46

1 FY 2007 results and comments INVESTOR & ANALYST UPDATE 29 February 2008

1

FY 2007 results and commentsINVESTOR & ANALYST UPDATE

29 February 2008

2

DISCLAIMER

The views expressed here contain information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking information in this presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendation or forecast by Banpu plc. Nothing in this release should be construed as either an offer to sell or a solicitation of an offer to buy or sell shares in any jurisdiction.

3

1. Introduction

2. Focus: mine planning process

3. Operational review

4. Commercial review

5. Financial review

4

1. Introduction

Chanin VongkusolkitChief Executive Officer

5

Banpu in 2007: big picture

1

Indonesia• 18mt coal sale

• Bontang port expansion

• Impact of force majeureand rains on output

China• Daning (3mt) and Hebi (1.4mt)

expansions in line expectation

• BPIC expansion under way

2

Thailand• LP2/CMMC: winding down

• BLCP: achieved targets

• HongSa: • EPC signed (CMEC/Harbin)

• Tariff MOU (Bt2.05/kWh 25yrs)

• Shareholder structure agreed (Ratch 40%, Lao 20%)

3

Luannan

Zhengding

Zouping

Hebi

Daning

Gaohe

HongSaLP2/ CMMC

Ratch

BLCP

Bharinto

Trubaindo

Jorong

Indominco

Kitadin

1

2

3

Stock exchange:

Ticker:

Date:

Shares offered:

Type:

Offering % (post):

Offer price:

Banpu % (post):

Lead underwriter:

Indo. Stock Exch.

ITMG

18th Dec 2007

225,985,000

Primary 100%

20%

Rp 14,000 /sh.

73.72%

UBS

*Indo Tambangraya Megah Tbk.

ITM listing*

OperationProject

OperationProject

POWER

COAL

6

Banpu in 2007: the figures

Coal sales

19.3 MT

Down 2.4 MT 11% Y-Y

Coal

28,577

427

3,903

2,405

Power

3,865

4,077

5,073

4,248

Revenue

Equity income

EBIT

Net income

Total

32,442

4,504

8,976

6,654

Y-Y

-3%

462%

49%

84%

Unit: Bt. million

7

Global economic and coal market context: year ahead

5.5 5.64.7

S. America

3.02.0 2.0

N. America

5.3 5.3 5.3Middle East

7.9 7.97.2

Asia Pacific (including Japan)

‘06 ‘07 ’08E

‘06 ‘07 ’08E

‘06 ‘07 ‘08E

‘06 ‘07 ‘08E

Source: IMF Data Mapper, McCloskey 2007 estimate

Key: GDP % growth

Thermal coal exports (Mt)

5223

Thermal coal imports (Mt)

65 Mt

COLUMBIA

USA & AMERICAS

67 Mt

187 Mt

79 Mt

RUSSIA & E. EUROPE

35

INDIA

203 Mt

INDONESIA

111 Mt

AUSTRALIA

3045

CHINA

S.AFRICA

EUROPE & MEDITERANEAN

2.2 2.0 1.7

Japan

‘06 ‘07 ‘08E64

S.KOREA

JAPAN

116 Mt

58

TAIWAN

3.7 3.63.0

Europe

‘06 ‘07 ’08E

37SE ASIA

8

Indonesia: year ahead

East Kalimantan

Bunyut PortSamarinda

Balikpapan

Palangkaraya

Banjarmasin

Jorong Port

Central Kalimantan

South Kalimantan

Bontang port

Kitadin

Indominco

Trubaindo

Bharinto

Jorong

ITM OPERATIONS & PROJECTS

OperationProject

OperationProject

POWER

COAL

CFP project

Production: target 19.5mt coal

Debottleneck: address contractor and equipment capacity constraints

Reserves: expansion: feasibility studies, adjustment of SRs, exploration

Costs: continue rationalisation schemes: Bontang CFP, washing plants, barge fleet management, flexible loading schedule to reduce demurrage charges

Acquisitions: Continue to evaluate new investment and acquisition opportunities

9

China: year ahead

LUANNAN100MWHebei

ZHENGDING48MWShandong

DANING (12%)4mtpaShanxi

GAOHE (10%)6mtpa (COD 2011)Shanxi

BANPU CHINA OPERATIONS & PROJECTS

OperationProject

OperationProject

POWER

COAL

*Production potential will be determined by de-gas tests mid-year; coal is semi-anthracite; 157mt reserves

Ownership 100% unless indicated otherwise

HEBI (40%)1.5mtpaHenan

ZOUPING (70%)100MWShandong

Daning: (56% AACI) completion of 15km rail spur to connect to provincial railway; 4mt target for 2008

Gaohe: (45% AACI) new 5-6mtpa* mine project selling to Chinese utilities and steel mills; first output 2010 – full output by 2013; ordering equipment; degas tests mid-year; licensing

AACI: Banpu position under review

Hebi: 1.5mt target 2008; further output expansion potential under study

Power: tariff adjustment vs coal cost increases likely to impact performance

10

Thailand: year ahead

Hong Sa (40%) Laos 1,800MW lignite-fired

CMMC Payao

open-pit LP-2 Lampangopen-pit

Ratch (15%) 3,995MW gas-fired

BLCP (50%) 1,434MW coal-fired

BANPU THAILAND OPERATIONS & PROJECTS

Ownership 100% unless indicated otherwise

OperationProject

OperationProject

POWER

COAL

Banpu Power: develop and strengthen O&M expertise

BLCP: 1.4GW operation (on-stream 2006/7); aim for smooth second year of operation

Hong Sa: 1.8GW project ($2.8bn) COD by 2013; target PPA by mid-08; financial closure by end-08

LP-2, CMMC: last output in 2008 (0.5mt); closure cost planning

11

Banpu corporate and financial: year ahead

ITM management: emphasis on developing best practice corporate governance, management systems and IR following listing.

HR: continued emphasis on integration, training (leadership, Technical Knowledge Portal and Innovation Promotion) and instilling Banpu Spiritfor growing multinational workforce

Renewable energy: make first investments (in line 2% asset policy)

Dividend policy: change to 50% payout of consolidated profit (subject to cash flows)

Thailand

Indonesia

China

24%14%

62%

Total staff: 3,266

BANPU GROUP EMPLOYEES BY GEOGRAPHIC LOCATION

Main staff nationalities: Indonesian, Chinese, Thai, Australian, British, Indian, Philippines

1212

2. Focus: mine planning process

Neil TurveyHead of Technical Development & Services

13

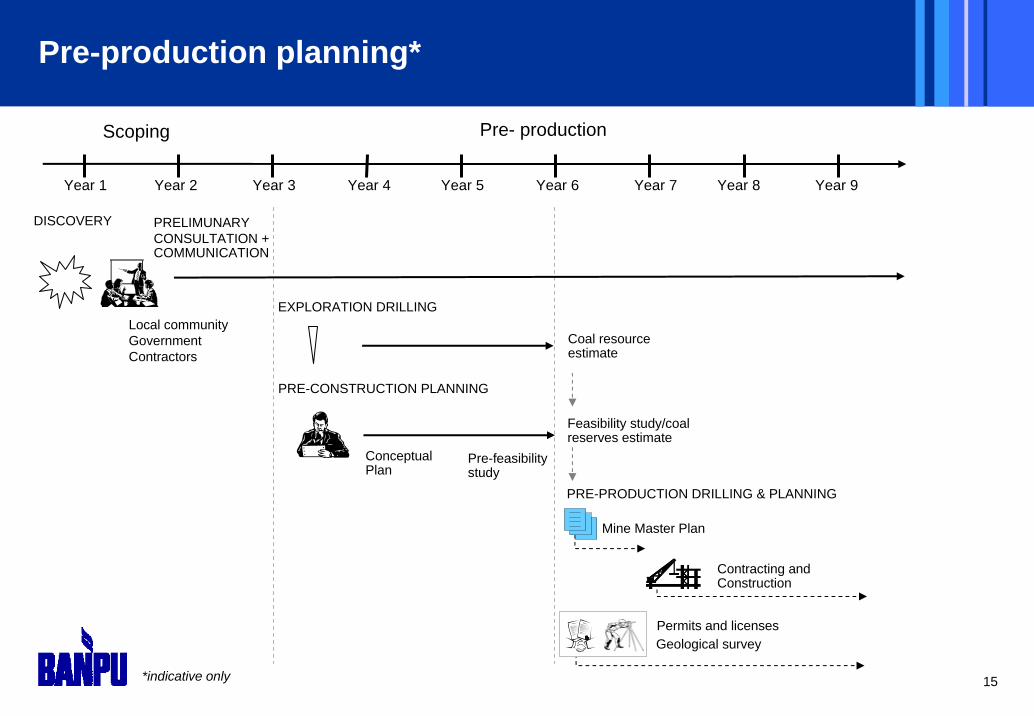

Mine planning process overview

Coal mines are complex operations and require detailed planning.Establishing a mine - and an ultimate production profile - is subject to a number of constraints including technical, financial, logistical, regulatory as well as commercial - and can take many years

Overall mine operations are guided by ‘Mine Master Plans’, which aim to maximize long term value from a coal deposit and are subject to key assumptions and constraints

Mine Master Plans need to be updated when key assumptions and constraints change. Any changes to mine planning are given careful consideration

Annual, quarterly, monthly and weekly mine operation planning islinked to the Mine Master Plan - and deliver the short term production and cost performance

14

Mine-to-port illustrations: Indominco and Trubaindo

Source: Company information

0 10 2515 205 km

PT. BHARINTO

40Km

SOUTH BLOCK

NORTH BLOCK

HAUL ROAD

Mahakam River

KedangpahuRiver

Raw coal stockpile

HAUL ROAD

Product coal conveyor/stacking/stockpile

BUNYUT PORT

BARGE 300KM TO TRANSHIPMENT

WEST BLOCKEAST BLOCK

Santan river

Port stock yard

Bontang City

ASHPHALT HAUL ROAD

4Km 2.5Km

35Km

ROM stockpile

SEA CONVEYOR

Mine stockyard

CONVEYOR

Panamax90,000DWT

0 106 82 km4

Indominco

0 10 2515 205 km

Operation

Stockpile

Ship Port

Hauling

Barge Port

Crusher

40Km

Product coal conveyor/stacking/

stockpile

Trubaindo

15

Pre-production planning*

*indicative only

DISCOVERY

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9

Pre- production

PRELIMUNARY CONSULTATION + COMMUNICATION

Local communityGovernmentContractors

Scoping

EXPLORATION DRILLING

PRE-CONSTRUCTION PLANNING

Feasibility study/coal reserves estimate

Conceptual Plan

Pre-feasibility study

PRE-PRODUCTION DRILLING & PLANNING

Coal resource estimate

Mine Master Plan

Contracting and Construction

Permits and licensesGeological survey

16

Production planning

Year 1 Year 2

MINE MASTER PLAN

PREPARE YEAR 1 ANNUAL MINE PLAN

Production

PREPARE YEAR 2 ANNUAL MINE PLAN

Quarterly Plan

Monthly & weekly plans

Year 1 annual budget

Year 2 annual budget

MINE MASTER PLAN UPDATE*

PREPARE YEAR 3 ANNUAL MINE PLAN

Year 3 annual budget

Quarterly Plan

Monthly & weekly plans

Pre- production

* if necessary

YEAR 2 PRODUCTION DRILLING

YEAR 3 PRODUCTION DRILLING

YEAR 1 PRODUCTION DRILLING

17

Production planning: Mine Master Plan update

Mine Master Plans provide a long term schedule of planned mine activities, with estimates of likely production, costs and revenues. They are updated only when key assumptions and constraints change significantly.

•Tax rates•WACC•Mine equity•Coal price forecasts

• What is the maximized NPV vs. strip ratio?

•Cash cost estimates•CAPEX estimates•Key infrastructure•Production vsReserves•Balance between contractor capacity and mine capacity

UPDATE COAL MODEL

•Coal reserves at different strip ratios

• Permits •Engineering •Geology•Infrastructure (roads, power?)•Asset synergies (coal blending, BoCT)•Integration of development projects

•Coal prices •Fuel prices•FOREX•Risk scenarios

PIT OPTIMISATION

‘BASE CASE’ MINE DESIGN

LONG TERM PRODUCTION SCHEDULE

SENSITIVITY ANALYSIS

•Development strategy•Mining sequence•Annual mining targets

Late January April/May

Master Plan production schedule

* Each step assumes that approvals are signed off. Each step may be subject to a number of revisions

18

Production planning: Annual Mine Plan preparation

FINANCIAL MINING STRATEGY

UPDATED RESERVE ESTIMATES

ANNUAL PRODUCTION SCHEDULE

DETAILED PRODUCTION SCHEDULE

PERMITTING & MINE DESIGN

July

The Annual Mine Plan forms the basis of annual operations. Using updated information, it marks the transition between the Mine Master Plan and its implementation. It is the basis of the annual mine budget for the following year.

•Infrastructure capacity•Detailed pit & dump designs•Geological limits on annual production rate (e.g. seam length, width and depth determine constraints on mining) •Environmental and legal

•Consistency with Mine Master Plan•Preliminary pit & dump layouts developed

• Impact of detailed pit designs on reserve estimates

• Consistency with the Mine Master Plan mining targets•Commercial and sales commitments

•Mining equipment availability (especially at short notice)•Rapidly expanding contractor industry in Indonesia –size and reliability issues

•Fuel price•‘Base case’ S/R •Coal price forecast•Cash costs•FOREX •Contractor prices

October

Annual Plan and budget (Year +1)

* Each step assumes that approvals are signed off. Each step may be subject to a number of revisions

•Quarterly plans•Monthly plans•Weekly plans

19

3. Operational review

Rawi CorsiriChief Operating Officer

20

Estimated 2008 production c.20m tonnes (excld. China)

Indominco-Bontang11.5 mt

Jorong3 mt

Thailand0.5 mt

Daning4.0 mt

(Banpu 12.5%)

Trubaindo5.0 mt

100% basis

Hebi1.5 mt(Banpu 40%)

Kitadin

21

Indonesian and Thai coal production review and outlook

Indominco-BontangCV 6250 - 6500 kcal/kg

2.6

SR 10.5:1

1Q07

12.4:1

0.2

2Q07

0.6

1Q07

SR 4.7

Kitadin-EmbalutCV 5800 kcal/kg

JorongCV 5300 kcal/kg

LP-2 / CMMCCV 4000 - 5000 kcal/kg

4.4

2Q07

TrubaindoCV 6550 – 7200 kcal/kg

10.5:1

0.5

3Q07

0.8

1Q07 2Q07

SR 5.4

1Q07 2Q07

SR 4.2 4.3

2.7

3Q07

0.7

1Q08F

0.1

4Q07

0.9

1Q08F

11.3:1

4.3

4.4

3.2

0.8

0.7Stable output; Stripping

ratio unchanged

Thai mines are in closure stage due to reserves

depletion

5.4

Increased stripping ratio to capture favorable

market price

Replaced mining contractor in October 2007; Increased

stripping ratio

3Q07

4.3

0.7

3Q07

0.2

4.4

8.0

Evaluating alternatives to utilize

existing assets

1Q08F

2.6

1.0

0.6

4Q07

3.1

4Q07

8.5

1.0

4Q07

0.7

1Q08F

22

DaningShanxi Province, PRC

CV 6800 – 7300 kcal/kg(Banpu 12.5%)

HZTM(Hebi Zhong Tai Mining)

Henan Province, PRCCV 5300 – 6800 kcal/kg

(Banpu 40%)

China coal operations

Coal price(RMB/t)

Production(Mt)

2006

372

1.28

4Q07

Coal price(RMB/t)

Production(Mt)

281

2.03

446

0.38

426

1.26

2007

423

1.44

381

3.09

1Q08F

458

0.36

432

0.51

Completed minor capacity increased to 1.5Mtpa;

Further expansion to 2Mtpa is under consideration

Production in 1Q08 will be briefly interrupted by

relocation of longwall

23

Total revenue

Availability Payment (AP)

Energy Payment (EP)

Dispatch (%)

Operating cost

EBIT

EBITDA

Power Thailand : BLCP

4Q/2007

3,853

1,856

1,789

70%

2,267

979

1,513

Q-Q

-29%

-43%

-13%

1%

-65%

-53%

Units: Bt. million

Equity income 2007

Bt 4,076 m*

* Based on Banpu’s 50% interest; including FX gain Bt591million

3Q/2007

5,517

3,284

2,056

87%

2,240

2,760

3,238

2007

20,307

11,716

7,906

87%

8,938

9,340

11,243

24

Power China : BPIC

* Unaudited figures

** Including transportation

*** Including Expansion

Sales* (USD m)

EBITDA (USD m)

Utilization (Hours)

Power tariff (RMB/kwh)

Coal price**(RMB/t)

100% basis

LuannanHebei Province, PRCPower 100MW; Steam 128tph(Banpu 100% )

ZhengdingHebei Province, PRCPower 48MW;Steam 180tph(100%)

Second phase (hot water) completed; expansion for

other lines have commenced

2007

#1 Major overhaul completed; #1 unit DCS

retrofit completed

3Q07

4Q07

ZoupingShandong Province, PRCPower 100MW***;Steam 490tph(70%)

Third phase (25MW) : turbine # 4 was in

commercial operation

2007

2007

38.1 14.0 6,961 0.42 437

25.8 8.2 9,227 0.34 383

46.3 10.4 8,953 0.32 484

9.8 4.2 1,813 0.42 421

10.0 1.7 1,712 0.42 489

3Q07 5.9 2.0 2,286 0.34 373

4Q07 7.6 2.2 2,343 0.34 414

3Q07 12.2 3.3 2,442 0.32 4694Q07 14.9 2.7 2,551 0.32 522

25

4. Commercial review

Philip GasteenHead of Marketing and Logistics

26

102030405060708090

100110120130

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

e

BJI

Weighted avg

Indominco

ASP 4q07 : $44.18 / tonne

ASP 2007 :$41.06 / tonne

US$/Tonne BJI* February 28, 2008

$127.90

Chinese winter cuts exportS. Africa electricity cutdisrupts mining operation

Australia flooding cuts export

Average Selling Prices (ASP)

Note: *Barlow Jonker Index (BJI) based on CV 6,700 kcal/kg GAD from Australia to JapanSource: Barlow Jonker

27

Strong market likely to stay strong

China

S.Africa

Australia

Demand easing in March from winter peaksStockpiling vs. small mine safetyTighter 2008 demand than forecast at end 2007. Exports drop while imports maintain

Coking coal supply constraints due to floods (forecast $300+/t)Diversion of thermal coal to metallurgical markets

Growing domestic power demandNew (expensive) production may not be sufficient to meet export orders, due investment risk

Pressure on thermal prices other things being equal

Overall impact?

1Q0810 Mt thermal coal ‘lost’from export markets

FY200825 - 30 Mt thermal coal ‘lost’ from export markets –could be 20 Mt from China / Vietnam

Approx 5 Mt in diversions annually from thermal to metallurgical markets in 2008 / 2009

28

70%

11%

19%

Contracted & Priced

Contracted & Unpriced

Uncontracted

• Very strong global import demand through 2008

• Thai coal fully sold

• Indonesian low CV grades largely placed

• Gradually committing remaining high CV grades

• EU contracts linked to API # 4

Indicative 2008 coal sales

Approx. 20 MT

29

Coal sales by geographic destination

INDIA

0.5 Mt

ITALY

OTHERS*

1.2Mt

1.0 Mt

1.2 Mt

THAILAND

CHINA

2.5 Mt

3.3 MtPHILIPPINES

1.4 Mt

1.1 MtINDONESIA

JAPAN

4.6 Mt

TAIWAN

2.9 Mt

0.8 MtS.KOREA

*Includes Vietnam, Pakistan and other small, non-regular purchasers

Mid-to-High CVLow-to-Mid CV

Total coal sales volume: 19.3Mt in 2007 (5.02Mt in 4Q07)

30

5. Financial review

Somruedee SomphongChief Financial Officer

3131

32,29433,242

25,046

2005 2006 2007

Sales revenues: coal and power

Note : Revenues from other businesses (e.g. industrial minerals) are not included

Consolidation of BPIC started in March 2006 (Bt2,808m revenue for the year)

Units: Bt. million

• 11% decrease in sale volume

• 17% increase in selling price

• 9% appreciation of Thai Baht

-3% Y on Y

Coal Bt28,429m

Power Bt3,865m+38% Y on Y

-7% Y on Y

0100200300400500600700800900

1000

2006 2007

Revenues in USD +6.59% Y on Y

32

14,013

2,426

2,429

3,016

3,162

16,638

1,667

2,123

3,035

6,971

18,758

6,126

2,616

175

717

38Trade

Thai mines

Kitadin-Embalut

Jorong

Trubaindo

Indominco

Bt. million GPM Sales revenue

Thai mines

Jorong

Trubaindo

Kitadin-Embalut

Indominco

39%39%

46%

36%

33%40%

10%37%48%

38%

43%

31%

2007

20062005

Avg. gross margin for coal in 2007 at 37%

41%42%

32%

Trade

3333

12,916

9,5288,874

2005 2006 2007

EBITDA

Units: Bt. million

Coal Bt7,398m

Power Bt5,518m+211% Y on Y

-5% Y on Y

+36%

Y on Y

3434

6,654

3,610

2,851

2,708

2005 2006 2007

Net Profit

Units: Bt. million

Coal Bt2,243m

Non-Recurring

+238% Y on Y

-3% Y on Y

+84%

Y on Y

5,559

Power Bt4,411m

35

2007-08 CAPEX plans: $363million

Units: USD million

22 45

120 Power Indonesia

Coal ChinaCoal Indonesia

45

230

Committed Feasibility ConceptualStatusCoal projects

Power projects

Bontang Port 66

BontangPower Plant 22

Bharinto 45 Indonesia 50China 120

China 60

The capital expenditure figures shown above are indicative only and do not include estimates for maintenance or sustaining capital expenditure. The figures shown in the ‘Conceptual’ column should be treated with extra caution and are likely to change as new projects are conceived, some are cancelled and as pre-feasibility analyses generate modified estimates of capital expenditure requirements.

Power China88

50

60

66

36

0.14

0.66

0.34

0.22

2004 2005 2006 2007

91

Balance sheet

Debt structureNet D/E (Times)

Net gearing (%)

As end of December 2007

18%25%

40%

Floating 49% Fixed 51%

12%

37

Dividend payment

3.753.25

7.55.5

42.6

4.754.25

5

2002 2003 2004 2005 2006 2007

Dividend per share (Bt)

(Special)

(1H07)

(2H07)

(1H06)

38

Question & Answer

39

APPENDICES

40

Operating profit

Units: Bt. million

Sales revenues – Power (BPIC) 3,865Cost of sales (20,964)Gross profit* 11,478 -8%

GPM 35%

2007 YoY %

32,442 -3%Sales revenues – Coal

Total sales revenues*

28,429 -7%

Gross profit - Coal 10,467 -10%Gross profit – Power (BPIC) 956

38%

18%

2006

2,808(20,838)12,541

38%

33,37830,434

11,681812

Note: * Including other business

GPM – Power (BPIC)GPM - Coal

25%37%

29%38%

41

Operating profit

Units: Bt. million

Gross profit 11,478 12,541 -8%GPM 35% 38%SG&A (3,952) (4,607)Royalty (3,247) (3,238)

Dividend income – Coal & Power 457 465 Other income 247 299

EBIT 8,976 6,036 49%

EBITDA 12,916 9,528 36%

2007 2006 YoY %

EBIT - Coal 3,903 4,744 -18%EBIT - Power 5,073 1,291

Income from associates 4,504 801

293%

EBITDA - Coal 7,398 7,979 -7%EBITDA - Power 5,518 1,549 256%

Other expenses - Operations (511) (225)

42

Units: Bt. million

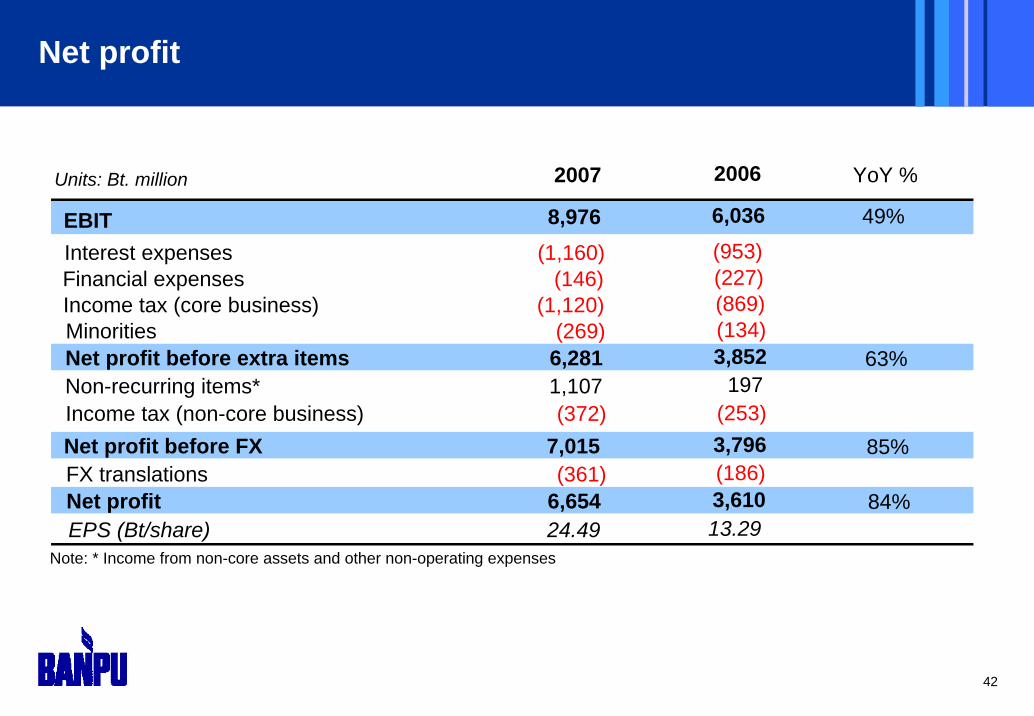

EBITInterest expenses (1,160)Financial expenses (146)Income tax (core business) (1,120)Minorities (269)Net profit before extra items 6,281Non-recurring items* 1,107Income tax (non-core business) (372)Net profit before FX 7,015 85%FX translations (361)Net profit 6,654 84%EPS (Bt/share) 24.49

Note: * Income from non-core assets and other non-operating expenses

YoY %2007

Net profit

63%

(953)(227)(869)(134)3,852

197(253) 3,796(186)3,61013.29

8,976 6,036 49%

2006

43

Operating profit

Units: Bt. million

Sales revenues – Power (BPIC) 1,164Cost of sales (6,198)Gross profit* 2,987 -6% -22%

GPM 33%

4Q07 QoQ % YoY %

9,185 6% -10%Sales revenues – Coal

Total sales revenues*

7,981 4% -13%

Gross profit - Coal 2,783 -4% -22%Gross profit – Power (BPIC) 193

23% 25%

-32% -30%

931(6,324)3,838

38%

4Q06

10,1629,210

3,554275

948(5,462)3,178

37%

3Q07

8,6417,654

2,884284

Note: * Including other business

GPM – Power (BPIC)GPM - Coal

17%35%

29%39%

30%38%

44

Operating profit

Units: Bt. million

Gross profit 2,987 3,838 -6% -22%GPM 33% 38%SG&A (1,029) (1,343)Royalty (884) (1,008)

Dividend income – Coal & Power - -Other income 92 83

EBIT 1,532 2,171 -40% -29%

EBITDA 1,876 3,042 -54% -38%

4Q07 4Q06 QoQ % YoY %

EBIT - Coal 1,133 1,481 13% -24%EBIT - Power 399 690

Income from associates 614 754

-74% -42%

EBITDA - Coal 1,284 2,276 -47% -44%EBITDA - Power 592 767 -64% -23%

3,17837%

(1,116)(882)

21734

2,554

4,060

1,0041,550

1,238

2,4211,639

Other expenses - Operations (251) (414)(120)

3Q07

45

Units: Bt. million

EBITInterest expenses (282)Financial expenses (34)Income tax (core business) (173)Minorities (154)Net profit before extra items 890Non-recurring items* 1,362Income tax (non-core business) (135)Net profit before FX 2,117 85%FX translations (134)Net profit 1,983 69%EPS (Bt/share) 7.30

Note: * Income from non-core assets and other non-operating expenses

YoY %4Q07

Net profit

-39%

(266)(57)

(345)(34)

1,469(325)

-1,144

311,1754.32

19%

15%

-51%

1,532 2,171 -40% -29%

(304)(34)

(51)1,830

(55)-

1,774(55)

1,7196.32

2,554

(335)

4Q06 QoQ %3Q07

46

Banpu’s Resources & Reserves statement (100% basis)

As at 31 December 2007 As at 31 December 2006

Measured Resources

Indicated Resources

Total Resources

Proved Reserves

Probable Reserves

Total Reserves

Total Resources

Total Reserves

Mine operation

Jorong 73.72 105.6 18.8 124.4 12.6 - 12.6 45.1 15.9

Indominco 73.72 526.3 82.7 609.0 21.9 71.9 93.8 289.7 86.0

Kitadin-Embalut 73.71 103.0 51.0 154.0 - 17.1 17.1 150.6 17.3

Kitadin-TandungMaYang

73.71 12.4 0.5 12.9 - 9.7 9.7 - -

Trubaindo 73.72 161.8 134.7 296.5 27.9 30.0 57.9 300.8 61.6

Lampang 100.00 1.6 - 1.6 0.3 - 0.3 2.5 1.1

Payao 100.00 0.8 - 0.8 0.4 - 0.4 1.2 1.1

Daning No. 1 12.49 61.8 35.0 96.8 69.7 - 69.7 102.5 72.0

Hebi Zhongtai 40.00 66.7 - 66.7 31.7 - 31.7 70.3 33.1

Project

Bharinto 72.98 183.5 114.5 298.0 36.5 9.8 46.3 218.4 28.5

Barasentosa* 94.99 - - - - - - 38.8 32.8

Total 1,223.3 437.2 1,660.6 201.0 138.4 339.5 1,220.0 349.4

Mine operation and project

Interest

(%)

Note : * Divest in May 07

Resources and Reserves are classified in accordance with JORC Code