28

From melting steel to 3D-printing: investing in the technology-driven German “Mittelstand” as at 22 March 2017

From melting steel to 3D-printing: investing in the technology-driven German “Mittelstand”

as at 22 March 2017

Long-terminvestments

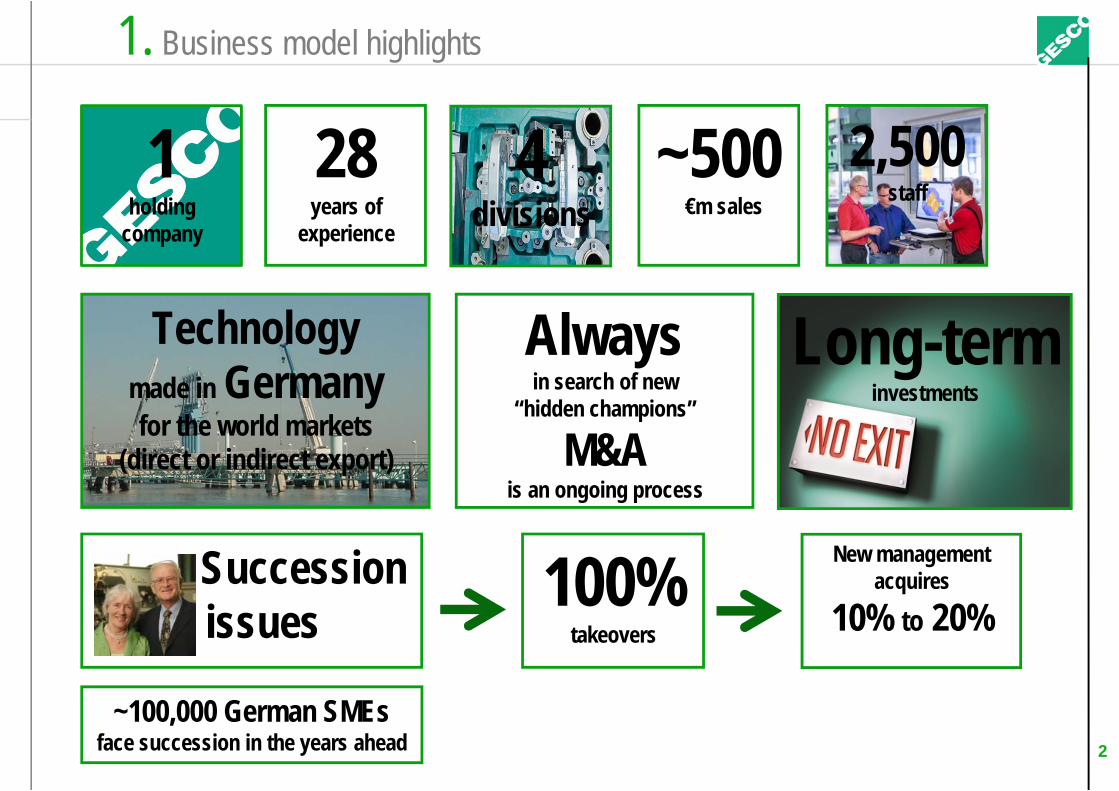

1holding

company

1. Business model highlights

2

~500€m sales

2,500staff

28years of

experience

Technologymade in Germanyfor the world markets

(direct or indirect export)

Alwaysin search of new

“hidden champions”

M&Ais an ongoing process

Succession issues

100% takeovers

New management acquires

10% to 20%

~100,000 German SMEsface succession in the years ahead

4divisions

GESCO – a Group in acceleration

Active portfolio management: one loss-maker to be sold, one “Hidden Champion” acquired Divestment: restructuring case Protomaster put for sale Acquisition: Pickhardt & Gerlach joins GESCO Group Portfolio becomes stronger and more robust

Active ownership: new impetus for profitable growth A new portfolio strategy

4 segments higher transparency, new framework for acquisitions Systematic benchmarking Optimisation projects for individual subsidiaries

A more active role of GESCO AG in terms of consulting and support for its companies

A stronger focus on free cash flow (working capital, investments)

Active M&A approach: access to entrepreneurs Continuously attractive deal flow via M&A network New portfolio strategy widens horizon for attractive targets In addition: proactive direct contact with business owners

3

1. Business model

GESCO – current situation and outlook

From an operating point of view, 2016/2017 turns out to be betterthan expected in Nov. 2016

Exit of loss-maker burdens 2016/2017 accounts, but reduces future risks

Newly aquired PGW will provide external growth All in all, our portfolio has been strengthened

New financial year 2017/2018 should generategrowth in sales and earnings on an organic basis

Optimisation projects have been identified in FY 2016/2017, will be implemented in FY 2017/2018 and generate impact in FY 2018/2019

We expect to start into the new FY with a strengthened, more robust portfolio and good perspectivesfor profitable organic as well as external growth

4

1. Business model

1. Business model

Our industryB-to-B and investment goods. From melting steel to 3D printing.

Our mission Being successful by supporting our customers’ success

with products and services made in Germany.

Our divisionsRepresenting strategically attractive end customer markets:

5

Production process technology

Resource technology

Health and infrastructure

technology

Mobility technology

Production processtechnology

(Share of Group salesapprox. 15 %)

Features: Dynamically growing markets, high degree of innovation, automation, trend towards “batch size 1”

Products / services:

Robotics and automation solutions in machine and plant construction, technology-intensivemanufacturing services

End customers:

Serial producers, e.g. in automotive, steel and consumer goods industries

Products/services(examples):

6

1. Business model: our divisions

3D printing(semi)automatic assembly lines

straighteningmachines

ResourceTechnology

(Share of Group salesapprox. 45 %)

Features: Consolidating markets, focus on niches and customer service

Products / services:

Customised preparation of primary materials, e.g. materials supply, transport and loading technology

End customers:

Material-intensive industrial companies, globally distributed production structures, broadly diversified

Products/services(examples):

7

1. Business model: our divisions

coating andhardening

high-alloyed tool steel

loading arms forgases and liquids

Health andinfrastructure

technology

(Share of Group salesapprox. 25 %)

Features: Close to end consumers, not very cyclical, relatively resilient to economic fluctuation

Products / services:

Components, modules and primary products

End customers:

Providers for mass markets close to end consumers(construction, sanitary equipment, food, hygiene, medicine)

Products/services(examples):

8

1. Business model: our divisions

paper sticks forhygiene and

sweets industry

arms for medtech spareparts for agri-cultural technology

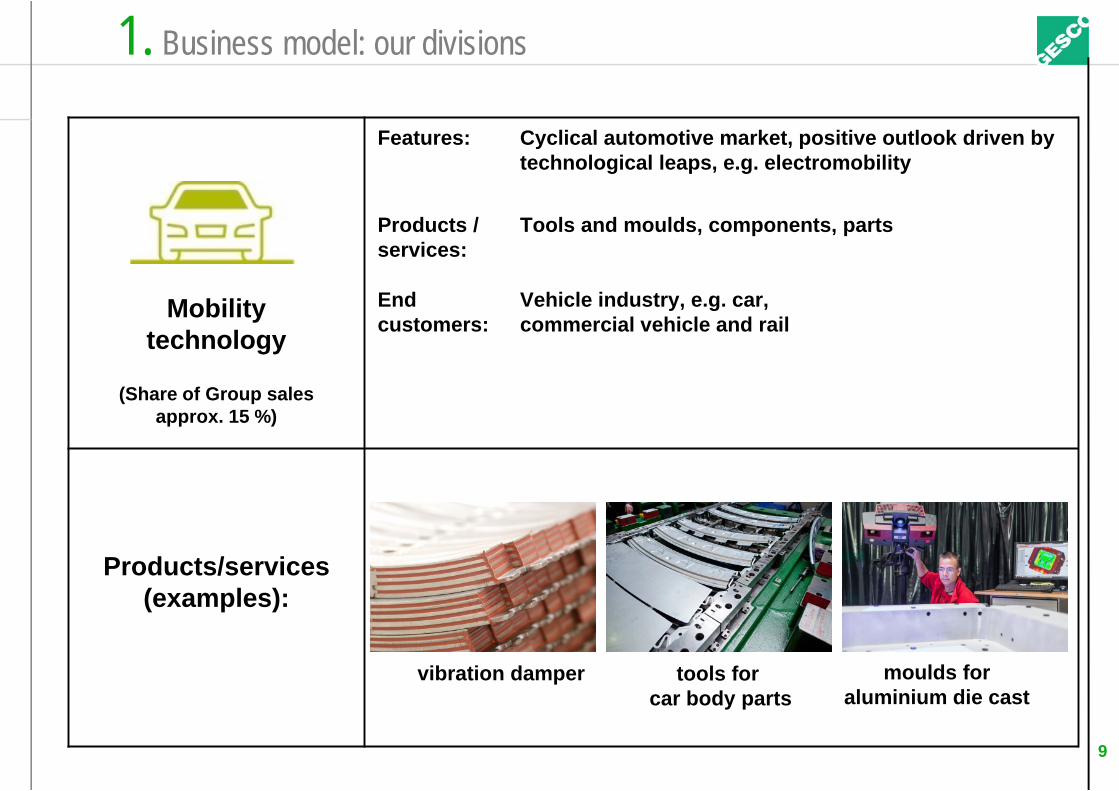

Mobility technology

(Share of Group salesapprox. 15 %)

Features: Cyclical automotive market, positive outlook driven by technological leaps, e.g. electromobility

Products / services:

Tools and moulds, components, parts

End customers:

Vehicle industry, e.g. car, commercial vehicle and rail

Products/services(examples):

9

1. Business model: our divisions

tools forcar body parts

vibration damper moulds foraluminium die cast

Please note:

FY subsidiaries = calendar year

10

2. Financial year 2016/2017

1 January 31 December

31 March 1 April

FY GESCO AG / GESCO Group = 1 April to 31 March

2. Financial year 2016/2017 – Q1 to Q3 (Jan. to Sept. 2016 at subsidiaries)

Q1-Q32015/2016

Q1-Q32016/2017 Change

Order intake €m 378.1 376.4 -0.4 %

Group sales €m 369.2 357.5 -3.2 %

EBITDA €m 40.5 35.7 -11.8 %EBIT €m 25.3 19.9 -21.0 %Group net income after minority interest €m 13.0 9.7 -25.0 %

Earnings per share acc. to IFRS 1) € 1.30 0.98 -25.0 %

Cashflow from operating activities €m 16.6 30.7 85.8 %1) Based on new no. of shares after share split 1:3 on 22.12.2016

11

The first nine months: General environment for capital goods still dampened Q1/Q2: comparatively weak, additionally burdened because

customers postponed deliveries of major orders to H2 Q3: significantly better, large orders delivered,

improvement in sales and margins Q1 to Q3: order intake stable, sales and earnings below prev. year’s figures Cash flow significantly improved

2. Financial year 2016/2017 – Division development Q1-Q3

12

€m Q1-Q32015/2016

Q1-Q32016/2017

Remarks

Production Process Technology

SalesEBIT

51.21.8

45.21.4

Numerous machines will be delivered in Q4. Full FY expectation: sales slightly under, earnings clearly above previous FY.

Resource Technology

SalesEBIT

165.814.9

166.413.7

Oil and chemical industry still reluctant to invest. Margin improvement in Q4. Full FY expectation: sales and earningsslightly above previous FY.

Healthcare /Infrastructure Technology

SalesEBIT

87.68.1

87.88.7

Very robust; profitable growth. Full FY expectation: sales slightly, earnings clearly above previous FY.

Mobility Technology 1)

SalesEBIT

64.97.6

59.73.5

Parts for series production and large tools develop lively, other sections suffer from car manufacturers’ reluctance to invest. Full FY expectation: sales and earnings clearly under previous FY.

1) Division includes restructuring caseProtomaster GmbH, which is put for sale.

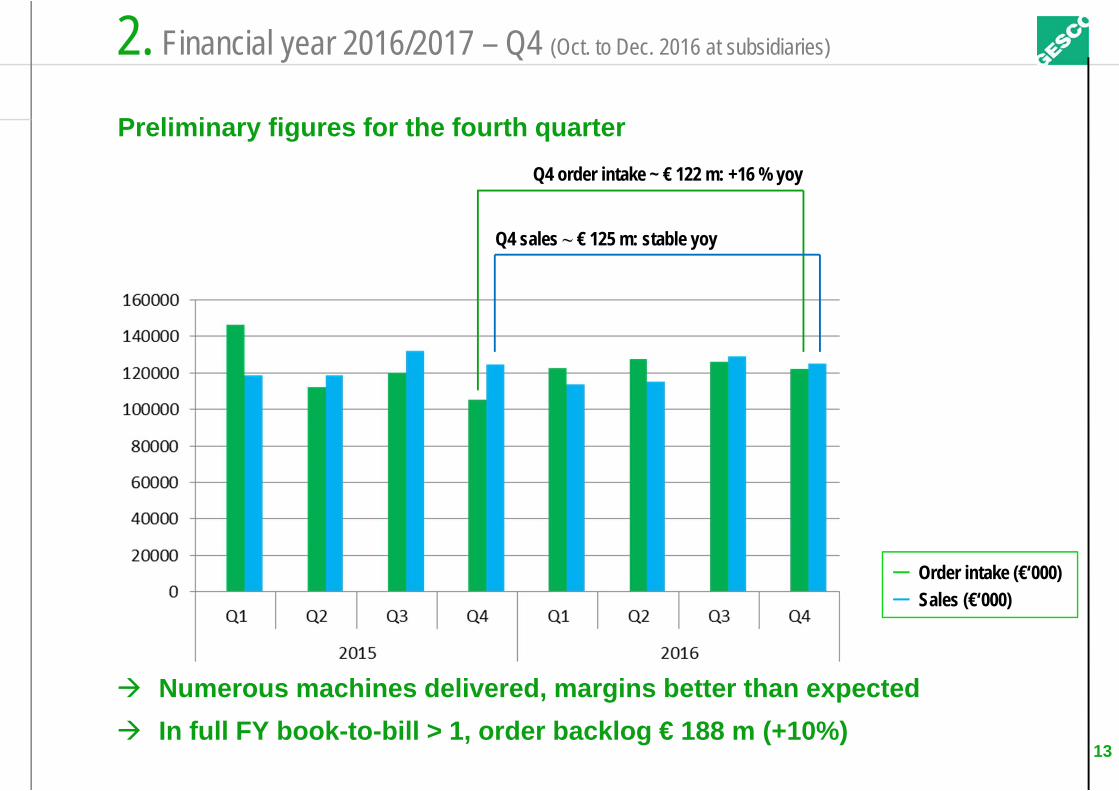

2. Financial year 2016/2017 – Q4 (Oct. to Dec. 2016 at subsidiaries)

Preliminary figures for the fourth quarter

13

Q4 order intake ~ € 122 m: +16 % yoy

─ Order intake (€‘000)─ Sales (€‘000)

Numerous machines delivered, margins better than expected In full FY book-to-bill > 1, order backlog € 188 m (+10%)

Q4 sales ~ € 125 m: stable yoy

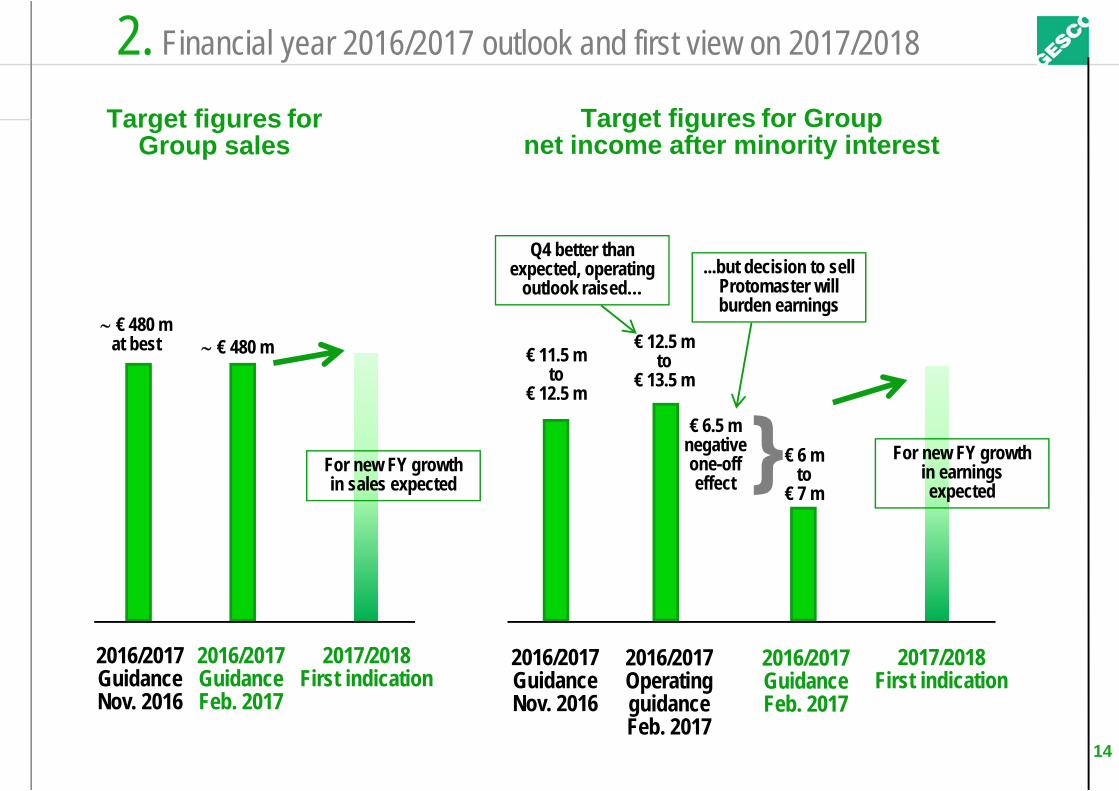

2. Financial year 2016/2017 outlook and first view on 2017/2018

Target figures for Group net income after minority interest

14

2016/2017GuidanceNov. 2016

€ 11.5 m to

€ 12.5 m

2016/2017GuidanceFeb. 2017

€ 12.5 m to

€ 13.5 m

€ 6 m to

€ 7 m}€ 6.5 m

negativeone-off effect

Q4 better than expected, operating

outlook raised…

2016/2017OperatingguidanceFeb. 2017

...but decision to sell Protomaster will burden earnings

Target figures for Group sales

2016/2017GuidanceNov. 2016

€ 480 mat best

2016/2017GuidanceFeb. 2017

€ 480 m

2017/2018First indication

2017/2018First indication

For new FY growth in sales expected

For new FY growth in earnings expected

More active approach towards M&A

Market still characterized by strong demand and a limited number of companies offered

Focus on 4 end customer segments

GESCO continuously generates high deal flow

GESCO has intensified its activities, aims to generate direct contact with entrepreneurs / business owners, which has already led to a number of personal meetings

15

3. M&A and Portfolio Development

Recent acquisition: Pickhardt & Gerlach Group (PGW)

Leading supplier of refined cold rolled strip steel Products: nickel-, copper-, brass- or zinc-coated strip steel Customer sectors: electro-technic industry, automotive,

decorative articles, sporting equipment, office supply Product examples: electronic circuit breakers,

file folders, windscreen wipers… Highly automated production systems

16

3. M&A and Portfolio Development

Recent acquisition: Pickhardt & Gerlach Group (PGW)

Family business, founded 1902, taken over by Hekhorn family in 1990 GESCO acquired 100% of the shares from Hekhorn family as part of a

succession planning process Signing Dec. 2016, approval of antitrust authorities in Jan. 2017 Managing Director of technology will continue to work for PGW Will be integrated in the Resource Technology division Approx. € 30 million sales, 40 employees

17

3. M&A and Portfolio Development

Decision to sell Protomaster GmbH

Communicated as a restructuring case since FY 2014/2015 Generated operating losses in FYs 2014, 2015 and 2016 GESCO supported Protomaster strongly over the last years On 2 Feb. 2017 decision to put Protomaster for sale Sales process started immediately Exit decision expected to burden Group net income after

minority interest in FY 2016/2017 with a one-off effect of ~ € 6.5 m Risks from that investment will be taken into account as far as recognisable

GESCO overall strategy unchanged: exit is and will continue to be „last resort “ and certainly an exception

18

3. M&A and Portfolio Development

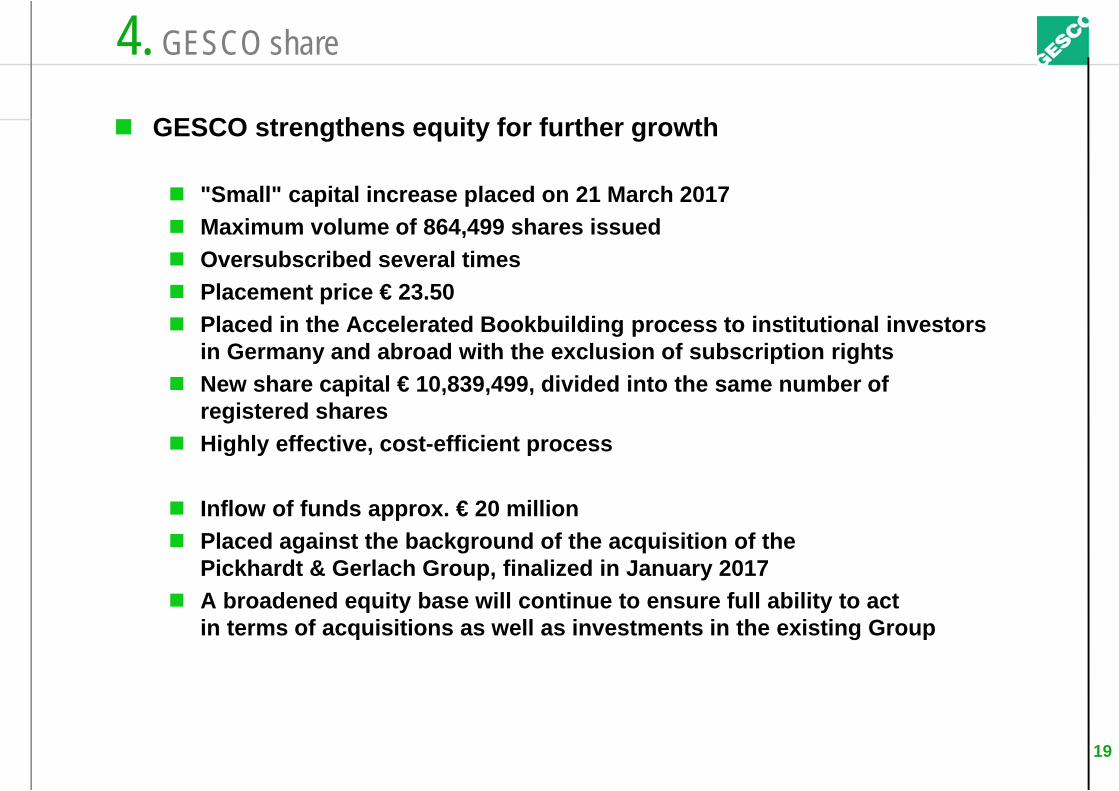

GESCO strengthens equity for further growth

"Small" capital increase placed on 21 March 2017 Maximum volume of 864,499 shares issued Oversubscribed several times Placement price € 23.50 Placed in the Accelerated Bookbuilding process to institutional investors

in Germany and abroad with the exclusion of subscription rights New share capital € 10,839,499, divided into the same number of

registered shares Highly effective, cost-efficient process

Inflow of funds approx. € 20 million Placed against the background of the acquisition of the

Pickhardt & Gerlach Group, finalized in January 2017 A broadened equity base will continue to ensure full ability to act

in terms of acquisitions as well as investments in the existing Group

19

4. GESCO share

4. GESCO share vs. SDAX and DAX 1 Year in % (total shareholder return)

20

Pleas note: Share split 1:3 was

implemented on 22 Dec. 2016

4. GESCO share vs. SDAX and DAX 10 Years in % (total shareholder return)

21

Pleas note: Share split 1:3 was

implemented on 22 Dec. 2016

4. The GESCO share – shareholder structure

22

Free float: 86.3%

13.7 % Stefan Heimöller (entrepreneur, member of supervisory board,private investor)

12.8 % Investmentaktiengesellschaft für langfristige Investoren TGV (institutional investor)

approx. 36.0 % other private investors

approx. 37.5 % otherinstitutional investors

Directors‘ Dealings: In current FY purchases by members of supervisory and executive board.

Appendix – GESCO management

23

Robert Spartmann* 1960

Board member since 2001. Financials, legal, HR,

M&A, advising holdings. Tax advisor and auditor.

Many years of experience in SME sector. From 1995 to 2000 external advisor

for GESCO Group.

Dr Eric Bernhard * 1972

Board member since Jan. 2016, CEO since July 2016. Portfolio strategy. Strategic

and operational development of subsidiaries. Investor Relations. Many years of

management experience in consulting and various

industries.

Executive Board

Appendix – GESCO management

Supervisory Board

24

Klaus MöllerfriedrichChairman

* 1947 Co-founder of GESCO.

Board member since 1989. Tax advisor, auditor,

consultant.

Stefan HeimöllerDeputy Chairman

* 1963Board member since 2013.

Business owner / entrepreneur.

Dr Nanna Rapp

* 1969 Board member since 2015.

MD of E.ON InhouseConsulting GmbH.

Appendix – GESCO Group overviewCompany Sales 2015

€‘000Staff as at31/12/2015

GESCO AGshareholding

AstroPlast Kunststofftechnik GmbH & Co. KG 16,262 92 100%

Paul Beier GmbH Werkzeug- und Maschinenbau & Co. KG 12,117 117 100%

C.F.K. CNC-Fertigungstechnik Kriftel GmbH 9,708 66 80%

Dömer GmbH & Co. KG Stanz- und Umformtechnologie 15,661 104 100%

Dörrenberg Edelstahl GmbH 179,243 509 90%

Frank Group 27,629 258 90%

Franz Funke Zerspanungstechnik GmbH & Co. KG 15,383 80 80%

Haseke GmbH & Co. KG 12,969 64 80%

Hubl GmbH 12,775 106 80%

Georg Kesel GmbH und Co. KG 11,239 60 90%

MAE Group 44,359 222 100%

Modell Technik Formenbau GmbH 13,961 115 100%

Pickhardt & Gerlach GmbH & Co. KG (Acquired in Dec. 2016) approx. 30,000 approx. 40 100%

Protomaster GmbH 17,688 123 82.17%

Setter Group 26,984 98 100%

SVT GmbH 33,464 186 90%

VWH GmbH 11,421 109 80%

Werkzeugbau Laichingen Group 26,594 177 100%

25

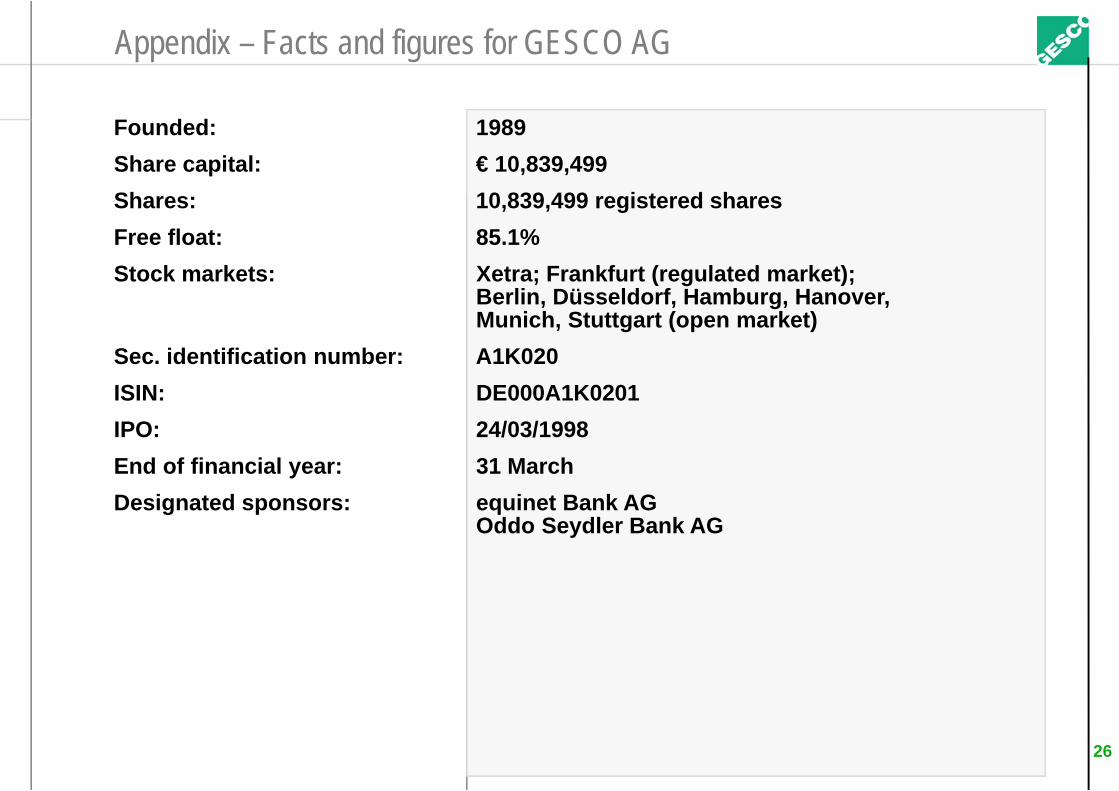

Founded: 1989Share capital: € 10,839,499Shares: 10,839,499 registered sharesFree float: 85.1%Stock markets: Xetra; Frankfurt (regulated market);

Berlin, Düsseldorf, Hamburg, Hanover, Munich, Stuttgart (open market)

Sec. identification number: A1K020ISIN: DE000A1K0201IPO: 24/03/1998 End of financial year: 31 MarchDesignated sponsors: equinet Bank AG

Oddo Seydler Bank AG

Appendix – Facts and figures for GESCO AG

26

Appendix – Financial calendar

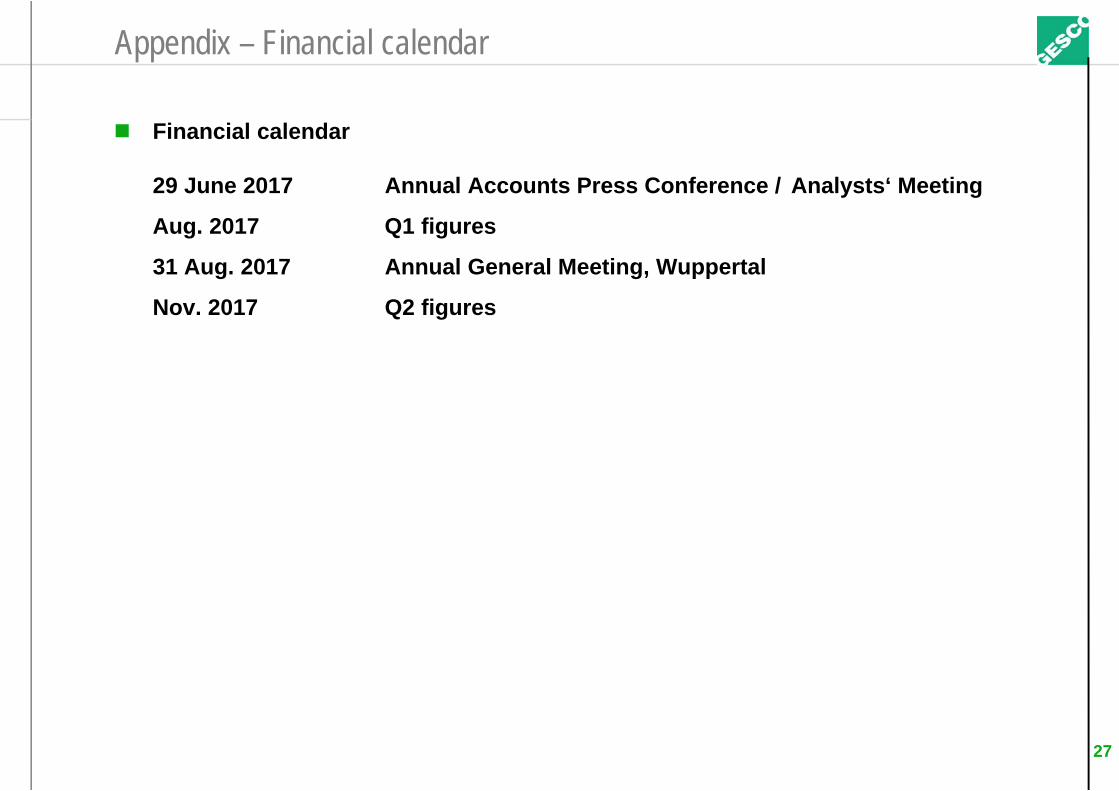

Financial calendar

29 June 2017 Annual Accounts Press Conference / Analysts‘ Meeting

Aug. 2017 Q1 figures

31 Aug. 2017 Annual General Meeting, Wuppertal

Nov. 2017 Q2 figures

27

Appendix – Investor relations contact

Investor RelationsGESCO AG Phone: +49 202 24820-18 Investor Relations Fax: +49 202 24820-49Oliver Vollbrecht Email: [email protected] 7 Internet: www.gesco.de 42103 WuppertalGermany

28

Anything else you’d like to know?

Contact: Oliver Vollbrecht, Head of IR

Phone: +49 202 2482018

Email: [email protected]

![Máster en DIRECCIÓN DE MARKETING Y GESTIÓN COMERCIAL … · 2019-08-23 · MÁSTER EN DIRECCIÓN DE MARKETING Y GESTIÓN COMERCIAL [GESCO] Los asistentes al programa GESCO, en](https://static.documents.pub/doc/80x56/5e832d23ead1ba17f376e61e/mster-en-direccin-de-marketing-y-gestin-comercial-2019-08-23-mster-en.jpg)