40

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES Consolidated Financial Statements December 31, 2007 and 2006 (With Independent Auditors’ Report Thereon)

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Consolidated Financial Statements

December 31, 2007 and 2006

(With Independent Auditors’ Report Thereon)

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Table of Contents

Page

Independent Auditors’ Report 1

Consolidated Balance Sheets, December 31, 2007 and 2006 2

Consolidated Statements of Operations, Years ended December 31, 2007 and 2006 3

Consolidated Statements of Changes in Net Assets, Years ended December 31, 2007 and 2006 4

Consolidated Statements of Cash Flows, Years ended December 31, 2007 and 2006 5

Notes to Consolidated Financial Statements 6

Schedules

1 Consolidating Balance Sheet Information, December 31, 2007 33

2 Consolidating Statement of Operations Information, Year ended December 31, 2007 35

3 Consolidating Statement of Changes in Net Assets Information, Year ended December 31, 2007 37

KPMG LLP 777 East Wisconsin Avenue Milwaukee, WI 53202

KPMG LLP, a U.S. limited liability partnership, is the U.S.member firm of KPMG International, a Swiss cooperative.

Independent Auditors’ Report

The Board of Directors Froedtert & Community Health, Inc.:

We have audited the accompanying consolidated balance sheets of Froedtert & Community Health, Inc. and affiliates (the Corporation) as of December 31, 2007 and 2006, and the related consolidated statements of operations, changes in net assets, and cash flows for the years then ended. These consolidated financial statements are the responsibility of the Corporation’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Corporation’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of Froedtert & Community Health, Inc. and affiliates as of December 31, 2007 and 2006, and the results of their consolidated operations and cash flows for the years then ended in conformity with U.S. generally accepted accounting principles.

As discussed in note 12 to the accompanying consolidated financial statements, the Corporation adopted the provisions of the Statement of Financial Accounting Standards No. 158, Employer’s Accounting for Defined Benefit Pensions and Other Post Retirement Plans, in 2007.

Our audits were made for the purpose of forming an opinion on the consolidated financial statements taken as a whole. The consolidating information included in schedules 1 through 3 is presented for purposes of additional analysis of the consolidated financial statements rather than to present the financial position, results of operations, and changes in net assets of the individual corporations. The consolidating information has been subjected to the auditing procedures applied in the audit of the consolidated financial statements and, in our opinion, is fairly stated, in all material respects, in relation to the consolidated financial statements taken as a whole.

Milwaukee, Wisconsin April 1, 2008

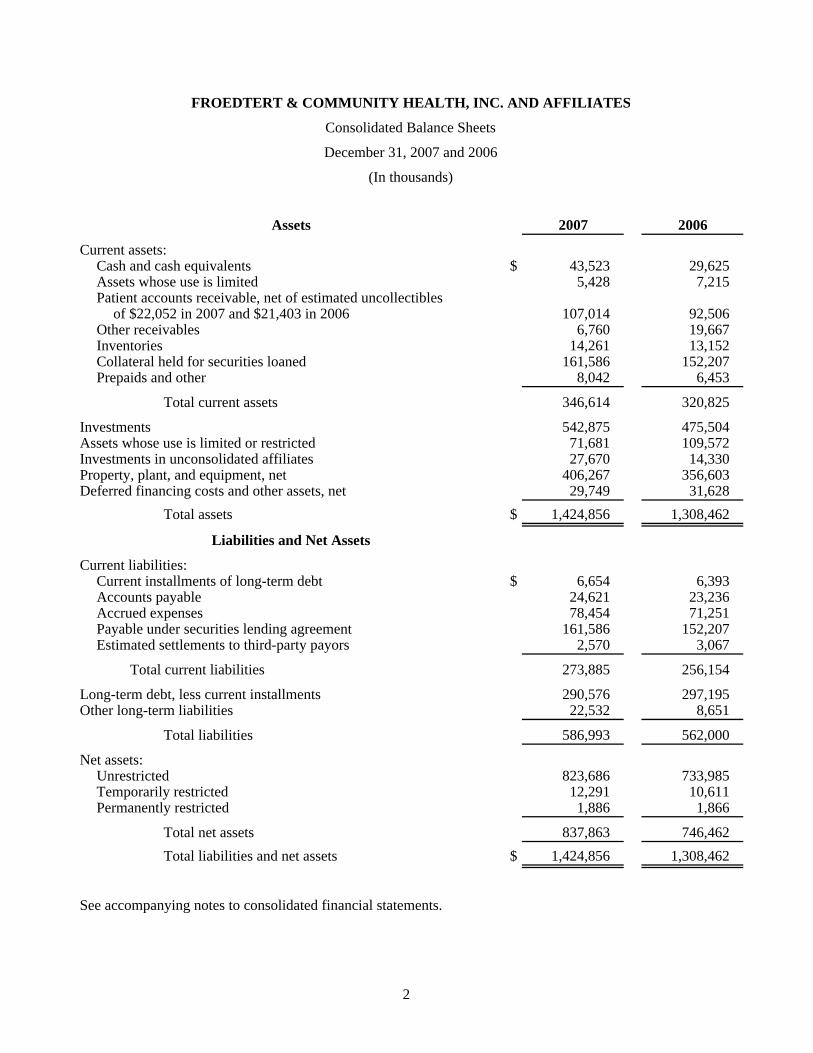

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Consolidated Balance Sheets

December 31, 2007 and 2006

(In thousands)

Assets 2007 2006

Current assets:Cash and cash equivalents $ 43,523 29,625 Assets whose use is limited 5,428 7,215 Patient accounts receivable, net of estimated uncollectibles

of $22,052 in 2007 and $21,403 in 2006 107,014 92,506 Other receivables 6,760 19,667 Inventories 14,261 13,152 Collateral held for securities loaned 161,586 152,207 Prepaids and other 8,042 6,453

Total current assets 346,614 320,825

Investments 542,875 475,504 Assets whose use is limited or restricted 71,681 109,572 Investments in unconsolidated affiliates 27,670 14,330 Property, plant, and equipment, net 406,267 356,603 Deferred financing costs and other assets, net 29,749 31,628

Total assets $ 1,424,856 1,308,462

Liabilities and Net Assets

Current liabilities:Current installments of long-term debt $ 6,654 6,393 Accounts payable 24,621 23,236 Accrued expenses 78,454 71,251 Payable under securities lending agreement 161,586 152,207 Estimated settlements to third-party payors 2,570 3,067

Total current liabilities 273,885 256,154

Long-term debt, less current installments 290,576 297,195 Other long-term liabilities 22,532 8,651

Total liabilities 586,993 562,000

Net assets:Unrestricted 823,686 733,985 Temporarily restricted 12,291 10,611 Permanently restricted 1,886 1,866

Total net assets 837,863 746,462 Total liabilities and net assets $ 1,424,856 1,308,462

See accompanying notes to consolidated financial statements.

2

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Consolidated Statements of Operations

Years ended December 31, 2007 and 2006

(In thousands)

2007 2006

Revenues:Net patient service revenue $ 856,747 770,777 Other operating revenue 46,420 42,272

Total revenues 903,167 813,049

Expenses:Salaries 278,856 264,281 Fringe benefits 81,378 69,623 Supplies 173,564 169,497 Contract services 98,988 96,842 Medical education 35,297 39,494 Provision for bad debts 34,441 34,618 Depreciation and amortization 37,280 34,597 Interest 7,436 7,849 Other 81,918 71,562

Total expenses 829,158 788,363

Operating revenues in excess of expenses 74,009 24,686

Nonoperating gains and losses:Investment income 33,571 31,233 Net unrealized gains, related to redesignation

of investment portfolio 24,888 — Minority interest (40) 216

Revenues in excess of expenses and gains and losses 132,428 56,135

Other changes in unrestricted net assets:Change in net unrealized gains and losses on investments (8,455) 6,959 Net unrealized gains related to redesignation

of investment portfolio (24,888) — Change in fair value of interest rate swap agreements (7,844) 4,603 Contributions and net assets released from restrictions for

property, plant, and equipment 1,584 782 Change in minimum pension liability 2,767 (847) Effect of adopting SFAS No. 158 relating to defined benefit plans (5,543) — Other (348) 77

Increase in unrestricted net assets 89,701 67,709

Unrestricted net assets at beginning of year 733,985 666,276 Unrestricted net assets at end of year $ 823,686 733,985

See accompanying notes to consolidated financial statements.

3

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Consolidated Statements of Changes in Net Assets

Years ended December 31, 2007 and 2006

(In thousands)

Temporarily PermanentlyUnrestricted restricted restricted

net assets net assets net assets Total

Balance, December 31, 2005 $ 666,276 9,568 341 676,185

Revenues in excess of expenses and gainsand losses 56,135 — — 56,135

Change in net unrealized gains andlosses on investments 6,959 190 — 7,149

Change in fair value of interestrate swap agreements 4,603 — — 4,603

Restricted contributions — 952 1,525 2,477 Restricted investment income — 634 — 634 Net assets released from restrictions

for operations — (531) — (531) Contributions and net assets released from

restriction for property, plant, and equipment 782 (222) — 560 Change in minimum pension liability (847) — — (847) Other 77 20 — 97

Increase in net assets 67,709 1,043 1,525 70,277

Balance, December 31, 2006 733,985 10,611 1,866 746,462

Revenues in excess of expenses and gainsand losses 132,428 — — 132,428

Change in net unrealized gains andlosses on investments (8,455) (197) — (8,652)

Net unrealized gains, related to redesignationof investment portfolio (24,888) — — (24,888)

Change in fair value of interestrate swap agreements (7,844) — — (7,844)

Restricted contributions — 3,055 20 3,075 Restricted investment income — 770 — 770 Net assets released from restrictions

for operations — (687) — (687) Contributions and net assets released from

restrictions for property, plant, and equipment 1,584 (1,584) — — Change in minimum pension liability 2,767 — — 2,767 Effect of adopting SFAS No. 158 related to

defined benefit plans (5,543) — — (5,543) Other (348) 323 — (25)

Increase in net assets 89,701 1,680 20 91,401 Balance, December 31, 2007 $ 823,686 12,291 1,886 837,863

See accompanying notes to consolidated financial statements.

4

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Consolidated Statements of Cash Flows

Years ended December 31, 2007 and 2006

(In thousands)

2007 2006

Cash flows from operating activities:Increase in net assets $ 91,401 70,277 Adjustments to reconcile increase in net assets to net cash

provided by operating activities:Depreciation and amortization 37,280 34,597 Provision for bad debts 34,441 34,618 Equity gain in unconsolidated affiliates, net (10,379) (7,299) Restricted contributions (2,300) (2,477) Change in net unrealized gains and losses on investments 9,048 (7,149) Change in fair value of interest rate swap agreements 7,844 (4,603) Increase in patient accounts receivable (48,949) (42,874) Decrease in estimated settlements to third-party payors (497) (655) Increase in accounts payable and accrued expenses 11,040 11,186 Change in minimum pension liability (2,767) 847 Effect of adopting SFAS No. 158 relating to defined

benefit plans 5,543 — Decrease (increase) in other receivables 12,907 (5,967) Increase in inventories (1,109) (771) Changes in other assets and liabilities and other adjustments 576 2,408

Net cash provided by operating activities 144,079 82,138

Cash flows from investing activities:Net additions to property, plant, and equipment (86,460) (59,290) Purchases of investments and assets whose use is limited or

restricted (575,293) (464,715) Proceeds from sales or maturities of investments and assets

whose use is limited or restricted 538,552 447,431 Additional capital contributions in unconsolidated affiliates (7,521) (5,412) Net distributions and dividends received from unconsolidated

affiliates, net 4,560 11,701

Net cash used in investing activities (126,162) (70,285)

Cash flows from financing activities:Repayments of long-term debt (6,319) (6,144) Restricted contributions 2,300 2,477

Net cash used in financing activities (4,019) (3,667)

Net increase in cash and cash equivalents 13,898 8,186

Cash and cash equivalents:Beginning of year 29,625 21,439 End of year $ 43,523 29,625

See accompanying notes to consolidated financial statements.

5

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

6 (Continued)

(1) Organization and Summary of Significant Accounting Policies

Froedtert & Community Health, Inc. (F&CH) is a nonstock, not-for-profit corporation organized to support and carry out the missions of Froedtert Health System, Inc. (FHS); Froedtert Memorial Lutheran Hospital, Inc. (FMLH); Community Health Care Services of Menomonee Falls, Inc. (CHCS); and Community Memorial Hospital of Menomonee Falls, Inc. (CMH). F&CH is the sole corporate member of FHS and CHCS.

FHS was formed to benefit and support FMLH. FMLH owns and operates an acute care hospital with 655 approved beds (of which 451 are currently staffed), clinics, and related operations in Wauwatosa, Wisconsin. The articles of incorporation and bylaws of FHS established FHS as the parent corporation of FMLH. FHS is also the sole corporate member of Froedtert Hospital Foundation, Inc. (Froedtert Foundation). The purpose of Froedtert Foundation is to raise money and to accept contributions for the purpose of developing philanthropic support for FMLH. Froedtert Foundation solicits, allocates, and dispenses funds exclusively for the maintenance, benefit, and support of FMLH programs, services, education, and capital improvements in accordance with priorities set by the Froedtert Foundation’s board of directors and donor restrictions. Froedtert Surgery Center, LLC (FSC) is a Wisconsin limited liability company created as a joint venture between FHS, Medical College of Wisconsin (MCW), and Advanced Healthcare S.C. (Advanced) to provide ambulatory surgery services. FHS has a 50% ownership in FSC.

CHCS was formed to provide managerial, planning, and administrative services for the maintenance, benefit, and support of CMH and other organizations. CMH owns and operates an acute care hospital with 237 approved beds (of which 202 are currently staffed) in Menomonee Falls, Wisconsin. Community Memorial Foundation of Menomonee Falls, Inc. (Community Memorial Foundation) is a separate Wisconsin not-for-profit corporation whose purpose is to support and assist CMH by soliciting, holding, managing, investing, and expending contributions, grants, and bequests. Community Outpatient Health Services of Menomonee Falls, Inc. (COHS) is a primary care clinic for the indigent. Horizon Ventures Limited, LLC (HVL) is a Wisconsin limited liability company created to establish cost-effective delivery structures in joint venture relationships with other healthcare organizations. CHCS is the sole corporate member of CMH, Community Memorial Foundation, COHS, and HVL.

The accompanying consolidated financial statements include the accounts of F&CH, FHS, FMLH, Froedtert Foundation, FSC, CHCS, CMH, Community Memorial Foundation, COHS, and HVL.

F&CH, FHS, FMLH, CHCS, and CMH are members of the obligated group (Obligated Group) for the purposes of the issuance of bonds through the Wisconsin Health and Educational Facilities Authority (WHEFA) (note 5). The Obligated Group consists only of the members mentioned above and excludes Froedtert Foundation, FSC, Community Memorial Foundation, COHS, and HVL. Total combined assets of the consolidated entities that are not members of the Obligated Group were approximately $10,970,000 and $10,806,000 at December 31, 2007 and 2006, respectively. Total combined net assets of the same entities were approximately $6,716,000 and $6,559,000 at December 31, 2007 and 2006, respectively, and total combined revenue less than expenses approximates $(138,000) and $(379,000) for the years ended December 31, 2007 and 2006, respectively.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

7 (Continued)

The significant accounting policies of F&CH are as follows:

(a) Principles of Consolidation

All significant intercompany accounts and transactions have been eliminated in the consolidation.

(b) Net Assets

Net assets are classified as either permanently or temporarily restricted when the use of the assets is limited by outside parties, or as unrestricted net assets when outside parties place no restrictions on the use of the assets or when the assets arise as a result of the operations of F&CH.

Unconditional promises to give cash and other assets to F&CH are reported at fair value at the date the promise is received. Pledges receivable to be collected after one year are discounted using a risk- free interest rate. Conditional promises to give and indications of intentions to give are reported at fair value at the date the gift is received. The gifts are reported as either temporarily or permanently restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified as unrestricted net assets and reported as operating revenue in the consolidated statements of operations if restricted for operating purposes and as an increase to unrestricted net assets if restricted to purchase property, plant, and equipment. Gifts for which donors have not stipulated restrictions, as well as contributions for which donors have stipulated restrictions that are met within the same reporting period, are reported as other operating revenue. F&CH’s temporarily restricted net assets are restricted for future construction and specific operations of FMLH and CMH. The permanently restricted net assets are endowment funds held by Froedtert Foundation, the principal of which may not be expended.

(c) Assets Whose Use is Limited or Restricted

Assets whose use is limited or restricted include assets set aside by management for executive compensation agreements and for program development and physician recruitment, assets set aside by agreements with third parties related to the sale of patient accounts receivable, assets held by trustees under debt agreements, and assets whose use is restricted by donors. Assets whose use is limited are reported as unrestricted net assets. Assets whose use is restricted by donors are reported as temporarily restricted or permanently restricted net assets.

(d) Revenues in Excess of Expenses and Gains and Losses

The consolidated statements of operations include revenues in excess of expenses and gains and losses. Changes in unrestricted net assets that are excluded from revenues in excess of expenses and gains and losses, consistent with industry practice, include change in net unrealized gains and losses on investments classified as other-than-trading securities; changes in fair value for the effective portion of interest rate swap agreements for those swaps that qualify for hedge accounting; contributions of property, plant, and equipment (including assets acquired using contributions that by donor restrictions were to be used for the purpose of acquiring such assets); recognition (reversal) of minimum pension liabilities; and permanent transfers of assets to and from affiliates for other than goods and services.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

8 (Continued)

(e) Net Patient Service Revenue

Net patient service revenue is reported at estimated net realizable amounts from patients, third-party payors, and others for services rendered and include estimated retroactive adjustments under reimbursement agreements with third-party payors. Retroactive adjustments are accrued on an estimated basis in the period the related services are rendered and adjusted in future periods, as final settlements are determined.

(f) Investments and Investment Income

Investments, including assets whose use is limited or restricted, with readily determinable fair values are stated at fair value generally based upon quoted market prices. Repurchase agreements are stated at cost, which approximates fair value. Realized gains and losses, interest and dividends on short-term investments, and interest and dividends on funds held under debt agreements, to the extent not capitalized, are classified as other operating revenue in the consolidated statements of operations. Realized gains and losses, unrealized gains and losses on trading securities, and interest and dividends on long-term investments are classified as nonoperating gains and losses in the consolidated statements of operations. Unrealized gains and losses on investments classified as other-than-trading securities are recorded directly to net assets.

F&CH invests in various investment securities including mutual funds, U.S. government securities, corporate debt instruments, and common stocks. Investment securities are exposed to various risks, such as interest rate, credit, and overall market volatility. Due to the level of risk associated with certain investment securities, it is reasonably possible that changes in the values of F&CH’s investments could occur in the near term and that such changes could materially affect the amounts reported in the consolidated financial statements.

Investments in joint ventures in which 20% to 50% interest is held are accounted for using the equity method of accounting. Investments in joint ventures with less than a 20% interest and for which F&CH does not exercise significant control are accounted for using the cost method. Investments in which greater than 50% interest is held are consolidated with the recording of minority interest. Minority interest is reflected as other long-term liabilities and nonoperating gains and losses in the consolidated financial statements.

(g) Inventories

Inventories are stated at cost, which is not in excess of market value.

(h) Property, Plant, and Equipment

Property, plant, and equipment are recorded at cost and depreciated using the straight-line method over their estimated useful lives. Equipment under capital leases and leasehold improvements are amortized on the straight-line method over the shorter of the lease term or the estimated useful life of the equipment or leasehold improvements.

Gifts of long-lived assets with explicit restrictions by donors that specify how the assets are to be used and gifts of cash or other assets that must be used to acquire long-lived assets are reported as restricted contributions. Absent explicit donor stipulations about how long those long-lived assets

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

9 (Continued)

must be maintained, expirations of donor restrictions are reported when the donated or acquired long-lived assets are placed in service.

(i) Long-Lived Assets

F&CH periodically assesses the recoverability of long-lived assets (including property, plant, and equipment and intangibles) when indications of potential impairment, based on estimated, undiscounted future cash flows, exist. Management considers such factors as current results, trends, and future prospects, in addition to other economic factors, in determining whether there is an impairment of the asset. F&CH has not recognized any impairment of long-lived assets during 2007 or 2006.

(j) Costs of Borrowing

Expenses incurred on the issuance of long-term debt and the original issue premium or discount are deferred and amortized using the declining-balance method over the term of the debt.

Net interest costs incurred on borrowed funds during the period of construction are capitalized as a component of the cost of significant construction projects.

(k) Cash and Cash Equivalents

For purposes of the consolidated statements of cash flows, cash and cash equivalents include highly liquid investments purchased with a maturity at date of purchase of three months or less, excluding assets whose use is limited or restricted.

(l) Income Taxes

F&CH and its affiliates, except HVL and FSC, are not-for-profit corporations as described in Section 501(c)(3) of the Internal Revenue Code (the Code) and are exempt from federal income taxes on related income pursuant to Section 501(a) of the Code. HVL and FSC are limited liability companies and are treated as partnerships for income tax purposes. Income and losses of both are passed through to their members.

Effective January 1, 2007, F&CH adopted Financial Accounting Standards Board (FASB) Interpretation No. 48 (FIN 48), Accounting for Uncertainty in Income Taxes, which clarifies the accounting for uncertainty in income taxes recognized in a company’s financial statements. FIN 48 prescribes a more-likely-than-not recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken. Under FIN 48, tax positions will be evaluated for recognition, derecognition, and measurement using consistent criteria and will provide more information about the uncertainty in income tax assets and liabilities. Based on an analysis prepared by F&CH, it was determined that the application of FIN 48 had no material effect on the recorded tax assets and liabilities of F&CH.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

10 (Continued)

(m) Use of Estimates

The preparation of consolidated financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements. Estimates also affect the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

(n) Derivative Instruments

Derivative instruments are reported at fair value on the consolidated balance sheets. For those derivatives that qualify as hedges, F&CH measures the effectiveness of the hedges on a quarterly basis. The derivatives that F&CH has entered into qualify as cash flow hedges. Under a cash flow hedge, the change in fair value of the derivative related to the effective portion of the hedge is recorded as a direct change in unrestricted net assets. The ineffective portion is reported in nonoperating gains and losses. If the ineffectiveness of a hedge exceeds certain prescribed levels, the derivative would no longer be eligible for hedge accounting, and all future changes in fair value of the derivative would be reported in nonoperating gains and losses.

(o) Reclassifications

Certain 2006 amounts have been reclassified to conform to the 2007 presentation.

(2) Investments and Assets Whose Use is Limited or Restricted

Investments and assets whose use is limited or restricted at fair value are summarized as follows (in thousands):

2007 2006

Cash and cash equivalents $ 23,981 27,048 U.S. government securities 128,768 151,095 Marketable equity securities 301,793 250,770 Capital certificate (note 11) 1,800 1,800 Subordinated note receivable (note 11) 1,349 1,342 Fixed income securities 122,606 136,250 Money market funds 27,511 5,365 Pledges receivable 581 690 Repurchase agreements 8,311 15,071 Interest receivable 3,284 2,860

Total investments and assets whose useis limited or restricted $ 619,984 592,291

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

11 (Continued)

Assets whose use is limited or restricted at fair value are summarized as follows (in thousands):

2007 2006

Assets whose use is limited or restricted:Under debt agreements (note 5) $ 38,450 91,544 By management:

For executive compensation agreements 11,357 9,624 For program development and physician recruitment 10,000 —

Under sale of receivables agreement (note 11) 3,149 3,142 By donors 14,177 12,477

Total assets whose use is limited or restricted $ 77,133 116,787

Assets whose use is limited or restricted are classified as current assets to the extent they are available to meet current liabilities.

On December 31, 2007, F&CH changed the designation of its long-term investment portfolio from other-than-trading portfolio to a trading portfolio. As a result of the redesignation, gross unrealized gains and losses of $38,971,000 and $14,083,000, respectively, are included in nonoperating gains and losses, in the accompanying consolidated statements of operations.

The composition of investment return on F&CH’s cash and cash equivalents, investments, and assets whose use is limited or restricted is as follows (in thousands):

2007 2006

Included in other operating revenue:Interest and dividends on short-term investments and funds

held under debt agreements $ 3,064 2,809 Net realized gains (losses) on short-term investments and

funds held under debt agreements 1 (20) Included in nonoperating gain and losses:

Interest and dividends on long-term investments 15,775 14,265 Realized gains on long-term investments 17,796 16,968 Net unrealized gains, related to redesignation of investment

portfolio 24,888 — Included in property, plant, and equipment, net:

Interest income capitalized 2,312 3,908 Unrestricted net assets:

Change in unrealized gains and losses on investments (8,455) 6,959 Redesignation of investment portfolio (24,888) —

Temporarily and permanently restricted net assets:Restricted investment income 770 634 Change in unrealized gains and losses on investments (197) 190

Total investment return $ 31,066 45,713

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

12 (Continued)

In December of 2003, F&CH entered into a securities lending agreement with a financial institution whereby fixed income securities are loaned to third parties in exchange for cash collateral that exceeds the market value of the securities loaned. Collateral is marked to market daily to reflect changes in fair value of the securities loaned. F&CH invests the cash collateral in short-term investments. The fair market value of the securities loaned under this arrangement was approximately $158,126,000 and $148,180,000 at December 31, 2007 and 2006, respectively. The fair market value of the collateral received under this arrangement was $161,586,000 and $152,207,00 at December 31, 2007 and 2006, respectively. F&CH reports the collateral held under the securities lending agreement as an asset with the obligation to return such collateral reported as a liability. The loan value was 102.2% and 102.7% of the collateral outstanding at December 31, 2007 and 2006, respectively.

F&CH had temporarily impaired investments in its investment and assets whose use is limited or restricted portfolios as of December 31, 2006. The following is a summary of F&CH’s unrealized losses as of December 31, 2006 (in thousands):

2006Less than 12 months 12 months or longer Total

Unrealized Unrealized UnrealizedFair value losses Fair value losses Fair value losses

Security type:Fixed income securities $ 17,810 (157) 105,946 (3,468) 123,756 (3,625) U.S. government securities 22,116 (59) 83,532 (2,542) 105,648 (2,601) Marketable equity securities 30,219 (2,900) 4,190 (1,928) 34,409 (4,828)

Total temporarilyimpaired securities$ 70,145 (3,116) 193,668 (7,938) 263,813 (11,054)

(3) Property, Plant, and Equipment

Property, plant, and equipment are summarized as follows (in thousands):

2007 2006

Land and land improvements $ 7,758 7,572 Leasehold improvements 48,040 39,418 Buildings 280,703 276,340 Fixed equipment 74,815 70,640 Movable equipment 199,169 182,316 Construction in progress 89,217 38,129

Total property, plant, and equipment 699,702 614,415

Less accumulated depreciation and amortization 293,435 257,812 Property, plant, and equipment, net $ 406,267 356,603

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

13 (Continued)

Construction in progress at December 31, 2007 and 2006 relates to various software projects, construction of a cancer center pavilion at FMLH, and various other renovation projects at both hospital campuses. Contractually committed costs for renovation and software projects totaled approximately $52,651,000 at December 31, 2007. Capitalized interest costs were approximately $3,629,000 and $3,845,000 for the years ended December 31, 2007 and 2006, respectively. Interest income of $2,312,000 and $3,908,000 was netted against capitalized interest expense in 2007 and 2006, respectively.

(4) Land Lease Agreement

In 1980, FMLH entered into a land lease agreement with Milwaukee County to lease the land on which the hospital resides. The lease terms are for FMLH to pay $1 annually through 2030, and a mutually agreed-upon amount in years 2031 through 2079. If the parties cannot mutually agree upon an amount, the annual rent will be determined as fair market value of the leased land times 10%. In December 1995, FMLH purchased certain assets of John L. Doyne Hospital (Doyne). As part of the purchase, FMLH entered into an amendment to the original land lease agreement to include the land previously used by Doyne. The lease payments on the new land lease are calculated as $1 plus 5.25% of FMLH’s annual operating cash flow, as defined in the agreement, for each of the years through 2020 and $1 annually in years 2021 to 2079. The lease agreements are accounted for as operating leases. Lease expense has been recognized in accordance with the terms of the lease agreements amounting to $6,877,000 and $2,919,000 for the years ended December 31, 2007 and 2006, respectively. Cumulative amounts recognized under the lease agreements approximate $48,174,000 through December 31, 2007 since the lease inception in 1995. Payments under the lease agreements are made in the year subsequent to the year in which they relate.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

14 (Continued)

(5) Long-Term Debt

Long-term debt is summarized as follows (in thousands):

Revenue bonds, Series 2001 – due in sinking fund installmentsannually, plus interest each year through 2030, ranging from4.50% to 5.70% (effective rate of 5.68% in 2007 and 5.40 % in2006) $ 16,030 17,735

Revenue bonds, Series 2005A – due in sinking fund installmentsranging from $4,070 to $4,925 annually, plus interest eachyear through 2010, ranging from 1.33% to 4.60% (effectiverate of 4.55% and 4.60% in 2007 and 2006, respectively) 14,494 18,749

Revenue bonds, Series 2005B – annual principal paymentsrange from $2,435 in 2011 to $5,020 in 2030. Interest ratesvary based on market condition (3.40% at December 31,2007 and 3.91% at December 31, 2006) 121,595 121,595

Revenue bonds, Series 2005C – annual principal paymentsrange from $600 in 2028 to $11,760 in 2035. Interest ratesvary based on market condition (3.52% at December 31,2007 and 3.91% at December 31, 2006) 63,800 63,800

Revenue bonds, Series 2005D – annual principal paymentsrange from $2,100 in 2011 to $5,225 in 2035. Interest ratesvary based on market condition (4.05% at December 31,2007 and 3.80% at December 31, 2006) 78,125 78,125

Note payable to Columbia St Mary’s, Inc., interest due inmonthly installments of $5, principal payment due in full onDecember 31, 2011 1,250 1,250

Other 1,698 1,889

Total debt 296,992 303,143

Less:Current installments of long-term debt 6,654 6,393 Unamortized premium (238) (445)

Total long-term debt $ 290,576 297,195

On May 18, 2005, WHEFA issued the Series 2005 revenue bonds on behalf of the Obligated Group. Members of the Obligated Group include F&CH, FHS, FMLH, CHCS, and CMH. Pursuant to the terms of the bond trust indenture, each Obligated Group member is jointly and severally liable for the guaranty of principal and interest on the revenue bonds issued by WHEFA on behalf of the Obligated Group.

Under the terms of the Series 2005 bond trust indenture (the Indenture) and subsequent supplementals to the Indenture, FMLH and CMH are required to maintain certain deposits with a trustee. Such deposits are included with assets whose use is limited in the consolidated balance sheets (note 2). The Indenture also places limits on the incurrence of additional borrowings and requires that the Obligated Group satisfy certain measures of financial performance as long as the bonds are outstanding. The payments on the

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

15 (Continued)

principal and interest on the Series B, C, and D bonds when due will be insured by financial guaranty insurance policies issued by Ambac Assurance Corporation, and are further collateralized by the revenues of the Obligated Group.

The Series B, C, and D bonds have variable interest rates. The interest rates on the Series B and C bonds have a maximum interest rate of 12%. The Series D bonds are auction rate bonds, whereby the interest rate is determined through a weekly auction process. The maximum interest rate on the Series D bonds is a percentage of London Interbank Offered Rate (LIBOR) based on the prevailing rating of the bonds. The maximum is between 175% of LIBOR on AAA rated bonds and 300% of LIBOR based on bonds rated below BBB. The Series D bonds are currently rated AAA.

The series B and C bonds have put options that allow the holders to redeem the bonds prior to maturity. F&CH has an agreement with an underwriter to remarket any bonds redeemed as a result of the exercise of put options. If the bonds cannot be remarketed, a bank will purchase the bonds. The bank will demand payment from F&CH under an accelerated payment schedule for these purchased bonds.

The credit markets have recently experienced a growing number of failed auctions for auction rate securities. When the auction fails, the current investors are forced to hold the securities and will earn a predetermined maximum or penalty rate until the next auction. A failed auction indicates that the fair value of the security is less than par as the failure implies that investors would be viewing the maximum coupon the auction process could produce as less than the yield that those same investors would demand to achieve a fair value of par. Subsequent to December 31, 2007, the Series D bonds have experienced failures in auctions. These failures have caused the interest rate paid by F&CH on those bonds to be higher than previously experienced. As of March 27, 2008, the Series D bonds traded at an interest rate of 4.55%.

Cash payments for interest, net of amounts capitalized, were approximately $7,433,000 and $7,781,000 in 2007 and 2006, respectively.

Scheduled maturities on all long-term debt for each of the next five years and thereafter are as follows (in thousands):

2008 $ 6,654 2009 6,915 2010 8,537 2011 6,950 2012 7,239 Thereafter 260,697

Based upon borrowing rates currently available to F&CH for similar financings with similar terms and average maturities, the fair value of total long-term debt was approximately $306,633,000 and $316,006,000 at December 31, 2007 and 2006, respectively.

(6) Derivative Instruments and Hedging Activities

The derivative instruments used by F&CH are interest rate swap agreements that are used to convert variable rate interest on the long-term debt to fixed rate interest. The variable interest rate on the debt

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

16 (Continued)

generally exposes F&CH to variability in cash flow in rising or declining interest rate environments. In converting variable rate interest to a fixed rate, the interest rate swap effectively reduces the variability of the cash flow of the debt.

(a) Objectives and Strategies

F&CH, at times, uses variable rate debt to finance its operations. The debt obligations expose F&CH to variability in interest payments due to changes in interest rates. Management believes that it is prudent to limit the variability of a portion of its interest payments. To meet this objective, management entered into interest rate swap agreements to manage fluctuations in cash flows resulting from interest rate risk.

By using derivative financial instruments to hedge exposures to changes in interest rates, F&CH exposes itself to credit risk and market risk. Credit risk is the failure of the counterparty to perform under the terms of the derivative contract. When the fair value of a derivative contract is positive, the counterparty owes F&CH, which creates credit risk for F&CH. When the fair value of a derivative contract is negative, F&CH owes the counterparty, and therefore, it does not pose credit risk. F&CH minimizes the credit risk in derivative instruments by entering into transactions with high quality counterparties.

Market risk is the adverse effect on the value of a financial instrument that results from a change in interest rates. The market risk associated with interest rate contracts is managed by establishing and monitoring parameters that limit the types and degree of market risk that may be undertaken.

(b) Risk Management Policies

F&CH assesses interest rate risk by continually identifying and monitoring changes in interest rate exposures that may adversely impact expected future cash flows and by evaluating hedging opportunities. F&CH maintains risk management control systems to monitor interest rate risk attributable to both the outstanding or forecasted debt obligations, as well as the offsetting hedge positions. The risk management control systems involve the use of analytical techniques, including cash flow sensitivity analysis, to estimate the expected impact of changes in interest rates on future cash flows.

F&CH does not use derivative instruments for speculative investment purposes.

(c) Transactions

Consistent with the objectives set forth above, the Obligated Group entered into interest rate swaps matched to its Series 2005B, 2005C, and 2005D revenue bonds. Under the terms of the interest rate swap agreements, the Obligated Group pays a fixed rate on the bonds and receives a variable rate of interest equal to 68% of the one-month LIBOR index, reset weekly.

The fair value of the interest rate swap is $(947,000), included in other long-term liabilities, and $6,897,000, included in deferred financing costs and other assets, net in the consolidated balance sheets at December 31, 2007 and 2006, respectively. For the year ended December 31, 2007, there was no ineffective portion of the hedge transaction; accordingly, the changes in the unrealized

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

17 (Continued)

derivative gains and losses of $(7,844,000) and $4,603,000 have been reported as direct increases and decreases to unrestricted net assets at December 31, 2007 and 2006, respectively.

The interest rate swap agreements for the Obligated Group at December 31, 2007 consist of the following:

Notional Fixed Variable pay ratesType amount Maturity date pay rate 2007 2006

2005B bonds $ 121,595,000 April 1, 2030 3.354% 3.301% 3.638%2005C bonds 63,800,000 April 1, 2035 3.447 3.301 3.6382005D bonds 78,125,000 April 1, 2035 3.177 3.301 3.638

Cash paid under the interest rate swap agreements was $41,000 and $210,000 and cash received under the interest rate swaps agreements was $845,000 and $563,000 during 2007 and 2006, respectively, included in interest in the consolidated statements of operations.

(7) Net Patient Service Revenue

A summary of the basis of reimbursement with major third-party payors follows:

Medicare – Inpatient acute care, most outpatient, and defined capital costs for services rendered to Medicare beneficiaries are paid at prospectively determined rates per case. These rates vary according to a payment classification system that is based on clinical, diagnostic, and other factors. Inpatient nonacute services, medical education, and certain organ acquisition costs related to Medicare beneficiaries are paid based upon cost reimbursement methods, established fee screens, or a combination thereof. FMLH and CMH are reimbursed for cost reimbursement items at tentative rates with final settlement determined after submission of annual cost reports and audits thereof by the Medicare fiscal intermediary. FMLH’s and CMH’s cost reports have been audited by the Medicare fiscal intermediary through December 31, 2002 and December 31, 2005, respectively.

Medicaid – Inpatient and outpatient services rendered to Medicaid program beneficiaries are reimbursed primarily based upon prospectively determined rates.

Milwaukee County (General Assistance Medical Program (GAMP) – FMLH has agreed to provide acute care to the medically indigent patients that qualify for GAMP. Milwaukee County has established a total maximum reimbursement level to FMLH for care provided under the GAMP program of approximately $9,200,000 in 2007 and 2006. FMLH recognized GAMP revenue at the maximum reimbursement level for both 2007 and 2006. Prior to meeting the maximum reimbursement level, services rendered to Milwaukee County patients covered by GAMP were reimbursed at 33% for inpatient and 17% for outpatient of FMLH’s gross charges in 2007 and 34% for inpatient and 20% for outpatient of FMLH’s gross charges in 2006.

There are various other proposals at the federal and state levels that could, among other things, reduce reimbursement rates, modify reimbursement methods, or increase managed care penetration, including Medicare and Medicaid. The ultimate outcome of these proposals and other market changes cannot presently be determined.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

18 (Continued)

The percentage of net patient service revenue applicable to services provided to Medicare, Medicaid, and GAMP patients was approximately 36% and 37% in 2007 and 2006, respectively. Laws and regulations governing the Medicare and Medicaid programs are extremely complex and subject to interpretation. As a result, there is at least a reasonable possibility that recorded estimates will change by material amounts in the near term. F&CH believes it is in compliance, in all material respects, with all applicable laws and regulations and is not aware of any pending or threatened investigations involving allegations of potential wrongdoing. While no such regulatory inquiries have been made, compliance with such laws and regulations may be subject to future government review and interpretation. Noncompliance with such laws and regulations could result in repayments of amounts improperly reimbursed, substantial monetary fines, civil and criminal penalties, and exclusion from the Medicare and Medicaid programs.

F&CH, FMLH, and CMH also have entered into reimbursement agreements with certain commercial insurance carriers and managed care organizations. The basis for reimbursement under these agreements includes prospectively determined rates per discharge, discounts from established charges, and prospectively determined per diem rates.

For the years ended December 31, 2007 and 2006, the consolidated statements of operations include approximately $2,724,000 and $4,352,000, respectively, as an increase in net patient service revenue for changes in estimates related to third-party contractual allowances and favorably determined retroactive settlements with third-party payors.

(8) Concentration of Credit Risk

F&CH grants credit without collateral to its patients, most of who are local residents and are insured under third-party payor agreements. The mix of accounts receivable from patients and third-party payors as of December 31, 2007 and 2006 is as follows:

2007 2006

Medicare 17% 16%Medicaid 2 3Managed care/contracted payor 59 57Self-pay 15 17Other 7 7

100% 100%

(9) Community Support

F&CH provides uncompensated care based on the cost of providing care to patients, in accordance with established policies. F&CH provides care to patients who meet certain criteria under its charity care policy without charge or at amounts less than its established rates. Because F&CH does not pursue collection of amounts determined to qualify as charity care, they are not reported as revenue. In addition, F&CH provides substantial community benefit through the provision of services to individuals supported by public programs, such as Medicare, Medicaid, and GAMP, through medical education and research and through a variety of other community benefit initiatives. Costs of providing community support are

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

19 (Continued)

developed using internal financial and cost accounting systems. The summary of F&CH’s community support for the years ended December 31, 2007 and 2006 is as follows (in thousands):

Unaudited, at cost2007 2006

Community support:Charity care $ 14,471 14,954 Bad debt 15,977 16,905 Medicare costs in excess of reimbursement 44,652 51,616 Medicaid and GAMP costs in excess of reimbursement 35,898 25,568 Medical education and research 38,547 35,761 Other community activities and support 8,590 8,845

Total community support $ 158,135 153,649

(10) Related Organizations and Other Significant Transactions

United/Dynacare, LLC

United/Dynacare, LLC is an independent diagnostic services provider of which FHS has a 50% ownership interest. FHS has an investment in United/Dynacare, LLC of approximately $10,456,000 and $3,645,000 at December 31, 2007 and 2006, respectively, included in investments in unconsolidated affiliates on the consolidated balance sheets. For the years ended December 31, 2007 and 2006, FHS recorded other operating revenue of approximately $8,810,000 and $7,713,000, respectively, included in the consolidated statements of operations, for FHS’s share of United/Dynacare, LLC’s net earnings. During 2007 and 2006, partnership distributions of approximately $2,000,000 and $7,500,000, respectively, were received from United/Dynacare, LLC. FMLH purchased laboratory services of approximately $37,123,000 and $35,066,000 from United/Dynacare, LLC in 2007 and 2006, respectively, which are included in contract services in the consolidated statements of operations.

Milwaukee Center for Diagnostic Imaging

FHS has a 40% investment in a joint venture, The Milwaukee Center for Diagnostic Imaging (MCDI), with an unrelated party. FHS has an investment in MCDI of approximately $1,271,000 and $1,094,000 at December 31, 2007 and 2006, respectively, included in investments in unconsolidated affiliates on the consolidated balance sheets. For the years ended December 31, 2007 and 2006, FHS recorded other operating revenue of approximately $954,000 and $685,000, respectively, included in the consolidated statements of operations, for FHS’s share of MCDI’s net earnings. During 2007 and 2006, partnership distributions of approximately $777,000 and $1,376,000, respectively, were received from MCDI.

Wisconsin Renal Care Group, LLC

FHS has a 45% ownership interest in a joint venture, Wisconsin Renal Care Group, LLC, (WRCG), with an unrelated party. FHS has an investment in WRCG of approximately $3,867,000 and $2,485,000 at December 31, 2007 and 2006, respectively, included in investments in unconsolidated affiliates on the consolidated balance sheets. For the years ended December 31, 2007 and 2006, FHS recorded other operating revenue of approximately $1,687,000 and $1,100,000, respectively, included in the consolidated

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

20 (Continued)

statements of operations, for FHS’s share of WRCG’s net earnings. During 2007 and 2006, partnership distributions of approximately $306,000 and $1,026,000, respectively, were received from WRCG.

Froedtert/MCW Clinics, LLC

FHS has a 75% ownership interest in a joint venture, Froedtert/MCW Clinics, LLC, with MCW. In accordance with the joint venture agreement, 75% of the losses and earnings of the joint venture are funded by or allocated to FHS and 25% funded by or allocated to MCW. Control of the joint venture is equally vested in both parties. FHS’s pro rata share of Froedtert/MCW Clinics, LLC’s net loss was approximately $(2,720,000) and $(3,912,000) in 2007 and 2006, respectively, recorded in other operating revenue in the consolidated statements of operations. Included in accounts payable on the consolidated balance sheets at December 31, 2007 and 2006 was approximately $886,000 and $965,000, respectively, for FHS’s unfunded pro rata share of Froedtert/MCW Clinics, LLC’s net deficit.

Vanguard Health Services, Inc.

CHCS holds 40% of the common stock of Vanguard Health Services, Inc. (Vanguard), a for-profit medical equipment and infusion therapy provider. CHCS’s investment in Vanguard of approximately $3,635,000 and $3,362,000 at December 31, 2007 and 2006, respectively, is included in investments in unconsolidated affiliates on the consolidated balance sheets. For the years ended December 31, 2007 and 2006, CHCS recorded other operating revenue of approximately $362,000 and $393,000, respectively, included in the consolidated statements of operations, for CHCS’s share of Vanguard’s net earnings.

Menomonee Falls Ambulatory Surgery Center

Menomonee Falls Ambulatory Surgery Center (MFASC) is a limited liability partnership between CMH and two nonaffiliated clinics formed to construct and operate an ambulatory surgery center on CMH’s campus. CMH has a 15% interest in the equity and net income or loss of MFASC. CMH’s investment in MFASC was $971,000 and $775,000 at December 31, 2007 and 2006, respectively, included in investments in unconsolidated affiliates. For the years ended December 31, 2007 and 2006, CMH recorded other operating revenue of approximately $772,000 and $758,000, respectively, included in the consolidated statements of operations, for CMH’s share of MFASC’s net earnings. During 2007 and 2006, partnership distributions of approximately $576,000 and $786,000, respectively, were received from MFASC.

Quality Health Solutions, Inc.

Quality Health Solutions, Inc. (QHS) was organized in 2005 for purposes of developing initiatives that improve the quality of medical services, promote healthcare delivery based on measured quality, and provide innovative care delivery methods. F&CH has a one-third interest in QHS, with the remaining interest divided equally between ThedaCare, Inc. and Bellin Health Systems, Inc. The investment in QHS was $17,000 and $55,000 at December 31, 2007 and 2006, respectively, included in investments of unconsolidated affiliates on the consolidated balance sheets. During 2005, F&CH also provided start-up funding in the amount of $100,000 that will be repaid by QHS, with interest, on or before June 30, 2010 as evidenced by a promissory note between the parties. For the year ended December 31, 2007 and 2006, F&CH recorded other operating loss of approximately $(38,000) and $(59,000), respectively, included in the consolidated statements of operations, for F&CH’s share of QHS’s net loss.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

21 (Continued)

Critical Care Solutions, LLC

Critical Care Solutions, LLC (CCS) is a limited liability partnership between F&CH and two unrelated parties, ThedaCare, Inc. and Bellin Health Systems, Inc., that began operations in 2005 as a provider of electronic ICU monitoring services. F&CH has a 33% ownership interest in CCS. During start-up, F&CH provided approximately $1,636,000 in funding for equipment and operations that will be repaid by CCS on or before December 1, 2014. A promissory note receivable in the amount of $1,474,000 is included on the consolidated balance sheets of F&CH at December 31, 2007 and 2006. The investment in CCS of $146,000 and $121,000 at December 31, 2007 and 2006, respectively, is included in investments of unconsolidated affiliates on the consolidated balance sheets. F&CH recorded other operating gain of $37,000 in 2007 and an operating loss of $(103,000) in 2006, included in the consolidated statements of operations, for F&CH’s share of CCS.

Kyron Clinical Imaging, Inc.

Kyron Clinical Imaging, Inc. (Kyron) was organized in 2004 for purposes of offering advanced software and services used to diagnose, treat, and manage soft tissue cancers with an initial focus on brain tumors. FHS has a 10% ownership in Kyron. FHS invested $1,500,000 in both 2007 and 2006 for start-up capital. The investment in Kyron of $3,000,000 and $1,500,000 at December 31, 2007 and 2006, respectively, is included in investments in unconsolidated affiliates on the consolidating balance sheets. FHS recorded no operating gain or loss on this investment during 2007 or 2006.

FMLH MCW Real Estate Ventures, LLC

FMLH MCW Real Estate Ventures, LLC (Real Estate Ventures) is a limited liability partnership between FHS and MCW that began operations in 2007. FHS has a 50% ownership in Real Estate Ventures. The purpose of Real Estate Ventures is to provide a platform for ongoing real estate ownership, development and/or leasing to contribute to the owner’s missions, and strategic initiatives. FHS paid $3,218,000 in 2007 for Real Estate Ventures to purchase a parcel of land. The investment in Real Estate Ventures of $3,218,000 at December 31, 2007 is included in investments of unconsolidated affiliates on the consolidated balance sheets.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

22 (Continued)

The following represents summary financial data (unaudited) for the aforementioned unconsolidated affiliates (in thousands):

2007Total

Total Total Total net incomeassets equity net revenue (loss)

United/Dynacare, LLC $ 35,274 24,912 70,957 17,620 MCDI 5,961 3,177 11,678 2,385 WRCG 13,208 10,777 11,369 3,748 Froedtert/MCW Clinics, LLC 3,461 2,204 14,457 (2,459) Vanguard 13,489 8,940 21,768 897 MFASC 7,635 4,958 13,413 5,807 QHS 163 52 132 (109) CCS 3,731 437 5,441 37 Kyron 1,512 1,410 196 (1,078) Real Estate Ventures 6,436 6,436 — (5)

2006Total

Total Total Total net incomeassets equity net revenue (loss)

United/Dynacare, LLC $ 19,659 11,091 63,837 15,426 MCDI 5,819 2,734 10,488 1,713 WRCG 7,091 5,889 9,907 2,347 Froedtert/MCW Clinics, LLC 3,603 2,302 11,606 (4,573) Vanguard 12,913 8,444 20,952 939 MFASC 8,130 5,261 12,657 4,910 QHS 206 165 196 (181) CCS 3,817 364 4,325 (338) Kyron 913 913 — (584)

Fitness Development Associates, LLC

FHS has a 40% ownership in a joint venture, Fitness Development Associates, LLC (Fitness Center). In December of 2004, FHS guaranteed $3,640,000 of debt of the Fitness Center. The debt is for six years with a balloon payment in December 2010 and an interest rate of 6.25%. FHS recorded the fair value of its guarantee of $526,000 and $694,000 at December 31, 2007 and 2006, respectively, as an investment and a corresponding other long-term liability on the consolidated balance sheets.

United Hospital System, Inc.

FMLH and FHS entered into a membership and affiliation agreement with United Hospital System, Inc. (UHS), a not-for-profit corporation located in Kenosha, Wisconsin, for the purpose of integrating activities in order to benefit the patients and communities served. FMLH records its investment in UHS of

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

23 (Continued)

$15,000,000 under the cost basis. The investment in UHS is noninterest bearing and unsecured. The investment is included in deferred financing costs and other assets on the consolidated balance sheets.

Medical College of Wisconsin

On December 31, 2003, an end-user access agreement was signed between FMLH and MCW for software license rights on FMLH’s Epic software for a payment of $5,000,000 permitting MCW access for 10 years. MCW agreed to prepay the user access fees in two installments of $2,500,000 on both December 31, 2004 and 2003. FMLH recognized $500,000 in user fee income in 2007 and 2006 that is included in other operating revenue in the consolidated statements of operations. The remaining $3,000,000 and $3,500,000 that has not been recognized as income is included in deferred revenue and other long-term liabilities at December 31, 2007 and 2006, respectively, on the consolidated balance sheets.

Froedtert Surgery Center, LLC

During 2004, FHS invested $1,200,000 for a 60% ownership in a joint venture, Froedtert Surgery Center, LLC (FSC) with MCW and Advanced. MCW and Advanced each owned a 20% interest in FSC. FSC began operations in March 2005. The 2005 F&CH consolidated financial statements include the balance sheets and statements of operations for the FSC and a minority interest. During 2006, FHS sold 10% of its interest to MCW for $300,000, which included a gain of $151,000 included in other operating revenue in the 2006 consolidated statement of operations. Subsequent to the sale, FHS retains majority board representation. In 2005, FMLH constructed a new building (Sargeant Health Center) that is being leased to FSC and MCW. FSC leases a portion of the Sargeant Health Center under an operating lease over a 20-year term with base rent adjusting annually based on consumer price index (CPI) increases. The lease revenue from MCW for the Sargeant Health Center was $755,000 and $1,053,000 in 2007 and 2006, respectively.

LindenGrove, Inc.

LindenGrove, Inc. (LindenGrove) is a separate Wisconsin nonstock, not-for-profit corporation. LindenGrove provides elder care services in Waukesha County, Wisconsin. Certain officers and members of the board of directors of CMH are also members of the board of directors of LindenGrove. No financial interest is recognized in the accompanying consolidated financial statements for LindenGrove as CMH does not exercise control over the entity and has no economic interest or rights to LindenGrove’s net assets.

(11) Accounts Receivable Sale

FMLH sells, with limited recourse, some of its nongovernmental patient accounts receivable in a revolving period sales arrangement up to a maximum of $12,000,000. FMLH does not include the sold receivables on the consolidated balance sheets. Receivables sold at December 31, 2007 and 2006 totaled approximately $11,999,000. No gain or loss resulted from the sale. FMLH expensed costs totaling approximately $419,000 and $505,000 in 2007 and 2006, respectively, relating to the sale.

In connection with the sale, FMLH was required to purchase a capital participation certificate of the purchaser for 15% of the maximum receivables eligible for sale, or $1,800,000. Investment income of approximately $84,000 and $61,000 was earned by FMLH on the certificate in 2007 and 2006.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

24 (Continued)

Additionally, FMLH has entered into a subordinated note agreement of approximately $1,349,000 and $1,342,000 at December 31, 2007 and 2006, respectively. The subordinated note agreement allows the purchaser to recover uncollected accounts receivable against this subordinated note only if FMLH does not fulfill its obligations to buy back any uncollectible accounts.

The capital participation certificate and the subordinated note are accounted for as retained interests and are reflected at estimated fair value in current assets whose use is limited. FMLH generally estimates fair value, based upon the present value of future cash flows, using management’s best estimates of key assumptions such as default rates and payment cycles. Because the expected payment cycle averages approximately 80 days, no discount rate has been applied in estimating the fair value of FMLH’s retained interests at December 31, 2007 and 2006.

The accounts receivable agreement may be terminated by providing 180 days’ notice. Upon termination of the agreement, the capital participation certificate and the subordinated note are refundable and available for current FMLH operations to the extent not needed to fund uncollectible accounts.

(12) Froedtert Memorial Lutheran Hospital Trust

FMLH is a beneficiary of the Froedtert Memorial Lutheran Hospital Trust (the Trust). The Trust holds variance power over the assets of the Trust and can redirect to whom the assets are given; therefore, the Trust’s assets are not included in the accompanying consolidated financial statements. Distributions are made at the discretion of the trustees.

(13) Employee Benefit Plans

Defined Contribution Plans

FMLH has a defined contribution pension plan covering substantially all FMLH employees. FMLH contributes 3% of eligible employee compensation. FMLH has a 403(b) thrift plan whereby substantially all employees are eligible to make before-tax contributions to the plan. FMLH will match one-half of such employee contributions up to a maximum amount as defined in the plans. FMLH’s contributions to these plans are made annually. FMLH’s pension expense for the defined contribution pension plan and the 403(b) thrift plan was $8,891,000 and $8,285,000 in 2007 and 2006, respectively. CHCS has a 403(b) thrift plan whereby substantially all of CHCS employees are eligible to make before-tax contributions to the plan. CHCS also has a corresponding 401(a) plan in which CHCS will match 50% of the first 5% of the employees’ salary deferral contributions to the 403(b) plan not to exceed 2.5% of each employee’s salary. CHCS’ contributions to the 401(a) plan are made annually. CHCS pension expense for the 401(a) plan was $912,000 and $809,000 for the years ending December 31, 2007 and 2006, respectively.

Defined Benefit Plans

FMLH has a defined benefit plan (the FMLH Plan) that covers certain former Milwaukee County employees who became employees of FMLH. FMLH and United/Dynacare, LLC are responsible for funding 10% of the FMLH plan, with Milwaukee County funding 90%. The Hospital has recorded the

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

25 (Continued)

difference between the projected benefit obligation and the fair market value of plan. There is a corresponding long-term receivable from United/Dynacare, LLC and Milwaukee County for their portion of the unfunded projected benefit obligation of $9,480,000 and $975,000 at December 31, 2007 and 2006, respectively, included in deferred financing costs and other assets, net in the consolidated balance sheets. FMLH’s pension expense for the FMLH Plan was approximately $387,000 and $454,000 in 2007 and 2006, respectively.

In September of 2006, the FASB issued Statement of Financial Accounting Standards (SFAS) No. 158, Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans—an amendment of FASB Statements No. 87, 88, 106, and 132 (R), effective for fiscal years ending after December 15, 2007. FASB No. 158 requires recognition in the consolidated balance sheet of the funded status of defined benefit pension plans and other postretirement plans, including all previously unrecognized actuarial gains and losses and unamortized prior service cost, as a component of unrestricted net assets. FMLH adopted FASB No. 158 effective December 31, 2007 by recording the unfunded status of the plan as noted above and through a direct reduction of unrestricted net assets totaling $1,261,000. There was no impact on the consolidated results of operations or cash flows.

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

26 (Continued)

Data relative to the FMLH Plan for 2007 and 2006 follows (in thousands):

2007 2006

Change in pension benefit obligation:Pension benefit obligation at beginning of year $ 41,170 37,304 Service cost 877 960 Interest cost 2,327 2,023 Actuarial loss (gain) (1,511) 1,543 Benefits and expenses paid (794) (660)

Pension benefit obligation at end of year 42,069 41,170

Change in plan assets:Fair value of plan assets at beginning of year 28,794 24,071 Actual return on plan assets 1,752 2,971 Employer contributions 2,670 2,615 Benefits and expenses paid (994) (863)

Fair value of plan assets at end of year 32,222 28,794

Reconciliation of funded status:Funded status (9,847) (12,376) Unrecognized actuarial loss 9,338 11,059 Unrecognized transition obligation 717 948 Unrecognized prior service cost 277 319

Net amount recognized at year-end $ 485 (50)

Amounts recognized in the accompanying consolidatedbalance sheets:

Accrued benefit liability $ (9,847) (4,188) Intangible asset — 1,267 Accrued minimum pension liability 10,332 2,871

$ 485 (50)

Net periodic pension cost is comprised of the following:Service cost $ 1,089 960 Interest cost on projected benefit obligation 2,327 2,023 Expected return on plan assets (2,360) (1,975) Net amortization and deferral 273 1,335 Recognized actuarial loss 806 —

Net periodic pension cost $ 2,135 2,343

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

27 (Continued)

2007 2006

Assumptions used:Discount rate – benefit obligation 6.00% 5.75%Discount rate – net periodic pension cost 5.75 5.50Average rate of compensation increase:

Benefit obligation 4.50 4.50Net periodic pension cost 4.50 4.50

Expected return of plan assets 7.50 8.00

The long-term rate of return on assets reflects historical returns and future expectations for returns in each asset class, as well as targeted asset allocation percentages within the pension portfolio. FMLH’s investment strategy is of a long-term nature and is intended to ensure that funds are available to pay benefits as they become due and to maximize the Trust’s total return at an appropriate level of investment risk.

The employer contribution for the FMLH Plan for the year ending December 31, 2008 is estimated to be $1,202,000. The benefits expected to be paid in each year from 2008 through 2012 are expected to be $1,442,000, $1,559,000, $1,736,000, $1,948,000, and $2,130,000, respectively. The aggregate benefits to be paid in the five years from 2013 through 2016 are expected to be $14,483,000. The expected benefits to be paid are based on the same assumptions used to measure the projected benefit obligation at December 31, 2007.

The weighted average asset allocation of the pension plan at December 31 follows:

2007 2006

Equity securities 60% 63%Debt securities 30 35Cash and equivalents 10 2

Total 100% 100%

FMLH intends to provide an appropriate range on investment options that span the risk/return spectrum. The investment options will allow for construction of a portfolio consistent with plan circumstances, goals, time horizons, and tolerance for risk. Major asset classes to be offered include:

TargetAsset class percentage

Equity securities 50% – 70%Debt securities 30% – 50%Other —%

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

28 (Continued)

CHCS is the sponsor of a noncontributory, defined benefit pension plan (the CHCS Plan), which covers substantially all employees of CHCS who work at least 1,000 hours in a 12-consecutive month period. CHCS funds the amount calculated by the CHCS Plan’s consulting actuary to meet the minimum Employee Retirement Income Security Act funding requirements. The CHCS Plan uses the projected-unit- credit-cost actuarial method. The CHCS Plan amortizes prior service cost on a straight-line basis over the average remaining service period of employees expected to receive benefits under the CHCS Plan. Actuarial gains or losses are deferred to the extent that, as of the beginning of the year, the unrecognized net gain or loss does not exceed 10% of the greater of the projected benefit obligation or the fair value of plan assets. If recognition is required, the excess gain or loss is amortized in the same manner as the prior service cost.

CHCS adopted SFAS No. 158 effective December 31, 2007 through a direct reduction of unrestricted net assets totaling $4,282,000. There was no impact on the consolidated results of operations or cash flows.

Data relative to the CHCS Plan follows (in thousands):

2007 2006

Change in projected benefit obligation:Projected benefit obligation at beginning of year $ 50,725 48,557 Service cost 2,400 2,489 Interest cost 3,003 2,759 Actuarial gain (3,670) (1,716) Benefits paid (1,365) (1,364) Plan amendment (1,017) —

Projected benefit obligation at end of year 50,076 50,725

Change in plan assets:Fair value of plan assets at beginning of year 39,574 36,039 Actual return on plan assets 1,434 3,682 Employer contributions 1,613 1,217 Benefits paid (1,365) (1,364)

Fair value of plan assets at end of year 41,256 39,574

Reconciliation of funded status:Funded status (8,820) (11,151) Unrecognized net loss — 7,458 Unrecognized prior service cost — 874

Net amount recognized at end of year $ (8,820) (2,819)

Amounts recognized in the accompanying consolidatedbalance sheets:

Accrued pension liability $ 8,820 2,821 Recognized accrued pension cost $ 8,820 2,821

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

29 (Continued)

2007 2006

Amounts not yet reflected in net periodic benefit costs andincluded as an accumulated reduction to unrestrictednet assets:

Prior service cost $ 395 — Accumulated loss 3,887 —

Unrecognized pension costs $ 4,282 —

Net periodic pension cost consists of the following:Service cost $ 2,400 2,489 Interest cost 3,003 2,760 Expected return on plan assets (2,946) (2,659) Net amortization and deferral 485 792 FAS 88 curtailment expense 390 —

Net periodic pension cost $ 3,332 3,382

Assumptions used:Discount rate for measurement of pension obligation 6.00% 6.00%Discount rate for determining net periodic pension cost 6.00 5.75Rate of increase in compensation levels 4.90 4.90Expected long-term rate of return on assets 7.75 7.75

The long-term rate of return on assets reflects historical returns and future expectations for returns in each asset class, as well as targeted asset allocation percentages within the pension portfolio. CHCS’ investment strategy is of a long-term nature and is intended to ensure that funds are available to pay benefits as they become due and to maximize the investments’ total return at an appropriate level of investment risk.

The minimum employer contributions for the CHCS Plan for the year ending December 31, 2008 are estimated to be $1,860,000. The benefits expected to be paid in each year from 2008 through 2012 are approximately $1,440,000, $1,554,000, $1,723,000, $1,897,000, and $2,099,000, respectively. The aggregate benefits to be paid in the five years from 2013 through 2017 are approximately $13,844,000. The expected benefits to be paid are based on the same assumptions used to measure the projected benefit obligation at December 31, 2007.

The weighted average asset allocation of the CHCS Plan at December 31 follows:

2007 2006

Equity securities 64% 64%Debt securities 35 35Other 1 1

Total 100% 100%

FROEDTERT & COMMUNITY HEALTH, INC. AND AFFILIATES

Notes to Consolidated Financial Statements

December 31, 2007 and 2006

30 (Continued)

CHCS intends to provide an appropriate range on investment options that span the risk/return spectrum. The investment options will allow for construction of a portfolio consistent with plan circumstances, goals, time horizons, and tolerance for risk. Major asset classes to be offered include:

TargetAsset class percentage

Equity securities 50% – 70%Debt securities 30% – 50%Other —%

Effective December 31, 2007, the CHCS Plan will no longer accept new participants. No additional benefits will accrue for participants who have not attained ago 40 or those will less than 5 years of vesting service as of December 31, 2007. Participation in a defined contribution plan will be offered to participants who were affected by this change.

Post Retirement Medical Plan

FMLH has an unfunded post retirement medical plan (the FMLH Medical Plan) that covers certain former Milwaukee County employees who became employees of FMLH. These employees had less than 15 years of vesting service and were not vested in Milwaukee County’s post retirement medical benefit plan. FMLH is responsible for providing the post retirement benefit coverage for this population if they achieve 15 years of vesting service (Milwaukee County & Froedtert combined) and they retire from the Hospital.

The projected benefit obligation at December 31, 2007 and 2006 using a discount rate of 6.00% and 5.75% was $2,822,000 and $2,786,000, respectively.

(14) Professional Liability Insurance

FMLH and CMH have professional liability insurance for claim losses of less than $1,000,000 per claim and $3,000,000 per year for professional liability claims incurred during a policy year, regardless of when the claim is reported (claims-occurred basis). Losses in excess of these amounts are covered through the FMLH and CMH mandatory participation in the Injured Patients’ and Families Compensation Fund of the State of Wisconsin.

(15) Commitments and Contingencies

Leases