21

July 2018 GRAÑA Y MONTERO Corporate Presentation

July 2018

GRAÑA Y MONTERO

Corporate Presentation

Business highlights

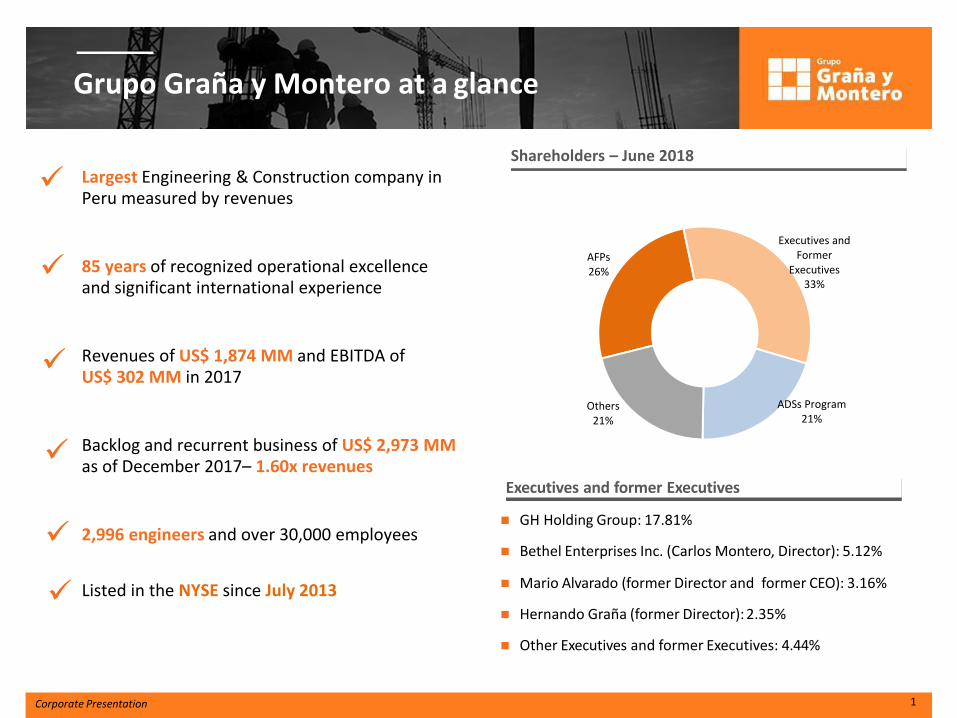

GH Holding Group: 17.81%

Bethel Enterprises Inc. (Carlos Montero, Director): 5.12%

Mario Alvarado (former Director and former CEO): 3.16%

Hernando Graña (former Director): 2.35%

Other Executives and former Executives: 4.44%

Executives and former Executives

Grupo Graña y Montero at a glance

1 Corporate Presentation

Shareholders – June 2018

Largest Engineering & Construction company in Peru measured by revenues

85 years of recognized operational excellence and significant international experience

Revenues of US$ 1,874 MM and EBITDA of US$ 302 MM in 2017

Backlog and recurrent business of US$ 2,973 MM as of December 2017– 1.60x revenues

2,996 engineers and over 30,000 employees

Listed in the NYSE since July 2013

AFPs 26%

Executives and Former

Executives 33%

ADSs Program 21%

Others 21%

Corporate Presentation 1Q2016

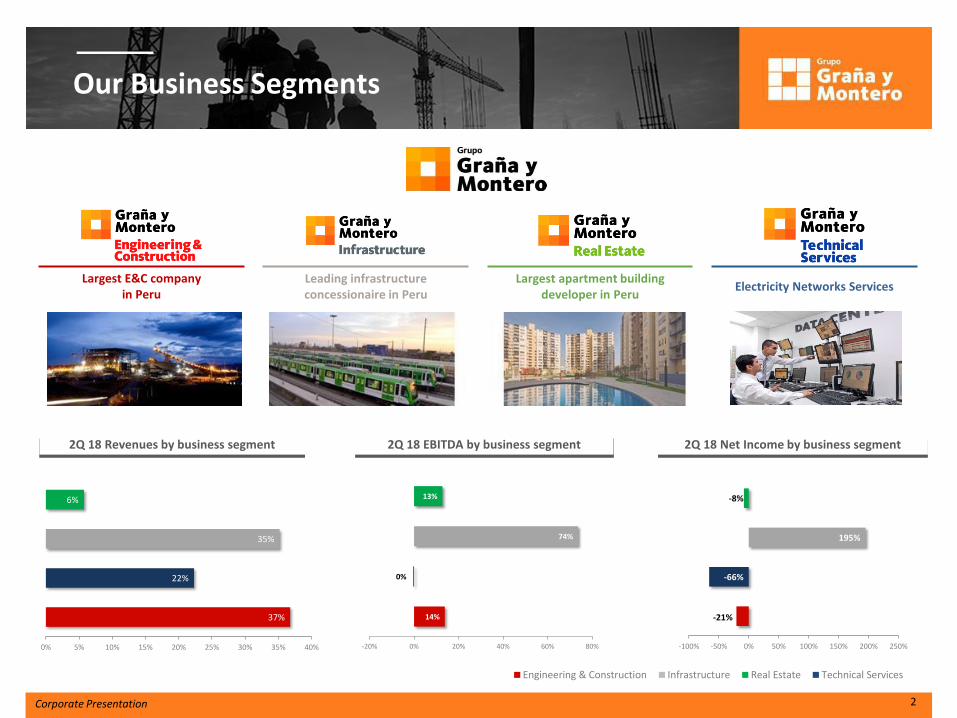

Our Business Segments

2Q 18 Revenues by business segment 2Q 18 Net Income by business segment

Largest E&C company in Peru

Leading infrastructure concessionaire in Peru

Largest apartment building developer in Peru

Electricity Networks Services

2Q 18 EBITDA by business segment

Corporate Presentation

Engineering & Construction Infrastructure Real Estate Technical Services

37%

22%

35%

6%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Ingeniería & Construcción Servicios Infraestructura Inmobiliaria

-21%

-66%

195%

-8%

-100% -50% 0% 50% 100% 150% 200% 250%

Ingeniería & Construcción Servicios Infraestructura Inmobiliaria

14%

0%

74%

13%

-20% 0% 20% 40% 60% 80%

Ingeniería & Construcción Servicios Infraestructura Inmobiliaria

2

Corporate Presentation 1Q2016

Engineering and Construction

Revenues and EBITDA

(S/. in millions)

Main companies:

• GyM: Construction company, founded in 1933, comprised of three divisions:

electromechanic construction, civil construction and building construction.

• GMI: Engineering consulting firm since 1984 consisting in two different divisions:

Supervision & Engineering and Geomatics.

• Vial y Vives- DSD: E&C company formed from a merger between two Chilean

companies, Vial y Vives and DSD Construcciones y Montajes.

• Morelco: Colombian company acquired in 2014, specialized in electromechanical

assemblies, civil works, and services for the oil and gas industry as well as energy

industry.

New contracts during 2018:

• Quellaveco (US$ 52.5 million)

• Talara Refinery (US$ 352.9 million)

• Minera Escondida (US$ 35.7 million)

3 Corporate Presentation

* On April2018, we sold our 87.59% interest in Stracon GyM

4,075

5,036

5,829

4,160

3,353

920

546

459

220

106

194

43

0102030405060708090100110120130140150160170180190200210220230240250260270280290300310320330340350360370380390400410420430440450460470480490500510520530540550560570580590600

0

1,000

2,000

3,000

4,000

5,000

6,000

2013 2014 2015 2016 2017 2Q 18

Mill

are

s

Revenues EBITDA

Corporate Presentation 1Q2016

Infrastructure

Revenues and EBITDA Main companies: • Norvial: Concessionaire of Red Vial 5 Highway

• Survial: Concessionaire of 1st Tranche of the Interoceanic Highway

• Concar: Operation and maintenance of infrastructure assets. It operates more

than 5,000km of Peruvian roads and highways, including three private

concessions, in addition to the Lima Metro

• Canchaque: Concessionaire of the Bs As-Canchaque Highway

• La Chira: Concessionaire for the construction, operation and maintenance of a

waste water treatment plant for Lima

• Ferrovías GyM: Concessionaire of Line 1 of the Lima Metro

• GMP: Oil production (Blocks I, III, IV, V), gas processing plant & operation of

10 fuel terminals in Peru

(S/. in millions)

4

4 Corporate Presentation

1,110

1,2491,353

1,175

1,448

881

262

294

337

299

365

231

0

50

100

150

200

250

300

350

400

-100

100

300

500

700

900

1,100

1,300

1,500

2013 2014 2015 2016 2017 2Q 18

Mill

are

s

Revenues Adjusted EBITDA

Corporate Presentation 1Q2016

Real Estate

Viva GyM: Real estate development company Affordable Housing Projects under execution: Parques del Callao, Parque Comas, Parques de Huancayo Housing Projects under execution: Edificio Klimt (San Isidro), Paul Harris and Pezet *On May 31, 2018, we sold 420 ha of Almonte land.

2013 2014 2015 2016 2017 2Q 2018

Units delivered

1,757 831 833 938 1,418 324

Units sold 1,134 642 903 1,720 1,604 967

Revenues and EBITDA

5 Corporate Presentation

(S/. in millions)

314

225 216

412

648

144135

7398

167

304

400

50

100

150

200

250

300

350

0

100

200

300

400

500

600

700

2013 2014 2015 2016 2017 2Q 18

Mill

are

s

Revenues Adjusted EBITDA

Corporate Presentation 9

Financial Performance

Corporate Presentation 1Q2016

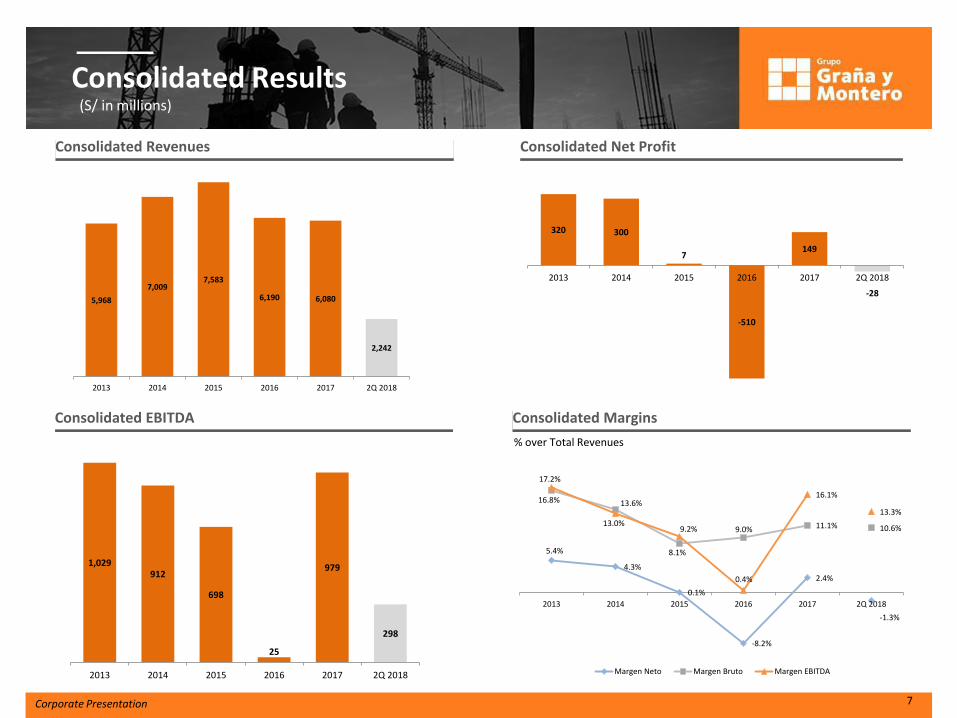

Consolidated Results (S/ in millions)

7

Consolidated EBITDA

Consolidated Net Profit

Consolidated Margins

% over Total Revenues

Consolidated Revenues

Corporate Presentation

5,968

7,0097,583

6,190 6,080

2,242

2013 2014 2015 2016 2017 2Q 2018

320 300

7

-510

149

-28

2013 2014 2015 2016 2017 2Q 2018

1,029912

698

25

979

298

2013 2014 2015 2016 2017 2Q 2018

5.4%

4.3%

0.1%

-8.2%

2.4%

-1.3%

16.8% 13.6%

8.1%

9.0% 11.1% 10.6%

17.2%

13.0%9.2%

0.4%

16.1%

13.3%

2013 2014 2015 2016 2017 2Q 2018

Margen Neto Margen Bruto Margen EBITDA

Corporate Presentation 1Q2016

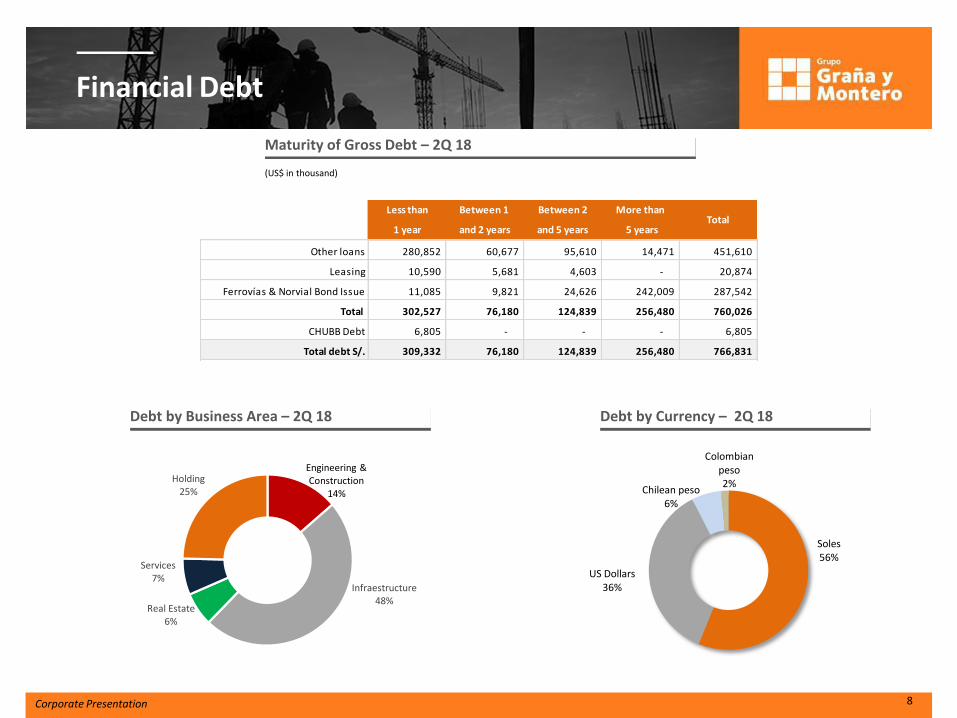

Financial Debt

Debt by Business Area – 2Q 18

Maturity of Gross Debt – 2Q 18

Debt by Currency – 2Q 18

(US$ in thousand)

Corporate Presentation 8

Less than Between 1 Between 2 More than

1 year and 2 years and 5 years 5 years

Other loans 280,852 60,677 95,610 14,471 451,610

Leasing 10,590 5,681 4,603 - 20,874

Ferrovías & Norvial Bond Issue 11,085 9,821 24,626 242,009 287,542

Total 302,527 76,180 124,839 256,480 760,026

CHUBB Debt 6,805 - - - 6,805

Total debt S/. 309,332 76,180 124,839 256,480 766,831

Total

Soles56%

US Dollars36%

Chilean peso6%

Colombian peso2%

Engineering & Construction

14%

Infraestructure48%

Real Estate6%

Services7%

Holding25%

Corporate Presentation 1Q2016

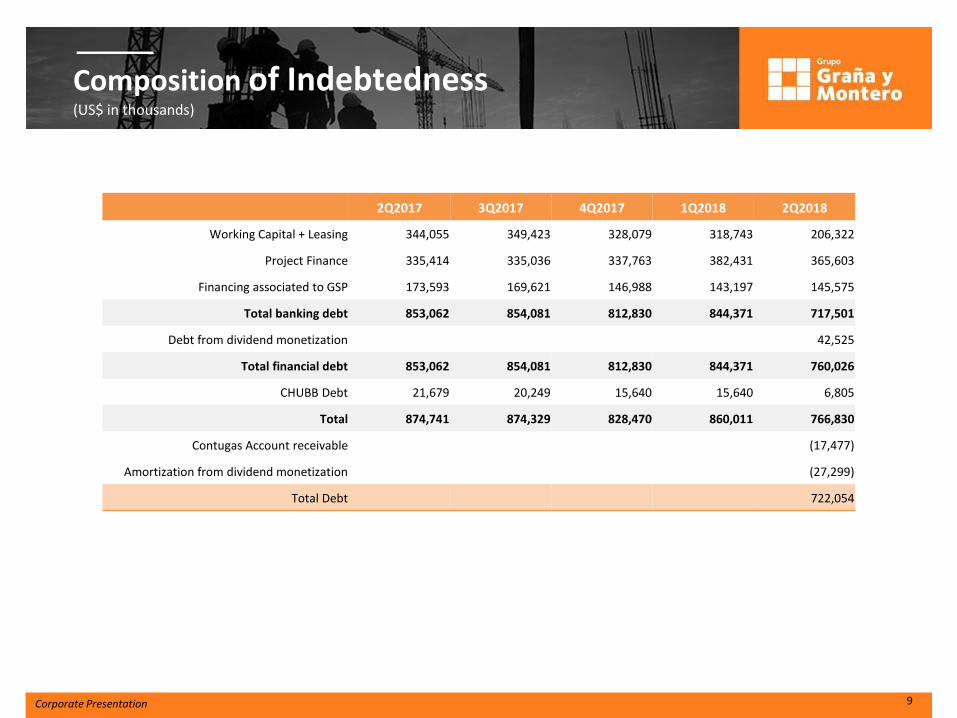

Composition of Indebtedness (US$ in thousands)

9 Corporate Presentation

2Q2017 3Q2017 4Q2017 1Q2018 2Q2018

Working Capital + Leasing 344,055 349,423 328,079 318,743 206,322

Project Finance 335,414 335,036 337,763 382,431 365,603

Financing associated to GSP 173,593 169,621 146,988 143,197 145,575

Total banking debt 853,062 854,081 812,830 844,371 717,501

Debt from dividend monetization 42,525

Total financial debt 853,062 854,081 812,830 844,371 760,026

CHUBB Debt 21,679 20,249 15,640 15,640 6,805

Total 874,741 874,329 828,470 860,011 766,830

Contugas Account receivable (17,477)

Amortization from dividend monetization (27,299)

Total Debt 722,054

Corporate Presentation 1Q2016

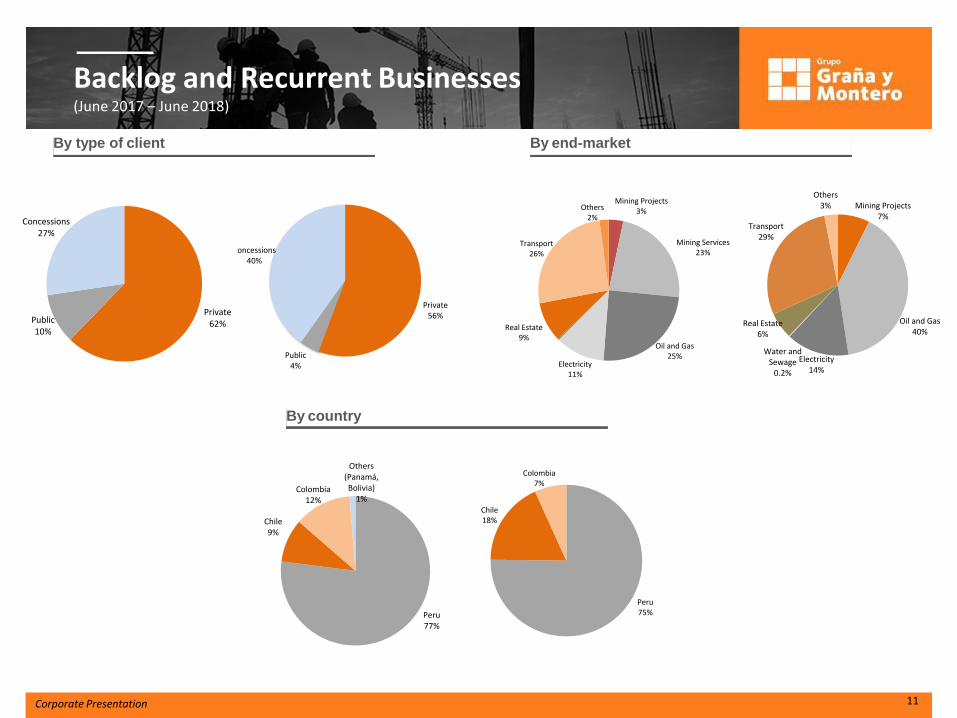

Backlog and Recurrent Businesses (US$ in thousand)

10

By segments

By type of contract (Only E&C)

Total Backlog + Recurrent Businesses

Corporate Presentation

2,602 2,5732,388

1,9701,809

596 609585

630642

1.63 1.59 1.58

1.43

1.59

1.00

1.50

2.00

2.50

3.00

0

1,000

2,000

3,000

4,000

2Q17 3Q17 4Q17 1Q18 2Q18

Backlog Recurrent Bussinesses Backlog + Recurrent Businesses/ Revenues Ratio

3,197 3,182 2,973 2,600 2,451 Engineering & Construction

34%

Infrastructure47%

Real Estate3%

Technical Services

16%

EPC57%

Unit Prices18%

Lump SUM25%

Backlog and Recurrent Businesses (June 2017 – June 2018)

By country

By type of client By end-market

11 Corporate Presentation

Mining Projects7%

Oil and Gas40%

Electricity14%

Water and Sewage

0.2%

Real Estate6%

Transport29%

Others3%

Mining Projects3%

Mining Services23%

Oil and Gas25%

Electricity11%

Real Estate9%

Transport26%

Others2%

Peru75%

Chile18%

Colombia7%

Peru77%

Chile9%

Colombia12%

Others (Panamá, Bolivia)

1%

Private56%

Public4%

Concessions40%

Private62%Public

10%

Concessions27%

Corporate Presentation 1Q2016

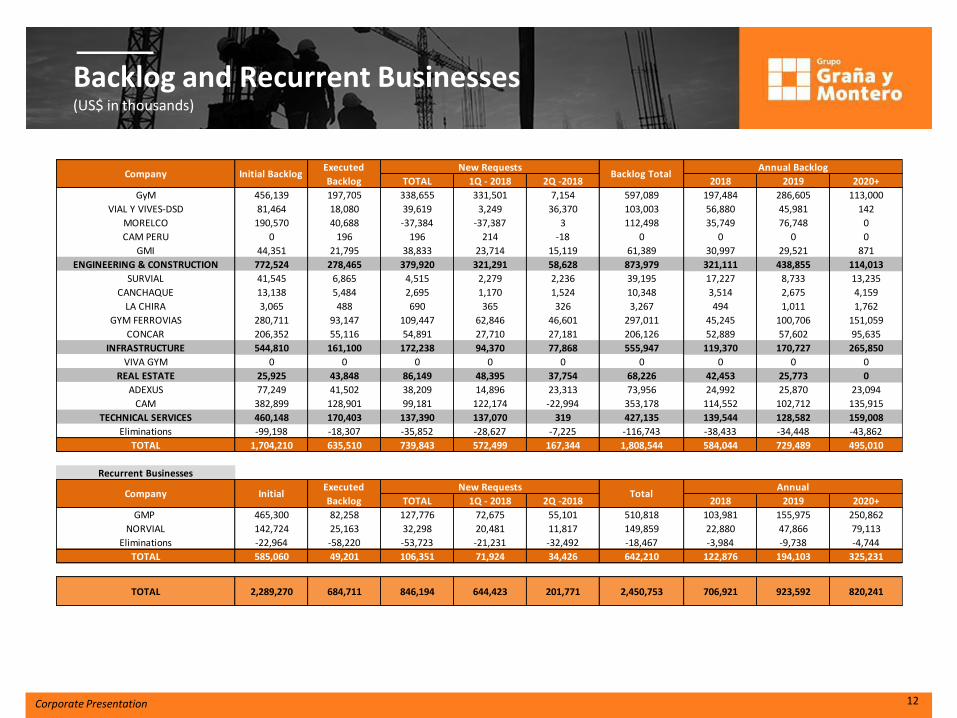

Backlog and Recurrent Businesses (US$ in thousands)

12 Corporate Presentation

TOTAL 1Q - 2018 2Q -2018 2018 2019 2020+

GyM 456,139 197,705 338,655 331,501 7,154 597,089 197,484 286,605 113,000

VIAL Y VIVES-DSD 81,464 18,080 39,619 3,249 36,370 103,003 56,880 45,981 142

MORELCO 190,570 40,688 -37,384 -37,387 3 112,498 35,749 76,748 0

CAM PERU 0 196 196 214 -18 0 0 0 0

GMI 44,351 21,795 38,833 23,714 15,119 61,389 30,997 29,521 871

ENGINEERING & CONSTRUCTION 772,524 278,465 379,920 321,291 58,628 873,979 321,111 438,855 114,013

SURVIAL 41,545 6,865 4,515 2,279 2,236 39,195 17,227 8,733 13,235

CANCHAQUE 13,138 5,484 2,695 1,170 1,524 10,348 3,514 2,675 4,159

LA CHIRA 3,065 488 690 365 326 3,267 494 1,011 1,762

GYM FERROVIAS 280,711 93,147 109,447 62,846 46,601 297,011 45,245 100,706 151,059

CONCAR 206,352 55,116 54,891 27,710 27,181 206,126 52,889 57,602 95,635

INFRASTRUCTURE 544,810 161,100 172,238 94,370 77,868 555,947 119,370 170,727 265,850

VIVA GYM 0 0 0 0 0 0 0 0 0

REAL ESTATE 25,925 43,848 86,149 48,395 37,754 68,226 42,453 25,773 0

ADEXUS 77,249 41,502 38,209 14,896 23,313 73,956 24,992 25,870 23,094

CAM 382,899 128,901 99,181 122,174 -22,994 353,178 114,552 102,712 135,915

TECHNICAL SERVICES 460,148 170,403 137,390 137,070 319 427,135 139,544 128,582 159,008

Eliminations -99,198 -18,307 -35,852 -28,627 -7,225 -116,743 -38,433 -34,448 -43,862

TOTAL 1,704,210 635,510 739,843 572,499 167,344 1,808,544 584,044 729,489 495,010

Recurrent Businesses

TOTAL 1Q - 2018 2Q -2018 2018 2019 2020+

GMP 465,300 82,258 127,776 72,675 55,101 510,818 103,981 155,975 250,862

NORVIAL 142,724 25,163 32,298 20,481 11,817 149,859 22,880 47,866 79,113

Eliminations -22,964 -58,220 -53,723 -21,231 -32,492 -18,467 -3,984 -9,738 -4,744

TOTAL 585,060 49,201 106,351 71,924 34,426 642,210 122,876 194,103 325,231

TOTAL 2,289,270 684,711 846,194 644,423 201,771 2,450,753 706,921 923,592 820,241

Annual Backlog

Company InitialExecuted

Backlog

New RequestsTotal

Annual

Company Initial BacklogExecuted

Backlog

New RequestsBacklog Total

Appendix

8 :0 4 1 / 2 1 0 /2 1 /1 2 1 / t n e m cu

Do 15 d ve

Unsa

Appendix

Corporate Presentation 1Q2016

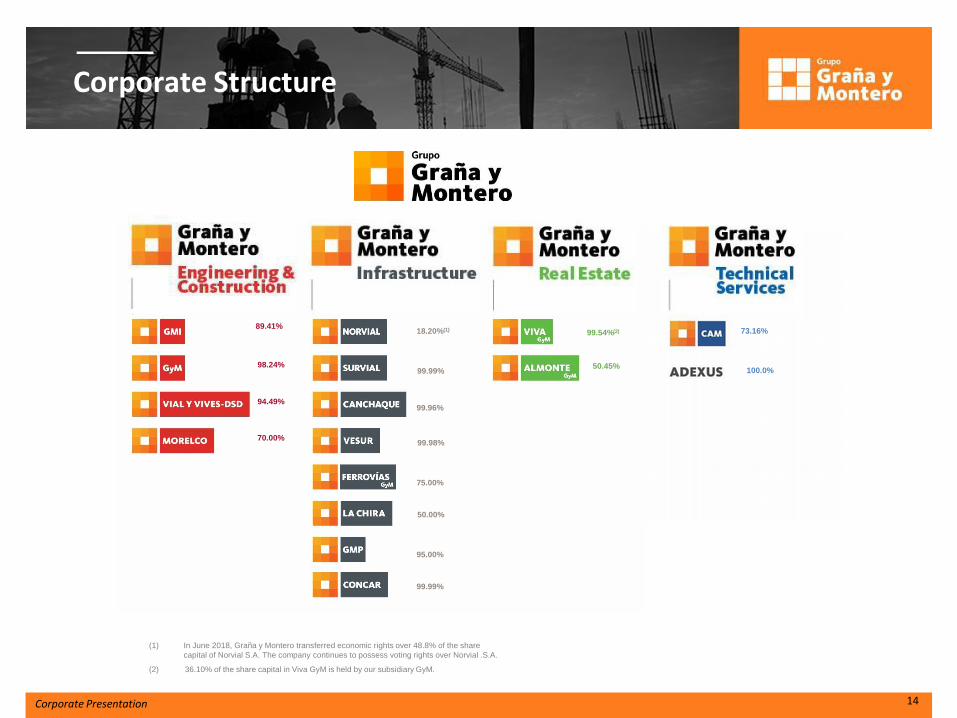

Corporate Structure

14 Corporate Presentation

(1) In June 2018, Graña y Montero transferred economic rights over 48.8% of the share

capital of Norvial S.A. The company continues to possess voting rights over Norvial .S.A.

98.24%

94.49%

70.00%

89.41% 18.20%(1)

99.99%

99.96%

99.98%

75.00%

50.00%

95.00%

99.99%

99.54%(1)

50.45%

99.54%(2)

50.45%

73.16%

100.0%

(2) 36.10% of the share capital in Viva GyM is held by our subsidiary GyM.

Corporate Presentation 1Q2016

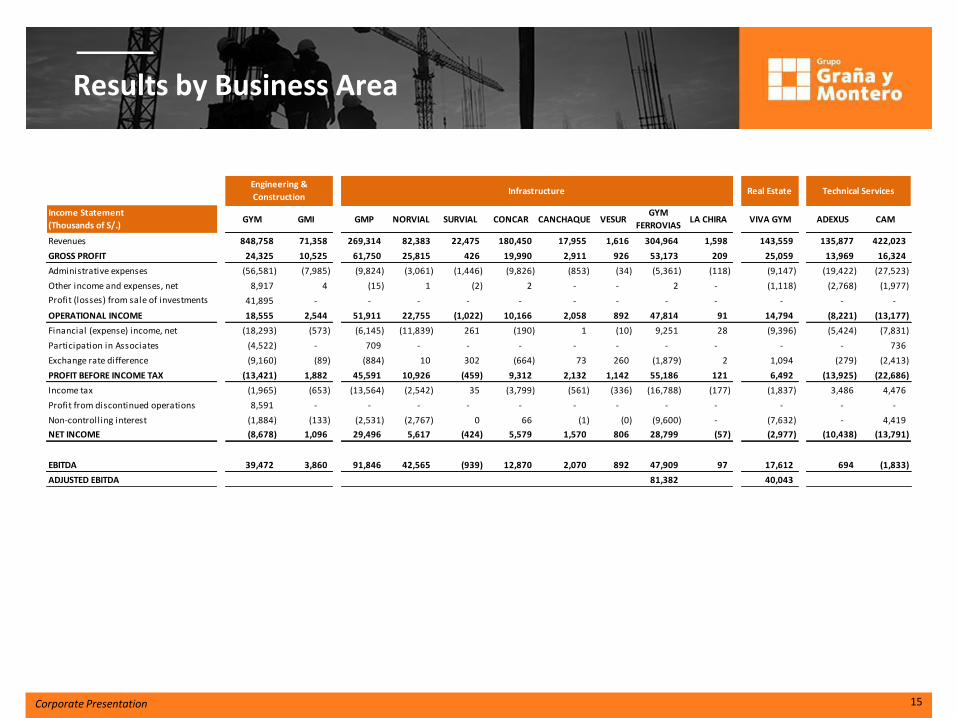

Results by Business Area

Corporate Presentation 15

Revenues 848,758 71,358 269,314 82,383 22,475 180,450 17,955 1,616 304,964 1,598 143,559 135,877 422,023

GROSS PROFIT 24,325 10,525 61,750 25,815 426 19,990 2,911 926 53,173 209 25,059 13,969 16,324

Administrative expenses (56,581) (7,985) (9,824) (3,061) (1,446) (9,826) (853) (34) (5,361) (118) (9,147) (19,422) (27,523)

Other income and expenses, net 8,917 4 (15) 1 (2) 2 - - 2 - (1,118) (2,768) (1,977)

Profit (losses) from sale of investments 41,895 - - - - - - - - - - - -

OPERATIONAL INCOME 18,555 2,544 51,911 22,755 (1,022) 10,166 2,058 892 47,814 91 14,794 (8,221) (13,177)

Financial (expense) income, net (18,293) (573) (6,145) (11,839) 261 (190) 1 (10) 9,251 28 (9,396) (5,424) (7,831)

Participation in Associates (4,522) - 709 - - - - - - - - - 736

Exchange rate difference (9,160) (89) (884) 10 302 (664) 73 260 (1,879) 2 1,094 (279) (2,413)

PROFIT BEFORE INCOME TAX (13,421) 1,882 45,591 10,926 (459) 9,312 2,132 1,142 55,186 121 6,492 (13,925) (22,686)

Income tax (1,965) (653) (13,564) (2,542) 35 (3,799) (561) (336) (16,788) (177) (1,837) 3,486 4,476

Profit from discontinued operations 8,591 - - - - - - - - - - - -

Non-controlling interest (1,884) (133) (2,531) (2,767) 0 66 (1) (0) (9,600) - (7,632) - 4,419

NET INCOME (8,678) 1,096 29,496 5,617 (424) 5,579 1,570 806 28,799 (57) (2,977) (10,438) (13,791)

EBITDA 39,472 3,860 91,846 42,565 (939) 12,870 2,070 892 47,909 97 17,612 694 (1,833)

ADJUSTED EBITDA 81,382 40,043

VESURGYM

FERROVIASCONCAR CAMADEXUSLA CHIRA VIVA GYM

Infrastructure

SURVIAL CANCHAQUEIncome Statement

(Thousands of S/.) GYM GMI GMP NORVIAL

Technical ServicesEngineering &

ConstructionReal Estate

Corporate Presentation 1Q2016

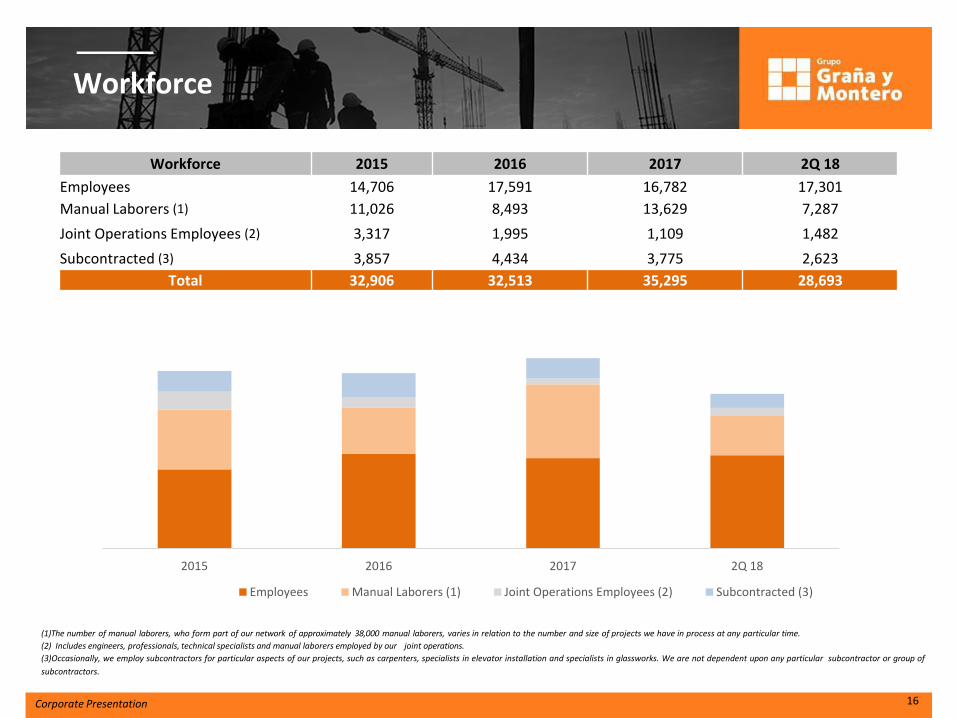

Workforce

(1)The number of manual laborers, who form part of our network of approximately 38,000 manual laborers, varies in relation to the number and size of projects we have in process at any particular time.

(2) Includes engineers, professionals, technical specialists and manual laborers employed by our joint operations.

(3)Occasionally, we employ subcontractors for particular aspects of our projects, such as carpenters, specialists in elevator installation and specialists in glassworks. We are not dependent upon any particular subcontractor or group of

subcontractors.

16 Corporate Presentation

2015 2016 2017 2Q 18

Employees Manual Laborers (1) Joint Operations Employees (2) Subcontracted (3)

Workforce 2015 2016 2017 2Q 18

Employees 14,706 17,591 16,782 17,301

Manual Laborers (1) 11,026 8,493 13,629 7,287

Joint Operations Employees (2) 3,317 1,995 1,109 1,482

Subcontracted (3) 3,857 4,434 3,775 2,623

Total 32,906 32,513 35,295 28,693

Corporate Presentation 1Q2016

• Graña y Montero (GRAMONC1) is listed in the Lima Stock

Exchange since 1997 and in the NYSE since July 2013

(GRAM)

• GRAMONC1 is included in the Corporate Governance Index

of the Lima Stock Exchange

Board of Directors

New Chief Executive Officer, Luis Diaz Olivero, appointed at the Board of Directors meeting on February 27, 2017.

7 of the 9 board members on March 31, 2017 (independent majority) were changed

Modification of the General Regulations of the Board of Directors and creation of the Committee on Risks, Compliance and Sustainability, composed of a majority of external and independent directors

The (I) Audit and Process Committees and (II) Human Board Management Committees are composed exclusively of independent external directors

The (III) Investment Committee is comprised of a majority of independent external directors

Four Operational Committees with at least two independent external directors within their members.

Most of the Subsidiaries of the Group have at least one (1) external director in their Board of Directors

17 Corporate Presentation

Corporate Governance

Non-Independent External Directors

Independent External Directors

Carlos Montero Graña Augusto Baertl Montori

Alfonso García Miró Peschiera Roberto Abusada Salah

Rafael Venegas Vidaurre

Pedro Pablo Errazuriz Dominguez

Alfonso de Orbegoso Baraybar

Manuel del Río Jimenez

Ernesto Balarezo Valdez

Corporate Presentation 1Q2016

Disclaimer

18 Corporate Presentation

Forward-looking statements

This presentation contains forward-looking statements. Forward-looking statements convey our current expectations or forecasts of future events. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to differ materially from the forward-looking statements that we make. Forward-looking statements typically are identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “project,” “plan,” “believe,” “potential,” “continue,” “is/are likely to,” or other similar expressions. Any or all of our forward-looking statements in this presentation may turn out to be inaccurate. Our actual results could differ materially from those contained in forward-looking statements due to a number of factors, including, among others: global macroeconomic conditions, including commodity prices, and economic, political and social conditions in the markets in which we operate, particularly in Peru; major changes in Peruvian government policies at the national, regional or municipal levels, including in connection with infrastructure concessions, investments in infrastructure and affordable housing subsidies; social conflicts in Peru that disrupt infrastructure projects, particularly in the mining sector; interest rate fluctuations, inflation and devaluation or appreciation of the nuevo sol in relation to the U.S. dollar (or other currencies in which we receive revenue); our ability to continue to grow our operations, both in Peru and internationally; the level of capital investments and financings available for infrastructure projects of the types that we perform, both in the private and public sectors; competition in our markets, both from local and international companies; our ability to complete acquisitions on favorable terms or at all and to integrate acquired businesses and manage them effectively post-acquisition; performance under contracts, where a failure to meet schedules, cost estimates or performance targets on a timely basis could result in reduced profit margins or losses and impact our reputation; developments, some of which may be beyond our control, that affect our reputation in our markets, including a deterioration in our safety record; industry-specific operational risks, such as operator errors, mechanical failures and other accidents; availability and costs of energy, raw materials, equipment and labor; our ability to obtain financing on favorable terms; our ability to attract and retain qualified personnel; our ability to enter into joint operations, and rules involved in operating under joint operation or similar arrangements; our exposure to potential liability claims and contract disputes, including as a result of environmental damage alleged to have been caused by our operations; our and our clients’ compliance with environmental, health and safety laws and regulations, and changes in government policies and regulations in the countries in which we operate; negotiations of claims with our clients of cost and schedule variances and change orders on major projects; volatility in global prices of oil and gas; the cyclical nature of some of our business segments; limitations on our ability to operate our concessions profitably, including changes in traffic patterns, and limitations on our ability to obtain new concessions; our ability to accurately estimate the costs of our projects; changes in real estate market prices, customer demand, preference and purchasing power, and financing availability and terms; our ability to obtain zoning and other license requirements for our real estate development; changes in tax laws; natural disasters, severe weather or other events that may adversely impact our business; and certain other factors disclosed in our registration statement on Form F-1 on file with the SEC.

The forward-looking statements in this presentation represent our expectations and forecasts as of the date of this presentation. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date of this presentation. In light of the risks and uncertainties described above, the future events and circumstances discussed in this presentation might not occur and are not guarantees of future performance.

36

Corporate Presentation 1Q2016

Contacts:

Mónica Miloslavich Chief Financial Officer (511) 213 6565 [email protected]

Adriana Caballero Head of Investor Relations (511) 213 6573 [email protected] [email protected] www.granaymontero.com.pe