31

125 CHAPTER CHAPTER CHAPTER CHAPTER-IV IV IV IV GROWTH AND PERFORMANCE OF PUBLIC SECTOR BANKS IN ANDHRA PRADESH AND ANANTAPURAMU DISTRICT

125

CHAPTERCHAPTERCHAPTERCHAPTER----IVIVIVIV

GROWTH AND PERFORMANCE OF

PUBLIC SECTOR BANKS IN ANDHRA

PRADESH AND ANANTAPURAMU

DISTRICT

126

The profile of Andhra Pradesh is presented with reference to Topography &

General features, Topographical Divisions Geographical divisions, climate,

Agriculture, Industry and Minerals, Power, Transport along with Demographic

profile. This section also presents the status of SHGs in Andhra Pradesh.

Topography & General Features

The state of Andhra Pradesh was formed with Kurnool, as its capital on 1st

October, 1953, but Andhra Pradesh was formed in November 1956

comprising the then Telugu speaking regions of Andhra, Telangana and the

former state of Hyderabad. Geometrically, the State lies between the latitudes

120 37 Land 190 54 L North and longitudes 760 46 land 840 46 L East.

Geographically, it occupies the middle portion of the eastern half of the Indian

peninsula with an area of 2,75,068 Sq.km which is 8.4% of the area of the

country. The state has land boundaries with Orissa, Madhya Pradesh and

Chattisgarh on the North Maharashtra and Karnataka on the West; Tamil

Nadu on the South and the Bay of Bengal on the East. Among all the States

of India, Andhra Pradesh has the longest continuous coastline of 974 Km.

There are 23 districts covering 1,126 mandals in Andhra Pradesh out of which

Anantapuramu district is the biggest in terms of area whereas Hyderabad is

the smallest.

Based on physical, social and economic conditions, Andhra Pradesh can be

divided into three regions - Coastal Andhra, Rayalaseema and Telangana.

Coastal Andhra Pradesh comprises of 9 districts viz., Srikakulam, Vizianagaram, Visakhapatnam, East Godavari, West Godavari, Krishna, Guntur, Prakasam and Nellore. The area of Coastal Andhra region is 92,900 Sq. Km. This region has fertile deltas of the rivers Godavari, Krishna and Pennar. A major portion of food and commercial crops that are grown in Andhra Pradesh are from this region. Hence, the coastal Andhra is also known as the Granary of South India. The highest concentration of population is found in this region. There are many industries like Steel Plants, Oil Refinery, Ship building, Bharat Heavy Plates and Vessels, Hindustan Zinc, Coromandel fertilizers etc., in the region Rayalaseema comprises four districts, viz., Chittoor, Kadapa, Kurnool and Anantapuramu. Rayalaseema region extends over an area of 67,400 Sq. Kms. The density of population is low as it is prone to frequent droughts and famines since ancient times. Economically and industrially this region is very backward compared to the other two

127

regions. It comprises of rocky area and infertile soils with very little rainfall. Telangana comprises 10 districts viz., Mahabubnagar, Hyderabad, Ranga Reddy, Medak, Nizamabad, Adilabad, Karimnagar, Warangal, Khammam, and Nalgonda. This region extends to an area of 1,14,800 Sq.Km. Most of the area is covered with dry and barren land. Hence, upland crops are grown with the help of available tank water. However, this region is well-developed industrially.

Topographical Divisions

Topographically 35 % of the area in the State lies below 150 metres altitude

forming the coastal plains. About 15% lies between 150 and 300m and nearly

37% between 300 and 600m both forming the plateau surface comprising

peneplained surfaces. About 13% of the area with an elevation above 600m is

treated as hilly tract, in which 10% lies between 600 and 900m and the

remaining at more than 900m above the sea level.

Geographical Divisions

Geographically, the State can be divided into 3 natural regions. The coastal

plains lie between the Eastern Ghats and the Bay of Bengal, stretching from

Srikakulam district in North to Nellore district in South. The Eastern Ghats lie

between the coastal plains and the western plateau, and begin from

Khondomal – Simlipal hills of Orissa passing through Andhra Pradesh parallel

to the East coast and in a South – West direction and merge with Western

Ghats near Nilgiris of Tamil Nadu (Legris and Meher – Homji. 1982). The

western plateau is an ancient plateau made of rocks of Archaean origin. This

plateau region consists the whole of Telangana region, Anantapuramu and

Kurnool district except Nallamalais.

Climate

The state has tropical monsoon type of climate, which is generally hot and

humid. The climate of the state is classified as tropical rainy climate

represented by all regions of the state except the southwestern portion where

the climate is of Hot-steppe.

Agriculture

Agriculture is the main occupation of about 62 per cent of the people in

Andhra Pradesh.. Rice is a major food crop and staple food of the State

contributing about 77 per cent of the foodgrain production. Other important

128

crops are groundnut, jowar, bajra, maize, ragi, small millets, pulses, castor,

tobacco, cotton and sugarcane. Forests cover 23 per cent of the State's area.

Important forest products are teak, eucalyptus, cashew, bamboo, softwood,

etc.

Industry and Minerals

There are several major industries in operation around Hyderabad and

Visakhapatnam. They manufacture machine tools, synthetic drugs,

pharmaceuticals, heavy electrical machinery, fertilizers, electronic

equipments, aeronautical parts, cement and cement products, chemicals,

asbestos, glass and watches. Andhra Pradesh has the largest deposits of

quality chrysolite asbestos in the country. Other important minerals found in

the state are copper ore, manganese, mica, coal and limestone. The

Singareni Coal Mines supply coal to the entire South India.

Power: Important power projects in the State are: Nagarjuna Sagar and

Neelam Sanjeeva Reddy Sagar (Srisailam Hydel Project), Upper Sileru,

Lower Sileru, Tungabhadra Hydel Projects and Nellore, Ramagundam,

Kothagudem, Vijayawada and Muddanur thermal power projects. The

Srisailam Hydro Electric project (Right Bank) with an installed capacity of 770

MW (Mega Watt) and the Srisailam Left Bank HES Capacity of 900 MW and

the Nagarjuna Sagar Complex with 960 MW are the principal sources of hydel

generation. Vijayawada Thermal power station with an installed capacity of

1,260 MW and Kothagudem Thermal power station with an installed capacity

of 1,200 MW are the main source of thermal power. The 1,000 MW coal-

based Simhadri Thermal power station aims at supplying the entire energy

generated to the State. Installed capacity of the state as on May 2007 is

11668.5 M.W. For massive capacity addition of 7513 MW, 14 new projects

are programmed by AP GENCO during XI Plan (2012).

Transport:

Roads: National Highways passing through Andhra Pradesh constitute 4,674

km. There are 62,110 km of the state roads including 9212 km of state

highways and 1,24,143 km of Panchayathi Raj Roads in the State as on

March 2007.

129

Railways: Of the railways route covering 5,107 km in Andhra Pradesh, 4,633

km is broad-gauge, 637 km is metre-gauge and 37 km is narrow gauge.

Aviation: Important airports in the state are located at Hyderabad, Tirupathi

and Visakhapatnam. International flights are operated from Hyderabad.

Ports : Visakhapatnam is a major port in the State. Minor ports are located at

Kakinada, Machilipatnam, Bheemunipatnam, Krishnapatnam, Vadarevu and

Kalingapatnam..

Tourist Center: Charminar, Salarjung Museum, Golconda Fort in Hyderabad,

Thousand pillar Temple and Fort in Warangal, Sri Lakshmi Narasimha Swamy

Temple at Yadagirigutta, Budda stupa at Nagarjuna Konda and Nagarjuna

Sagar, Sri Venkateswara Temple at Tirumala-Tirupathi, Sri

Mallikarjunaswamy Temple at Srisailam, Kanakadurga Temple at Vijayawada,

Sri Satyanarayanaswamy Temple at Annavaram, Sri Varaha Narasimha

Swami Temple at Simhachalam, Sri Sita Rama Temple at Bhadrachalam,

Araku Valley, Horsley Hills, Nelapattu, etc., are the major tourist attractions in

Andhra Pradesh. Thirty-three life-size statues of eminent Telugu personalities

of the state were erected on Tank-bund of Hussainsagar lake in Hyderabad. .

A giant statue of Lord Buddha of a height of about 60 feet has been erected

on the Gibraltar Rock in the Hussainsagar lake which separates Hyderabad

and Secunderabad cities (Government of India, 2008).

Demographic Profile

The demographic profile of Andhra Pradesh has been presented

in Table 4.1

130

Table 4.1

Profile of Andhra Pradesh

S No. Particulars Male (%) Female (%) Total (%)

1 Number of Households 21022588

2 Population 42442146 42138631 84,580,777

(50.18) (49.82)

3 Population – Rural 28243241 28118461 56361702

(50.11) (49.89) (66.64)

4 Population – Urban 14198905 14020170 28219075

(50.32) (49.68) (33.36)

5 Population (0-6 Years) 4714950 4427852 9142802

(51.57) (48.43) (10.81)

6 S.C. Population 6913047 6965031 13878078

(49.81) (50.19) (16.41)

7 S.T. Population 2969362 2948711 5918073

(50.17) (49.83) (7.00)

8 No. of Literates 28251243 22305517 50556760

(74.88) (59.15) (67.02)

9 No. of Illiterates 14190903 19833114 34024017

(25.12) (40.85) (32.98)

10 Total workers 24185595 15237311 39422906

(56.98) (36.16) (46.61)

11 Main workers 21460081 11577297 33037378

(88.73) (75.98) (83.80)

12 Marginal workers 2725514 3660014 6385528

(11.27) (24.02) (16.20)

13 Non-workers 18256551 26901320 45157871

(43.02) (63.84) (53.39)

14 Cultivators 4357304 2134218 6491522

131

(18.02) (14.01) (16.47)

15 Agricultural Labourers 8130022 8837732 16967754

(33.62) (58.00) (43.04)

16

Workers in Household

Industries 643092 796045 1439137

(2.66) (5.22) (3.65)

17 Other workers 11055177 3469316 14524493

(45.71) (22.77) (36.84)

18 Household size 4.02

19 Sex ratio 993

20 Sex ratio ( 0-6 Years) 939

21 Sex ratio (SC) 1008

22 Sex ratio (ST) 993

Source: Registrar General, Census of India, 2011

As per table 4.1 the total population of the Andhra Pradesh State is

84,580,777. Among them 42,442,146 constituting 50.18 per cent are males

and 42,138,631 constituting 49.82 are females. The sex ratio of the state is

992. In this regard the state occupies third place after Kerala and Tamil Nadu.

But with regard to 0-6 years sex ratio the state stood in 11th place along with

Karnataka and Jharkhand. The population living in rural areas of the state

constitutes 66.64 per cent and the remaining 33.36 per cent population is

living in urban areas. The total child population of the state is 9142802. They

constitute 10.81 per cent of total population. The percentage of male and

female child population is 51.57 and 48.43 respectively. It is pertinent to note

that among the scheduled Castes the female population (6965031) is

outnumbering male (6913047) population. The share of Scheduled caste

population is 16.41 per cent of total state population. The Scheduled Tribes

constitute about 7 per cent of state’s population. The Scheduled Tribe Male

population is 2969362 (50.17) and female population is 2948711(49.83).

The literate population of the state is 50556760. Among them 14190903 are

male literates and 22305517 are female literates. The literacy rate of males

and females is 74.88 per cent and 59.15 per cent respectively. So the male

and female literacy gap is 15.73 per cent in the state. Among illiterates there

is glaring difference between male and females. The total working population

132

of the state is 39422906. Among them 21460081constituting 64.96 are male

and the remaining 15237311 constituting 38.65 are females.

The rural population comprises 72.69 per cent to the total population of the

state. S.C. and S.T. population in the state constitute 16.19 per cent and 6.59

per cent respectively. The number of literates in the State is 3,99,34,323

which constitutes 52.40 per cent of the total population. Among literates there

is glaring difference between male and female literates. Among the total

literates the male and female literates constitute 58.71 per cent and 41.29 per

cent respectively, which shows the backwardness among the total population

of the State. The workers constitute 45.78 per cent among the worker again

male and female workers constitute 62.08 per cent and 37.92 per cent

respectively, which again shows less female participation in the State.

Size of the household is 4.48 in the State. The sex ratio of the State is 978

females per 1000 males. More details however can be seen from Table 2.7

However according to 2011 Census, the State has a total population of

8,46,65,533 out of which men and women constitute 50.21 per cent and 49.79

per cent respectively. Decadal growth rate (1991-2001) is found to be 14.59

against 11.10 for the decade 2001-2011. The sex ratio is found to be 992

females per thousand males. The density of population is 308 per sq.km. The

total literates in the State are 5, 14,38,510 who constitute 67.66 per cent.

Among the literates, the male and female percentage is 55.92 and 44.08

respectively.

Distribution of Commercial Banks

The district wise distribution of all commercial banks in Andhra Pradesh

was shown in table 4.2.

Table- 4.2

District-Wise Distribution of Commercial Banks of All Scheduled

Commercial Banks (As on March 2012) Sl. No District Offices ( in Number)

133

State Bank

of India &

its

Associates

Nationalised

Banks

Foreign

Banks

Regional

Rural

Banks

Private

Sector

Banks

All

Scheduled

Banks 1. Srikakulam 52 67 - 61 14 194

2. Vizianagaram 53 63 - 57 17 190

3. Visakhapatnam 142 210 1 57 54 464

4. East Godavari 133 266 1 24 51 475

5. West Godavari 90 230 - 23 42 385

6. Krishna 129 288 - 53 59 529

7. Guntur 136 224 - 70 47 477

8. Prakasam 70 149 - 65 21 305

9. S.P.S. Nellore 61 136 - 66 23 286

10. Chittoor 66 160 - 94 37 357

11. Y.S.R 70 77 1 78 25 251

12. Anantapuramu 64 110 - 90 44 308

13. Kurnool 77 116 1 75 29 298

14. Mahbubnagar 78 75 - 77 13 243

15. Ranga Reddy 170 261 - 48 125 604

16. Hyderabad 222 495 11 12 198 938

17. Medak 67 78 - 70 20 235

18. Nizamabad 73 87 - 41 20 221

19. Adilabad 58 40 - 78 14 190

20. Karimnagar 77 99 - 57 26 259

21. Warangal 78 97 - 51 37 263

22. Khammam 76 59 - 75 17 227

23. Nalgonda 69 81 - 81 17 248

ANDHRA PRADESH 2,111 3,468 15 1,403 950 7,947

Source: Hand Book of Statistics, 2012-13, Govt. of Andhra Pradesh.

As per table 4.2, there are3,468 nationalised banks in Andhra Pradesh.

Among them 495 banks constituting 14.27 per cent are functioning in the

district of Hyderabad. On the other hand only 40 constituting 1.10 per cent of

nationalized banks branches are working in Adilabad district.

There are 2,111 offices of SBI and its associates. In this regard also

Hyderabad district has lion share of offices. Nearly 10.52 per cent of SBI

134

associates are working in Hyderabad. The lowest number i.e. 52 offices of

SBI associates are functioning in Srikakulam district. There are 15 foreign

banks in the State. Among them 11 constituting 73.33 per cent are

functioning in the Hyderabad district. One each foreign banks are working in

Visakhapatnam, East Godavari, YSR Kadapa and Kurnool district. With

regard to Regional Rural Bank (RRB) offices the Chittoor district is ahead with

94 offices and Hyderabad stood at the lowest rung of ladder with 12 branches.

In the State there are 950 private sector banks in Andhra Pradesh. Again,

with regard to private sector bank branches Hyderabad district occupies first

position with 198 offices. In Mahaboobnagar district only 13 private sector

banks are working.

Deposits

The particulars of Bank group wise deposits of Scheduled Commercial

Banks in the State are given in table 4.3.

135

Table-4.3

Bank Group-Wise Deposits of Scheduled Commercial Banks According to Type of Deposits March 2011

(No. of Accounts in Thousands, Amount in Millions)

Bank Group

CURRENT SAVINGS TERM TOTAL

No. of

Accounts Amount

No. of

Accounts Amount

No. of

Accounts Amount

No. of

Accounts Amount

State Bank of India and its

Associates 490,138 103459.7 22,484,664 297583 3,713,137 529862.1 26,687,939 930904.8

% of A.P. Share 12.79 8.49 13.59 7.38 10.44 8.43 13.03 8.07

Nationalised Banks 1,207,709 128798.2 25,788,308 328602.9 5,228,464 907575.3 32,224,481 1364976.4

% of A.P. Share 5.55 4.07 8.46 4.67 6.67 4.92 7.95 4.76

Foreign Banks 11,559 15594.3 208,742 16678.6 23,388 38465.3 243,689 70738.2

% of A.P. Share 3.83 2.19 7.14 4.19 3.2 3.11 6.16 3.01

Regional Rural Banks 64,423 3836.4 7,286,687 55620.7 1,301,756 75760.7 8,652,866 135217.7

% of A.P. Share 3.8 4.6 7.85 6.16 9.37 11.64 7.98 8.26

Private sector Banks 476,617 95137.8 4,256,590 149126.7 1,072,201 181035.5 5,805,408 425300

136

% of A.P. Share 4.12 6.26 7.36 6.51 5.82 3.06 6.61 4.37

Source: Reserve Bank of India

137

The data in table 4.3 shows that in all categories of banks the number

of accounts and amount is higher with regard savings deposits. The second

and third places were occupied by term and current deposits. With regard to

total number of accounts as well as amount of deposits the nationalised banks

top the list in the state. There are 32, 2224,481 thousand deposit accounts in

nationalised banks. In these accounts an amount of Rs. 13,64,976.4 millions

is saved as deposits. In SBI and its associated there are 26,687,939

thousand deposit accounts. In these accounts an amount of Rs.930,904.8

millions is saved as deposits. In foreign banks there are 243,689 thousand

accounts. In these accounts the deposit amount is Rs.70,738.2 millions. In

Regional Rural Banks, there are 8,652,866 thousand accounts and in these

accounts Rs.135, 217.7 millions was deposit. In private sector banks there

are 5,805,408 accounts and the deposit amount in these accounts is Rs.425,

300 millions.

Deposits and Credit

The details of bank group-wise deposits and credit in Andhra Pradesh

are given in table 4.4.

138

Table - 4.4

Bank Group-Wise Deposits and Credit (Total Credit and Credit of Small Borrowal Accounts) Of Scheduled

Commercial Banks in Andhra Pradesh as on March 2011

(No. of Accounts in Thousands, Amount in Millions)

DEPOSITS TOTAL CREDIT OF WHICH :CREDIT TO

SMALL BORROWERS

No. of

Accounts Amount

No. of

Accounts

Amount

Outstanding

No. of

Accounts

Amount

Outstanding

State Bank of India and its

Associates 26,688 930904.8 4,511 991636.8 3,822 170161.2

% of A.P. Share 13.03 8.07 19.43 11.11 21.41 17.71

Nationalised Banks 32,224 1364976.4 5,431 1608678.2 4,809 227541.0

% of A.P. Share 7.95 4.76 14.05 7.45 15.09 13.82

Foreign Banks 244 70738.2 23 42432.4 16 967.2

% of A.P. Share 6.17 3.01 0.42 2.13 0.35 2.17

Regional Rural Banks 8,653 135217.7 2,923 135149.9 2,831 107218.1

139

% of A.P. Share 7.98 8.26 14.57 13.77 14.73 15.35

Private sector Banks 5,805 425300 1,508 434532.2 1,271 38554.1

% of A.P. Share 6.61 4.37 4.53 5.99 4.44 7.89

All Scheduled Commercial

Banks 73,614 2927137 14,396 3212429 12,749 544441.6

% of A.P. Share 9.09 5.43 11.92 7.88 12.48 14.18

Source: Reserve Bank of India

140

As per table 4.4 there are 26,688 deposit accounts in SBI and its associates.

The amount in these deposit accounts is Rs.930,904.8 millions. In SBI and its

associates there are 4,511thousand accounts and outstanding amount in these

accounts is Rs.991, 636.8 millions. Among them 3,822 accounts are small borrowers’

accounts. Here, also the share of nationalised banks is higher than other category

banks. In these banks there are 32,224 deposit accounts and an amount of Rs.1,

364,976.4 millions is deposited in these accounts. The total credit accounts of

nationalised banks are 5,431. Among them 4,809 accounts are small borrowers’

accounts. The deposit accounts of regional rural banks are Rs. 135,217.7 millions.

There are 73,614 deposit accounts in the state. There are 14,392 credit accounts in the

state and among them 12,749 are small borrowal accounts. The share of state at all

India level is not evenly distributed.

Latest Developments of banking Sector in Andhra Pradesh

At the end of September, 2012, the deposits and advances of Banks in the State stood

at Rs.3, 69,724 crores and Rs.4, 32,712 crores with YoY growth of 19.94% and 24.07%

respectively. As at the end of December, 2012 (provisional), the deposits and advances

stood at Rs.3, 74,730 crores and Rs.4, 47,438 crores with YoY growth of 17.58% and

21.24% respectively.

Credit Deposit Ratio

The CD Ratio of Banks in the State stood at 117.04% as on 30.09.2012 and at 119.40%

as on 31.12.2012(provisional); which continues to be one of the highest in the country.

Performance under Annual Credit Plan 2012-13

Against the annual disbursement target of Rs. 82,167 crores for the year 2012-13 under

the Priority Sector, banks have disbursed Rs. 47,874 crores achieving 58.26% by

30.09.2012 and disbursed Rs.64,592 crores achieving 78.61% by 31.12.2012

(provisional).

Under Agriculture Sector, against the Kharif target of Rs. 31,630 crores, banks have

disbursed Rs. 37,986 crores surpassing the target by Rs.6, 356 crores with an

achievement of 120.09%.

Under Agricultural Production Credit and investment credit, the achievement is 116.75%

and 130.30% respectively.

141

Priority Sector Advances

The Priority Sector advances as at the end of September, 2012 stood at Rs.1, 94,887

crores and Rs. 1, 98,665 crores at the end of December, 2012 (provisional). This

constitutes 49.41per cent of total advances and 50.37% respectively as on 30.09.2012

as on 31.12.2012 (provisional) against the regulatory norm of 40%. YoY growth in

Priority Sector advances was at Rs.31, 972 crores for September, 2012 and Rs.30, 445

crores for December, 2012(provisional). There is need for all Banks to increase their

focus on Priority Sector lending.

Agriculture Advances

The Agriculture advances as at the end of September, 2012 were at Rs.1, 12,062

crores and Rs. 1, 16,927 crores as at the end of December, 2012 (provisional). This

forms 28.41 per cent and 29.65 per cent for and 31.12.2012 (provisional) respectively,

against regulatory prescription of 18 per cent of total advances of 31.03.2012. The

outstanding agricultural credit of the State continues to be one of the highest in the

country.

Extending finance to Licensed Cultivators

It is stated that with a positive outlook, State level Bankers Committee (SLBC) has

approved a target of Rs.2000 for extending finance to the licensed cultivators. As per

the latest information available with SLBC, banks could lend Rs.270.76 crores to LEC

holders.

It is observed that apart from several steering Committee meetings of SLBC, the issue

was also deliberated in the Conference of Joint Collectors and in the meeting it was

decided by the government that in the coming season LECs will be issued well before

the commencement of season by the end of April, 2013. This initiative of Government

needs to be supported by Banks for sustaining Agriculture Sector. The bankers

requested for the support of Government for recovery of earlier dues and in educating

the owner farmers. It is felt that a special meeting of branch managers at mandal/district

level along with Agriculture department officials at the beginning of the season may help

in resolving the issues and go a long way.

142

MSME Sector advances

The outstanding under Micro Small and medium Enterprise (MSME) Sector stood at

Rs.39, 854.86 crores as on 30.09.2012 and Rs. 40,527 crores as on 31.12.2012

(provisional). Under CGTMSE Scheme, banks could extend finance to 17,286 units

amounting to Rs. 543.53 crores during the current year up to 29.01.2013 and the efforts

of banks need to be stepped up for more coverage under the scheme. It is opined that

concerted efforts from District Industries Centers and Industries Associations are also

required for improving performance under the scheme.

Housing Sector

The outstanding credit under Housing Sector was Rs.31, 327 crores as on 30.09.2012

and it was Rs.28, 351 crores as on 31.12.2012 (provisional). In respect of weaker

section housing programs, the Housing Department ensured that at least a few number

of houses may be reallocated in respect of cases where there is mis-utilization and

repayment is not forthcoming so as to create a demonstrative effect as per decision

taken by Government. This will go a long way in improving recovery position of banks

under weaker section housing programmes and will ultimately result in further flow of

credit to this segment.

Education Loans

The outstanding credit under Educational Loans stood at Rs. 5,716 crores as on

30.09.2012 and it was Rs. 5,171 crores as on 31.12.2012 (provisional); as against the

target of Rs.6,780 crores given by Government of India for the year. It is felt that Banks

need to step up the efforts for improving lending to the needy segments.

143

SHG-Bank Linkage Programme

It is clear that banks have lent Rs.6, 352 crores to 2,50,982 SHGs under Rural SHG

segment and Rs.1,447 crores to 54,235 SHGs under Urban SHG segment. The

outstanding credit to SHGs as on 30.09.2012 was at Rs. 16,684 crores and Andhra

Pradesh continues to lead the rest of the country.

The Scheme for financing Women SHGs with the support of Anchor Non Governmental

Organization (NGO) is being implemented in 16 LWE districts of the State. Against the

target for formation of 14,490 SHGs, 4,447 SHGs were formed under the scheme and

efforts are continuing.

Financial Inclusion

Government of India has decided to introduce Direct Benefit Transfer into the bank

accounts of the beneficiaries under various welfare schemes being implemented to start

with, in five pilot districts of Andhra Pradesh and the program was formally launched in

East Godavari district on January 6, 2013.

Financial Literacy Centers (FLCs) and Rural Self Employment Training Institutes (RSETIs)

As per the guidelines of RBI, apart from opening of FLCs in all Lead District Offices,

financial literacy activities are to be taken up by all rural branches of banks. FLCs are

yet to be opened in 11 Lead District Manager (LDM) Offices and the concerned Lead

Banks are requested to take immediate steps for opening. All rural branches need to be

sensitized on taking up financial literacy activities and inform the same to their

controlling offices periodically for submission of report to RBI. Sensitization of bank

branches is required in extending finance to RSETI trained candidates.

Recovery of Bank Loans

It is mentioned that it is needless to mention that unless recovery performance is good,

it may not be possible for Banks to support the financial requirement. To sustain the

144

lead position of the State achieved under Agriculture, SHG, etc. segments efforts are to

be put in place for improving recovery performance. To achieve this the Departments

concerned of the Government have to extend helping hand on recovery front which will

go a long way in improved lending performance by Banks.

Organizational Status of Credit delivery system in Anantapuramu District

The banking system needs to be imparted new ethos to convert into a marked

instrument for the benefit of weaker and under-privileged sections of the community through

mobilization of more deposits, enlargement of credit deployment for achieving higher production

and promotion of banking habit. All this sought to be got through the means of branch

expansion. "The branch expansion is a key factor on the development of the banking sector and

constitutes the first systematic plan effort for overall economic development.”1

The branch expansion programmes has been initiated soon after the completion of initial surveys and identification un-banked and under-banked potential centres. Since the introduction of the Lead Bank Scheme, the branch expansion programme has shown an impressive progress in the district of Anantapuramu. The branch network in district is presented in the Table 4.5. Table 4.5

Branch Expansion S.No

Year Rural Semi- Urban

Urban Total Growth (in %)

1 2000 124 69 34 227 - 2 2001 125 72 34 230 1.32

3 2002 125 72 35 234 1.74

4 2003 125 73 36 234 00

5 2004 130 75 39 244 4.27

6 2005 133 76 47 256 4.92

7 2006 135 79 53 267 4.30

8 2007 135 80 59 274 2.62

9 2008 139 83 67 289 5.47

145

10 2009 142 85 83 310 3.81

11 2010 144 87 90 321 3.55

12 2011 144 87 90 321 00 Source: Annual Credit Plans, Lead Bank Office, Anantapuramu The table 4.5 shows that there were 227 branches in 2000 in Anantapuramu district. This number was increased to 321 branches in 2010.but it is regrettable to note that the expansion of bank branches in rural and semi-urban areas is very less, when compared to urban branches. The urban branches increased more than two times during 11 years of study. During trhe same time, additionally 20 and 18 new branches are opened in rural and semi-urban areas. "The presence of banking in right place half the battle.”2 Division-wise Branch Expansion The division-wise data of branch expansion during 1992-2004 is shown in Table 4.6. Table 4.6 Division Wise Branch Expansion

S. No Year Anantapuramu Dharmavaram Penukonda Total

1 2000 87 54 86 227

2 2001 90 54 86 230

3 2002 90 55 87 232

4 2003 90 55 89 234

5 2004 95 56 93 244

6 2005 98 63 95 256

7 2006 101 69 97 267

8 2007 99 77 98 274

9 2008 108 81 100 289

10 2009 117 90 103 310

11 2010 122 95 104 321

12 2011 122 95 104 321

Source: Annual Credit Plans, Lead Bank Office, Anantapuramu.

146

Table 4.6 reveals that the number of bank branches in all three divisions of the district gradually increased with some variations. During 12 years of study in Anantapuramu division 35 new bank branches are opened. In case of Dharmavaram and Penukonda Revenue Divisions the increase is 41and 18 new branches. It implies that a more number of branches have been opened started in Dharmavaram Revenue Division and Anantapuramu Revenue Divisions compared to Penukonda Revenue Division, besides being a business centre with a good of number of other branches of nationalized banks, the Revenue Division is relatively smaller in size geographically. The per branch population served was 14,400 in 2000 and this ratio to 12,854 population in 2011. These facts reveals that the per branch population coverage is reduced due to expansion of bank branch network. Deposits

Deposits are the main source to the banks and accounted for about 90 per cent of their liabilities. In economic life of any country, deposits play an important role assisting trade, commerce, industry and agriculture. Due to the implementation of the 20 Point Economic Programme of Mrs. Indira Gandhi, mobilization of deposits by the banks has acquired an added significance. The sources of any economic programme entirely depend on channel of credit which compels to make a ceaseless effort for deposits. The lending function of banks is closely associated with the volume of deposits mobilized. No denying fact is that the deposit are vital to the existence of banks, credit merely follows strength. To tap more and more deposits, the banks should have this aim, as B.P. Sarma opined, "No place is too significant and no deposit is too small.”23 An increased lending business depends on increased deposits; and deposit-credit-deposit gets established positive relation. To quote the maxim is worth-saying here: 'Credits' are children of deposits and deposits are children of credits. It holds good even to- day.3 It is worth to note that every advance may not turn up into deposit; but it depends upon the efficient working and wider coverage of banking sector. The banking sector, therefore, is to identify the deposit potential areas before opening branches and the efforts for deposit mobilization should be planned properly on tailor - made basis. It is worth to share the significant view of an economist, I.G. Patel, former Governor of Reserve Bank of India, who spoke at the Public Sector Economic Conference held on 20-21, September, 1981 that "banks create money but do not create saving. And it is savings which makes the economy to run.”4

A significant change has been occurring in savings pattern during past two decades. In the past, the prime motives for savings of an average man for safety, return, and liquidity have how changed to return, tax benefit and liquidity. Towards this, the attributable factors are: Awareness of financial market and its mechanism;

147

Change in living standard, lifestyle, and value system; Rapid industrialization; Monetary policy, incidental tax and tax structure; and Risk forecasting and bearing capacity. This new approach with good customer-service is more pivotal and most urgent for savings channelization. A stiff competition between the institution and within the institution persists. "The secret of success, even in adverse circumstances and stiff competition lies in the formation of a winning team imbued with special feeling: With that winning, we can be assured of a good customer service which is the most important factor in deposit mobilization”5 Deposits mobilization is presented in table 4.7.

148

Table 4.7 Deposit Mobilization (Rs. In lakh)

S.No Year Deposits Variation

Per Branch Deposits

1 2000 122319 - 538.85 2 2001 150696 28377 655.20

3 2002 176628 25932 754.82 4 2003 204536 27908 874.09 5 2004 232544.1 28008.05 953.05 6 2005 292468 59923.95 1142.45 7 2006 295597.1 3129.05 1107.11 8 2007 338490.2 42893.19 1235.37

9 2008 451958.3 113468.1 1563.87 10 2009 576269.25 124311 1858.93 11 2010 662757.5 86488.25 2064.67 12 2011 755718.25 92960.75 2354.26

Source: Annual Credit Plans, Lead Bank Office, Anantapuramu Table 4.7shows that the deposit position of the all commercial banks in Anantapuramu

district, Rs. 122319 lakh in 2000 and Rs. 755718.25 lakh in 2011. The increase of

deposits is to the tune of Rs. 633399.3 lakh. During 2000-2011, the increase of deposits

on an average is worked out Rs. 57581.75 lakh per year. So far as the per branch

mobilization of deposits of the commercial banks is concerned, it is Rs. 538.05 lakh in

2000 which went up to Rs. 2354.26 lakh in 2004.

The analysis on deposits, undoubtedly, disclose that the deposits of the commercial banks have shown a great change in the scale and scope of their development, because of spread of banking habit and saving habit among the people. Credit Deployment Credit is Sine-qua-non for economic growth and development more so in the case of the most backward district of Anantapuramu. Many economists have studied the role of credit in raising production and generating employment opportunities. Rao, Vyas, and Banupratap Singh have opined that the production of enterprise depends on the quantum and quality of credit supplied. Edward, W. Reed has stated thus: "Economic development demands adequate and flexible amount of credit.”30 While saying bank lending is very important input to the economy, Desai has observed that "bank loan called agents of indirect production.” 6

Successful credit management depends on the estimation of credit needs of various sectors as well as sections of the economy. The bank's credit should be responsible and flexible to the every changing needs to the planned economic development. Hence, credit planning is an integral part of economic planning. Estimation of credit demand of

149

various borrowing units of the economy and assessment of availability of funds of lending are the two important characteristic features of a good credit planning. If any difference between two exists, it is termed as 'credit gap'. This will become a cause for underdeveloped economy. The banks should provide loans to the projects, having considerations such as: Acceleration of growth of economy; Employment-oriented and labour-intensive programmes; Exploitation of knowhow without involving foreign collaboration; Benefits which are likely to flow to weaker sections; Export-oriented projects; Projects located in notified no-industry districts and other backward areas; and Projects which are of great importance to the economy. Poverty Alleviation Programmes (PAPs) Lending banking services with the national priority of promoting economic growth and social justice was the call of the day. This led social control over banks in 1967 followed by nationalization of banks in 1969 which were considered landmarks in the growth of Indian banking. In other words, specific programmes designed to alleviate poverty through self-employment and work employment was the main thrust. Accordingly, various poverty alleviation programmes has been adopted to direct the flow of bank credit to the poorer sections of the society. The assistance under this programme comes under priority sector and weaker sections lending. The poverty alleviation programmes in which Lead Bank has been participated are listed and explained in the following paragraphs.

Integrated Rural Development Programme (IRDP)

The (IRDP) was introduced in 1980 by amalgamating various other programmes, like, SFDA, MFAL, DPAP, CADP, etc. The programme has been conceived to achieve the removal of poverty and generation of employment with a sharp focus on target-group comprising small and marginal farmers, agricultural labourers and rural artisans. The banks under IRDP have provided credit in 2002-2004 to the tune of Rs. 543.05 lakh. Differential Rate of Interest Scheme The Differential Rate of Interest (DRI) Scheme was launched in 1972. Under this Scheme, the banks are needed to lend one per cent of total credit. The scheme aims at augmenting the "income of weaker sections by helping them to engage in productive small enterprises with financial support from the banks. The basic objective of this scheme is to render the target groups self- reliant. Assistance is made available under this programme at highly concessional rate

150

of four per cent interest. Under this, by 2003-2004, only 1620 persons were provided credit to the tune of Rs. 259.00 lakh. Credit Package for Rural Women Rural women constitute 76 of total women population of the district indicating that there is a need for development of women. Rural women continue to be backward because they have been trapped in age-old traditions, illiteracy and social set up. They are considered themselves as cheap labour available in not only rural areas but also in semi-urban and urban areas and being paid fewer wages than the men folk. As per present norms at least 5 of credit shall go to women. Owing to special focus given to women, preference is given to women under different poverty alleviation programmes of both State and Central Governments. They are: Under SGSY, SJSRY, PMRY, etc., 40 of the allocation is reserved for women; and Much importance is given to women by assisting SHGs who are economically backward. There are more than 27000 women groups in the district, which are formed by DRDA, NGOs and UNDP. Out of these 20350 groups had been linked since 1999 to 2004 by all the banks in the district. The groups have been assisted by DRDA in the form of revolving fund and matching groups. Even under other general lending, women have been assisted by banks for the purpose of leaf plate making, mat weaving, tailoring, agarbathi making, readymade dress making, cloth business, setting up of STD booths, computer centres, Xerox, bangle and fancy store, petty shops, vegetable vending, soda shops and small hotels etc. Prime Minister's Rojgar Yojana Programme (PMRY) This programme is being implemented since 1993. Persons between age group of 18 to 35 years are eligible for assistance under the scheme. In case of SC/ST and women beneficiaries the upper age limit has been relaxed by 10 years. Similarly, the upper limit of project cost has been increased to Rs. 2.00 lakh in case of activities other than business. The PMRY would now cover all eligible activities including agriculture and allied activities but excluding (i). direct agricultural operations like raising crops, purchase of manure etc., (ii). Demand for loans under PMRY existed mainly for business/retail trade, where the scope for its mis-utilisation is very high. The programme is implemented by District Industrial Centre. Subsidy is 15 of project cost with a maximum of Rs. 7500 and beneficiary contribution is 5%. As per the guidelines form the Central Government, Prime Minister's RojgarYojana is implemented in the District by the District Industrial Centre and Bankers. During 2003-04 the district's target was 1291 units, against which disbursements were 1072. Priority Sector Credit The priority sector credit programme started with the social control over commercial banks in 1968. With the nationalization of commercial banks in 1969, a new era has

151

started in credit interest scheme; the advances should be at one per cent of the priority sector credit. With highlights from the priority sector concept that a major portion of priority sector credit is to lend to agriculture. This is a welcome feature of rural economy. "Neglect of agriculture was pinpointed as one of the failings of our banking sector, and therefore, at the time of nationalization of banks, it was hoped that they will pay more attention to the agriculture".7 An active as well as efficient role of Lead Bank can be visualized by the share of the priority sector credit to the total bank credit. The data credit deployment is provided in Table 4.8.

152

Table 4.8 Priority Sector Credit

S.No

Year Agriculture SSI Tertiary

Total priority sector credit

Total bank credit

% of priority sector loan to total bank credit

1 2000 31849.26 3654.42 3142.74 38646.42 106256.38 36.37 2 2001 31756.57 3743.84 3152.62 35653.03 116576.00 33.16

3 2002 34285.73 3894.34 3387.64 41567.71 127306.00 32.65 4 2003 41568.45 4457.21 3974.63 50000.29 145260.00 34.42 5 2004 5269.87 4867.34 61349.68 61349.68 172976.00 35.47 6 2005 68824.45 5304.00 12576.60 86959.58 191587.65 35.65 7 2006 73457.00 5366.50 18094.00 101738.52 201834.52 36.23 8 2007 89138.00 5525.20 12903.00 123451.26 212589.30 36.51

9 2008 115042.00 6127.00 21126.00 164740.00 214586.25 37.54 10 2009 138226.00 8237.00 23831.25 170294.20 223721.50 38.01 11 2010 175164.23 14558.26 20021.54 182456.25 248256.20 38.76 12 2011 210650.21 22569.00 36579.38 198471.50 253421.20 39.25

Source: Annual Credit Plans, Lead Bank Office, Anantapuramu Table 4.8 clearly explains that the total bank credit has increased by Rs. 106256.38 lakh in 2000 to Rs. 253421.20 in 2011, the agriculture loan has increased from Rs. 31849.26 lakh in 2000 to Rs. 210650.21 lakh in 2011. This growth is accounted for 7.1 times. In the case of small scale sector, the banks have provided an amount of Rs. 3654.42 lakh in 2000 which was increased to Rs. 22569 lakh in 2011. This increase is accounted for more than 7 times. All the banks put together provided credit to the tune of Rs.3142.74 lakh in 2000 and Rs. 36579.38 lakh in 2011 to the tertiary sector, implying the fact that it went up more than 11 times is observed. From this analysis, it is noticed that the bank's performance in credit distribution is better in the case agriculture sector followed by small scale sector while it is negligible in tertiary sector. Credit Deposit Ratio Credit- deposit ratio is referred to the amount of credit sanctioned in a region or state deposits mobilized from that region or state. The credit-deposit ratio explains the degree to which a region or State has benefited from the bank credit out of its deposits from that region or state. "Credit-deposit ratio is the yardstick which reflects all operations of the bank and also influences operational efficiency.8 It is therefore, a tool to measure the banking business. Raghavareddy and Dakshina Murthy have described the credit- deposit ratio thus: "It is a shorthand description of the relationship between the two stock variables at any point of time.9 Growth and development of economy is a requisite, but this should be with social aim. Obviously, this led the bank nationalization in the country. A great economist, Gunnar Myrdal, has appropriately said on the functioning

153

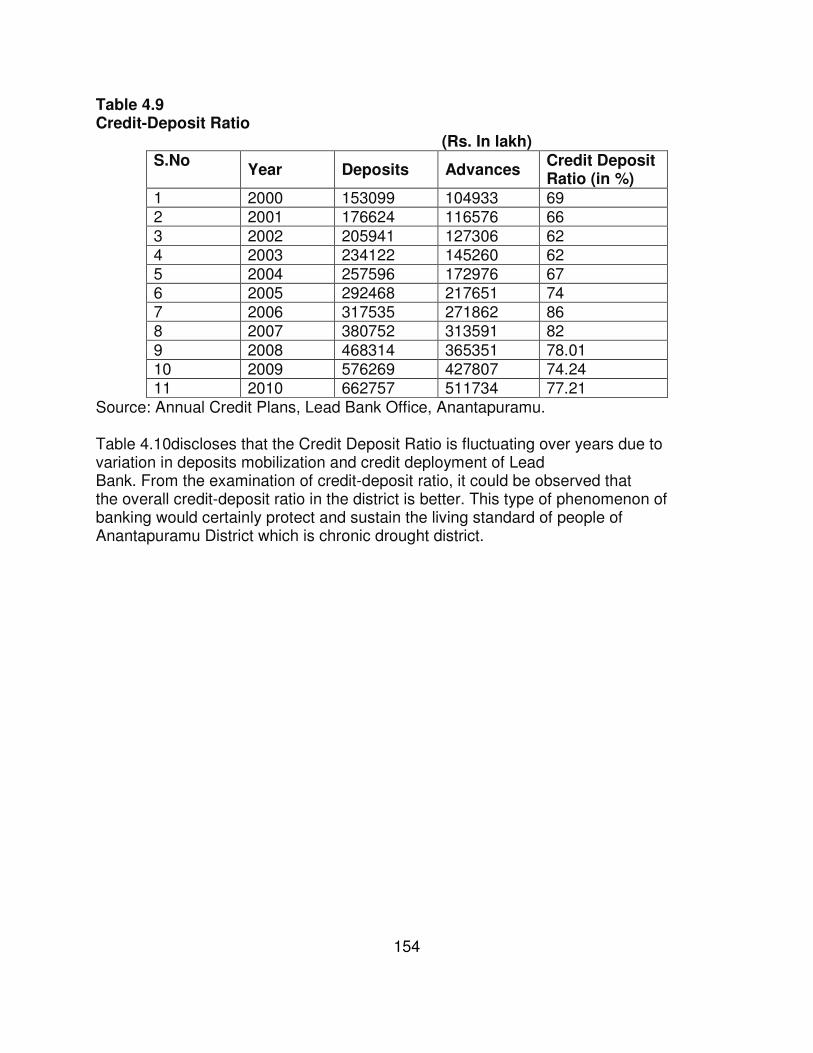

style of banking in rural development. He said: "Studies in many countries have shown how the banking system tends to become an instrument for siphoning the savings from rural areas and financing in urban and metropolitan areas lead to further regional imbalances that is operation of backward effects on the one hand and spread effects on the other by the banks in Indian rural development. 10 It is a matter of great concern to study the role of banks in reducing the regional imbalances through the means of credit-de Data on credit-deposit ratio is analyzed and presented in Table 4.9.

154

Table 4.9 Credit-Deposit Ratio (Rs. In lakh)

S.No Year Deposits Advances

Credit Deposit Ratio (in %)

1 2000 153099 104933 69 2 2001 176624 116576 66

3 2002 205941 127306 62 4 2003 234122 145260 62 5 2004 257596 172976 67 6 2005 292468 217651 74 7 2006 317535 271862 86 8 2007 380752 313591 82

9 2008 468314 365351 78.01 10 2009 576269 427807 74.24 11 2010 662757 511734 77.21

Source: Annual Credit Plans, Lead Bank Office, Anantapuramu. Table 4.10discloses that the Credit Deposit Ratio is fluctuating over years due to variation in deposits mobilization and credit deployment of Lead Bank. From the examination of credit-deposit ratio, it could be observed that the overall credit-deposit ratio in the district is better. This type of phenomenon of banking would certainly protect and sustain the living standard of people of Anantapuramu District which is chronic drought district.

155

References

Talwar, R.K.,"Some Issues in Rural Banking", The Journal of Indian Institute of

Bankers, Vo1.42, No. 2, April-June, 1972, p.11.

Rangarajan, C. (Experts from the Inaugural Address) (1995), "Imperatives of Raising

Rural Income and Farm Productivities," The Hindu, (Bangalore), June 8, p.25.

Sarma, B.P.,The Role of Commercial Banks in India's Developing Economy,

(Doctoral Thesis), New Delhi, Sultan Chand & Co. Pvt. Ltd.,1974, p. 60.

Quddas Mohammed, (1976), Control of Commercial Banks in India, Sahitya Bhavan,

Agra, p. 27

Krishnaji, P. (1988), "Diversification of Banking Business-Challenges, Problems and

Prospects", Pigmy Economic Review, Vol. 34, No. 3, October, 1988, p.1.

Rajeev Khosla (1990), "Deposit Mobilisation", The banker, Volume 37, No. 1, March,

p.32.

Rao, C.H.H.,Technological Change and Distribution of Gains in Indian Agriculture,

Delhi, Mac-Graw Hill Book Company Limited, 1975, p.65.

Vyas, V.S., Reapportur's Report on Institutional Finance for Agricultural Development,"

Indian Journal of Agricultural Economics, Vol. XXIII, No4, October-December, 1968,

pp.1-2.

Banupratap Sing , Making Farming Viable Capital Constraint, The Hindu - Survey of

Indian Agriculture, March 5, 1989 .

Edward,W. Read, Commercial Banks Management, New York, Haffer and Row

Publishers, New Delhi, 1985,p. 167. .