29

www.nsr.com © 2015 – NSR Future Satellite Applications and Services in Brazil and Worldwide Blaine Curcio Senior Analyst, NSR Brasília, Brazil 17 September 2015

www.nsr.com © 2015 – NSR

Future Satellite Applications and Services in Brazil and Worldwide

Blaine Curcio

Senior Analyst, NSR

Brasília, Brazil

17 September 2015

www.nsr.com © 2015 – NSR 2

Presentation Agenda

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

17 September 2015

About NSR

The Market Today: How Much, Where, and What Kind?

Future Markets for Traditional FSS—Video Markets Remain the Key

Revenue Generators

Future Markets for GEO-HTS—Data Applications Leading the Way

Potential Future Markets for Non GEO-HTS—Bigger Pie Due to

Cheaper Slices?

Bottom Line

2nd Annual Seminar on Spectrum Management--Brasilia

www.nsr.com © 2015 – NSR

About NSR

NSR is a Global Leader in Satellite Market Research and Consulting

Founded in 2000, NSR specializes in analysis of growth

opportunities across the satellite industry

NSR’s expert consultants are located globally and possess over 140 years of combined

industry experience.

Multi-Client Reports on Various Satellite Topics

Extensive Client Research, Consulting and Advisory Services

“Holistic” approach to research enables NSR to anticipate trends with a higher

degree of confidence and precision than the competition and stay ahead of the curve.

www.nsr.com

3

17 September 2015

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

2nd Annual Seminar on Spectrum Management--Brasilia

www.nsr.com © 2015 – NSR

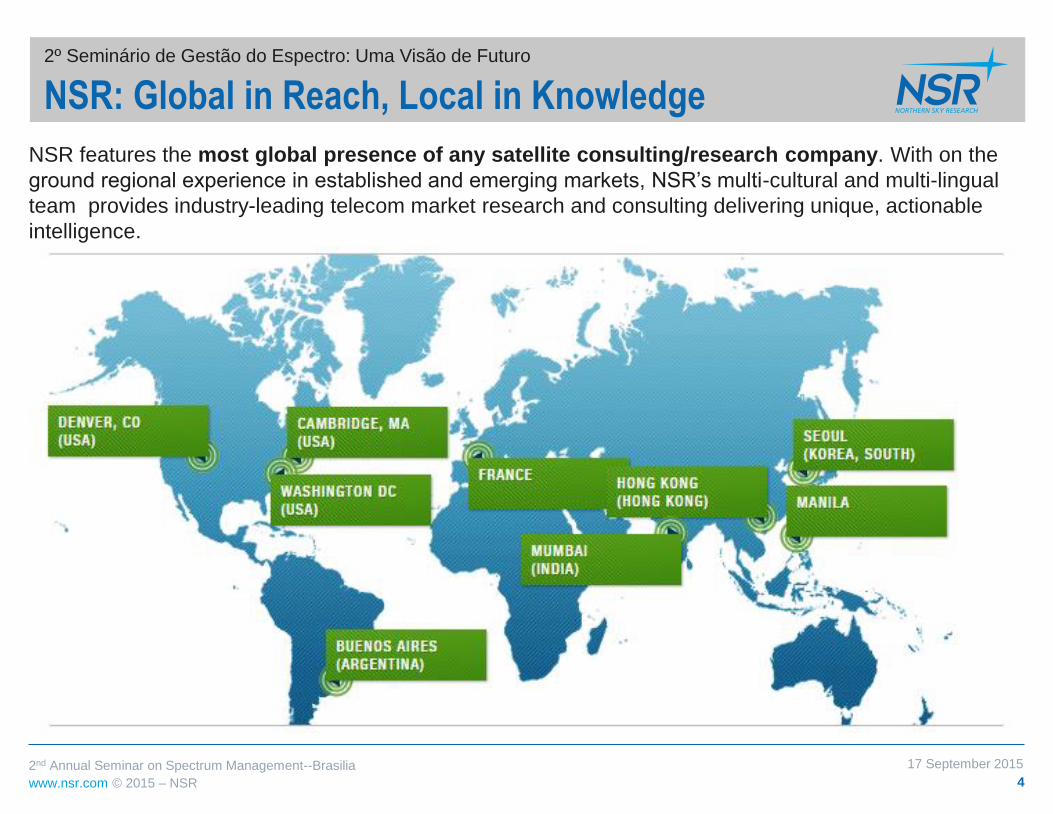

NSR features the most global presence of any satellite consulting/research company. With on the

ground regional experience in established and emerging markets, NSR’s multi-cultural and multi-lingual

team provides industry-leading telecom market research and consulting delivering unique, actionable

intelligence.

NSR: Global in Reach, Local in Knowledge

4

17 September 2015

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

2nd Annual Seminar on Spectrum Management--Brasilia

www.nsr.com © 2015 – NSR

The Market Today

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

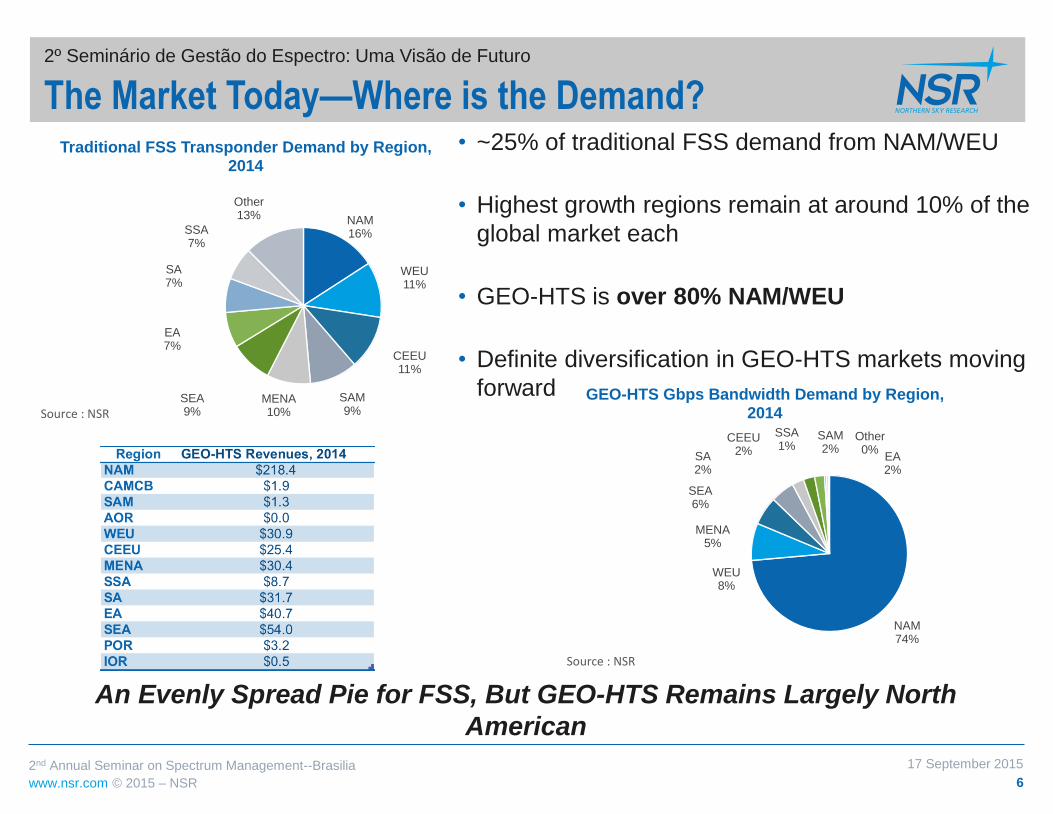

The Market Today—Where is the Demand?

6

An Evenly Spread Pie for FSS, But GEO-HTS Remains Largely North

American

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

NAM 16%

WEU 11%

CEEU 11%

MENA 10%

SAM 9%

SEA 9%

EA 7%

SA 7%

SSA 7%

Other 13%

Traditional FSS Transponder Demand by Region, 2014

Source:NSR

NAM 74%

WEU 8%

SEA 6%

MENA 5%

EA 2%

SA 2%

CEEU 2%

SSA 1%

SAM 2%

Other 0%

GEO-HTS Gbps Bandwidth Demand by Region, 2014

Source:NSR

• ~25% of traditional FSS demand from NAM/WEU

• Highest growth regions remain at around 10% of the

global market each

• GEO-HTS is over 80% NAM/WEU

• Definite diversification in GEO-HTS markets moving

forward

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

The Traditional FSS Market Today—Dominated by Video

7

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

0% 25% 50% 75% 100%

Traditional FSS Demand by Application, 2014

Distribution DTH Enterprise Data

Contribution & OUTV Gov/Mil Telephony & Carrier

Commercial Mobility Broadband Access Source:NSR

0% 25% 50% 75% 100%

Traditional FSS Demand by Application, 2014

Distribution DTH Enterprise Data

Contribution & OUTV Gov/Mil Telephony & Carrier

Commercial Mobility Broadband Access Source:NSR

0% 25% 50% 75% 100%

Traditional FSS Demand by Application, 2014

Distribution DTH Enterprise Data

Contribution & OUTV Gov/Mil Telephony & Carrier

Commercial Mobility Broadband Access Source:NSR

0% 25% 50% 75% 100%

Traditional FSS Demand by Application, 2014

Distribution DTH Enterprise Data

Contribution & OUTV Gov/Mil Telephony & Carrier

Commercial Mobility Broadband Access Source:NSR

0% 25% 50% 75% 100%

Traditional FSS Demand by Application, 2014

Distribution DTH Enterprise Data

Contribution & OUTV Gov/Mil Telephony & Carrier

Commercial Mobility Broadband Access Source:NSR

0% 25% 50% 75% 100%

Traditional FSS Demand by Application, 2014

Distribution DTH Enterprise Data

Contribution & OUTV Gov/Mil Telephony & Carrier

Commercial Mobility Broadband Access Source:NSR

0% 25% 50% 75% 100%

Traditional FSS Demand by Application, 2014

Distribution DTH Enterprise Data

Contribution & OUTV Gov/Mil Telephony & Carrier

Commercial Mobility Broadband Access Source:NSR

0% 25% 50% 75% 100%

Traditional FSS Demand by Application, 2014

Distribution DTH Enterprise Data

Contribution & OUTV Gov/Mil Telephony & Carrier

Commercial Mobility Broadband Access Source:NSR

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

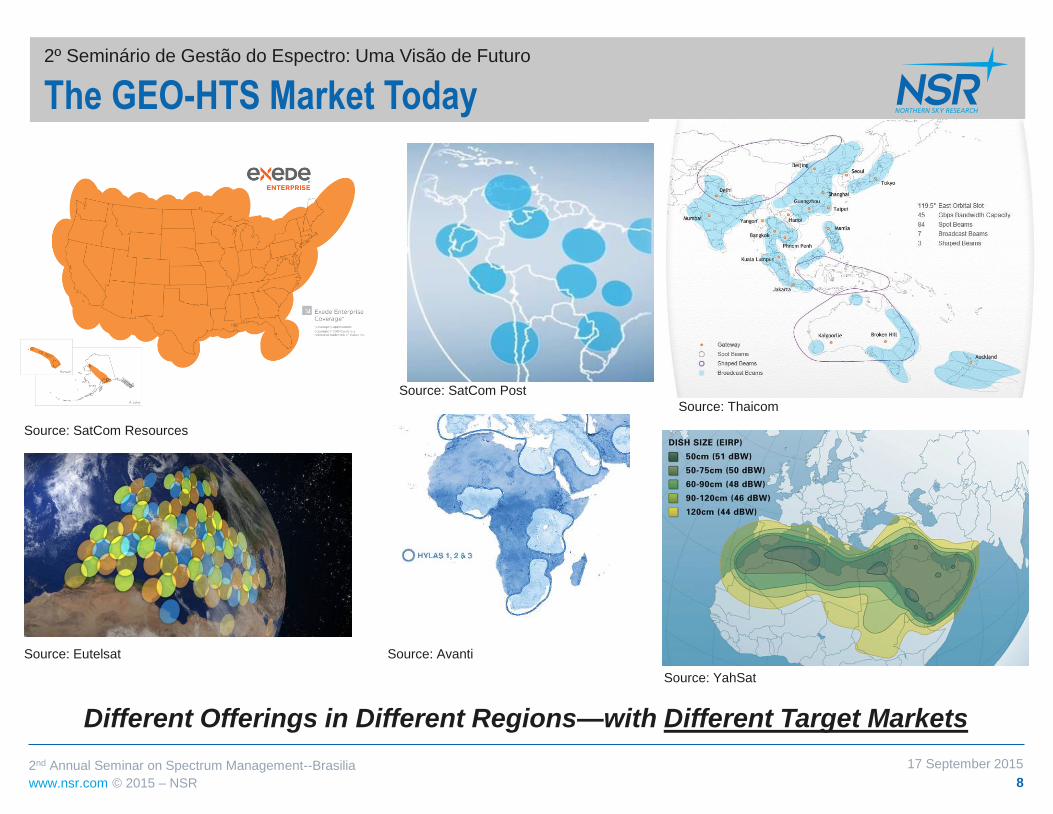

The GEO-HTS Market Today

8

Different Offerings in Different Regions—with Different Target Markets

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

Source: Eutelsat Source: Avanti

Source: YahSat

Source: Thaicom

Source: SatCom Post

Source: SatCom Resources

www.nsr.com © 2015 – NSR

The Market Tomorrow

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

Future Satellite Applications—Where Is Growth At the Highest Level?

10

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

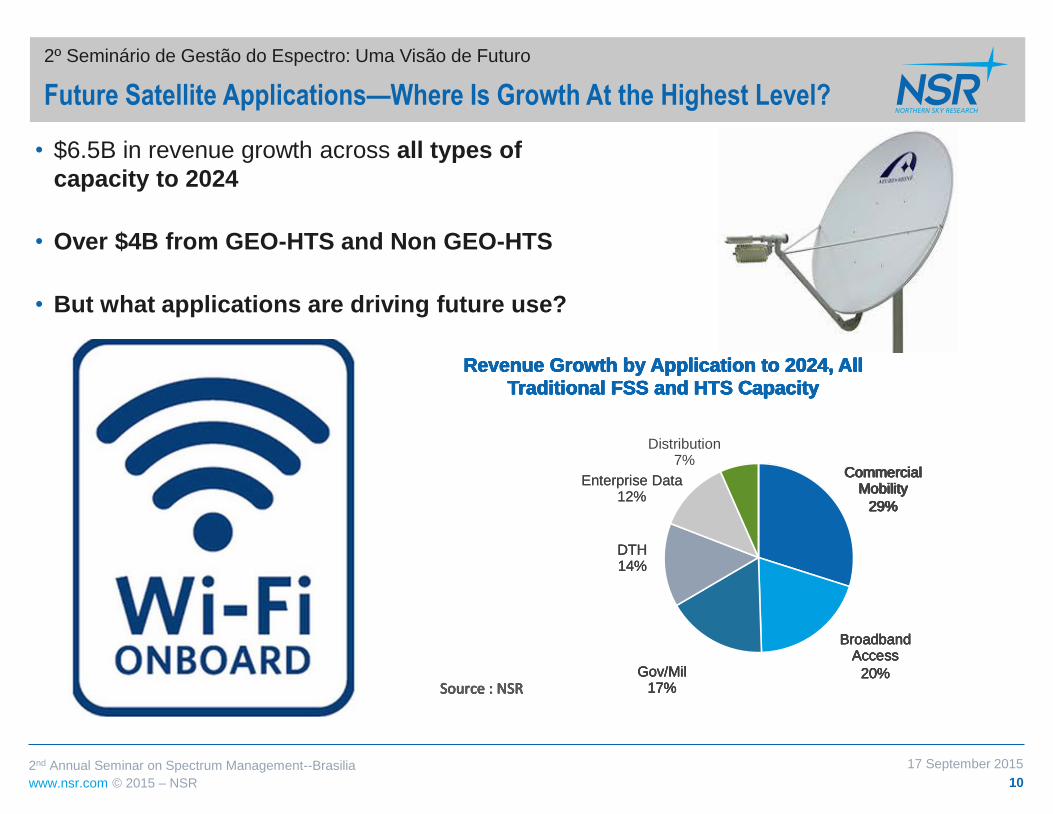

• $6.5B in revenue growth across all types of

capacity to 2024

• Over $4B from GEO-HTS and Non GEO-HTS

• But what applications are driving future use?

Commercial Mobility

29%

Revenue Growth by Application to 2024, All Traditional FSS and HTS Capacity

Source:NSR

Commercial Mobility

29%

Broadband Access

20%

Revenue Growth by Application to 2024, All Traditional FSS and HTS Capacity

Source:NSR

Commercial Mobility

29%

Broadband Access

20% Gov/Mil 17%

Revenue Growth by Application to 2024, All Traditional FSS and HTS Capacity

Source:NSR

Commercial Mobility

29%

Broadband Access

20% Gov/Mil 17%

DTH 14%

Revenue Growth by Application to 2024, All Traditional FSS and HTS Capacity

Source:NSR

Commercial Mobility

29%

Broadband Access

20% Gov/Mil 17%

DTH 14%

Enterprise Data 12%

Revenue Growth by Application to 2024, All Traditional FSS and HTS Capacity

Source:NSR

Commercial Mobility

29%

Broadband Access

20% Gov/Mil 17%

DTH 14%

Enterprise Data 12%

Distribution 7%

Revenue Growth by Application to 2024, All Traditional FSS and HTS Capacity

Source:NSR

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

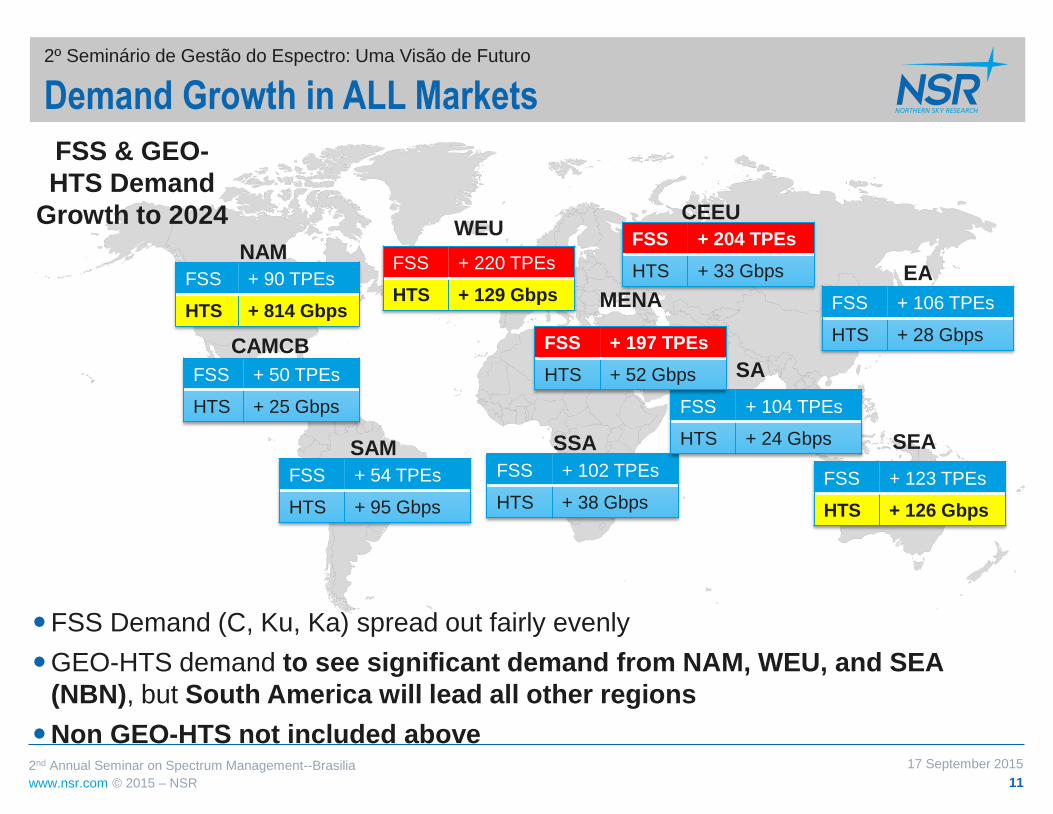

Demand Growth in ALL Markets

11

FSS Demand (C, Ku, Ka) spread out fairly evenly

GEO-HTS demand to see significant demand from NAM, WEU, and SEA

(NBN), but South America will lead all other regions

Non GEO-HTS not included above

FSS + 90 TPEs

HTS + 814 Gbps

FSS + 50 TPEs

HTS + 25 Gbps

FSS + 54 TPEs

HTS + 95 Gbps

FSS + 123 TPEs

HTS + 126 Gbps

FSS + 102 TPEs

HTS + 38 Gbps

FSS + 204 TPEs

HTS + 33 Gbps

FSS + 106 TPEs

HTS + 28 Gbps

FSS & GEO-

HTS Demand

Growth to 2024

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

NAM

CAMCB

SAM

WEU

MENA

CEEU

SSA

SA

EA

SEA

FSS + 220 TPEs

HTS + 129 Gbps

FSS + 104 TPEs

HTS + 24 Gbps

FSS + 197 TPEs

HTS + 52 Gbps

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

Commercial Mobility—Aero & Maritime Leading the Way

12

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

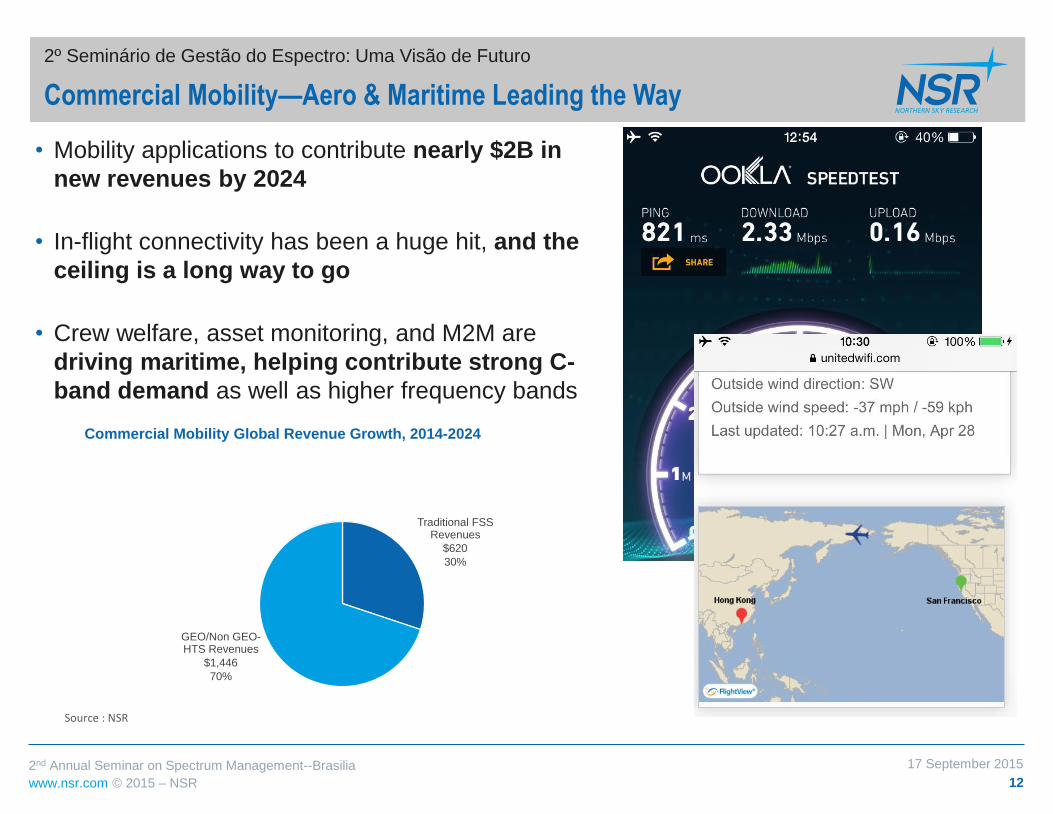

• Mobility applications to contribute nearly $2B in

new revenues by 2024

• In-flight connectivity has been a huge hit, and the

ceiling is a long way to go

• Crew welfare, asset monitoring, and M2M are

driving maritime, helping contribute strong C-

band demand as well as higher frequency bands

Traditional FSS Revenues

$620

30%

GEO/Non GEO-HTS Revenues

$1,446

70%

Commercial Mobility Global Revenue Growth, 2014-2024

Source:NSR

www.nsr.com © 2015 – NSR 13

BYOD: Fueling Mobility SATCOM Revenues

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

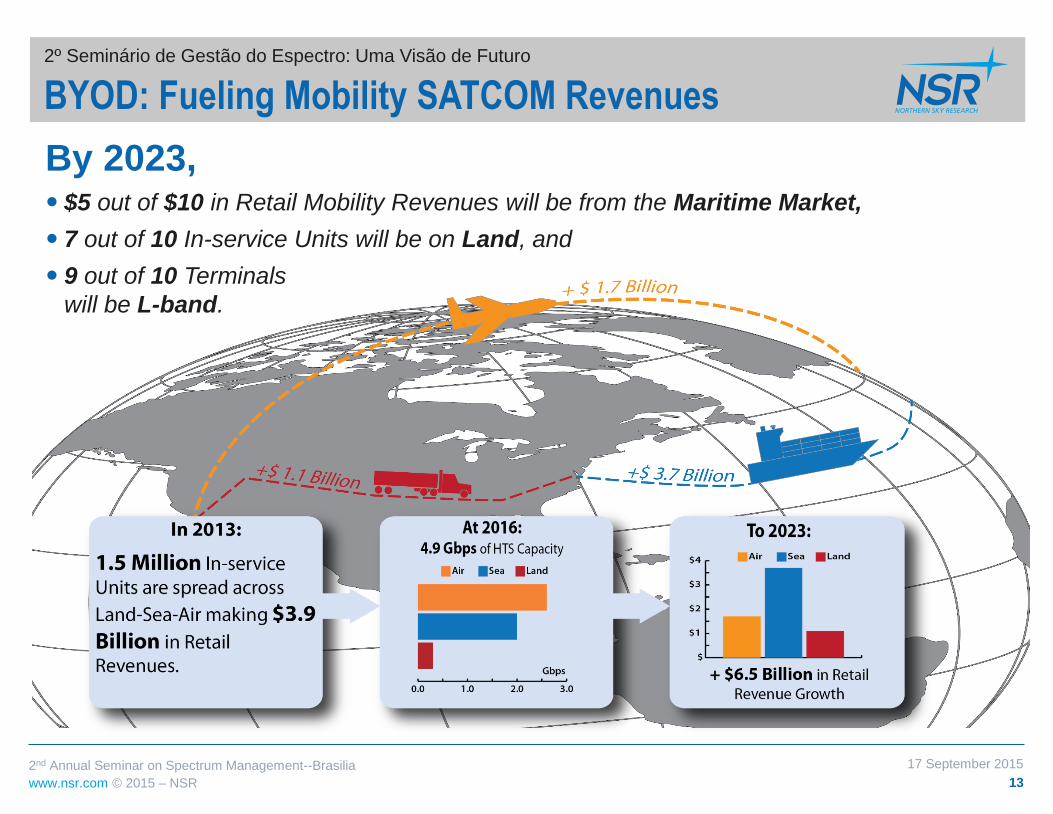

By 2023, $5 out of $10 in Retail Mobility Revenues will be from the Maritime Market,

7 out of 10 In-service Units will be on Land, and

9 out of 10 Terminals

will be L-band.

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

Enterprise Data—VSATs, Backhaul, & Trunking

14

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

• Biggest revenue increases to come from

GEO-HTS

• Part EpicNG migration, but largely

new demand

• Big opportunities in emerging markets

for VSAT and Backhaul and Trunking,

with Video Offload remaining a

wildcard

C-band -$318.1M

Ka-band $89.8

Ku-band $247.9

Non-GEO $349.2

GEO-HTS $493.9

-$400

-$200

$0

$200

$400

$600

US

$ M

illio

ns

Enterprise Data Revenue Change by Capacity Type, 2014-2024

• Total HTS Revenue increase:

$843M

• Total Traditional FSS Revenue

increase: $18M

-

40.0

80.0

120.0

160.0

0

300

600

900

1,200

1,500

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Re

ve

nue

s ($

millio

ns)

In-s

erv

ice

Units

Global Video Offload via Satellite Market

In-service Units Revenues Source : NSR Source : NSR Source:NSR

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

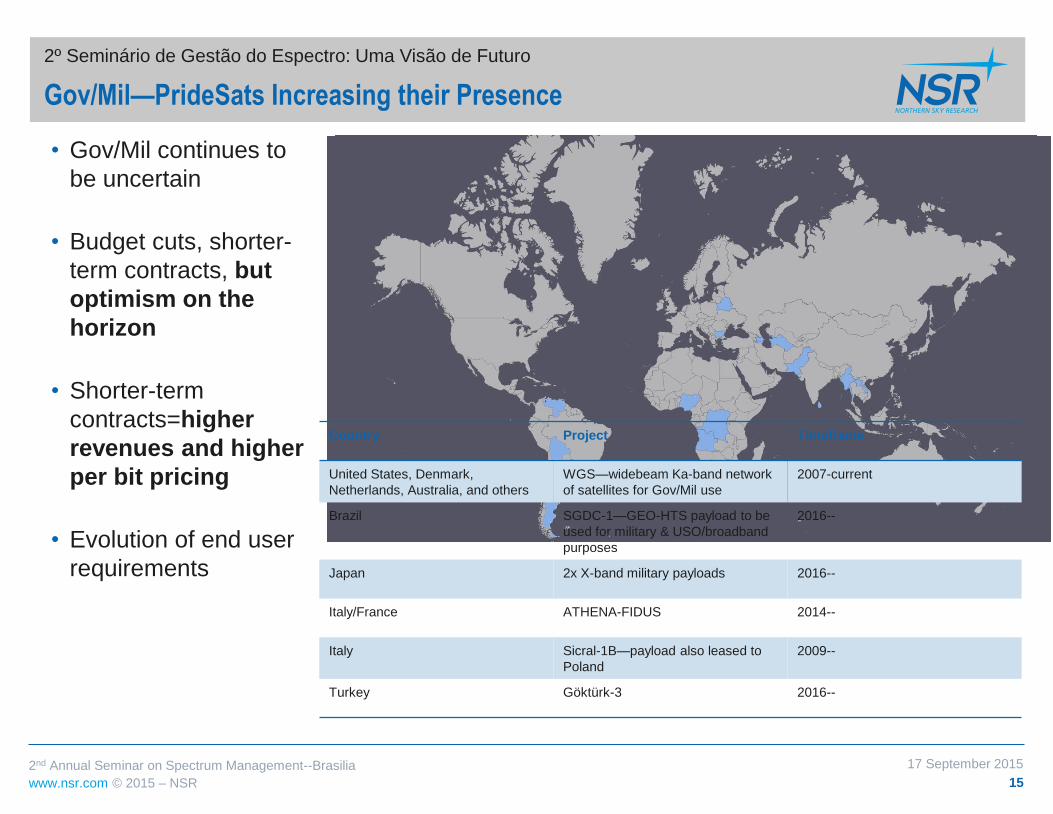

Gov/Mil—PrideSats Increasing their Presence

15

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

• Gov/Mil continues to

be uncertain

• Budget cuts, shorter-

term contracts, but

optimism on the

horizon

• Shorter-term

contracts=higher

revenues and higher

per bit pricing

• Evolution of end user

requirements

Country Project Timeframe

United States, Denmark,

Netherlands, Australia, and others

WGS—widebeam Ka-band network

of satellites for Gov/Mil use

2007-current

Brazil SGDC-1—GEO-HTS payload to be

used for military & USO/broadband

purposes

2016--

Japan 2x X-band military payloads 2016--

Italy/France ATHENA-FIDUS 2014--

Italy Sicral-1B—payload also leased to

Poland

2009--

Turkey Göktürk-3 2016--

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

DTH Markets—Growth from Multiple Fronts

16

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

• Content is king

• UHD to push up revenues in developed regions, and

potentially serve as a differentiator for developing

markets

• Indian growth story is slowing markedly, lots of

inactives and low ARPUs. Does this bode poorly for

other markets?

Source: The Guardian

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

Broadband Markets—More than Just North America

17

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

• Broadband via Satellite becoming viable in more

regions

• Price remains the biggest stumbling block—not many

developing countries offer sufficient ARPUs for

business cases—this could potentially be removed

with a LEO-HTS constellation targeting broadband,

such as OneWeb, SpaceX Constellation, LeoSat,

etc.

www.nsr.com © 2015 – NSR

HTS Business Model Discussion

www.nsr.com © 2015 – NSR 19

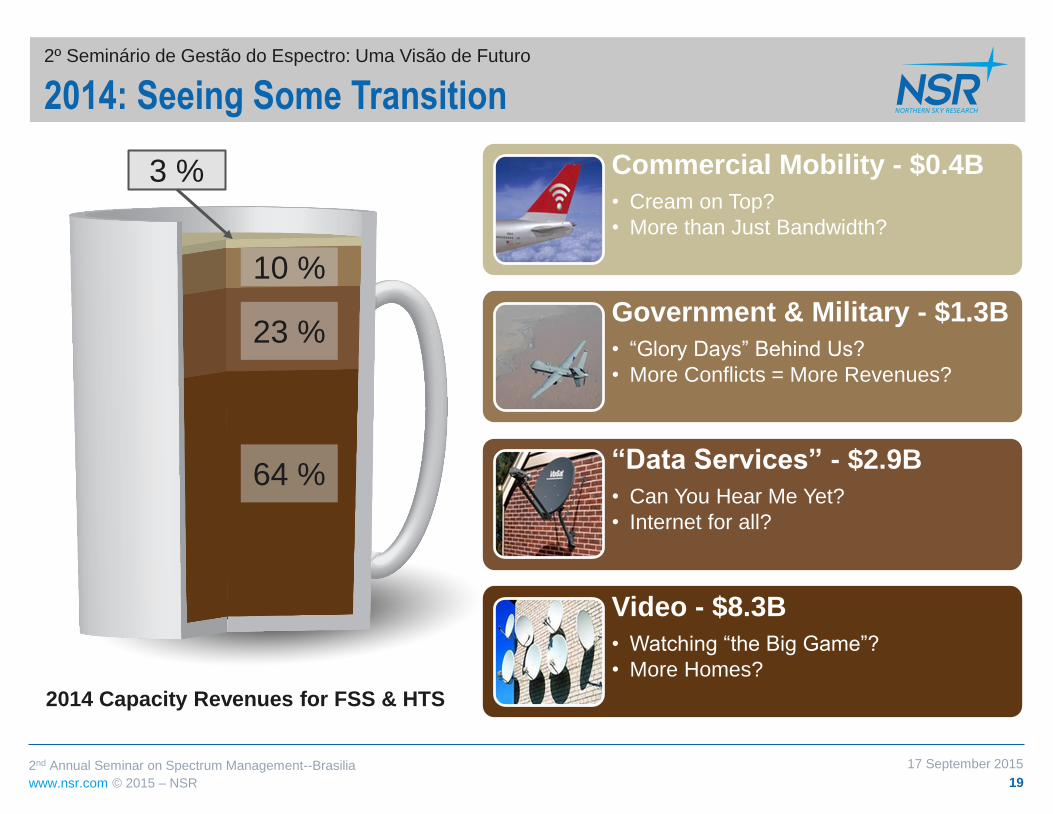

2014: Seeing Some Transition

Commercial Mobility - $0.4B

• Cream on Top?

• More than Just Bandwidth?

Government & Military - $1.3B

• “Glory Days” Behind Us?

• More Conflicts = More Revenues?

“Data Services” - $2.9B

• Can You Hear Me Yet?

• Internet for all?

Video - $8.3B

• Watching “the Big Game”?

• More Homes?

2014 Capacity Revenues for FSS & HTS

64 %

23 %

10 %

3 %

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

www.nsr.com © 2015 – NSR 20

From Cream & Sugar – to Bigger Cups & Lattes

2014

64%

23%

10 %

3 %

2019

59 %

24 %

10 %

7%

2024

50 %

25 %

13 %

12 %

Capacity R

evenues

$13B

$16B

$20B

“Traditional Markets” to Data-Centric Plays The crème on top is where the new opportunities come from

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

GEO & Non GEO-HTS: Establishing New Markets and New Opportunities

21

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

“ViaSat and Eutelsat enter first-of-a-kind agreement to

link High Capacity Ka-band Satellite Networks

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

Where Will GEO-HTS Revenues be Generated?

22

Aero Enterprise VSAT

Backhaul Consumer Broadband

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

Maritime Military Energy Video?

www.nsr.com © 2015 – NSR

System Orbit Launch Date Years to Launch Satellites Bit Rate Throughput (Gbps) Services

Iridium LEO 1991 2.5-3** 72+ Low N/A Telephony, Data

Globalstar LEO 1991 2.5-3** 52+ Low N/A Telephony, Data

Orbcomm LEO 1993 3*** 30+ Low N/A Data

ICO MEO 1995 2 10+ Low N/A Telephony, Data

Skybridge LEO 1998 N/A 80+ High N/A Data

Teledesic LEO 1990s N/A 280+ High N/A Data

O3b MEO 2007 2 12-20 High 80-360 Data, Backhaul

OneWeb LEO 2018-19 3** 640-2,400 High 6,000 Data, Backhaul

SpaceX LEO 2019-20 3** 4,000+ High 8,000+? Data, Backhaul

COMMStellation LEO 2015? 2-3** 75+ High? N/A Data

Ximwei LEO 2019? N/A 30+ High? N/A Data, Voice?

LeoSat LEO 2018-2019 2-3** 80-120 High? 1,000-2,000

Laser Light MEO 2018 N/A 8 High? N/A Data

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

HTS and Constellations – Past, Present & Future

23

• Even one constellation needs more launcher capability than is available right now

• Any constellations will result in “Bubble for Backhaul" more than other user segments

• Will the “Iridium of Broadband” follow its predecessor

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

www.nsr.com © 2015 – NSR

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

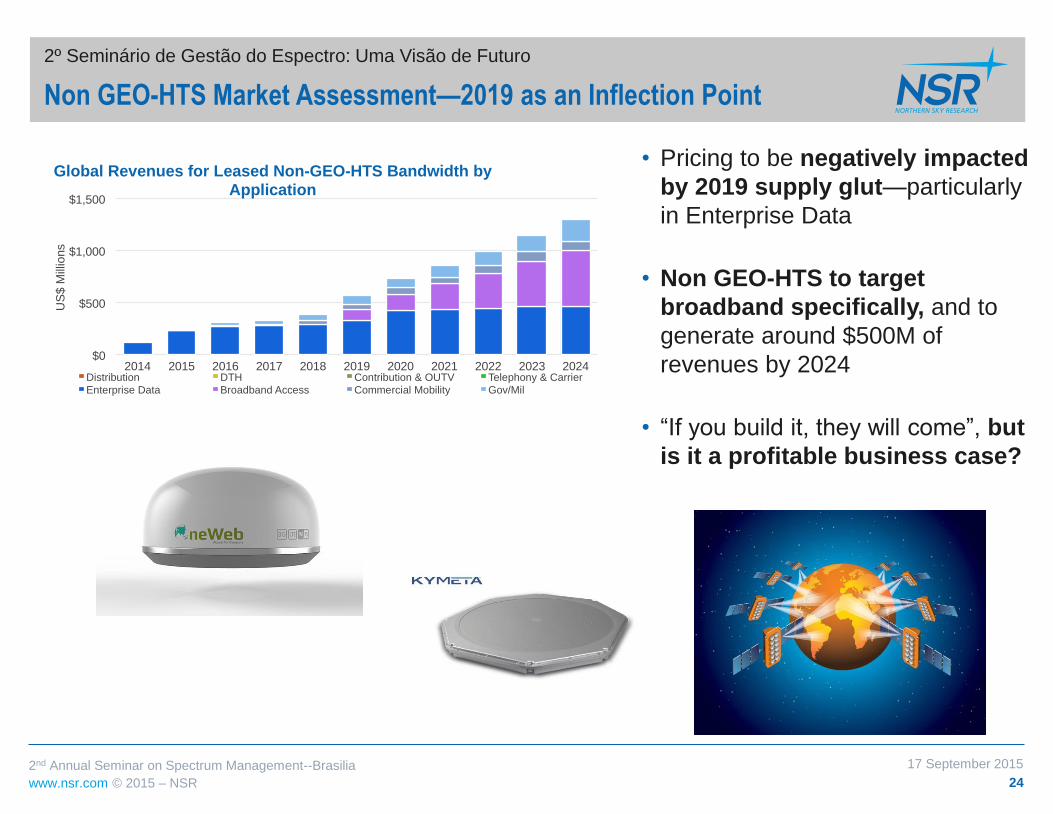

Non GEO-HTS Market Assessment—2019 as an Inflection Point

24

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

• Pricing to be negatively impacted

by 2019 supply glut—particularly

in Enterprise Data

• Non GEO-HTS to target

broadband specifically, and to

generate around $500M of

revenues by 2024

• “If you build it, they will come”, but

is it a profitable business case?

$0

$500

$1,000

$1,500

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

US

$ M

illio

ns

Global Revenues for Leased Non-GEO-HTS Bandwidth by Application

Distribution DTH Contribution & OUTV Telephony & Carrier

Enterprise Data Broadband Access Commercial Mobility Gov/Mil

www.nsr.com © 2015 – NSR 25

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

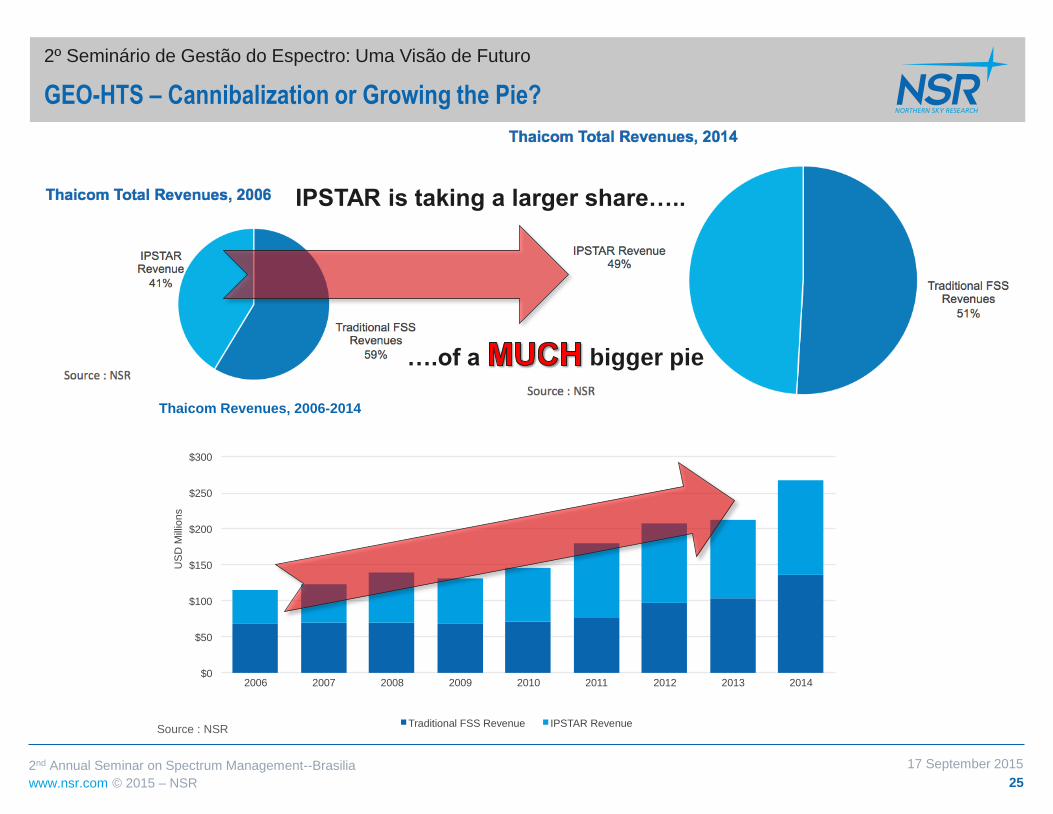

GEO-HTS – Cannibalization or Growing the Pie?

$0

$50

$100

$150

$200

$250

$300

2006 2007 2008 2009 2010 2011 2012 2013 2014

US

D M

illio

ns

Thaicom Revenues, 2006-2014

Traditional FSS Revenue IPSTAR Revenue Source : NSR

IPSTAR is taking a larger share…..

….of a bigger pie

2nd Annual Seminar on Spectrum Management--Brasilia 17 September 2015

www.nsr.com © 2015 – NSR

Bottom Line

www.nsr.com © 2015 – NSR 27

2º Seminário de Gestão do Espectro: Uma Visão de Futuro

Bottom Line

17 September 2015 2nd Annual Seminar on Spectrum Management--Brasilia

• GEO-HTS will provide the best opportunities to create new markets moving

forward, frequency reuse unlocks new markets through increased bandwidth

efficiency.

• Traditional FSS to see demand increase incrementally in some areas, though

overall much more limited opportunities

• O3b business case continues to pick up steam, with entry of a potential LEO-HTS

constellation looming in the medium-term

• Overall, around $6.5 billion in new revenue by 2024, for a CAGR of around 3.5%.

www.nsr.com © 2015 – NSR

Questions?

Blaine Curcio, Senior Analyst

September 17, 2015

Northern Sky Research, LLC, 1000 N. West St. Suite 1200 Wilmington, DE 19801 Phone: 302-295-4981 | Fax: 302-295-4801

Online E-mail: [email protected] | Web: www.nsr.com

U.S. Office

Contact NSR