market and the rate of inflation is positive, the market price of risk is higher than that depicted in the standard CAPM.

Risk of any asset is not just a function of its covariance with the market; it is also a function of its

covariance with the rate of inflation.

If an asset’s rate of return is positively correlated with the rate of inflation, the standard CAPM formulation overstates the risk of the asset.

Describe the following multi-period versions of CAPM: Multi-beta CAPM

Multi-beta CAPM says expected return is a function of (related to) several sensitivities.

1 1 2 2 ...

i F

iM M F il l F il l F

R R

R R R R R R

For example:

i F

iM M F il ll F

R R

R R R R

Price of inflation risk

Sensitivity to inflation risk

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 42 www.bionicturtle.com

Elton, Chapter 16:

Arbitrage Pricing

Model (APT)

In this chapter…

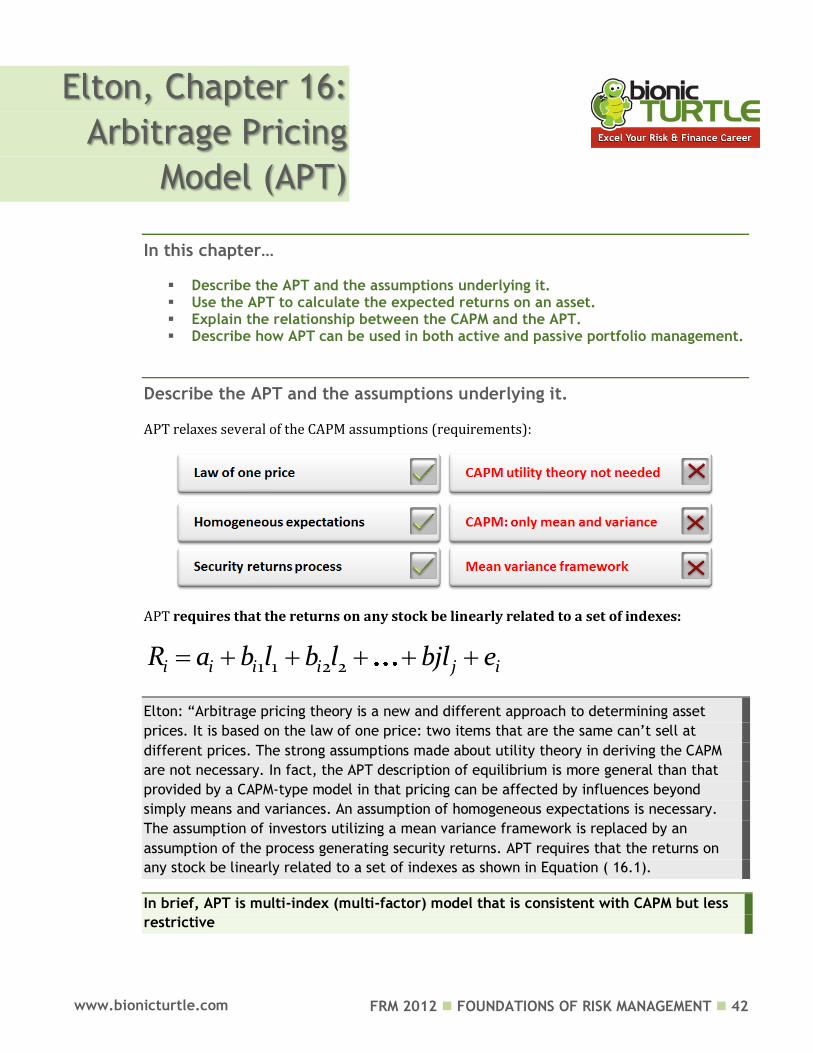

Describe the APT and the assumptions underlying it. Use the APT to calculate the expected returns on an asset. Explain the relationship between the CAPM and the APT. Describe how APT can be used in both active and passive portfolio management.

Describe the APT and the assumptions underlying it.

APT relaxes several of the CAPM assumptions (requirements):

APT requires that the returns on any stock be linearly related to a set of indexes:

1 1 2 2i i i i j iR a b l b l bjl e

Elton: “Arbitrage pricing theory is a new and different approach to determining asset

prices. It is based on the law of one price: two items that are the same can’t sell at

different prices. The strong assumptions made about utility theory in deriving the CAPM

are not necessary. In fact, the APT description of equilibrium is more general than that

provided by a CAPM-type model in that pricing can be affected by influences beyond

simply means and variances. An assumption of homogeneous expectations is necessary.

The assumption of investors utilizing a mean variance framework is replaced by an

assumption of the process generating security returns. APT requires that the returns on

any stock be linearly related to a set of indexes as shown in Equation ( 16.1).

In brief, APT is multi-index (multi-factor) model that is consistent with CAPM but less

restrictive

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 43 www.bionicturtle.com

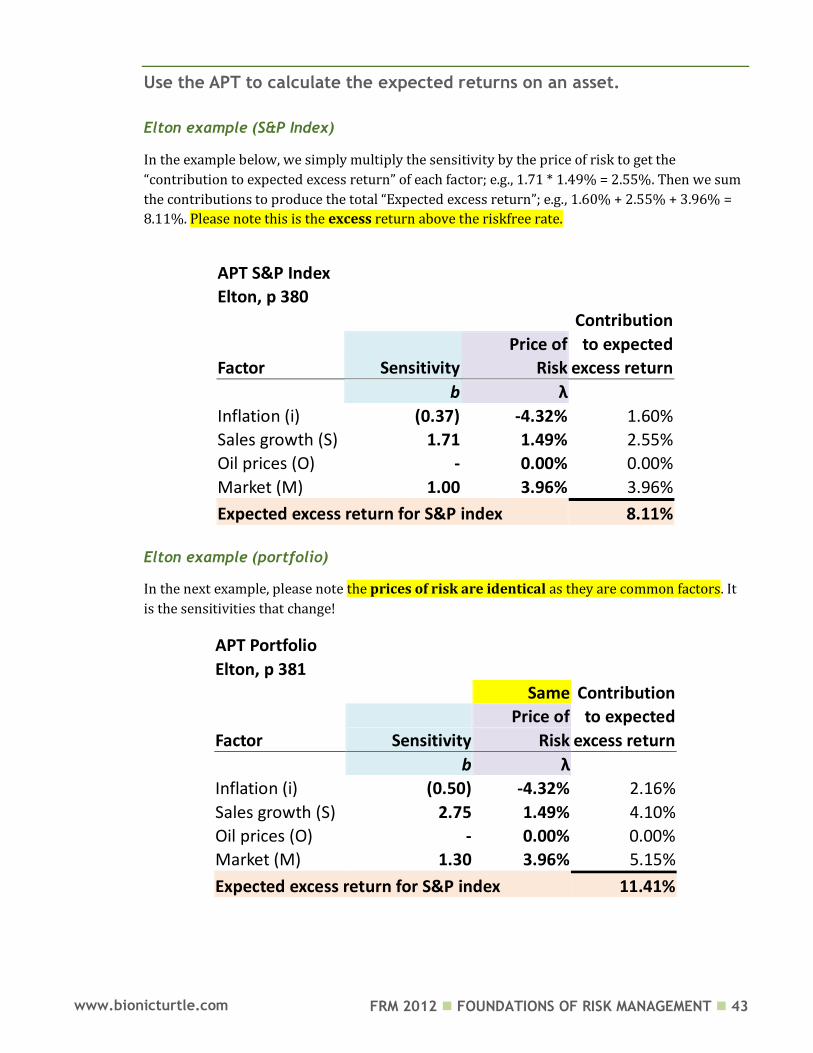

Use the APT to calculate the expected returns on an asset.

Elton example (S&P Index)

In the example below, we simply multiply the sensitivity by the price of risk to get the

“contribution to expected excess return” of each factor; e.g., 1.71 * 1.49% = 2.55%. Then we sum

the contributions to produce the total “Expected excess return”; e.g., 1.60% + 2.55% + 3.96% =

8.11%. Please note this is the excess return above the riskfree rate.

APT S&P Index Elton, p 380

Contribution

Price of to expected

Factor Sensitivity Risk excess return

b λ

Inflation (i) (0.37) -4.32% 1.60%

Sales growth (S) 1.71 1.49% 2.55%

Oil prices (O) - 0.00% 0.00%

Market (M) 1.00 3.96% 3.96%

Expected excess return for S&P index 8.11%

Elton example (portfolio)

In the next example, please note the prices of risk are identical as they are common factors. It

is the sensitivities that change!

APT Portfolio Elton, p 381

Same Contribution

Price of to expected

Factor Sensitivity Risk excess return

b λ

Inflation (i) (0.50) -4.32% 2.16%

Sales growth (S) 2.75 1.49% 4.10%

Oil prices (O) - 0.00% 0.00%

Market (M) 1.30 3.96% 5.15%

Expected excess return for S&P index 11.41%

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 44 www.bionicturtle.com

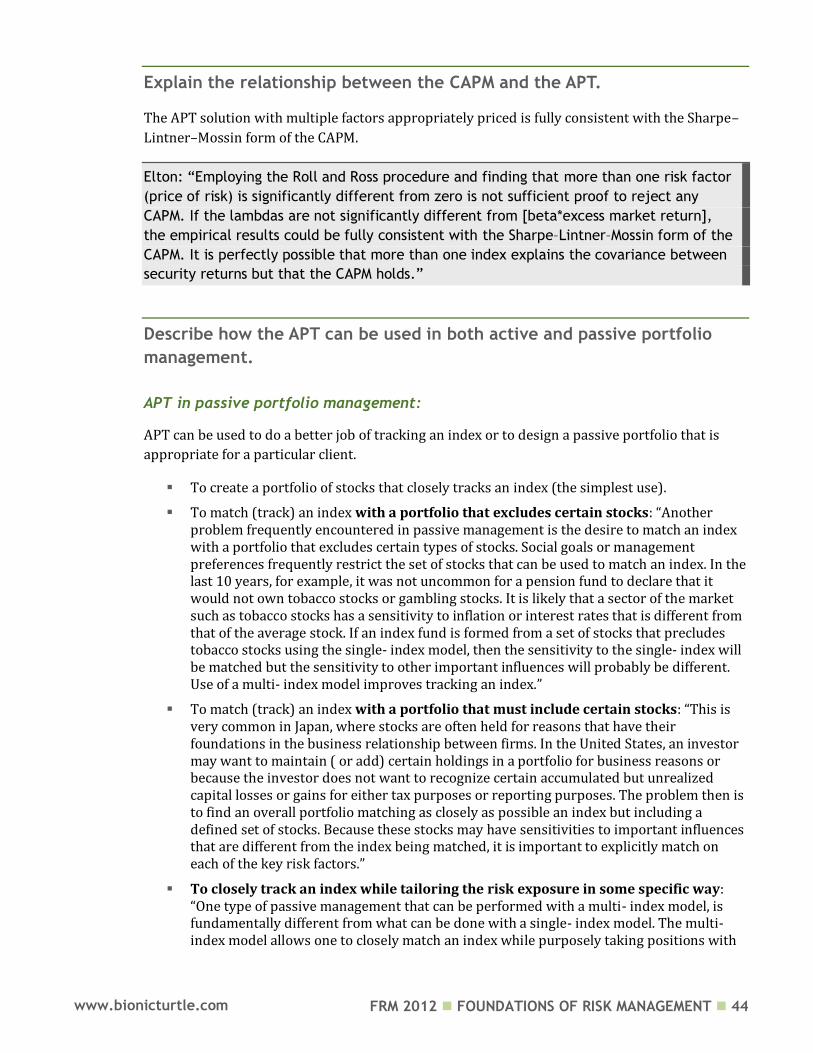

Explain the relationship between the CAPM and the APT.

The APT solution with multiple factors appropriately priced is fully consistent with the Sharpe–

Lintner–Mossin form of the CAPM.

Elton: “Employing the Roll and Ross procedure and finding that more than one risk factor

(price of risk) is significantly different from zero is not sufficient proof to reject any

CAPM. If the lambdas are not significantly different from [beta*excess market return],

the empirical results could be fully consistent with the Sharpe–Lintner–Mossin form of the

CAPM. It is perfectly possible that more than one index explains the covariance between

security returns but that the CAPM holds.”

Describe how the APT can be used in both active and passive portfolio

management.

APT in passive portfolio management:

APT can be used to do a better job of tracking an index or to design a passive portfolio that is

appropriate for a particular client.

To create a portfolio of stocks that closely tracks an index (the simplest use).

To match (track) an index with a portfolio that excludes certain stocks: “Another problem frequently encountered in passive management is the desire to match an index with a portfolio that excludes certain types of stocks. Social goals or management preferences frequently restrict the set of stocks that can be used to match an index. In the last 10 years, for example, it was not uncommon for a pension fund to declare that it would not own tobacco stocks or gambling stocks. It is likely that a sector of the market such as tobacco stocks has a sensitivity to inflation or interest rates that is different from that of the average stock. If an index fund is formed from a set of stocks that precludes tobacco stocks using the single- index model, then the sensitivity to the single- index will be matched but the sensitivity to other important influences will probably be different. Use of a multi- index model improves tracking an index.”

To match (track) an index with a portfolio that must include certain stocks: “This is very common in Japan, where stocks are often held for reasons that have their foundations in the business relationship between firms. In the United States, an investor may want to maintain ( or add) certain holdings in a portfolio for business reasons or because the investor does not want to recognize certain accumulated but unrealized capital losses or gains for either tax purposes or reporting purposes. The problem then is to find an overall portfolio matching as closely as possible an index but including a defined set of stocks. Because these stocks may have sensitivities to important influences that are different from the index being matched, it is important to explicitly match on each of the key risk factors.”

To closely track an index while tailoring the risk exposure in some specific way: “One type of passive management that can be performed with a multi- index model, is fundamentally different from what can be done with a single- index model. The multi-index model allows one to closely match an index while purposely taking positions with

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 45 www.bionicturtle.com

respect to certain types of risk different from the positions contained in the index. For example, consider a pension fund that has cash outflows affected by inflation (COLA or cost-of-living adjustments). The payments for such a pension fund increase with inflation. Thus the overseers want a portfolio that will perform especially well when the rate of inflation increases.”

APT in active portfolio management:

An obvious advantage of a multi-index model is that it allows the user to increase or decrease,

with intention, exposures to selected common factors.

To make common factor bets: “What a multi-index model does that cannot be done with a single- index model is allow the user to make factor bets. If you believe that unexpected inflation will accelerate at a rate above that anticipated by the market, then you may want to place a bet by increasing your exposure with inflation. This can be done holding a portfolio with sensitivity to inflation larger than the S& P index. Obviously the more indexes included in the model, the more active bets you can make. For example, in the Salomon model described earlier in this chapter, you can take active bets on economic growth, the stage of the business cycle, long- term interest rates, short- term interest rates, inflation rates, the value of the U. S. dollar, or the state of the stock market.”

To build optimal portfolios: “Multi- index models and APT models can be used just as the single-index model and CAPM models are used to form optimal portfolios building upon estimates of the performance of individual securities. The simplest approach is … where a multi-index model is used to generate the covariance between securities while expected returns and variances are supplied by some combination of analysts’ forecasts and historical data.”

To judge the valuation of securities: “Another application of APT is to use APT to determine stocks that are under- or overvalued. In this procedure an analyst produces a forecast of the return on a stock. The APT is then used together with estimates of the sensitivity of the stock to the factors to calculate a required return for the stock. If the estimated return is above what’s required given the stock’s sensitivity and the s, the stock is purchased.

Related, to track an index or benchmark but enhance with active tilt: “One of the most common uses of the APT model is to form a portfolio of stocks that while closely tracking a target will also produce a return in excess of that index. One way to implement this type of procedure is simply to employ the index- matching procedure described earlier in this chapter but only allow selection from among a set of stocks that analysts have earmarked as superior performers. Other techniques use either numeric discrete ranking of stocks or expected return on stocks in an attempt to produce an excess return above an index while using the multi-index model to track an index as closely as possible. Portfolios designed this way have become known as research-tilted index funds. Although some additional risk is involved (the index can’t be matched as closely when selecting from a restricted set of stocks), investors who use this technique feel that an excess return can be earned with only a slight loss in the ability to track the index. The advantage of the multi- index model over the simple- index model is that the target index can be tracked more closely because the different sources of risk are explicitly taken into consideration.”

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 46 www.bionicturtle.com

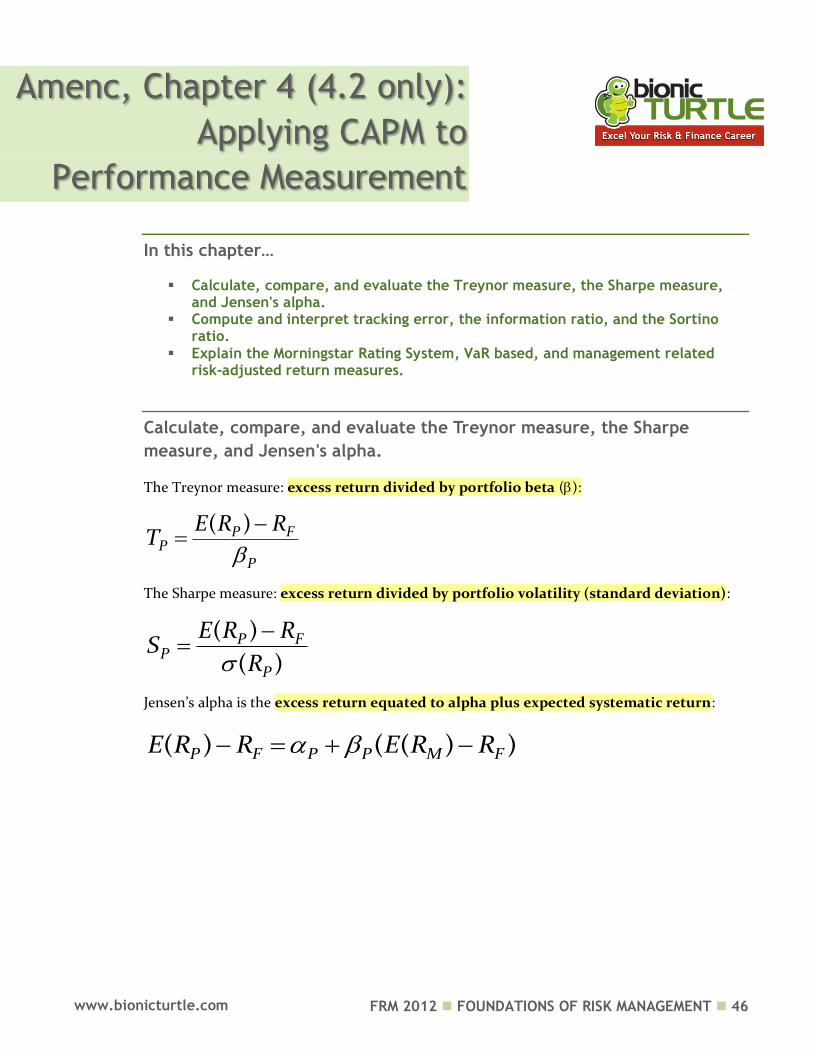

Amenc, Chapter 4 (4.2 only):

Applying CAPM to

Performance Measurement

In this chapter…

Calculate, compare, and evaluate the Treynor measure, the Sharpe measure, and Jensen's alpha.

Compute and interpret tracking error, the information ratio, and the Sortino ratio.

Explain the Morningstar Rating System, VaR based, and management related risk-adjusted return measures.

Calculate, compare, and evaluate the Treynor measure, the Sharpe

measure, and Jensen's alpha.

The Treynor measure: excess return divided by portfolio beta ():

( )P FP

P

E R RT

The Sharpe measure: excess return divided by portfolio volatility (standard deviation):

( )

( )P F

PP

E R RS

R

Jensen’s alpha is the excess return equated to alpha plus expected systematic return:

( ) ( ( ) )P F P P M FE R R E R R

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 47 www.bionicturtle.com

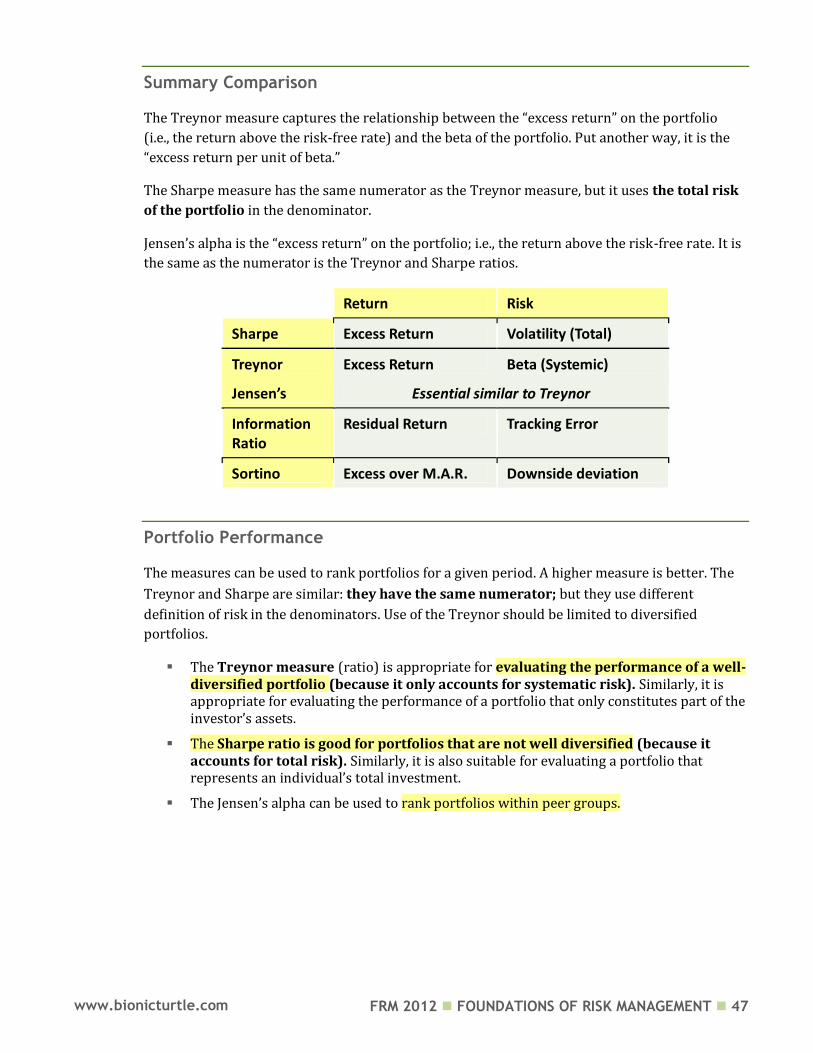

Summary Comparison

The Treynor measure captures the relationship between the “excess return” on the portfolio

(i.e., the return above the risk-free rate) and the beta of the portfolio. Put another way, it is the

“excess return per unit of beta.”

The Sharpe measure has the same numerator as the Treynor measure, but it uses the total risk

of the portfolio in the denominator.

Jensen’s alpha is the “excess return” on the portfolio; i.e., the return above the risk-free rate. It is

the same as the numerator is the Treynor and Sharpe ratios.

Return Risk

Sharpe Excess Return Volatility (Total)

Treynor Excess Return Beta (Systemic)

Jensen’s Essential similar to Treynor

Information Ratio

Residual Return Tracking Error

Sortino Excess over M.A.R. Downside deviation

Portfolio Performance

The measures can be used to rank portfolios for a given period. A higher measure is better. The

Treynor and Sharpe are similar: they have the same numerator; but they use different

definition of risk in the denominators. Use of the Treynor should be limited to diversified

portfolios.

The Treynor measure (ratio) is appropriate for evaluating the performance of a well-diversified portfolio (because it only accounts for systematic risk). Similarly, it is appropriate for evaluating the performance of a portfolio that only constitutes part of the investor’s assets.

The Sharpe ratio is good for portfolios that are not well diversified (because it accounts for total risk). Similarly, it is also suitable for evaluating a portfolio that represents an individual’s total investment.

The Jensen’s alpha can be used to rank portfolios within peer groups.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 48 www.bionicturtle.com

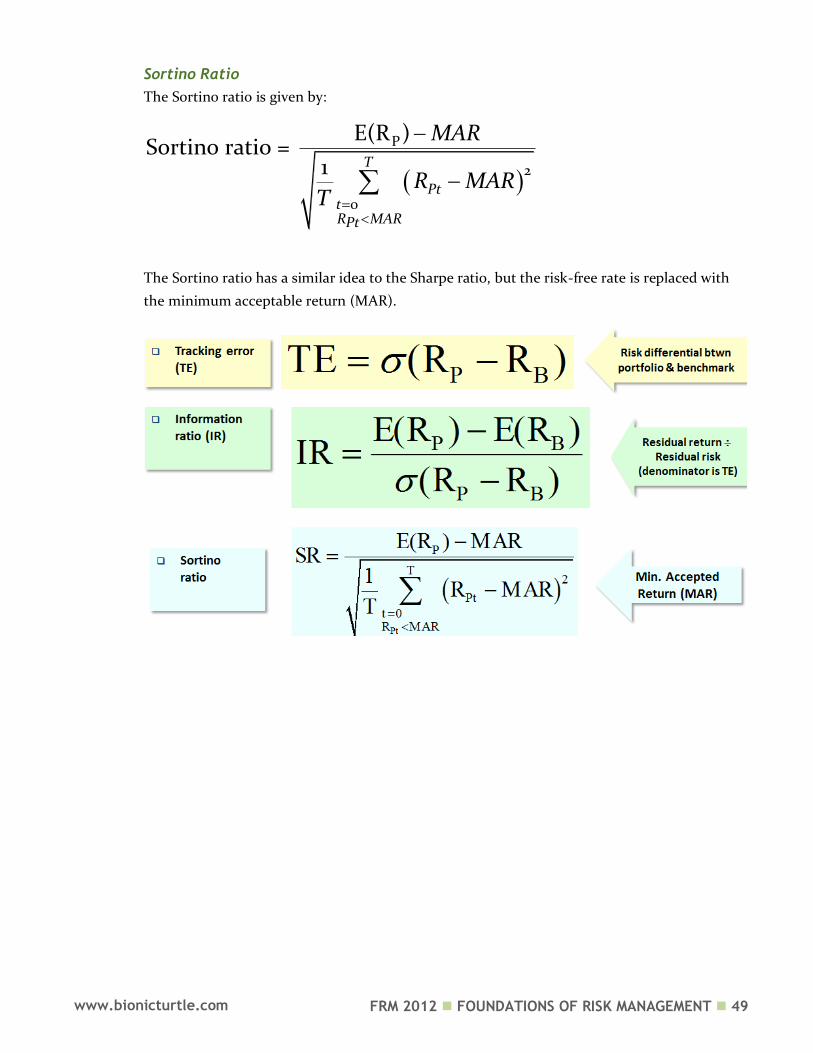

Compute and interpret tracking error, the information ratio, and the

Sortino ratio.

Tracking Error (TE)

Tracking error (TE) is the standard deviation of the difference between the portfolio return

and the benchmark return:

( )P BTE R R

Tracking error is used to analyze benchmark funds; i.e., funds that assume a risk profile (and

construction, generally) similar to a particular profile but then deviates from the benchmark in

an attempt to add value. The ideal, of course, is to add value without assuming additional risk.

Information ratio (IR)

The information ratio (IR, aka, the appraisal ratio) is given by:

( ) ( )

( )P B

P B

E R E RIR

R R

The information ratio (IR) is also used to evaluate the manager of a benchmark fund. It helps

to answer the question, “was the manager sufficiently rewarded for the risk incurred by

deviating from the benchmark?”

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 49 www.bionicturtle.com

Sortino Ratio

The Sortino ratio is given by:

P

2

0

E(R )Sortino ratio =

1 T

PttR MARPt

MAR

R MART

The Sortino ratio has a similar idea to the Sharpe ratio, but the risk-free rate is replaced with

the minimum acceptable return (MAR).

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 50 www.bionicturtle.com

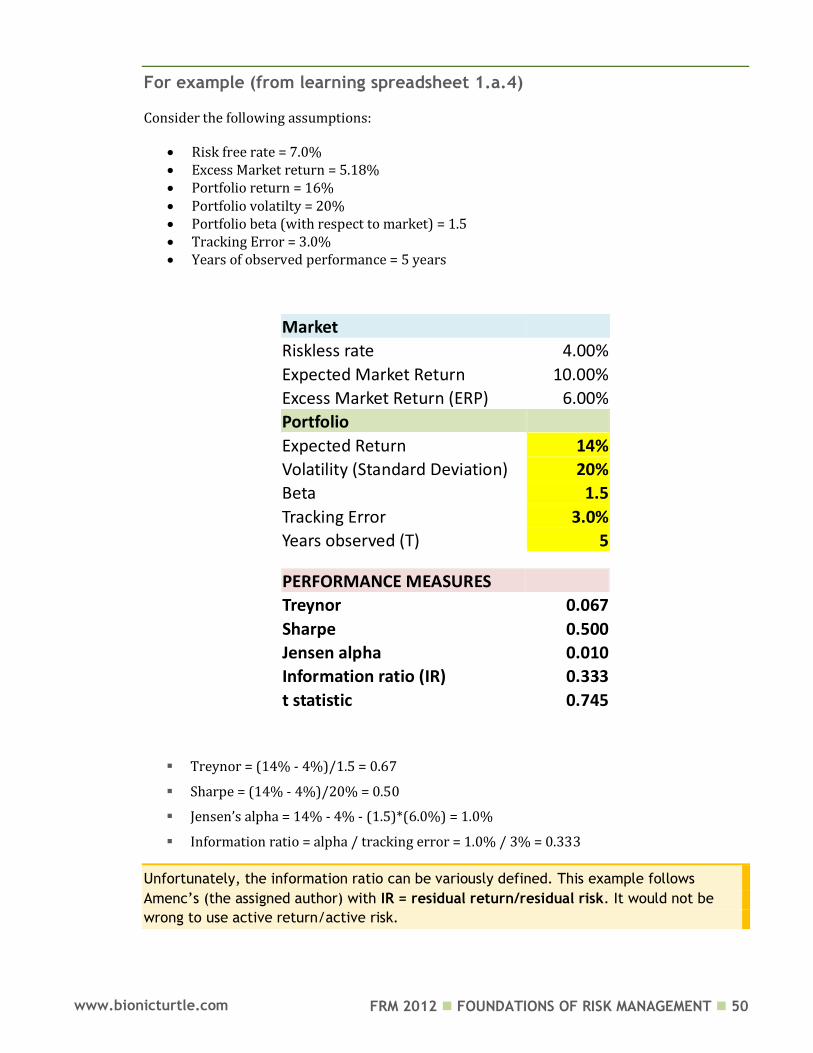

For example (from learning spreadsheet 1.a.4)

Consider the following assumptions:

Risk free rate = 7.0% Excess Market return = 5.18% Portfolio return = 16% Portfolio volatilty = 20% Portfolio beta (with respect to market) = 1.5 Tracking Error = 3.0% Years of observed performance = 5 years

Market

Riskless rate 4.00%

Expected Market Return 10.00%

Excess Market Return (ERP) 6.00%

Portfolio

Expected Return 14%

Volatility (Standard Deviation) 20%

Beta 1.5

Tracking Error 3.0%

Years observed (T) 5

PERFORMANCE MEASURES

Treynor 0.067

Sharpe 0.500

Jensen alpha 0.010

Information ratio (IR) 0.333

t statistic 0.745

Treynor = (14% - 4%)/1.5 = 0.67

Sharpe = (14% - 4%)/20% = 0.50

Jensen’s alpha = 14% - 4% - (1.5)*(6.0%) = 1.0%

Information ratio = alpha / tracking error = 1.0% / 3% = 0.333

Unfortunately, the information ratio can be variously defined. This example follows

Amenc’s (the assigned author) with IR = residual return/residual risk. It would not be

wrong to use active return/active risk.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 51 www.bionicturtle.com

Explain the Morningstar Rating System, VaR based, and management

related risk-adjusted return measures.

Morningstar Rating System (4.2.9.1.)

The Morningstar measure is called a risk-adjusted rating (RAR).The principle of the measure is

to rand different funds that belong to the same peer group. The RAR for a fund is calculated as

the difference between its relative returns and its relative risk. The relative return and the

relative risk for the fund are obtained by dividing, respectively, the return and the risk of the

fund by a quantity, called the base, which is common to all the funds in the peer group, or

P P Pi i iRAR RR RRisk

(relative return) =

(relative risk) =

PiPi

g

PiPi

g

RRR

BR

RiskRRisk

BRisk

Where (g) denotes the peer group containing the fund Pi;

RPi denotes the return on fund Pi, in excess of the risk-free rate;

RiskPi denotes the risk of fund Pi;

BRg denotes the base used to calculate the relative returns of all the funds in the group;

BRiskg denotes the base used to calculate the relative risks of all the funds in the group.

“The Morningstar measure is based on an investment period of one month, although funds

are in fact held for longer periods, and a decrease in one month can be compensated for

by an increase in the following month. This measure is not therefore very appropriate for

measuring the risk of funds that are held over a long period.” -- Amenc

Analysis based on the Value at Risk (VaR; 4.2.9.3)

The numerator is the same as with Sharpe and Treynor: excess return. But risk is replaced with

a risk indicator based on value at risk (VaR):

0

P F

P

P

R R

VaR

V

RP denotes the return on the portfolio; RF denotes the return on the risk-free asset; VaRP denotes the VaR of the portfolio; V(0)P denotes the initial value of the portfolio.

FRM 2012 FOUNDATIONS OF RISK MANAGEMENT 52 www.bionicturtle.com

Measure taking the management style into account (VaR; 4.2.9.4)

This is a risk-adjusted performance measure that includes the management style as defined by

Sharpe. The annualized risk-adjusted performance (RAP ) of a fund is measured in relation to

the market benchmark:

M

P P F FP

RAP R R R

σM denotes the annualized standard deviation of the market returns;

σP denotes the annualized standard deviation of the returns of fund P;

RP denotes the annualized return of fund P; and

RF denotes the risk-free rate.

This relationship is drawn directly from the capital market line: it allows us to look at the

performance of the fund in relation to that of the market. The most interesting funds have the

highest RAP value. To obtain a relative measure, one just calculates the difference between the

RAP for the fund and the RAP for the benchmark, with the benchmark’s RAP measure being