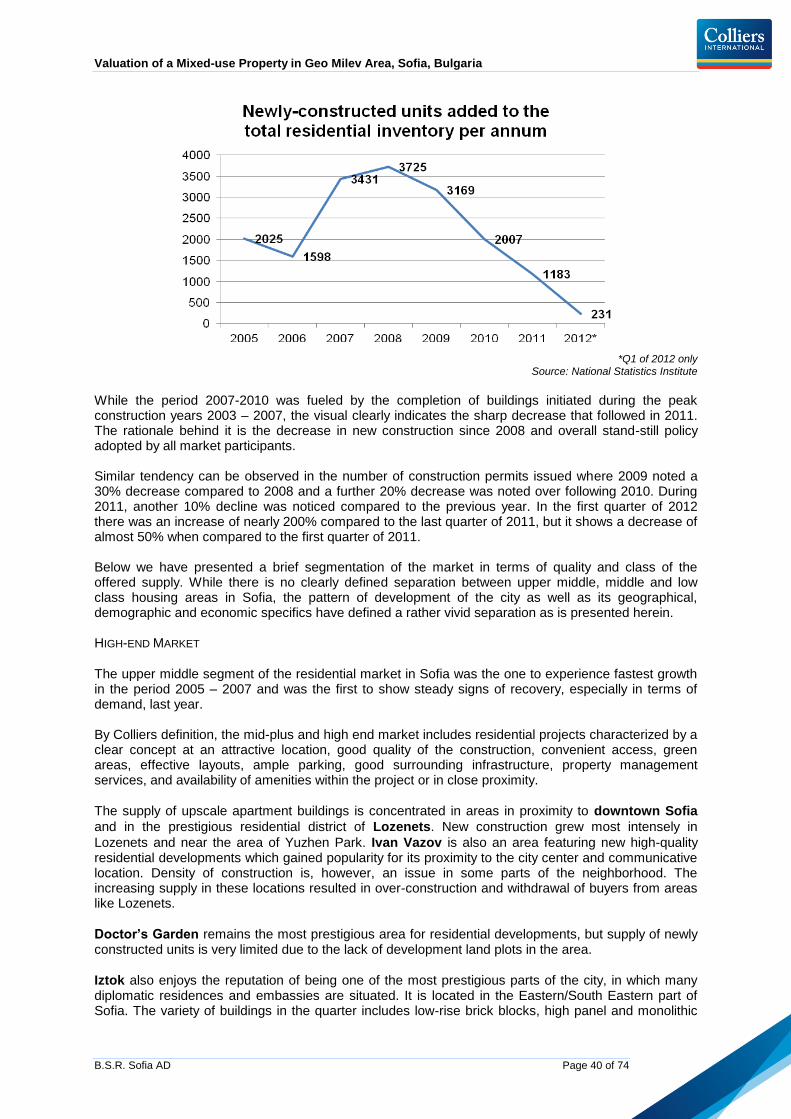

94

VALUATION OF A MIXED-USE PROPERTY Geo Milev Area Sofia Bulgaria PREPARED EXCLUSIVELY FOR B.S.R. SOFIA AD PREPARED BY: JULY 2012

VALUATION OF A MIXED-USE PROPERTY

Geo Milev Area

Sofia

Bulgaria

PREPARED EXCLUSIVELY FOR

B.S.R. SOFIA AD

PREPARED BY:

JULY 2012

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 2 of 74

EXECUTIVE SUMMARY

GENERAL TOPICS – PROPERTY 1

Type of property Office Development Project

Address 63 Shipchenski Prohod Boulevard

Post code / City Sofia

Region Sofia - City Region

Country Bulgaria

Plot Number Part of Regulated Land Plots - XI square 95в; XII square 95в; the east real part of the former УПИ XV square 95в

Plot size 4,500 m²

TBA of the buildings 37,825 m²

Tenure Freehold

Marketability Good

Suitability for loan and mortgage purposes

Good

Use according to Zoning Plan

Mixed-use development

Special remarks None

OPINION OF VALUE

Purpose of Valuation: accounting statements Special assumptions: none

Market Value excl. purchasers costs

€ 14,833,000

Instruction date 18th

of June 2012

Revaluation reference date 30th

of June 2012

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 3 of 74

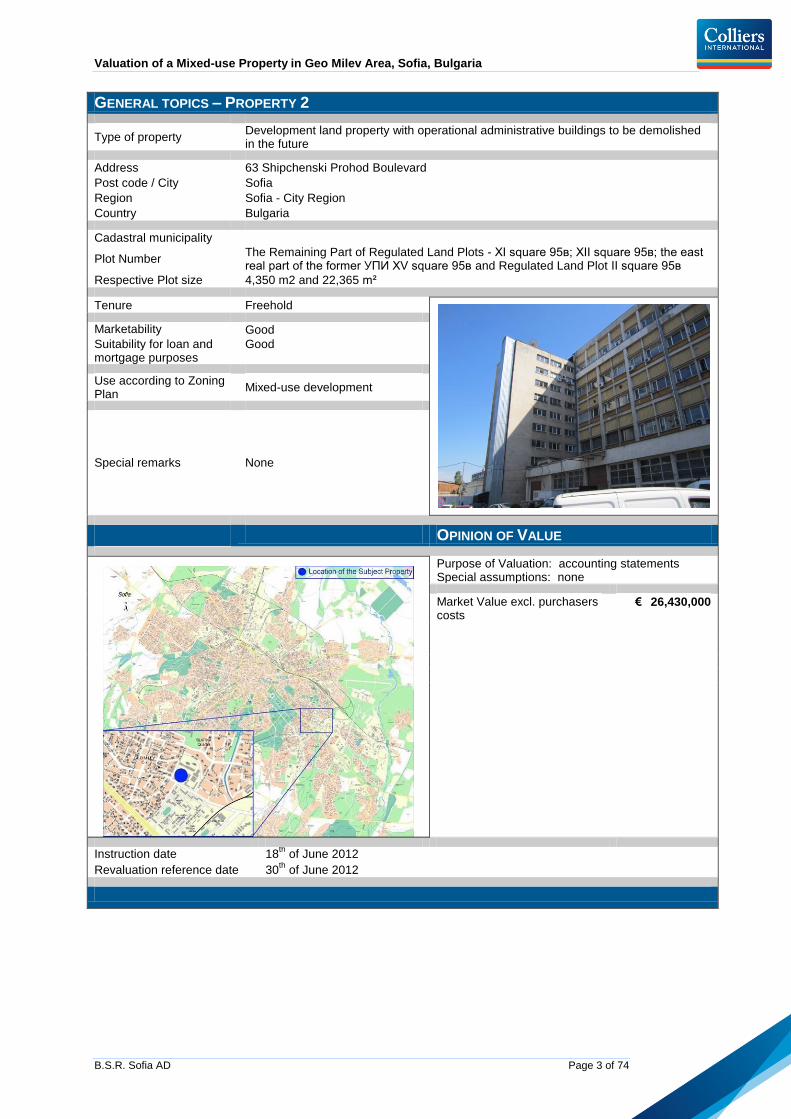

GENERAL TOPICS – PROPERTY 2

Type of property Development land property with operational administrative buildings to be demolished in the future

Address 63 Shipchenski Prohod Boulevard

Post code / City Sofia

Region Sofia - City Region

Country Bulgaria

Cadastral municipality

Plot Number The Remaining Part of Regulated Land Plots - XI square 95в; XII square 95в; the east real part of the former УПИ XV square 95в and Regulated Land Plot II square 95в

Respective Plot size 4,350 m2 and 22,365 m²

Tenure Freehold

Marketability Good

Suitability for loan and mortgage purposes

Good

Use according to Zoning Plan

Mixed-use development

Special remarks None

OPINION OF VALUE

Purpose of Valuation: accounting statements Special assumptions: none

Market Value excl. purchasers costs

€ 26,430,000

Instruction date 18th

of June 2012

Revaluation reference date 30th

of June 2012

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 4 of 74

CONTENTS PAGE

STATUS OF VALUER AND CONFLICTS OF INTEREST ...................................................................... 5

COMPLIANCE WITH RICS AND IVS VALUATION STANDARDS ......................................................... 5

LIABILITY AND PUBLICATION .............................................................................................................. 5

GENERAL INFORMATION ...................................................................................................................... 7

BULGARIA MACROECONOMIC COMMENTARY ............................................................................... 11 GENERAL REMARKS ....................................................................................................................... 11 GROSS DOMESTIC PRODUCT .......................................................................................................... 12 INFLATION ...................................................................................................................................... 15 LABOR FORCE INDICATORS ............................................................................................................. 16 BALANCE OF PAYMENTS ................................................................................................................. 18 DEBT INDICATORS .......................................................................................................................... 18 FOREIGN DIRECT INVESTMENT ........................................................................................................ 18 FORECAST ..................................................................................................................................... 20

SOFIA OFFICE PROPERTY MARKET COMMENTARY ...................................................................... 21 GENERAL REMARKS ....................................................................................................................... 21 DEFINITION OF CLASS A, B, AND C OFFICE BUILDINGS .................................................................... 21 SOFIA SUB-MARKETS ..................................................................................................................... 21 EXISTING CLUSTERS WITH OFFICE BUILDINGS ................................................................................. 23 SUPPLY* ........................................................................................................................................ 27 VACANCY** & AVAILABILITY ............................................................................................................ 28 DEMAND ........................................................................................................................................ 29 RENTAL RATES*** .......................................................................................................................... 30 YIELDS .......................................................................................................................................... 31 PROJECTS IN THE PIPE-LINE ........................................................................................................... 32

SOFIA RESIDENTIAL MARKET COMMENTARY ................................................................................ 38 GENERAL REMARKS ....................................................................................................................... 38 SOFIA DISTRICTS ............................................................................................................................ 39 SUPPLY ......................................................................................................................................... 39 DEMAND ........................................................................................................................................ 42 APARTMENT UNITS SALES PRICES .................................................................................................. 42

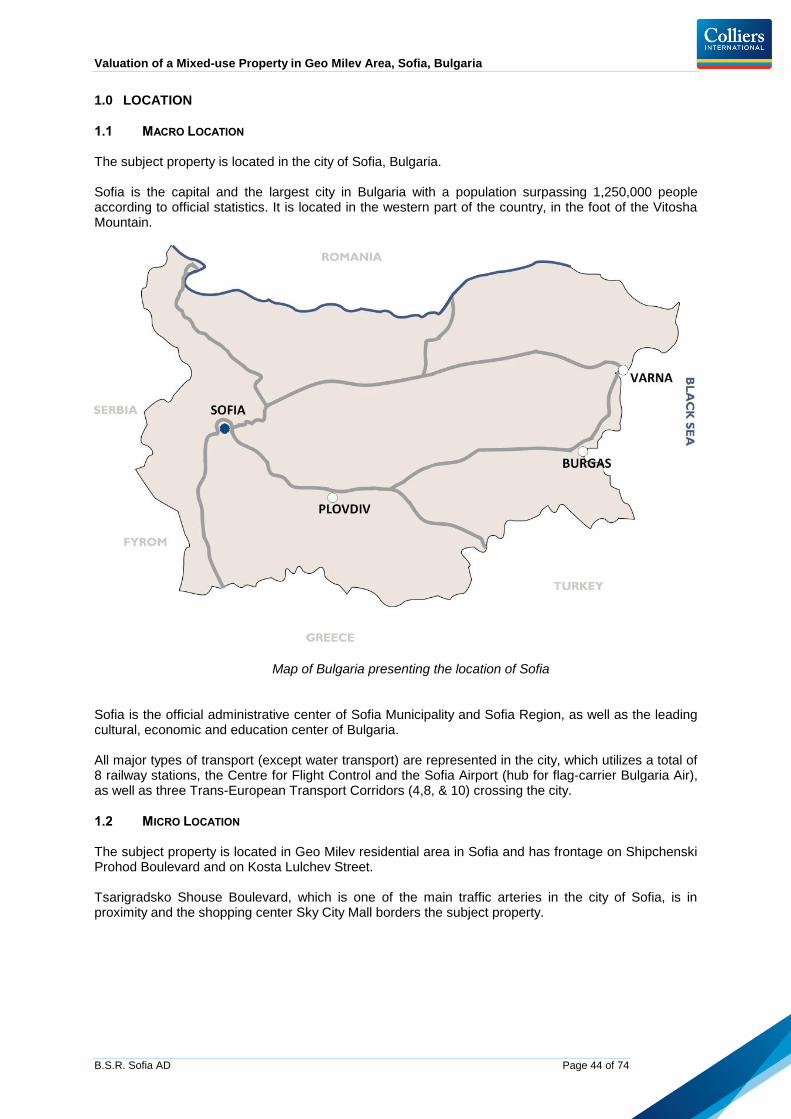

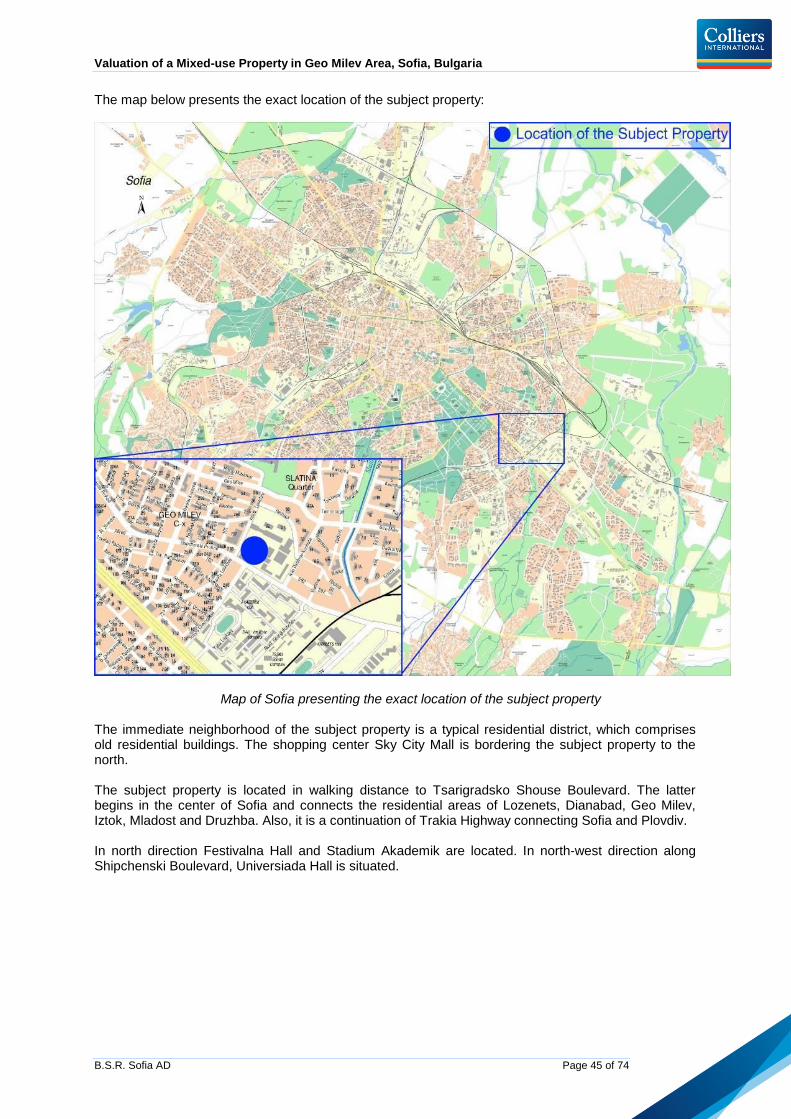

1.0 LOCATION ................................................................................................................................... 44 1.1 MACRO LOCATION .............................................................................................................. 44 1.2 MICRO LOCATION ............................................................................................................... 44

2.0 SUBJECT PROPERTY ................................................................................................................ 47

3.0 ACCOMMODATION .................................................................................................................... 48

4.0 CONDITION ................................................................................................................................. 48

5.0 LEGAL & PLANNING .................................................................................................................. 49 5.1 OWNERSHIP ....................................................................................................................... 49 5.2 SIZE ................................................................................................................................... 49 5.3 LIENS ................................................................................................................................. 49 5.4 CURRENT ZONING ............................................................................................................... 49 5.5 FUTURE DEVELOPMENT ...................................................................................................... 50

6.0 TENURE DETAILS ...................................................................................................................... 51 6.1 TENANCIES ......................................................................................................................... 51 6.2 NON-RECOVERABLE COSTS ................................................................................................ 51

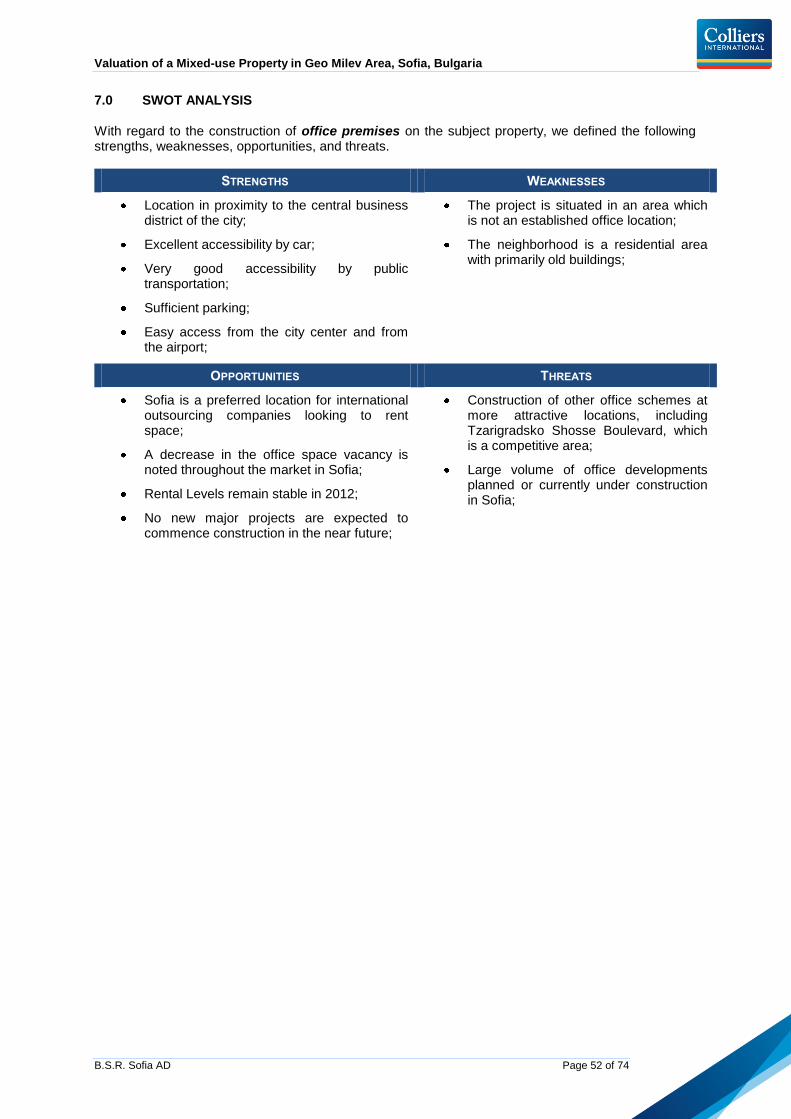

7.0 SWOT ANALYSIS ........................................................................................................................ 52

8.0 VALUATION ................................................................................................................................. 54 8.1 VALUATION APPROACH ....................................................................................................... 54 8.2 FACTORS AFFECTING VALUE ............................................................................................... 54

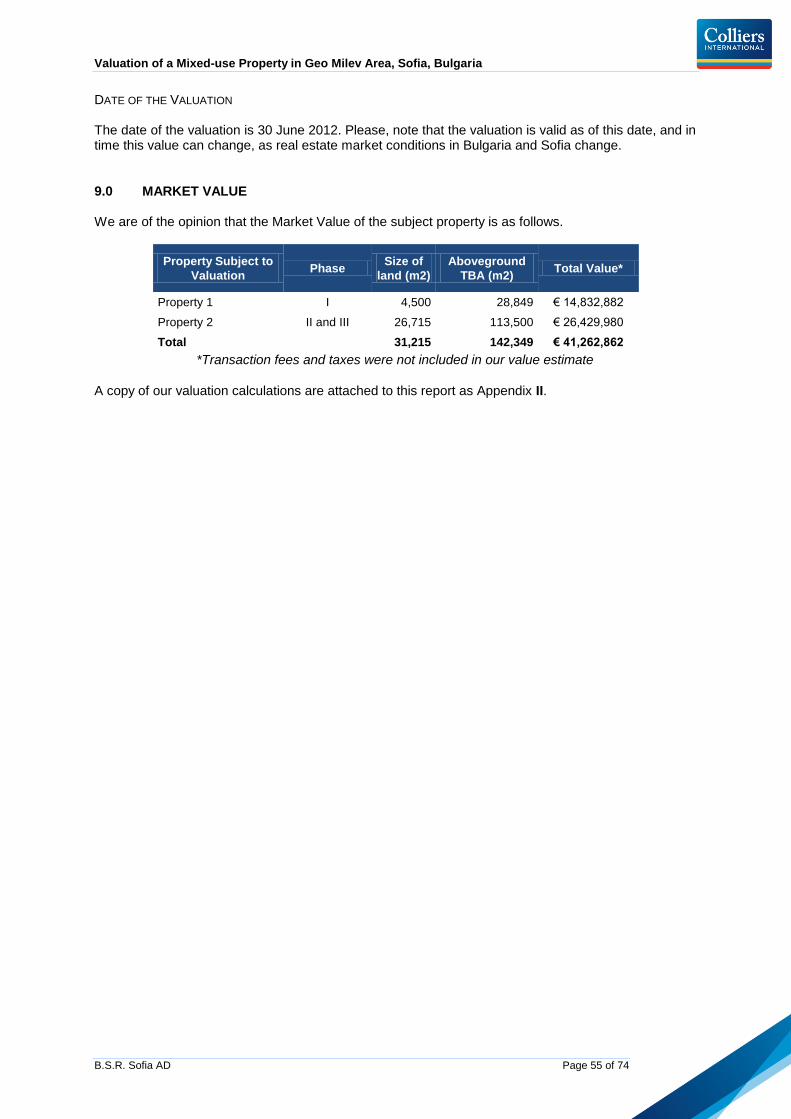

9.0 MARKET VALUE ......................................................................................................................... 55

GENERAL ASSUMPTIONS & DEFINITIONS ....................................................................................... 73

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 5 of 74

Mr. Guy Matarasso Mr. Lazar Geshev B.S.R. Sofia AD 53 Khan Asparuh Street, Sofia 1000 Bulgaria Dear Sirs

MIXED-USE PROPERTY IN SOFIA, BULGARIA

We have considered the above property in order to provide you with our opinion of the Market Value for

financial reporting purposes. We have adopted a valuation date as at 30th

of June 2012.

STATUS OF VALUER AND CONFLICTS OF INTEREST The properties have been valued by suitably qualified surveyors who fall within the requirements as to competence as set out in VS 1.5, 1.6 and 1.7 of the RICS Valuation Standards 8

th Edition (the ‘Red

Book’) issued by the Royal Institution of Chartered Surveyors (the ‘RICS’) and effective 30 March 2012. We confirm that Colliers complies with the requirements of independence, integrity and objectivity under the RICS Valuation Standards 8

th Edition, VS 1.7 and 1.8 and that we have no conflict of interest

in acting on your behalf in this matter. We further would like to state that an open brokerage agreement has been signed in July 2011 between Colliers International EOOD and the Assignor. The latter agreement concerns the leasing of the office premises. This engagement has been discussed with the client who has agreed to proceed with the work on the present assignment.

COMPLIANCE WITH RICS AND IVS VALUATION STANDARDS As per the requirements of RICS Red Book, 8

th edition, VS 1.2, we confirm that the valuations have

been made in accordance with the appropriate sections of the Valuation Statements (‘VS’) contained within the ‘Red Book’ prepared by the ‘RICS’. This is an internationally accepted basis of assessing the value of real estate. The valuation is compliant with both RICS Valuation Standards and the International Valuation Standards, as per RICS Red Book, 8

th edition, VS 1.2

Our General Assumptions and Definitions are presented as an Appendix III to this report.

LIABILITY AND PUBLICATION

This report is private and confidential and for the sole use of BSR Sofia AD. The information contained in this report is privileged and remains intellectual property of Colliers International. It is intended for the use of the individuals and company named in this report and others who have been specifically authorized by Colliers International. Any dissemination, distribution or copying is strictly prohibited without the written consent of Colliers International.

Business Park Sofia Building 7B, Floor 2 1715 Sofia, Bulgaria Tel: (+359 2) 976 9 976 Fax: (+359 2) 976 9 977 www.colliers.com

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 6 of 74

We do not accept any responsibility to any third party for the whole or any part of its contents. Neither the whole nor any part of this valuation or any reference thereto may be included within any published document, circular or statement or disclosed in any way without our prior written consent to the form and context in which it may appear. In breach of this condition, no responsibility can be accepted to third parties for the comments or advice contained in this report. We trust that this report is satisfactory for your purposes. Yours faithfully,

GEORGI KIROV NEVENA MARINOVA-BOGOEVA, MRICS DIRECTOR, INVESTMENT SERVICES MANAGER, VALUATION AND ADVISORY SERVICES

COLLIERS INTERNATIONAL COLLIERS INTERNATIONAL Dated: 27

th of July 2012

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 7 of 74

GENERAL INFORMATION

1. CLIENT

B.S.R. Sofia AD 53 Khan Asparuh Street Sofia, Bulgaria Represented by Mr. Gai Mataraso and Mr. Yair Abrahami

2. VALUATION TEAM QUALIFICATIONS

Mr. Georgi Kirov

Director Investment Services and Valuation and Advisory Services Georgi Kirov has an Executive MBA from the University of Chicago Booth. He directly leads the Investment Sales team and has overall responsibility for the Valuations team. He lead and completed the largest real estate transaction for offices in Southeast Europe – the sale of Business Park Sofia, Bulgaria, with transaction volume of US$ 251 million. He is a member of Colliers Southeast European Investment Advisory Group. Key clients include Credit Suisse, Unicredit, BNP Paribas, BSPF, US Embassy, British Commonwealth Office, Tishman International, General Electric, ECE, AIG, etc.

Mrs. Nevena Marinova-Bogoeva, MRICS

Manager, Valuation and Advisory Services Nevena Marinova holds a Master Degree in Real Estate Investments and Finance from Heriot-Watt University in Great Britain. She is a member of the Royal Institution of Chartered Surveyors. Key clients include Rothschild Private Equity, GE Real Estate, Credit Suisse, Hypo Alpe Adria, Erste Group Immorent, etc.

3. ORDER

Colliers International was appointed by B.S.R. Sofia AD, 53 Khan Asparuh Street, Sofia, Bulgaria to perform a valuation of the property in Sofia as per agreement dated 18

th of June 2012. The objective of

the valuation is to determine Market Value as of 30th

June 2012 of the above property for the purpose of financial reporting.

4. MARKET VALUE Our valuation has been carried out in accordance with the definition of Market Value relevant to international property valuations. The definition of Market Value is set by the International Valuation Standards Committee (International Valuation Standards IVS 2011, 9

th ed.) and adopted by the

European Group of Valuers´ Associations (European Valuation Standards EVS 2003) as well as the

Royal Institution of Chartered Surveyors (RICS Valuation Standards 8th ed., VS 3.2). Therein Market

Value is defined as:

"The estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion."

5. ON-SITE INSPECTION Our team inspected the property on the 29

th of June 2012. The pictures enclosed were taken during

the course of the inspection in digital format. The inspection of the subject property for valuation and the immediate vicinity were carried out by random sampling and without claim to completeness. For hidden components, a condition free of defects was assumed.

6. VALUATION DATE 30 June 2012

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 8 of 74

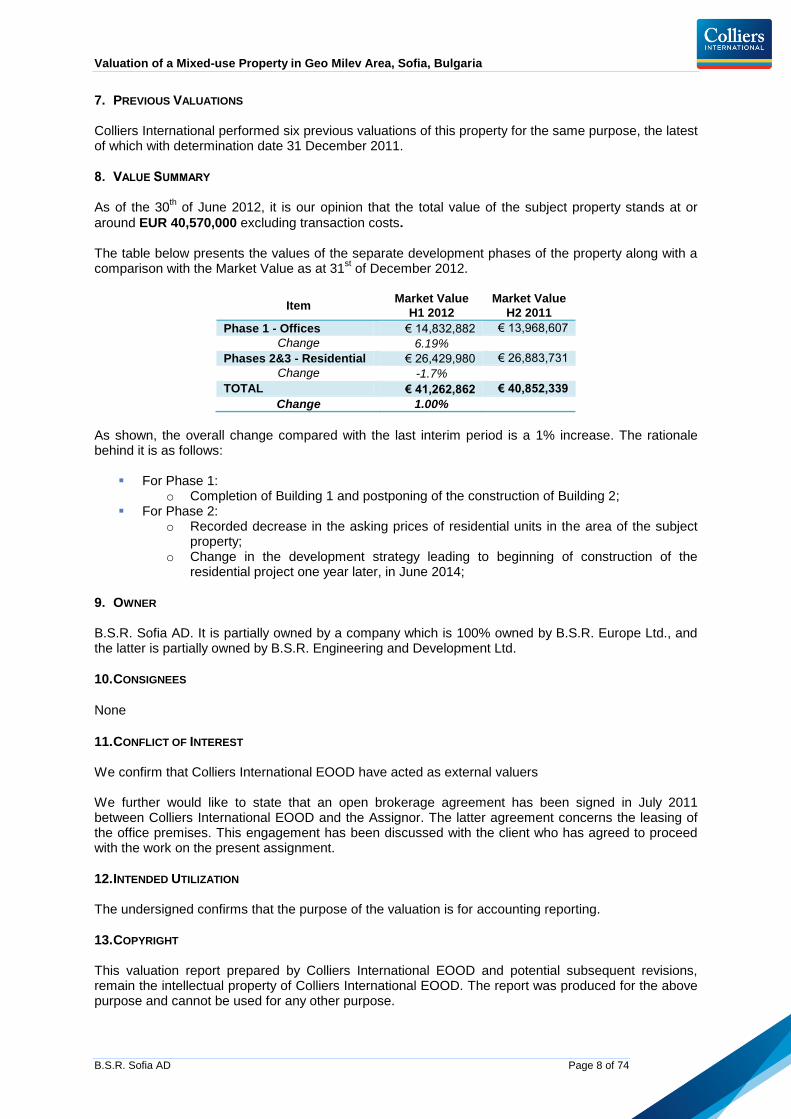

7. PREVIOUS VALUATIONS Colliers International performed six previous valuations of this property for the same purpose, the latest of which with determination date 31 December 2011.

8. VALUE SUMMARY As of the 30

th of June 2012, it is our opinion that the total value of the subject property stands at or

around EUR 40,570,000 excluding transaction costs. The table below presents the values of the separate development phases of the property along with a comparison with the Market Value as at 31

st of December 2012.

Item Market Value

H1 2012

Market Value

H2 2011

Phase 1 - Offices € 14,832,882 € 13,968,607

Change 6.19%

Phases 2&3 - Residential € 26,429,980 € 26,883,731

Change -1.7%

TOTAL € 41,262,862 € 40,852,339

Change 1.00%

As shown, the overall change compared with the last interim period is a 1% increase. The rationale behind it is as follows:

For Phase 1: o Completion of Building 1 and postponing of the construction of Building 2;

For Phase 2: o Recorded decrease in the asking prices of residential units in the area of the subject

property; o Change in the development strategy leading to beginning of construction of the

residential project one year later, in June 2014;

9. OWNER B.S.R. Sofia AD. It is partially owned by a company which is 100% owned by B.S.R. Europe Ltd., and the latter is partially owned by B.S.R. Engineering and Development Ltd.

10. CONSIGNEES

None

11. CONFLICT OF INTEREST We confirm that Colliers International EOOD have acted as external valuers We further would like to state that an open brokerage agreement has been signed in July 2011 between Colliers International EOOD and the Assignor. The latter agreement concerns the leasing of the office premises. This engagement has been discussed with the client who has agreed to proceed with the work on the present assignment.

12. INTENDED UTILIZATION The undersigned confirms that the purpose of the valuation is for accounting reporting.

13. COPYRIGHT This valuation report prepared by Colliers International EOOD and potential subsequent revisions, remain the intellectual property of Colliers International EOOD. The report was produced for the above purpose and cannot be used for any other purpose.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 9 of 74

14. PRINCIPLES OF VALUATION All statements made by the Valuer in terms of the actual characteristics of the plots and buildings and any improvements have been exclusively taken from documentation provided by the Client, which were assessed for the purposes of the report, and the findings of the local inspection. During the local inspection no measurements were taken, or functional tests carried out on the site. All statements made by the Valuer are based on the findings of the local inspection (visual inspection only). A professional investigation of potential structural damage was not undertaken. It is assumed that without examination there are no features of the soil or subsoil that could possibly affect or compromise the sustainable suitability of the property or the health of residents and users. Not being notified of the opposite, we assumed that there are no factors which might adversely affect the current status and/or future development of the subject property, including archaeological finds, landslides or other abnormal land conditions, structural defects, etc. On the date of valuation, it is assumed, without verification, that all public charges, contributions and fees etc., which may have an impact on the value, have been levied and paid unless specifically outlined in the valuation. The valuation was estimated in EUR, rather than in local currency (Bulgarian lev). We do not foresee any problems arising, since the Bulgarian lev has been pegged to the euro since 1999 at a fixed rate of BGN 1.95583 for EUR 1. No change in this exchange rate is foreseen by the Bulgarian government.

15. SPECIAL FEATURES OF THE VALUATION In valuing the property owned by B.S.R. Sofia AD we applied only the Income Capitalization Approach for estimating its market value. The Method is presented in detail below. DISCOUNTED CASH FLOWS As per RICS Red Book, 8th edition, the Income Approach is defined as follows:

“An approach that provides and indication of value by converting future cash flows to a single current capital value.”

DCF analysis uses future free cash flow projections and discounts them to arrive at a present value, which is used to evaluate the potential for investment. If the value estimated through the DCF analysis is higher than the current cost of the investment, the investment opportunity may be considered a good one. It is calculated as:

Source: Investopedia

There are many variations when it comes to what can be used for the cash flows and discount rate in a DCF analysis. The purpose of the calculations is to estimate the income to be received from an investment and to adjust for the time value of money.

16. LIMITS OR EXCLUSION OF LIABILITY The information contained in this report incurs liability to the Assignor of the report only. Liability to any third party is excluded. The contents of this Valuation Report may be relied upon only by the addressees in connection with the Purpose described in the Intended Utilization of this report. No reliance may be placed upon the contents of the Valuation Report and Schedule by any party who is

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 10 of 74

not an addressee of this Valuation Report or by an addressee of this Valuation Report for any purpose other than in connection with the Intended Utilization of this Report. Before this Report, or any part thereof, is reproduced or referred to, in any document, circular or statement, and before its contents, or any part thereof, are disclosed orally or otherwise to a third party, the valuer’s written approval as to the form and context of such publication or disclosure must first be obtained. Such publication or disclosure will not be permitted unless, where relevant, it incorporates the Special Assumptions and/or Departures referred to herein. For the avoidance of doubt such approval is required whether or not Colliers International is referred to by name and whether or not the contents of our Report are combined with others. It should be noted that the undersigned has signed an indemnity agreement with the Client limiting the appraiser's liability as per the following in brief: The appraiser has PI insurance for a maximum sum, which is the full extent of insured liability per event and per period. Colliers International is liable towards the Client as per the terms and conditions of its professional indemnity insurance. The Appraiser is obligated to revert to the insurer regarding any claims made against the appraiser regarding professional liability up to the insured sum. If the claims are beyond the insured sum, claims that are a direct result of the information provided by the client will be the full responsibility of the client. The appraiser will bear full responsibility for any acts of gross negligence in preparing the valuation. The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, Colliers International cannot guarantee it. No responsibility is assumed for any future changes in the market trends, occupancy rates, and sales and rental levels. Projections in particular are based on various assumptions and subjective determinations as to which no guarantee or assurance can be given. These assumptions may vary, as market conditions change.

17. CONFIRMATION OF COMPETENCE As per the requirements of the RICS Red Book 8

th ed., VS 1.5, 1.6 and 1.7 we confirm this valuation is

prepared by, or under the supervision of, an appropriately qualified valuer who accepts responsibility for it. The valuers have sufficient local and national knowledge of the particular property market, and the skills and understanding to undertake this valuation competently.

18. DOCUMENTATION The client provided the following documentation as a basis for the valuation:

Copy of Usage Permit for Phase 1 Tenancy Schedules Tenant Contribution and Operating Expenses Budget

For preparing this report we relied upon this documentation provided by the Assignor. On the basis of the provided documents we assumed that the property has good and clear title. We based our calculations on sizes, concept design and tenant schedules provided by the Assignor and their representatives. The valuation is very sensitive to input data, including accurate property information

provided to us. Should they prove incorrect or incomplete, the accurateness of the valuation may be adversely affected. Colliers is not responsible for the information provided by the Assignor which was depended upon when carrying out the valuation.

19. PROPORTION OF FEES PAYABLE BY THE CLIENT

The proportion of the total fees payable by the Client during the preceding year (2011) relative to the total annual fee income of Colliers International EOOD are minimal.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 11 of 74

BULGARIA MACROECONOMIC COMMENTARY

GENERAL REMARKS In the context of the general economic slowdown on a global level, Bulgaria has experienced a relatively lower degree of negative impact during 2008. However, 2009 showed clear downward trends in key macroeconomic estimations. All of them indicate a financial and economic slowdown in Bulgaria, which, however occurred with a substantial lag of almost 6 months in comparison to Central and Western Europe. In 2010 the economy of Bulgaria began to expand. Thanks to sound financial discipline and good policy that the government led by the middle of 2010, Bulgaria is entering a stage of recovery from the crisis. The country maintains good macroeconomic stability. While the global economy is going out of its deepest recession, Bulgaria benefited from stronger exports and its economy is ready for a gradual recovery. After initial stabilization of the industries, mainly oriented towards exports of goods and services, as a result of restructuring carried out in many sectors of economy and optimization of business improvement, we have already seen improvement in other sectors such as mining, paper and paperboard production and tobacco products. At the beginning of 2012 Bulgaria’s economy was expanding, but signs of a slowdown were evident. The debt crisis in the Euro zone poses a threat to the recovery of the national economy, which is driven mainly by intensive growth of exports to the EU member states. GDP growth shows an increase by 1.7% in 2011, falling behind the rates projected by the government albeit still higher than in the Euro zone which estimates a 1.5% increase. The deteriorating economic situation in Europe result in problems for Bulgaria and force several international financial institutions to cut their forecasts for the country’s real GDP growth in 2012 which is currently expected at 1.5%. Nevertheless, Bulgaria managed to go through the global economic downturn comparatively better than most countries in the region thanks to the conservative management of public finance. Bulgaria is the only European country that has seen its rating upgraded by Moody’s since the beginning of 2010. In 2012 domestic demand remains weak as people are cutting dramatically on consumer spending while at the same time increasing savings as a reflection of negative economic expectation, fear of a new downturn and the constantly rising unemployment. The European Commission forecasts a gradual recovery in private consumption parallel to a stabilization of the labor market in 2012. In terms of foreign direct investments (FDI), which are vital for Bulgaria’s economy, the situation continues to give grounds for concern as in 2011 FDI inflow was only 15% of its 2007 levels. However, in 2011 the negative trend of the previous three years was reversed and a slight increase in annual FDI inflow was registered since 2007. Meanwhile, the government continues to pursue a policy aiming to tighten public spending in order to ensure a slim budget deficit. Two unpopular reforms should be launched in 2012 – retirement age is to be increased and privatization of unprofitable state-owned companies, such as the national railroad and the post office should begin. A top priority for the government remains better absorption of EU funds on which it relies heavily for infrastructure investments. The positive trend of the GDP that started in 2010 continues in 2011 with an increase of 1.7% but is expected to halt in 2012 as economic growth and industrial production shows a negative forecast. Unemployment is on the rise since 2008 and is expected to increase in 2012 as well. The first quarter of 2012 has an unemployment rate of 12.9 which is the highest since the first quarter of 2004. Foreign direct investments in 2011 show an increase of 11% compared to the previous year ending the negative trend from 2007. The following table and graph summarize the key economic indicators for the period 2006 - 2011 and a forecast for 2012.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 12 of 74

Economic Indicators

2006 2007 2008 2009 2010 2011 2012f

Economic Growth (GDP, annual var. in %) 6.4 6.4 6.2 -5.5 0.4 1.7 1.5

Inflation (CPI, annual variation in %, eop) 6.5 12.5 7.8 0.6 4.5 2.8 2.7

Industrial Production (annual var. in %) 6.0 9.6 0.7 -18.3 2.0 5.8 0.9

External Debt (% of GDP) 66.7 78.2 94.2 105.0 108 103 92.0

Current Account Balance (% of GDP) -17.4 -25.3 -23.1 -8.9 -1.4 1.8 1.3

Unemployment rate (% of active population,

eop) 9.1 6.9 6.3 7.6 9.5 10.4 10.7 Source: Focus Economics

Source: Focus Economics

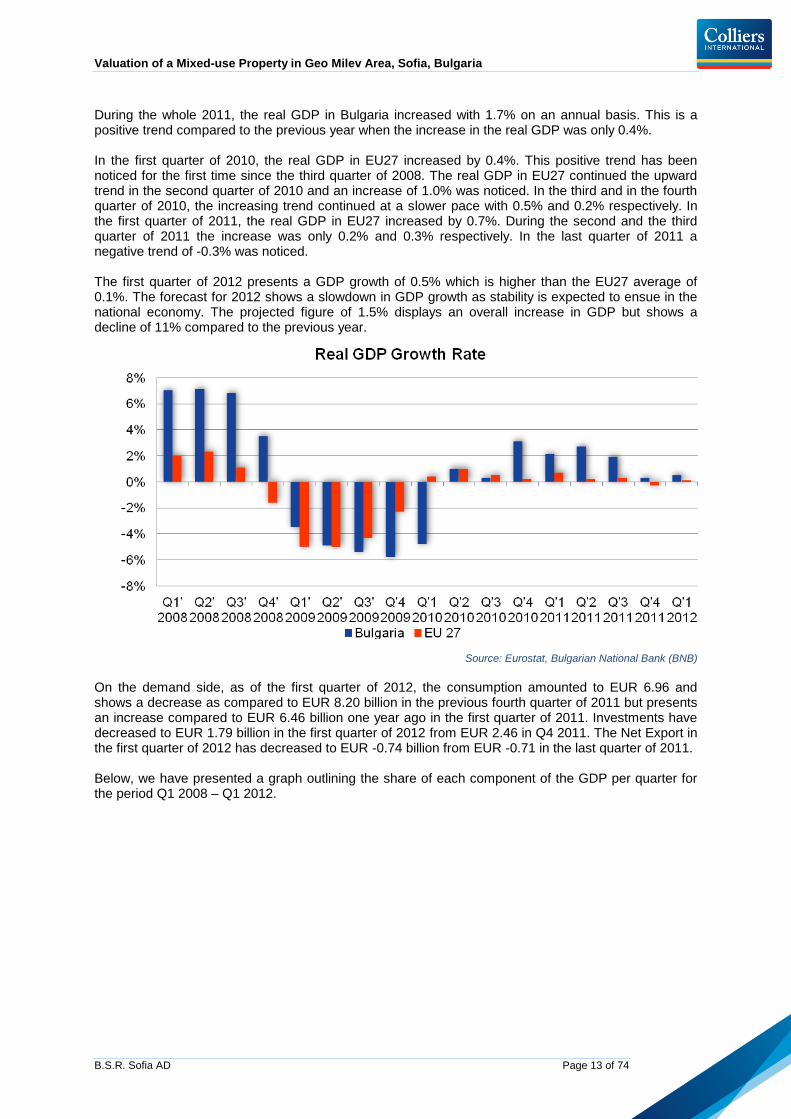

GROSS DOMESTIC PRODUCT The effect of the global market deterioration in Bulgaria became visible with a certain time lag. The slowdown of the economic activity started in the last quarter of 2008, when the GDP growth ceased its acceleration pace and posted a moderate increase of 3.5% on a yearly basis. From January to December 2008 the GDP increased by 6.0% reaching EUR 34.11 billion. Thus, in 2008 Bulgaria commanded one of the highest growth rates within the European Union. In the fourth quarters of 2009, however, the real GDP growth posted a decrease of 3.5%, 4.9%, 5.4% and 5.8% respectively, thus, outlining a negative trend in the macroeconomic climate of Bulgaria for the first time in 12 years. The decrease on an annual basis was primarily caused by the contraction of the corporate investments on the one hand, and a certain decrease in consumption of the population on the other. In the first quarter of 2010, the real GDP in Bulgaria posted a decrease of 4.8%, however in the second quarter of the year an increase of 1.0% was noticed. In the third quarter of 2010, the posted increase was barely 0.3%. In the last quarter of 2010, the real GDP in Bulgaria increased with even 3.1%, almost reaching the level in the fourth quarter of 2008. In the first quarter of 2011, the real GDP in Bulgaria continued its positive trend and a growth of 2.1 % was noticed. The real GDP in Bulgaria increased with even 2.7% in the second quarter of the year. During the third quarter of the year, the noticed increase was 1.9%. In the last quarter of 2011 the positive trend decreased to 0.3% but kept the positive figures.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 13 of 74

During the whole 2011, the real GDP in Bulgaria increased with 1.7% on an annual basis. This is a positive trend compared to the previous year when the increase in the real GDP was only 0.4%. In the first quarter of 2010, the real GDP in EU27 increased by 0.4%. This positive trend has been noticed for the first time since the third quarter of 2008. The real GDP in EU27 continued the upward trend in the second quarter of 2010 and an increase of 1.0% was noticed. In the third and in the fourth quarter of 2010, the increasing trend continued at a slower pace with 0.5% and 0.2% respectively. In the first quarter of 2011, the real GDP in EU27 increased by 0.7%. During the second and the third quarter of 2011 the increase was only 0.2% and 0.3% respectively. In the last quarter of 2011 a negative trend of -0.3% was noticed. The first quarter of 2012 presents a GDP growth of 0.5% which is higher than the EU27 average of 0.1%. The forecast for 2012 shows a slowdown in GDP growth as stability is expected to ensue in the national economy. The projected figure of 1.5% displays an overall increase in GDP but shows a decline of 11% compared to the previous year.

Source: Eurostat, Bulgarian National Bank (BNB)

On the demand side, as of the first quarter of 2012, the consumption amounted to EUR 6.96 and shows a decrease as compared to EUR 8.20 billion in the previous fourth quarter of 2011 but presents an increase compared to EUR 6.46 billion one year ago in the first quarter of 2011. Investments have decreased to EUR 1.79 billion in the first quarter of 2012 from EUR 2.46 in Q4 2011. The Net Export in the first quarter of 2012 has decreased to EUR -0.74 billion from EUR -0.71 in the last quarter of 2011. Below, we have presented a graph outlining the share of each component of the GDP per quarter for the period Q1 2008 – Q1 2012.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 14 of 74

Source: Bulgarian National Bank (BNB)

On the supply side, the gross value added in current prices (GVA) in Q1 2012 was measured to be EUR 6.8 billion. That shows a decrease compared to the last quarter of 2011 when the GVA was EUR 8.50 billion. Breakdowns of the GVA in Q1 2012 and in the whole previous 2011 are presented below. It is visible from the graphics that the Agriculture and Forestry share has increased in Q1 2012 in comparison to the whole 2011 whilst the other two sectors have decreased.

Source: National Statistic Institute

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 15 of 74

Source: National Statistic Institute

INFLATION

In 2008 the increase of CPI continued until June when it reached 15.3% on an annual basis. In the second half of 2008 it started to stabilize and in the last two months of 2008 registered a visible decrease. This was largely attributable to the downward trends in the growth of international fuel and commodity prices reflecting global economic activity slowdown. By the end of 2008 the inflation on an annual basis stood at 7.8% (measured according to the national methodology by CPI). By the end of 2009, the inflation rates stood at 0.6%, which was the lowest level for the period from 1998 to 2010. In 2010 the inflation started increasing again and reached 4.5%. In Q1, Q2, Q3 and Q4 2011 the inflation in Bulgaria was 2.2%, 0.7%, -0.7% and 1.0% respectively. The inflation rate on annual basis in Bulgaria for 2011 was 2.8%, down from 4.5% in 2010. In 2012 inflation is expected to mark a slight decrease to 2.7% that will coincide with the European Harmonized Index of Consumer Prices (HICP) which as of April 2012 stands at 2.7%%.

Source: Eurostat, BNB

As visible from the graph above, the main increase in the prices was noted in the period of 2007 to 2008. It is mainly attributable to the increase of foreign direct investments and was further boosted by catching up of price disparities between Bulgaria and the rest of the European Union.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 16 of 74

During 2010 and 2011, a considerable increase of the inflation in the European Union was noticed – 2.1% and 3.1 % respectively. The annual inflation (measured by HICP) in April 2012 in the European Union was 2.7% showing a decrease of 0.6% compared to March 2012. A year earlier the rate was 3.3%. In April 2012, the lowest annual rates were observed in Sweden (1.0%), Greece (1.5%), Ireland and Romania (both 1.9%) and the highest in Hungary (5.6%), Estonia (4.3%), the Czech Republic and Poland (both 4.0%)

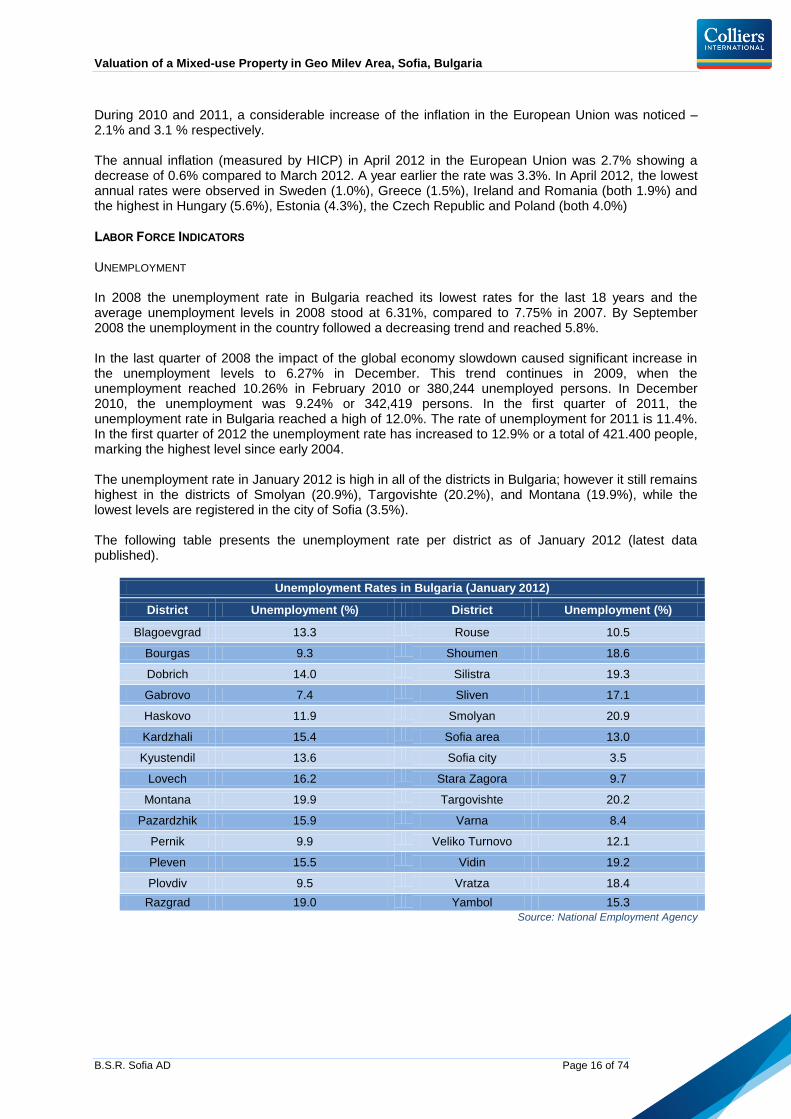

LABOR FORCE INDICATORS UNEMPLOYMENT In 2008 the unemployment rate in Bulgaria reached its lowest rates for the last 18 years and the average unemployment levels in 2008 stood at 6.31%, compared to 7.75% in 2007. By September 2008 the unemployment in the country followed a decreasing trend and reached 5.8%. In the last quarter of 2008 the impact of the global economy slowdown caused significant increase in the unemployment levels to 6.27% in December. This trend continues in 2009, when the unemployment reached 10.26% in February 2010 or 380,244 unemployed persons. In December 2010, the unemployment was 9.24% or 342,419 persons. In the first quarter of 2011, the unemployment rate in Bulgaria reached a high of 12.0%. The rate of unemployment for 2011 is 11.4%. In the first quarter of 2012 the unemployment rate has increased to 12.9% or a total of 421.400 people, marking the highest level since early 2004. The unemployment rate in January 2012 is high in all of the districts in Bulgaria; however it still remains highest in the districts of Smolyan (20.9%), Targovishte (20.2%), and Montana (19.9%), while the lowest levels are registered in the city of Sofia (3.5%). The following table presents the unemployment rate per district as of January 2012 (latest data published).

Unemployment Rates in Bulgaria (January 2012)

District Unemployment (%) District Unemployment (%)

Blagoevgrad 13.3 Rouse 10.5

Bourgas 9.3 Shoumen 18.6

Dobrich 14.0 Silistra 19.3

Gabrovo 7.4 Sliven 17.1

Haskovo 11.9 Smolyan 20.9

Kardzhali 15.4 Sofia area 13.0

Kyustendil 13.6 Sofia city 3.5

Lovech 16.2 Stara Zagora 9.7

Montana 19.9 Targovishte 20.2

Pazardzhik 15.9 Varna 8.4

Pernik 9.9 Veliko Turnovo 12.1

Pleven 15.5 Vidin 19.2

Plovdiv 9.5 Vratza 18.4

Razgrad 19.0 Yambol 15.3

Source: National Employment Agency

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 17 of 74

AVERAGE SALARY

The average national salary in the first quarter of 2012 is EUR 314, which represents more than 6% increase in comparison to the same period of 2011. The highest average salaries are reported in the Information and communication and Electricity, gas, steam and air conditioning supply sectors, respectively EUR 805 and EUR 750, and the lowest rates are reported in the sectors of Administrative and support service activities industry – EUR 230 and in Accommodation and food services – EUR 232.

Source: National Statistic Institute

EMPLOYMENT BY ECONOMY SECTORS The total number of employed people in Bulgaria in Q1 2012 amounted to 2,104,458. More than half of the Bulgarian population is employed in the services sector, which follows the general trend in the European Union. In the last decade the employment in the industrial and manufacturing sectors shrunk considerably and thus resulted in a redistribution of labor force to other sectors of the economy. In the last five years the financial, banking and real estate sectors, as well as the government, persistently attracted labor force. The impact of the global economic and financial slowdown has been most visible in the employment rate in sectors such as Real estate activities, Construction, Agriculture, forestry and fishing and Other service activities where the employment has decreased by 12%, 7%, 6% and 4% respectively in Q1 2012 compared to the same period of the previous year. An increase is observed in Water supply, sewerage and waste management as well as in Information and communication by 8% and 6% respectively. The graph below presents the employment by Economy sectors as of the first quarter of 2012 compared to the first quarter of 2011.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 18 of 74

Source: National Statistic Institute

BALANCE OF PAYMENTS The account balance for 2011 is EUR 0.7 billion (1.8% of GDP), compared to a deficit of EUR -0.5 billion (-1.4% of GDP) in 2010. The main factor for the notable increase was the increase of the export, investments and the current capital account.

DEBT INDICATORS

By the end of 2011 the External Debt exceeded EUR 37.0 billion (102.6% of GDP). Compared to the previous year when the External Debt exceeded EUR 37.8 billion (108.2% of GDP), a decrease of 2.2% is noticed.

FOREIGN DIRECT INVESTMENT

With the global financial market conditions taking down the pressure to costs and to the availability of external liquidity, an increase of approximately 11% in the total FDI for 2011 compared to 2010 has been recorded. The total foreign direct investment by the end of the first quarter of 2012 amounted to EUR 0.24 billion.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 19 of 74

Source: BNB

Six countries contributed the most in the inflow of FDI in 2011. The current investor number one in Bulgaria is the Netherlands with EUR 556.5 million FDI in 2011 and EUR 257.1 million in the first quarter of 2012.

Source: BNB

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 20 of 74

FORECAST Growth in 2012 is expected to slow to 1.5% on the back of weaker domestic and external demand, affected by a crisis-hit and risk-averse Europe. Export volume growth, which has been a major driver of the economy in recent years, will slow considerably in 2012 on account of the expected mild recession in the Eurozone, Bulgaria’s main trading partner. Consumer spending and investment both remain subdued as economic uncertainty persists, unemployment is high and consumers continue to avoid credit usage. However, given the recent long period of weakness, both consumption and investment have the potential to pick up strongly once the uncertainty lifts. The continuing Eurozone debt crisis carries considerable downside risks to the forecast for Bulgaria. In particular, if Eurozone banks' balance sheets are more negatively affected than currently forecasted, then credit provision could stagnate or even fall back, weighing on investment and growth. Bulgaria's banking system is more robust than in some other EU countries. At 12% on paper and 17% in reality (because of the National Bank’s recommendation for the banks not to distribute dividends) the capital adequacy ratio is well over the required EU minimum of 8%. Undershooting the 2011 deficit target, along with having one of the lowest public debt ratios in the EU, helped to keep Bulgaria insulated from the current turmoil on European debt markets and on the right track to fiscal sustainability. Indeed, yields have declined slightly, avoiding additional pressure on an otherwise already tight budget.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 21 of 74

SOFIA OFFICE PROPERTY MARKET COMMENTARY The following section presents the trends evident at the office property market in Sofia.

GENERAL REMARKS The total stock of contemporary class A and B office space reached 1,570,242 square meters during the first half of 2012, an increase by approximately 2%. The quality of the supply of office space does not respond adequately to the rising requirements on the demand side from the international companies. The overall office space vacancy on the Sofia market continued to decrease – from 26% in the beginning of 2012 to 23% by the end of June. Most preferred are office projects class A, which meet international standards. The net absorption of contemporary office space during the first half of 2012 was only 30,000 square meters. The demand is driven mainly by international outsourcing companies who are expanding their business in Bulgaria. Total office occupancy reached over 1,307,209 square meters by the first six months of the year. In the first half of 2012, average asking rents remained unchanged across all submarkets.

DEFINITION OF CLASS A, B, AND C OFFICE BUILDINGS For the purposes of comparison, office buildings are classified in three categories according to their location and physical characteristics. It is important to point out that there is no universal definition. Rather, judgments are made based on the particular market with the common notion that Class A is represented by the premium office product available on the subject market. Class B & C buildings are respectively defined in reference to the quality of the existing Class A supply. When defining Class A, B, or C office space, the latter key features associated with the quality of the office space should be used:

HVAC system Suspended ceilings and raised floors Floor to ceiling height minimum 2.70 Flexibility of internal design High category cabling Modern high speed lifts, if applicable Provision of dedicated car parking Reliable telephone and communications equipment Dual power supply and/or power supply system back-up

Thus, Class A buildings could be more precisely defined as office properties with quality criteria being at the upper end of the scale which are also characterized by good accessibility and location within a recognized business area. Class B office buildings reflect an average or typical building for the market based on the above-mentioned criteria. Finally, class C properties meet below-average requirements and represent the office space of lowest quality available on the market.

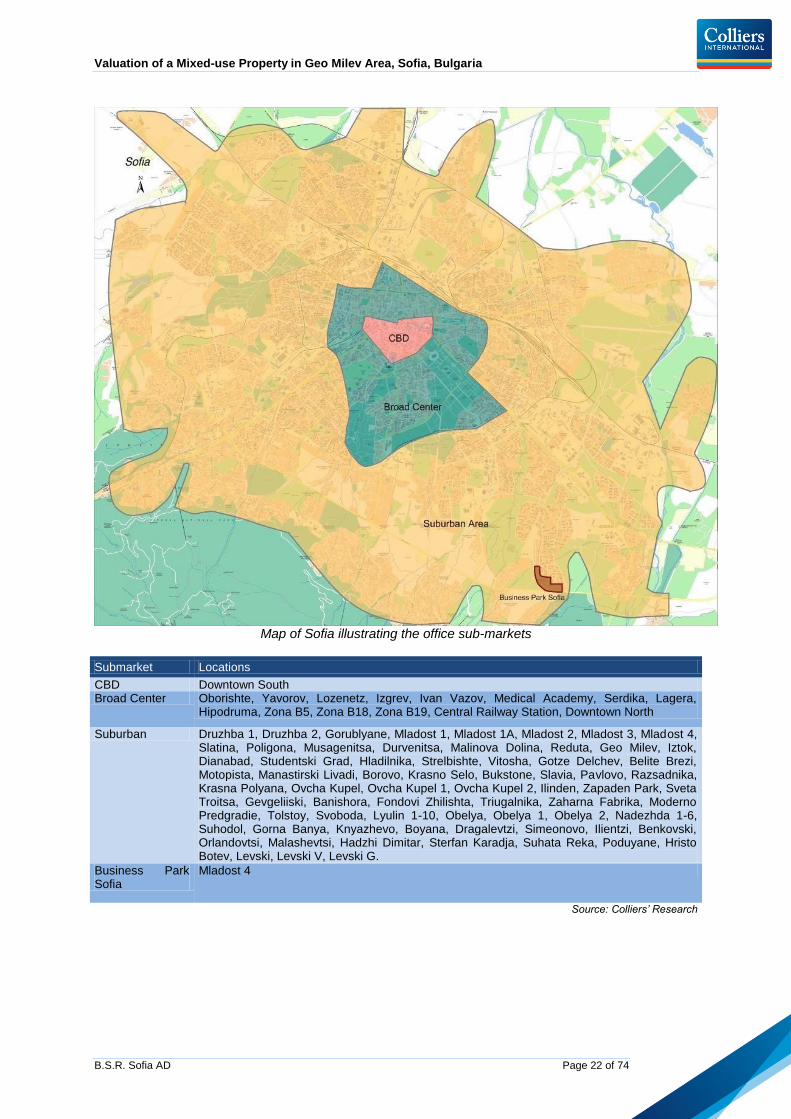

SOFIA SUB-MARKETS The office real estate market in Sofia has undergone a rapid development in the past few years. While several years ago there was no suburban office market, today we can clearly differentiate between the Central Business District (CBD), the Broad Center (BC) and the Suburban office markets. Here it is important to point out that a significant portion of the office supply in Sofia is concentrated in one office complex, namely Business Park Sofia, which is situated in Mladost 4 residential area, bordering the southern arc of the Ring Road of the capital. This is why throughout the present chapter we have explicitly outlined the latter as a separate submarket. A map illustrating the boundaries of the submarkets and a summary table are presented below.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 22 of 74

Map of Sofia illustrating the office sub-markets

Submarket Locations

CBD Downtown South Broad Center Oborishte, Yavorov, Lozenetz, Izgrev, Ivan Vazov, Medical Academy, Serdika, Lagera,

Hipodruma, Zona B5, Zona B18, Zona B19, Central Railway Station, Downtown North

Suburban Druzhba 1, Druzhba 2, Gorublyane, Mladost 1, Mladost 1A, Mladost 2, Mladost 3, Mladost 4, Slatina, Poligona, Musagenitsa, Durvenitsa, Malinova Dolina, Reduta, Geo Milev, Iztok, Dianabad, Studentski Grad, Hladilnika, Strelbishte, Vitosha, Gotze Delchev, Belite Brezi, Motopista, Manastirski Livadi, Borovo, Krasno Selo, Bukstone, Slavia, Pavlovo, Razsadnika, Krasna Polyana, Ovcha Kupel, Ovcha Kupel 1, Ovcha Kupel 2, Ilinden, Zapaden Park, Sveta Troitsa, Gevgeliiski, Banishora, Fondovi Zhilishta, Triugalnika, Zaharna Fabrika, Moderno Predgradie, Tolstoy, Svoboda, Lyulin 1-10, Obelya, Obelya 1, Obelya 2, Nadezhda 1-6, Suhodol, Gorna Banya, Knyazhevo, Boyana, Dragalevtzi, Simeonovo, Ilientzi, Benkovski, Orlandovtsi, Malashevtsi, Hadzhi Dimitar, Sterfan Karadja, Suhata Reka, Poduyane, Hristo Botev, Levski, Levski V, Levski G.

Business Park Sofia

Mladost 4

Source: Colliers’ Research

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 23 of 74

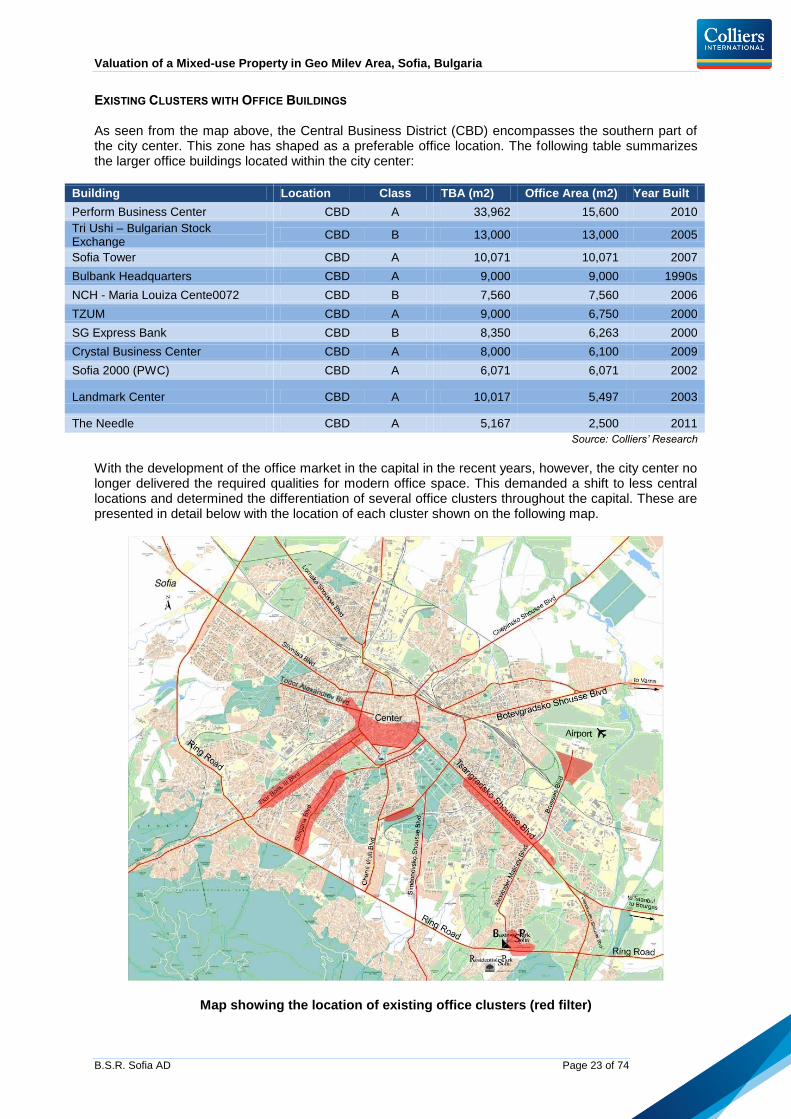

EXISTING CLUSTERS WITH OFFICE BUILDINGS As seen from the map above, the Central Business District (CBD) encompasses the southern part of the city center. This zone has shaped as a preferable office location. The following table summarizes the larger office buildings located within the city center:

Building Location Class TBA (m2) Office Area (m2) Year Built

Perform Business Center CBD A 33,962 15,600 2010

Tri Ushi – Bulgarian Stock Exchange

CBD B 13,000 13,000 2005

Sofia Tower CBD A 10,071 10,071 2007

Bulbank Headquarters CBD A 9,000 9,000 1990s

NCH - Maria Louiza Cente0072 CBD B 7,560 7,560 2006

TZUM CBD A 9,000 6,750 2000

SG Express Bank CBD B 8,350 6,263 2000

Crystal Business Center CBD A 8,000 6,100 2009

Sofia 2000 (PWC) CBD A 6,071 6,071 2002

Landmark Center CBD A 10,017 5,497 2003

The Needle CBD A 5,167 2,500 2011

Source: Colliers’ Research

With the development of the office market in the capital in the recent years, however, the city center no longer delivered the required qualities for modern office space. This demanded a shift to less central locations and determined the differentiation of several office clusters throughout the capital. These are presented in detail below with the location of each cluster shown on the following map.

Map showing the location of existing office clusters (red filter)

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 24 of 74

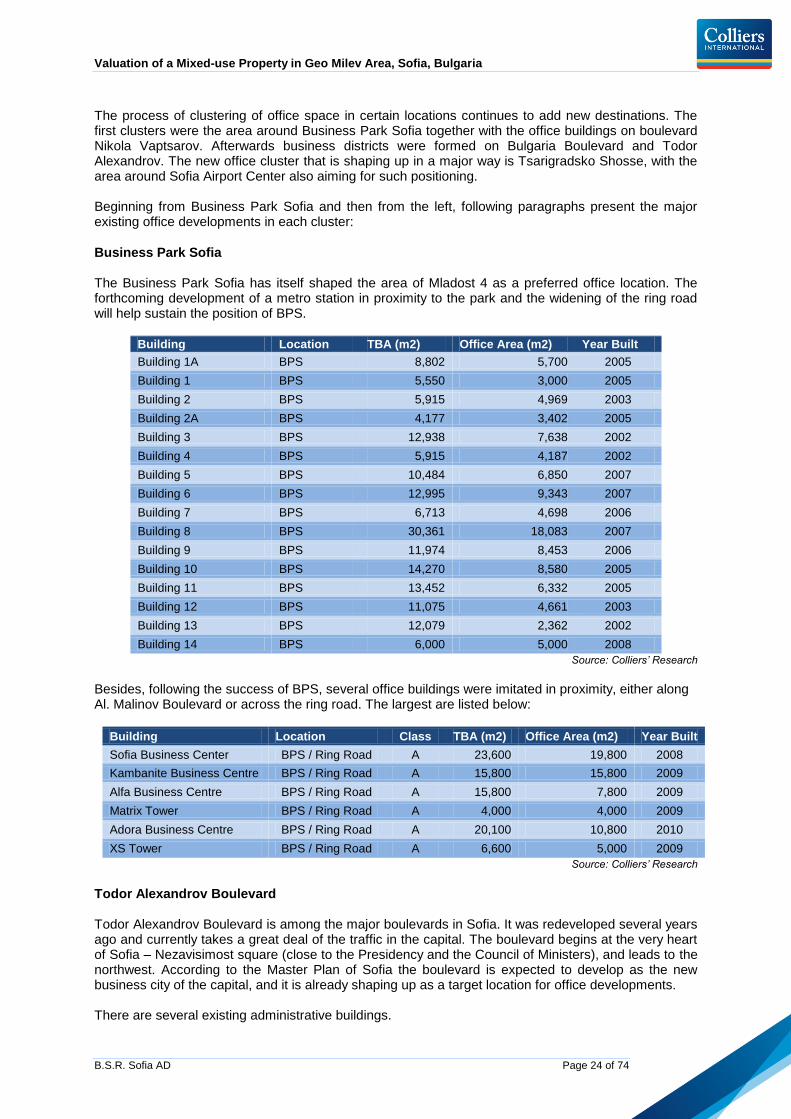

The process of clustering of office space in certain locations continues to add new destinations. The first clusters were the area around Business Park Sofia together with the office buildings on boulevard Nikola Vaptsarov. Afterwards business districts were formed on Bulgaria Boulevard and Todor Alexandrov. The new office cluster that is shaping up in a major way is Tsarigradsko Shosse, with the area around Sofia Airport Center also aiming for such positioning. Beginning from Business Park Sofia and then from the left, following paragraphs present the major existing office developments in each cluster:

Business Park Sofia The Business Park Sofia has itself shaped the area of Mladost 4 as a preferred office location. The forthcoming development of a metro station in proximity to the park and the widening of the ring road will help sustain the position of BPS.

Building Location TBA (m2) Office Area (m2) Year Built

Building 1A BPS 8,802 5,700 2005

Building 1 BPS 5,550 3,000 2005

Building 2 BPS 5,915 4,969 2003

Building 2A BPS 4,177 3,402 2005

Building 3 BPS 12,938 7,638 2002

Building 4 BPS 5,915 4,187 2002

Building 5 BPS 10,484 6,850 2007

Building 6 BPS 12,995 9,343 2007

Building 7 BPS 6,713 4,698 2006

Building 8 BPS 30,361 18,083 2007

Building 9 BPS 11,974 8,453 2006

Building 10 BPS 14,270 8,580 2005

Building 11 BPS 13,452 6,332 2005

Building 12 BPS 11,075 4,661 2003

Building 13 BPS 12,079 2,362 2002

Building 14 BPS 6,000 5,000 2008

Source: Colliers’ Research

Besides, following the success of BPS, several office buildings were imitated in proximity, either along Al. Malinov Boulevard or across the ring road. The largest are listed below:

Building Location Class TBA (m2) Office Area (m2) Year Built

Sofia Business Center BPS / Ring Road A 23,600 19,800 2008

Kambanite Business Centre BPS / Ring Road A 15,800 15,800 2009

Alfa Business Centre BPS / Ring Road A 15,800 7,800 2009

Matrix Tower BPS / Ring Road A 4,000 4,000 2009

Adora Business Centre BPS / Ring Road A 20,100 10,800 2010

XS Tower BPS / Ring Road A 6,600 5,000 2009

Source: Colliers’ Research

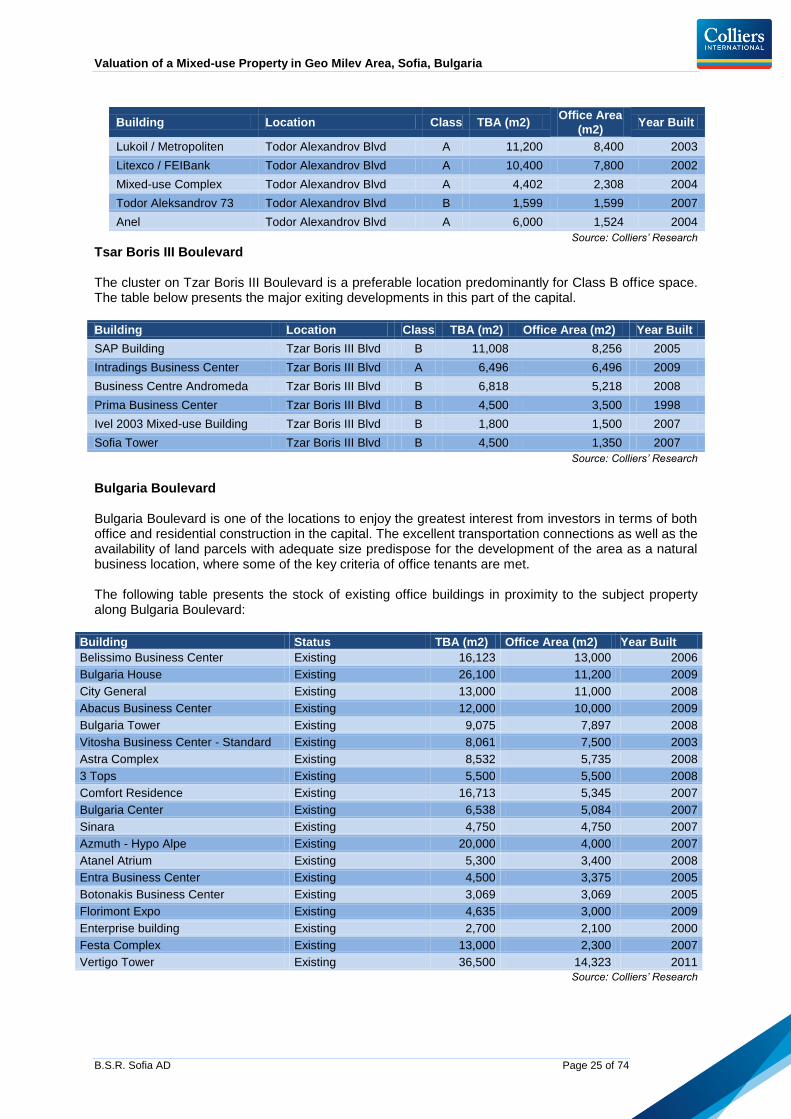

Todor Alexandrov Boulevard Todor Alexandrov Boulevard is among the major boulevards in Sofia. It was redeveloped several years ago and currently takes a great deal of the traffic in the capital. The boulevard begins at the very heart of Sofia – Nezavisimost square (close to the Presidency and the Council of Ministers), and leads to the northwest. According to the Master Plan of Sofia the boulevard is expected to develop as the new business city of the capital, and it is already shaping up as a target location for office developments. There are several existing administrative buildings.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 25 of 74

Building Location Class TBA (m2) Office Area

(m2) Year Built

Lukoil / Metropoliten Todor Alexandrov Blvd A 11,200 8,400 2003

Litexco / FEIBank Todor Alexandrov Blvd A 10,400 7,800 2002

Mixed-use Complex Todor Alexandrov Blvd A 4,402 2,308 2004

Todor Aleksandrov 73 Todor Alexandrov Blvd B 1,599 1,599 2007

Anel Todor Alexandrov Blvd A 6,000 1,524 2004

Source: Colliers’ Research

Tsar Boris III Boulevard The cluster on Tzar Boris III Boulevard is a preferable location predominantly for Class B office space. The table below presents the major exiting developments in this part of the capital.

Building Location Class TBA (m2) Office Area (m2) Year Built

SAP Building Tzar Boris III Blvd B 11,008 8,256 2005

Intradings Business Center Tzar Boris III Blvd A 6,496 6,496 2009

Business Centre Andromeda Tzar Boris III Blvd B 6,818 5,218 2008

Prima Business Center Tzar Boris III Blvd B 4,500 3,500 1998

Ivel 2003 Mixed-use Building Tzar Boris III Blvd B 1,800 1,500 2007

Sofia Tower Tzar Boris III Blvd B 4,500 1,350 2007

Source: Colliers’ Research

Bulgaria Boulevard Bulgaria Boulevard is one of the locations to enjoy the greatest interest from investors in terms of both office and residential construction in the capital. The excellent transportation connections as well as the availability of land parcels with adequate size predispose for the development of the area as a natural business location, where some of the key criteria of office tenants are met. The following table presents the stock of existing office buildings in proximity to the subject property along Bulgaria Boulevard:

Building Status TBA (m2) Office Area (m2) Year Built

Belissimo Business Center Existing 16,123 13,000 2006

Bulgaria House Existing 26,100 11,200 2009

City General Existing 13,000 11,000 2008

Abacus Business Center Existing 12,000 10,000 2009

Bulgaria Tower Existing 9,075 7,897 2008

Vitosha Business Center - Standard Existing 8,061 7,500 2003

Astra Complex Existing 8,532 5,735 2008

3 Tops Existing 5,500 5,500 2008

Comfort Residence Existing 16,713 5,345 2007

Bulgaria Center Existing 6,538 5,084 2007

Sinara Existing 4,750 4,750 2007

Azmuth - Hypo Alpe Existing 20,000 4,000 2007

Atanel Atrium Existing 5,300 3,400 2008

Entra Business Center Existing 4,500 3,375 2005

Botonakis Business Center Existing 3,069 3,069 2005

Florimont Expo Existing 4,635 3,000 2009

Enterprise building Existing 2,700 2,100 2000

Festa Complex Existing 13,000 2,300 2007

Vertigo Tower Existing 36,500 14,323 2011

Source: Colliers’ Research

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 26 of 74

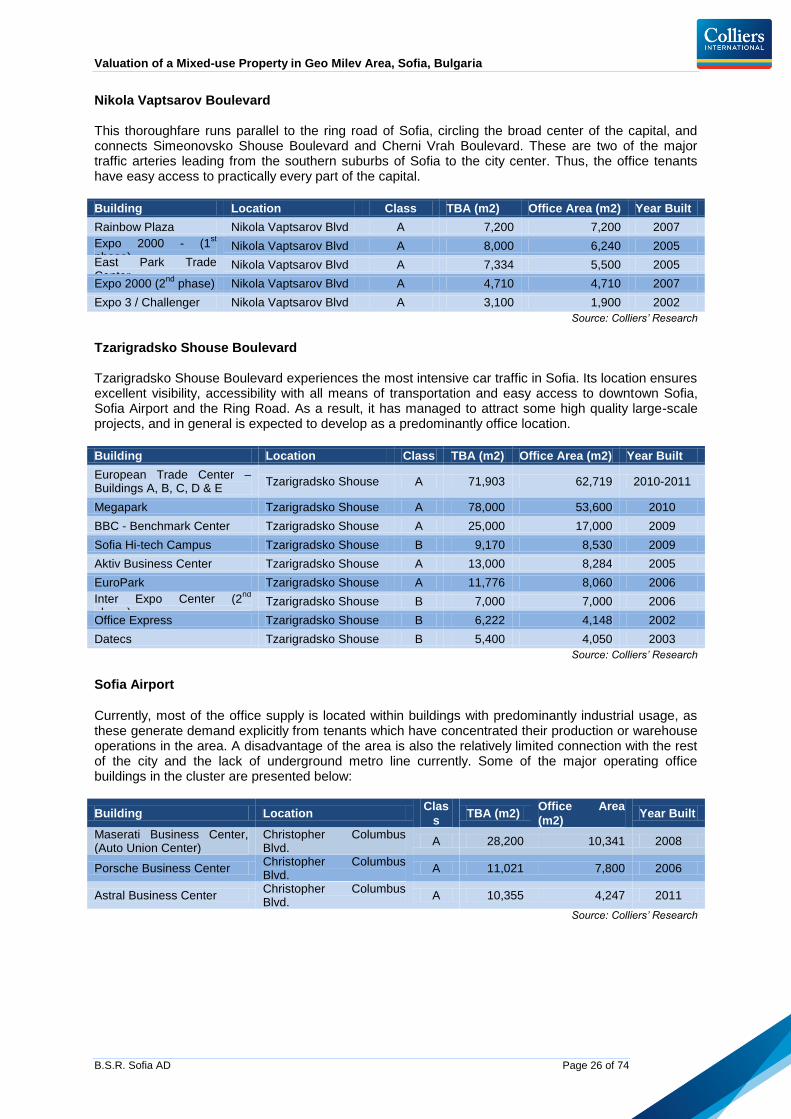

Nikola Vaptsarov Boulevard This thoroughfare runs parallel to the ring road of Sofia, circling the broad center of the capital, and connects Simeonovsko Shouse Boulevard and Cherni Vrah Boulevard. These are two of the major traffic arteries leading from the southern suburbs of Sofia to the city center. Thus, the office tenants have easy access to practically every part of the capital.

Building Location Class TBA (m2) Office Area (m2) Year Built

Rainbow Plaza Nikola Vaptsarov Blvd A 7,200 7,200 2007

Expo 2000 - (1st

phase) Nikola Vaptsarov Blvd A 8,000 6,240 2005

East Park Trade Center

Nikola Vaptsarov Blvd A 7,334 5,500 2005

Expo 2000 (2nd

phase) Nikola Vaptsarov Blvd A 4,710 4,710 2007

Expo 3 / Challenger Nikola Vaptsarov Blvd A 3,100 1,900 2002

Source: Colliers’ Research

Tzarigradsko Shouse Boulevard Tzarigradsko Shouse Boulevard experiences the most intensive car traffic in Sofia. Its location ensures excellent visibility, accessibility with all means of transportation and easy access to downtown Sofia, Sofia Airport and the Ring Road. As a result, it has managed to attract some high quality large-scale projects, and in general is expected to develop as a predominantly office location.

Building Location Class TBA (m2) Office Area (m2) Year Built

European Trade Center – Buildings A, B, C, D & E

Tzarigradsko Shouse A 71,903 62,719 2010-2011

Megapark Tzarigradsko Shouse A 78,000 53,600 2010

BBC - Benchmark Center Tzarigradsko Shouse A 25,000 17,000 2009

Sofia Hi-tech Campus Tzarigradsko Shouse B 9,170 8,530 2009

Aktiv Business Center Tzarigradsko Shouse A 13,000 8,284 2005

EuroPark Tzarigradsko Shouse A 11,776 8,060 2006

Inter Expo Center (2nd

phase)

Tzarigradsko Shouse B 7,000 7,000 2006

Office Express Tzarigradsko Shouse B 6,222 4,148 2002

Datecs Tzarigradsko Shouse B 5,400 4,050 2003

Source: Colliers’ Research

Sofia Airport

Currently, most of the office supply is located within buildings with predominantly industrial usage, as these generate demand explicitly from tenants which have concentrated their production or warehouse operations in the area. A disadvantage of the area is also the relatively limited connection with the rest of the city and the lack of underground metro line currently. Some of the major operating office buildings in the cluster are presented below:

Building Location Clas

s TBA (m2)

Office Area

(m2) Year Built

Maserati Business Center, (Auto Union Center)

Christopher Columbus Blvd.

A 28,200 10,341 2008

Porsche Business Center Christopher Columbus Blvd.

A 11,021 7,800 2006

Astral Business Center Christopher Columbus Blvd.

A 10,355 4,247 2011

Source: Colliers’ Research

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 27 of 74

SUPPLY* *The “Supply” section comprise existing Class A and B office buildings, no more than 15 years old and with office areas exceeding 1,000 square meters. The inventory of office space in Sofia increased by approximately 2% during the first half of 2012. At present, the total stock of Class A and Class B office premises is estimated at 1,570,242 square meters, although this comprises varying degrees of quality. 13% of the total office stock for rent is located in Sofia’s Central Business District, while 68% of the office supply, or 1,049,369 square meters, are located in the suburban areas of the capital. The Broad Center represents 20%. As mentioned above the total stock of Class A office premises has reached 824,352 square meters. However, following international classification of office space and the requirements of multinational clients, the actual class A office space that meets the requirements is estimated at approximately 310,000 square meters, concentrated in 17 contemporary office projects. The characteristics of these buildings include high construction quality, good location, easy access both by car and public transport, efficient layout, and high-quality systems. This Class A office space represents only 19% of the overall stock on the market. The table below presents the trends in the development of the office submarket in Sofia for the period H2 2008 – H1 2012.

Submarket H2 2008 H1 2009 H2 2009 H1 2010 H2 2010 H1 2011 H2 2011

H1 2012*

CBD 147,954 150,604 154,304 172,917 188,517 188,517 199,770 204,963

Broad Centre 220,486 221,625 241,669 248,086 272,019 291,335 291,335 315,910

Suburban 505,546 592,352 665,565 746,650 857,243 898,228 1,047,535 1,049,396

Total Gross

Area* 873,986 964,581 1,061,538 1,167,653 1,317,779 1,378,080 1,538,640 1,570,242

Source: Colliers’ Research *The total floor space of a building, including unusable space, measured from the outside walls

The following table shows the total stock of contemporary office space for the period H1 2008 to H1 2012:

Source: Colliers’ Research

The most developed area with contemporary office space remains the Suburban area, with a share of 67% of the total market and a slight growth compared to six months ago. On a year-on-year basis the stock in this area has increased with 151,168 square meters. The Suburban stock is mostly concentrated along the main boulevards and traffic arteries in Sofia. This trend is driven by the lack of suitable land plots for large office projects in the CBD and Broad Center area.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 28 of 74

Several office buildings were completed during the past year and added their share to the total office stock in Sofia. High-quality premises appeared in the Suburban locations, as well as in the Central Business District. The new suburban projects are located along main traffic routes in Sofia providing excellent accessibility such as Sopharma Towers located on Dragan Tsankov Boulevard, which added 23,000 square meters to the contemporary Class A office space in Sofia. Other developments completed during the second half of 2011 are The Needle in the Central Business District with 2,500 square meters leasable office area; Vertigo and Astral business centers, which combined delivered approximately 20,000 square meters of office space to the market in the suburban area. In order to account for the most recent development of the office property market, below we have presented a table with key data for selected recent office deliveries.

SELECTED CLASS A & B OFFICE BUILDINGS COMPLETED IN H1 2012

Building Name Location Gross Office Area (m2)

TAO Broad Center 1 700

Urban Model Broad Center 6 000

Energy Center Broad Center 8 000

Monterosa Business Point CBD 5 000 Source: Colliers’ Research

Currently, approximately 310,000 square meters of office space is in the active pipeline. 70% of the future supply is located in the suburban areas of the city, and only few of them can be classified as Class A. Compared to the end of 2010 this number has decreased with 150,000 square meters, which is mostly a result of projects being completed. The chart below presents the total amount of class A and B office space under construction as of H2 2011.

Source: Colliers’ Research

Further details on the larger projects currently under development are presented in the Section

Projects in the Pipe-line of the present chapter.

VACANCY** & AVAILABILITY **Vacancy: unoccupied class A and B office space with permission for usage. The overall vacancy in Sofia office market has slightly decreased by 3% to 363,857 square meters. In percentages, the vacancy at the end of 2011 amounted to 25.2% of total, contemporary stock in Sofia and in H1 2012 that percentage is 23%.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 29 of 74

The distribution of vacant office space is not spread evenly across the city. The majority of vacant space continues to be concentrated in the suburban part of the capital, where the share of unoccupied space is equal to 263,033 square meters. Vacancy in the Central Business District reached 38, 732 square meters. The absorption of vacant office space will continue, mainly due to the lack of new office supply in the active pipeline. It will be focused on Class A office projects, which meet international standards. The vacancy in the CBD has slightly increased, amounting to 36,374 square meters, mainly due to the completion of new projects. In the Suburban areas, the vacancy level remained unchanged. This is due to the fact that several projects were completed during this period, while at the same time the absorption in the premium Class A office premises increased as well. Absorption of vacant space is expected to continue, mainly concentrated in offices class A. The charts below present the vacancy rates per submarket.

Source: Colliers’ Research

DEMAND The net absorption for the first half of 2012 was 30,000 square meters. To a large extent this demand was driven by international outsourcing companies, which have expanded their business in Bulgaria, such as the American IT company Ingram Micro. Other international companies have also registered interest in Bulgaria as an appropriate destination to outsource activities. These companies have the financial means and the clear belief, that high-quality office premises are needed to support their core business. As a result of the competitive rental prices, more companies could afford to relocate to higher-class office space or location with better accessibility and attractiveness. The Suburban areas along major traffic arteries such as Tsarigradsko Shouse enjoyed strong demand from tenants who appreciate quick access and contemporary office space with European Trade Center and Megapark attracting several new tenants. Clients for office space have become more knowledgeable and selective with regard to real estate leasing and purchases. Companies started to realize the importance of better access, improved working environment, property management services and availability of amenities. The majority of office occupiers prefer to lease office space rather than to buy. Demand for offices both less than 200 square meters in size or more than 2,000 square meters is limited.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 30 of 74

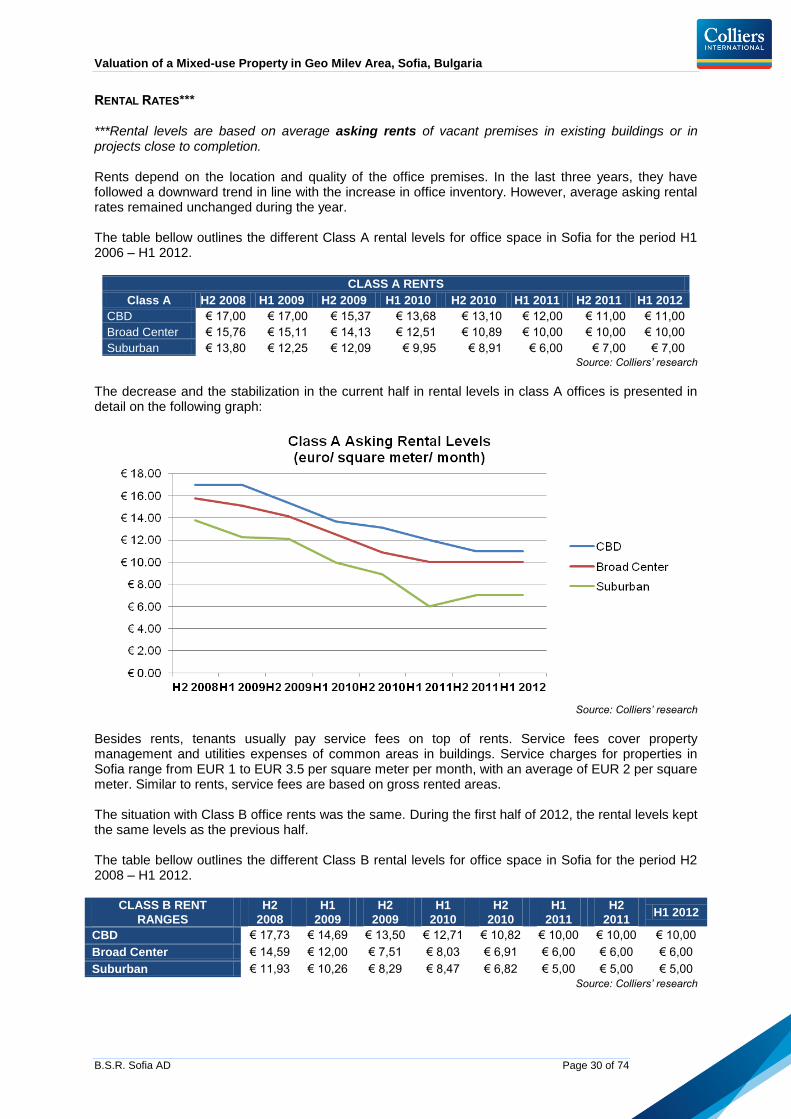

RENTAL RATES*** ***Rental levels are based on average asking rents of vacant premises in existing buildings or in projects close to completion. Rents depend on the location and quality of the office premises. In the last three years, they have followed a downward trend in line with the increase in office inventory. However, average asking rental rates remained unchanged during the year. The table bellow outlines the different Class A rental levels for office space in Sofia for the period H1 2006 – H1 2012.

CLASS A RENTS

Class A H2 2008 H1 2009 H2 2009 H1 2010 H2 2010 H1 2011 H2 2011 H1 2012

CBD € 17,00 € 17,00 € 15,37 € 13,68 € 13,10 € 12,00 € 11,00 € 11,00

Broad Center € 15,76 € 15,11 € 14,13 € 12,51 € 10,89 € 10,00 € 10,00 € 10,00

Suburban € 13,80 € 12,25 € 12,09 € 9,95 € 8,91 € 6,00 € 7,00 € 7,00 Source: Colliers’ research

The decrease and the stabilization in the current half in rental levels in class A offices is presented in detail on the following graph:

Source: Colliers’ research

Besides rents, tenants usually pay service fees on top of rents. Service fees cover property management and utilities expenses of common areas in buildings. Service charges for properties in Sofia range from EUR 1 to EUR 3.5 per square meter per month, with an average of EUR 2 per square meter. Similar to rents, service fees are based on gross rented areas. The situation with Class B office rents was the same. During the first half of 2012, the rental levels kept the same levels as the previous half. The table bellow outlines the different Class B rental levels for office space in Sofia for the period H2 2008 – H1 2012.

CLASS B RENT

RANGES

H2

2008

H1

2009

H2

2009

H1

2010

H2

2010

H1

2011

H2

2011 H1 2012

CBD € 17,73 € 14,69 € 13,50 € 12,71 € 10,82 € 10,00 € 10,00 € 10,00

Broad Center € 14,59 € 12,00 € 7,51 € 8,03 € 6,91 € 6,00 € 6,00 € 6,00

Suburban € 11,93 € 10,26 € 8,29 € 8,47 € 6,82 € 5,00 € 5,00 € 5,00

Source: Colliers’ research

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 31 of 74

The decrease and the stabilization in the current half in rental levels in class B offices is presented in detail on the following graph:

Source: Colliers’ research

It should be mentioned that the gross area described above is different from the gross floor area of these buildings. The reason for that is that the gross floor area includes the total area on each floor plate to the outer edge of the building while the net area used to calculate the rent includes inner columns and only half of the outer walls.

YIELDS The investment market in Bulgaria remains quite fragmented, with limited number of transactions. The following table presents the development in prime yields for office properties since 2005.

Property Developer Buyer Timing GLA

(m2)

TBA

(m2)

Gross

Initial

Yield

Soravia Business Centre Soravia Landmark Q1 2005 6,500 10,000 7.75%

B1 in BPS Lindner Blue House Q2 2005 3,659 5,347 n/a

Business Park Sofia Lindner Gramercy Q4 2006 115,123 187,000 7.6%

Challenger Building PCI Automotive Blue House Q2/3 2005

2,934 9.2%

Sofia Tower ITIT; Aviv GE; Quinlan Private Q1 2006 8,500 10,000 8.8%

Porsche Center Orchid Developments

Landmark Q1 2007 8,000 8,500 8.0%

Landmark Portfolio Altima, Thor Biorgolfson

Bridgecorp Q4 2007 92,300 7-8%

Business Park Varna Sistec Africa-Izrael Investment Europe

Q4 2007 63,000 119,000 9.9%

BSR Center BSR Center Atlas Estates Limited Q4 2007 3,472 3,472 8.0%

Avto Union Center Avto Union Holding

Eurohold Q3 2009 10,341 28,165 10%

Source: Colliers’ research

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 32 of 74

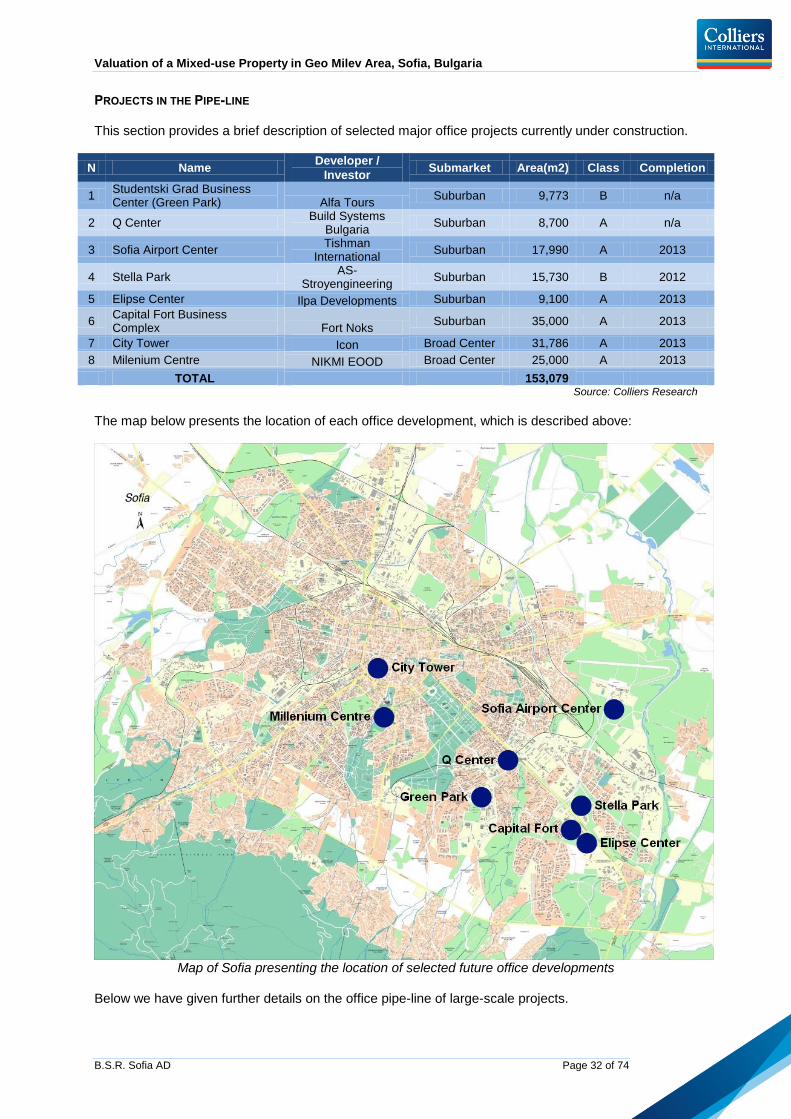

PROJECTS IN THE PIPE-LINE This section provides a brief description of selected major office projects currently under construction.

N Name Developer /

Investor Submarket Area(m2) Class Completion

1 Studentski Grad Business Center (Green Park) Alfa Tours

Suburban 9,773 B n/a

2 Q Center Build Systems

Bulgaria Suburban 8,700 A n/a

3 Sofia Airport Center Tishman

International Suburban 17,990 A 2013

4 Stella Park AS-

Stroyengineering Suburban 15,730 B 2012

5 Elipse Center Ilpa Developments Suburban 9,100 A 2013

6 Capital Fort Business Complex Fort Noks

Suburban 35,000 A 2013

7 City Tower Icon Broad Center 31,786 A 2013

8 Milenium Centre NIKMI EOOD Broad Center 25,000 A 2013

TOTAL 153,079 Source: Colliers Research

The map below presents the location of each office development, which is described above:

Map of Sofia presenting the location of selected future office developments

Below we have given further details on the office pipe-line of large-scale projects.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 33 of 74

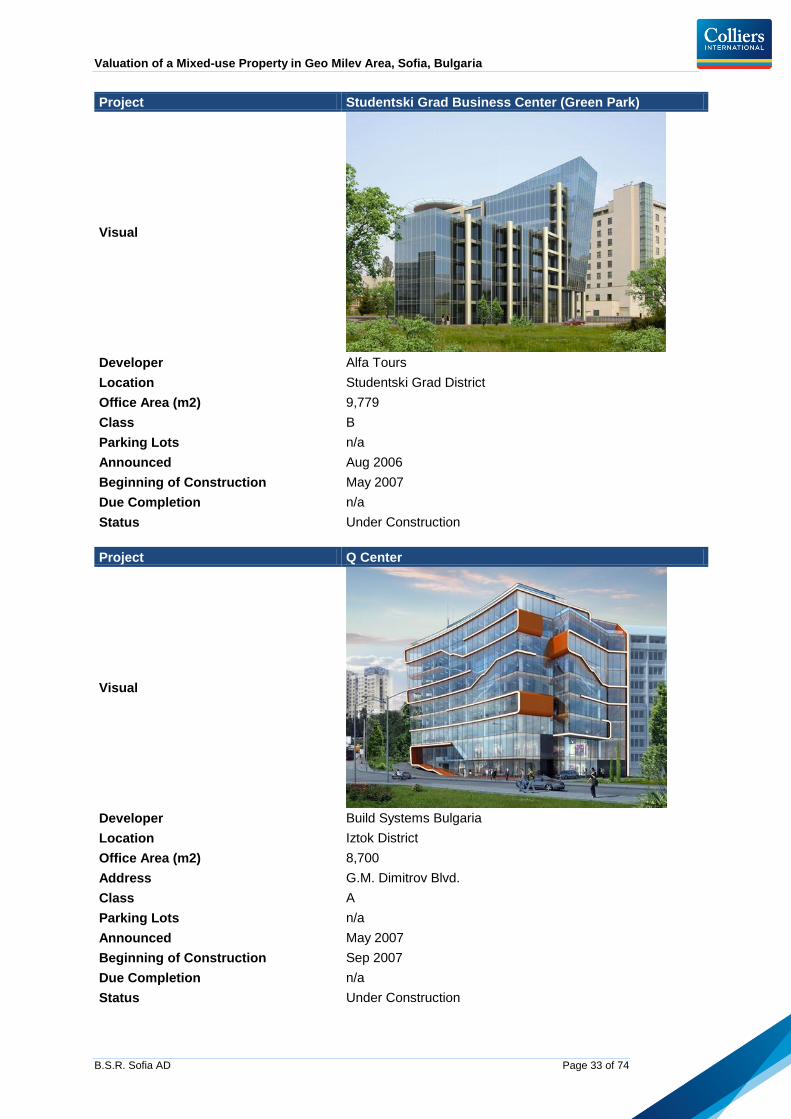

Project Studentski Grad Business Center (Green Park)

Visual

Developer Alfa Tours

Location Studentski Grad District

Office Area (m2) 9,779

Class B

Parking Lots n/a

Announced Aug 2006

Beginning of Construction May 2007

Due Completion n/a

Status Under Construction

Project Q Center

Visual

Developer Build Systems Bulgaria

Location Iztok District

Office Area (m2) 8,700

Address G.M. Dimitrov Blvd.

Class A

Parking Lots n/a

Announced May 2007

Beginning of Construction Sep 2007

Due Completion n/a

Status Under Construction

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 34 of 74

Project Sofia Airport Center

Visual

Developer Tishman International

Location Sofia Airport

Address Christopher Columbus Blvd

Land Plot Size (m2) 124,835

Total Built-up Area (m2) 165,000

Office Area (m2) 17,990

Class A

Parking Lots 499

Announced Nov 2006

Beginning of Construction Jun 2007

Due Completion 2013

Status Under Construction

Project Stella Park

Visual

Developer AS-Stroyengineering

Address Tsarigradsko shose Blvd

Office Area (m2) 15,730

Class A

Parking Lots 71

Announced Jun 2007

Beginning of Construction Oct 2007

Due Completion Dec 2012

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 35 of 74

Status Under Construction

Project Elipse Centre

Visual

Developer Ilpa Developments

Location Mladost, 7-mi km

Address Tsarigradsko Shouse Blvd.

Land Plot Size (m2) 3,660

Total Built-up Area (m2) 18,764

Office Area (m2) 9,100

Class A

Parking Lots 165

Announced Jun 2007

Beginning of Construction Aug 2008

Due Completion Officially announced 2013

Status Currently on hold

Project Capital Fort Business Complex

Visual

Developer Fort Noks

Location 7th Kilometar

Address Tsarigradsko Shousse Blvd.

Land Plot Size (m2) 17,707

Total Built-up Area (m2) 80,088

Office Area (m2) 42,300

Class A

Parking Lots 720

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 36 of 74

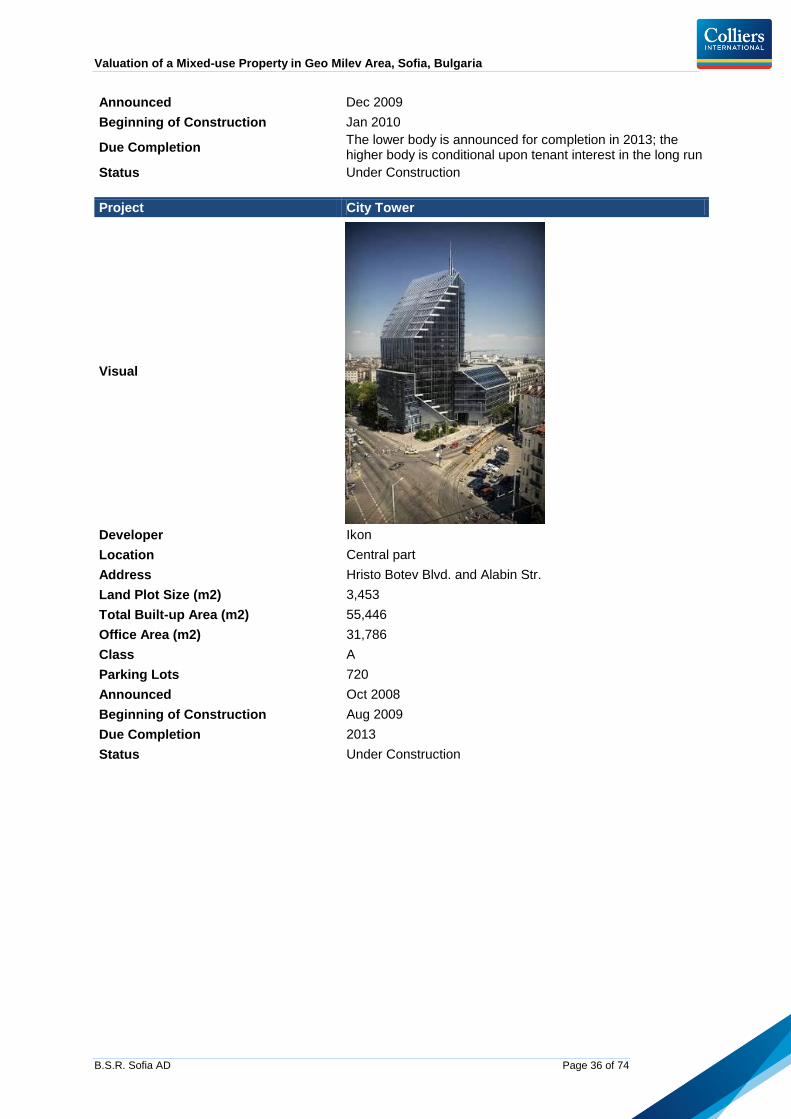

Announced Dec 2009

Beginning of Construction Jan 2010

Due Completion The lower body is announced for completion in 2013; the higher body is conditional upon tenant interest in the long run

Status Under Construction

Project City Tower

Visual

Developer Ikon

Location Central part

Address Hristo Botev Blvd. and Alabin Str.

Land Plot Size (m2) 3,453

Total Built-up Area (m2) 55,446

Office Area (m2) 31,786

Class A

Parking Lots 720

Announced Oct 2008

Beginning of Construction Aug 2009

Due Completion 2013

Status Under Construction

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 37 of 74

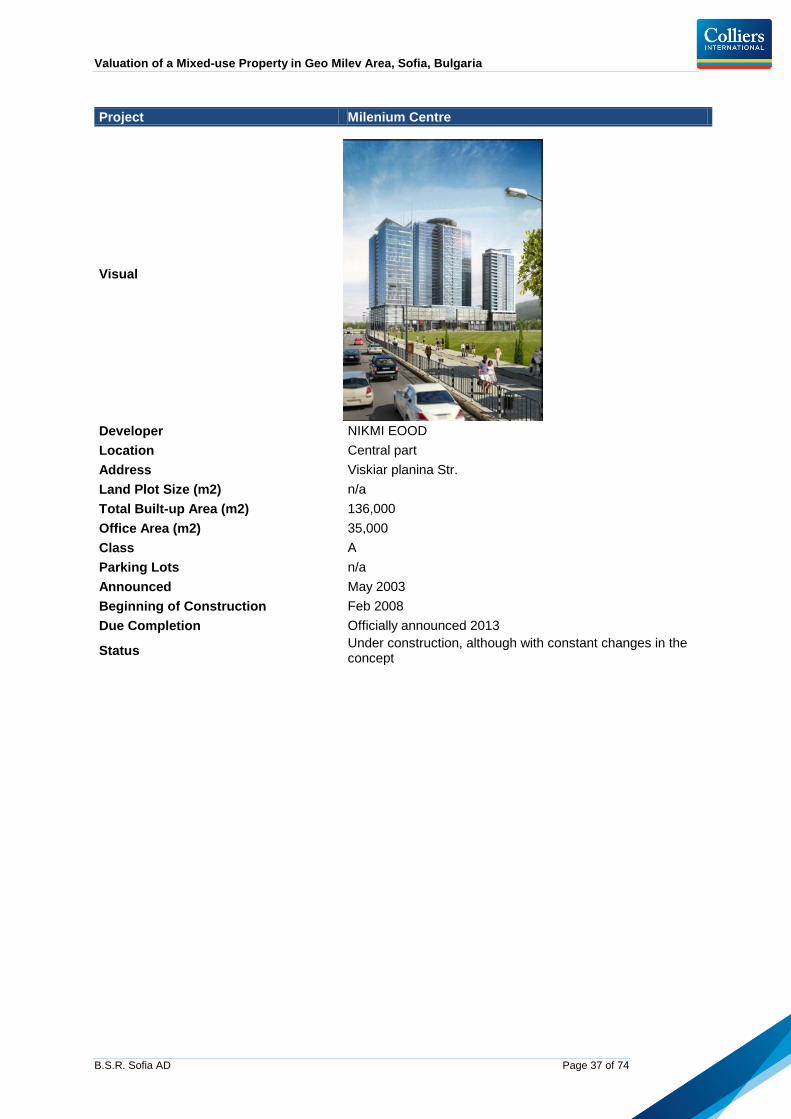

Project Milenium Centre

Visual

Developer NIKMI EOOD

Location Central part

Address Viskiar planina Str.

Land Plot Size (m2) n/a

Total Built-up Area (m2) 136,000

Office Area (m2) 35,000

Class A

Parking Lots n/a

Announced May 2003

Beginning of Construction Feb 2008

Due Completion Officially announced 2013

Status Under construction, although with constant changes in the concept

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 38 of 74

SOFIA RESIDENTIAL MARKET COMMENTARY The following section presents an overview of the residential property market in Sofia. Further in the section we have focused explicitly on Geo Milev residential area, where the subject property is located.

GENERAL REMARKS HISTORIC TRENDS The central part of the city and the oldest housing estates of Sofia were built-up mainly with massive brick blocks of houses with beautiful facades in the typical socialist style and traditions and the majority of them have already become monuments of culture. The housing estates, which were developed later on in time – in the 1970s, were built-up predominantly with panel and monolithic concrete structure blocks. One of the characteristic features of the zones developed by the end of the 1980s is the vast inter-block areas with gardens and parks. A new stage in the construction development of the capital started in the beginning of the 1990s – the so-called “new development”. Due to the fact that in the first years of the period there were no clearly established construction regulations, some parts of the city were over-built with blocks of questionable quality. RECENT DEVELOPMENT The period 2000 – 2008 was marked by an unprecedented market activity in the residential property market in Sofia. Development surged triggered by overall economic upturn, increasing purchasing power and availability of financing. Generally, the first years of the period were defined by development in middle and middle-up residential areas situated mostly along or in proximity to the southern arc of the ring road and near Vitosha Mountain. The continuous positive economic growth triggered demand in the lower market segment as well, which lead to subsequent increase in construction in the rest of the capital. 2008 marked the ending of the vigorous and rather hectic growth of the residential property market and the beginning of a period with a somewhat different pace of development. The financial distress evident on an international level begun to influence the property market in Bulgaria and the development of some projects was put on hold due to lack of financing. Demand also diminished predominantly on account of the unfavorable terms on mortgage lending. Throughout 2009 and 2010, the changing market conditions triggered substantial price decrease and the introduction of diverse payment schemes aiming to facilitated transactions in view of the shrinking demand. 2011, on the other hand, saw stabilization of prices and positive signals from buyers, however, mostly in the middle and middle-up market segments, as well as purchases not dependent on bank financing. At the same time multiple low-quality constructions and stand-alone buildings remain vacant, which puts downward pressure on asking prices. This trend has throughput the first half of 2012. CHOICE OF LOCATION The location of new developments was determined by several main criteria:

Land availability Proximity to public and social infrastructure Proximity to green areas (Vitosha Mountain and/or larger parks) Proximity to diverse amenities Increasing demand based on exogenous factors (e.g. new office developments)

As a general trend, during the last decade the residential market in Sofia went through a transition from supply-dominated to demand-dominated market. This, along with the drastic change in the macroeconomic conditions in Bulgaria and globally, is expected to drive a much more healthy development of the market with only quality projects of reputable developers being constructed and marketed as opposed to the chaotic boom leading the growth of the market until 2007.

Valuation of a Mixed-use Property in Geo Milev Area, Sofia, Bulgaria

B.S.R. Sofia AD Page 39 of 74

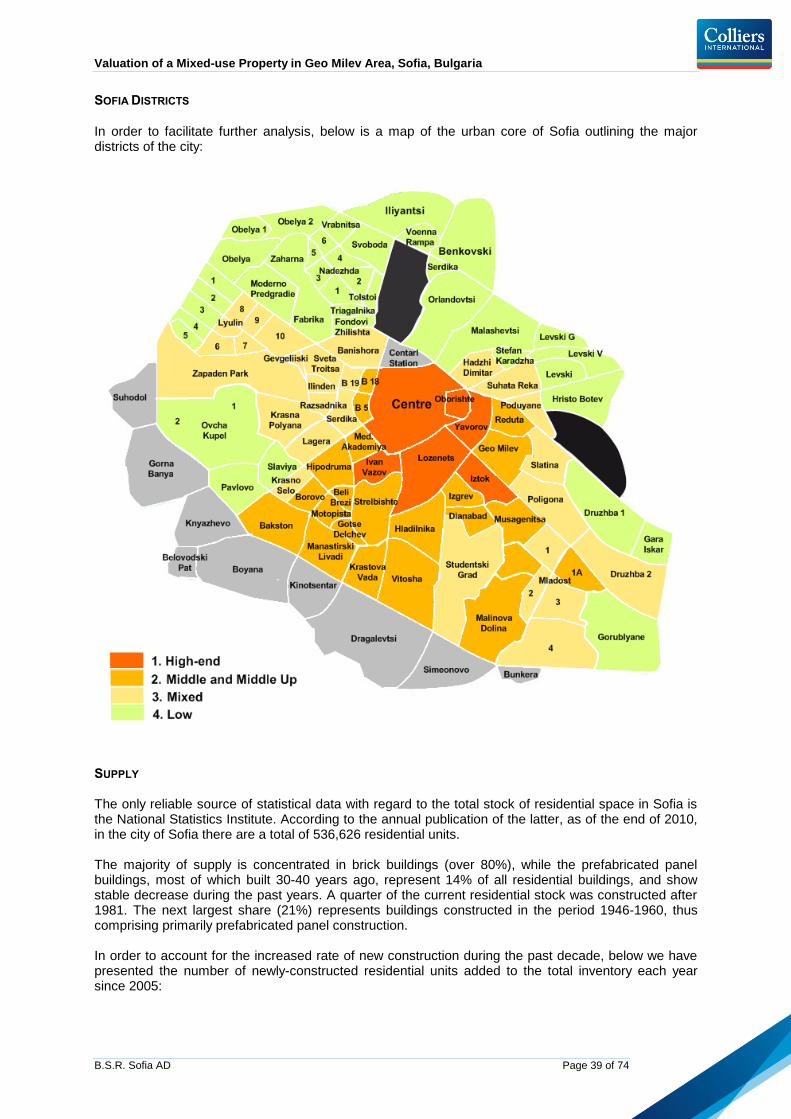

SOFIA DISTRICTS

In order to facilitate further analysis, below is a map of the urban core of Sofia outlining the major districts of the city: