24

Globecomm Systems Inc. February 2013

Globecomm Systems Inc.

February 2013

Forward Looking StatementForward Looking Statement

22

This presentation contains forward-looking statements made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward looking statements are based on management's current expectations and observations. You should not place undue reliance on our forward-looking statements because the matters they describe are subject to certain risks, uncertainties and assumptions that are difficult to predict. Our forward-looking statements are based on the information currently available to us. Over time, our actual results, performance or achievements may differ from those expressed or implied by our forward-looking statements, and such differences might be significant and materially adverse to our security holders.

We have identified some of the important factors that could cause future events to differ from our current expectations and they are described in our most recent Annual Report on Form 10-K, including without limitation under the captions ''Risk Factors'' and ''Management's Discussion and Analysis of Financial Condition and Results of Operations,'' and in other documents that we may file with the SEC, all of which you should review carefully. Please consider our forward-looking statements in light of those risks as you read this presentation.

Communication Solution ProviderCommunication Solution Provider

33

We Design, Integrate, Install, and Manage Broadband Networks Anywhere.

Our Team: ~500 Employees. >100 Engineers creating custom, state of the art communication solutions.

Global Network: comprised of satellite, fiber and wireless nodes enabling secure broadband anywhere.

Corporate GrowthCorporate Growth

44

Fueled byAcquisitions

Company Evolution

Financial HighlightsFinancial Highlights

55

Evolving business model with “sticky”, recurring, higher margin revenue streams provides predictability, stability and visibility.

35 consecutive profitable quarters.

Strong operational cash flow - $78.3 million generated from fiscal 2010-2012.

Completed 5 strategic acquisitions valued at $75 million since April 2007.

$56 million in net cash at 12/31/12.

$72.5 million credit facility with CitiBank provides additional acquisition flexibility.

Global operation with minimal foreign currency exposure.

Remaining NOLs and credits cover most cash taxes (small amounts will be paid for AMT and foreign taxes) throughout fiscal 2013.

The Globecomm Cloud

66

.

Market Vertical Development

77

Technology Disruption Allow for New Market Entry

Diversity Across Market Verticals Leads to StabilityDiversity Across Market Verticals Leads to Stability

88

GovernmentNon DoD

42%

GovernmentDoD 18%

Wireless 13%

Media8%

Enterprise 9%

Maritime10%

Government Vertical SnapshotGovernment Vertical Snapshot

What Do You See?

We see the importance of providing the right tools to promote peace and security.

$0

$50

$100

$150

$200

$250

2011A 2012A 2013E

156

225 198

Wireless Vertical Snapshot

1010

Supporting > 12M min and > 1.5 TB

of data per month on our Hosted Platform Domestic and International Telcos

Tier 2 and 3 Telcos Rural telecommunication providers

Emerging cellular operators Indonesia, Indochina, Malaysia, Africa, Latin

America, and Middle East

What Do You See?

We see the opportunity to provide communication to those out of reach

$0$10$20$30$40$50$60$70

2011A 2012A 2013E

13.1 16.6 4.8

24.0

51.6

38.1

Infrastructure Services

Media & Entertainment Vertical SnapshotMedia & Entertainment Vertical Snapshot

Distributing over 100 channels and half a million hours of video content per year

Content Providers with Domestic and International Growth

Service Providers providing transport and media content

Online Media Providers

What Do You See?

We see the need to distribute more video content to an increasing number of users and devices

$0

$5

$10

$15

$20

$25

$30

2011A 2012A 2013E

12.5 12.7 19.5

11.1 11.4

6.9

Infrastructure Services

What Do You See?

We see the need to make sure the businesses stay connected and that the corporate message gets through, wherever users are.

Application Based Solutions:

Enterprise media platform for training, corporate, and digital display

Addresses migration from satellite to hybrid and terrestrial networks

Globecomm can design and operate a network that is both satellite and terrestrial

Gain access into Streaming Media Market

Enterprise Vertical SnapshotEnterprise Vertical Snapshot

$0

$5

$10

$15

$20

$25

$30

$35

$40

2011A 2012A 2013E

3.0

16.4 10.1

18.1

20.4

19.6

Infrastructure Services

Maritime Vertical SnapshotMaritime Vertical Snapshot

1313

Servicing over 3200 Vessels with

the world's largest Ku-band maritime service coverage, reaching 95% of the world's shipping lanes

email and Internet access

real-time monitoring of cargo or shipboard systems

automatic roaming between Ku-band satellite beams and automatic failover to Inmarsat Fleet Broadband

What Do You See?

We see the need for mariners to stay connected to the shore to improve their day-to-day activities

$0

$5

$10

$15

$20

$25

$30

$35

2011A 2012A 2013E

23

28

33

Financial Highlights Financial Highlights

1414

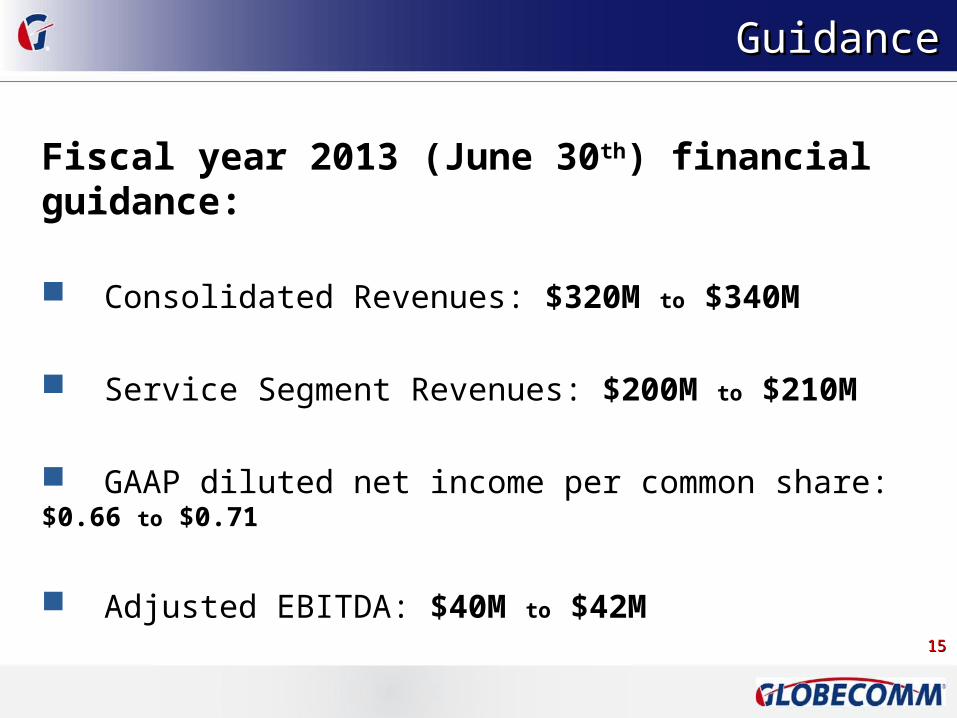

GuidanceGuidance

1515

Fiscal year 2013 (June 30th) financial guidance:

Consolidated Revenues: $320M to $340M

Service Segment Revenues: $200M to $210M

GAAP diluted net income per common share: $0.66 to $0.71

Adjusted EBITDA: $40M to $42M

Revenue Profile Revenue Profile

1616

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2009 2010 2011 2012 YTD 2013

$170,161

$227,817

$274,191

$381,901

$160,902

Consolidated Revenues

Infrastructure Services

Balance Sheet Remains StrongBalance Sheet Remains Strong

17

June 2011 June 2012 Dec. 2012 ASSETS Cash $48.0 $72.2 $73.6 A/R 59.3 59.2 56.0 Inventory 42.4 30.7 36.4 Goodwill From Acquisitions 70.2 68.5 69.0 Other Assets 74.7 79.5 77.2 TOTAL ASSETS $294.6 $310.1 $312.2 LIABILITIES & EQUITY Liabilities $84.0 $70.0 $65.7Debt 26.8 20.7 17.6Equity 183.8 219.4 228.9

TOTAL LIABILITIES & EQUITY $294.6 $310.1 $312.2

$56 million of net cash at 12/31/12. Tangible book value of ~ $6.80 per share at 12/31/12.

($ in millions)

Strong Financial MetricsStrong Financial Metrics

1818

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

2009 2010 2011 2012 YTD 2013

$9,011$13,560

$16,506

$48,201

$14,700

Operating Cash Flow

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

2009 2010 2011 2012 YTD 2013

$12,236

$20,911

$33,932

$42,599

$17,767

Adjusted EBITDA

Globecomm’s significant investments in Cap-Ex, coupled with Earn-Out Adjustments, make Adjusted EBITDA a key metric in measuring the business progress.

Strong operating cash flow to be enhanced by ~$10M in NATO inventory turning into cash in FY13.

EPS and Adjusted EPSEPS and Adjusted EPS

1919

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

2009 2010 2011 2012 YTD 2013

$0.16

$0.38 $0.41

$1.26

$0.28

Fully Diluted Earnings Per Share

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

2009 2010 2011 2012 YTD 2013

$0.16

$0.34

$0.62

$0.74

$0.28

Adjusted Fully Diluted Earnings Per Share

Globecomm currently anticipates fully diluted earnings per share and adjusted fully diluted earnings per share to be the same in fiscal 2013.

2020

Globecomm Continues to Invest in Facilities & TechnologyGlobecomm Continues to Invest in Facilities & Technology

Nearly $47 Million In Capital Expenditure Spending Over Four Years.

We Continue to Make the Global Network More Robust and Invest in Software Applications to Add Value Long-Term.

Strategic Acquisitions Have Enhanced CapabilitiesStrategic Acquisitions Have Enhanced Capabilities

2121

$18.5 Million $5.7 Million $7.0 Million $24.0 Million $19.9 Million

April 2007 March 2009 June 2009 March 2010 April 2011

Globecomm has invested over $75 million in strategic acquisitions in 5 years.

The Company has a disciplined methodology that combines a cultural, strategic and financial view towards acquisitions and will continue to review targets.

With $52 million in net cash and a $72.5 million credit facility, we are well positioned to seek out additional opportunities with cash as the primary source of funding.

Globecomm Systems Inc.Globecomm Systems Inc.

2222

Supplemental Financial Supplemental Financial InformationInformation

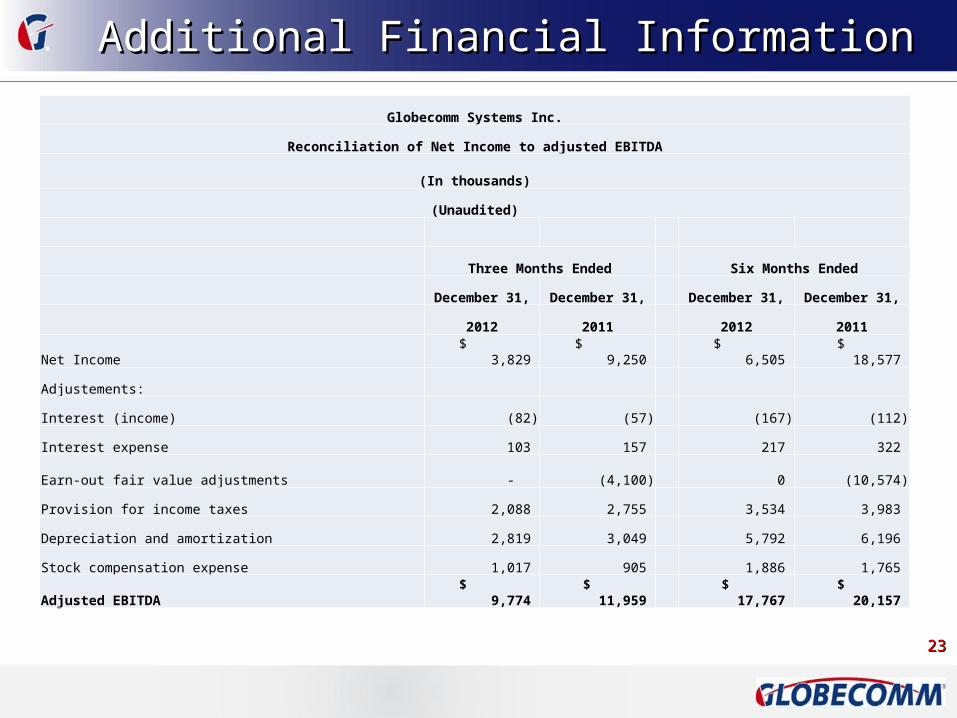

Additional Financial Information Additional Financial Information

2323

Globecomm Systems Inc.

Reconciliation of Net Income to adjusted EBITDA

(In thousands)

(Unaudited)

Three Months Ended Six Months Ended

December 31, December 31, December 31, December 31,

2012 2011 2012 2011

Net Income $ 3,829 $ 9,250 $ 6,505 $ 18,577

Adjustements:

Interest (income) (82) (57) (167) (112)

Interest expense 103 157 217 322

Earn-out fair value adjustments - (4,100) 0 (10,574)

Provision for income taxes 2,088 2,755 3,534 3,983

Depreciation and amortization 2,819 3,049 5,792 6,196

Stock compensation expense 1,017 905 1,886 1,765

Adjusted EBITDA $ 9,774 $ 11,959 $ 17,767 $ 20,157

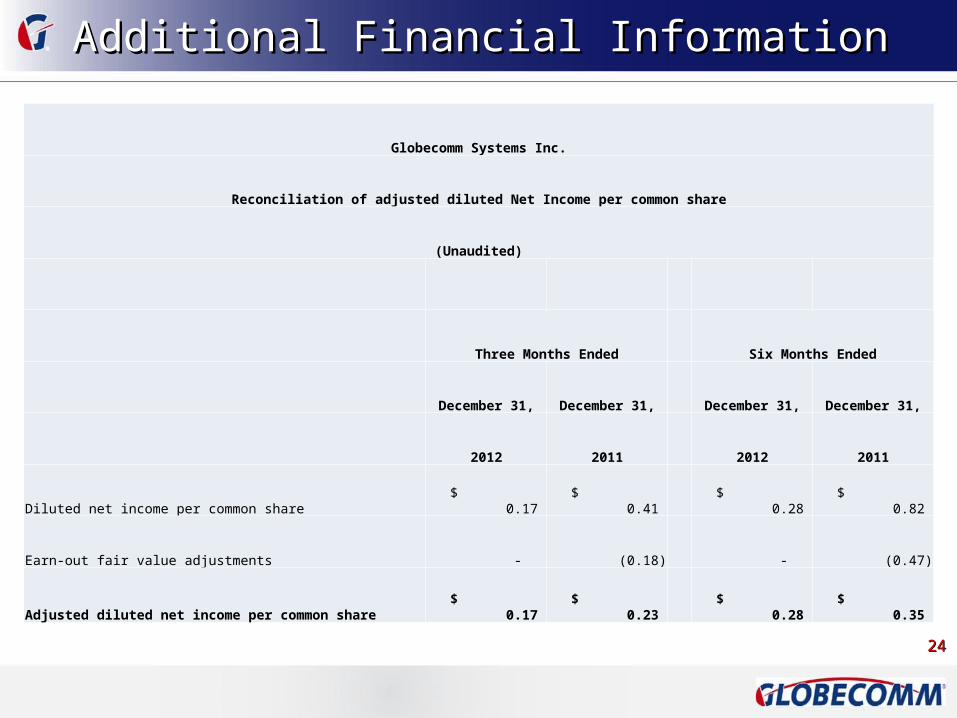

Additional Financial Information Additional Financial Information

2424

Globecomm Systems Inc.

Reconciliation of adjusted diluted Net Income per common share

(Unaudited)

Three Months Ended Six Months Ended

December 31, December 31, December 31, December 31,

2012 2011 2012 2011

Diluted net income per common share $ 0.17 $ 0.41 $ 0.28 $ 0.82

Earn-out fair value adjustments - (0.18) - (0.47)

Adjusted diluted net income per common share $ 0.17 $ 0.23 $ 0.28 $ 0.35