30

Growth in a Time of Uncertainty

Growth in a Time of Uncertainty

1 The Retail and Shopper Specialists

Contents

Introduction .........................................................................02

Executive Summary ...........................................................06

Key Findings: Manufacturer Rankings ............................................14 Retailer Rankings .......................................................19

1 The Retail and Shopper Specialists

2

1

43

The Best

Identify the best manufacturers and retailers, as ranked by their trading partners

Key MetricsDefine the importance of key metrics between trading partners

Insight

Provide insight into what makes them “the best”

2

Improvement

Highlight areas for improvement

Through its benchmarking studies Kantar Retail has provided insight into industry best practices in category management and trade promotion management for the past 19 years.

The PoweRanking® survey originated from these studies with the objective of researching and benchmarking how retailers and manufacturers view their relationships with each other.

The study reveals which retailers and manufacturers are rated highest in performance by their trading partners, thus setting benchmarks for others.

Kantar Retail sponsored the first annual PoweRanking® survey in 1997.

Introduction

The specific goals of the research were to discover:

3 The Retail and Shopper Specialists

In autumn 2015 custom questionnaires were sent to managers at all levels at hypermarket, supermarket, convenience and personal care retailers. At the same time, questionnaires were sent to managers at grocery (food and nonfood), health and beauty care and general merchandise manufacturers.

More than 430 retailer and manufacturer managers responded to the study. The names of the respondents are confidential.

The results of the 2015 survey were compared with the results for 2014 and 2013.

Retailers were asked to rank manufacturers in the following areas:

Strategy• Clearest company strategy

• Important consumer brands

• Growth and profitability

Business Fundamentals• Sales force

• Innovative marketing

• Insights/category leadership

• Supply chain

• Shopper marketing

Others• In-store support

• Digital marketing

• New product launch and promotion

Manufacturers were asked to rank retailers on similar criteria:

Strategy• Clearest company strategy

• Store branding

• Power retailers in the next five years

Business Fundamentals• Best to do business with

• Category management teams

• Innovative merchandising

• Supply chain

• Category leadership

Others• In-store execution

• Growth and profitability

• Digital marketing

Methodology

4

To accurately reflect the percentage of respondents ranking each company among the top three, the results were tabulated on a two-year rolling basis. Additionally, we carried out follow-up qualitative interviews among a diverse mix of manufacturers and retailers to provide further insight. The PoweRanking® report consolidates or separates companies based on how they are perceived by their trading partners. The methodology takes into account mergers and acquisitions and combines operations into the parent company where appropriate for this year versus one year ago. Where retailers and manufacturers operate largely as independent companies, they are treated as such in the data. For example, the 2015 survey still treats Tesco China and CRV as separate retailers.

PoweRanking® CompositesThe 2015 PoweRanking® survey includes the overall PoweRanking® Composite, which is created by weighting the three strategic rankings equally with the five business fundamental rankings (see previous page) to place more importance on the strategic rankings. This reflects the importance of a sound strategy.

Strategic CompositeThe Strategic Composite combines the three strategic measures (see previous page) into an overall composite to provide better insight into which manufacturers and retailers are the most strategically important to their trading partners.

Business Fundamentals CompositeThe Business Fundamentals Composite combines the five fundamental areas of business (see previous page) into an overall composite. This reflects the retailers’ and manufacturers’ opinions of their trading partners.

As a dynamic monitor, the PoweRanking® survey measures new market trends constantly. Kantar Retail added the digital marketing measure in 2011. In-store support and execution, new product launch and promotion (for manufacturers) and growth and profitability (for retailers) are unique to the China PoweRanking®. These measures are not included as part of the PoweRanking® Composite.

Methodology

5 The Retail and Shopper Specialists

More than 430 manufacturer and retailer participants provided information. Respondents included all levels of retailer and manufacturer management.

Below is a list of some of the leading companies they represent.

Leading Manufacturer and Retailer Participants

6

Executive Summary

6

7 The Retail and Shopper Specialists

Executive Summary

Compared with 2013 and 2014, retailers value manufacturers differently. With the continued slowdown in the Chinese economy, this should hardly come as a surprise. While organic growth, distribution, new stores and product choice drove past growth, we now see retailers making moves to win more with existing shoppers. Since volume growth is lagging, Chinese retailers are realizing that value growth – through powerful brands, in-store execution, and tailored shopper communication – will be a key success factor. As a result, retailers need manufacturers’ help to create in-store demand, thus paving the way for retailer-supplier collaboration on category management, shopper insights, and innovation. Specifically, retailers are looking to manufacturers to lead consumer understanding in these areas:

1. Good marketing: Building strong brands

Retailers realize they need to win with existing shoppers as much as they need to attract new shoppers. This, in turn, means they need to succeed with winning brands that can have a halo effect across the store.

2. Local understanding: Having the right product

China is not a homogeneous market. Retailers expect suppliers to understand local shoppers and to differentiate by brand, assortment, promotion, and pricing based on those shoppers insights. The dictum of “retail is local” remains as true as ever, and increasingly so in the complex China landscape.

3. Efficiency: Managing the cost of doing business

Retailers are aiming to create greater efficiencies in three key areas:

• Multiformat management

• Supply chains

• Brand proliferation and innovation

As the market matures, we expect retailers to shift their focus from revenue to efficiency in managing not only costs but also return on capital.

Standing still is not an option: Making the top 10 is more difficult

Local China companies are challenging the dominance of multinationals in setting the pace. We see familiar names in the rankings, but the gap is closing. More companies are being mentioned and Chinese businesses are becoming strong challengers. On the retailer side, we see RT-Mart overtaking Walmart, CRV remaining a strong player, Yonghui moving up the rankings, and homegrown eTailer JD.com entering the top 10. We cannot overstate the need for retailers and manufacturers to collaborate and communicate effectively in this fast-changing landscape.

8

Executive SummaryWhat Matters Most to Retailers?

What Matters Most to Retailers? (Percent Retailers Ranking 5 out of 1-5 in Importance)

Rank

2015 2014

Important Consumer Brands 1 7

Clear Company Strategy 2 2

Growth & Profitability 3 1

Shopper Insights/Category Leadership 4 8

Supply Chain Management 5 3

Customer/Sales Team 6 4

Shopper Marketing Programs 7 9

Innovative Marketing Approach 8 10

In-store Support 9 5

New Product Launch & Promotion 10 6

Digital Marketing 11 11 39.6%

50.0%

53.1%

55.2%

57.3%

58.3%

59.4%

61.5%

63.5%

67.7%

68.8%

-

What Matters Most to Retailers? (Percent Retailers Ranking 5 out of 1-5 in Importance)

Key Points

• More than half of responding retailers regard most metrics as “extremely important.” However, strategic metrics came out on top – indicating that retailers need manufacturers to help them set direction. When so many metrics are viewed as “extremely important,” it is clear that retailers are likely to value prioritizing objectives and setting direction.

• Interestingly, important consumer brands has jumped in importance. This supports other research showing that volume growth in China is flat, but value growth remains strong, indicating a trend toward branded (and specifically, premium branded) products. Retailers realize they will succeed if they win with premium brands. Furthermore, they see the importance of differentiating their offer on premium brands, thus creating a need for shopper marketing and marketing innovation in general.

• Retailers also see the growing importance of shopper insights and shopper marketing programs in dealing with manufacturers. Retailers must become more efficient in reaching consumers. With growth now harder to find, being more effective in targeting existing shoppers is key. Generally more efficient categories will become important in driving financial metrics – not just revenue and profitability – but overall return on capital employed. As result, launching new products has slipped in importance.

9 The Retail and Shopper Specialists

Manufacturers are facing a more complex retail landscape. Within this landscape, however, they have great opportunity to grow market share by expanding distribution, winning in growing channels, and partnering with successful retailers. They have more choices in their go-to-market strategy than before, but with limited investment dollars, they will need to choose strategically. In this context, retailers need to think how they will partner and win with leading suppliers, such as by:

• Spending more time explaining their strategy and articulating the areas in which they need manufacturers’ support. Retailers cannot expect suppliers to have all the ideas.

• Establishing and sharing clear KPIs with manufacturers, ideally through joint business planning.

• Ensuring perfect implementation of the agreements and tracking them through joint scorecards to focus on in-store execution. With so many possible investment choices amid slowing growth, neither manufacturers nor retailers can expect ongoing financial support if these agreements do not deliver against ROI targets.

• Being clear as to which brands they want to partner with and then thinking how they want to leverage branded items. It is one thing for retailers to say branded products are important and another to explain how they want to partner with manufacturers to win with shoppers.

As they recognize the eCommerce channel’s growth and size, manufacturers are also viewing eCommerce companies as strong partners. It is no accident these companies appear in the top 10 of our composite ranking for the first time. An opportunity for first-mover advantage exists; yet given the China eCommerce channel’s diversity and level of competition with several large players, international best practices may not be good enough. This sector, which Kantar Retail believes is the largest and most diverse in the world, will need homegrown approaches and solutions. This challenge is true for manufacturers and traditional retailers alike.

It is fair to say that just as opportunities are widespread, so is competition. Chinese manufacturers are becoming more sophisticated and have the potential to penetrate low-tier cities, leveraging their local market and consumer understanding to build an advantage over multinationals. If foreign retailers want to expand into low-tier cities, they will need to partner with local Chinese players. The same is true for foreign manufacturers.

10

Executive SummaryWhat Matters Most to Manufacturers?

Rank2015 2014

In-store Execution 1 1Clear Company Strategy 2 4

Growth & Profitability 3 2Supply Chain Management 4 6

Category Management/Buying Team 5 5Best to Do Business With 6 3

Best Store Branding 7 9Category Leadership 8 7

Projected to be Power Retailers 9 10Innovative Merchandising Approach 10 8

Digital Marketing 11 11 37.6%48.2%48.9%49.6%

52.5%56.7%57.4%58.2%

63.1%65.2%

84.4%

What Matters Most to Manufacturers? (Percent Manufacturers Ranking 5 out of 1-5 in Importance)

Key Points

• In-store execution remains the most fundamental factor for manufacturers in dealing with retailers. Since they need to make investment choices, retailers will succeed only if they deliver on agreements with suppliers.

• Retailers’ company strategy has risen in significance in a more challenging environment. Manufacturers need to focus on the right partner. This emphasizes the need for joint business planning, clear manufacturer-retailer KPIs, and tracking progress through scorecards.

• Supply chain and store branding also play a critical role, especially as major players try to penetrate more lower-tier cities by expanding multiformat strategies.

11 The Retail and Shopper Specialists

Executive SummaryChinese Successes

Compared with 2014, there are several new players alongside the familiar names of the past. Yet even with Procter & Gamble, Unilever, and Coca-Cola topping the list, the gap with other players is closing. This is partly due to the improved performance of companies in the next tier, but also through the increasingly complex choices that must be made to win in the China market.

The big winners are those with a clear strategy amid this complexity. Wyeth is a good example. It is outperforming its parent company Nestlé by winning through branding – even displacing Coca-Cola on that ranking. It is successful at executing an in-store brand strategy, as well as communication and leveraging shopper insights. We see it as well-placed to exploit low-tier growth potential because of its excellent sales force, clear channel strategy, trustworthy supply chain, and in-store support.

As we predicted last year, homegrown manufacturers are making great progress in the rankings.

Yili scores highly on its clearly articulated strategy, perceived growth potential in modern trade, marketing innovation (with some traditional branded players slipping), and in-store support. Similarly, COFCO is valued as a potential source of growth and commended for its strong sales force. These major Chinese companies are now capable of challenging the best Western companies, even in modern trade.

Among multinationals, Mars entered the top 10 thanks to its shopper insights strategy, clear shopper marketing, and focus on business fundamentals.

In the retailer rankings, RT-Mart has closed the gap with and overtaken Walmart as the top player. As we pointed out in 2014, RT-Mart succeeds due to its clear business strategy. It is viewed as a highly efficient player, making it an attractive investment destination. With its continued expansion, we expect it to continue to put pressure on international players.

CRV held the third position, with the integration of Tesco now largely behind it. As it leverages scale and focuses on category, shopper, and business fundamentals, we expect it to put further pressure on Walmart, Carrefour, and other players.

Yonghui climbed to the fourth position, with improvements to its own branding and fresh offer.

JD.com came in seventh, catapulted by the increasing sales in the rapidly growing eCommerce channel. This yet again shows the importance of this channel for most manufacturers and the progress that Chinese eTailers have made in a very short time. This is significant not just for manufacturers, but also for traditional brick-and-mortar stores.

12

Executive SummaryAction Steps

Winning through branding

Brands have an undeniable place in the hearts and minds of Chinese consumers. On a fundamental level, brands need to deliver on trust/reliability, but as consumers strive for premium brands, retailers and manufacturers should support each other through improved shopper insight, shopper marketing strategies, and in-store brand execution.

Execute in store

Shopper insight and communication have impact only when executed in store. Retailers will have to deliver on their commitments or risk seeing investment diverted. This is especially true in tier-one cities, where channel-specific offers will have to be created. Sustained and consistent willingness to partner will be required, with manufacturers and retailers both committing resources to the process.

Battleground 1: Lower-tier cities

Lower-tier cities are now one of two key battlegrounds for retailers and manufacturers. Winning there seems to be easier for Chinese businesses, as Yili, RT-Mart, and CRV have demonstrated. Their knowledge of consumer needs and shopper behaviors, translated into clear strategy, has underpinned their success. Other manufacturers and retailers simply must replicate this to succeed.

Battleground 2: Omnichannel and eCommerce

As we said last year, China is increasingly becoming omnichannel, and that is the second key battleground in which the correct strategic choices will be the path to success. Clarity on priority channels, the role of each channel, shopper missions, and channel-specific shopper insights are all essential for success. With the growth of eCommerce and several pure eTailing players, retailers will need to clarify how they want to play in different channels – and then communicate those choices to manufacturers.

Sales force and supply-chain efficiency

Amid declining growth (and little positive news on the horizon), building efficiencies is now part of the new normal. Collaboration is now more important than ever to unlock opportunities. Balance sheet-oriented financial measures will have to be part of the joint business planning process, specifically around capital investment and inventory management. The role of in-store management and the supply chain is now greater than ever before. Retailers and manufacturers will have to partner, share data, and plan jointly to strike the fine balance between managing working capital while not missing out on revenue-building opportunities.

The Retail and Shopper Specialists13

Manufacturer Rankings

14

15 The Retail and Shopper Specialists

CompanyStrategy

ConsumerBrands

Growth & Profitability

Sales Force/Customer Team

Marketing Approach

Insight/Category Leadership

Supply Chain

Shopper Marketing

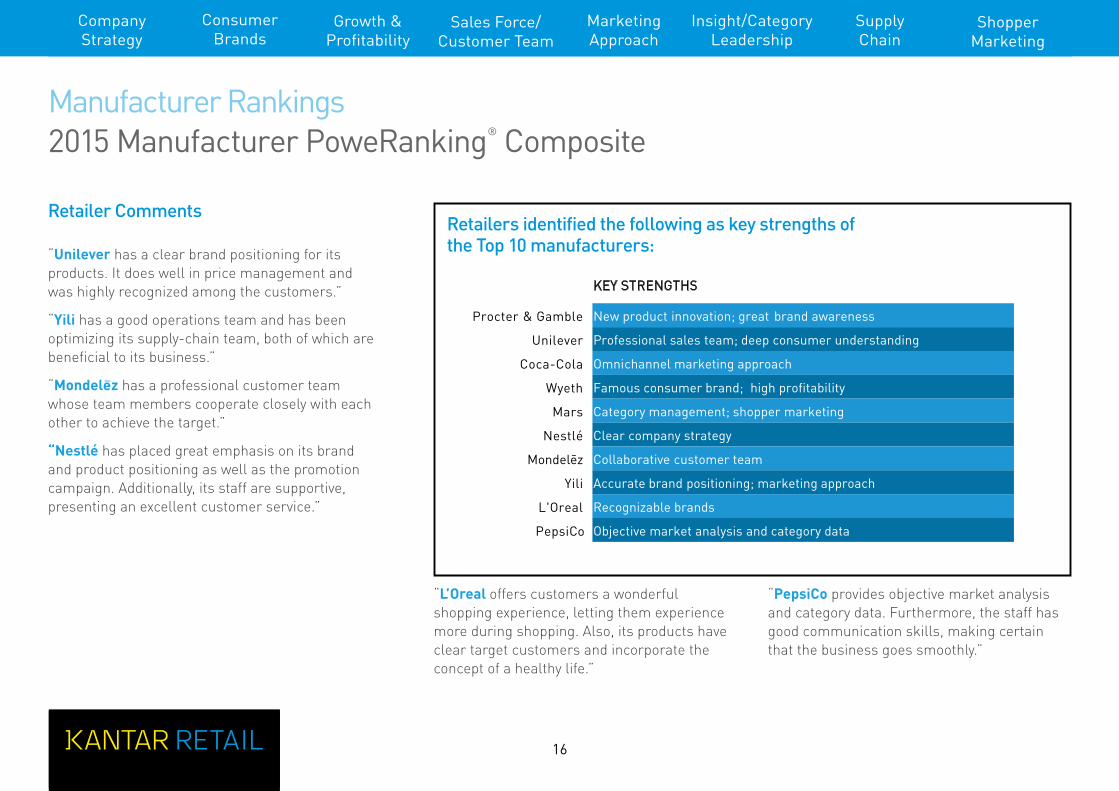

Manufacturer Rankings2015 Manufacturer PoweRanking® Composite

4.4%

4.6%

5.4%

6.1%

6.8%

6.9%

8.2%

11.5%

21.8%

33.3%

-

Rank

2015 2014

Procter & Gamble 1 1

Unilever 2 2

Coca-Cola 3 3

Wyeth 4 8

Mars 5 11

Nestlé 6 6

7 4

Yili 8 16

L'Oreal 9 7

Pepsico 10 5

Mondelez

2015 Manufacturer PoweRanking® CompositeThe composite score is a two-year rolling aggregate of the percent of retailers ranking manufacturers among the top three on individual metrics.Procter & Gamble

• Remains No.1, but with a lower score this year (33.3%) than last year (37.7%)

Wyeth• Retains its momentum, rising to No. 4

Mars• Reaches the Top 10 for the first time, with a leap to

No. 5

Yili• Dramatic improvement, rising from No. 16 to No. 8

“Unilever has a clear annual development plan, which is compatible with its quarterly and monthly development plan. Its highly motivated staff and efficient management system contribute to the successful business.”

“Coca-Cola has various methods to promote new products, integrating resources from all sides.”

Highlights:

“Procter & Gamble is a leading manufacturer. Its supply chain is mature, its sales teams are highly motivated and the management system is worth learning by other manufacturers.”

Retailer Comments

16

CompanyStrategy

ConsumerBrands

Growth & Profitability

Sales Force/Customer Team

Marketing Approach

Insight/Category Leadership

Supply Chain

Shopper Marketing

“Unilever has a clear brand positioning for its products. It does well in price management and was highly recognized among the customers.”

“Yili has a good operations team and has been optimizing its supply-chain team, both of which are beneficial to its business.”

“Mondele–z has a professional customer team whose team members cooperate closely with each other to achieve the target.”

“Nestlé has placed great emphasis on its brand and product positioning as well as the promotion campaign. Additionally, its staff are supportive, presenting an excellent customer service.”

Retailers identified the following as key strengths of the Top 10 manufacturers:2015

Score %

Procter & Gamble 33.3%

Unilever 21.8%

Coca-Cola 11.5%

Wyeth 8.2%

Mars 6.9%

Nestlé 6.8%

6.1%

Yili 5.4%

L'Oreal 4.6%

PepsiCo 4.4%

KEY STRENGTHS

New product innovation; great brand awareness

Professional sales team; deep consumer understanding

Omnichannel marketing approach

Famous consumer brand; high profitability

Category management; shopper marketing

Clear company strategy

Collaborative customer team

Accurate brand positioning; marketing approach

Recognizable brands

Objective market analysis and category data

Mondelez

Retailer Comments

“L’Oreal offers customers a wonderful shopping experience, letting them experience more during shopping. Also, its products have clear target customers and incorporate the concept of a healthy life.”

“PepsiCo provides objective market analysis and category data. Furthermore, the staff has good communication skills, making certain that the business goes smoothly.”

Manufacturer Rankings2015 Manufacturer PoweRanking® Composite

Retailers identified the following as key strengths of the Top 10 manufacturers:

17 The Retail and Shopper Specialists

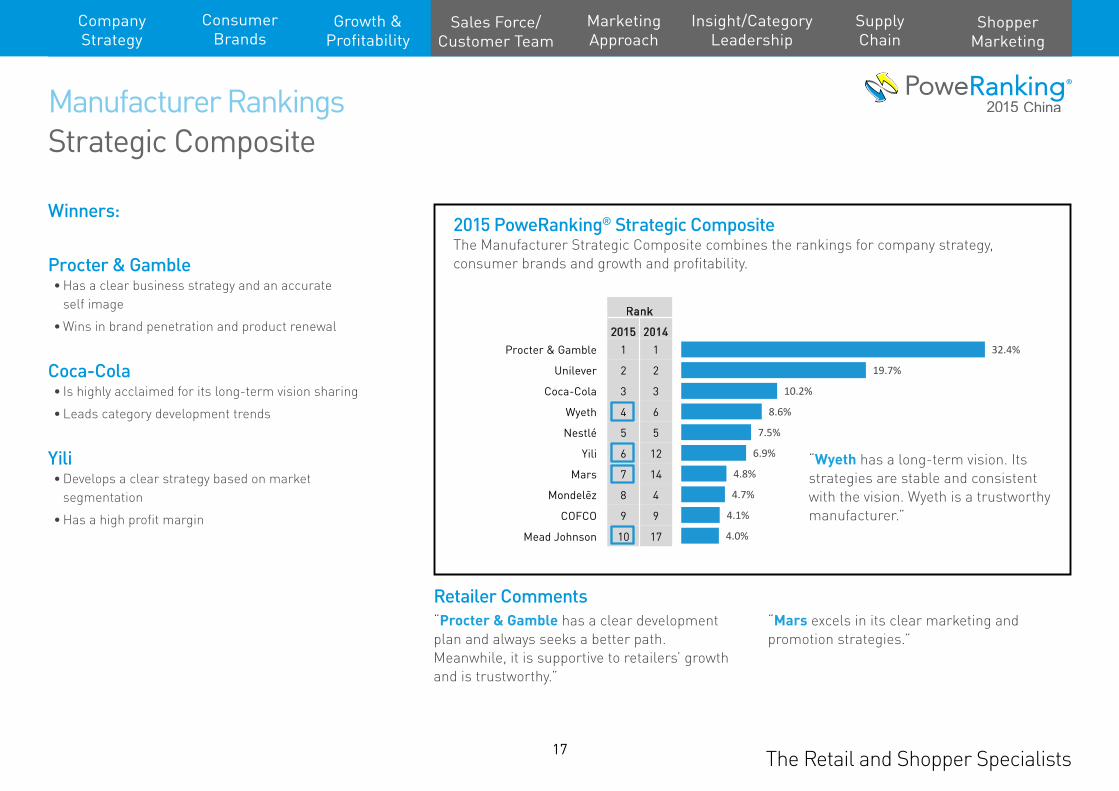

Procter & Gamble• Has a clear business strategy and an accurate

self image

• Wins in brand penetration and product renewal

Coca-Cola• Is highly acclaimed for its long-term vision sharing

• Leads category development trends

Yili• Develops a clear strategy based on market

segmentation

• Has a high profit margin4.0%

4.1%

4.7%

4.8%

6.9%

7.5%

8.6%

10.2%

19.7%

32.4%

2015 PoweRanking® Strategic Composite(Manufacturer’s Strategic Composite is a combination of rankings on: Company Strategy, Consumer Brands and Growth & Profitability)

Rank

2015 2014

Procter & Gamble 1 1

Unilever 2 2

Coca-Cola 3 3

Wyeth 4 6

Nestlé 5 5

Yili 6 12

Mars 7 14

8 4

COFCO 9 9

Mead Johnson 10 17

Mondelez

Winners:

“Procter & Gamble has a clear development plan and always seeks a better path. Meanwhile, it is supportive to retailers’ growth and is trustworthy.”

“Mars excels in its clear marketing and promotion strategies.”

Manufacturer RankingsStrategic Composite

2015 PoweRanking® Strategic CompositeThe Manufacturer Strategic Composite combines the rankings for company strategy, consumer brands and growth and profitability.

“Wyeth has a long-term vision. Its strategies are stable and consistent with the vision. Wyeth is a trustworthy manufacturer.”

Retailer Comments

CompanyStrategy

ConsumerBrands

Growth & Profitability

Sales Force/Customer Team

Marketing Approach

Insight/Category Leadership

Supply Chain

Shopper Marketing

18

Unilever• Remains in second position, but closes the gap with

Procter & Gamble

• Works closely with retailers in all aspects

Mars• Helpful and cooperative team, providing satisfying

services to retailers

Nestlé• Excels in logistics compared with competitors

• Provides skillful client service

2015 Manufacturer Business Fundamentals Composite(Manufacturer’s Business Fundamentals Composite is a combination of rankings on: Sales Force, Marketing Approach, Category Leadership, Supply Chain and Shopper Marketing)

Rank

2015 2014

Procter & Gamble 1 1

Unilever 2 2

Coca-Cola 3 3

Mars 4 11

Wyeth 5 10

6 4

Nestlé 7 9

Pepsico 8 5

L'Oreal 9 8

Master Kong 10 7 4.6%

5.2%

5.5%

6.2%

7.6%

7.9%

9.0%

12.7%

24.0%

34.2%

Mondelez

Winners:

“Wyeth indeed shows its expertise and professionalism whether in terms of the sales force, marketing approach, or supply-chain system. It is … comfortable to cooperate with them.”

“Nestlé has a deep understanding of its business target and the staff works closely with a single objective.”

Manufacturer RankingsBusiness Fundamentals Composite

2015 Manufacturer Business Fundamentals CompositeThe Manufacturer Business Fundamentals Composite combines the rankings for sales force, marketing approach, category leadership, supply chain and shopper marketing.

“Mars has a fantastic management team, ranging from supply chain to category management, all of which contribute to the ultimate outputs.”

Retailer Comments

CompanyStrategy

ConsumerBrands

Growth & Profitability

Sales Force/Customer Team

Marketing Approach

Insight/Category Leadership

Supply Chain

Shopper Marketing

19 The Retail and Shopper Specialists

Retailer Rankings

19 The Retail and Shopper Specialists

20

RT-Mart• Overtakes Walmart for the No.1 position

Yonghui• Moves up one spot to the No. 4 ranking

JD.com• Represents the only eTailer ranking among the Top 10

FamilyMart• Represents the only convenience store retailer

among the Top 10

2015 Retailer PoweRanking® Composite(The composite score is a two-year rolling aggregate of individual metric score of the percent of manufacturers ranking retailers among the top three.)

Rank

2015 2014

RT-Mart 1 2

Walmart 2 1

CRV 3 3

Yonghui 4 5

Carrefour 5 4

Watsons 6 6

JD.com 7 11

Auchan 8 9

FamilyMart 9 12

Metro 10 8 6.5%

7.2%

7.6%

7.9%

16.4%

20.8%

26.1%

28.5%

60.1%

60.8%

Highlights:

“Auchan has a clear development strategy and is mature in its business operation. It aims to improve shoppers’ experience.”

“Yonghui prioritizes its different strategies according to specific situations, which is particularly significant to its development.”

Retailer Rankings2015 Retailer PoweRanking® Composite

2015 Retailer PoweRanking® CompositeThe composite score is a two-year rolling aggregate of the percent of manufacturers ranking retailers among the top three on individual metrics.

“RT-Mart demonstrates its strategy explicitly. It obtains growth through good execution and steady expansion.”

Manufacturer Comments

CompanyStrategy

Store Branding

Projected Power Retailers

Best to Do Business With

Cat-Man/Buying Teams

Innovative Merchandising

Supply Chain

CategoryLeadership

21 The Retail and Shopper Specialists

“Yonghui still retains its strength in fresh food. It has expanded its new format ambitiously.”

“We have good communication and execution with Walmart HQ during contract negotiations.”

“CRV’s new formats (Legou Express, SGlife) enable quick adaptation to upgraded shopper demands.”

“FamilyMart enjoys fast store expansion and draws in the customers effectively through its membership system.”

Manufacturers identified the following as key strengths of the Top 10 retailers:

2015Score %

RT-Mart 60.8

Walmart 60.1

CRV 28.5

Yonghui 26.1

Carrefour 20.8

Watsons 16.4

JD.com 7.9

Auchan 7.6

FamilyMart 7.2

Metro 6.5

KEY STRENGTHS

Clear business strategy; high productivity

Strong DC system; professional category management

Large market share; business recombination

Leadership on fresh food category

Step forward on digital platform; new national DCs

Frequent in-store promotion

Increasing sales driven by rapid eCommerce growth

High in-store execution

Fast store expansion

Clear positioning

Manufacturer Comments

“Carrefour is a leading retailer in the digital platform. It opens the WeChat platform and accepts Alipay and WeChat payment. Its mobile APP is also available.”

“Metro has clearly positioned itself. We have meetings to communicate annual plans. It cooperates closely with us for further development.”

Retailer Rankings2015 Retailer PoweRanking® Composite

Manufacturers identified the following as key strengths of the Top 10 retailers:

CompanyStrategy

Store Branding

Projected Power Retailers

Best to Do Business With

Cat-Man/Buying Teams

Innovative Merchandising

Supply Chain

CategoryLeadership

22

RT-Mart• Maintains a clear corporate strategy

• Has a straightforward price strategy

• Steadily expands its store base

Walmart• Has a good corporate culture and operation

• Noted for smooth business cooperation

Carrefour• Makes progress in centralization

• Shows a clear strategy: stable hyper growth plus rapid development of new formats

2015 Retailer Strategic Composite(Retailer’s Strategic Composite is a combination of rankings on: Company Strategy, Store Branding and Projected Power Retailers)

Rank

2015 2014

RT-Mart 1 1

Walmart 2 2

CRV 3 3

Yonghui 4 4

Carrefour 5 5

Watsons 6 6

JD.com 7 10

Auchan 8 7

FamilyMart 9 12

C-Store 10 17 6.9%

7.2%

7.7%

8.9%

13.9%

17.6%

31.4%

34.9%

55.2%

63.6%

Winners:

“Walmart communicates with manufacturers regularly. Its strategies are distinctive, logical and flexible, guiding the company to grow healthily and step by step.”

“C-Store has a standardized speed-of-store opening, store size and layout. Its positioning is reasonable and the company has its leading corporate concept.”

Retailer RankingsStrategic Composite

2015 Retailer Strategic CompositeThe Retailer Strategic Composite combines the rankings for company strategy, store branding and projected Power Retailers.

“JD.com is recognized for its cooperation with offline retailers and rapid expansion of its category offering.”

Manufacturer Comments

CompanyStrategy

Store Branding

Projected Power Retailers

Best to Do Business With

Cat-Man/Buying Teams

Innovative Merchandising

Supply Chain

CategoryLeadership

23 The Retail and Shopper Specialists

Walmart• Collaborates on joint business planning

• Regularly communicates with manufacturers

• Maintains strong distribution with wide coverage

RT-Mart• Shows innovation in store layout and promotions

• Has high store traffic, which translates to high sales

Carrefour• Is professional in category management

2015 Retailer Business Fundamentals Composite(Retailer’s Business Fundamentals Composite is a combination of rankings on: Best to Do Business With, Cat-Man/Buying Teams, Merchandising, Supply Chain and Category Leadership)

Rank

2015 2014

Walmart 1 1

RT-Mart 2 2

Carrefour 3 3

CRV 4 4

Yonghui 5 7

Watsons 6 5

Metro 7 8

Auchan 8 10

Tesco 9 6

FamilyMart 10 12 7.2%

7.3%

7.5%

8.4%

18.8%

20.7%

22.0%

24.0%

58.1%

65.1%

Winners:

“Metro earns a good reputation among manufacturers as well as shoppers. Also, it will optimize its category management and maximize the manufacturers’ interests.”

“Auchan possesses a mature supply-chain system and buying team in which all team members are industrious and hardworking.”

Retailer RankingsBusiness Fundamentals Composite

2015 Retailer Business Fundamentals CompositeThe Retailer Business Fundamentals Composite combines the rankings for best to do business with, category management/buying teams, merchandising, supply chain and category leadership.

“Yonghui has a particular advantage in the fresh food category. Based on its clear policy and measurable KPIs, it highly supports and cooperates with suppliers’ creative campaigns.”

Manufacturer Comments

CompanyStrategy

Store Branding

Projected Power Retailers

Best to Do Business With

Cat-Man/Buying Teams

Innovative Merchandising

Supply Chain

CategoryLeadership

24

Our Core Capabilities

Shopper Insights We help you turn shoppers into buyers by understanding shopper needs, motivations, behaviors, barriers, and triggers across the path to purchase

Sales Process Automation We help you to optimize and automate sales force, KAM activities, and investments through our Sales Master 1 application, increasing your ROI

Go to Market We help you to improve your performance with retailers through better business planning and alignment of brand with retailer and shopper objectives and by choosing which channels to compete in, how best to access them, and how to win within them

Organizational Performance We help you to develop the commercial capability of your organization and the commercial competency of your people through organization design; commercial process mapping; competency modeling and the assessment, design, and delivery of training academies

Retailer & Channel Insights We help you shape your go-to-market strategy, assess new channel opportunities, and strengthen your customer relationships by understanding how the overall retail landscape is evolving

Category & Shopper Solutions We help you unlock future sources of real growth through the development of fact- based Category Drivers and Activation Platforms. These are tailor-made for specific channels and retailers and are purpose-built to influence purchase behavior

Retail & Purchase Data Analytics We help you to apply best-in-class analytical tools and consulting services to create winning strategies in store and online across assortment, merchandising, promotions, and price

Retail Virtual Reality We help you to create virtual retail environments and product content for virtual merchandising, store design, category management, retail execution, and shopper research so you can make better, faster retail decisions

The Retail and Shopper Specialists

The Kantar Retail NarrativeWe areThe Retail and Shopper Specialists

Our PurposeWe help our clients sell more – effectively and profitably

Our Belief and PhilosophyWe connect a world-class set of retail and shopper assets with pragmatic, solution-oriented people to grow client businesses

Our Brand storyEvery business challenge requires a unique solution.

We bring together a collection of retail and shopper assets – insights, tools, analytics, and experienced consultants who think pragmatically while building and delivering integrated solutions. Our passion is using the right combination of these assets to grow your business.

Our teams create real-world solutions to deliver faster growth, and we plug in seamlessly as part of your extended team. We connect these solutions to your core work, embedding them so your organization benefits systemically and continuously.

These solutions are aimed at your critical business decisions – how to best drive future growth, where to play, how to win, and how to optimally allocate resources. In turn, our solutions help you win the critical decisions made by shoppers and buyers along their purchase journey. Our specialized knowledge and expertise can be targeted toward specific business issues, while our integrated solutions transform businesses and generate breakthrough performance improvement.

Kantar Retail, China 1502B, WPP Campus 399 Hengfeng Road Shanghai China +86.21.2287.0500

www.kantarretail.com

The Retail and Shopper Specialists

This publication is the sole property of Kantar Retail and must not be copied,

reproduced, or transmitted in any form or by any means, either in whole or

in part, without the prior written consent of Kantar Retail. The information

contained in this publication has been obtained from sources generally

regarded to be reliable. However, no representation is made, or warranty

given, in respect of the accuracy of this information. We would like to be

informed of any inaccuracies so that we may correct them. Kantar Retail

does not accept any liability in negligence or otherwise for any loss or

damage suffered by any party resulting from reliance on this publication.

Copyright © Kantar Retail 2016

www.kantarretail.com

WeChat: KantarRetail

Price: USD2,000

![[Webinar] Sleigh the Season: What Holiday Shopper Want, How Retailers Plan to Deliver](https://static.documents.pub/doc/80x56/58713f0b1a28abf0568b7a6d/webinar-sleigh-the-season-what-holiday-shopper-want-how-retailers-plan.jpg)