50

© 2015 IHS Global Outlook ihs.com IHS The Global Economic Outlook: The “Great Divergence” Nariman Behravesh, Chief Economist, +1 781 301 9101, [email protected] March 2015 ECONOMICS

© 2015 IHS

Global Outlook

ihs.com

IHS

The Global Economic Outlook:

The “Great Divergence”

Nariman Behravesh, Chief Economist, +1 781 301 9101, [email protected]

March 2015

ECONOMICS

© 2015 IHS

The “Great Divergence” and “Back to the Future”

• US growth is accelerating even as growth in other parts of

the world remains weak or decelerates further.

• US consumers are back to being the engines of global

growth.

• US oil production is higher than Saudi Arabia’s.

• The plunge in oil prices is creating winners and losers.

• The world’s central banks are moving in different directions.

• The dollar is rising, while most other currencies are falling.

• Back to the Future: This is very reminiscent of the 1980s

and 1990s.

Global Outlook/ March 2015

© 2015 IHS

Global Overview

• The momentum of the global economy will improve in 2015.

• Global growth accelerated marginally from 2.5% in 2012 to 2.7% in

2014 …

• … Most of that was thanks to the developed economies.

• Better prospects in 2015 will be the result of solid and improving growth

in the US and a slight pickup in the pace of Eurozone and Japanese

economic activity.

• The plunge in oil prices will add 0.4 to 0.6 percentage point to global

growth over the coming year.

• More stimulus by the Bank of Japan, People’s Bank of China and the

European Central bank will also support growth.

• China’s growth will slow further.

• For other large emerging markets, it will be a good news (India), bad

news (Brazil and Russia) story.

Global Outlook/ March 2015

© 2015 IHS

-4

-2

0

2

4

6

8

10

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

Perc

en

t ch

an

ge

World Advanced countries Emerging markets

Global Outlook/ March 2015

The emerging markets growth premium is the

lowest since the early 2000s

Real GDP

© 2015 IHS

-6

-4

-2

0

2

4

6

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Perc

en

t ch

an

ge

United States Eurozone Japan

Global Outlook/ March 2015

Real GDP growth in the United States,

Eurozone and Japan

Real GDP

© 2015 IHS

-12

-8

-4

0

4

8

12

16

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Perc

en

t ch

an

ge

Real exports Real GDP

Global Outlook/ March 2015

Growth in world trade volume is gradually picking up

Real GDP and trade

© 2015 IHS

15

20

25

30

35

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Perc

en

t o

f w

orl

d G

DP

Global Outlook/ March 2015

After exceptional gains in 1994-2008, the pace of

globalization has slowed

World imports’ share of GDP

© 2015 IHS

Oil and other commodity prices have tumbled in

response to structural excess supply

• Rising production and weak demand growth have left the global oil

market oversupplied, driving down prices.

• In keeping its output target of 30 million barrels per day, OPEC is letting

markets decide the clearing price for oil.

• Since demand is price-inelastic in the short run, market equilibration will

occur mainly through supply adjustments.

• A mismatch between fundamentals and financial market expectations

caused a price rally in February.

• Price volatility will likely remain high.

• As oil production growth slows in the second half of 2015, prices will

begin to recover.

• Other commodity prices have fallen mostly because of weak demand

from and excess capacity in China.

Global Outlook/ March 2015

© 2015 IHS

Global Outlook/ March 2015

Global crude oil price dynamics

Downside

risks

• Sluggish demand growth, especially

from China

• Increasing North American production

• Rising production in Iraq and Libya

• Fight for market share by producers

• Potential rise in Iranian oil exports

Upside

risks

• Accelerating global demand, partly in

response to lower prices

• Heightened geopolitical tensions and

potential supply disruptions (Iraq, Libya,

Nigeria, Venezuela and elsewhere)

• Rising development costs

© 2015 IHS

Global Outlook/ March 2015

US crude oil prices: A big drop – but for how long?

Crude oil and natural gas prices

0

2

4

6

8

10

12

14

0

20

40

60

80

100

120

140

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Do

lla

rs/m

illi

on

Btu

Do

lla

rs/b

arr

el

Crude oil, WTI (Left scale) Natural gas, Henry Hub (Right scale)

Source: IHS Energy

© 2015 IHS

Winners and losers from low oil prices

• Winners:

• US consumers are the biggest winners

• European consumers benefit proportionally less because of high gasoline taxes

• Emerging-market consumers will also benefit less because of large fuel subsidies

• Energy-intensive industries, such as agriculture and transportation

• Governments in oil-importing countries with large fuel subsidies

• Losers:

• Oil producers, especially those with high costs

• Major oil exporters, especially those at a ―fiscal break-even point‖ above US$100 per

barrel such as Iran, Russia, Venezuela, Ecuador and Angola

• Net effect:

• In the United States and worldwide, the net effect on consumers and producers is

positive, boosting real GDP growth by roughly 0.5 percentage point in 2015.

• A US$60 drop in oil prices represents a transfer of about US$2 trillion from oil

exporters to oil importers — the latter have a higher marginal propensity to spend

than the former.

Global Outlook/ March 2015

© 2015 IHS

Global Outlook/ March 2015

Industrial materials prices are also falling

Industrial materials prices

0

1

2

3

4

5

6

2002 2004 2006 2008 2010 2012 2014

IHS

weekly

in

dexes,

2002:1

=1

All industrial materials Chemicals Nonferrous metals

© 2015 IHS

US growth will be solid, in the 2.5 to 3.0% range

• The US is doing better than most because the principal driver of growth is

domestic demand.

• Prospects for consumer spending (roughly 70% of GDP) look bright, thanks to

strong jobs growth, improved household finances and lower gasoline prices.

• Arguably, US consumers are the biggest beneficiaries of the ―Great

Divergence.‖

• Even though income distribution and poor wage growth are issues, consumers

are in a good mood.

• Capital spending will also contribute to growth, despite the expected drop in

energy investment because of weak oil prices.

• Net exports will be a potential drag, because of feeble growth overseas and a

strengthening dollar.

• Ironically, weakness in other parts of the world benefits the US by lowering oil

prices and keeping interest rates low.

Global Outlook/ March 2015

© 2015 IHS

Global Outlook/ March 2015

US real GDP growth and the unemployment rate

Real GDP and unemployment

4.0

5.2

6.4

7.6

8.8

10.0

-9

-6

-3

0

3

6

2006 2008 2010 2012 2014 2016

Perc

en

t

An

nu

al

perc

en

t ch

an

ge

Real GDP growth (Left scale) Unemployment rate (Right scale)

© 2015 IHS

Looking forward, US consumer spending will

continue to drive the bulk of economic growth

2.3 2.2 2.4

3.0 2.7 2.8

-1

0

1

2

3

4

2012 2013 2014 2015 2016 2017

Real GDP Consumer spending Fixed investment Housing

Inventories Exports Imports Government

An

nu

ali

zed

perc

en

tag

e c

han

ge

Global Outlook/ March 2015

Contribution to real GDP growth

© 2015 IHS

The drop in gasoline prices means substantial near-term

savings for US households

16

Retail gasoline price and annualized spending on motor fuels

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Th

ou

san

d d

ollars

/ho

useh

old

Do

llars

/gallo

n

Retail gasoline price Spending on motor fuels per household (Right scale)

Global Outlook/ March 2015

© 2015 IHS

Rising US household net worth encourages

consumption and discourages saving

Household saving rate and net worth

4.5

5.0

5.5

6.0

6.5

7.0

0

3

6

9

12

15

1980 1985 1990 1995 2000 2005 2010 2015 2020

Ra

tio

Pe

rce

nt

of

dis

po

sa

ble

in

co

me

Saving rate (Left scale) Household net worth/disposable income (Right scale)

Global Outlook/ March 2015

© 2015 IHS

US business fixed investment growth is led by

equipment

Real business fixed investment

-30

-20

-10

0

10

20

30

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Year-

over-

year

perc

en

t ch

an

ge

Equipment Structures Intellectual products

Global Outlook/ March 2015

© 2015 IHS

0

2

4

6

8

10

12

14

16

18

Info Equip/ GDP IP+SW/GDP * Other Equip/GDP Structures / GDP

In real terms, the share of US capex in knowledge will

accelerate, but not in nominal terms.

0

2

4

6

8

10

12

14

16

18

Real spending (% of GDP) Nominal spending (% of GDP)

* = Intellectual Property + Software

Global Outlook/ March 2015

© 2015 IHS

Contributions from unconventional energy sources will

continue to add to US GDP

Global Outlook/ March 2015

0

50

100

150

200

250

300

350

1996 2001 2006 2011 2016 20210

20

40

60

80

100

120

140

160

180

1996 2001 2006 2011 2016 2021

US imports of petroleum products

(billions of 2009 dollars)

US mining and petroleum structures

(billions of 2009 dollars)

© 2015 IHS

Is the US labor market getting tight enough to

drive wage pressures?

3

4

5

6

7

8

9

10

11

-200

-100

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015

Un

em

plo

ym

en

t ra

te (

%)

Nu

mb

er

of

new

jo

bs (

000

s)

Employment growth Unemployment rate

Global Outlook/ March 2015

Job creation and the unemployment rate

© 2015 IHS

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2011 2012 2013 2014 2015 2016 2017 2018

Pe

rce

nt

ch

an

ge

., y

/y

All goods and services Excluding food and energy

Here’s what the Fed is watching to identify inflation

Global Outlook/ March 2015

Personal consumption price deflators

This doesn’t count

as deflation

Fed 2% threshold

© 2015 IHS

The European recovery will pick up some steam, and UK

growth will remain robust

• The good news is that the Eurozone was able to eke out positive (albeit

low) growth in 2014, after two years of recession.

• Growth will be better in 2015 thanks to lower oil prices, a weak euro,

reduced fiscal headwinds and accommodative monetary policy.

• Low inflation and (very) gradually improving labor market conditions will

support consumer spending. This is especially true for Germany and

Northern European economies.

• Stronger export growth (thanks to a weaker euro) and growing pent-up

demand boost capital spending.

• As a result, there will likely be an acceleration of Eurozone growth in

2015 to 1.5% (from 0.8% in 2014).

• Meanwhile (much like the US), UK growth will be solid (2.5 to 3.0%).

Global Outlook/ March 2015

© 2015 IHS

-6

-4

-2

0

2

4

6

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

Perc

en

t ch

an

ge

Global Outlook/ March 2015

The Eurozone economy will slowly recover

Real GDP

© 2015 IHS

Global Outlook/ March 2015

Real GDP growth in Europe’s major economies

-6

-4

-2

0

2

4

6

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Perc

en

t ch

an

ge

Germany UK France Italy Spain

Real GDP

© 2015 IHS

2

4

6

8

10

12

14

2005 2007 2009 2011 2013 2015 2017

Perc

en

t o

f la

bo

r fo

rce

France Germany Italy United Kingdom

Global Outlook/ March 2015

European unemployment rates have diverged

Unemployment rate

© 2015 IHS

Japan’s economy will regain weak growth momentum

• In 2014 Japan suffered through its fourth recession in six years.

• The latest downturn can be blamed on the April sales tax hike, which

hurt consumer spending and investment more than expected.

• This has been especially tough for Japanese households, whose

inflation-adjusted wages have fallen about 5% over the past year.

• In response to worsening economic picture, the government of Shinzo

Abe has postponed the next sales tax hike from October 2015 to April

2017; it will likely also provide some temporary stimulus in 2015.

• The Bank of Japan has also embarked on a new round of aggressive

quantitative easing.

• These growth-supportive policies helped growth turn positive in the

fourth quarter of 2014, but for 2015 growth will only be around 1%.

Global Outlook/ March 2015

© 2015 IHS

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

1986 1990 1994 1998 2002 2006 2010 2014 2018

Perc

en

t ch

an

ge

Global Outlook/ March 2015

Japan’s economy has limited growth potential

Real GDP

© 2015 IHS

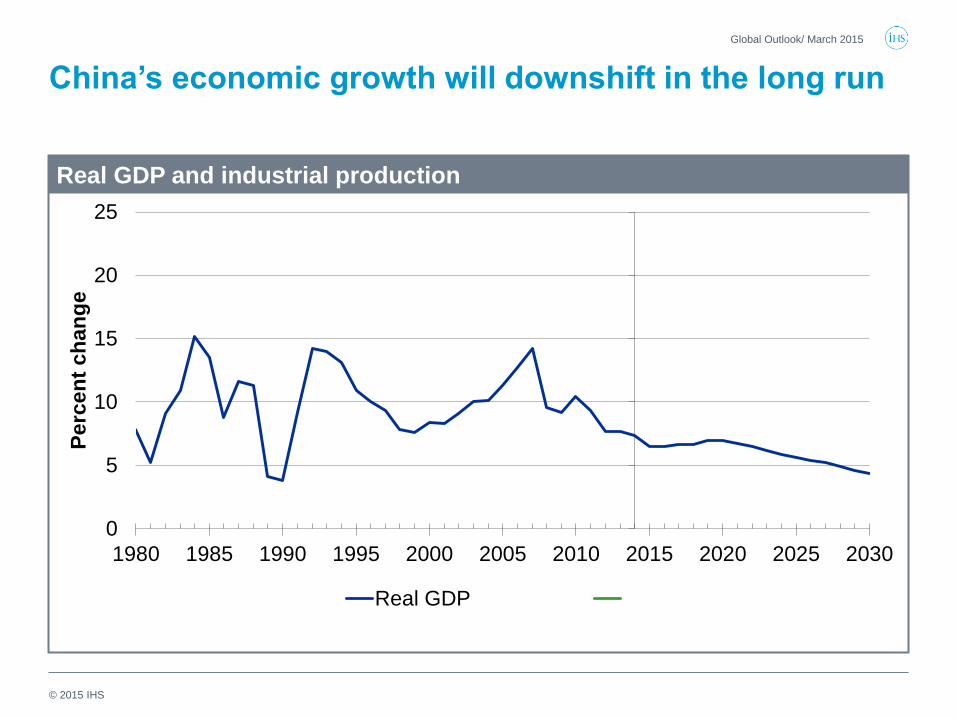

China’s growth rate will decelerate more

• The recent wobbles in the Chinese economy are due mostly to weak

domestic demand (because of the real estate bust).

• Government stimulus has been modest and temporary, resulting in

equally brief upticks in growth.

• The government is trying to balance concerns about weak jobs growth

and social unrest with its desire to tackle the glut of debt and industrial

overcapacity in the Chinese economy.

• In November, the People’s Bank of China cut interest rates for the first

time since 2012; it will likely cut rates again.

• Bottom line: limited support from fiscal and monetary policy will not be

enough to prevent growth from weakening further, from 7.4% in 2014 to

around 6.5% in 2015 through 2017.

• Will the vast (and growing) excess industrial capacity in China continue

to drag down prices in key commodity markets (e.g. steel and

chemicals)

Global Outlook/ March 2015

© 2015 IHS

0

5

10

15

20

25

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Perc

en

t ch

an

ge

Real GDP

Global Outlook/ March 2015

China’s economic growth will downshift in the long run

Real GDP and industrial production

© 2015 IHS

0

3

6

9

12

15

18

02 03 04 05 06 07 08 09 10 11 12 13 14*

Tri

llio

n C

NY

Bank loans (LCU and FX) Other financing Entrusted loans

Bank acceptance bills Trust loans

Global Outlook/ March 2015

China’s lending has stabilized at a high level

Source: People’s Bank of China

Lending flows

* IHS forecast

© 2015 IHS

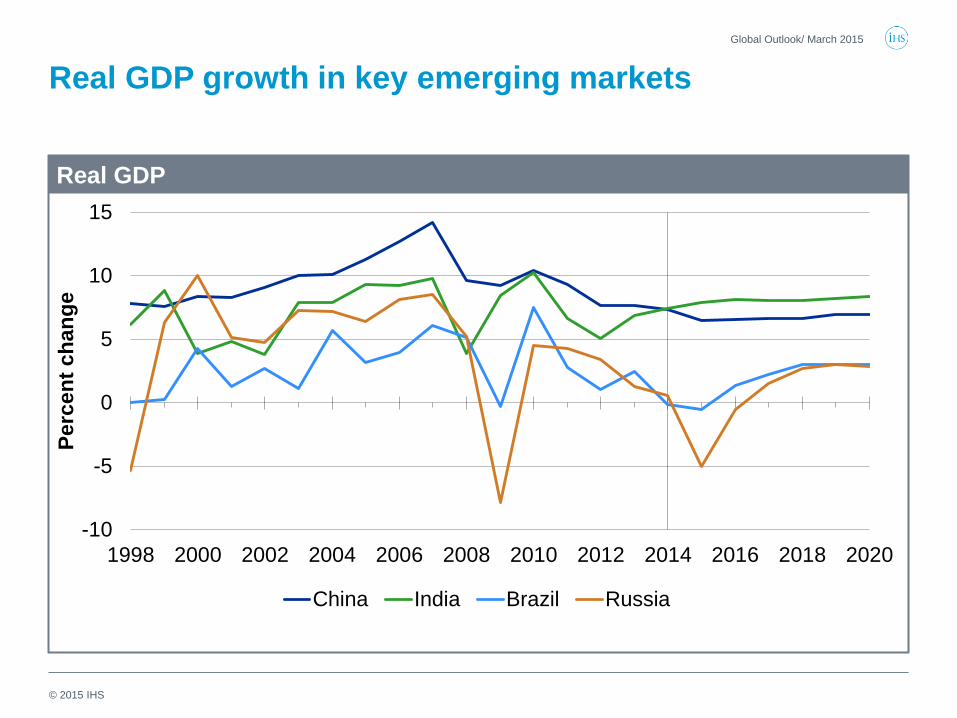

Other large emerging markets:

A good news-bad news story

• Brazil suffered a mild recession in 2014, and 2015 growth is likely to

decline again (by around -0.5%).

• Russia avoided recession in 2014 but will see its economy contract by

around 5% in 2015, because of the triple whammy of sanctions,

plunging oil prices and capital flight.

• Good news: many other emerging markets are likely to see better

growth in 2015 than in 2014, thanks to lower oil prices, a boost in global

liquidity and stronger growth in the US and Europe.

• India’s prospects look particularly promising, and growth could be

stronger than in China, for the next few years.

• Growth is likely to remain strong in Asia and Africa.

• Some countries will do especially well, including Indonesia, Malaysia,

the Philippines, Poland, Peru, Egypt, Kenya and Ethiopia.

Global Outlook/ March 2015

© 2015 IHS

Global Outlook/ March 2015

Why has growth in emerging markets slowed?

Cyclical forces

• Withdrawal of policy stimulus

• Excess capacity after investment booms

• Sluggish export markets

• Increased risk aversion

Structural forces

• Slower labor force growth

• Slower pace of globalization

• Falling commodity prices

• Lack of market reforms

© 2015 IHS

-10

-5

0

5

10

15

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Perc

en

t ch

an

ge

China India Brazil Russia

Global Outlook/ March 2015

Real GDP growth in key emerging markets

Real GDP

© 2015 IHS

-1

0

1

2

3

4

5

6

7

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Mideast-N. Africa

Sub-Saharan

Africa

Japan OtherAsia-

Pacific

An

nu

al

perc

en

t ch

an

ge

2013 2014 2015 2016 2017-21

Global Outlook/ March 2015

Asia-Pacific (excluding Japan) and Sub-Saharan Africa

will achieve the fastest growth in real GDP

Real GDP

© 2015 IHS

Inflation will remain a distant threat, while deflationary

worries persist

• With commodity prices low and falling, and global growth anemic, the

risk of inflation rising much above current levels is low.

• The exceptions are emerging markets where sharp drops in exchange

rates will lead to spikes in inflation (e.g. Russia).

• Disinflationary forces are the strongest in the developed world.

• Headline US inflation could briefly go negative, but core consumer

price inflation is likely to remain in the 1 to 2% range.

• Low oil prices will exacerbate deflationary pressures in the Eurozone –

headline CPI inflation was already down to -0.5% in January – but a

lower euro will exert in some upward pressure.

• Inflation in other parts of the world, already fairly low, will probably ease

further because of declining energy and food prices.

Global Outlook/ March 2015

© 2015 IHS

-3

-2

-1

0

1

2

3

4

5

6

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

% c

han

ge f

rom

a y

ear

earl

ier

United States United Kingdom Eurozone Japan

Global Outlook/ March 2015

Consumer price inflation is subsiding in the advanced

economies

Consumer price index

© 2015 IHS

-2

0

2

4

6

8

10

12

14

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Mideast-N. Africa

Sub-Saharan

Africa

Japan OtherAsia-

Pacific

An

nu

al

perc

en

t ch

an

ge

2013 2014 2015 2016 2017-21

Global Outlook/ March 2015

Consumer price inflation varies by region,

but is not a threat

Consumer price inflation

© 2015 IHS

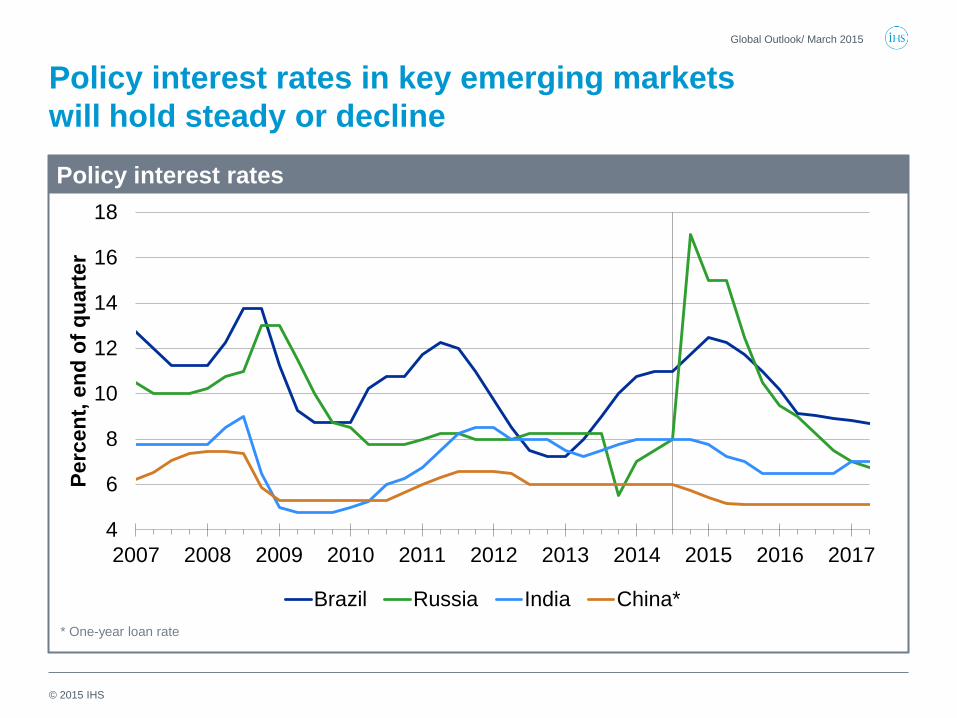

The Fed will likely start raising interest rates, while most

other central banks will be on hold or provide more

stimulus

• Divergent growth prospects mean central banks will go their separate

ways in 2015.

• The Fed is expected to raise rates this year – although weaker inflation

(because of falling oil prices) could delay rate hikes.

• In contrast, the European Central Bank, Bank of Japan and People’s

Bank of China will lower rates (if they can) and/or boost liquidity.

• So far the actions of the BoJ have been the most aggressive, while

those of the ECB and PBoC have been more limited – but more is in

the pipeline.

• In the emerging world, many central banks have already started to

lower rates, or will soon – even those that raised them recently (e.g.

Brazil and Russia).

Global Outlook/ March 2015

© 2015 IHS

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Perc

en

t, e

nd

of

qu

art

er

United States Eurozone Japan United Kingdom

Global Outlook/ March 2015

The Fed will likely lead the upturn

in policy interest rates

Policy interest rates

© 2015 IHS

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Perc

en

t, e

nd

of

qu

art

er

Brazil Russia India China*

Global Outlook/ March 2015

Policy interest rates in key emerging markets

will hold steady or decline

* One-year loan rate

Policy interest rates

© 2015 IHS

The US dollar will rise against most currencies, while

the euro and yen will fall

• With strong US growth and expectations that the Fed will raise rates

sooner than most, the dollar strengthened in 2014 and will rise further

in 2015.

• Weaker growth in the Eurozone and Japan, as well as expectations of

more stimulus from their central banks, means the euro and yen will fall

further from current levels.

• Much like the US dollar, the British pound will see some upward

pressure.

• Falling oil prices will exert downward pressure on the Canadian dollar.

• Emerging market currencies are likely to continue to slide against the

dollar – the currencies of oil-exporting countries will come under

intense downward pressure, as the Russian rouble already has.

Global Outlook/ March 2015

© 2015 IHS

Global Outlook/ March 2015

The dollar: rising, but still competitive

Real trade-weighted dollar index

0.6

0.8

1.0

1.2

1.4

1.6

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020

Ind

ex,

2009 =

1.0

Major trading partners Other important trading partners

© 2015 IHS

Global Outlook/ March 2015

Exchange rates per US dollar

Quarterly averages

Canadian dollar

Japanese yen

Euro

Chinese renminbi

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1998 2001 2004 2007 2010 2013 20160.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1998 2001 2004 2007 2010 2013 2016

4

5

6

7

8

9

1998 2001 2004 2007 2010 2013 2016

60

80

100

120

140

1998 2001 2004 2007 2010 2013 2016

© 2015 IHS

Global Outlook/ March 2015

Many emerging-market currencies have depreciated

and are vulnerable

40

50

60

70

80

90

100

110

Jan-13 May-13 Sep-13 Jan-14 May-14 Sep-14 Jan-15

US

D/lo

cal

cu

rren

cy,

2013:1

=10

0

China India Brazil Russia South Africa

Weekly exchange rate index

© 2015 IHS

-8 -6 -4 -2 0 2 4

China

Russia

Poland

Mexico

India

Indonesia

Brazil

Turkey

South Africa

Current-account balance Fiscal balance

Global Outlook/ March 2015

Vulnerable countries depend on external financing:

Current-account and fiscal balances

Percent of GDP, 2014

External financing

© 2015 IHS

Perennial downside risks will be balanced by some

upside risks

• In the past few years, the global economy has been plagued by a

number of ―curses.‖

• One of the worst has been the deleveraging necessary to reduce high

debt levels, which has resulted in feeble spending by households and

businesses, government austerity and banks’ unwillingness to lend.

• The good news is that this hindrance to growth is easing in many

countries, especially the UK and US.

• Moreover, while geopolitical risks remain high, the impact on oil

markets has – so far – been nonexistent, thanks to rising US oil

production.

• Other potential risks include a relapse in Europe and a hard landing in

China.

Global Outlook/ March 2015

© 2015 IHS

Global Outlook/ March 2015

Risks to the global economy

Risk Signposts

China hard landing • Loan defaults by developers and local governments trigger

a banking crisis and a credit squeeze.

• The property market downturn affects consumer spending.

• The government responds with only limited fiscal stimulus.

Eurozone setback

• Banking problems intensify, reducing credit availability.

• Growth stalls and deflation sets in.

• High unemployment leads to social unrest.

Energy supply shocks • Conflicts in the Middle East and Africa lead to disruptions

in oil production and transportation.

• Oil prices rebound.

• The Russia-Ukraine conflict cuts gas supplies to Europe.

US recovery stalls

• Businesses and households spend more cautiously.

• Recoveries in housing and automotive markets relapse.

© 2015 IHS

Summary

• Lower oil prices, monetary stimulus in Europe and Asia, and solid US

growth will provide the foundations for a pickup in the global economy.

• The US expansion is led by domestic demand, as consumer spending

and residential construction accelerate.

• The Eurozone will gradually recover; contagion from the ongoing Greek

situation will be limited.

• Emerging markets will not regain the peak growth rates of the 2000s.

• The Asia-Pacific region will make the strongest contribution to global

economic growth, although China’s locomotive role is diminishing.

• Risks abound: wars in the Middle East, the Russia-Ukraine conflict,

China’s rising debt and central bank ―exit strategies.‖

Global Outlook/ March 2015

IHS Customer Care:

• Americas: +1 800 IHS CARE (+1 800 447 2273); [email protected]

• Europe, Middle East, and Africa: +44 (0) 1344 328 300; [email protected]

• Asia and the Pacific Rim: +604 291 3600; [email protected]

© 2014 IHS. No portion of this report may be reproduced, reused, or otherwise distributed in any form without prior written consent, with the exception of any internal client distribution as may be permitted in the license agreement between client and IHS.

Content reproduced or redistributed with IHS permission must display IHS legal notices and attributions of authorship. The information contained herein is from sources considered reliable but its accuracy and completeness are not warranted, nor are the

opinions and analyses which are based upon it, and to the extent permitted by law, IHS shall not be liable for any errors or omissions or any loss, damage or expense incurred by reliance on information or any statement contained herein. For more

information, please contact IHS at Customer Care (see phone numbers and email addresses above). All products, company names or other marks appearing in this publication are the trademarks and property of IHS or their respective owners.