12

From Cottage to Global… Challenges and Opportunities facing Australian Wine Companies James Lovell, Vice-President Global Supply Chain Planning 2006 ABARE Conference 2 March 2006

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | dominick-mcdonald |

| View: | 215 times |

| Download: | 1 times |

From Cottage to Global… Challenges and Opportunities facing Australian Wine Companies

James Lovell, Vice-President Global Supply Chain Planning2006 ABARE Conference2 March 2006

CONSUMER LED & CUSTOMER

DRIVEN

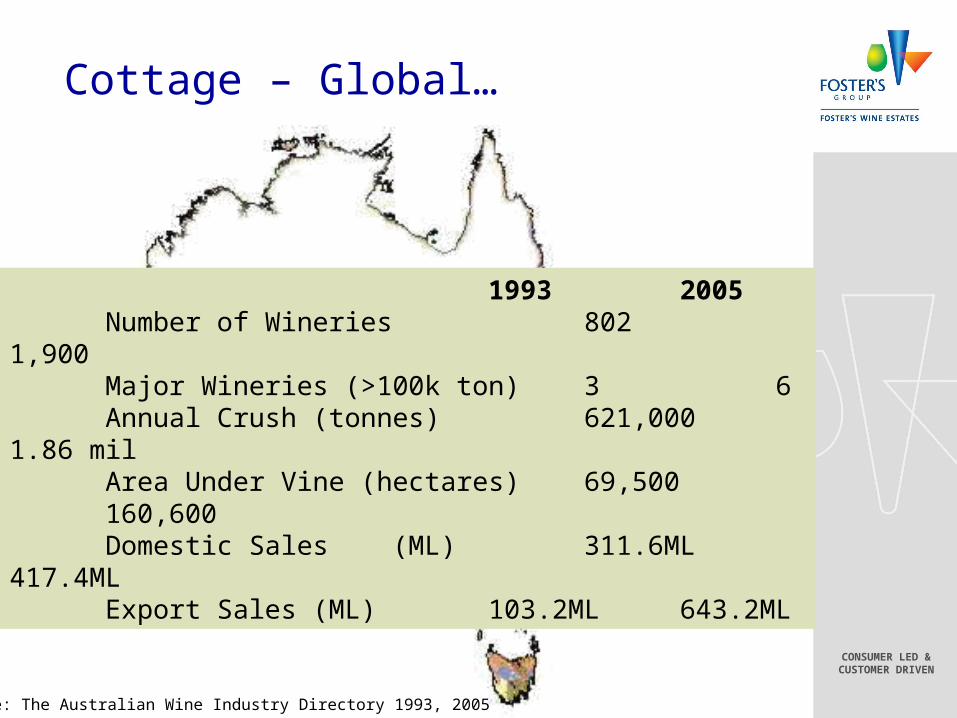

Cottage – Global…

1993 2005Number of Wineries 802 1,900Major Wineries (>100k ton) 3 6Annual Crush (tonnes) 621,000 1.86 milArea Under Vine (hectares) 69,500 160,600Domestic Sales (ML) 311.6ML 417.4MLExport Sales (ML) 103.2ML 643.2ML

Source: The Australian Wine Industry Directory 1993, 2005

CONSUMER LED & CUSTOMER

DRIVEN

Area Under Vine

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1881

1891

1901

1911

1921

1931

1941

1951

1961

1971

1981

1991

2001

2005Source: Vintage: The Australian Wine Industry Statistical Yearbook 2002

Hectares

CONSUMER LED & CUSTOMER

DRIVEN

Beverage Wine Production

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1923

1933

1941

1951

1961

1971

1981

1991

2001

2005

Unfortified Fortified

Source: Vintage: The Australian Wine Industry Statistical Yearbook 2002

CONSUMER LED & CUSTOMER

DRIVEN

2004 Share of Production

Chardonnay

18%Other White

25%

Other Red

12%

Multipurpose

4%

Shiraz

24%

Cabernet

Sauvignon17%

Varietal Mix

Source: Vintage: Australian Wine & Brandy Corporation

1982 Share of Production

Chardonnay1%

Other White

40%

Other Red

16%

Multipurpose

24%

Shiraz

13%Cabernet

Sauvignon6%

CONSUMER LED & CUSTOMER

DRIVEN

Introduction

Leadership Drives Change

Evolution Takes Time

Opportunities and ChallengesSUCCESS!

Then… Now…

CONSUMER LED & CUSTOMER

DRIVEN

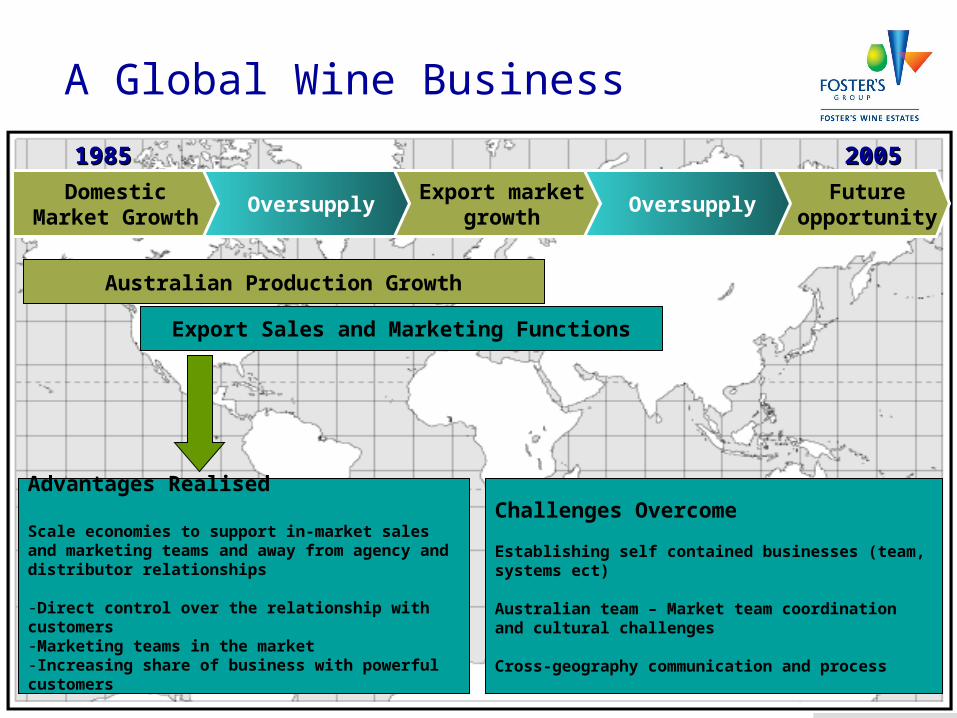

Future opportunity

OversupplyExport market

growthOversupply

Domestic Market Growth

A Global Wine Business

19851985 20052005

Australian Production Growth

Advantages Realised

Scale economics in wine manufacturing and packaging

Scale economies in component purchase

Specialist and technical expertise

Challenges Overcome

Manufacturing facility consolidation

Organisational complexity and process – from generalists to specialists

Systems and Technology implementation

(Acquisition integration)

CONSUMER LED & CUSTOMER

DRIVEN

Future opportunity

OversupplyExport market

growthOversupply

Domestic Market Growth

A Global Wine Business

19851985 20052005

Australian Production Growth

Export Sales and Marketing Functions

Advantages Realised

Scale economies to support in-market sales and marketing teams and away from agency and distributor relationships

-Direct control over the relationship with customers-Marketing teams in the market-Increasing share of business with powerful customers

Challenges Overcome

Establishing self contained businesses (team, systems ect)

Australian team – Market team coordination and cultural challenges

Cross-geography communication and process

CONSUMER LED & CUSTOMER

DRIVEN

Future opportunity

OversupplyExport market

growthOversupply

Domestic Market Growth

A Global Wine Business

19851985 20052005

Australian Production Growth

Export Sales and Marketing Department

Global Supply Chain

Advantages Realised

Increasing segment portfolio breadth and increased customer relevanceReduced business risk of a diverse, multi-country sourcing platformFurther scale to support in-market sales and marketing functionsGlobally leveraged supply chain expertise and economics

Challenges Overcome

Cultural barriers and organisational integration

Complexity, complexity, complexity – and the planning systems and operational structures to manage

Global supply chain implementation

CONSUMER LED & CUSTOMER

DRIVEN

Future opportunity

OversupplyExport market

growthOversupply

Domestic Market Growth

A Global Wine Business

19851985 20052005

Australian Production Growth

Export Sales and Marketing Department

Global Supply Chain

The Future – Winning the Wine Game

Advantages Realised

Multi-beverage route to market – sales/marketing scale and market power

Back-end integration with customers – VMI, service effectiveness and business insight

Bolt-on routes to market and further production sourcing options

Challenges Overcome

Cultural barriers and organisational integration, again

Standardising systems and process to benchmark FMCG

Retaining flexibility and responsiveness

(Acquisition Integration)

CONSUMER LED & CUSTOMER

DRIVEN

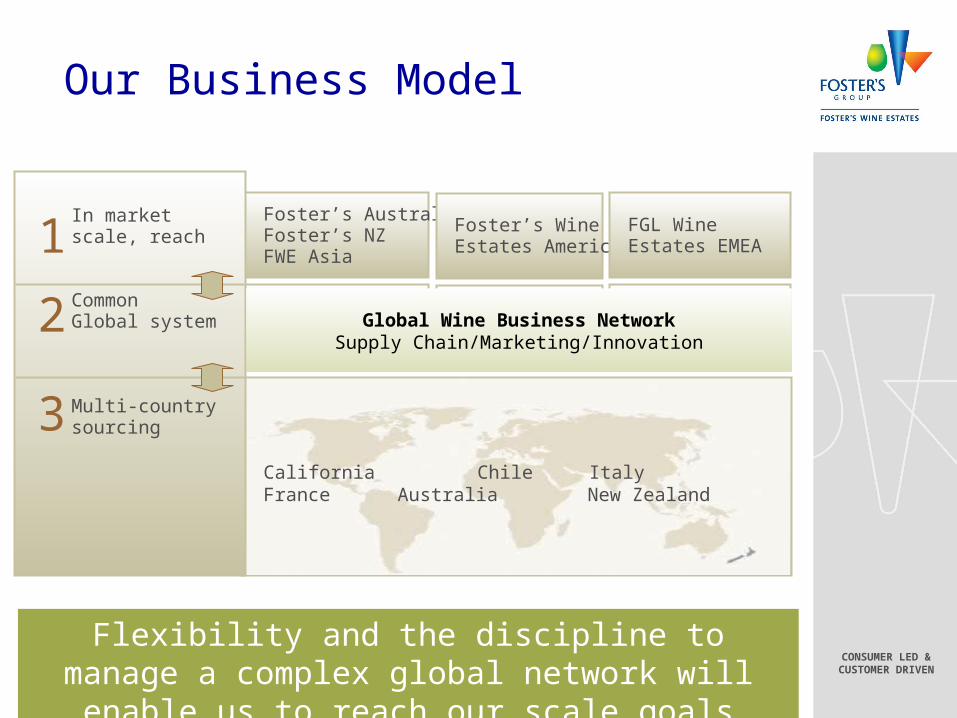

Our Business Model

Foster’s AustraliaFoster’s NZFWE Asia

Foster’s WineEstates Americas

FGL WineEstates EMEA

Branding Innovation Supply Chain

California Chile Italy France Australia New Zealand

In market scale, reach

CommonGlobal system

Multi-countrysourcing

1

2

3

Flexibility and the discipline to manage a complex global network will enable us to reach our scale goals

Global Wine Business NetworkSupply Chain/Marketing/Innovation

From Cottage to Global… Challenges and Opportunities facing Australian Wine Companies

James Lovell, Vice-President Global Supply Chain Planning2006 ABARE Conference2 March 2006