THE STRENGTHENING OF EXTERNAL PUBLIC CONTROL: Guarantee for Financial Sustainability and Good Governance EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS STRATEGIC PLAN 2011-2017 MAGAZINE No. 18 - 2012

Transcript

The STrengThening of exTernal Public conTrol:Guarantee for Financial Sustainability and Good Governance

euroPean organiSaTion of SuPreMe auDiT inSTiTuTionS

STRATEGIC PLAN2011-2017

MAGAZINE No. 18 - 2012

ISSN: 1027-8982

ISBN: 84-922117-6-8

Depósito Legal: M.23.968-1997

EUROSAI magazine is published annually on behalf of EUROSAI (European Organisation of Supreme Audit Institutions) by the EUROSAI Secretariat.

The magazine is dedicated to the advancement of public auditing procedures and techniques as well as to providing information on EUROSAI activities.

The editors invite submissions of articles, reports and news items which should be sent to the editorial offices at TRIBUNAL DE CUENTAS, EUROSAI Secretariat, Fuencarral 81, 28004-Madrid, SPAIN.

The aforementioned address should also be used for any other correspondence related to the magazine.

The magazine is distributed to the Heads of all the Supreme Audit Institutions throughout Europe who participate in the work of EUROSAI.

EUROSAI magazine is edited and supervised by Ramón Álvarez de Miranda, EUROSAI Secretary General; and Karen Ortiz Finnemore, Director of the EUROSAI Secretariat; Pilar García Rodríguez, Fernando Rodríguez del Portillo, Jerónimo Hernández, and Teresa García García. Designed, produced and printed by Cromotex, S.L. EUROSAI magazine is printed on environmentally-friendly, chlorine-free (EFC) 115 gsm coated art paper (Satimatt Club) which is bio-degradable and can be recycled.

Printed in Spain.

The articles and contributions of this Magazine are under the exclusive responsibility of their authors. The opinions and beliefs are those of the contributors and do not necessarily reflect the views or policies of the Organization.

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

>2<

EDITorIAL

EUrosAI AcTIVITIEsNew Secretary GeNeral of eUroSaI 9XXXIX eUroSaI GoverNING Board MeetING 11Summary of the Main Discussions and AgreementsAnkara (Turkey), 28 May 2012

vII eUroSaI–olacefS coNfereNce. Good GoverNaNce IN PUBlIc Sector: role of SaIS 15TheSAIofGeorgia

tBIlISI StateMeNt 19eUroSaI SeMINar oN aPPlIcatIoN of Software toolS IN aUdIt 21Prague (The Czech Republic), 18-20 September 2012TheSAIoftheCzechRepublic

eUroSaI actIvItIeS 2012 27advaNce of eUroSaI actIvItIeS 2013 28aPPoINtMeNtS IN tHe eUroSaI SaIS IN 2012 28

InFormATIon on EUMeetING of tHe coNtact coMMIttee of tHe HeadS of tHe SUPreMe aUdIt INStItUtIoNS of tHe eUroPeaN UNIoN 31Estoril(Portugal),18-19October2012

aNNUal rePort of tHe eUroPeaN coUrt of aUdItorS oN tHe IMPleMeNtatIoN of tHe eU BUdGet coNcerNING tHe 2011 fINaNcIal year 33otHer rePortS, oPINIoNS aNd docUMeNtS adoPted By tHe eUroPeaN coUrt of aUdItorS IN 2012 35New MeMBerS joINING tHe eUroPeaN coUrt of aUdItorS IN 2012 37

IssAI sPoTLIGHTNewS froM tHe ISSaI HarMoNISatIoN Project 41Dr.NorbertWeinrichter.MemberofEUROSAIGoalTeam2“ProfessionalStandards”,Rechnungshof(Austria)

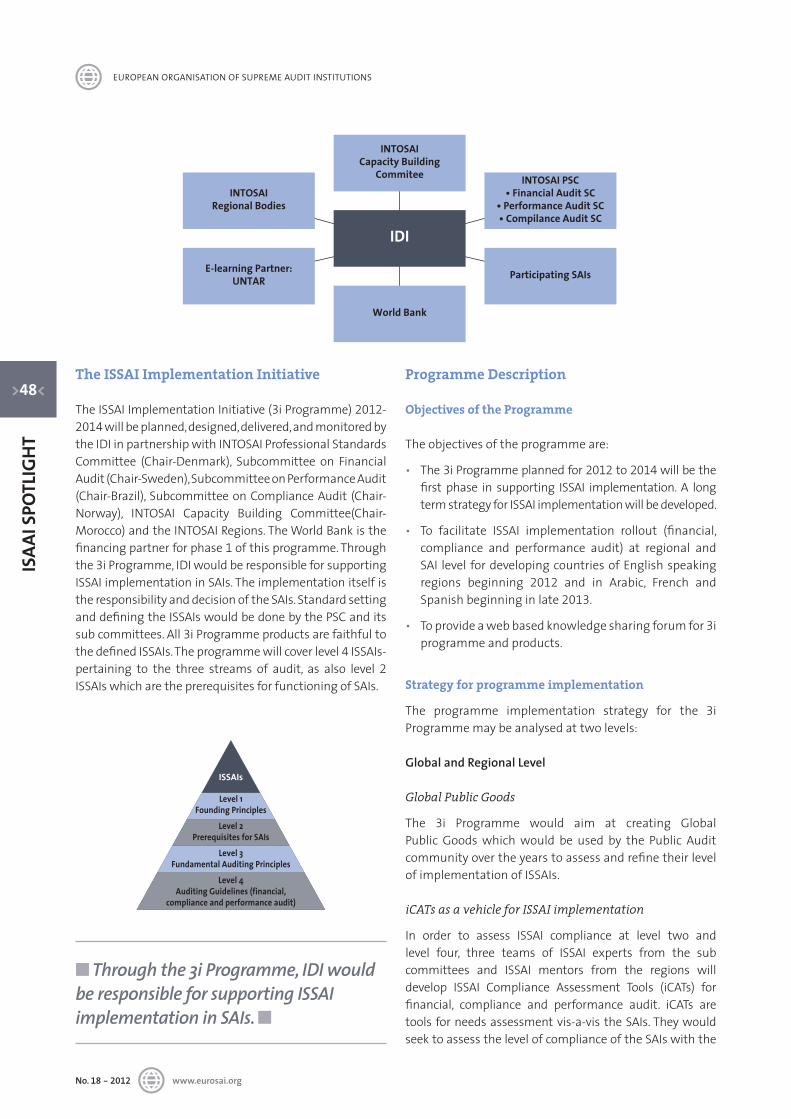

tHe ISSaI IMPleMeNtatIoN INItIatIve. StaNdardIzatIoN of aUdIt SkIllS for StreNGtHeNING PUBlIc aUdIt 47INTOSAIDevelopmentIniciative(IDI)

rEPorTs AnD sTUDIEs

EUrosAIsTrATEGIcPlAn2011-2017eUroSaI Goal teaM 2—aPPlIcatIoN of ISSaI wItHIN eUroSaI 55Prof.Dr.DieterEngels.PresidentoftheBundesrechnungshof,ChairmanofGoalTeam2“ProfessionalStandards”

eUroSaI Goal teaM 3—kNowledGe SHarING 57TheSAIoftheCzechRepublic

eUroSaI Goal teaM 4—GoverNaNce aNd coMMUNIcatIoN 61TheSAIofPortugal

2012-2013 actIvItIeS of tHe eUroSaI workING GroUP oN eNvIroNMeNtal aUdItING (wGea) 65TheEUROSAIWGEASecretariat

taSk force oN aUdIt & etHIcS 67TheSAIofPortugal

PlaNS aNd ProSPectS of eUroSaI taSk force oN tHe aUdIt of fUNdS. allocated to dISaSterS aNd cataStroPHeS 71TheSAIofUkraine,ChairofTaskForce

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

ThEsTrEnGThEnInGoFExTErnAlPUblIcconTrol:GUArAnTEEForFInAncIAlsUsTAInAbIlITyAnDGooDGovErnAncEreflectIoNS oN tHe IMPortaNce of StreNGtHeNING tHe BodIeS for tHe eXterNal coNtrol of PUBlIc ecoNoMIc-fINaNcIal actIvIty IN tHe PreSeNt coNteXt 77RamónÁlvarezdeMiranda.PresidentoftheSpanishCourtofAuditandSecretaryGeneralofEUROSAI

tHe StreNGtHeNING of eXterNal PUBlIc coNtrol: GUaraNtee for fINaNcIal SUStaINaBIlIty aNd Good GoverNaNce 81Dr.CarlosPólitFaggioni.ComptrollerGeneraloftheRepublicofEcuadorandPresidentofOLACEFS

tHe StreNGtHeNING of tHe PUBlIc eXterNal aUdIt “GUaraNtee for fINaNcIal SUStaINaBIlIty aNd Good GoverNaNce” 85GiocondaTorresdeBianchini.PanamaGeneralComptroller,ExecutiveSecretaryofOLACEFS

StreNGtHeNING eXterNal PUBlIc aUdItING tHroUGH eNHaNced relatIoN BetweeN SaI aNd INterNal aUdIt 89Dr.KunYang.ChairmanoftheBoardofAuditandInspection,Korea.SecretaryGeneralofASOSAI

StreNGtHeNING eXterNal PUBlIc aUdItING: a SafeGUard for fINaNcIal SUStaINaBIlIty aNd Good GoverNaNce. PrecoNdItIoNS to BecoMe a Good GoverNaNce SafeGUard 93IngunaSudraba.AuditorGeneraloftheRepublicofLatvia

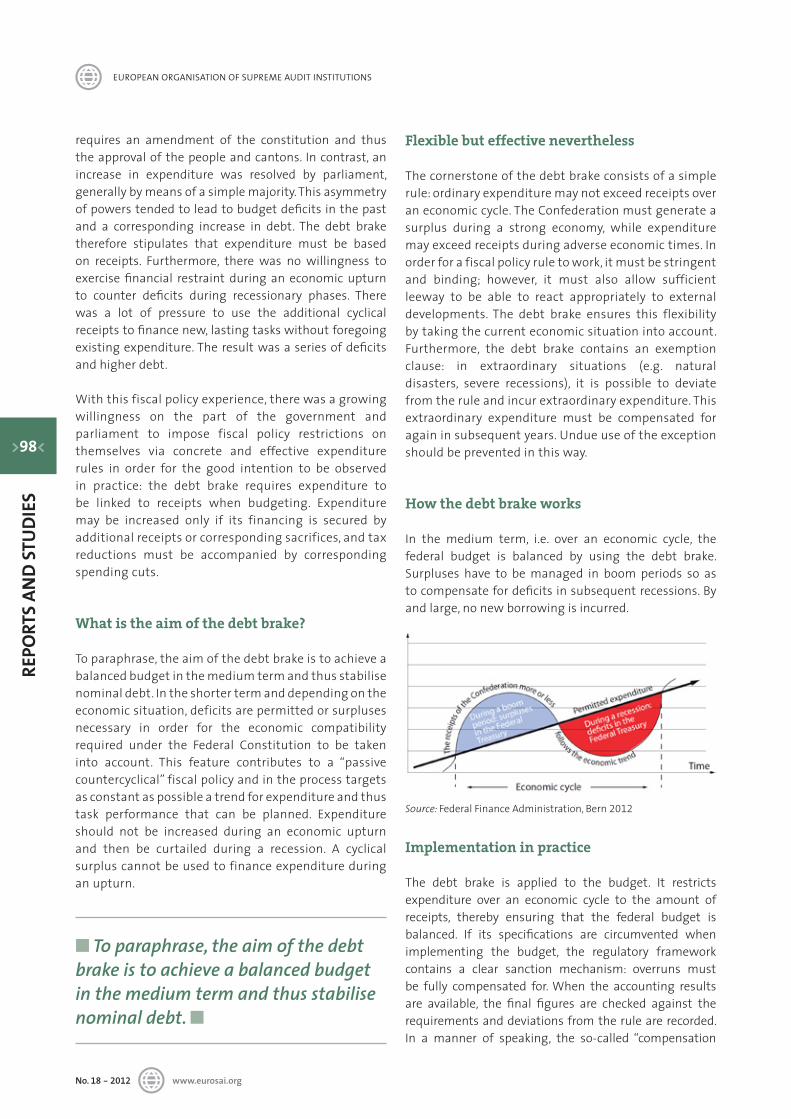

tHe deBt Brake—aN effectIve tool for a SUStaINaBle fIScal PolIcy 97KurtGrüter.ChairmanoftheSwissFederalAuditOffice

SUPreMe aUdIt INStItUtIoNS aS a SafeGUard for fIScal SUStaINaBIlIty 101Assoc.Prof.Dr.RecaiAkyel.PresidentofTurkishCourtofAccounts

StreNGtHeNING eXterNal PUBlIc aUdItING: a SafeGUard for fINaNcIal SUStaINaBIlIty aNd Good GoverNaNce 105TheSAIofAzerbaijan

followING UP aUdIt fINdINGS aNd recoMMeNdatIoNS: aN eSSeNtIal SteP to Good GoverNaNce 107DilyankaZhelezarova.AuditorintheECA’sMethodologyandSupportUnit

StreNGtHeNING eXterNal PUBlIc aUdItING: a SafeGUard for fINaNcIal SUStaINaBIlIty aNd Good GoverNaNce 111TheSAIofFrance

attractIve IN tHe SHort-terM, rISky IN tHe loNG-rUN. aUdIt eXPerIeNce of tHe State aUdIt offIce of HUNGary IN relatIoN to HUNGarIaN PPP ProjectS 115TheSAIofHungary

traNSPareNcy, BUdGetary StaBIlIty aNd fINaNcIal SUStaINaBIlIty. a cHalleNGe for eXterNal coNtrol 119ManuelAznarLópez.MemberoftheSpanishCourtofAudit

traNSPareNcy IN PUBlIc MaNaGeMeNt: eXterNal coNtrol 123ÁngelAlgarraParedes.MemberoftheSpanishCourtofAuditJorgeFerránDilla.FinancialAdvisorattheserviceoftheSpanishCourtofAudit

SoMe IdeaS oN tHe jUrISdIctIoNal StreNGtHeNING of tHe coUrt of aUdIt 129JoséManuelSuárezRobledano.Judge.MemberoftheSpanishCourtofAudit.ProsecutionDepartmentno.3

tHe StreNGtHeNING of eXterNal coNtrol IN SPaIN: GUaraNtee for fINaNcIal SUStaINaBIlIty aNd Good GoverNaNce 133JoséAntonioMonzóTorrecillas.AuditoroftheSpanishCourtofAudit

StreNGtHeNING eXterNal PUBlIc aUdIt: SUPPort of fINaNcIal StaBIlIty aNd ProPer GoverNaNce 137TheAccountingChamberofUkraine

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

EDIT

orI

Al

>5<

Dear colleagues,

True to its annual date, the EUROSAI Magazine once more offers us a suitable framework for the communication and sharing of experiences among both members and non-members of the Organisation. This occasion is the first in which I have had the opportunity to use this vehicle of communication for addressing you all as Secretary General of EUROSAI, after my appointment as President of the Spanish Court of Audit last year.

I would first of all like to take the opportunity to express my most sincere acknowledgement and my profound gratitude to Manuel Núñez Pérez, the previous Secretary General of EUROSAI and President of the Spanish Court of Audit, for his untiring work at the head of the Secretariat over the past four years. His initiatives, his willingness and his dedication to the Organisation represent a model when it comes to taking over as Secretary General. I would also like to make special mention of María José de la Fuente y de la Calle for her invaluable dedication, both professional and personal, to the Secretariat up to 2012. Over the past 10 years she has shown an unsurpassable level of commitment and effort to the Organisation, thereby contributing to the proper functioning of EUROSAI. We in the Secretariat thank her for her valuable work and we wish her every success in the new tasks and responsibilities facing her as Member of the Court of Audit.

In 2012 the Goal Teams set up by the Strategic Plan 2011-2017 approved in the VIII EUROSAI Congress have carried out intense activity, holding various plenary meetings in order to make firm progress in the effective implementation of that Plan and in attaining the Strategic Objectives defined in it, and we can already see the splendid result obtained as the outcome of that effort. Likewise, the various working groups and taskforces of EUROSAI have also made solid progress in the implementation of the work programmes for 2011-2014, which were presented to the VIII Congress, tackling the continuation or completion of activities in progress and starting up new initiatives.

During the past year EUROSAI has continued to intensify cooperation and sharing of experiences with other Regional Groups of INTOSAI with which solid ties exist, especially via the VII EUROSAI-OLACEFS Conference held in Tiflis (Georgia) in September under the theme “Good governance in the public sector: Role of the SAI”. In the year which we are now starting, this path of international cooperation is going to be furthered by means of holding the IV EUROSAI-ARABOSAI Conference, which will be taking place in Azerbaijan in April 2013 and will be focusing on the main theme “Modern Challenges for SAIs’ Capacity Building”.

This year, the main theme chosen for the “Reports and Studies” Section of the Magazine has been “The strengthening of external public control: guarantee for financial sustainability and good governance”. I consider this to be a subject of great and topical interest, constituting a preoccupation and challenge for the Institutions of external control, both within the framework of our Organisation and within that of INTOSAI, and that it will undoubtedly be present in the debates that are going to be generated around the themes which will be discussed during the the XXI INCOSAI, due to take place in Beijing in October 2013.

I would not wish to end without expressing the willingness of this EUROSAI Secretariat to make itself available to all its members, and also special gratitude to those who have collaborated with their contributions to this issue of the Magazine, making its publication possible. I also want to offer this meeting place to all those wishing to contribute to this joint project, enabling it to act as a vehicle for information and sharing of experiences among the members of our Organisation. n

ramón Álvarez de mirandaPresidentoftheSpanishCourtofAuditSecretaryGeneralofEUROSAI

As President of the Spanish Court of Audit, he has alsotaken over, from Mr Manuel Núñez-Pérez, as SecretaryGeneralofEUROSAI.

The new President of Court of Audit of Spain holdsa degree in Economics and Business Studies fromUniversidadComplutensedeMadridandheisacharteredaccountant and member of the Official Registry ofAccountsAuditors.HewasalsoamemberoftheSpanishParliamentforseveralyearsandworkedintheeconomicstudiesdepartmentatUrquijoBank.Hehascontributedwith articles in several technical publications and hassat on the Public Sector Administration and AccountingCommissionoftheAECA(SpanishAssociationofBusinessAdministrationandAccounting).

MrÁlvarezdeMirandabecameanofficeroftheSpanishCourtofAuditin1986andhasheldvariouspositionsatsaid establishment throughout his professional career.In 2001, he was elected Member of the Institutionby the Spanish Parliament, being entrusted with thecoordination of the Department for Auditing LocalEntities.InJuly2012,hewasre-appointedasaMemberoftheCourtofAuditbytheSpanishParliamentforasecondnine-yearterm.n

1. TheGBtooknoteofthe2011-2012EUROSAIActivityReport, the2011 EUROSAI Financial Report, and the2011 Report of the EUROSAI Auditors, which statedthat financial statements provided a true and fairviewoftheEUROSAIfinancialsituation.2011wasthelastyearcoveredbytheBudget2009-2011,approvedat theVII Congress, amounting the execution of thebudget along the tri-annual budgetary period to98’6%ofthetotal.

2. The GB was provided with information on thecurrent developments and further steps to begiven by the INTOSAI community in the light of the2011 UN Resolution on “Promoting the efficiency,accountability, effectiveness and transparency ofpublic administration by strengthening supremeaudit institutions”. An overview of the results of theEUROSAI annual survey for monitoring the actionstakenbyitsmembersinordertostrengthenexternalpublic control and SAIs independence was alsoreported, resulting that, at least 50% of them havemadeprogressinthisline.

3. In the framework of the implementation of theEUROSAI Strategic Plan, Goal Teams 1 (Chair: SAIFrance), 2 (Chair: SAI Germany), 3 (Chair: SAI CzechRepublic) and 4 (Chair: SAI Portugal) presentedtheir annual reports. An overall report on theimplementationofthePlan,includinganevaluationofcross-cuttingissues,wasalsopresented,resulting99%ofthetasksexecutedbyGoalTeamsasplanned.TheGBapprovedtheTermsofReferenceandoperational

plans of each Goal Team, as well as the document“Planning, Monitoring and Reporting Requirements”,aimedatguidingGoalTeams’action.Allthesepapersandmaterialsareavailableon theEUROSAIwebsite,undertheitem“StrategicPlanning”.

The GB also approved the mock up and the keyfeatures of the new EUROSAI website, which will beprofessionally designed and implemented under thecoordinationoftheEUROSAISecretariat.

4. The GB took note of the2011-2012 Activity Reportsof the EUROSAIWorking Groups on IT (Chair: SAI ofSwitzerland) and Environmental Audit (Chair: SAIof Norway); of the Task Forces on “Audit of FundsAllocatedtoCatastrophesandDisasters”(Chair:SAIofUkraine)and“Audit&Ethics” (Chair:SAIofPortugal)which was set up at theVIII Congress; as well as ofthe progress made by the “Monitoring CommitteeforsettingupandmonitoringtheDataBaseofGoodPracticesonAuditQuality”(Chair:SAIofHungary).

5. Several issues were discussed by the GB under theheading“EUROSAIcooperation”:

n Cooperation with INTOSAI, its Regional WorkingGroups,andexternalpartners:

• Fluent cooperation of EUROSAI with INTOSAIis developed through their Presidencies andGeneral Secretariats. EUROSAI and INTOSAICommittees, Subcommittees, Goal Teams,Working Groups and Task Forces collaboratein their respective framework. A relevantinteractionisalsodevelopedinthecontextoftheINTOSAI-DonorCooperation.

• CooperationwithINTOSAIRegionalGroups:

xxxIx EUrosAI GoVErnInG BoArD mEETInGSummary of the Main Discussions and AgreementsAnkara (Turkey), 28 May 2012

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

— The VII EUROSAI-OLACEFS Conference tookplaceinTbilisi(Georgia)on17-19September2012, under the theme “Good governancein public sector: Role of the SAIs”. Thistheme was developed in two sub-themes:“Enhancingstakeholders’confidence:auditingmanagement, integrity, accountability andthe tone at the top quality” and “Publicfinance management reform: trends andlessonslearned”.

— The IV EUROSAI-ARABOSAI Conference willbeheldinAzerbaijanin2013.Preparationshavealreadystarted.

— TheGBsupportedASOSAIGB’sofferfortheSAI of the Russian Federation to host theII EUROSAI-ASOSAI Conference in 2014.The date for the Conference is still to bedetermined avoiding it to interfere the IXEUROSAI Congress. The GB also endorsedASOSAI’sproposalforwideningcooperationactivities by launching it at technical levelinthefieldofcapacitybuilding.

— The GB agreed to explore ways ofcooperation with AFROSAI, entrusting theEUROSAIPresidencyandSecretariatactionsaimedatapproachingthisgoal.

— TheGBsupported toconsiderfurtherwaysand formulas for promoting cooperationwith INTOSAI Regional Groups, at strategiclevel(byHeadsofSAIs)andattechnicallevel(amongauditors).TheSecretaryGeneralwasentrustedwithexploringnewopportunities.

n CooperationwithIDI:

• Cooperation with IDI remains a priority.The GB was reported on IDI’s activities andprojects, with special attention to those ofspecific interest for EUROSAI. In this context,the Trans-regional IDI Programme on ISSAIImplementation2012-2015waspresented,aswellasanapproachwasgiventotheprogressof the INTOSAI-Donor Cooperation, whoseSecretariatishostedbyIDI,andmainlyaimedthisyearatmatchingproposalsforSAIcapacitydevelopment initiatives with donors and SAIproviders.

n Cooperationwithexternalpartners:

• The GB was informed on the cooperationdeveloped under practical basis with theEuropeanConfederationofInstitutesofInternalAudit (ECIIA), developed mainly through GoalTeam 2, with the support of the EUROSAI

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

Secretariat, in the area of the INTOSAI Gov ofcommoninterest.

6. TheGBagreedonthefollowingfinancialissues:

n Developing “EUROSAI Financial Rules”, compilingexisting rules displayed in diverse regulationsand agreements and adapting and developingthenecessaryrulesinaccordancewiththeneedsof the EUROSAI Strategic Plan. A draft will bepresented to the GB by the Secretariat, with thesupportofGoalTeam4,in2013.

n TheGBapprovedgrantingthefollowingfinancialcontributionsfromtheEUROSAIbudget:

• Funding technical equipment and conferenceroomfortheSeminar“ApplicationofSoftwareToolsinAudit”(Prague,September2012).

• Granting a commitment authorisation forfundsforfinancingthenewEUROSAIwebsite.

from three perspectives: Innovation in auditingmethods and techniques, in SAI’s organisationand in public services and government. The DutchSAI presented some initiatives which will providethe Congress with an interactive and innovativeatmosphere.

9. Information was provided on the key actionsdeveloped for implementing the INTOSAI 2011-2016 Strategic Plan, in what concerns each of theStrategic Goals: Professional Standards (raisingawarenessandpromotingimplementationofISSAIsandINTOSAIGov),CapacityBuilding(strengtheningtheSAIssupplysideofcapacitybuildingandseekinga better coordination of the actions developed),KnowledgeSharing (INTOSAIWorkingGroups/TaskForces information, effective reinforcing INTOSAIcommunication,fosteringprofessionalnetworking,promoting partnerships) and Model Organisation(progress of F&A Task Force and INTOSAI-DonorCooperation). An updating was also made inrelation to the XXI INCOSAI. The 22nd UN/INTOSAISymposiumwasannouncedtobeheldinViennaon5-7March2013.

10. The GB supported the offer of the Turkish SAI ofhostingtheXEUROSAICongress,in2017.

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

overview

On 17-19th September the VII EUROSAI–OLACEFSconference was held in Tbilisi, Georgia. The theme ofthe Conference was“Good Governance in Public Sector:Role of SAIs”. The topic was aimed at addressing theincreasing demand of the citizens for the better publicadministration and public funds management in thetimes of financial hardship for the governments andhighlighting the possibilities for SAIs to contribute tobetter accountability, transparency and efficiency of thegovernment activities. Under the heading there were2 sub-topics that are pivotal for the SAI for effectivelycarrying out its functions: Enhancing ManagementIntegrity, Accountability and Tone at the Top andfacilitatingPublicFinancialManagementReform.

The conference was succession of the cooperationstartedsince2000betweentheEUROSAIandOLACEFSwithintheINTOSAIcommunitythatenvisagessharingexperience and best practices between its membersand various Working Groups on important publicauditissuesforcontinuousimprovementofqualityofSAIwork.

The event coincided with the 20th Anniversary of theStateAuditOfficeofGeorgiaandhostingtheeventgaveSAI the opportunity to share its own experiences andchallenges in establishing the State Audit Office as animportant player of Public Financial Management withtheparticipants.

VII EUrosAI–oLAcEFs conFErEncE. GooD GoVErnAncE In PUBLIc sEcTor: roLE oF sAIs

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

session I—Enhancing stakeholder confidence: Auditing management Integrity, Accountability and “Tone at the Top”

Credibility isakeyfactor forSupremeAudit Institutionsand it can be achieved by enhancing accountability,transparency, integrityandtoneat thetopwithintheseorganizations. This session was presided by the SAI ofPortugalaspresidentofEUROSAI.

As it was stated by the EUROSAI members in the lastCongress,heldinLisbon,“transparencyandaccountabilityarebothdemocraticvaluesandarefundamentalforgoodgovernance.Accountabilityisabroadconceptincludingawiderangeof responsibilities forpublicmanagers,suchasprofessionalandmanagementskills,compliancewithfinancial and other regulations, meeting performanceexpectationsandethicalconduct”.

SAI of Portugal in its presentation highlighted theimportanceofhavingmethodologicalbaseforensuringethical government that consists of audit manualdescribingstrategiesandrulesforethicalbehavior.ISSAI30,theINTOSAICodeofEthics,isalsoaconstantreferenceforauditors.Butprovisionsfortheethicalbehaviorisnot

enough, so SAIs should look into the implementationmeasuresaswell.TheSAIofPortugallooksat3aspectsofensuringtheethicalbehavior:

• Guidance.• Management.• Control.

Foreachof thesecertainactionsareneeded:guidancecan be reinforced by detailed advice for the code ofethics and training, the management should favorethical behavior of its employees and making ethicalcriteriaforannualperformanceevaluations.Forcontrol

n As it was stated by the EUROSAI members in the last Congress, held in Lisbon, “transparency and accountability are both democratic values and are fundamental for good governance. n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

measures, checklists and internal audits have beenconsidered. Following proposals of the PortuguesePresidency, the EUROSAI Governing Board agreed tosetupaTaskForce todealwithAudit&Ethics,aimingprimarily to promote ethical conduct and integrity,bothinSAIsandinpublicorganizations.ThegoaloftheEUROSAITaskForceonAudit&Ethics,asethicsinSAIsisconcerned,istoreinforce,frameandproviderobustnessto the management of ethical conduct, with practicalandfeasibletoolsthatintendtohelptheinstitutionsintheireverydaywork.

Spanish Court of Audit presented an interesting caseshowingthepositivecontributiontheSAIcanhaveonthe accountability in public sector. In2003 the CourtofAuditreportedtotheSpanishParliamentthattherewereproblemsregardingtheaccountabilityoftheLocalPublic Sector and informed about the possible legaland administrative solutions that could be adoptedinorderfor theLocalEntitiestorendertheiraccountscompleteandwithinthelegallyestablisheddeadlines.InresponsetothistheInformationandCommunicationTechnologywasintroducedthatsignificantlyimprovedthe reporting and reviewing activities of the localgovernments.

After successfully establishing the electronic reportingsystem,theSpanishCourtofAccountsmadethereportsandaccountsofthelocalgovernmentspubliclyavailablethat besides facilitating audit activities, increasedtransparencyandaccountabilitytothecitizens.

The Turkish Court of Accounts in its presentationemphasizedtheimportanceofthehighqualityofitsownwork and the need to follow the high moral values forachievingit.Besidestheconventionalmeansofachievingtherighttoneatthetopandindependencesuchasbroad

mandate laid out in the constitution, the TCA recentlyestablished audit management software program thatenables to organize audit work and gives managementthe opportunity to monitor the findings and workingdocuments.

TheBrazilianCourtofAccountspresentedtherecentpeerreviewthathasbeencarriedoutbytheOrganizationforEconomic Cooperation and Development (OECD). Thepurposeofpeerreviewistoassesstheauditoftheannualfinancialstatementof the federalgovernmentofBrazil.Potentialbenefitsofsuchreviewsamongothersare:

1. Report prepared by a multilateral institution (OECD)withbroadknowledgeofplanning,budget,finances,accounting,governance, transparency,accountability,andsoon.

session II—Public Finance management reform: Trends and Lessons Learned

In order to live up to the high expectations of thesociety and further reinforce the principles of goodgovernance, many governments are embarking onsignificant modification of their Public FinancialManagementSystems.ThePFMservesasanoverarchingframeworkunderwhichmanyfacetsofpublicfinancialadministration are improved. The PFM concerns suchvitalissuesofpublicfinancialadministrationasbudgetplanningandexecution,establishmentofpublicinternalcontrols and internal audit, procurement, accountingand IT systems, treasury, etc. These issues constitutethe very core of the public financial management andultimately,thegoodgovernance.

Thereareanumberofsimilaritiesintheimplementationof the PFM within the EUROSAI, as countries aspireto fully implement common guidelines and bestpractice regarding the public financial management.Naturally,countriesareondifferentstagesoftheprocess,and potential to gain from each other’s experience is

n The goal of the EUROSAI Task Force on Audit & Ethics, as ethics in SAIs is concerned, is to reinforce, frame and provide robustness to the management of ethical conduct, with practical and feasible tools that intend to help the institutions in their everyday work. n

n The PFM serves as an overarching framework under which many facets of public financial administration are improved. n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

significant for state agencies as well as for SAIs. SAIscontribute to the implementation of the PFM, beingoneofthekeyplayers.TheytakepartinthePFMreformin many ways: participating in the formulation andrefinement of clear budgetary, financial, accounting,internalcontrolsandrelatedlegislation;byauditingPFMreformasawholeorseparatepartsofPFMsystemandkeyissues,sparkingnationaldebatesonmanypressingissuesaboutthemanagementofpublicfunds.

1. Recent developments have clearly demonstratedthe importanceof reasonablyplannedandexecutedfiscal policy ensured in mid and long term period.ConsequentlyroleoftheSAIsworkhavesignificantlyincreasedfromspecificaudits to thefiscaldisciplineandfiscalsustainabilityissues:

1.1. Debt Management—to increase oversight andperformance of in executive and operationalpublic.

1.2. Risk management and vulnerability analysis—enforce and encourage risk assessment andmanagementatagencylevelandPFMlevelasawhole.

1.3. Improved reporting framework and increasedmonitoring&controlofexternalauditfunctionofstateagenciesandfinancialinstitutions.

2. ContributiontoPFMreform:

2.1. Legislative initiative by SAI to improve mainregulatory PFM framework of the country acomprehensive, clear and implemented legalframeworkforPFMshouldbe:

• Structuredaccording to thePFMstructure inthecountry.

• With simple and transparent regulations-avoidingredundantbureaucracy.

• Promoting accountability and making thecooperation with the SAO obligatory (e.g. inHungariancase).

3. Disseminationsofgoodpractices—SAIshouldidentifyand disclose not only deficiencies and irregularitiesfound out during the course of audits, but goodpractices as well, to share knowledge and promotetheirroleasadvisorandpartneralongwithevaluator.

4. Guidelines—existence of guidelines solely does notguaranteethat thegoalsenvisagedbytheguidelinewouldbeachieved,asinthecaseofPublicDebtbestpractices and ISSAI guidelines that have alreadyexistedbeforethefinancialcrisis.n

n There are a number of similarities in the implementation of the PFM within the EUROSAI, as countries aspire to fully implement common guidelines and best practice regarding the public financial management. n

• The economic and social environment and citizens’demands require reforms from States aimed atmanagingpublicresourcesmoreefficiently,accordingto principles of accountability, transparency andintegrity,thusensuringfiscalsustainability;

• AsstatedintheUnitedNationsResolutionA/66/209of 22 December 2011, SAIs play an important rolein promoting the above-mentioned principles. InorderforSAIs tocontributetogreateraccountabilityof public institutions, it is essential to ensure theirindependence and the high quality of their work,increasingtheconfidenceoftheirstakeholders;

• Soundstrategies,internalandexternalcommunication,ethical requirements, quality control mechanismsandmonitoringarekeyelementsforSAIstoattaina“toneatthetop”operation.ITdevelopmentsandpeerreviewsarevaluableinstrumentsforenhancingSAIs’capacitiesandtheiraccountabilityandtransparency,therebyincreasingthetrustofcitizens;

• SAIs substantially contribute to good governance insafeguardingandsustainingtheefficientcontrolfunctionsdeveloped by parliaments, issuing recommendationsaimedatreinforcingpublicmanagementandprovidingpublic bodies and society with information on thesematters;

• The practices and experiences of each SAI representa valuable source of information for the others, socooperation becomes a masterpiece for improvingpublicmanagementandexternalauditatgloballevel,takingadvantageofinternationalsynergies;

Encourage:

• Both Organizations to spread these principleswithin their regional communities and to worktogether in order to audit and promote greaterefficiency, accountability, effectiveness, integrity andtransparencyinpublicmanagementforthebenefitofcitizens;

• Their Members to lead by example, improving thequalityoftheirworkandraiseawarenessofthevaluesandbenefitsoftheSAIsinachievinggoodgovernance;

• Both Organizations to intensify cooperation withinINTOSAI community, through their diverse levels ofdecision making and working structures, in orderto get the maximum synergies of each other andto achieve the greatest impact from their commonaction;

• The Presidents and the Secretaries General ofEUROSAI and OLACEFS to forward the Statement tothe President and Secretary General of INTOSAI, thePresidents and the Secretaries General of the otherINTOSAIRegionalWorkingGroups,aswellastootherstakeholders.n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

The Supreme Audit Office of the Czech Republic, undertheauspicesandfinancialsupportofEUROSAI,hostedaninternational Seminar on Application of Software Toolsin Audits. The seminar was held in Prague, the CzechRepublicfrom18to20September2012.TheseminarwasofficiallylistedasaEUROSAITrainingEvent.

The EUROSAI seminar was attended by more than 70delegatesfrom26EuropeanSupremeAudit InstitutionsandfromtheEuropeanCourtofAuditors.RepresentativesfromtheinternationalorganizationASOSAIattendedtheseminarasobservers.

Themaintopicsoftheseminarwerefocusedon:

• The purchase, implementation and operation of theAudit Management System (AMS) for managing andevaluatingtheaudits.

• TheuseoftheAMSinpractice.• The use of data processing tools (CAATs) during the

audit.

The primary objective of the seminar was to exchangeideas, provide information and share best practiceregardingtheuseoftheAMSanddataprocessingtoolsinauditsbycomparingpositions,methodsandresultsusedbyparticipatingSAIsinthefieldofapplicationsupportofindividualauditsteps.

Implementing new systems and procedures for themanagement and control of audits should result inthe organization acquiring benefits to audit work byincreasedeffectivenessandefficiencyofworkprocessesand standardized audit procedures, facilitating theteam work, enhancing the accuracy and timeliness ofSAIs’outcomes.Ontheotherhand,itinevitablyrequireschanges within the organization, places increaseddemands on staff and often calls for significantfinancialsupport.Theimplementationofanewsystemor upgrading the current one without sufficient andproper information and care can also cause moredamagethanbenefit.

InanenvironmentofEUfinancialcrisis,SAIs,aswithallinstitutions financed from public money, are facing thechallenge to work more effectively and efficiently withfewer resources. To share information and to followlessons learned contribute to prevent possible mistakesandeconomizemoney.

Oneofthereasonsfororganizingtheeventwasthecallforinformationinthisfieldwhichwouldbediscussedinbroaderandcomparativeperspectiveintheinternationalcontext.BasedontheevaluationofthequestionnaireontrainingprioritiesoftheEUROSAImemberstateswhichwas circulated in 2011 the use of IT technologies inauditswas identifiedasa topicofcommoninterest. In2011theCzechSupremeAuditOfficethereforedecidedto organize an international seminar on Application ofSWToolsinAudit.

n The primary objective of the seminar was to exchange ideas, provide information and share best practice regarding the use of the AMS and data processing tools in audits by comparing positions, methods and results used by participating SAIs in the field of application support of individual audit steps. n

EUrosAI sEmInAr on APPLIcATIon oF soFTwArE TooLs In AUDITPrague (The Czech Republic), 18-20 September 2012

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

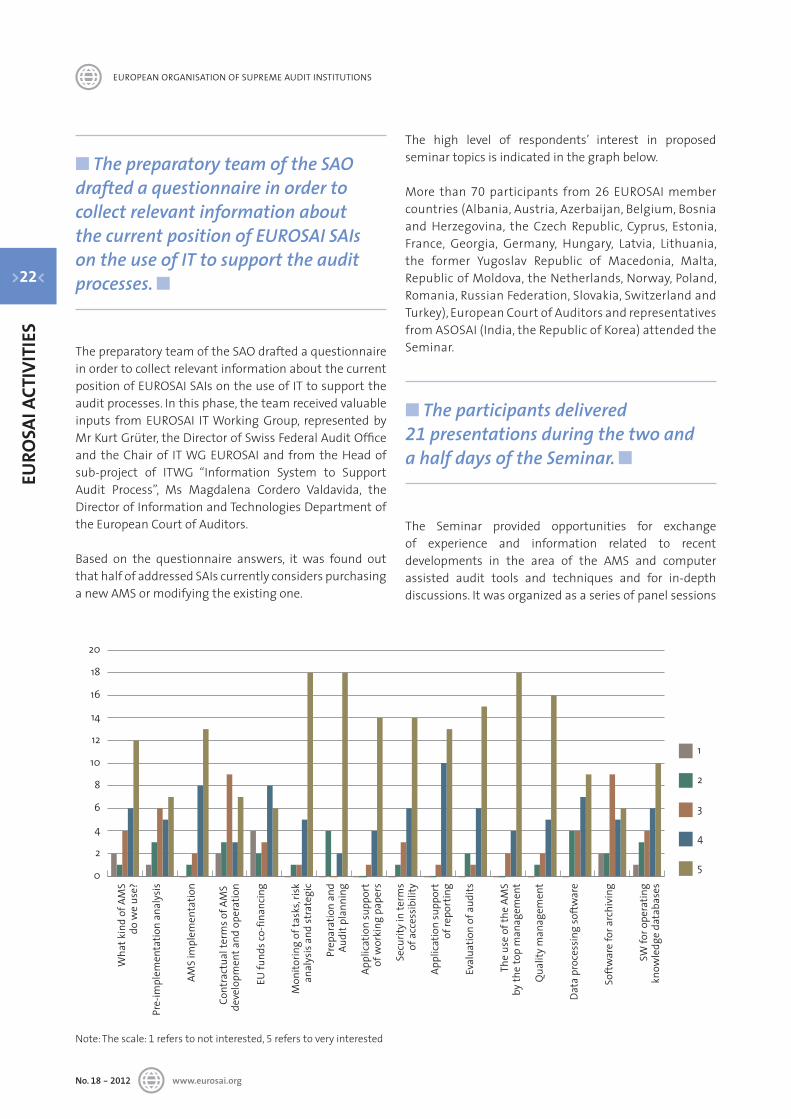

ThepreparatoryteamoftheSAOdraftedaquestionnaireinordertocollectrelevantinformationaboutthecurrentpositionofEUROSAISAIsontheuseofITtosupporttheauditprocesses.Inthisphase,theteamreceivedvaluableinputs from EUROSAI ITWorking Group, represented byMrKurtGrüter,theDirectorofSwissFederalAuditOfficeand the Chair of ITWG EUROSAI and from the Head ofsub-project of ITWG “Information System to SupportAudit Process”, Ms Magdalena Cordero Valdavida, theDirectorofInformationandTechnologiesDepartmentoftheEuropeanCourtofAuditors.

Based on the questionnaire answers, it was found outthathalfofaddressedSAIscurrentlyconsiderspurchasinganewAMSormodifyingtheexistingone.

The high level of respondents’ interest in proposedseminartopicsisindicatedinthegraphbelow.

More than70 participants from26 EUROSAI membercountries(Albania,Austria,Azerbaijan,Belgium,Bosniaand Herzegovina, the Czech Republic, Cyprus, Estonia,France, Georgia, Germany, Hungary, Latvia, Lithuania,the former Yugoslav Republic of Macedonia, Malta,RepublicofMoldova,theNetherlands,Norway,Poland,Romania,RussianFederation,Slovakia,SwitzerlandandTurkey),EuropeanCourtofAuditorsandrepresentativesfromASOSAI(India,theRepublicofKorea)attendedtheSeminar.

The Seminar provided opportunities for exchangeof experience and information related to recentdevelopments in the area of the AMS and computerassisted audit tools and techniques and for in-depthdiscussions.Itwasorganizedasaseriesofpanelsessions

n The preparatory team of the SAO drafted a questionnaire in order to collect relevant information about the current position of EUROSAI SAIs on the use of IT to support the audit processes. n

n The participants delivered 21 presentations during the two and a half days of the Seminar. n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

related to the main topics with each presentationfollowed by a discussion. The participants delivered21 presentations during the two and a half days of theSeminar.

Thefirsttwosessionsweredevotedtotheprocurement,implementation and operation of the AMS formanagingandevaluatingtheauditsintheoryandinpractice.Thethirdpartwasfocusedonuseofcomputerassistedaudittoolsandtechniques.Thecontributorsrepresented a wide range of professionals—managersresponsibleforimplementationofsystems,administrators, developers and auditors as the endusersoftheAMS.

The participants learned from presentations focused onparticularauditmanagementsystemsusedbydifferentSAIsmainlythat:

• To achieve an integrated environment sufficienttechnicalinfrastructureisnecessary.

• Technologieswhichhavenotbeentriedandtestedandsolutions with functionalities which do not complywithusersrequirementsarenotrecommended.

• The relationship/proportion between user orientedfunctionalities,maintenanceand,useracceptanceandcostshastobebalanced.

• The proper use, sharing and managing informationeliminates time consuming procedures not providingany added value and contributes to timeliness andcorrectnessofauditreports.

Theseminarwasorganisedwithafinancialsupportofthe EUROSAI. The Supreme Audit Office applied for afinancial contribution. The application was approvedat the XXXIX Meeting of the Governing Board heldin Ankara. The total expenses spent on the seminar(covering themeeting room and technical equipmentrental, services provided during the seminar, workinglunches etc.) were approximately 14 400 €. Thecontributiongrantedfromthe2012EUROSAIbudgetofapproximately5200€(roughly1/3oftotalexpenses)coveredexpensesrelatedtorentingconferenceroomsandtechnicalequipment.

Theseminarwasverywellratedfrombothprofessionalandorganizationalviews,basedonresultsofevaluationquestionnaires which were completed by participantsandcontributorsonthelastdayoftheseminar.

Additionally,ontheoccasionofdraftingthiscontributionwe asked some of the participants to make theircommentsupontheSeminar.

n The seminar was organised with a financial support of the EUROSAI. The Supreme Audit Office applied for a financial contribution. n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

n mr massimo magnini, a representative of EUROSAI IT Working Group

“The participants had the opportunity to follow not only speeches but also several online demos and have demonstrated a large interest concerning self’s developed Audit management Systems, particularly for the different approaches concerning the Risk Management module and for the customized features. It is considered as very important that audit planning is automatically based on risk analysis and system is designed to track the action taken on the recommendations.

The presentations indicate that different SAIs are at different levels of development which range from automating a few processes to a fully integrated system; these systems have been developed using different platforms and methods ( SharePoint seems to be one of the most used).

These results can also constitute a valuable input to the activities of EUROSAI ITWG.”

n mr Emanuele Fossati, IT Service Manager, European Court of Auditors

“Being involved ourselves in a major project about the modernisation of our Audit Tools, we found all the

presentations very interesting (especially where live systems were shown) and thanks to the coffee breaks dedicated to networking, we came home with new ideas to be explored. We were mainly interested in seeing other Courts’ different approaches to Audit Document Management on one side, and Audit Process Management on the other: we could see good examples of very different strategies, mainly depending on the specific type of SAI’s management and institutional objectives. We wanted to see if there was a “best in class” approach, but we understood that everybody heavily tailored their systems. Another very rich area that captured our attention concerned the various experiences in CAAT, mainly “automated” data gathering and statistical analysis, because it could make auditors work more efficient and effective.”

n mr Darius salalis, Principal Auditor, National Audit Office of Lithuania—The seminar was surprisingly interesting and informative

“At the first glance more than 20 presentations during such a short period of time looked as overload of the seminar without giving a chance to know information systems of sister-institutions as well as to learn the principles and goals of their creation. The reality was completely converse to the first impression.

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

Each presentation had plenty of room for those who were interested in the topic and willing to discuss and question various aspects of audit management as well as supreme audit office activity supervision information systems presented by each speaker. Discussions during the seminar and nonstop debates during the breaks showed that almost all the supreme audit offices, face the same challenges, i.e. ambitions to digitalize audit process and all its supporting activities in the office. The seminar gave a chance to make a step all together towards realization of this idea instead of searching the ways individually and making mistakes that could be avoided or reduced when the approach is discussed and “touched” in mutual assistance manner.

National Audit Office of Lithuania recognizes the outcome of the seminar as a constructive contribution to the information system renovation process in the Office.”

n mr Pawel- Banas, mr wiesl-aw Karlinski, mr Piotr Prokopczyk, the Supreme Audit Office of Poland—Added Value of the Seminar

“From perspective of the representatives from the Polish Supreme Audit Office, the Prague Seminar added most value in the following areas:

Characteristics and features of a well formed ITsystem supporting audit activities. Moreover, one ofthe presentations appeared to confirm the tendencyof still stronger position of agile methodologies in ITinvestments, which raised the question whether theyaregoingtodominatethe‘SAIcomputerizationindustry’nextyears?

Analysis of typical SAI processes almost ready to use by others.

Comparison of TeamMate and CaseWare advantages versus weaknesses.

Use CAAT software (IDEA) examples in financial audit (tax arrears) and compliance audit (unemployment benefits). Such an idea calls for a deep consideration within the EUROSAI family to think about a possibility of creation an open database of such examples. The IT Working Group is being developing a project (www.egov.nik.gov.pl) that would be ready to cooperate”.

n mr Joo Hee Kim, Senior Research Fellow, ASOSAI observer

“Sharing experience of outsourcing and in-house development of the AMS at different levels and various platforms would reduce the possibility of errors in specific environments. In Korean case, information accessibility and functionality improvements were not easy to reach. Bearing in mind limitations of budget and personnel without affecting the efficiency and effectiveness of the audit, I appreciated watching cases of in-house development. Furthermore, the comparison of using metadata in different SAIs was valuable.

I learned a lot from productive discussions where many questions and remarks were debated.

I would appreciate the continuation of such kind of knowledge sharing and possible active cooperation in this field in future.

I would like to thank EUROSAI for giving me the opportunity to attend this seminar in a role of observer and special thanks for the hospitality of the Supreme Audit Office of Czech Republic”.

Theseminarconfirmed that theapplicationofsoftwaretools in audit is a challenging issue which encouragedthe participants to consider new possibilities of mutualcooperationinthisareainfuture.n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

InFormATIon on EU

>31<

InFo

rmAT

Ion

on

EU

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

The2012annualmeetingof theContactCommitteeoftheHeadsoftheEUSupremeAuditInstitutions(SAIs)andof the European Court of Auditors (ECA) was hosted bythe Tribunal de Contas of Portugal, in Estoril, on18 and19October2012.Themeeting,chairedby thePresidentof Tribunal de Contas, Mr. Guilherme d’Oliveira Martins,wasattendedby93delegatesfromMemberStates’SAIsand the ECA, as well as the SAIs of Croatia (accedingcountry), four candidate countries (the former YugoslavRepublic of Macedonia, Montenegro, Serbia andTurkey)andrepresentativesof IDI-INTOSAI(Norway)andSIGMA(OECD).

ThefirstthemeofthemeetingwasaddressedthroughaSeminar:Challenges for SAIs in preparing for the next EU financial framework period.

The Seminar had the participation of a distinguishedguest speaker, the European Commissioner Mr. AlgirdasSemeta, responsible for Taxation and Customs Union,AuditandAnti-Fraud.RepresentativesofseveralnationalEU SAIs and the ECA presented their viewpoints andcurrentexperiences.

Itwasrecognizedthatthelargeandimportant“package”of legislative proposals regarding the next financialframework period will significantly alter the financialmanagementlandscapeoftheEU.

The ECA and the national EU SAIs, as external auditorsoftheEUanditsMemberStates,willbeaffectedbythereviewoftheexistingarrangementsforEUspendingandfunding launched on the occasion of the multiannualfinancial framework (MFF) 2014-2020. The ContactCommittee has been made aware of some of the

challenges raised by this process and has analyzed theproposals and their potential impact on the work of itsmembers,aswellasonthesoundmanagementofEUandnationalfinances—thediscussionsontherevisionoftheFinancialRegulationattheContactCommitteemeetingsheldin2010and2011havehelpedtoclarifythesubject.

ThenewFinancialRegulationwillreinforcetheaccountabilityofMemberStates.NewlegislativeactsoftheEUconcernfundamental matters such as strengthening budgetarysurveillance and economic policies surveillance ofMember States; enforcing the correction of excessivedeficits and macroeconomic imbalances and settingrequirementsfortheirfiscalframework.

SAIs of the Member States of the EU and the ECA aimatcontributing tobettersystemsand toenhancing theeffectiveness of the national use of Community funds,as well as to the new economic and fiscal governancemeasures of the European Union, and are concernedwith an independent and professional view on how toimprovethequalityofspending,includingbothnationaland EU contributions in co-financed projects; therefore,the importance of initiatives of cooperation betweennationalSAIsandtheECAwithregardtoEUfundsmustbehighlighted.

Inthecontextofthesecondtheme, Latest developments in responding to the financial crisis and SAIs’ experience of related audits, the results of some specific analysisrequested by the Contact Committee were delivered:the report of the Task Force to explore possibilitiesfor cooperation with Eurostat and national statisticalinstitutions; the state of play of the joint initiative ofthe Euro-area SAIs regarding the external audit of the

mEETInG oF THE conTAcT commITTEE oF THE HEADs oF THE sUPrEmE AUDIT InsTITUTIons oF THE EUroPEAn UnIonEstoril (Portugal), 18-19 October 2012

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

EuropeanStabilityMechanism;thereportoftheWorkingGroup to undertake a pilot study to identify possiblepublicauditdeficitsintheareaofnewarrangements;theprogressreportoftheFiscalPolicyAuditNetwork.

Moreover, some SAIs presented their viewpoints andexperiences, mainly in the framework of the financialcrisis, considering recent developments regardingfinancial audit and the role of SAIs; implications onaccountingstandardsandthesuitabilityofIPSASforEUMemberStates;thebudgetaryrulesandtheincomesideoftheStateBudget.

After the discussions of both themes I and II, theintervention of another notable guest speaker must beregistered: Governor of Banco de Portugal, Mr. Carlos daSilvaCosta,whodelivered theclosingconferenceof thethematicpartoftheSeminar.

The debates on the above mentioned themes gaverise to the adoption of six resolutions on the followingsubjects: 1. Network on Europe 2020 Strategy audit; 2.Supreme Audit Institutions’ cooperation with Eurostat and National Statistical Institutions;3.The results of the pilot study on the Access of Supreme Audit Institutions to the main financial supervisors in EU Member States; 4. The 2013 future activities of the EU SAI Contact Committee;5.Public accounting standards;6.The tasks and roles of the external public audit in the light of recent developments in the European Union economic governance.

and were informed about the report on best audit practices and main audit recommendations for corporate governance audits of state and municipality owned enterprises (SAI of Latvia) and the Seminar Experience gained during the winding up of the programming period 2000-2006(SAIofHungary).

In the context of information of common interest, theContactCommitteehasgotinformationontwoEUrelatedauditsbyMemberStates’SAIs:Monitoring Risks to Public Finances(TheNetherlands)andResults of the Cooperative Audit of CO2 Emission Trading Systems(Denmark).

In the meeting there was also a presentation by theSecretary General of INTOSAI and President of the SAIofAustriaonthesignificantResolutionA/66/209oftheGeneralAssemblyoftheUnitedNations:“Promoting the efficiency, accountability, effectiveness and transparency

of public administration by strengthening Supreme Audit Institutions”.

The President and the Secretary General of EUROSAIreferredtothecurrentstatusofEUROSAIactivities.

TheNetwork of SAIs of Candidate and Potential Candidate Countries and the ECA also delivered information on itsactivities.

ThemeetingofOctober2013oftheContactCommitteemeeting will be held in Vilnius, hosted by the SAI ofLithuaniaandchairedbytheAuditorGeneralMsGiedr ·eSvedien ·e.n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

On 6 November 2012 the European Court of Auditorspublished its annual reports on the implementation oftheEUbudgetandtheEuropeanDevelopmentFundsforthe2011financialyear.

Theobjectiveoftheannualreportsistoprovidefindingsand conclusions that help the European Parliament,CouncilandcitizenstoassessthequalityofEUfinancialmanagement,andtomakeusefulrecommendationsforimprovement.

Central to the2011annual reportsare the18thannualstatements of assurance (or“DAS”) on the reliability ofthe EU accounts and the regularity of the transactionsunderlying them. Moreover, the 2011 annual report ontheimplementationoftheEUbudgetincludestwonewchapters in order to provide more focused results onagricultureandcohesion,anditaidscomparisonbetweendifferentareasandyearsbyincludingcomparativefiguresrelatedto2010fortheestimatederrorrates.Italsobringsmore insight into EU performance management andmeasurementfollowingthewell-receivedintroductionofthissubjectinthe2010annualreport.

In2011, theEUspent€129.4billion,witharound80%on agriculture and cohesion policies, where the task ofimplementingtheEUbudgetissharedbytheCommissionandEUMemberStates.

As regards the reliability of the EU accounts, the ECAconcluded that the 2011 consolidated accounts of theEU present fairly, in all material respects, the financialpositionof theUnionasof31December2011,and theresults of its operations and its cash flows for the yearthen ended, in accordance with the provisions of theFinancialRegulationandtheaccountingrulesadoptedbytheCommission’saccountingofficer.

Asfortheregularityoftransactions,intheECA’sopinion,EU revenue and commitments underlying the 2011

accountswere legalandregular inallmaterialrespects.In contrast, the ECA concluded that the examinedsupervisory and control systems were partially effectivein ensuring the legality and regularity of paymentsunderlyingthe2011accountsandthat thosepaymentsweremateriallyaffectedbyerror.TheECA’sestimateforthe most likely error rate for payments underlying the2011accountswas3.9%for theEUbudgetasawhole,whichmeansthattheleveloferrorremainedsimilar to2010whenitwas3.7%.

The ECA’s overall opinion on payments is supported byspecificassessmentsofthepolicygroups.AllindividuallyassessedareasofEUspendingwereaffectedbymaterialerror with the exception of administrative and otherexpenditure(€9.8billion)andexternalrelations,aidandenlargement (€6.2 billion), although in the latter areatheauditedcontrolsystemswereonlypartiallyeffectiveandinterimandfinalpaymentswereaffectedbymaterialerror.

ForAgriculture:marketanddirectsupport(€43.8billion)theestimatederrorratewas2.9%.Aroundthreequartersof quantifiable errors were “accuracy” errors, with themostfrequentbeingover-declarationbybeneficiariesofland area when claiming for EU funds. The majority oferrorsamountindividuallytolessthan5%oftheclaim.The effectiveness of the control systems—notably theintegrated administration and control system (IACS)—wasadverselyaffectedbyinaccuratedatainthevariousdatabases and incorrect administrative treatment ofclaimsbythepayingagencies.

rural development, environment, fisheries and health(€ 13.9 billion) was the most error prone area of EUspendingwithanestimatederrorrateof7.7% in2011.Themajorityof themost likelyerrorrateconcerned theeligibility of expenditure for non-area-related measures.Intheareaofruraldevelopment,theauditofthecontrolsystems revealed that administrative and on-the-spot

AnnUAL rEPorT oF THE EUroPEAn coUrT oF AUDITors on THE ImPLEmEnTATIon oF THE EU BUDGET concErnInG THE 2011 FInAncIAL yEAr

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

checkswerenotsufficientlyrigoroustomitigatetheriskofdeclaringineligibleexpenditure.Intheareaofmaritimeaffairs and fisheries, the ECA found that unforeseenexpenditureresultedfrominsufficientmonitoringoffishcatches.

The estimated error rate for policy group regionalpolicy, energy and transport (€ 34.8 billion) remainedhigh at6.0 %.TheECA foundserious failures to respectpublic procurement rules. The second most frequenttype of error was ineligible payments with projectsfailingtofulfilthenecessaryconditions.For62%ofthetransactions affected by error, the ECA considers thatsufficient information was available for the MemberStateauthoritiestohavedetectedandcorrectedatleastsome of the errors prior to certifying the expenditureto the Commission. The ECA’s audits also showed thatthere was no assurance that financial correctionsmechanisms adequately compensated for the detectederrorsandresolvedallmaterialissuesattheclosureoftheoperationalprogrammes.

For Employment and social affairs (€ 10.3 billion) theestimatedmost likelyerrorratewas2.2%.Themajorityof errors detected concerned the reimbursement ofineligible costs. The results of the ECA’s audit indicatedweaknesses in the management and control systemsestablishedintheMemberStates,inparticularinthefirstlevelchecksofexpenditure.TheECAfoundthatsufficientinformation was available to Member State authoritiesforthemtohavedetectedandcorrectedatleastsomeoftheerrorsin76%oftheESFtransactionsaffectedbyerror,beforecertifyingtheexpendituretotheCommission.

Finally, in the policy group research and other internalpolicies (€ 10.6 billion) the ECA concluded that theestimatedmostlikelyerrorratewas3.0%.Themainsourceoferrorwastheover-declarationofcostsbybeneficiariesfor projects funded by the framework programmes forresearchand technologicaldevelopment (FPs).UnderFP

rules, beneficiaries’ cost claims should in certain casesbe accompanied by audit certificates from independentaudit firms.The control systems assessment of the ECArevealederrorsin81%oftheauditedprojectsthathadapositiveauditcertificate.

InChapter10ofthe2011annualreport,theECApresentsits observations on the Commission’s self-assessmentsof performance as stated in the annual activity reportsof the Commission’s directors-general, and highlightssome of the main themes arising from the ECA’s 2011special reports on performance. The Commission’sself-assessment on performance was evolving andrepresented some welcome improvements on previousyears. Nevertheless, ECA performance audits in 2011identified a lack of good quality needs assessments,weaknesses in the design of programmes which impairreporting on results and impacts, and a need for theCommissiontodemonstrateEUaddedvalue.

In conclusion, and as indicated by the ECA President inhispresentationsoftheAnnualReportstotheEuropeanParliamentandCouncil,therehavebeenimprovementsinEUfinancialmanagementoverthecurrentprogrammingperiod (2007-2013), but there is still some way to gobefore it is up to standard in all areas. The fall in theCourt’sestimatederrorratefortheEUbudgetasawholeunder this framework period shows that improving therules and design of spending schemes from one periodto the next does make a difference. Decisions on thelegislationgoverningspendingschemesunder thenextfinancialframework(2014to2020)shouldconsiderthatreducing the level of irregular payments and improvingperformanceandaccountabilityrequiresimplerspendingschemeswithclearerobjectives,easiertomeasureresults,andmorecost-effectivecontrolarrangements.

The ECA’s annual reports on the implementation of the 2011 EU budget and European Development Funds can be found on http://eca.europa.eu.n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

The European Court of Auditors adopted the followingspecialreportsin2012:

• Special Report No1/2012—Effectiveness of European Union development aid for food security in sub-Saharan Africa.

• Special Report No 2/2012—Financial instruments for SMEs co-financed by the European Regional Development Fund.

• Special Report No 3/2012—Structural funds: did the Commission successfully deal with deficiencies identified in the Member States’ management and control systems?

• Special Report No 4/2012—Using Structural and Cohesion Funds to co-finance transport infrastructures in seaports: an effective investment?

• Special Report No 5/2012—The Common External Relations Information System (CRIS).

• SpecialReportNo6/2012—European Union Assistance to the Turkish Cypriot Community.

• SpecialReportNo7/2012—The reform of the common organisation of the market in wine: Progress to date.

• Special Report No 8/2012—Targeting of aid for the modernisation of agricultural holdings.

• SpecialReportNo9/2012—Audit of the control system governing the production, processing, distribution and imports of organic products.

• SpecialReportNo10/2012—The effectiveness of staff development in the European Commission.

• SpecialReportNo11/2012—Suckler cow and ewe and goat direct aids under partial implementation of SPS arrangements.

• SpecialReportNo12/2012—Did the Commission and Eurostat improve the process for producing reliable and credible European statistics?

• Special Report No 13/2012—European Union Development Assistance for Drinking-Water Supply and Basic Sanitation in Sub-Saharan Countries.

• Special Report No 14/2012—Implementation of EU hygiene legislation in slaughterhouses of countries that joined the EU since 2004.

• Special Report No15/2012—Management of conflict of interest in selected EU Agencies.

• Special Report No 16/2012—The effectiveness of the Single Area Payment Scheme as a transitional system for supporting farmers in the New Member States.

• Special Report No 17/2012—The EDF contribution to a sustainable road network in sub-Saharan Africa (11FED228).

• Special Report No 18/2012—European Union Assistance to Kosovo related to the rule of law.

• SpecialReportNo19/2012—Follow-up of the European Court of Auditors’ Special Reports.

• Special Report No 20/2012—Is Structural measures funding for municipal waste management infrastructure projects effective in helping Member States achieve EU waste policy objectives?

• Special Report No 21/2012—Cost-effectiveness of Cohesion Policy Investments in Energy Efficiency.

oTHEr rEPorTs, oPInIons AnD DocUmEnTs ADoPTED By THE EUroPEAn coUrT oF AUDITors In 2012

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

• Special Report No 22/2012—Do the European Integration Fund and European Refugee Fund contribute effectively to the integration of third-country nationals?

• Special Report No 23/2012—Have EU Structural Measures successfully supported the regeneration of industrial and military brownfield sites?

• Special Report No 24/2012—The European Union Solidarity Fund’s response to the 2009 Abruzzi earthquake: The relevance and cost of the operations.

• Special Report No 25/2012—Are tools in place to monitor the effectiveness of European Social Fund spending on older workers?

In addition the followingopinions were adoptedby theECAin2012:

• Opinion No 1/2012—on certain proposals for regulations relating to the common agricultural policy for the period 2014-2020.

• OpinionNo2/2012:

— On an amended proposal for a Council Decisionon the system of own resources of the EuropeanUnion.

— OnanamendedproposalforaCouncilRegulationlaying down implementing measures for thesystemofownresourcesoftheEuropeanUnion.

— OnanamendedproposalforaCouncilRegulationonthemethodsandprocedureformakingavailablethe traditional and GNI-based own resources andonthemeasurestomeetcashrequirements.

— On a proposal for a Council Regulation on themethods and procedure for making available theownresourcebasedonthevalueaddedtax.

— On a proposal for a Council Regulation on themethods and procedure for making available theown resource based on the financial transactiontax.

• Opinion No 3/2012—on a proposal for a Regulation of the European Parliament and of the Council on the Hercule III programme to promote activities in the field of the protection of the European Union’s financial interests.

• Opinion No4/2012—on the Commission’s evaluation report on the Union’s finances based on results achieved, established under Article 318 of the Treaty on the Functioning of the European Union.

• OpinionNo5/2012—on the proposal for a Regulation of the European Parliament and of the Council amending the Staff Regulations of Officials and the Conditions of Employment of Other Servants of the European Union.

• OpinionNo6/2012—on the proposal for a Regulation of the European Parliament and of the Council laying down the rules for the participation and dissemination in “Horizon 2020—the Framework Programme for Research and Innovation (2014-2020)”.

• Opinion No 7/2012—concerning a proposal for a Regulation of the European Parliament and of the Council introducing, on the occasion of the accession of Croatia, special temporary measures for the recruitment of officials and temporary staff of the European Union.

• OpinionNo8/2012—on the proposal for a Directive of the European Parliament and of the Council on the fight against fraud to the Union’s financial interests by means of criminal law.

• Opinion No 9/2012—on an amended proposal for a Regulation of the European Parliament and of the Council laying down common provisions on the European Regional Development Fund, the European Social Fund, the Cohesion Fund, the European Agricultural Fund for Rural Development and the European Maritime and Fisheries Fund covered by the Common Strategic Framework and laying down general provisions on the European Regional Development Fund, the European Social Fund and the Cohesion Fund and repealing Council Regulation (EC) N° 1083/2006.

Moreover, 49 specific annual reports on the Europeanagencies and other decentralised bodies have beenadopted.Thereportsincludeanopiniononthereliabilityoftheir2011financialstatementsandonthelegalityandregularityoftheunderlyingtransactions.

TheECA’sAnnualActivityreportfor2011waspublishedin April2012. It provides an overview of the key resultsandachievementsduringthepreviousyearaswellasthemaindevelopmentsinitsauditenvironmentandinternalorganisation.

All ECA reports and opinions can be found on the ECA’s websitehttp://eca.europa.eu.n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

Following nominations from their Member States, andafter consultation with the European Parliament, theCounciloftheEuropeanUnionappointedthefollowingnewMemberstotheEuropeanCourtofAuditorsin2012forrenewabletermsofsixyears:

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

IssAI sPoTLIGHT

>41<

IsAA

IsPo

TlIG

hT

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

Introduction—why it is important

The“ISSAI Harmonisation Project” is one of the currentcore endeavours of INTOSAI. It proposes to replace anentire level of ISSAIs by2013 to develop the ISSAIs intoa truly coherent set of standards within a consistentframework.Notanylevel,butthe“FundamentalAuditingPrinciples” on level 3 which describe the core of SAIs’activities—theauditprocess.

The four documents have been exposed to the INTOSAIcommunity on the ISSAI Framework for discussion. [1]They address important areas for the ISSAI and theINTOSAIcommunity—forexample,theywill,forthefirsttime, address the authority of the ISSAIs and containspecificguidance toSAIsconcerningoptionsonmakingstatementsofcompliancewiththeISSAI.Theyalsoprovideadescriptionoftheconceptofpublicsectorauditingandmarkthestructureofthestandards.

Therefore, it is essential that the EUROSAI communitycarefully considers the exposed documents and SAIsactively bring their experience and competence to theexposureprocess.Inordertofacilitatethatprocess,thefollowingarticletriestodescribesomeofthehistoricalbackground leading to the project, its mandate, somekey elements of the documents exposed and the nextsteps to be undergone by the INTOSAI communityundertheINTOSAIDueProcessforINTOSAIProfessionalStandards.[2]

some History—How it came about

Facingagrowingsophisticationoftherulesforprivatesector auditing and perceiving an expectation for

similar standards for the public sector environment,thePSCSteeringCommitteeinWashington2006markedanimportantturningpointinthedevelopmentoftheISSAIs by establishing the “dual approach”: Existing(private sector) standards should be recognizedand used, complimentary public sector guidanceshould be developed where necessary. The PSC alsoredefinedtheGeneralAuditingStandardsof1992as“Fundamental Auditing Principles”. These, togetherwithguidelinesbasedon thedualapproachwere tobe the core of the public sector auditing standardsandguidelines.

After a survey on the use and needs for standardsin the public sector, INCOSAI XIX in 2007 in Mexicoadopted the current ISSAI Framework by classifying arange of different existing documents into four levelsand numbered them systematically. The first andsecond levels of ISSAI were to deal with institutionalrequirement for the SAI. ISSAIs 100-999 (“level 3”)should contain the fundamental principles of carryingoutauditingofsectorpublicentities.Levelfourshouldcontain detailed operational guidelines informing SAIshowtoimplementtheseprinciplesinspecificinstances(i.e.financialandperformanceaudits).

n The PSC also redefined the General Auditing Standards of 1992 as “Fundamental Auditing Principles”. These, together with guidelines based on the dual approach were to be the core of the public sector auditing standards and guidelines. n

nEws From THE IssAI HArmonIsATIon ProJEcTDr. norbert weinrichterMemberofEUROSAIGoalTeam2“ProfessionalStandards”Rechnungshof(Austria)

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

Level3 was initially filled by the“old” INTOSAI AuditingStandards developed in 1992. Already at this stage,however,itwasforeseenthatarevisionwouldbenecessaryin light of newer documents. In 2010, INCOSAI XXapproved further documents on level 4 including over30 on financial audit, but also on performance andcomplianceaudit.

The INCOSAI XX also highlighted the relevance of theISSAI framework as a comprehensive set of standardsand guidelines that support SAIs around the world intheir daily auditing practice. It stated that the ISSAIspresenttheessenceofpublicsectorauditingandcalledupon INTOSAI’s members to implement the ISSAIs inaccordancewiththeirmandateandnational legislation.At the same time INCOSAI—as discussed already atthe PSC meetings in Brasilia 2009, Bruxelles 2010 andCopenhagen 2010—mandated the PSC to revise level

Thecentralgoaloftheprojectisto“revisetheISSAI100-999Fundamental Auditing Principles in order to ensure thattheydescribethegeneralroleandauditingfunctionofaSAIandarerelevantandusefulforallmembersofINTOSAI;theyprovideanoverviewandfurtherreferencesto thefullsetofISSAIswheremoreoperationalguidanceisprovidedandtheyprovideaconsistentsetofconceptsandanimprovedlink between ISSAI 1 The Lima Declaration and the newset of comprehensive guidelines that were launched in2010.” Subsequently the project group will consider howthe ISSAIs 10-99 and 1000-5999 can be aligned to therevised fundamental auditing principles where necessary.Members of the project group are Austria, Brazil, China,Denmark(Chair),EuropeanCourtofAuditors,India,Mexico,Norway,Slovakia,SouthAfrica,Sweden,UKandUSA.

content—what it proposes

structure of the documents

The revised ISSAI 100 will establish the fundamental,commonprinciplesandconceptsapplicabletoallpublic

n The INCOSAI XX also highlighted the relevance of the ISSAI framework as a comprehensive set of standards and guidelines that support SAIs around the world in their daily auditing practice. n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

sector audits. The revised ISSAIs 200, 300 and 400 willelaborate the principles and concepts as they applyspecifically in financial, performance and complianceaudit.Thisstructuremayseemobvious,butitisactuallyafirstimportantstepforward.

Neither the LIMA declaration (which does not usethe concept of compliance audit), nor the “old” level3 documents (which are roughly organized accordingtostepsortheauditprocess)ormerereferencetotheframeworks used in private sector auditing were ableto form a conceptual high level basis for the currentstructure of the existing guidelines of level 4. Thecurrentproposalthuslaysagroundworkforabalancedviewofpublicsectorauditingwithaviewonallthreebranches.

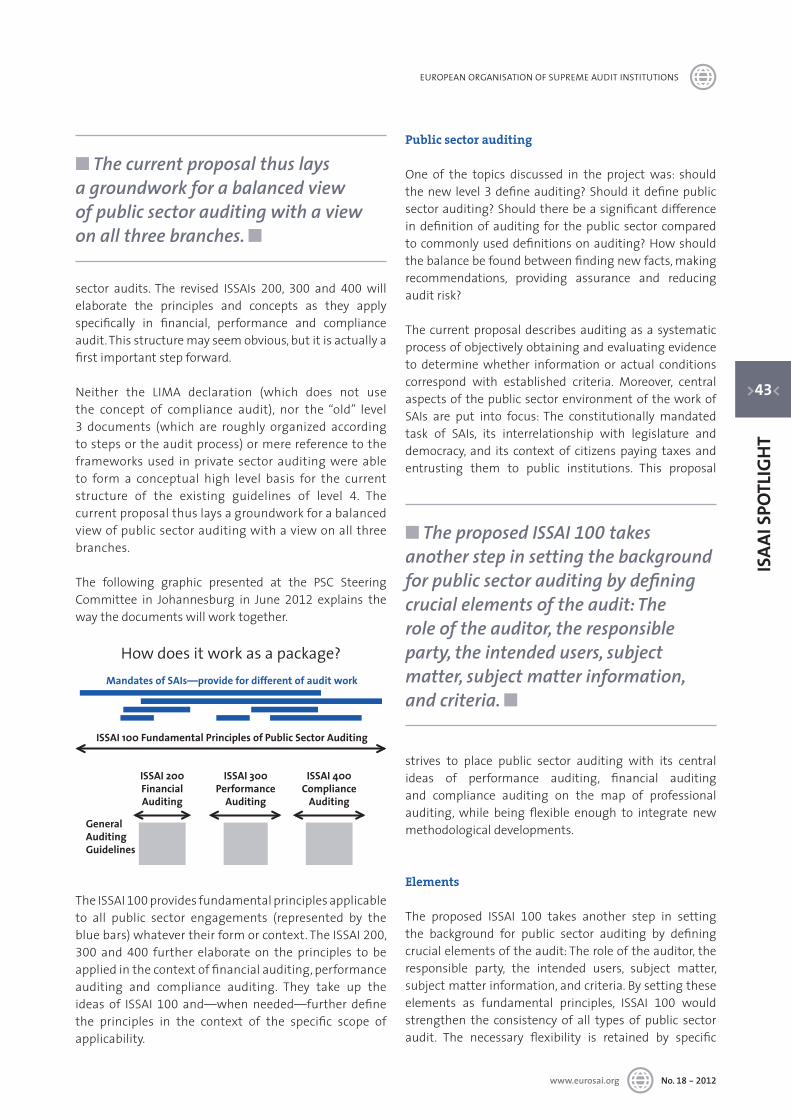

The following graphic presented at the PSC SteeringCommittee in Johannesburg in June 2012 explains thewaythedocumentswillworktogether.

How does it work as a package?Mandates of SAIs—provide for different of audit work

ISSAI 100 Fundamental Principles of Public Sector Auditing

ISSAI 300Performance

Auditing

ISSAI 400Compliance

Auditing

ISSAI 200FinancialAuditing

GeneralAuditingGuidelines

TheISSAI100providesfundamentalprinciplesapplicableto all public sector engagements (represented by thebluebars)whatevertheirformorcontext.TheISSAI200,300 and400 further elaborate on the principles to beappliedinthecontextoffinancialauditing,performanceauditing and compliance auditing. They take up theideas of ISSAI100 and—when needed—further definethe principles in the context of the specific scope ofapplicability.

Public sector auditing

One of the topics discussed in the project was: shouldthenew level3defineauditing? Should itdefinepublicsectorauditing?Shouldtherebeasignificantdifferencein definition of auditing for the public sector comparedtocommonlyuseddefinitionsonauditing?Howshouldthebalancebefoundbetweenfindingnewfacts,makingrecommendations, providing assurance and reducingauditrisk?

Thecurrentproposaldescribesauditingasasystematicprocessofobjectivelyobtainingandevaluatingevidenceto determine whether information or actual conditionscorrespond with established criteria. Moreover, centralaspectsofthepublicsectorenvironmentoftheworkofSAIs are put into focus: The constitutionally mandatedtask of SAIs, its interrelationship with legislature anddemocracy, and its context of citizens paying taxes andentrusting them to public institutions. This proposal

strives to place public sector auditing with its centralideas of performance auditing, financial auditingand compliance auditing on the map of professionalauditing, while being flexible enough to integrate newmethodologicaldevelopments.

Elements

The proposed ISSAI 100 takes another step in settingthe background for public sector auditing by definingcrucialelementsoftheaudit:Theroleoftheauditor,theresponsible party, the intended users, subject matter,subjectmatterinformation,andcriteria.Bysettingtheseelements as fundamental principles, ISSAI 100 wouldstrengthen the consistency of all types of public sectoraudit. The necessary flexibility is retained by specific

n The current proposal thus lays a groundwork for a balanced view of public sector auditing with a view on all three branches. n

n The proposed ISSAI 100 takes another step in setting the background for public sector auditing by defining crucial elements of the audit: The role of the auditor, the responsible party, the intended users, subject matter, subject matter information, and criteria. n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.orgNo. 18 - 2012

references to the underlying subject matter for eachbranchofaudit.

With reference to performance audit this proposalactually widens the application of these elements,since until now no ISSAI on performance auditsincluded these concepts. To do so, the proposalincludes broader concepts, such as on criteria, whichmay include “what should be according to laws,regulationsorstandards,what isexpectedaccordingtosoundprinciplesandbestpractice,andwhatcouldbe(givenbetterconditions).”

confidence and Assurance

One of the difficult tasks of the project group was toexplain and define the way the different types of auditrelatetotheconceptofassurance.Thisconceptisofkey

importance in the auditing standards for financial andcompliance audit, but does not appear in the INTOSAIstandardsforperformanceaudit.Theprojectgrouphaveaddressedthisinthefollowingway:

Depending on the purpose of the audit, the level ofconfidencemaybecommunicatedindifferentways;

A) By providing an explicit statement on the level ofassuranceinanopinioninastandardizedformatorinaconclusioninanon-standardizedform.

B) Byproviding aconsistentandpersuasive descriptionof the audit objective, the evidence obtained, thefindings,theconclusionsandrecommendations.

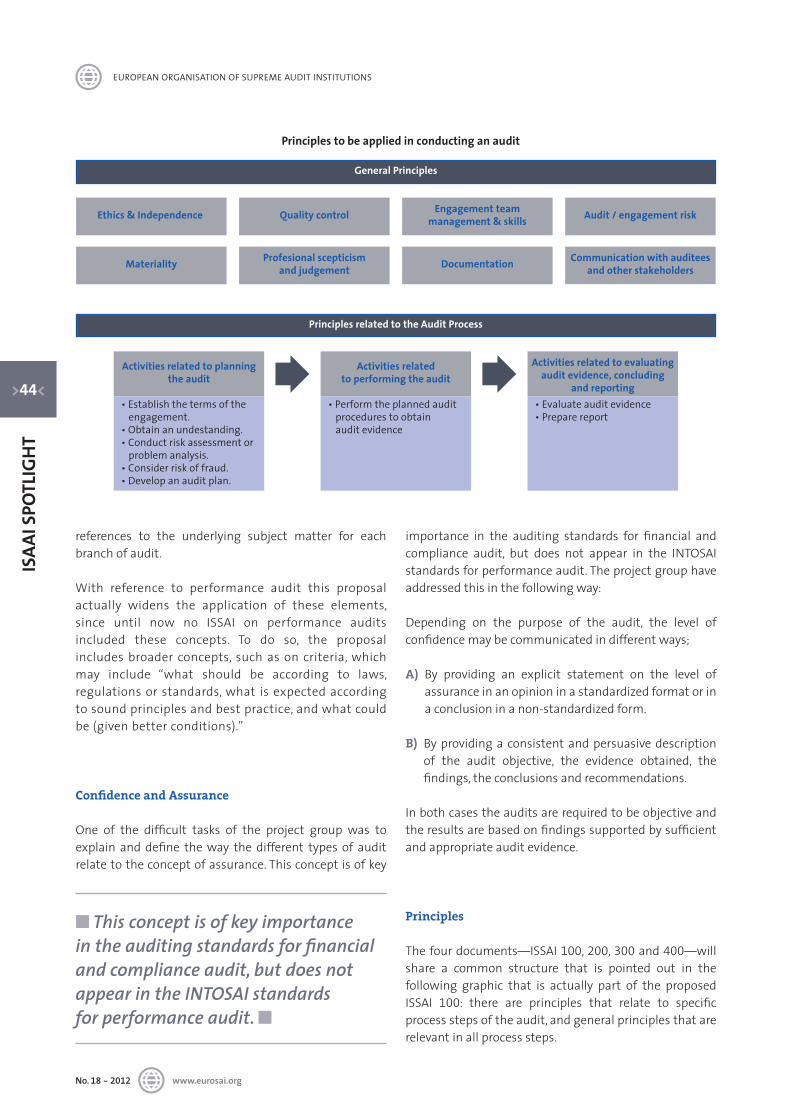

Thefourdocuments—ISSAI100,200,300and400—willshare a common structure that is pointed out in thefollowing graphic that is actually part of the proposedISSAI 100: there are principles that relate to specificprocessstepsoftheaudit,andgeneralprinciplesthatarerelevantinallprocesssteps.

n This concept is of key importance in the auditing standards for financial and compliance audit, but does not appear in the INTOSAI standards for performance audit. n

EUROPEAN ORGANISATION OF SUPREME AUDIT INSTITUTIONS

www.eurosai.org No. 18 - 2012

How to make reference to the use of the IssAIs

Forthefirsttime,theISSAIswilladdresstheauthorityoftheISSAIandcontainspecificguidancetoSAIsconcerningoptionsonhowtomakereferencetotheuseoftheISSAIs.Basically, the proposal defines two options on how toformulatestatementsofcompliance:

Option 1: “We conducted our audit in accordance with national standards based on (or consistent with) the Fundamental Auditing Principles (level 3) of the International Standards of Supreme Audit Institutions”.

Option2—IfISSAIsatlevel4areadoptedastheauditingstandard:”We conducted our (financial, performance and/or compliance) audit in accordance with the International Standards of Supreme Audit Institutions (on financial, performance and/or compliance auditing)”.

Thus, SAIs would need to adopt standards. These canbe national ones (which then need to comply with theISSAIsatlevel3,theFundamentalAuditingPrinciples),ortheycanbetheISSAIsat level4.AcarefulconsiderationofthesetwooptionswillbeatthecenterofmanySAI´schoicesofimplementation.

Thetwooptionsalsomean:therewillbenowayaroundcompliance with level3 if a SAI is interested in making

reference to the ISSAI framework. This considerationhighlights the relevance of active participation in theexposureprocess.

next steps—what your sAI should do

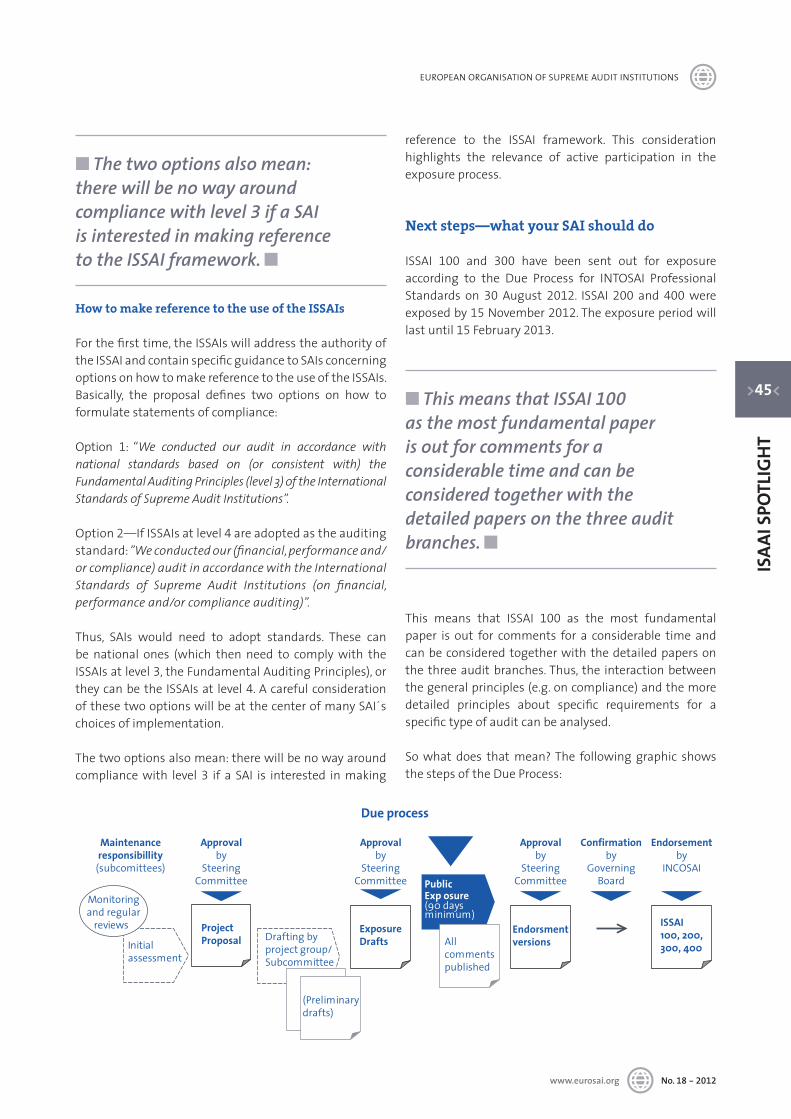

ISSAI 100 and 300 have been sent out for exposureaccording to the Due Process for INTOSAI ProfessionalStandards on30 August2012. ISSAI200 and400 wereexposedby15November2012.Theexposureperiodwilllastuntil15February2013.

This means that ISSAI 100 as the most fundamentalpaper is out for comments for a considerable time andcanbeconsidered togetherwith thedetailedpapersonthe threeauditbranches.Thus, the interactionbetweenthegeneralprinciples(e.g.oncompliance)andthemoredetailed principles about specific requirements for aspecifictypeofauditcanbeanalysed.

So what does that mean?The following graphic showsthestepsoftheDueProcess:

n The two options also mean: there will be no way around compliance with level 3 if a SAI is interested in making reference to the ISSAI framework. n

Due process

Initialassessment

ProjectProposal

ExposureDrafts

Endorsmentversions

Approvalby

SteeringCommittee

Approvalby

SteeringCommittee

Approvalby

SteeringCommittee

Confirmationby

GoverningBoard

(Preliminarydrafts)

Public Exp osure (90 days minimum)

ISSAI100, 200,300, 400

Endorsementby

INCOSAI

Maintenanceresponsibillity

(subcomittees)

Monitoringand regular

reviews Drafting byproject group/Subcommittee

Allcommentspublished

n This means that ISSAI 100 as the most fundamental paper is out for comments for a considerable time and can be considered together with the detailed papers on the three audit branches. n

The final steps for the documents will be a PSCsteering Committee Meeting in June 2013 to decideon an endorsement version to be presented first to theGoverning Board in October 2013 and then to the XXIINCOSAIinOctober2013.

conclusion

Implementation of the ISSAIs is a strategic goal ofthe INTOSAI as expressed—among others—in theJohannesburg Declaration2010. A variety of measuresare taken to enhance and strengthen this process—from a CBC guide on Strategic Consideration beforeimplementing the ISSAI, to IDI initiatives, the SAIperformance measurement framework of the INTOSAIWorking Group on the Value and Benefits of SAIs totheworkoftheIDI tohelpSAIs intheday-to-dayworkof implementation. All of those measures assume agivenpurposeandstructureof the ISSAIson theauditprocess—theverybasisofwhichisformedthroughtheISSAIHarmonisationProject.

TheessenceofthisarticleistopointouttheimportanceofthedocumentsresultingfromtheISSAIHarmonisationProject, which are currently exposed for comments.They are worthy of your attention—in exposure and inimplementation.SowhathappensafterfinalizationoftheHarmonisationProject?ItwillbeuptotheindividualSAIsand to the INTOSAI community to deliver on the ISSAIsmain promises: quality, credibility and professionalismby further developing audit practices and sharingexperiences.

For more information about the ISSAI HarmonisationProject, documents etc. on the project’s website pleasevisitthefollowingwebsite:

http://www.psc-intosai.org/composite-280.htm