GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES Consolidated Financial Statements As of December 31, 2009 and 2008 (With the Independent Auditor’s Report Thereon) (TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

Transcript

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Financial Statements

As of December 31, 2009 and 2008

(With the Independent Auditor’s Report Thereon)

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

Contents Page Independent Auditor’s Report Financial Statements Balance Sheet 1 Income Statement 2 Statement of Changes in Stockholders’ Equity 3 Statement of Cash Flows 4 Notes to the Financial Statements 6 – 50

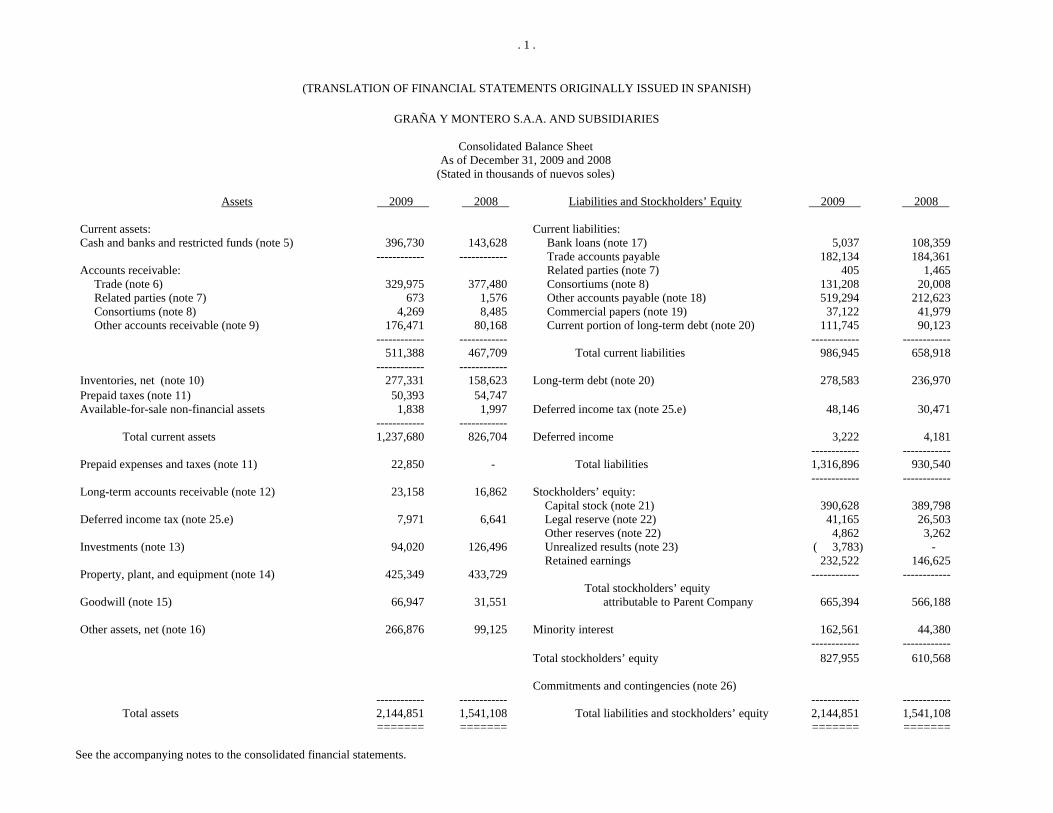

. 1 .

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Balance Sheet As of December 31, 2009 and 2008

(Stated in thousands of nuevos soles)

Assets 2009 2008 Liabilities and Stockholders’ Equity 2009 2008 Current assets: Current liabilities: Cash and banks and restricted funds (note 5) 396,730 143,628 Bank loans (note 17) 5,037 108,359 ------------ ------------ Trade accounts payable 182,134 184,361 Accounts receivable: Related parties (note 7) 405 1,465

Total current assets 1,237,680 826,704 Deferred income 3,222 4,181 ------------ ------------ Prepaid expenses and taxes (note 11) 22,850 - Total liabilities 1,316,896 930,540 ------------ ------------ Long-term accounts receivable (note 12) 23,158 16,862 Stockholders’ equity: Capital stock (note 21) 390,628 389,798 Deferred income tax (note 25.e) 7,971 6,641 Legal reserve (note 22) 41,165 26,503 Other reserves (note 22) 4,862 3,262 Investments (note 13) 94,020 126,496 Unrealized results (note 23) ( 3,783) - Retained earnings 232,522 146,625 Property, plant, and equipment (note 14) 425,349 433,729 ------------ ------------ Total stockholders’ equity Goodwill (note 15) 66,947 31,551 attributable to Parent Company 665,394 566,188 Other assets, net (note 16) 266,876 99,125 Minority interest 162,561 44,380 ------------ ------------ Total stockholders’ equity 827,955 610,568 Commitments and contingencies (note 26) ------------ ------------ ------------ ------------

Total assets 2,144,851 1,541,108 Total liabilities and stockholders’ equity 2,144,851 1,541,108 ======= ======= ======= =======

See the accompanying notes to the consolidated financial statements.

. 2 .

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

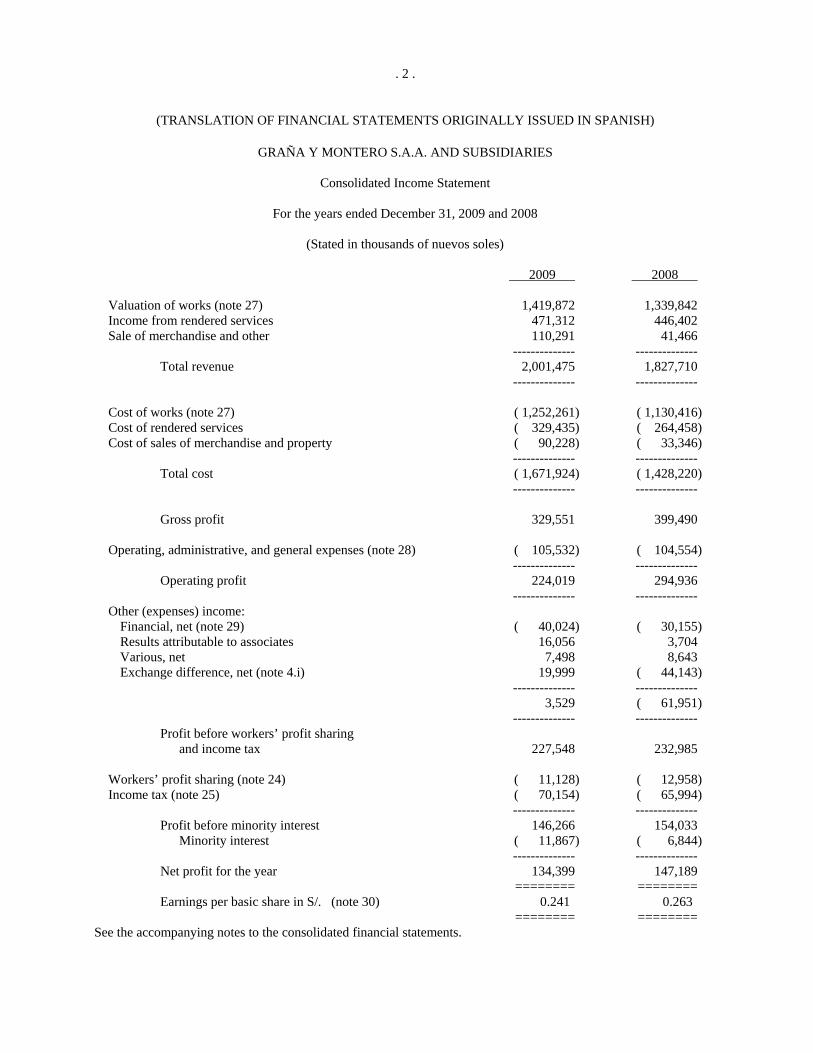

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Income Statement

For the years ended December 31, 2009 and 2008

(Stated in thousands of nuevos soles)

2009 2008 Valuation of works (note 27) 1,419,872 1,339,842 Income from rendered services 471,312 446,402 Sale of merchandise and other 110,291 41,466 -------------- --------------

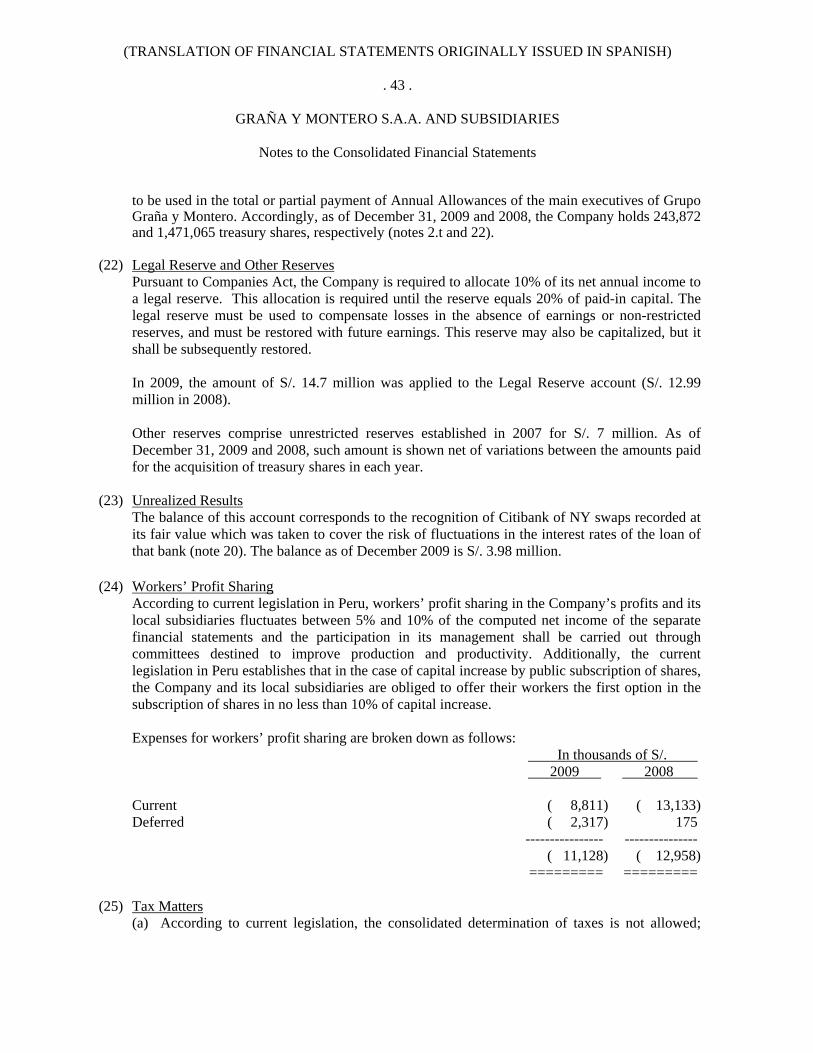

Total revenue 2,001,475 1,827,710 -------------- -------------- Cost of works (note 27) ( 1,252,261) ( 1,130,416)Cost of rendered services ( 329,435) ( 264,458)Cost of sales of merchandise and property ( 90,228) ( 33,346) -------------- --------------

Total cost ( 1,671,924) ( 1,428,220) -------------- --------------

Gross profit 329,551 399,490 Operating, administrative, and general expenses (note 28) ( 105,532) ( 104,554) -------------- --------------

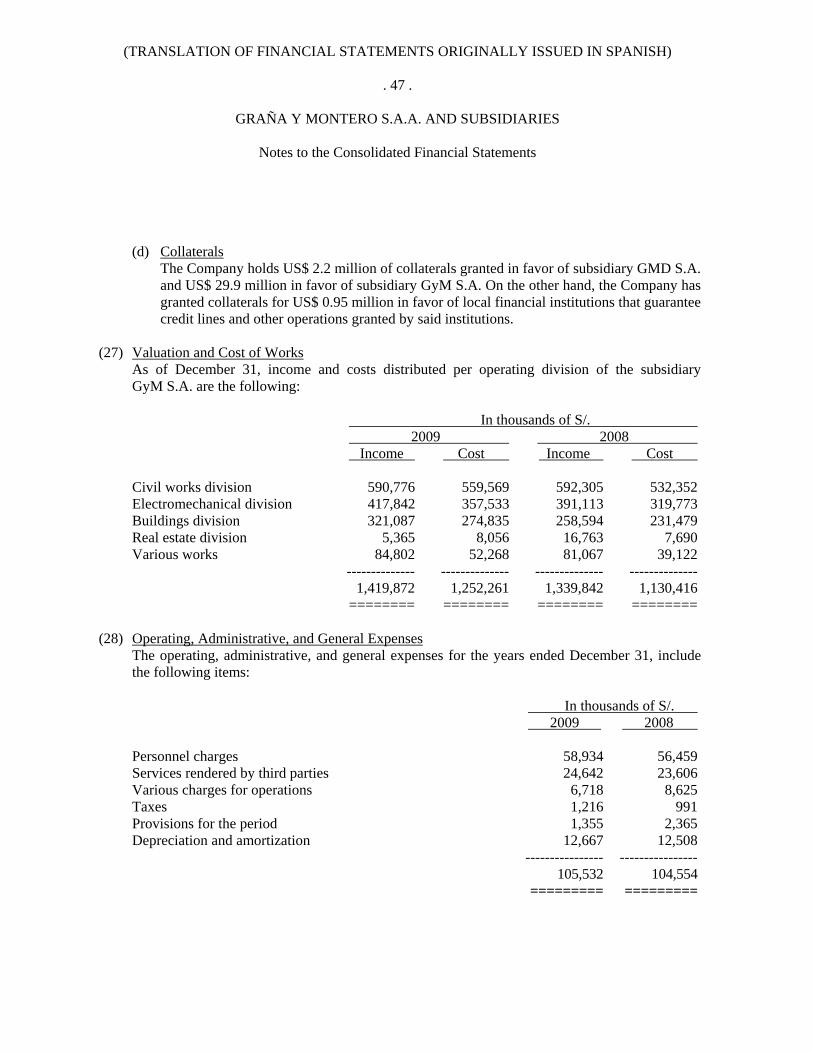

Operating profit 224,019 294,936 -------------- -------------- Other (expenses) income: Financial, net (note 29) ( 40,024) ( 30,155) Results attributable to associates 16,056 3,704 Various, net 7,498 8,643 Exchange difference, net (note 4.i) 19,999 ( 44,143) -------------- -------------- 3,529 ( 61,951) -------------- --------------

Profit before workers’ profit sharing and income tax 227,548 232,985

-------------- -------------- Net profit for the year 134,399 147,189

======== ======== Earnings per basic share in S/. (note 30) 0.241 0.263

======== ======== See the accompanying notes to the consolidated financial statements.

. 3 .

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Consolidated Statement of Changes in Stockholders’ Equity

For the years ended December 31, 2009 and 2008

(Stated in thousands of nuevos soles)

Capital stock

(note 21)

Legal

reserve (note 22)

Other

reserve (note 22)

Unrealized earnings (note 23)

Retained earnings

Total equity attributable to

Parent Company

Minority interest

Total stockholders’ equity

Balances as of December 31, 2007 299,423 13,514 4,388 - 130,012 447,337 33,874 481,211 Capitalization 91,042 - - - ( 91,042) - - - Transfer to legal reserve - 12,989 - - ( 12,989) - - - Dividends paid - - - - ( 25,981) ( 25,981) - ( 25,981)Adjustment - - - - ( 564) ( 564) 3,662 3,098 Treasury shares (note 21) ( 667) - ( 1,126) - - ( 1,793) - ( 1,793)Net profit for the year - - - - 147,189 147,189 6,844 154,033 ------------- ------------- ------------- ------------- -------------- -------------- ------------- ------------- Balances as of December 31, 2008 389,798 26,503 3,262 - 146,625 566,188

44,380

610,568

Transfer to legal reserve - 14,662 - - ( 14,662) - - - Dividends paid - - - - ( 29,438) ( 29,438) - ( 29,438)Adjustment - - - - ( 4,402) ( 4,402) - ( 4,402) Minority interest (note 15) - - - - - - 106,314 106,314 Treasury shares (note 21) 830 - 1,600 - - 2,430 - 2,430 Fluctuation in derivative fair value - - - ( 3,783) - ( 3,783) - ( 3,783)Net profit for the year - - - - 134,399 134,399 11,867 146,266 ------------- ------------- ------------- ------------- -------------- -------------- ------------- ------------- Balances as of December 31, 2009 390,628 41,165 4,862 ( 3,783) 232,522 665,394 162,561 827,955 ======== ======== ======== ======== ======== ======== ======== ======== See the accompanying notes to the consolidated financial statements.

. 4 .

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

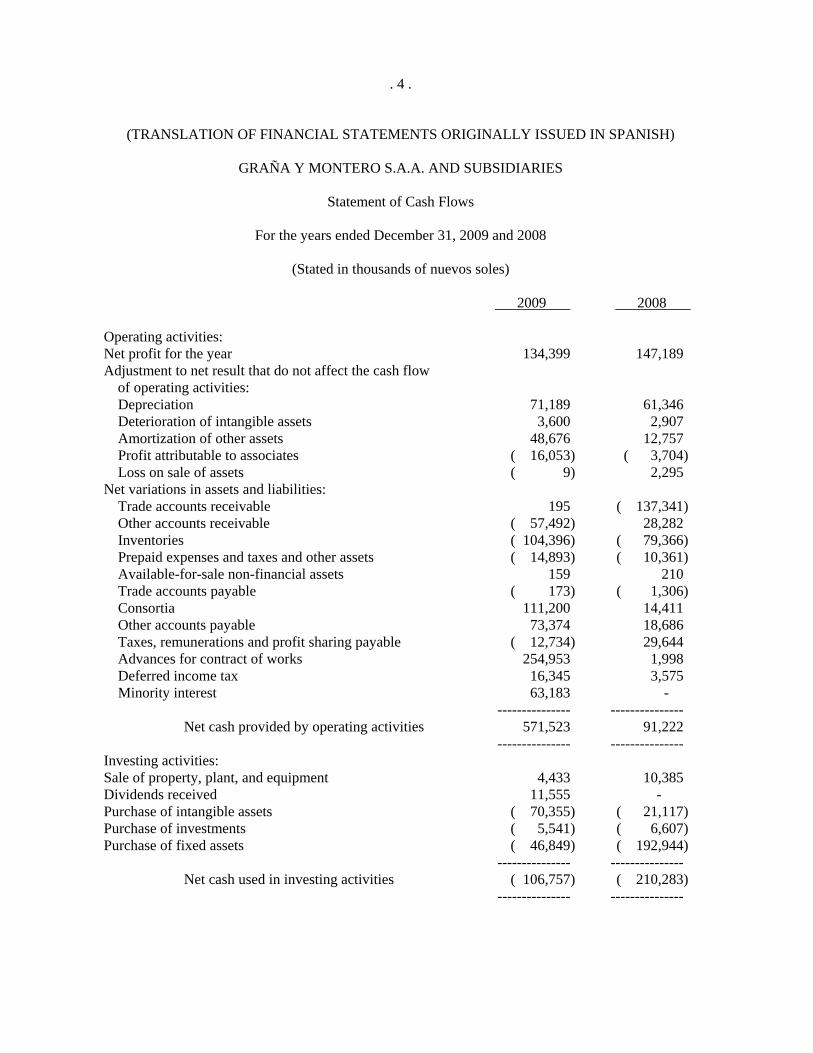

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Statement of Cash Flows

For the years ended December 31, 2009 and 2008

(Stated in thousands of nuevos soles)

2009 2008 Operating activities: Net profit for the year 134,399 147,189 Adjustment to net result that do not affect the cash flow

of operating activities: Depreciation 71,189 61,346 Deterioration of intangible assets 3,600 2,907 Amortization of other assets 48,676 12,757 Profit attributable to associates ( 16,053) ( 3,704) Loss on sale of assets ( 9) 2,295

Net variations in assets and liabilities: Trade accounts receivable 195 ( 137,341) Other accounts receivable ( 57,492) 28,282 Inventories ( 104,396) ( 79,366) Prepaid expenses and taxes and other assets ( 14,893) ( 10,361) Available-for-sale non-financial assets 159 210 Trade accounts payable ( 173) ( 1,306) Consortia 111,200 14,411 Other accounts payable 73,374 18,686 Taxes, remunerations and profit sharing payable ( 12,734) 29,644 Advances for contract of works 254,953 1,998 Deferred income tax 16,345 3,575 Minority interest 63,183 -

--------------- --------------- Net cash provided by operating activities 571,523 91,222

--------------- --------------- Investing activities: Sale of property, plant, and equipment 4,433 10,385 Dividends received 11,555 - Purchase of intangible assets ( 70,355) ( 21,117) Purchase of investments ( 5,541) ( 6,607) Purchase of fixed assets ( 46,849) ( 192,944) --------------- ---------------

Net cash used in investing activities ( 106,757) ( 210,283) --------------- ---------------

. 5 .

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

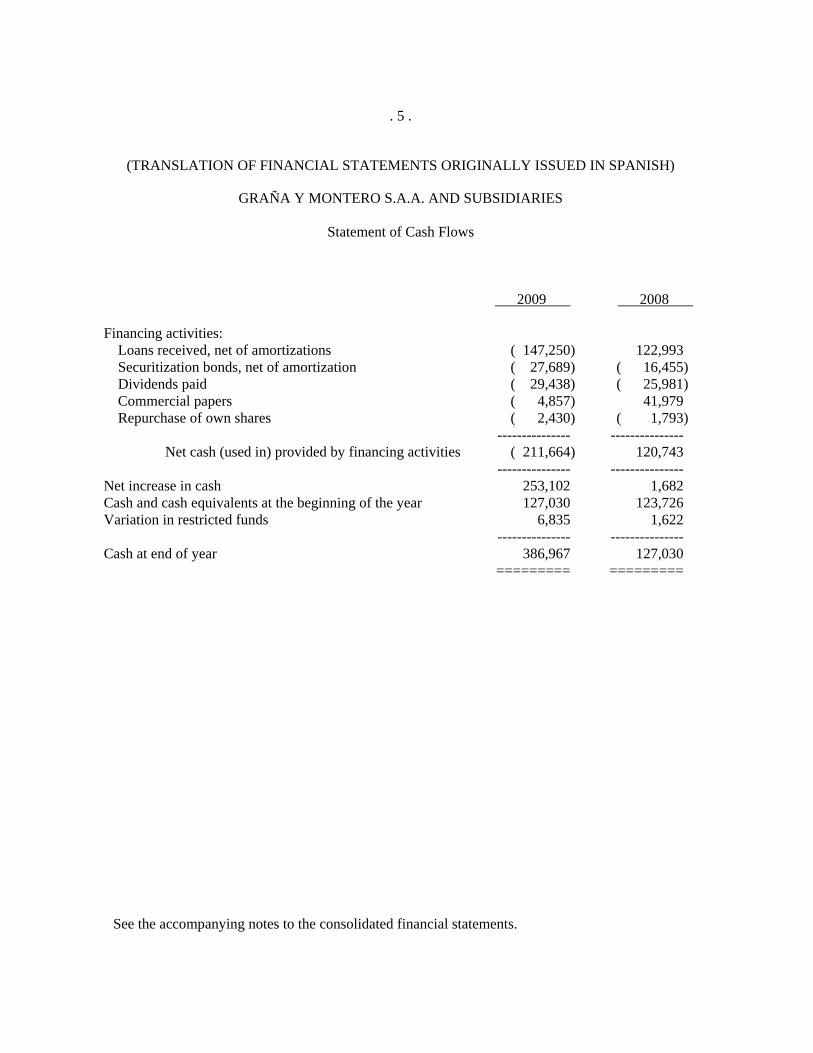

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Statement of Cash Flows

2009 2008 Financing activities:

Loans received, net of amortizations ( 147,250) 122,993 Securitization bonds, net of amortization ( 27,689) ( 16,455) Dividends paid ( 29,438) ( 25,981) Commercial papers ( 4,857) 41,979 Repurchase of own shares ( 2,430) ( 1,793)

--------------- --------------- Net cash (used in) provided by financing activities ( 211,664) 120,743

--------------- --------------- Net increase in cash 253,102 1,682 Cash and cash equivalents at the beginning of the year 127,030 123,726 Variation in restricted funds 6,835 1,622 --------------- --------------- Cash at end of year 386,967 127,030 ========= =========

See the accompanying notes to the consolidated financial statements.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 6 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

As of December 31, 2009 and 2008

(1) Business Activity Graña y Montero S.A.A. was incorporated on August 12, 1996 as the holding company of Grupo Graña y Montero. Its main activity is to invest in subsidiaries and related parties. Additionally, as from September 2005, it renders services of general management, financial management, commercial management, legal advisory and human resources management (prior to that date, it rendered business advisory services) to said companies. The Company’s legal domicile is located at Av. Paseo de la República 4675, Surquillo.

Likewise, as from year 2006, Graña y Montero S.A.A. has been engaged in the leasing of offices to the Group companies and to third parties. Year 2009 consolidated financial statements will be submitted to Board of Directors and General Stockholders’ Meeting within the terms established by law for the separate financial statements of Graña y Montero S.A.A.:

(a) Subsidiaries:

The consolidated financial statements of Graña y Montero S.A.A. and Subsidiaries (hereinafter the Group) include assets, liabilities, revenue and expenses of the following subsidiaries:

• GyM S.A. is engaged in the business of civil construction, electromechanical assembly, buildings, management and development of real property projects and other related services.

• GMP S.A. is engaged in the exploitation, production, treatment, and trading of oil, natural gas and its derivatives, as well as the storage and delivery of fuels.

• GMD S.A. is engaged in providing IT solutions in the Peruvian corporate market. • GMI S.A. Ingenieros Constructores is engaged in providing services of advisory and

engineering consultancy, execution of surveys and projects, project management and works supervision.

• Concar S.A. is engaged in the operation and maintenance of highways on concession. • Fashion Center S.A. is engaged in developing and operating the conditioning and fitting

out project for commercial and recreational use of the area of Parque Salazar of the district of Miraflores.

• Until June 30, 2007, Larcomar S.A. was engaged in the operation of the project that is currently operated by Fashion Center S.A.

• Survial S.A., is engaged in the execution of the concession agreement of phase 1 of Southern Inter-oceanic highway.

• Concesión Canchaque S.A. is engaged in the execution of the concession agreement of the Buenos Aires – Canchaque highway.

• GMV S.A. is engaged in the real estate business, management services and project management and other services related to real estate and building sectors.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 7 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

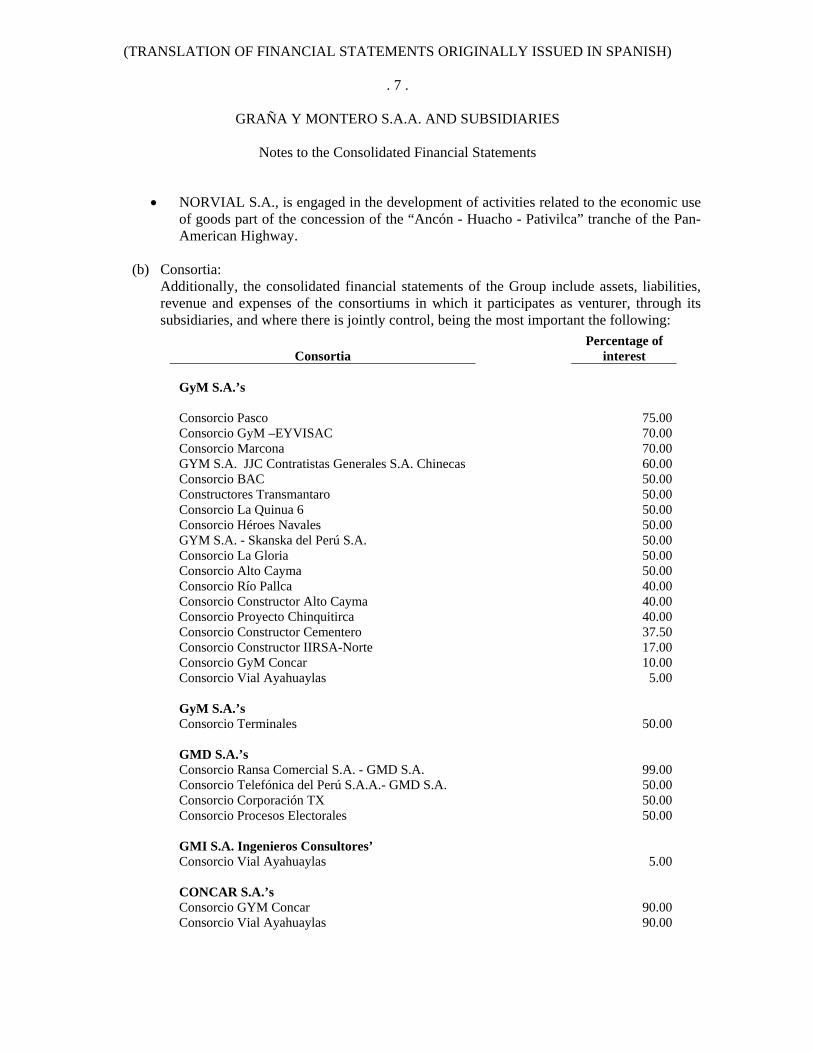

• NORVIAL S.A., is engaged in the development of activities related to the economic use of goods part of the concession of the “Ancón - Huacho - Pativilca” tranche of the Pan-American Highway.

(b) Consortia:

Additionally, the consolidated financial statements of the Group include assets, liabilities, revenue and expenses of the consortiums in which it participates as venturer, through its subsidiaries, and where there is jointly control, being the most important the following:

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 8 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

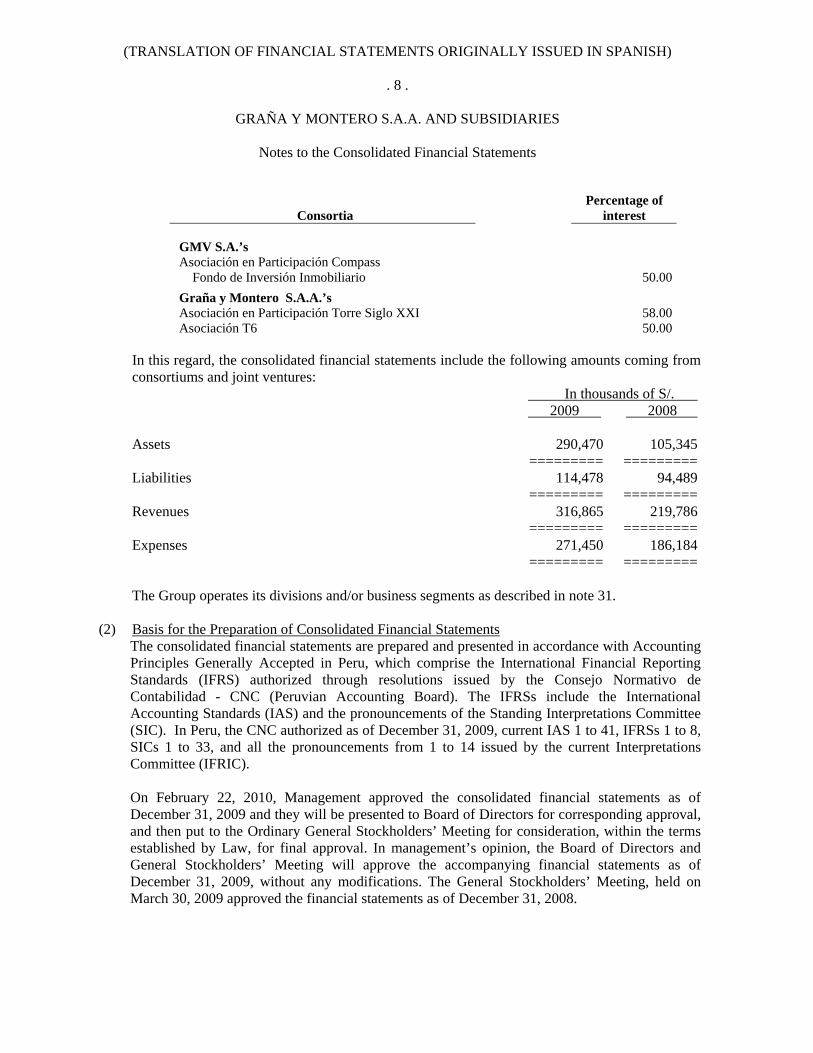

Consortia Percentage of

interest GMV S.A.’s Asociación en Participación Compass Fondo de Inversión Inmobiliario 50.00Graña y Montero S.A.A.’s Asociación en Participación Torre Siglo XXI 58.00Asociación T6 50.00

In this regard, the consolidated financial statements include the following amounts coming from consortiums and joint ventures:

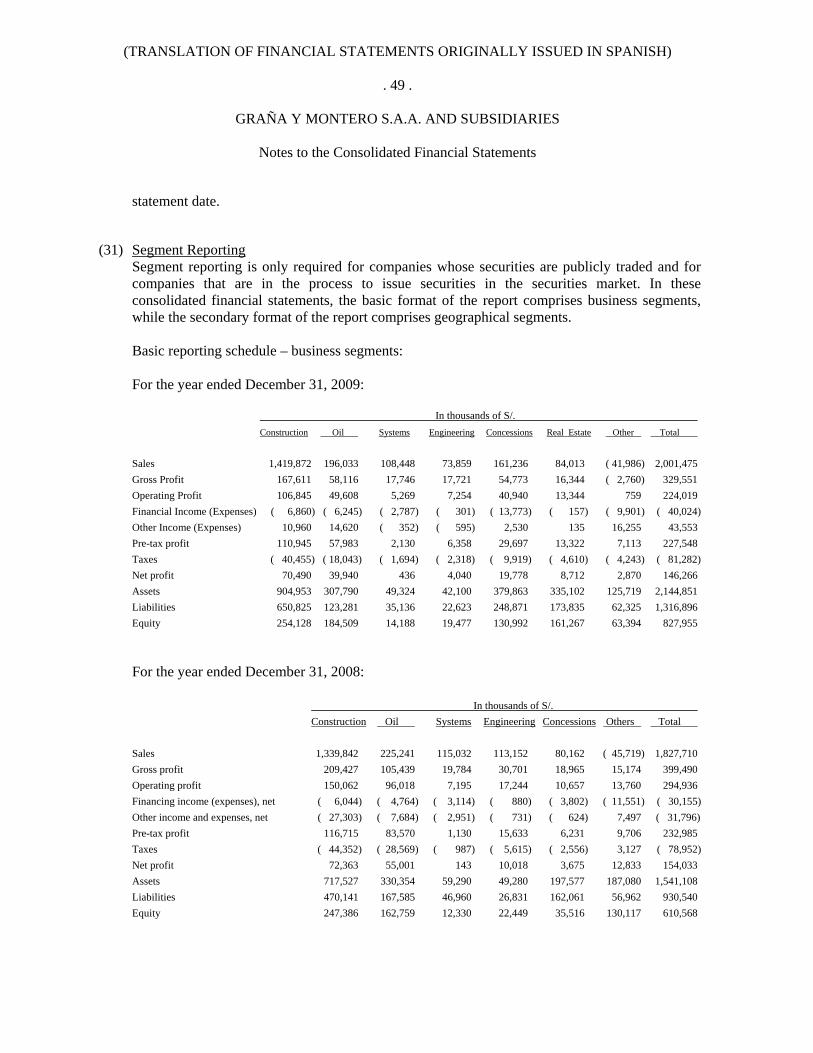

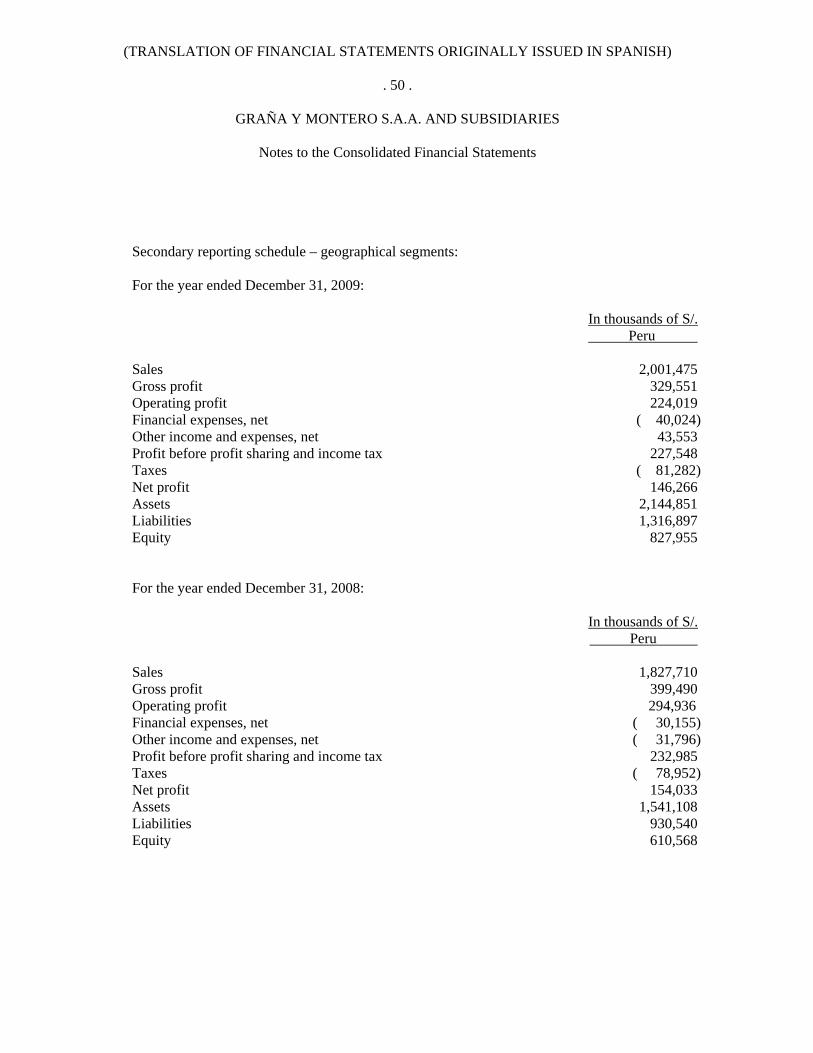

The Group operates its divisions and/or business segments as described in note 31.

(2) Basis for the Preparation of Consolidated Financial Statements The consolidated financial statements are prepared and presented in accordance with Accounting Principles Generally Accepted in Peru, which comprise the International Financial Reporting Standards (IFRS) authorized through resolutions issued by the Consejo Normativo de Contabilidad - CNC (Peruvian Accounting Board). The IFRSs include the International Accounting Standards (IAS) and the pronouncements of the Standing Interpretations Committee (SIC). In Peru, the CNC authorized as of December 31, 2009, current IAS 1 to 41, IFRSs 1 to 8, SICs 1 to 33, and all the pronouncements from 1 to 14 issued by the current Interpretations Committee (IFRIC). On February 22, 2010, Management approved the consolidated financial statements as of December 31, 2009 and they will be presented to Board of Directors for corresponding approval, and then put to the Ordinary General Stockholders’ Meeting for consideration, within the terms established by Law, for final approval. In management’s opinion, the Board of Directors and General Stockholders’ Meeting will approve the accompanying financial statements as of December 31, 2009, without any modifications. The General Stockholders’ Meeting, held on March 30, 2009 approved the financial statements as of December 31, 2008.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 9 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(a) Measurement Bases

The consolidated financial statements have been prepared in conformity with the historical cost principle, except for the derivative instruments recorded at fair value.

(b) Functional and Presentation Currency The consolidated financial statements are presented in nuevos soles (S/.) which is the

Company’s functional and presentation currency.

(c) Significant Accounting Estimates and Criteria The accounting estimates and criteria used for the preparation of the consolidated financial statements are continuously evaluated and are based on historical experience and other factors, including the reasonable expectation of occurrence of future events depending on the circumstances. The Company makes estimates and assumptions regarding the future. Resulting accounting estimates may vary from respective actual results. However, it is the opinion of management that estimates and assumptions applied by the Company do not have significant risk as to produce a material adjustment to the balances of assets and liabilities for next year. Significant estimations related to the consolidated financial statements are: amortization of intangible assets, depreciation of property, plant, and equipment, provision for severance indemnities, provision for income tax, and workers’ profit sharing, liability, the accounting criteria for which is described below. Review of carrying amount and provision for impairment The Company applies the guidelines stated in IAS 36 to determine whether a permanent asset requires from a provision for impairment. This determination requires the use of professional judgment by Management to analyze the indicators that might present impairment as well as the determination of value in use. In this last case, it is required to apply judgment in the elaboration of future cash flows that include the projection of future operations level of the Company, projection of economic factors that affect income and costs, as well as the election of the discount rate to be applied in this flow. Taxes Interpretations of applicable tax legislation are required in determining obligations and tax expenses. The Company looks for professional counseling in tax matters before taking any decision on it. Although Management considers that its estimates are prudent and appropriate, interpretation differences may arise with tax authorities affecting the charges for taxes in the future.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 10 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

Management has exercised its critical judgment when applying accounting policies for the preparation of the accompanying financial statements, as explained in the corresponding accounting policies.

(d) Consolidated Financial Statements The consolidated financial statements comprise the financial statements of Graña y Montero S.A.A., and the financial statements of the subsidiaries and consortia detailed in note 1.

Subsidiaries The subsidiaries are all entities over which the Company has authority to govern their operating and financial policies generally for being holder of more than half of voting shares. Subsidiaries are consolidated from the date on which their control is transferred to the Company. They are de-consolidated from the date the control ceases. The Company uses the purchase method to record the acquisition of subsidiaries. The cost of acquisition is measured as the fair value of delivered assets, equity instruments issued, and liabilities incurred or assumed at the date of the exchange, plus costs directly attributable to the acquisition. Identifiable assets acquired and liabilities assumed in a business combination are initially measured at fair value at the acquisition date. The excess of the cost of acquisition over the fair value of the Company’s interest in identifiable net assets acquired is recorded as goodwill in the assets. If the cost is lower than the subsidiary’s fair value of net assets (badwill), the difference is recognized directly in the income statement. Transactions, balances and unrealized gains among the companies that the Group controls are eliminated. Also, unrealized losses are eliminated unless the transaction provides evidence of impairment in the value of the assets transferred.

Consortia The Company’s interest in jointly controlled entities is recorded by the proportionate consolidation method, through which the Company includes in the relevant components of its consolidated financial statements the proportionate shareholding of its interest in revenue and expenses, assets and liabilities and individual cash flows of the joint venture. Significant transactions between the Company and joint ventures have been eliminated. Minority Interest Interests from third parties, that are not part of the Group, are shown as minority interests under the equity in the consolidated balance sheet and in the consolidated income statement.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 11 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements (3) Main Accounting Policies

Main accounting principles applied in the preparation of consolidated financial statements are detailed below. These principles and practices have been applied consistently to all years presented in these financial statements; unless otherwise indicated.

(a) Cash and Cash Equivalents

Cash and cash equivalents comprise cash in hands, overnight, time and sight deposits held at banks with original maturities between two and three months.

(b) Trade Accounts Receivable and Provision for Doubtful Accounts Accounts receivable are initially recorded at their fair value and are subsequently valued at amortized cost, less the provision for deterioration. The provision for deterioration of trade accounts receivable is determined when there is objective evidence that the Group will not collect all the amounts overdue according to terms originally established. Management considers that the balances of trade accounts receivable as of December 31, 2009 and 2008 do not present uncollectibility risks. Trade accounts receivable are presented net of the advances received from clients provided that they are related with the same work agreement and said agreement establishes the possibility of compensation.

(c) Inventories

Inventories are valued at construction, acquisition and/or contribution costs, which do not exceed the net realizable value. The cost of construction materials is determined through the weighted average method, except in the case of inventories in transit, determined by the specific identification method. The net realizable value is the estimated selling price in the ordinary course of business, less cost to sale, and the commercialization costs. For the reductions of inventory book value at net realizable value, a provision for inventory impairment is recorded in the results of the period when those reductions occur.

(d) Financial Instruments

A financial instrument is any contract that gives rise to both a financial asset in one entity and a financial liability, or equity instrument in another. In the case of the Group, financial instruments correspond to primary instruments such as accounts receivable, accounts payable, long-term debts, commercial papers, derivative instruments, and shares representing capital share in other companies. Financial instruments are classified as asset, liability or equity according to the substance of the contract. The interest, dividends, gains, and losses generated by a financial instrument, and classified as liability, are recorded as income or expense in the income statement. The payment to holders of financial instruments classified as equity is recorded directly against equity. The financial instruments are compensated when the Group has the legal right to

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 12 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

compensate them, and management has the intention of paying them on a net basis or negotiating the asset, and paying the liability simultaneously. Fair value is the amount for which an asset could be exchanged between knowledgeable, purchaser and a seller, or a liability settled between a debtor and a creditor in an arm’s length transaction. In Management’s opinion, the carrying amount of financial instruments as of December 31, 2009 and 2008, is substantially similar to their fair values due to their short period of realization and/or maturity. The recognition and valuation criteria of those accounts are disclosed in the notes to the financial statements on accounting policies.

(e) Financial Assets

The Group classifies its investments in the following categories: i) marketable financial assets, ii) loans and accounts receivable, iii) Held-to-maturity investments, and iv) available-for-sale financial assets. The classification depends on the purpose for which investments were acquired. Management determines the classification of their investments as of the date of their initial recognition and reassesses this classification as of every closing date.

• Financial assets at fair value through profit or loss

A financial asset is classified in this category if it was mainly acquired in order to be sold in the short-term or if it is so designated by Management. Derivative financial instruments are also classified as marketable unless they are designated as hedges. Assets in this category are classified as current assets if they are held as marketable or they are expected to be realized within 12 months as from the balance sheet date. During 2009 and 2008, the Group did not hold any investment under this category.

• Loans and accounts receivable

Loans and accounts receivable are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They arise when the Group provides with money, goods or services directly to a debtor, with no intention to trading the account receivable. They are included in current assets, except for maturities exceeding 12 months after balance sheet date; these ones are classified as non-current assets. Loans and accounts receivable are included in trade accounts receivable from affiliates and various accounts receivable in the balance sheet (notes 6, 7, 8 and 9).

• Held-to-maturity investments

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities acquired with the intention and ability to hold them to maturity. During 2009 and 2008, the Group did not hold any investment under this category.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 13 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

• Available-for-sale financial assets Available-for-sale financial assets are non-derivative financial assets designated in this category or that do not classify in any of the other categories. These assets are shown as non-current assets unless Management has express intention to sell the investment within 12 months after the date of the balance sheet. During 2009 and 2008, the Group did not hold any investment under this category.

Recognition and Measurement Investment purchases and sales are recognized as of the trade date, date on which the Group commits to purchase or sale the asset. Transaction costs related to financial assets recorded at fair value through profit and losses are recognized in the income statement. Financial assets are derecognized when the rights to receive cash flows from investments have expired or have been transferred, and the Group has substantially transferred all risks and rewards derived from ownership. Available-for-sale financial assets and held-for-trading assets are subsequently recognized at fair value. Loans, accounts receivable, and held-to-maturity investments are measured at their amortized cost using the effective interest method. Realized and unrealized gains and losses arising from changes in the fair value of the “held-for-trading” category are included in the income statement, in the period they are originated. Unrealized gains and losses arising from changes in the fair value of non-monetary securities, classified as available-for-sale, are recognized in equity. When securities classified as available-for-sale are sold or impaired, accumulated fair value adjustments are included in the income statement as gains or losses on investment in securities. Fair value of quoted investments is based on current bid prices. If market is not active (or securities are not quoted), the Company establishes the fair value by using valuation techniques.

The Group evaluates at each balance sheet date, if there is objective evidence of the impairment of a financial asset or group of financial assets.

(f) Available-for-Sale Non-Financial Assets Assets are classified as available for sale when their book value is expected to be recovered through their sale, when there is a plan for such a sale, and it is highly probable that their sale occurs in the short-term. These assets are valued at the lower of their cost or at their realizable value, less cost to sell.

(g) Derivative Instruments The Group uses derivative instruments to reduce the risk of exchange rate fluctuations in its foreign currency accounts payable. Derivative instruments are recorded in conformity with IAS 39 “Financial Instruments: Recognition and Measurement”.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 14 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

Derivative Instrument Contracts, for which the Group has established a fair value hedging relationship, are recorded as assets or liabilities in the balance sheet and are presented at fair value. Changes in the fair value are presented in the income statement, under net gains (losses) on derivative instruments. Derivative instruments are assessed at the beginning of the hedge and are considered highly effective if they are within a range of 80-125%. These hedges can be effective or not to compensate the risk of variations in the exchange rate of accounts payable in foreign currency recognized in the financial statements. In both cases, changes in the fair value are directly recorded in the results of the period. Likewise, the Group is exposed to the market risk due to changes in the interest rate and uses derivative instruments to mitigate partially this risk. Derivative Instrument Contracts, for which the Group has established a hedging relationship of future cash flows, are recorded as assets or liabilities in the balance sheet and presented at its fair value. As these hedges are effective to compensate the exchange risk in the interest rate, changes in the fair value are recorded directly to an equity account. These amounts are transferred to the results of the period in which the financial liability is settled and are presented in the net gains (losses) on derivative instruments. Such instruments shall be evaluated on a periodic basis and consider their effectiveness to reduce the risk associated to the exposure that is being covered. If in any moment, the hedging is not effective, changes in the fair value, as from that moment, shall be shown in the results of the period.

(h) Investments in Associates Associates are all entities on which the Group exerts significant influence but not control. Investments in associates are recorded under the equity method, recognizing changes in the results and the equity of the associate, on a proportion basis, in the Group’s financial statements. Dividends received from the associates are recorded as a decrease in the investment value.

(i) Joint Venture The Group’s interest in jointly controlled entities is recorded by the proportionate consolidation method, through which the Group includes in the relevant components of its financial statements the proportionate shareholding of its interest in revenue and expenses, assets and liabilities and individual cash flows of the joint venture. Significant transactions between the Group and joint ventures have been eliminated.

(j) Property, Plant, and Equipment Property, plant, and equipment are recorded at acquisition cost, less accumulated depreciation (note 14). Historical cost includes disbursements directly attributable to the acquisition of these items. Subsequent costs attributable to the goods of the fixed asset improving their original performance are capitalized; other costs are recognized in the results.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 15 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

Lands are not depreciated. Depreciation of plant and equipment and vehicles recognized as “Large Equipment” is calculated based on their use hours, in relation to the estimated useful hours of these assets. The depreciation of other assets that do not qualify as “Large Equipment” is calculated by straight line method to assign its cost less its residual value during the estimated useful life, as follows:

Years

Buildings and premises 5 to 33 Plant and equipment 5 to 10 Vehicles 5 to 10 Furniture and fixtures 4 to 10 Various equipment 4 to 10 The residual value and the useful life of an asset are reviewed and adjusted, if necessary, at each balance sheet date. The carrying amount of an asset is written off immediately at its recoverable amount when the carrying amount of the asset exceeds its estimated recoverable value. Gains and losses for sale of fixed assets correspond to the difference between the income from the transaction and the asset carrying amount. Those are included in the income statement. Assets under construction are capitalized as a separate component of property, plant and equipment. At completion, the cost is transferred to the appropriate category. Work-in-progress is not depreciated.

(k) Impairment Loss

When there are events or circumstantial economic changes indicating that the value of long-live asset might not be recoverable, Management reviews the carrying amount of these assets. If the result of the analysis is that the carrying amount of the asset exceeds its recoverable amount, the Company recognizes an impairment loss in the income statement, or the revaluation surplus is decreased in the case of revalued assets, by an amount equivalent to the excess in the carrying amount net of its tax effects related to deferred income tax and workers’ profit sharing. Recoverable amounts are estimated for each asset or, if it is not possible, for each cash-generating unit. The recoverable amount of a long-life asset or a cash-generating profit is the higher of the asset’s fair value less costs to sell and its value in use. Fair value less cost to sell of a long-life asset or cash-generating profit, is the amount obtainable from its sale, in a transaction conducted on mutual independence conditions between knowledgeable parties, less corresponding costs to sell. Value in use is the present value of the future cash flows expected to arise from value of an asset or a cash-generating unit. Book balances of non-financial assets different from those of the goodwill that have been written off due to deterioration are reviewed as of the date of each report to verify any possible reversal of deterioration.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 16 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(l) Finance Lease Agreements Lease and/or sale agreements with a leaseback agreement on plant and equipment, through which the Group substantially assumes all risks and rewards related to the property of leased assets, are classified as finance lease and are capitalized at the inception of the lease terms, at an amount equal to the fair value of leased property, or if lower, to the present value of the minimum lease payments. Lease payments are apportioned between the reduction of the outstanding liability and the finance charge so as to produce a constant periodic rate of interest on the remaining balance of the liability. Obligations for finance and/or sale leases with finance leaseback agreements, net of financial charges, are included in the Long-term Debt account in the balance sheet. The financial cost is charged to results over the lease period. The cost of assets acquired through finance lease and/or sale with finance leaseback agreement is depreciated over their estimated useful life.

(m) Public Service Concession Arrangements

Public service concession arrangements operated by Consorcio Terminales, a consortium in which subsidiary Graña y Montero Petrolera S.A. has a 50% interest, are recorded as intangible assets because cash flows are conditional on usage levels of public service by users. Revenue and costs relating to construction of public infrastructure works are recognized by reference to the stage of completion, while revenue and expenses related to rendering of public services are recognized on an accrual basis.

(n) Goodwill

Goodwill represents the excess of the cost of an acquisition over the fair value of the Group’s interest of the identifiable net assets of a subsidiary as of the acquisition date. Likewise, the goodwill arising during the acquisition of minority interest in a subsidiary represents the excess of cost of the additional investment over fair value of net identifiable assets as of the date of acquisition. Goodwill is reviewed to determine whether a recognition of provisions for impairment is required. It is recorded at cost less accumulated provisions for impairment. Impairment losses are recognized in the income statement and are not reversed. Gains and losses from the sale of subsidiaries or associates include the carrying amount of goodwill related to the sold entity. Goodwill is allocated to cash-generating units to conduct impairment tests. Each of those cash-generating units represents the Group’s investment in every place where it operates per primary reporting segment (note 15).

(o) Other Assets

Concessions included in Other Assets item of the balance sheet are recognized as such based on the forecast that these will generate future economic benefits for the Group. Concessions are recorded at cost. These fees are amortized at straight-line method based on the remaining maturity of concession agreements. Repairs of highways and works in parking lots are capitalized, and regular maintenance of highways and parking lots are recognized in expenses when they are incurred.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 17 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

Investments in exploration, development and subscription rights of concession agreements are amortized as from the period when income from its exploitation is obtained until the maturity of the respective agreements. On the other hand, if it were the case, investments in exploration and exploitation, referred to those exploration agreements in which it has been determined that results are not successful, are charged to the results in the period when this situation is determined, after the compensation attributable to the interests of third parties in said investments. Costs related to the development or maintenance of software are recognized in results when incurred. However, costs that are directly related to single and identifiable software, that are controlled by the Group and that will provide future economic benefits higher than their cost in more than one year, are recognized as intangible assets. Direct costs related to the development of software include personnel costs and an aliquot part of general expenses. Development costs of capitalized software are amortized by straight-line method in the estimate of its useful life, without exceeding five years.

(p) Loans

Loans are initially recognized at their fair value, net of transaction costs incurred. These loans are subsequently recorded at their amortized cost, and any resulting difference between the funds received (net of transaction costs) and the redemption value is recognized in the income statement over the period of the loan using the effective interest method. Loans are classified as current liability unless the Group has the unconditional right to differ settlement of the liability for at least twelve months after the balance sheet date.

(q) Provisions

Provisions are recognized when the Group has a present legal obligation, either legal or constructive, as a result of past events, and when it is probable that an outflow of resources will be required to settle the obligation, and it is possible to reliably estimate its amount. Restructuring cost provisions comprise lease termination penalties and employee termination payment. Provisions for future operating losses are not recognized. When there are a number of similar obligations, the probability that an outflow of resources will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognized although the likelihood of outflow for any specific item included in the same class of obligations may be small. Provisions are recognized at present value of expenditures expected to be required to settle the obligation using pre-tax rates that reflect the current market assessment of the time value of money and the risks specific to the obligation. The increase in the provision due to the passage of time is recognized as interest expense in the income statement.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 18 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(r) Share of the Profits The Group recognizes a liability and an expense for workers’ profit sharing in profits equivalent to 5% and 10% of taxable base determined according to the current tax legislation for each subsidiary.

(s) Income Tax

Current income tax is determined according to current tax provisions (note 25). Deferred income tax is recorded using the liability method, recognizing the effect of temporary differences that arise between the tax base of assets and liabilities and its balance in the financial statements. Deferred tax assets are only recognized as it is probable to have taxable benefits in the future against the credits that can be used.

The effect of these temporary differences is also considered in the calculation of workers’ profit sharing.

(t) Capital Stock

Common shares are classified as equity. When the capital stock recognized as equity is repurchased (treasury shares) in conformity with the IFRSs, the payment made including any cost directly related (net of taxes) is deducted from the Group’s equity until shares are amortized, reissued or sold (this repurchase has a different connotation under article 105 of Companies Act). When such shares are subsequently reissued or sold, any payment received, net of incremental costs directly attributable to the transaction and effects corresponding to income tax, is included in the equity (note 21).

(u) Dividend Distribution

Dividend distribution to stockholders is recognized as liability in the financial statements in the period when dividends are approved by General Stockholders’ Meeting.

(v) Contingent Liabilities and Contingent Assets

Contingent liabilities are not recognized in financial statements. They are only disclosed in the notes to financial statements unless the possibility of an outflow of economic resources is remote. Contingent assets are not recognized in financial statements, and they are only disclosed when an inflow of economic benefits is probable.

(w) Revenue Recognition

The Group recognizes revenues when the amount can be reliably measured, it is probable that future economic benefits will flow to the Group, and specific criteria are met per type of revenue as described below. Revenues are recognized in the results as follows:

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 19 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

Income from work valuations Income from work valuations and their respective costs are recognized as such when executing them, according to work progress. Additionally, such income and costs are adjusted to recognize the final projected profit margin of works which is monthly reviewed. Income is invoiced prior approval of works owners. Sale of goods Ordinary revenues from sale of goods are recognized and recorded when the products are delivered and the significant risks and rewards of ownership of the goods are transferred to the buyer, and the collection of corresponding accounts receivable is fairly certain.

Rendering of services Revenues from rendered services are recognized in the accounting period in which the services are rendered, by reference to the stage of completion of the service, determined based on the services performed to date as a percentage of total services to be performed. Revenue and costs for services rendered are recognized as such when the services are rendered.

Interest and dividends Interest income is recognized on a time proportion basis, using the effective interest method. Revenues from dividends are recognized when the right to receive the payment has been established.

(x) Standards Not Yet Adopted by the Company Certain standards and interpretations have been issued internationally. In Peru, the CNC has not yet approved the following standards:

- IFRS 9 Financial Instruments: This standard is related to classification and measurement of financial assets; it will be effective in January 2013 and its early adoption is recommended. This standard does not supersede IAS 39.

- IFRIC 15 Agreements for the Construction of Real Estate: Effective on or after January

1, 2009. - IFRIC 16 Hedges of a Net Investment in a Foreign Operation: Effective for periods

beginning on or after October 1, 2008. - IFRIC 17 Distributions of Non-cash Assets to Owners: Effective beginning on or after

July 1, 2009. - IFRIC 18 Transfers of Assets from Customer: Effective for transfers received on or after

July 1, 2009.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 20 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

- Revisions to certain accounting standards and interpretations previously issued, most of

them applicable internationally for periods beginning on or after January 1, 2009.

The Company’s management has not yet determined the potential effect that those standards, not yet approved by the CNC, might have on the preparation of its financial statements.

(4) Financial Risk Management

The Group’s activities may expose it to a variety of financial risks related to the effects of fluctuations in the debt and equity market prices, fluctuations in foreign exchange, interest rates, and fair values of financial assets and financial liabilities. The Group’s general program for the administration of risks is mainly focused on financial market unpredictability, and seeks to minimize potential adverse effects on the Group’s financial behavior. Administration and Finance Management is in charge of the administration of risk following the policies approved by the Board of Directors. The Administration and Finance Management identifies, evaluates, and covers the financial risks in close cooperation with operating units. (i) Currency risk

The Group's activities and indebtedness in foreign currency exposes it to exchange rate fluctuation risk, specially concerning the U.S. dollar. In order to reduce the Group’s exposure, it conducts efforts to keep an appropriate balancing between assets and liabilities and between income and expenses in foreign currency. Balances in U.S. dollars (US$) as of December 31 are summarized as follows:

In thousands of US$ 2009 2008

Assets: Cash and banks 94,350 18,372 Trade accounts receivable 110,666 107,353 Other accounts receivable 64,546 ) 51,728

---------------- --------------- Net liability position ( 21,712) ( 54,486)

========= =========

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 21 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

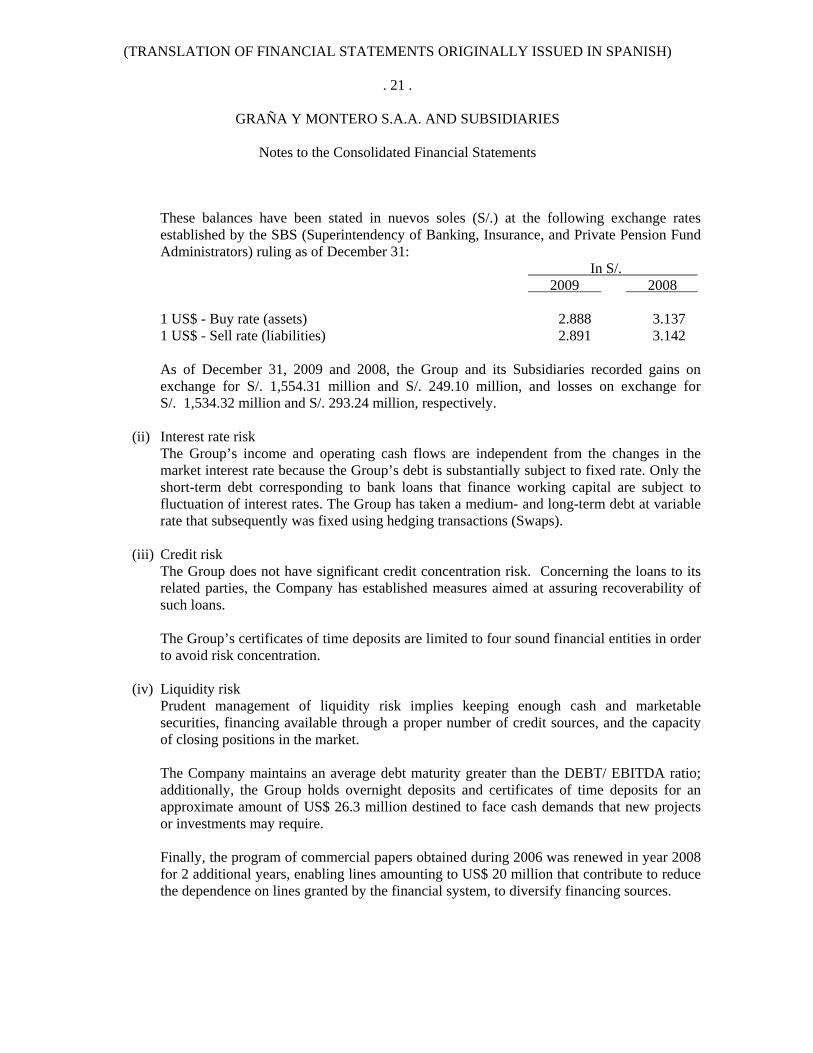

These balances have been stated in nuevos soles (S/.) at the following exchange rates established by the SBS (Superintendency of Banking, Insurance, and Private Pension Fund Administrators) ruling as of December 31:

As of December 31, 2009 and 2008, the Group and its Subsidiaries recorded gains on exchange for S/. 1,554.31 million and S/. 249.10 million, and losses on exchange for S/. 1,534.32 million and S/. 293.24 million, respectively.

(ii) Interest rate risk

The Group’s income and operating cash flows are independent from the changes in the market interest rate because the Group’s debt is substantially subject to fixed rate. Only the short-term debt corresponding to bank loans that finance working capital are subject to fluctuation of interest rates. The Group has taken a medium- and long-term debt at variable rate that subsequently was fixed using hedging transactions (Swaps).

(iii) Credit risk

The Group does not have significant credit concentration risk. Concerning the loans to its related parties, the Company has established measures aimed at assuring recoverability of such loans. The Group’s certificates of time deposits are limited to four sound financial entities in order to avoid risk concentration.

(iv) Liquidity risk

Prudent management of liquidity risk implies keeping enough cash and marketable securities, financing available through a proper number of credit sources, and the capacity of closing positions in the market. The Company maintains an average debt maturity greater than the DEBT/ EBITDA ratio; additionally, the Group holds overnight deposits and certificates of time deposits for an approximate amount of US$ 26.3 million destined to face cash demands that new projects or investments may require. Finally, the program of commercial papers obtained during 2006 was renewed in year 2008 for 2 additional years, enabling lines amounting to US$ 20 million that contribute to reduce the dependence on lines granted by the financial system, to diversify financing sources.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 22 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

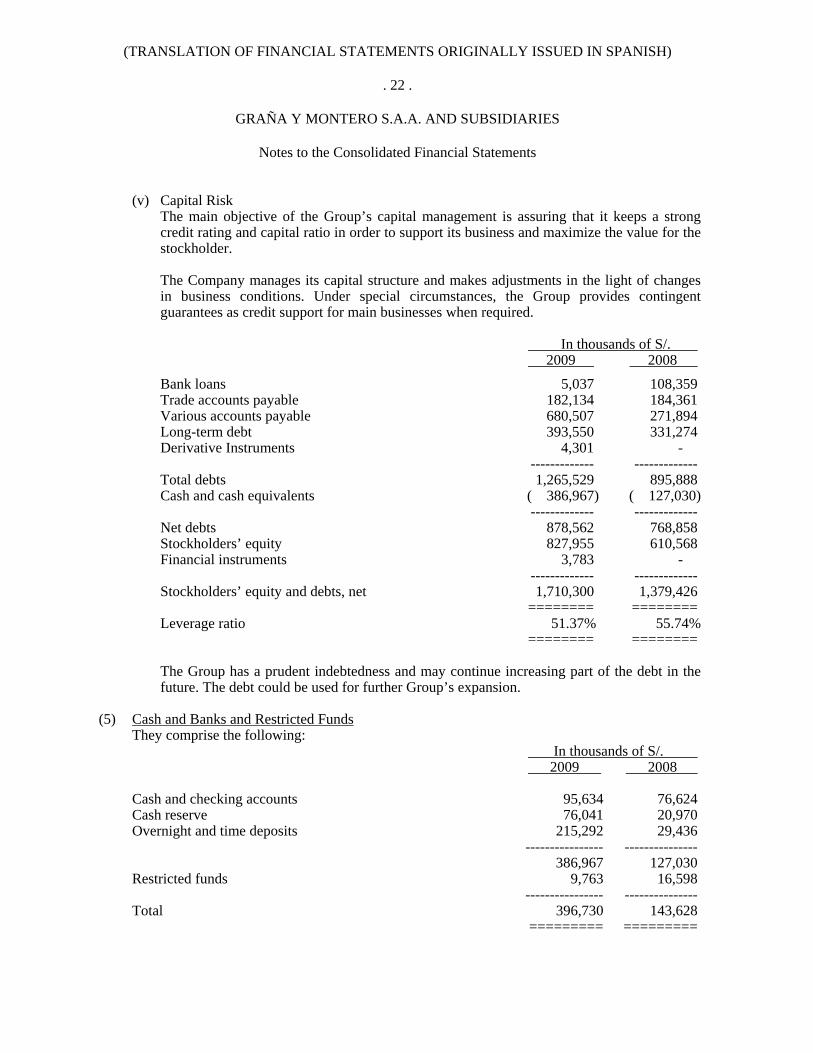

(v) Capital Risk The main objective of the Group’s capital management is assuring that it keeps a strong credit rating and capital ratio in order to support its business and maximize the value for the stockholder. The Company manages its capital structure and makes adjustments in the light of changes in business conditions. Under special circumstances, the Group provides contingent guarantees as credit support for main businesses when required. In thousands of S/. 2009 2008 Bank loans 5,037 108,359 Trade accounts payable 182,134 184,361 Various accounts payable 680,507 271,894 Long-term debt 393,550 331,274 Derivative Instruments 4,301 - ------------- ------------- Total debts 1,265,529 895,888 Cash and cash equivalents ( 386,967) ( 127,030) ------------- ------------- Net debts 878,562 768,858 Stockholders’ equity 827,955 610,568 Financial instruments 3,783 - ------------- ------------- Stockholders’ equity and debts, net 1,710,300 1,379,426 ======== ======== Leverage ratio 51.37% 55.74% ======== ======== The Group has a prudent indebtedness and may continue increasing part of the debt in the future. The debt could be used for further Group’s expansion.

(5) Cash and Banks and Restricted Funds They comprise the following: In thousands of S/. 2009 2008

Cash and checking accounts 95,634 76,624 Cash reserve 76,041 20,970 Overnight and time deposits 215,292 29,436 ---------------- --------------- 386,967 127,030 Restricted funds 9,763 16,598 ---------------- --------------- Total 396,730 143,628

========= =========

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 23 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

As of December 31, 2009, the Group holds checking accounts, cash reserve, and time deposits at local banks in domestic and foreign currency for approximately S/. 133.22 million and US$ 87.86 million at interest rates ranging from 0.10% to 0.20% annually (S/. 64.32 million and US$ 19.99 million, respectively, as of December 31, 2008). As of December 31, 2009, restricted funds mainly includes US$ 3.40 million (US$ 4 million as of December 31, 2008) from subsidiary GMP S.A. held at Banco de Crédito del Perú, to guarantee obligations of a related party.

(6) Trade Accounts Receivable Trade accounts receivable comprise invoices receivable and provisions pending invoicing mainly related to income from work valuations, income from rendered services, and sale of merchandise and property. As of December 31, 2009 and 2008, trade accounts receivable are shown net of advances from clients of S/.109.32 million and S/.110.60 million, respectively. Those invoices receivable have current maturity, do not accrue interest, and do not have specific collaterals. Aging of accounts receivable is as follows:

In thousands of S/. 2009 2008

Current 297,992 341,936 30 days past due 24,557 29,665 Past due over 30 days 7,426 5,879

---------------- --------------- Total 329,975 377,480

========= ========= As of December 31, 2009, trade accounts receivable mainly decreased due to collection of accounts receivable related to stage of completion of the works in the contracts of Concesión Canchaque S.A. for S/. 20.31 million and Survial S.A. for S/. 16.29 million (as of December 31, 2008 S/. 66.97 million and S/. 45.66 million for Concesión Canchaque S.A. and Survial S.A. respectively). Those balances are guaranteed by the Peruvian government once OSITRAN issue the corresponding Certificados de Avance de Obra - CAO (work completion certificates). Likewise, for the collection from Pluspetrol for S/. 10.23 million for the works at Andoas and Topping Plant.

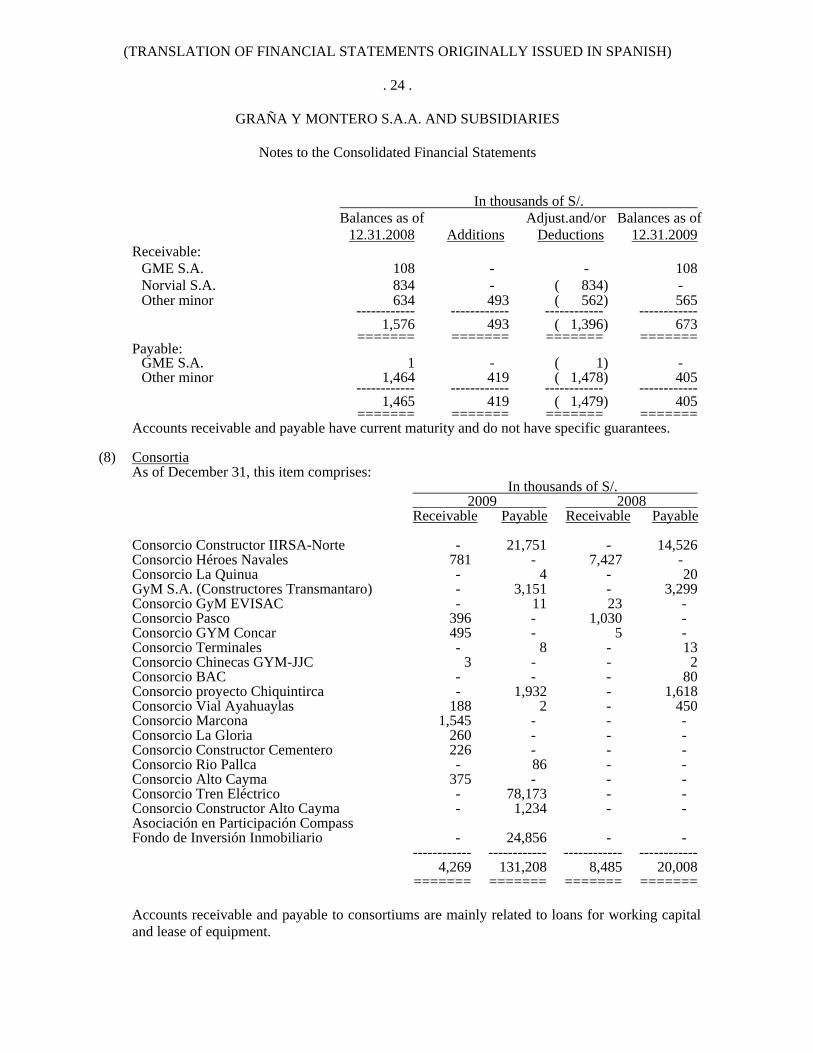

(7) Related Parties The movement of accounts receivable and payable with related parties for the year ended December 31, 2009, is as follows:

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 24 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

In thousands of S/. Balances as of Adjust.and/or Balances as of 12.31.2008 Additions Deductions 12.31.2009

======= ======= ======= ======= Accounts receivable and payable to consortiums are mainly related to loans for working capital and lease of equipment.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 25 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(9) Other Accounts Receivable

They comprise the following: In thousands of S/. 2009 2008

Guarantee deposits for agreements (a) 16,594 16,977 Advances to suppliers (b) 55,661 24,304 Current portion of long-term account receivable (note12) 4,579 4,625 Various (c) 99,637 34,262

---------------- --------------- 176,471 80,168

========= =========

(a) Guarantee deposits as of December 31, 2009 are related to the following works: Hotel Libertador for S/. 5.23 million, Electrical and Instrumentation works for S/. 2.77 milion, BCP computing center for S/. 1.90 million, Construction and remodeling of Centro Cívico for S/. 1.58 million, Building LNG for S/. 1.47 million (Cell-house building for S/. 2.6 million, Upper Level of Capital Building for S/. 2.1 million, Hotel Libertador for S/. 2.1 million, C1 EPC11 Malvinas for S/. 1.8 million, Main Civil Work LNG and Cashiriari civil works for S/. 0.90 million, La Granja tunnel for S/. 1.0 million, Main Civil Works for S/. 1.0 million, Minera Yanacocha for S/. 0.77 million, Rio Tinto Minera Limitada SAC for S/. 0.56 million, Doe Run Perú for S/. 0.32 million as of December 31, 2008).

(b) Advances given to suppliers are related to the following works: Machu Picchu hydropower plant for S/. 21.38 million, Hotel Libertador for S/. 8.7 million, Bayobar phosphate Plant for S/. 5 million, imports and their corresponding procedures for S/. 3.05 million, BCP computing center for S/. 2.29 million, Construction and remodeling of Centro Cívico for S/. 1.94, asphalting of IIRSA Norte for S/. 1.9 million (Consorcio Constructor del Sur for S/. 4.5 million, JJC S.A. for S/. 4.46 million, Golf Millenium for S/. 3.7 million, Buildings LNG for S/. 1.5 million, lease of Block 58 for S/. 1.4 million, Edificio Oficinas Capital for S/. 1.0 million, Topping Plant Huayuri for S/. 1.0 million, Parques de Riva Agüero for S/. 1.1 million, and advances for imports and their corresponding procedures for S/. 2.9 million as of December 31, 2008).

(c) Various accounts receivable as of December 31, 2009 includes mainly the allocation

corresponding to JJC Contratistas Generales for S/. 41.2 million, of the portion of securitized bonds transferred to trust administered by Intertítulos for S/. 15.5 million, leases of equipment and reimbursable expenses receivable from CONIRSA for S/. 4.35 million, the balance of the compensation fund for S/. 3.0 million related to the regulatory framework of the Hydrocarbons Act and reimbursements of expenses of Ingenieros Civiles Contratistas Generales for S/. 1.5 million (regular withholding of securitized bonds for S/. 7.72 million with Intertítulos, the compensation fund for S/. 4.0 million related to the regulatory framework of the Hydrocarbons Act and lease of equipment and reimbursable expenses receivable from CONIRSA for S/. 4.6 million as of December 31, 2008).

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 26 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

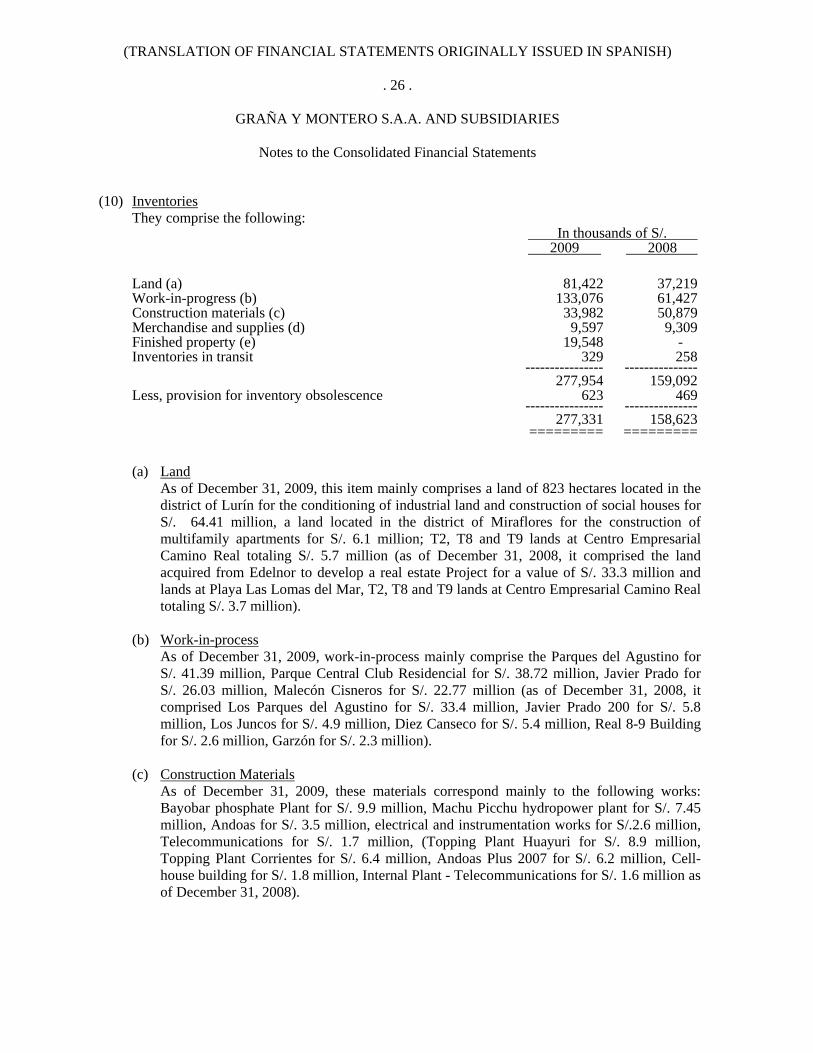

Notes to the Consolidated Financial Statements (10) Inventories

They comprise the following: In thousands of S/. 2009 2008

Land (a) 81,422 37,219 Work-in-progress (b) 133,076 61,427 Construction materials (c) 33,982 50,879 Merchandise and supplies (d) 9,597 9,309 Finished property (e) 19,548 - Inventories in transit 329 )258 ---------------- --------------- 277,954 159,092 Less, provision for inventory obsolescence 623 469 ---------------- ---------------

277,331 158,623 ========= ========= (a) Land As of December 31, 2009, this item mainly comprises a land of 823 hectares located in the

district of Lurín for the conditioning of industrial land and construction of social houses for S/. 64.41 million, a land located in the district of Miraflores for the construction of multifamily apartments for S/. 6.1 million; T2, T8 and T9 lands at Centro Empresarial Camino Real totaling S/. 5.7 million (as of December 31, 2008, it comprised the land acquired from Edelnor to develop a real estate Project for a value of S/. 33.3 million and lands at Playa Las Lomas del Mar, T2, T8 and T9 lands at Centro Empresarial Camino Real totaling S/. 3.7 million).

(b) Work-in-process

As of December 31, 2009, work-in-process mainly comprise the Parques del Agustino for S/. 41.39 million, Parque Central Club Residencial for S/. 38.72 million, Javier Prado for S/. 26.03 million, Malecón Cisneros for S/. 22.77 million (as of December 31, 2008, it comprised Los Parques del Agustino for S/. 33.4 million, Javier Prado 200 for S/. 5.8 million, Los Juncos for S/. 4.9 million, Diez Canseco for S/. 5.4 million, Real 8-9 Building for S/. 2.6 million, Garzón for S/. 2.3 million).

(c) Construction Materials As of December 31, 2009, these materials correspond mainly to the following works: Bayobar phosphate Plant for S/. 9.9 million, Machu Picchu hydropower plant for S/. 7.45 million, Andoas for S/. 3.5 million, electrical and instrumentation works for S/.2.6 million, Telecommunications for S/. 1.7 million, (Topping Plant Huayuri for S/. 8.9 million, Topping Plant Corrientes for S/. 6.4 million, Andoas Plus 2007 for S/. 6.2 million, Cell-house building for S/. 1.8 million, Internal Plant - Telecommunications for S/. 1.6 million as of December 31, 2008).

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 27 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(d) Supplies and Merchandise

They mainly comprise supplies in general for the exploitation of blocks and gas plant of the subsidiary GMP S.A. for S/. 6.19 million, accessories, and supplies in general for maintenance of roads for S/. 1.98 million, computing and telecommunications equipment for S/. 1.43 million (as of December 31, 2008 it comprised supplies in general for the exploitation of blocks and gas plant of the subsidiary GMP S.A. for S/. 3.1 million, accessories, and telecommunications and computing supplies for S/. 2.4 million).

(e) Finished Property

It mainly comprises property at Las Lomas del Mar for S/. 0.67 million and Los Parques del Agustino for S/. 18.88 million.

(11) Prepaid Expenses and Taxes They comprise the following: In thousands of S/. 2009 2008 Sales tax credit (a) 27,427 32,938 Corporate tax credit /Temporary Tax on Net Assets (ITAN) 11,185 12,321 Prepaid insurances 7,153 4,666 Other 4,628 4,822 --------------- --------------- Total 50,393 54,747 ========= ========= Non-current portion of sales tax credit (a) 22,850 - ========= =========

(a) Sales tax credit amounting to S/. 33.32 million is mainly due to the acquisition of goods and services conducted by Concesionaria Survial S.A. during execution of construction. The concessionaire Survial S.A. considers that this tax credit will be compensated with the sales tax arising from transactions levied with such tax. Based on projections for its compensation, management has established a current portion of S/. 10.47 which will be recovered in 2010 economic period.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 28 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

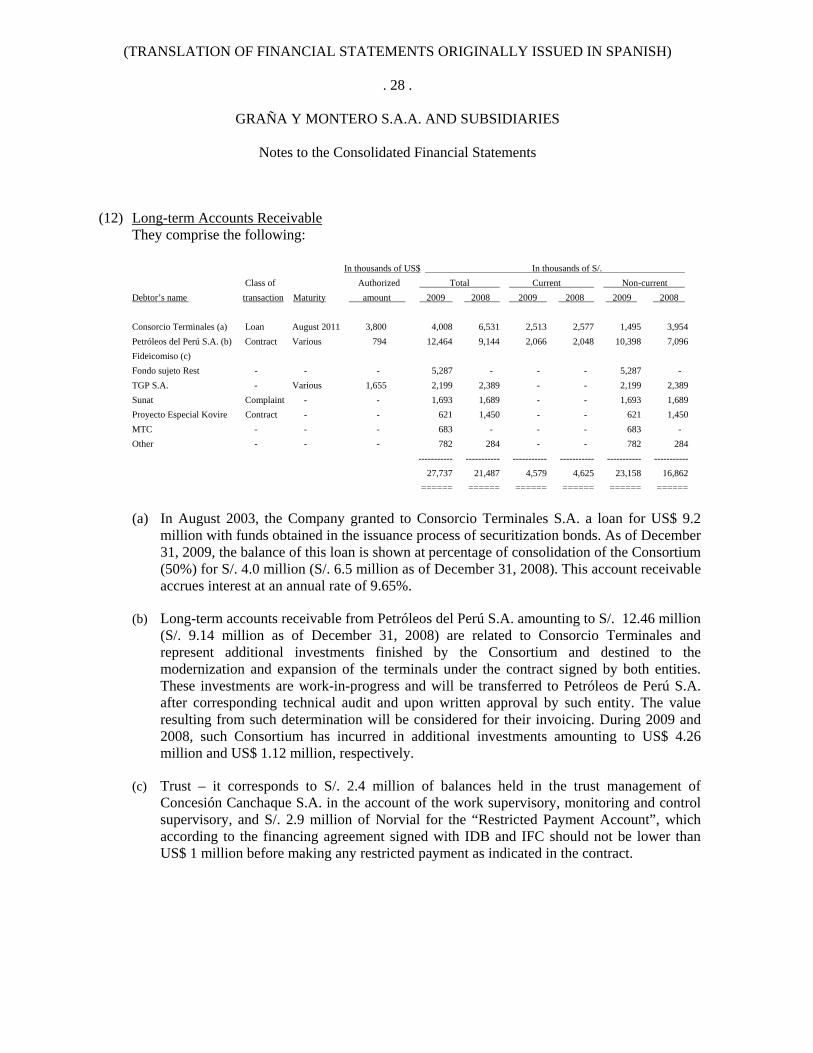

Notes to the Consolidated Financial Statements (12) Long-term Accounts Receivable

They comprise the following: In thousands of US$ In thousands of S/. Class of Authorized Total Current Non-current

(a) In August 2003, the Company granted to Consorcio Terminales S.A. a loan for US$ 9.2

million with funds obtained in the issuance process of securitization bonds. As of December 31, 2009, the balance of this loan is shown at percentage of consolidation of the Consortium (50%) for S/. 4.0 million (S/. 6.5 million as of December 31, 2008). This account receivable accrues interest at an annual rate of 9.65%.

(b) Long-term accounts receivable from Petróleos del Perú S.A. amounting to S/. 12.46 million

(S/. 9.14 million as of December 31, 2008) are related to Consorcio Terminales and represent additional investments finished by the Consortium and destined to the modernization and expansion of the terminals under the contract signed by both entities. These investments are work-in-progress and will be transferred to Petróleos de Perú S.A. after corresponding technical audit and upon written approval by such entity. The value resulting from such determination will be considered for their invoicing. During 2009 and 2008, such Consortium has incurred in additional investments amounting to US$ 4.26 million and US$ 1.12 million, respectively.

(c) Trust – it corresponds to S/. 2.4 million of balances held in the trust management of

Concesión Canchaque S.A. in the account of the work supervisory, monitoring and control supervisory, and S/. 2.9 million of Norvial for the “Restricted Payment Account”, which according to the financing agreement signed with IDB and IFC should not be lower than US$ 1 million before making any restricted payment as indicated in the contract.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 29 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

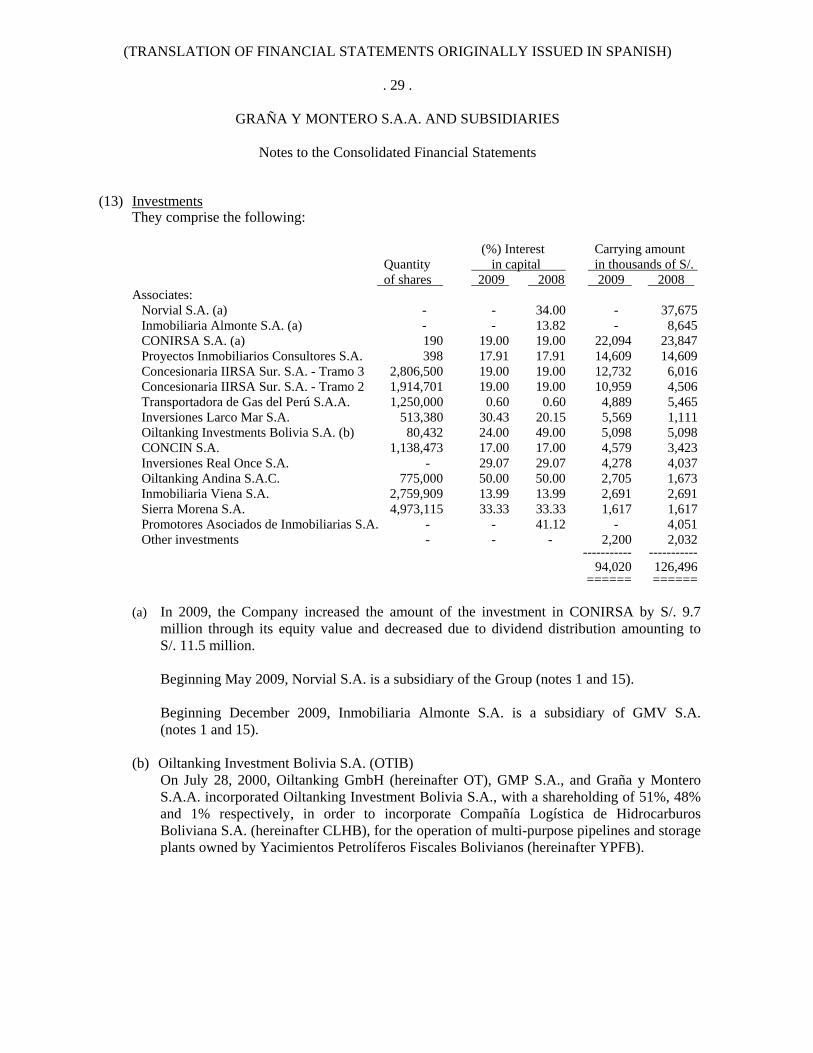

Notes to the Consolidated Financial Statements (13) Investments

They comprise the following:

(%) Interest Carrying amount Quantity in capital in thousands of S/. of shares 2009 2008 2009 2008

(a) In 2009, the Company increased the amount of the investment in CONIRSA by S/. 9.7

million through its equity value and decreased due to dividend distribution amounting to S/. 11.5 million. Beginning May 2009, Norvial S.A. is a subsidiary of the Group (notes 1 and 15). Beginning December 2009, Inmobiliaria Almonte S.A. is a subsidiary of GMV S.A. (notes 1 and 15).

(b) Oiltanking Investment Bolivia S.A. (OTIB) On July 28, 2000, Oiltanking GmbH (hereinafter OT), GMP S.A., and Graña y Montero

S.A.A. incorporated Oiltanking Investment Bolivia S.A., with a shareholding of 51%, 48% and 1% respectively, in order to incorporate Compañía Logística de Hidrocarburos Boliviana S.A. (hereinafter CLHB), for the operation of multi-purpose pipelines and storage plants owned by Yacimientos Petrolíferos Fiscales Bolivianos (hereinafter YPFB).

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 30 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

On May 1, 2006, the Bolivian government enacted Supreme Decree 28701 establishing

“nationalization of hydrocarbons” and demanding oil companies that develop gas and oil production activities in Bolivian territory, to deliver all hydrocarbons production. Through this decree, 50% is adjudicated to YPFB plus 1 share of certain Bolivian companies in which CLHB is included. On September 22, 2009, the Company entered into an agreement whereby the Company gave a term until December 24, 2009 to receive a proposal from the Bolivian Government for the valuation of CLHB. Taking into consideration that no proposal was received until the established term, January 8, 2010, the Company presented an Arbitration Notice before the Permanent Court of Arbitration in The Hague – as set forth in the agreement. This fact, and the term for designation of the arbitrator were previously communicated to the Bolivia’s Ministry of Legal Affairs through our Attorneys, Chadbourne & Parke. On February 12, the new Bolivian Minister of Legal Defense sent a communication in which she did not recognize the agreement. The Company and its partners have decided to continue as plaintiff in the arbitration process, considering that they have enough proofs as to demonstrate that they were correctly communicated through the channel designated by the Government of Bolivia,as well as proofs that the Bolivian Government has benefited from the granted term. Therefore, they are requesting the Presidency of the Legal Court to designate the arbitrator to represent the Government of Bolivia. As of December 31, 2009 and 2008, the financial statements do not include assets, liabilities, income and expenses of OTIB due to jointly loss of control as a consequence of the decrease of its interest, resulting from the nationalization. As of December 31, 2009, the balance of the exposure of the investment in CLHB amounts to S/. 4.8 million.

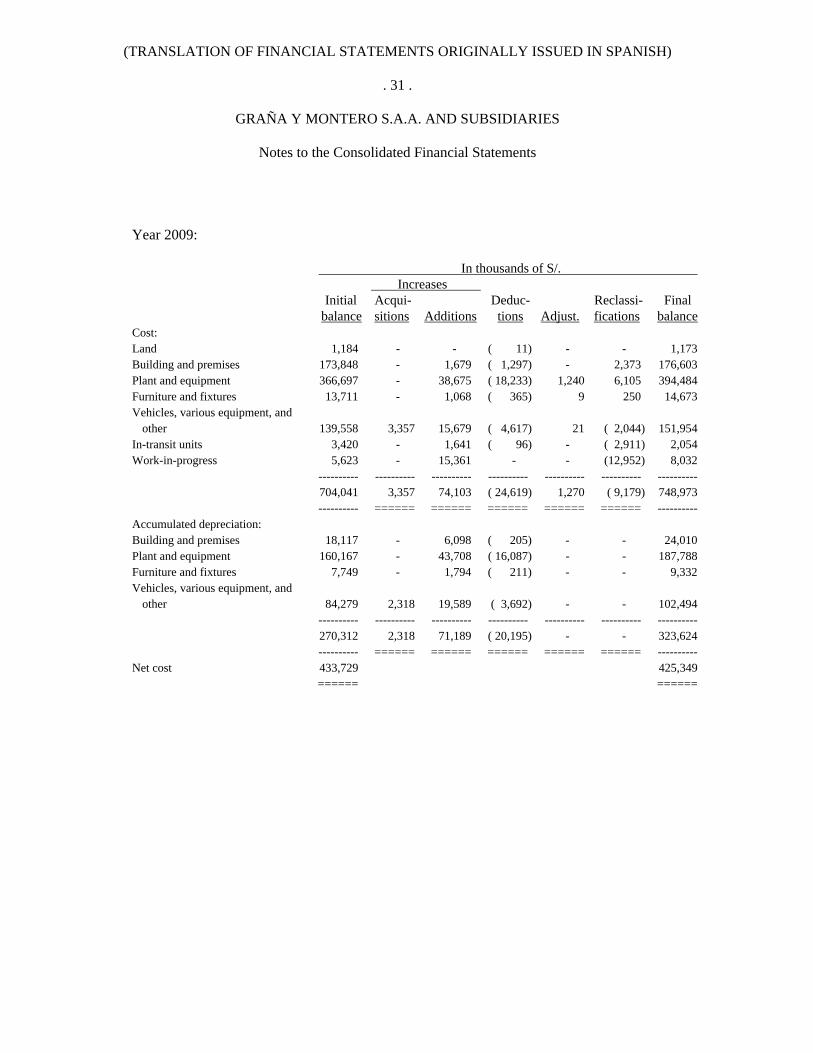

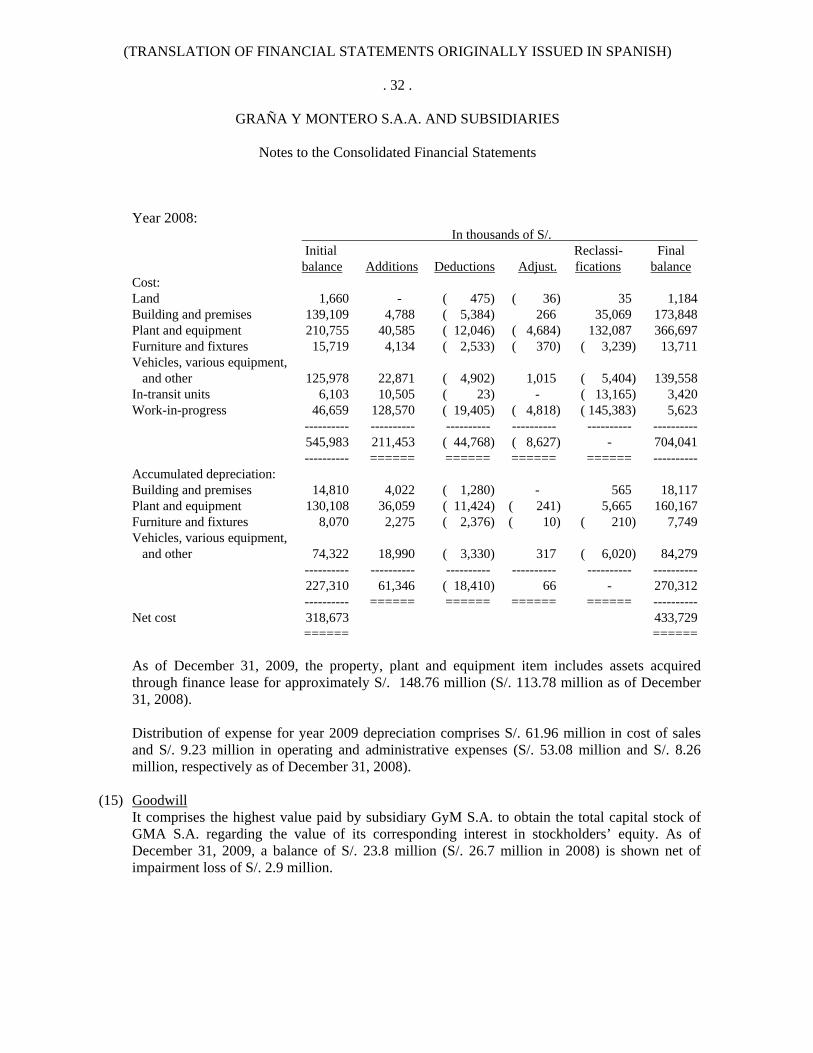

(14) Property, Plant, and Equipment

The movement of the Property, Plant, and Equipment account and the corresponding accumulated depreciation for the period ended December 31, 2009 and 2008 is the following:

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 31 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

Year 2009: In thousands of S/. Increases Initial Acqui- Deduc- Reclassi- Final balance sitions Additions tions Adjust. fications balance Cost: Land 1,184 - - ( 11) - - 1,173 Building and premises 173,848 - 1,679 ( 1,297) - 2,373 176,603 Plant and equipment 366,697 - 38,675 ( 18,233) 1,240 6,105 394,484 Furniture and fixtures 13,711 - 1,068 ( 365) 9 250 14,673 Vehicles, various equipment, and

and other 74,322 18,990 ( 3,330) 317 ( 6,020) 84,279 ---------- ---------- ---------- ---------- ---------- ---------- 227,310 61,346 ( 18,410) 66 - 270,312 ---------- ====== ====== ====== ====== ---------- Net cost 318,673 433,729 ====== ====== As of December 31, 2009, the property, plant and equipment item includes assets acquired through finance lease for approximately S/. 148.76 million (S/. 113.78 million as of December 31, 2008). Distribution of expense for year 2009 depreciation comprises S/. 61.96 million in cost of sales and S/. 9.23 million in operating and administrative expenses (S/. 53.08 million and S/. 8.26 million, respectively as of December 31, 2008).

(15) Goodwill

It comprises the highest value paid by subsidiary GyM S.A. to obtain the total capital stock of GMA S.A. regarding the value of its corresponding interest in stockholders’ equity. As of December 31, 2009, a balance of S/. 23.8 million (S/. 26.7 million in 2008) is shown net of impairment loss of S/. 2.9 million.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 33 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

Increase in the investment in Inmobiliaria Almonte S.A. in year 2009 for S/. 19 million, corresponds to the higher value paid by the subsidiary GMV S.A. This higher value paid is supported in the appraisal of lands of Inmobiliaria Almonte, and will be recovered when the Company’s Proyecto Inmobiliario be developed. Impairment of goodwill was evaluated using the fair value of the subsidiary’s net assets, mainly supported by the appraisal of its evaluation. The results of this evaluation did not determine the impairment of the carrying amount. In May 2009, Graña y Montero S.A.A. acquired 8,876,950 class B shares, belonging to Besco equivalent to 16.1% of total shares representative of capital stock of NORVIAL, increasing its interest from 34% to 50.1%. The take over on Norvial S.A. will allow the Group to incorporate net assets and results from this Subsidiary in line with the Company’s strategy for consolidating long-term stable cash flow business. During the eight (8) months ended December 31, 2009, Norvial S.A. contributed with the net result of S/. 4.1 million. If the acquisition had occurred on January 1, 2009, the Company’s Management estimates that the consolidated revenues would have amounted to S/. 63.5 million and the consolidated net result would have amounted to S/. 6.25 million. The higher value paid for this acquisition in respect to the fair value is a Goodwill equivalent to S/. 19.25 million. The evaluation of the impairment of this goodwill was made using the fair value of concession contract supported by the capacity of its generation of cash. The result of this appraisal did not determined impairment in the carrying amount. In February 2007, Graña y Montero S.A.A. acquired 1,103,509 shares at market value that represented an additional shareholding of 5.47% in the subsidiary GMD S.A., paying an amount of S/. 4.9 million thus increasing its shareholding from 83.21% to 88.68%. The highest value paid on fair value of net assets acquired through this share block was S/. 4.8 million and was recognized as goodwill in the balance sheet. The evaluation of impairment of this goodwill was made using the value in use of the corresponding cash-generating unit. The key criteria for the calculation of the value in use have been: a) projection period: 10 years, b) Growth rate: 6% and perpetual growth up to 3%, and c) discount rate: 11%. The results of this evaluation did not determine impairment in the carrying amount.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 34 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

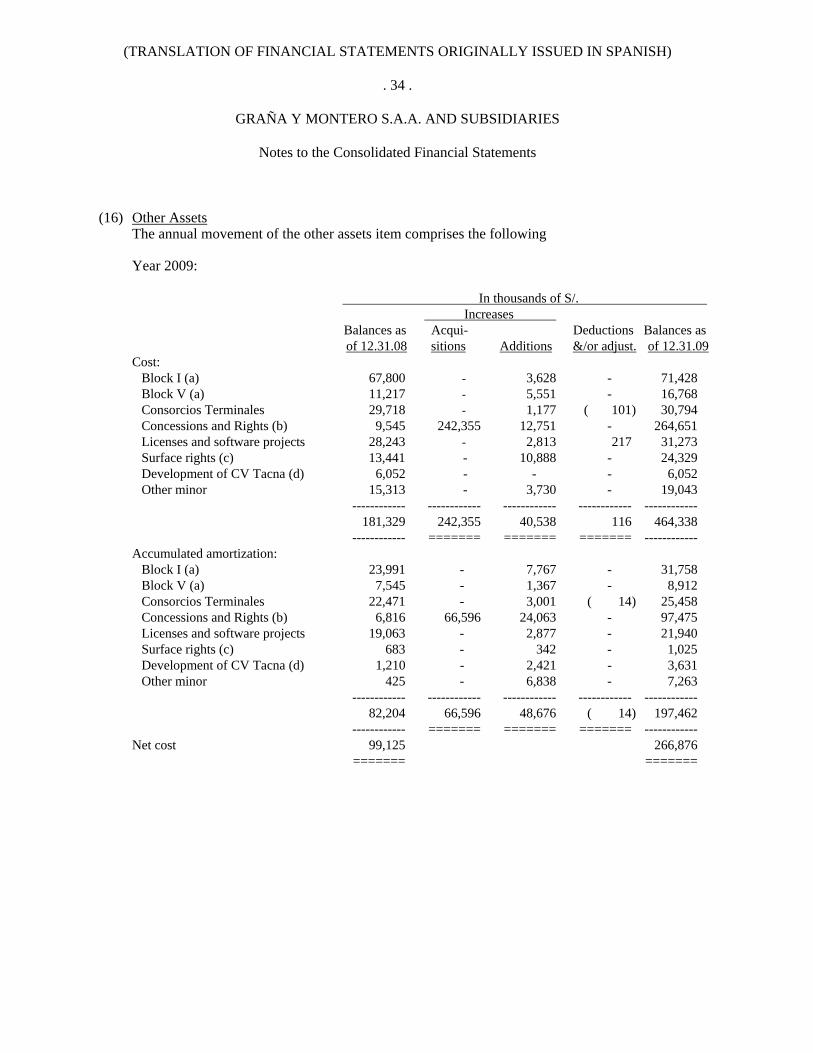

Notes to the Consolidated Financial Statements (16) Other Assets

The annual movement of the other assets item comprises the following

Year 2009:

In thousands of S/. Increases Balances as Acqui- Deductions Balances as of 12.31.08 sitions Additions &/or adjust. of 12.31.09

Cost: Block I (a) 67,800 - 3,628 - 71,428 Block V (a) 11,217 - 5,551 - 16,768 Consorcios Terminales 29,718 - 1,177 ( 101) 30,794 Concessions and Rights (b) 9,545 242,355 12,751 - 264,651 Licenses and software projects 28,243 - 2,813 217 31,273 Surface rights (c) 13,441 - 10,888 - 24,329 Development of CV Tacna (d) 6,052 - - - 6,052 Other minor 15,313 - 3,730 - 19,043

Costs capitalized in the balance of this account are mainly referred to:

(a) Investment expenses in exploration, development and subscription rights obtained through

oil exploitation agreements of blocks I and V and the right obtained for the concession in the administration of oil distribution terminals owned by PETROPERU S.A.

(b) Concessions and rights, mainly comprise intangible assets from Norvial S.A., incorporated

as a consequence of the control obtained by Graña y Montero S.A.A. in period 2009.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 36 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

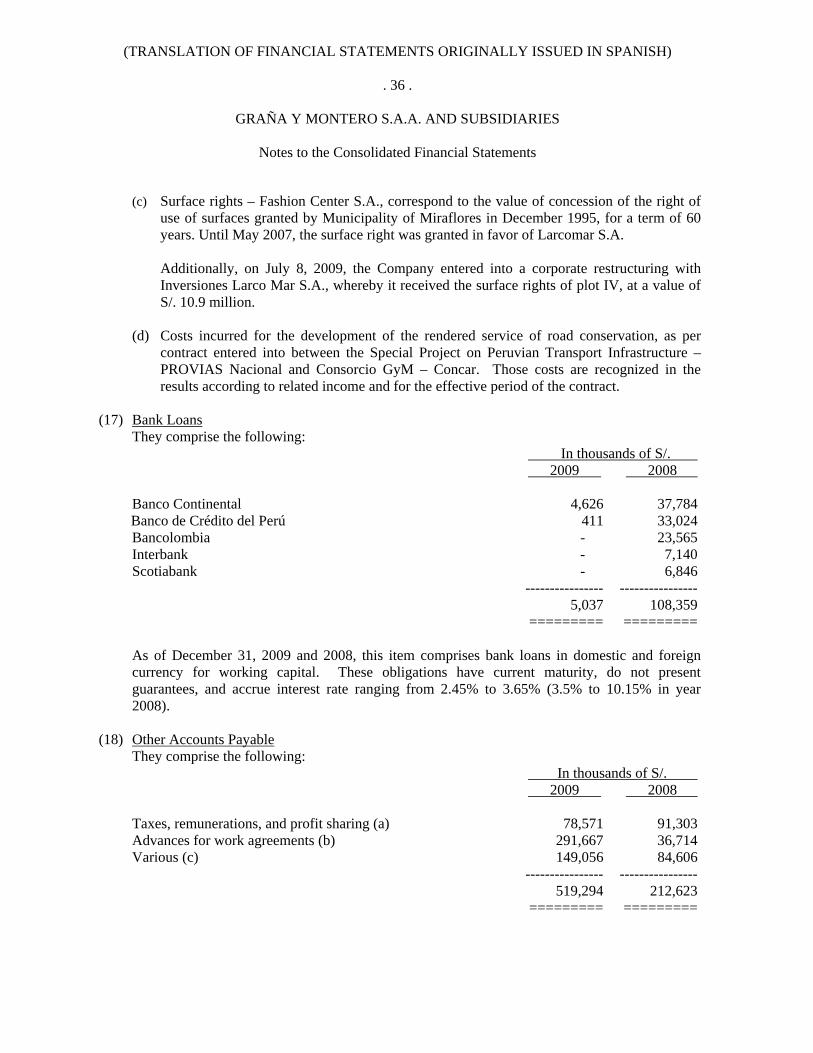

(c) Surface rights – Fashion Center S.A., correspond to the value of concession of the right of use of surfaces granted by Municipality of Miraflores in December 1995, for a term of 60 years. Until May 2007, the surface right was granted in favor of Larcomar S.A.

Additionally, on July 8, 2009, the Company entered into a corporate restructuring with

Inversiones Larco Mar S.A., whereby it received the surface rights of plot IV, at a value of S/. 10.9 million.

(d) Costs incurred for the development of the rendered service of road conservation, as per

contract entered into between the Special Project on Peruvian Transport Infrastructure – PROVIAS Nacional and Consorcio GyM – Concar. Those costs are recognized in the results according to related income and for the effective period of the contract.

(17) Bank Loans

They comprise the following: In thousands of S/. 2009 2008

Banco Continental 4,626 37,784 Banco de Crédito del Perú 411 33,024

As of December 31, 2009 and 2008, this item comprises bank loans in domestic and foreign currency for working capital. These obligations have current maturity, do not present guarantees, and accrue interest rate ranging from 2.45% to 3.65% (3.5% to 10.15% in year 2008).

(18) Other Accounts Payable They comprise the following: In thousands of S/. 2009 2008

Taxes, remunerations, and profit sharing (a) 78,571 91,303 Advances for work agreements (b) 291,667 36,714 Various (c) 149,056 84,606

---------------- ---------------- 519,294 212,623

========= =========

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 37 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

(a) Taxes, remunerations, and profit sharing comprise mainly income tax for S/. 21.89 million,

sales tax for S/. 14.82 million, workers’ profit sharing for S/. 14.38. million, provision for vacations payable for S/. 19.26 million, social contributions and laws for S/. 8.23 million (income tax for S/. 22.62 million, sales tax for S/. 15.82 million, workers’ profit sharing for S/. 10.90 million, provision for vacations payable for S/. 16.53 million, social contributions and laws for S/.13.38 million as of December 31, 2008).

(b) Advances for work contracts correspond mainly to advances received from clients at the

Machu Picchu hydropower plant for S/. 144 million, revenues received from clients for the sale of properties at Parques del Agustino, Edificio Javier Prado and Edificio Malecón Cisneros projects for S/. 66.91 million, from the Ministry of Transport and Communications through the Peruvian Transportation Infrastructure special project (PROVIAS NACIONAL) for S/. 29.18 million, Bayobar phosphate Plant for S/. 20.7 million, Hotel Libertador for S/. 13.2 million, BCP Computing Center for S/. 7.9 million (the Peruvian Transportation Infrastructure special project for S/. 21.26 million, Centro de Distribución NASA UNIQUE for S/. 10 million, Roasting and Acid plant mainly for S/. 8.2 million, Electrical and Instrumentation works for S/. 6.9 million, Building LNG for S/. 5.9 million, Edificio Golf Millenium for S/. 5 million, Concesionaria Vial del Sur S.A. for S/. 1.58 million, Perenco Perú Limited for S/. 0.50 million as of December 31, 2008).

(c) Various accounts payable as of December 31, 2009 mainly comprises balances with JJC for

S/. 66.28 million for contributions to the Joint Venture related to the Buenos Aires – Canchaque highway project and provision for severance indemnities for S/. 5.9 million (S/. 22 million corresponding to Joint Venture in the Buenos Aires – Canchaque highway project, Kontiki beach for S/. 2 million, Besco for S/. 2.2 million and provision for severance indemnities for S/. 5.5 million as of December 31, 2008).

(19) Commercial Papers

During July and November 2009, Graña y Montero S.A.A. settled the commercial papers issued in 2008 for a total of US$ 14 million which were issued to finance own and subsidiaries’ working capital operations. Likewise, during the months of March and August 2009, the Company issued commercial papers for S/. 6 million and US$ 7 million, at an interest rate of 4.2345% and 2.1711% respectively and a maturity of 12 months in the case of both issuances.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 38 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

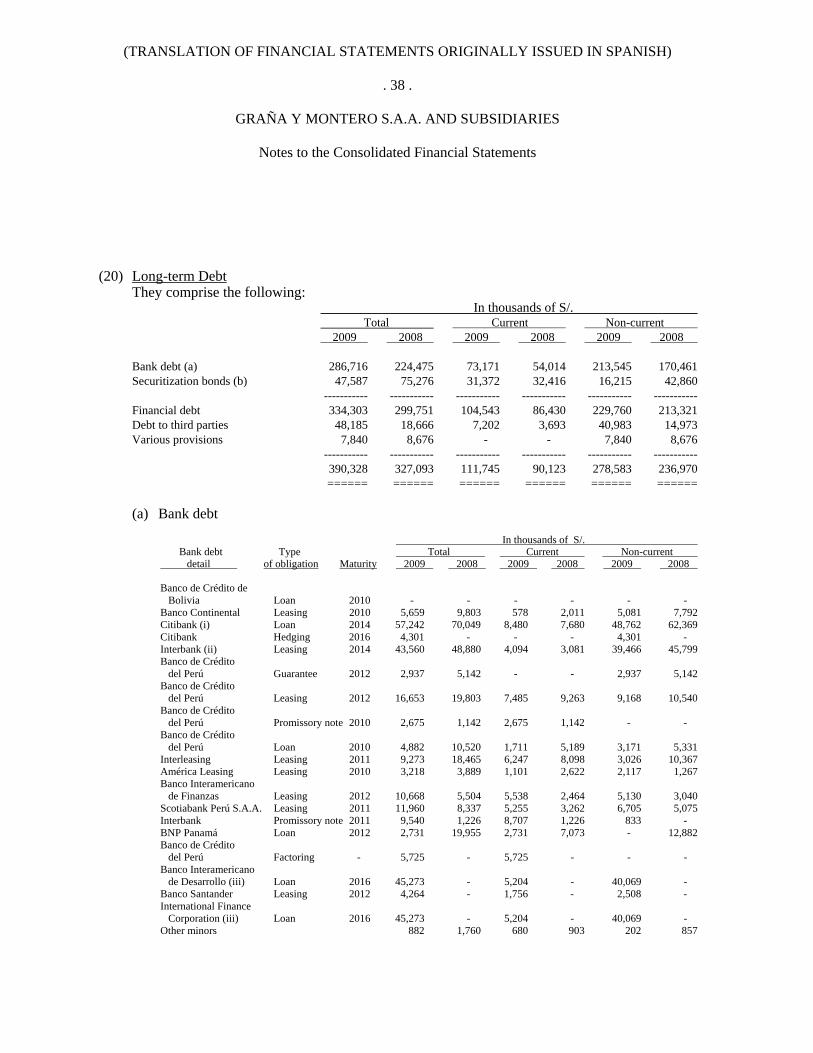

(20) Long-term Debt They comprise the following: In thousands of S/. Total Current Non-current 2009 2008 2009 2008 2009 2008

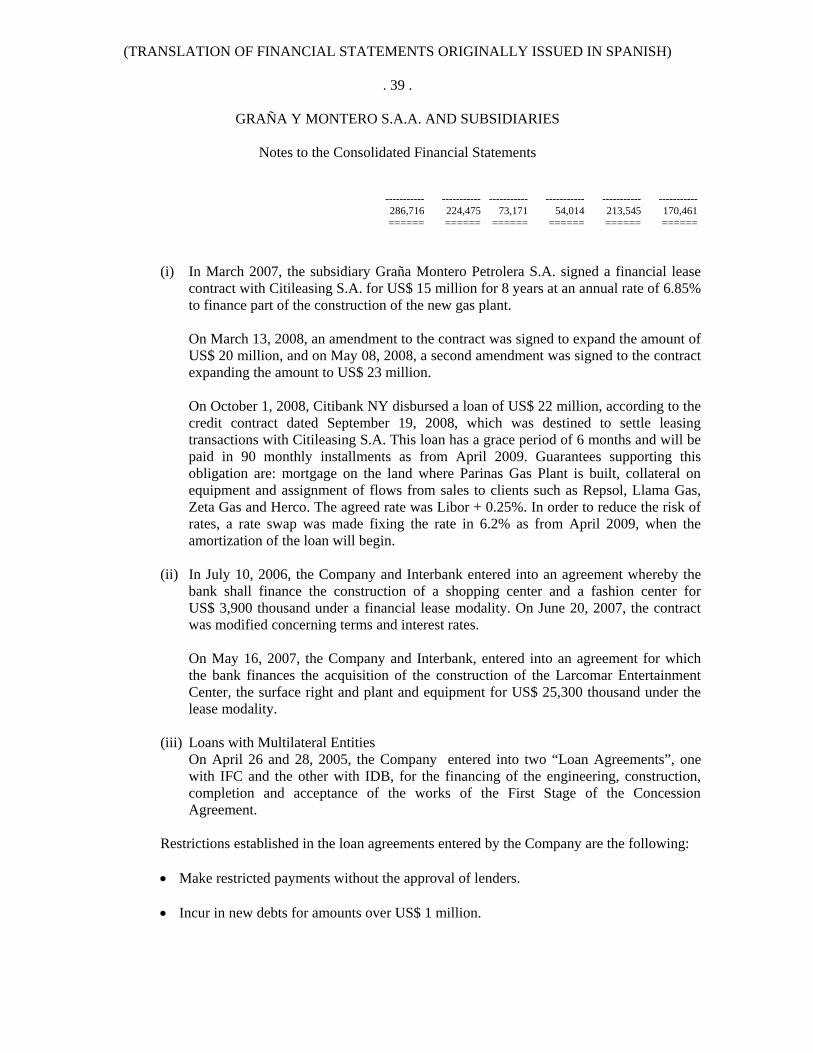

(i) In March 2007, the subsidiary Graña Montero Petrolera S.A. signed a financial lease contract with Citileasing S.A. for US$ 15 million for 8 years at an annual rate of 6.85% to finance part of the construction of the new gas plant.

On March 13, 2008, an amendment to the contract was signed to expand the amount of US$ 20 million, and on May 08, 2008, a second amendment was signed to the contract expanding the amount to US$ 23 million.

On October 1, 2008, Citibank NY disbursed a loan of US$ 22 million, according to the

credit contract dated September 19, 2008, which was destined to settle leasing transactions with Citileasing S.A. This loan has a grace period of 6 months and will be paid in 90 monthly installments as from April 2009. Guarantees supporting this obligation are: mortgage on the land where Parinas Gas Plant is built, collateral on equipment and assignment of flows from sales to clients such as Repsol, Llama Gas, Zeta Gas and Herco. The agreed rate was Libor + 0.25%. In order to reduce the risk of rates, a rate swap was made fixing the rate in 6.2% as from April 2009, when the amortization of the loan will begin.

(ii) In July 10, 2006, the Company and Interbank entered into an agreement whereby the

bank shall finance the construction of a shopping center and a fashion center for US$ 3,900 thousand under a financial lease modality. On June 20, 2007, the contract was modified concerning terms and interest rates. On May 16, 2007, the Company and Interbank, entered into an agreement for which the bank finances the acquisition of the construction of the Larcomar Entertainment Center, the surface right and plant and equipment for US$ 25,300 thousand under the lease modality.

(iii) Loans with Multilateral Entities On April 26 and 28, 2005, the Company entered into two “Loan Agreements”, one

with IFC and the other with IDB, for the financing of the engineering, construction, completion and acceptance of the works of the First Stage of the Concession Agreement.

Restrictions established in the loan agreements entered by the Company are the following:

• Make restricted payments without the approval of lenders. • Incur in new debts for amounts over US$ 1 million.

(TRANSLATION OF FINANCIAL STATEMENTS ORIGINALLY ISSUED IN SPANISH)

. 40 .

GRAÑA Y MONTERO S.A.A. AND SUBSIDIARIES

Notes to the Consolidated Financial Statements

• Create new mortgages in favor of third parties. • Go into partnerships with third parties that shares the Company’s profit.