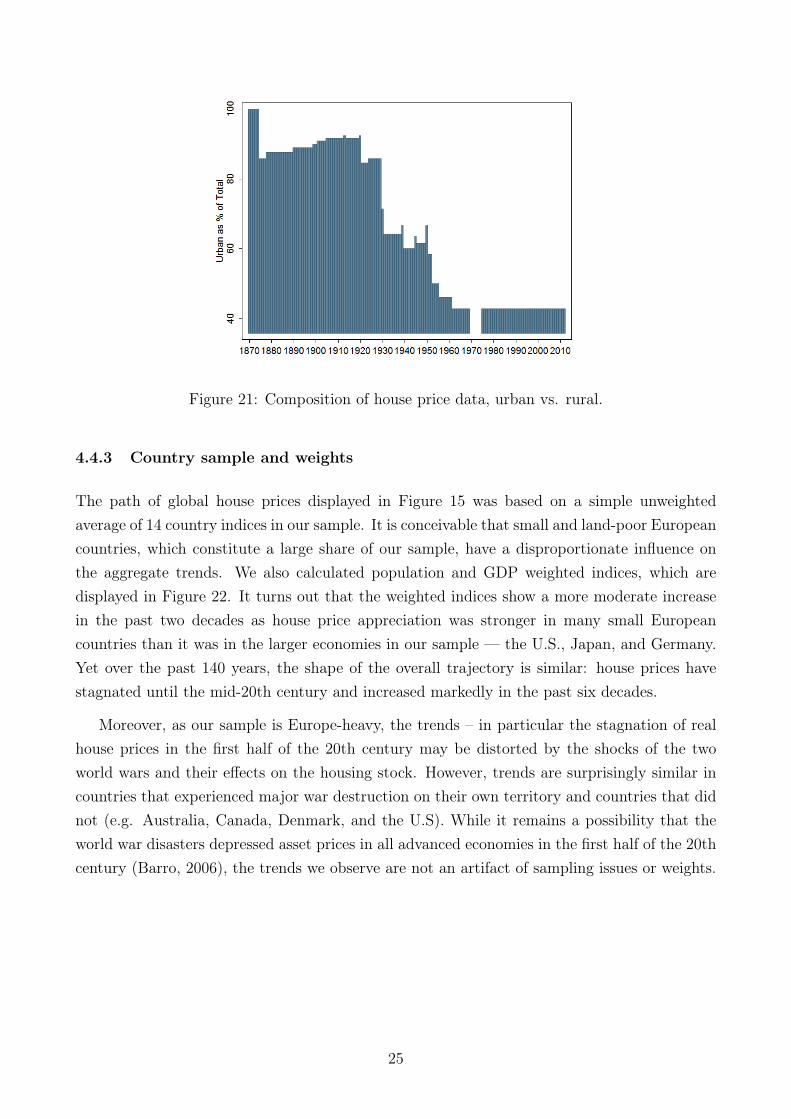

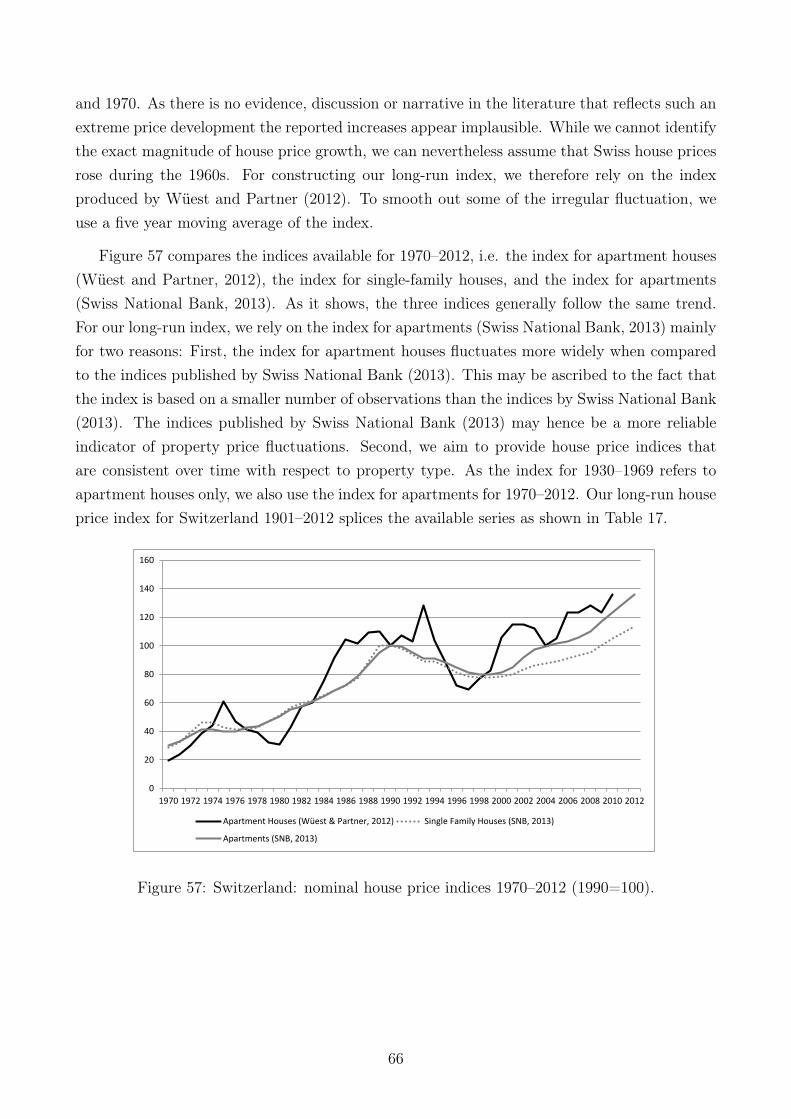

AUS BEL CAN CHE DNK DEU FIN FRA GBR JPN NLD NOR SWE USA Total1870 153 290 568 142 077 1888 048 1554 2156 003 142 036 173 8517 160711880 585 411 1568 257 158 3384 085 2309 2506 016 184 106 588 15009 285461890 1533 453 2854 324 201 4287 190 3328 2783 098 261 156 802 26828 474981900 2129 456 3833 387 291 5168 265 3811 3008 162 277 198 1130 31116 569561910 2805 468 5368 446 345 6121 336 4048 3218 783 319 298 1383 38671 713831920 4177 494 8423 508 433 5755 399 3820 3271 1044 361 329 1487 40692 804681930 4422 513 9106 514 529 5818 513 4240 3263 1457 368 384 1652 40081 832221940 4502 504 9101 522 492 6194 459 4060 3209 1840 331 397 1661 37606 811911950 4446 505 9334 515 482 4982 473 4130 3134 1978 320 447 1652 36014 790141960 4224 463 9526 512 430 5219 532 3900 2956 2048 325 449 1539 35012 771781970 4201 426 9596 501 289 4767 584 3653 1897 2089 315 429 1220 33117 735691980 3946 398 9336 500 294 4575 610 3436 1764 2132 276 424 1201 28800 677731990 3549 351 8688 503 284 4412 585 3432 1658 2025 278 404 1121 24400 639072000 3985 344 7313 449 286 4083 587 3194 1688 2005 280 401 1282 20500 57201Note Dates are approximate Bold denotes peakSources Mitchell (2013) Statistics Canada (various years) Statistics Japan (2012)

It is important to note that not only the extension of the global railway network petered outin the first half of the 20th century The dramatic efficiency gains in maritime transportationwere also realized in the late 19th and early 20th century (Mohammed and Williamson 2004)The 19th century revolution in shipping rested on two developments first the fall of ironand steel prices that led to the introduction of metallic hulls second parallel advances inengine technology that led to much improved fuel efficiency (Harley 1988 1980 North 19651958) Between 1870 and 1914 shipping costs fell by about 50 percent relative to the pricesof commodities (Jacks and Pendakur 2010) By contrast as Hummels (2007) has showncommodity-deflated real freight rates barely fell after 1950 Figure 29 exhibits that internationaltransport costs had fallen strongly until the mid-20th century This is likely to have left itsmark on land prices

To analyze how a reduction in transport costs affects the land price we set up a simplemodel with heterogeneous land in the spirit of Ricardo (1817) and von Thuumlnen (1826) Theland rent depends on land location as measured by the distance to the marketplace Falling

transportation costs raise the land rent net of transportation costs and lead to an expansionof developed land

Consider a perfectly competitive one-sector economy There is a continuum of firms indexedby i isin [0 1] There is also a continuum of land plots indexed by i isin [0 1] Every firm i isconnected to and owns a piece of land Zi14 The size of each land plot is identical across firmsand normalized to one ie Zi = 1 for all i In equilibrium there are active firms indexed by0 lt i le ilowast as well as inactive firms indexed by ilowast lt i le 1 Active firms develop their land byincurring a fixed cost k and combine (developed) land Zi and labor Li to produce a final outputgood according to Yi = (Li)

α(Zi)1minusα where 0 lt α lt 1 denotes a constant technology parameter

In order to sell their output firms have to transport their products to the marketplace Thisactivity is subject to iceberg transportation costs τi We parametrize the transportation costsby τi = ai where 0 lt a le 1 Normalizing the output price to unity pY = 1 the revenue net oftransportation costs of firm i isin [0 ilowast] is given by Ri = (1minus ai)(Li)α(Zi)

1minusα

The analysis proceeds in two steps The first step focuses on the labor market Individuallabor demand of firm i isin [0 ilowast] for any given wage rate w results from the usual first-order

condition for profit-maximizing labor employment to read as follows Llowasti =[α(1minusai)wlowast(ilowast)

] 11minusα where

we have set Zi = 1 The equilibrium wage rate wlowast(ilowast) is determined by the labor marketclearing condition

int ilowast0Li(w)di = LS where LS denotes exogenous labor supply Notice that

the equilibrium wage rate wlowast(ilowast) increases with the number of active firms ilowast The amountof labor employed by any firm i isin [0 ilowast] in general equilibrium declines as more firms becomeeconomically active or equivalently as more pieces of land are being used economically Thesecond step focuses on the land market Let vZi (τ) denote the land return which may bethought of as residual income accruing to the land owner ie vZi = partR

partZi= (1minusai)(1minusα)(Li)

αThe price pZi of land plot i isin [0 ilowast] is given by the present value of the infinite stream of landreturns ie pZi =

intinfintvZi (τ)eminusr(τminust)dτ Given that vZi is constant in equilibrium the land price

may be expressed as pZi = vZi r where r denotes the constant real interest rate A specificland plot i is being developed if the land price exceeds the development costs ie pZi ge kTherefore the number of developed land plots in equilibrium ilowast equal to the number of activefirms is determined by the following condition

(1minus ailowast)(1minus α)(Llowastilowast)α

r= k (7)

where Llowastilowast is equilibrium labor demand of the marginal firm i = ilowast

What are the effects of radical innovations in the transportation sector like those thatoccurred in the late 19th and early 20th century with respect to land supply The decline in

14Whether firms own a piece of land and reap land return (residual income) or rent the required land fromlandowners by paying a rental rate is not critical with respect to the implications With regard to the landprice both institutional arrangements are equivalent

36

transportation costs enlarged the present value of land returns net of transportation costs forany land plot i Equation 7 then implies that the number of developed land plots rises Inother words the drop in transportation costs triggers an expansion of economically used landFigure 30 illustrates this reasoning The dashed horizontal line shows the constant developmentcosts k while the two downward sloping curves display the value of developed land pZi = vZi r

for alternative values of a15 Now as a falls the curve pZi = vZi r shifts outwards such that ilowast

increases as displayed in Figure 30 The intermediate result therefore is that a reduction intransportation costs unequivocally increases the supply of economically used land

Figure 30 Land supply in response to reduction in transportation costs

How does an increase in land supply triggered by a reduction in transport costs affect theaggregate land price defined as pZ = 1

ilowast

int ilowast0pZi di The combination of reduced transportation

costs and enhanced land supply unfolds three distinct mechanisms with respect to the aggregateland price pZ which can be summarized as follows (for details see Appendix A1)

1 Complementary-factor effect Additional land is developed and employed in output pro-duction Every piece of land is combined with a lower amount of labor This effectdepresses the average land price16

2 Composition effect More distant and therefore less profitable pieces of land are beingdeveloped and used economically This effect also reduces the average land price

15These curves are downward sloping for two reasons First land plots are located further away from themarketplace as i increases which implies higher transportation costs τi = ai Second as i increases the numberof firms - hence aggregate labor demand - goes up such that each piece of land is combined with a lower amountof labor

16There would be an additional effect in multi-sector models As output of the land intensive sector increasesthe goodsrsquo price falls and the competitive land return should decline further

37

3 Revaluation effect Already developed pieces of land become more valuable because thecompetitive land return net of transportation costs vZi increases This effect increases theaverage land price

The complementary-factor effect and the composition effect reduce the land price and thiscan dominate the revaluation effect such that the aggregate land price pZ declines as a falls Ina growing economy the competitive land return can be expected to increase over time becauseland is in fixed supply This drives up land prices But if profit-maximizing firms endogenouslydetermine the overall land use a substantial decline in transportation costs triggers the devel-opment of additional land plots As a result land may effectively not represent a fixed factorfor an extended period and the land price may remain constant or even fall despite continuouseconomic growth

In our view the interaction of transport cost declines and economic growth provides anovel and powerful explanation for the observed path of long-run land prices The large-scale construction of the railway system during the 19th century and early 20th resulted ina substantial decline in transportation costs and likely suppressed land prices during the pre-World War II period After World War II these effects faded so that economic growth led toan increase in the land price In the next section we will discuss two additional factors thatmay have reinforced this trend higher expenditure shares for housing services and growingrestrictions on land use (Glaeser et al 2005a Glaeser and Gyourko 2003)

63 Land prices in the second half of the 20th century

As noted above the trajectory of land prices in the second half of the 20th century is notas puzzling from the perspective of a standard neoclassical model With continuous economicgrowth the value of land could be expected to grow However two additional factors mighthave contributed to an even starker increase of land prices

First empirical data show that the mean housing expenditure share remained nearly con-stant in the pre-World War II period (average annual growth rate 006 percent) whereasit grew by an average annual growth rate of 11 percent after World War II17 However theincrease in expenditure shares is not uniform across countries as Table 4 demonstrates Forinstance the expenditure share remained largely constant in the United States As a resultthe unweighted mean expenditure share shown in Figure 31 may be biased upwards

How did the rising housing expenditure share after World War II impact the evolution ofland prices To answer this question we set up a simple two-sector model with housing and

17The empirical findings on the (long-run) income elasticity of the demand for housing services is howeverinconclusive For instance Fernandez-Kranz and Hon (2006) review the literature and report values that rangebetween 05 percent and 28 percent

38

AUS BEL CAN CHE DEU DNK FIN FRA GBR ITA JPN NLD NOR SWE USA1870 012 014 017 014 0151880 013 014 019 013 0101890 014 013 018 012 0121900 011 014 017 011 019 014 01119131914 008 013 016 017 010 016 014 0141920 007 016 012 009 005 008 0111930 010 019 014 019 014 008 012 018 025 0161940 009 019 023 015 019 013 009 015 018 022 0131950 016 010 010 008 011 016 0111960 011 019 016 013 013 018 011 013 019 0141970 014 020 016 017 017 018 018 015 013 015 021 018 0141980 018 021 015 019 025 019 019 016 013 016 021 018 0141990 020 024 021 020 026 018 020 017 016 018 023 019 0152000 020 023 023 023 023 026 025 023 019 018 023 009 019 021 0152010 023 023 024 024 025 029 027 026 025 023 025 010 021 020 016Note Dates are approximate Sources See Appendix B

Table 4 Share of housing expenditure in GDP

manufacturing production described in Appendix A3 to study the quantitative implicationsof rising expenditure shares The intuition is simple As the production of housing servicesrelies more heavily on land ndash the land cost share in production is higher ndash compared to themanufacturing sector aggregate demand for land rises when the expenditure share for housingservices rises With fixed land supply the land price increases A back-of-the-envelope calcu-lation on the basis of the model yields the following results From the data we observe anaverage increase in the expenditure share during the second half of the 20th century by a factorof about 165 Such an increase translates into an additional 42 percent of price appreciationrelative to a scenario with constant expenditure shares The contribution of rising expenditureshares on the land price is therefore substantial Further details on this exercise can be foundin Appendix A3

Figure 31 Share of residential service expenditure in GDP

39

A second important reason for the steep increase of land prices in the second half of the20th century has been pointed out by Glaeser and Ward (2009) Glaeser et al (2005a) andGlaeser and Gyourko (2003) These studies point to growing restrictions on land supply drivenby changes in the regulatory regime that make large-scale development increasingly difficultMore stringent and widespread land use and building regulation were introduced during thesecond half of the 20th century (MacLaughlin 2012 Glaeser et al 2006) As a result of landuse restrictions on new home construction housing supply could not increase in response torising house prices which limited the supply of new homes (Glaeser et al 2005a Glaeser andGyourko 2003) For urban areas in the northeastern US for example Glaeser and Ward(2009) and Glaeser et al (2005b) show that regulations substantially reduced the number ofnew construction permits In the case of the Greater Boston area the total number buildingpermits in the 2000s stood at less than 50 percent of its 1960s level (Glaeser and Ward 2009)These studies further argue that there is a strong relation between house prices and land-useregulation They estimate that in the mid-2000s house prices might have been between 23 (inthe case of Boston) and 50 percent (in the case of Manhattan) lower if regulation had not greatlystagnated new permits (Glaeser et al 2006 2005b) In the US the impact of regulation mayalso explain some of the house price dispersion across American housing markets (Glaeser et al2005a) Similar effects have been documented for other countries such as the UK (Cheshireand Hilber 2008)

To summarize the rise of residential land prices in the second half of the 20th centuryconstitutes much less of a puzzle than their stability in the preceding eight decades Whenthe effects of the transport revolution faded land increasingly became a fixed factor Twoadditional factors are likely to have pushed up land prices even more rising expendituresshares for housing services and growing restrictions on land use

7 Conclusion

In The Wizard of Oz Dorothyrsquos house is transported by a tornado to a strange new plot ofland The story illuminates the fact that a home consists of both the structure of the houseand the underlying land The findings of our study illustrate that it is in fact the price of landthat has been the most significant element for long-run trends in home prices

We show that after a long period of stagnation from 1870 to the mid-20th century houseprices rose strongly in real terms during the second half of the 20th century albeit with consid-erable cross-country heterogeneity These patterns in the data cannot be explained with qualityimprovements or composition shifts in the index Moreover urban and rural house prices haverisen in lockstep in recent decades and farmland prices have also increased

The decomposition of house prices into the replacement cost of the structure and land

40

prices reveals that land prices have been the driving force for the observed trends Residentialland prices have remained constant for almost the first hundred years of modern economicgrowth from the late 19th century until the post-World War II decades but increased stronglythereafter in most countries Stated differently explanations for the long-run trajectory ofhouse prices must be mapped onto the underlying land price dynamics

In this paper we presented two explanations for the trajectory of land prices in moderneconomic history The two explanations complement each other but they are not exclusiveFirst we demonstrated how the transport revolution in the late 19th and early 20th century ledto a substantial drop in transport costs which triggered an increase of land supply This declinein transport costs petered out in the second half of the 20th century so that land increasinglybehaved like a fixed factor Second we revealed evidence that expenditure for housing servicesgrew faster than income after World War II In other words housing appears to behave like asuperior good

In our view the combination of both trends helps explain the cross-country trajectory ofland prices in the 19th and 20th century Additional explanations focusing for instance ongrowing government interventions in the housing market aimed at expanding home ownershipor the easing of financial frictions would be complementary as these factors would show up in arising expenditure share Moreover additional explanations will have to align with the stylizedfacts presented here in particular with the prominent increase of the price of land in the secondhalf of the 20th century and the comparatively minor role of changes in the replacement valueof the structure

Research interest in housing markets has surged in the wake of the global financial crisisYet despite its importance for the discipline of macroeconomics the study of housing mar-ket dynamics was hampered by the lack of comparable long-run and cross-country data fromeconomic history Our study closes this gap We hope that with the data presented in thisstudy new avenues for empirical and theoretical research on housing market dynamics andtheir interactions with the macroeconomy will become possible

41

References

Abelson P and D Chung (2004) ldquoHousing Prices in Australia 1970 to 2003rdquo MacquarieUniversity Economics Research Papers 92004

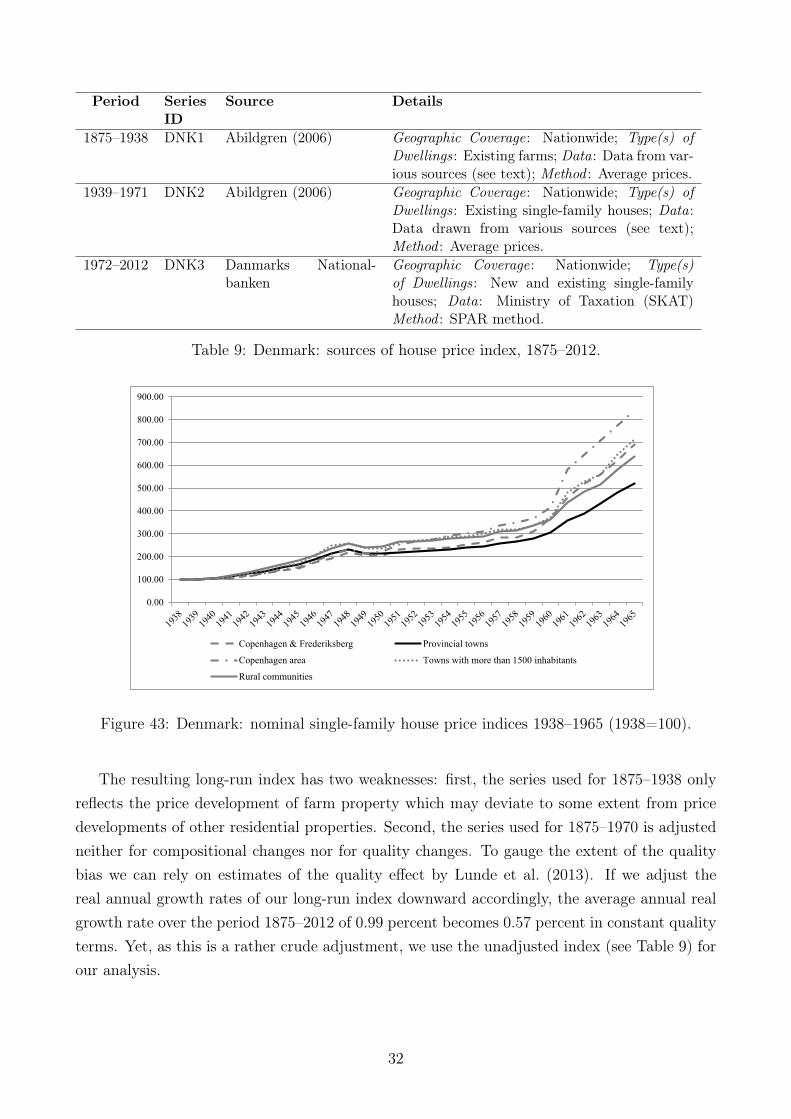

Abildgren K (2006) ldquoMonetary Trends and Business Cycles in Denmark 1875ndash2005rdquo Dan-marks Nationalbank Working Papers 432006

Adam K and M Woodford (2013) ldquoHousing Prices and Robustly Optimal MonetaryPolicyrdquo mimeo

Association of German Municipal Statisticians (various years) Statistisches JahrbuchDeutscher Staumldte Statistisches Jahrbuch Deutscher Gemeinden Association of GermanMunicipal Statisticians

Australian Bureau of Statistics (2013) ldquoHouse Price Indexes Eight CapitalCitiesrdquo httpwwwabsgovauAUSSTATSabsnsfDetailsPage64160Mar202013

OpenDocument

Bailey M J R F Muth and H O Nourse (1963) ldquoA Regression Method for RealEstate Price Index Constructionrdquo Journal of the American Statistical Association 58 933ndash942

Bank for International Settlements (2013) ldquoProperty Price Statisticsrdquo httpwwwbisorgstatisticspphtm

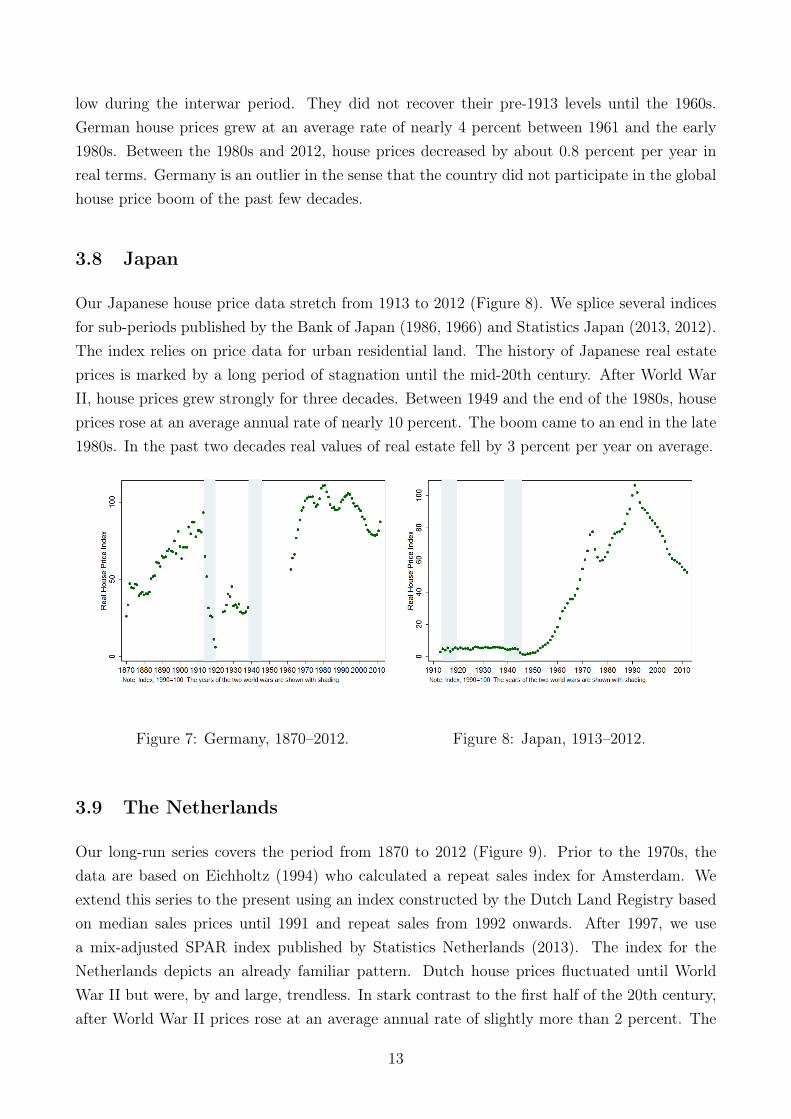

Bank of Japan (1966) Hundred Year Statistics of the Japanese Economy Tokyo Bank ofJapan

mdashmdashmdash (1986) Bank of Japan The First Hundred Years Appendices Tokyo Bank of Japan

Barro R J (2006) ldquoRare Disasters and Asset Markets in the Twentieth Centuryrdquo TheQuarterly Journal of Economics 121 823ndash866

Belgian Association of Surveyors (2013) ldquoABEX Construction Cost Indexrdquo http

wwwabexbemodulesicontentindexphppage=13

Bohlin J (2014) ldquoA Price Index for Residential Property in Goumlteborg 1875ndash2010rdquo in His-torical Monetary and Financial Statistics for Sweden House Prices Stock Returns NationalAccounts and the Riksbank Balance Sheet 1620ndash2012 ed by R Edvinsson T Jacobsenand D Waldenstroumlm Stockholm Ekerlids vol 2

Bordo M D and J Landon-Lane (2013) ldquoWhat Explains House Price Booms Historyand Empirical Evidencerdquo NBER Working Paper 19584

42

Bourassa S C M Hoesli D Scognamiglio and S Zhang (2011) ldquoLand Leverageand House Pricesrdquo Regional Science and Urban Economics 41 134ndash144

Brunsman H G and D Lowery (1943) ldquoFacts from the 1940 Census of Housingrdquo Journalof Land amp Public Utility Economics 19 89ndash93

Butlin N G (1964) Investment in Australian Economic Development 1861ndash1900 Cam-bridge Cambridge University Press

Canadian Real Estate Association (1981) Annual Report 1981 Ottawa Canadian RealEstate Association

Capozza D R and R W Helsley (1989) ldquoThe Fundamentals of Land Prices and UrbanGrowthrdquo Journal of Urban Economics 26 295ndash306

Case B H O Pollakowski and S M Wachter (1991) ldquoOn Choosing BetweenHouse Price Index Methodologiesrdquo American Real Estate and Urban Economics AssociationJournal 19 286ndash307

Case B and J M Quigley (1991) ldquoThe Dynamics of Real Estate Pricesrdquo Review ofEconomics and Statistics 22 50ndash58

Case B and S Wachter (2005) ldquoResidential Real Estate Price Indices as Financial Sound-ness Indicators Methodological Issuesrdquo in Real Estate Indicators and Financial StabilityBasel Bank for International Settlements no 21 in BIS Papers 197ndash211

Case K E (2007) ldquoThe Value of Land in the United Statesrdquo in Land Policies and theirOutcomes ed by G K Ingram and Y-H Hong Cambridge MA Lincoln Institute of LandPolicy

Case K E and J M Quigley (2008) ldquoHow Housing Booms Unwind Income EffectsWealth Effects and Feedbacks through Financial Marketsrdquo European Journal of HousingPolicy 8 161ndash179

Case K E and R J Shiller (1987) ldquoPrices of Single-Family Homes Since 1970 NewIndexes for Four Citiesrdquo New England Economic Review SeptOct 45ndash56

Centre for Urban Economics and Real Estate University of British

Columbia (2013) ldquoCanadian Cities Housing and Real Estate Datardquo http

wwwsauderubccaFacultyResearch_CentresCentre_for_Urban_Economics_

and_Real_EstateCanadian_Cities_Housing_and_Real_Estate_Data

Cheshire P C and C A Hilber (2008) ldquoOffice Space Supply Restrictions in BritainThe Political Economy of Market Revengerdquo The Economic Journal 118 F185ndashF221

43

Conseil General de lrsquoEnvironnement et du Developpement Durable (2013)ldquoLong Run Data Series 1800ndash2010rdquo httpwwwcgedddeveloppement-durablegouv

frrubriquephp3id_rubrique=137

Davis M A and J Heathcote (2005) ldquoHousing and the Business Cyclerdquo InternationalEconomic Review 46 751ndash784

mdashmdashmdash (2007) ldquoThe Price and Quantity of Residential Land in the United Statesrdquo Journal ofMonetary Economics 54 2595ndash2620 data located at Land and Property Values in the USLincoln Institute of Land Policy httpwwwlincolninsteduresources

Davis M A and M G Palumbo (2007) ldquoThe Price of Residential Land in Large USCitiesrdquo Journal of Urban Economics 63 352ndash384

De Bruyne J-P (1956) ldquoLrsquoEvolution des Prix des Immeubles Urbains de lrsquoAgglomerationBruxelloise de 1878 a 1952rdquo Bulletin de lrsquoInstitut de Recherches Economiques et Sociales 2257ndash93

Del Negro M and C Otrok (2007) ldquo99 Luftballons Monetary Policy and the HousePrice Boom across US Statesrdquo Journal of Monetary Economics 54 1962ndash1985

Department for Communities and Local Government (2013)ldquoHouse prices from 1920 annual house price inflation United Kingdomfrom 1970rdquo httpswwwgovukgovernmentstatistical-data-sets

live-tables-on-housing-market-and-house-prices

Deutsches Volksheimstaumlttenwerk (1959) Handhabung des Preisstops Grundstuumlck-spreisentwicklung und Anwendung des Baulandbeschaffungsgesetzes vol 14 of Wis-senschaftliche Untersuchungen und Vortraumlge Cologne Deutsches Volksheimstaumlttenwerk

Eichholtz P M (1994) ldquoA Long-Run House Price Index The Herengracht Index 1628ndash1973rdquo Real Estate Economics 25 175ndash192

Eitrheim O and S K Erlandsen (2004) ldquoHouse Price Indices for Norway 1819ndash2003rdquoin Historical Monetary Statistics for Norway 1819ndash2003 ed by O Eitrheim J T Klovlandand J F Ovigstad Oslo Norges Bank no 35 in Norges Bank Skriftserie OccasionalPapers

European Commission (2013) ldquoHandbook on Residential Property Price Indices (RPPIs)rdquoeurostat Methodologies and Working papers

Federal Housing Finance Agency (2013) ldquoHouse Price Indexesrdquo httpwwwfhfa

govDefaultaspxPage=87

44

Federal Statistical Office of Germany (various years) Kaufwerte fuumlr Bauland Fach-serie 17 Reihe 5 Wiesbaden Federal Statistical Office of Germany

Feinstein C H and S Pollard (1988) Studies in Capital Formation in the UnitedKingdom 1750ndash1920 Oxford Clarendon Press

Fernandez-Kranz D and M T Hon (2006) ldquoA Cross-Section Analysis of the IncomeElasticity of Housing Demand in Spain Is There a Real Estate Bubblerdquo Journal of RealEstate Financial Economics 32 449mdash470

Firestone O J (1951) Residential Real Estate in Canada Toronto University of TorontoPress

Fishback P V and T Kollmann (2012) ldquoNew Multi-City Estimates of the Changes inHome Values 1920-1940rdquo NBER Working Paper 18272

Fishback P V J Rose and K Snowden (2013) Well Worth Saving How the NewDeal Safeguarded Home Ownership Chicago University of Chicago Press

Fleming M (1966) ldquoThe Long-Term Mesurement of Construction Costs in the United King-domrdquo Journal of the Royal Statistical Society 129 534ndash556

Francke M and A van de Minne (2013) ldquoLand Structure and Depreciationrdquo ResearchPaper Universiteit van Amsterdam

Geltner D and D Ling (2006) ldquoConsiderations in the Design and Construction of Invest-ment Real Estate Research Indicesrdquo Journal of Real Estate Research 28 411ndash444

General Register Office (1951) Census 1951 England and Wales Preliminary ReportLondon HMSO

Glaeser E L J D Gottlieb and K Tobio (2012) ldquoHousing Booms and City CentersrdquoAmerican Economic Review 102 127ndash133

Glaeser E L and J Gyourko (2003) ldquoThe Impact of Building Restrictions on HousingAffordabilityrdquo FRBNY Economic Policy Review 9 21ndash39

Glaeser E L J Gyourko and R Saks (2005a) ldquoWhy Have Housing Prices Gone UprdquoAmerican Economic Review 95 329ndash333

mdashmdashmdash (2005b) ldquoWhy is Manhattan So Expensive Regulation and the Rise in House PricesrdquoJournal of Law and Economics 48 331ndash370

Glaeser E L and J E Kohlhase (2004) ldquoCities Regions and the Decline of TransportCostsrdquo Papers in Regional Science 83 197ndash228

45

Glaeser E L J Kolko and A Saiz (2001) ldquoConsumer Cityrdquo Journal of EconomicGeography 1 27ndash50

Glaeser E L J Schuetz and B A Ward (2006) Regulation and the Rise of Hous-ing Prices in Greater Boston Boston MA Pioneer Institute for Public Policy ResearchCambridge MA Rappaport Institute for Greater Boston

Glaeser E L and B A Ward (2009) ldquoThe Causes and Consequences of Land UseRegulation Evidence from Greater Bostonrdquo Journal of Urban Economics 65 265ndash278

Goodhart C and B Hofmann (2008) ldquoHouse Prices Money Credit And the Macroe-conomyrdquo Oxford Review of Economic Policy 24 180ndash205

Grebler L D M Blank and L Winnick (1956) Capital Formation in ResidentialReal Estate Trends and Prospects Princeton Princeton University Press

Gyourko J C Mayer and T Sinai (2006) ldquoSuperstar Citiesrdquo American EconomicJournal 5 167ndash199

Harley C (1980) ldquoTransportation the World Wheat Trade and the Kuznets Cycle 1850ndash1913rdquo Explorations in Economic History 17 218ndash250

mdashmdashmdash (1988) ldquoOcean Freight Rates and Productivity 1740ndash1913 The Primacy of MechanicalInvention Reaffirmedrdquo Journal of Economic History 48 851ndash875

Hendershott P H and T G Thibodeau (1990) ldquoThe Relationship between Medianand Constant Quality House Prices Implications for Setting FHA Loan Limitsrdquo Real EstateEconomics 18 323ndash334

Hornstein A (2009a) ldquoNote on a Model of Housing with Collateral Constraintsrdquo FRBRichmond Working Paper 09-3

mdashmdashmdash (2009b) ldquoProblems for a Fundamental Theory of House Pricesrdquo FRB Richmond Eco-nomic Quarterly 95 1ndash24

Hummels D (2007) ldquoTransportation Costs and International Trade in the Second Era ofGlobalizationrdquo Journal of Economic Perspectives 21 131ndash154

Jacks D S and K Pendakur (2010) ldquoGlobal Trade and the Maritime Transport Revo-lutionrdquo The Review of Economics and Statistics 92 745ndash755

Janssens P and P de Wael (2005) 50 Jaar Belgische Vastgoedmarkt Waar GeschiedenisTot Toekomst Vergroeit Brussels Roularta Books

Jordagrave O M Schularick and A M Taylor (2014) ldquoBetting the Houserdquo mimeo

46

Land Registry (2013) ldquoHouse Price Indexrdquo httpwwwlandregistrygovukpublic

house-prices-and-sales

Leamer E E (2007) ldquoHousing IS the Business Cyclerdquo in Proceedings - Economic PolicySymposium - Jackson Hole ed by F K City 149ndash233

Mack A and E Martiacutenez-Garciacutea (2012) ldquoA Cross-Country Quarterly Database of RealHouse Prices A Methodological Noterdquo FRB Dallas Globalization and Monetary Policy In-stitute Working Paper 99

MacLaughlin R B (2012) ldquoLand Use Regulation Where Have We Been Where Are WeGoingrdquo Cities 29 S50ndashS55

Maiwald K (1954) ldquoAn Index of Building Costs in the United Kingdom 1845ndash1938rdquo TheEconomic History Review 7 187ndash203

Matti W (1963) ldquoHamburger Grundeigentumswechsel und Bauland 1903ndash1907 und 1955ndash1962rdquo Hamburg in Zahlen Monatsschrift des Statistischen Landesamtes der Freien undHansestadt Hamburg

Mian A and A Sufi (2014) ldquoHouse Price Gains and US Household Spending from 2002to 2006rdquo mimeo

Mitchell B (2013) ldquoInternational Historical Statistics 1750ndash2010 [Online]rdquo httpwwwpalgraveconnectcompcdoifinder1010579781137305688

Mohammed S I and J G Williamson (2004) ldquoFreight Rates And Productivity GainsIn British Tramp Shipping 1869-1950rdquo Explorations in Economic History 41 172ndash203

National Institute of Statistics and Economic Studies (2012) ldquoComptesdu Logement 2011 Tableaux de Donnees 2011 et Series Chronologiques 1984ndash2011rdquo httpwwwstatistiquesdeveloppement-durablegouvfrpublicationsp

referencescomptes-logement-2011-premiers-resultats-2012html

Nichols D A (1970) ldquoLand and Economic Growthrdquo American Economic Review 60 332ndash340

Norges Eiendomsmeglerforbund (2012) ldquoBoligprissstatistikkrdquo httpwwwnefno

xppubtoppboligprisstatistikk

North D (1958) ldquoOcean Freight Rates and Economic Development 1750ndash1913rdquo Journal ofEconomic History 18 537ndash555

mdashmdashmdash (1965) ldquoThe Role of Transportation in the Economic Development of North Americardquoin Les Grandes voies maritimes dans le monde XV-XIX siecles ed by International Commit-tee of Historical Sciences Commission internationale drsquohistoire maritime Paris SEVPEN

47

OECD (2014) OECDStat Paris OECD

Piketty T (2014) Capital in the Twenty-First Century Cambridge Harvard UniversityPress

Piketty T and G Zucman (2014) ldquoCapital Is Back Wealth-to-Income Ratios in RichCountries 1700ndash2010rdquo Quarterly Journal of Economics 129

Ricardo D (1817) Principles of Political Economy and Taxation

Schularick M and A M Taylor (2012) ldquoCredit Booms Gone Bust Monetary PolicyLeverage Cycles and Financial Crises 1870ndash2008rdquo American Economic Review 102 1029ndash1061

Shiller R J (1993) ldquoMeasuring Asset Values for Cash Settlement in Derivative MarketsHedonic Repeated Measures Indices and Perpetual Futuresrdquo Journal of Finance 48 911ndash931

mdashmdashmdash (2009) Irrational Excuberance New York Broadway Books 2nd revised and updateded

Silver M (2012) ldquoWhy House Price Indexes Differ Measurement and Analysisrdquo IMF Work-ing Paper 12125

Soumlderberg J S Bloumlndal and R Edvinsson (2014) ldquoA Price Index for Residen-tial Property in Stockholm 1875ndash2012rdquo in Historical Monetary and Financial Statistics forSweden House Prices Stock Returns National Accounts and the Riksbank Balance Sheet1620ndash2012 ed by R Edvinsson T Jacobsen and D Waldenstroumlm Stockholm Ekerlidsvol 2

Stapledon N (2007) ldquoLong Term Housing Prices in Australia and Some Economic Perspec-tivesrdquo PhD thesis University of New South Wales Sydney

mdashmdashmdash (2012a) ldquoHistorical Housing-Related Statistics for Australia 1881ndash2011 ndash A Short NoterdquoUNSW Australian School of Business Research Paper 522012

mdashmdashmdash (2012b) ldquoTrends and Cycles in Sydney and Melbourne House Prices from 1880 to 2011rdquoAustralian Economic History Review 52 203ndash217

Statistical Office of the City of Helsinki (various years) Helsinki Statistical Year-book Helsinki Helsingin Kaupungin Tilastokonttorin

Statistics Belgium (2013) ldquoBouw En Industrie - Verkoop Van Onroerende Goed-eren 1986ndash2012rdquo httpstatbelfgovbenlmodulespublicationsstatistiques

economiedownloadsbouw_en_industrie_verkoop_onroerende_goederenjsp

48

Statistics Berlin (various years) Statistisches Jahrbuch der Stadt Berlin Berlin StatisticsBerlin

Statistics Canada (various years) Canada Year Book Ottawa

Statistics Finland (2011) ldquoPrices of Dwellings in Housing Companiesrdquo http

wwwstatfitilashi201102ashi_2011_02_2011-07-29_laa_001_enhtml2

Methodologicaldescription

Statistics Japan (2012) ldquoHistorical Statistics of Japanrdquo httpwwwstatgojp

englishdatachoukiindexhtm

mdashmdashmdash (2013) ldquoJapan Statistical Yearbook 2013rdquo httpwwwstatgojpenglishdata

nenkanindexhtm

Statistics Netherlands (2013) ldquoPrijzen Bestaande Koopwoningenrdquo httpwwwcbsnlnl-NLmenuthemasprijzencijfersdefaulthtm

Summerhill W (2006) ldquoThe Development of Infrastructurerdquo in The Cambridge EconomicHistory of Latin America ed by V Bulmer-Thomas J H Coatsworth and R C CondeCambridge MA Cambridge University Press vol 2 293ndash326

Swiss Federal Statistical Office (2013) ldquoStadt Zuumlrich Handaumlnderungen von Grund-stuumlcken nach Art des Kaufs 1899ndash1990rdquo httpwwwbfsadminchbfsportalde

indexinfotheklexikonlex2Document81325xls

Taylor G R (1951) The Transportation Revolution 1815ndash1860 vol 4 of Economic Historyof the United States ME Sharpe

United Nations (2014) On-line Data Urban and Rural Population New York UnitedNations

US Bureau of the Census (1975) Historical Statistics of the United States ColonialTimes to 1970 Washington US Dept of Commerce Bureau of the Census

von Thuumlnen J H (1826) Der isolierte Staat in Beziehung auf Landwirtschaft und Nation-aloumlkonomie

Wickens D L (1937) Financial Survey of Urban Housing Statistics on Financial Aspectsof Urban Housing Washington US Department of Commerce

Williamson J and K OrsquoRourke (1999) Globalization and History Cambridge MA MITPress

Wuumlest and Partner (2012) Immo-Monitoring 2012-1

49

No Price Like HomeGlobal House Prices 1870ndash2012

Appendix

1

Contents

Contents 2

A Supplementary material 3

A1 Land heterogeneity and transportation costs 3

A2 A brief review of the theoretical literature 4

A3 Housing expenditure share 5

A4 Figures and tables 7

B Data appendix 8

B1 Description of the methodological approach 8

B2 Australia 10

B3 Belgium 18

B4 Canada 23

B5 Denmark 29

B6 Finland 33

B7 France 37

B8 Germany 41

B9 Japan 48

B10 The Netherlands 53

B11 Norway 56

B12 Sweden 60

B13 Switzerland 63

B14 United Kingdom 67

B15 United States 74

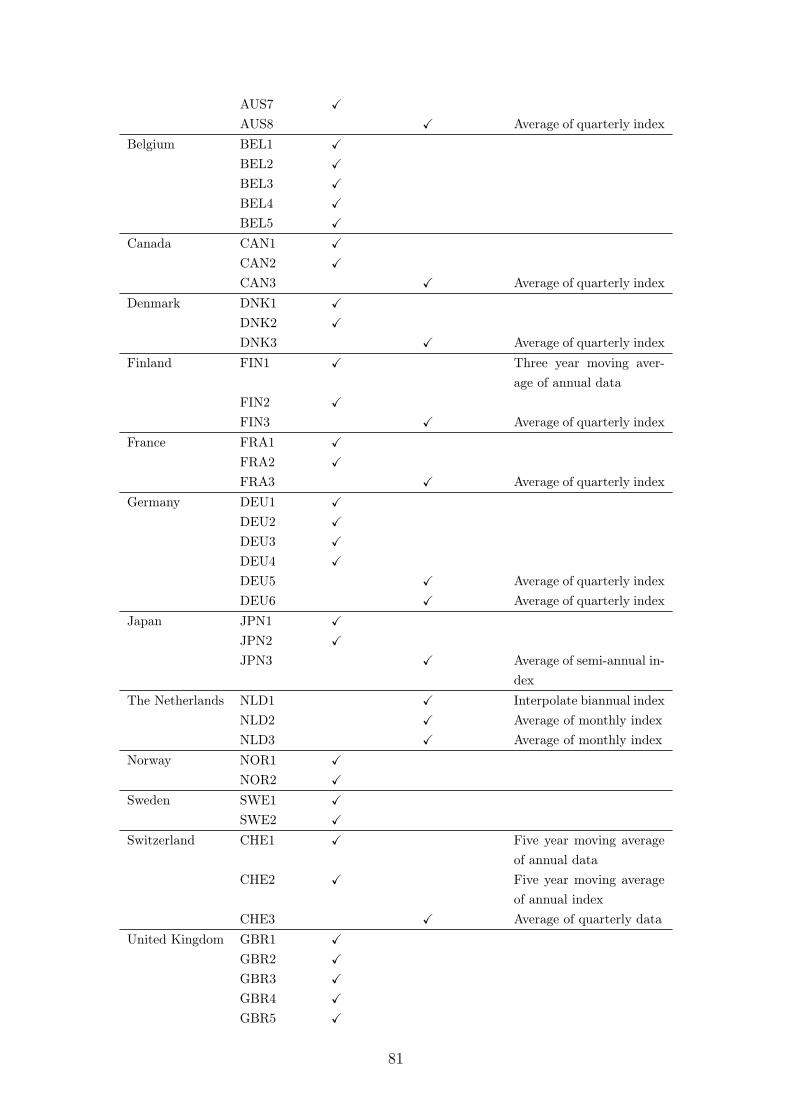

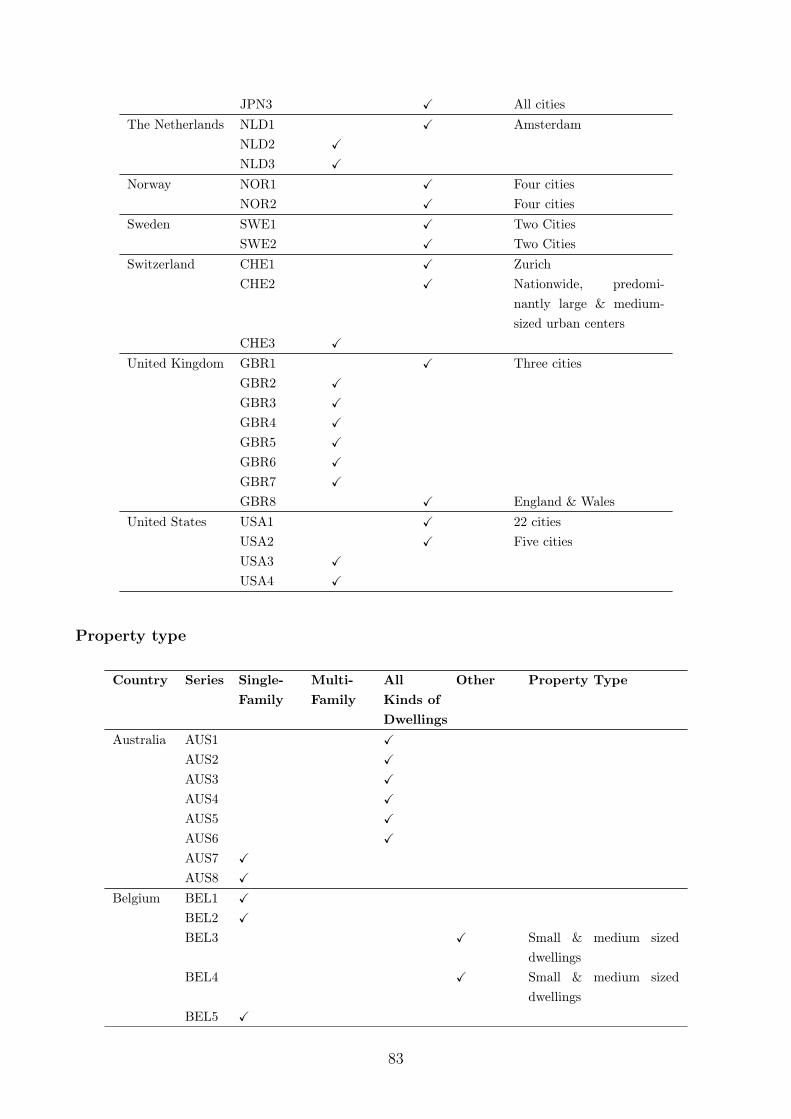

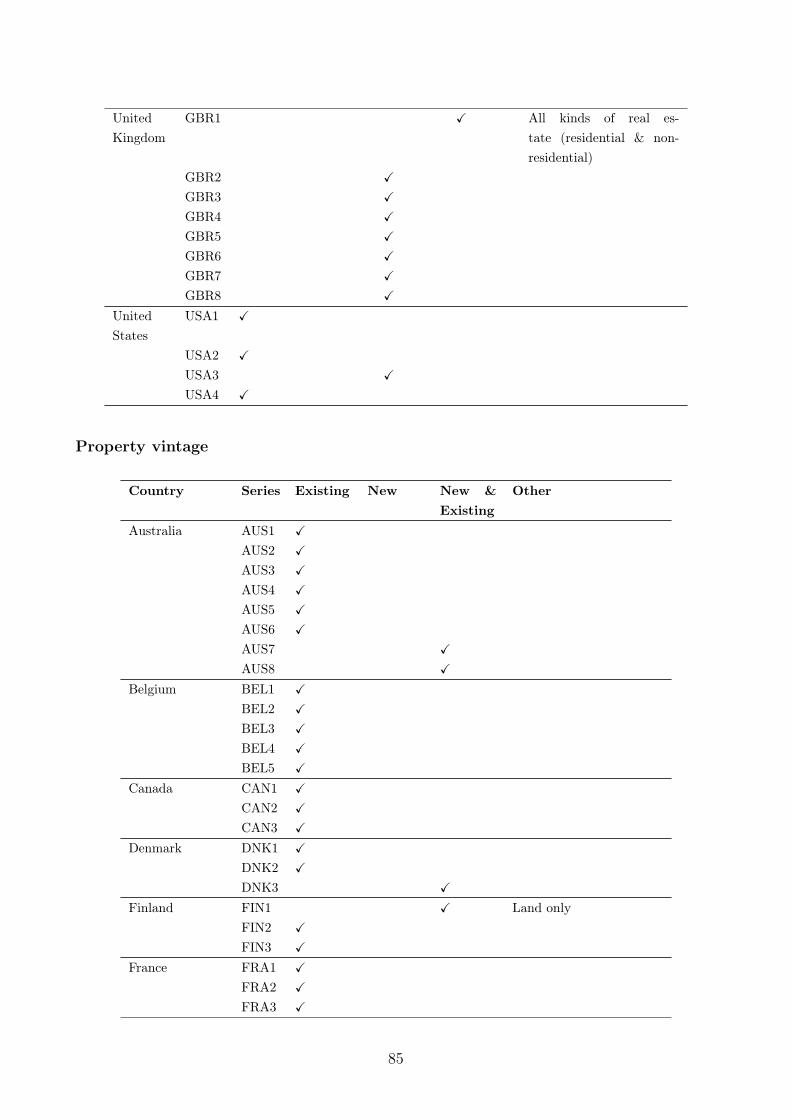

B16 Summary of house price series 80

References 90

2

Appendix

A Supplementary material

A1 Land heterogeneity and transportation costs

This brief section demonstrates how to solve the land price model in the spirit of Ricardo andvon Thuumlnen presented in section 62 for the land price The notation is as explained in themain text We start with the labor market equilibrium for a given number of active firms iFrom the first-order condition for optimal labor demand w = (1 ai)crarr(Li)crarr1 (recall Zi = 1)the individual labor demand schedule reads

Li(w) =

crarr(1 ai)

w

11crarr

(8)

The equilibrium wage rate w results from the labor market clearing condition which equatesaggregate labor demand

R i

0 Li(w)di and aggregate labor supply LS Noting Equation 8 onegets

Z i

0

crarr(1 ai)

w

11crarr

di = Ls (9)

where i denotes the number of active firms in equilibrium which is treated as unknown at thisstage Determining the definite integral on the LHS of Equation 9 and solving with respect tow gives w = w(i a) At this stage individual labor demand in equilibrium L

i (w) can be

determined for any given i

Next we turn to the land market The competitive land return is given by the marginalproduct of land in output production net of transportation costs ie

vZi =(1 ai)Yi

Zi

= (1 ai)(1 crarr)(Li)crarr (10)

The price pZi of land plot i 2 [0 i] is given by the present value of the infinite stream of landreturns ie pZi =

R1t

vZi ()er(t)d Given that vZi is constant in equilibrium the land price

may be expressed as pZi = vZi r A specific land plot i is being developed if the land priceexceeds the development costs ie pZi k Therefore the number of developed land plots inequilibrium i equal to the number of active firms is determined by the following condition

(1 ai)(1 crarr) [Li(w

)]crarr

r= k (11)

where Li(w

) is equilibrium labor demand of the marginal firm i = i The preceding equationnoting w = w(i a) determines the number of active firms as a function of a ie i = i(a)

3

The aggregate land price is defined as pZ = 1i

R i

0 pZi di Noting pZi = vZi r and vZi =

(1 ai)(1 crarr)(Li)crarr pZi may be expressed as follows

pZ =1

i(a)

Z(1)z|i(a)

0

(1

(2)z|a i)(1 crarr)[L

i (w(i(

(3)z|a )))]crarr

rdi (12)

where (1) indicates the composition effect (2) the revaluation effect and (3) the comple-mentary factor effect respectively The RHS of the preceding equation indicates how a changein a influences the equilibrium land price

A2 A brief review of the theoretical literature

This section provides a brief review of the theoretical literature on the housing market Davisand Heathcote (2005) set up a multi-sector growth model with housing production The focusis however not on the evolution of aggregate house prices but on stylized business cycle factsassociated with residential and non-residential investments Hornstein (2009ba) followingDavis and Heathcote sets up a general equilibrium model that captures a housing market Thefocus is on the surge in house prices in the US between 1975 and 2005 The main drivingforce is the increasing relative scarcity of land as measured by the difference between thegrowth rate of per capita income and the growth rate at which new land becomes availableDavis and Heathcote (2007 2597) have found based on empirical work for the US over1975 to 2005 that both trend growth in house prices and cyclical house price fluctuations areprimarily attributable to changes in the price of residential land and not to changes in the priceof structure Hornstein argues that this model has the clear potential to account for the trendin prices of new houses although it cannot account for the differential price trends in the marketfor new and existing houses Li and Zeng (2010) employ a two-sector neoclassical growth modelwith housing to explain a rising real house price driven by a comparably low technical progressin the construction sector Poterba (1984) employs a dynamic model of the housing sector tostudy how inflation affects the real house price and the size of the housing stock He argues thatpersistent high inflation rates reduces homeownersrsquo user cost and may lead to an increase inhouse prices and the housing stock Glaeser et al (2005a) show that focusing on the US sincethe 1970s changes in the housing-supply regulations caused house prices to increase Glaeserand Gottlieb (2009 44) stress that urbanization induced by agglomeration economies andinelastic housing supply in cities pushes the aggregate housing prices upwards

4

A3 Housing expenditure share

Consider a perfectly competitive and static economy with two sectors In the manufacturingsector labor L is combined with land ZM to produce consumption goods M Moreover realestate development firms combine structures X and land ZH to produce residential servicesOne house generates one unit of housing services As the model describes a static economythere is no stock of houses that may accumulate over time The house price and the price forhousing services therefore coincide The sectoral production functions read as follows

M = (L)1crarr ZMcrarr

(13)

H = (X)1 ZH

(14)

where 0 lt crarr lt 1 denote constant technology parameters Only the intersectoral allocationof land is endogenous whereas L and X are fixed18 Aggregate income is given by PY =

pMM + pHH where P = 1 denotes the price level pM the (real) price of the manufacturinggood and pH the (real) price of residential services Let 0 lt lt 1 denote the share of incomedevoted to housing services ie = pHH

Y Equilibrium in the market for residential services is

then described by19

pHH = Y (15)

Total land supply is fixed and normalized to one The land constraint reads ZM + ZS = 1The intersectoral land allocation is determined by the equality of the competitive land returnsacross sectors ie

pMcrarrM

ZM= pH

H

ZH (16)

The land return equals the land price in this static model ie pZ = pMcrarr MZM The equi-

librium share of land allocated to the housing sector turns out to read ZH = (crarr)+crarr

Noticethat unsurprisingly the share of land allocated to the housing sector increases with the housingexpenditure share ie ZH

gt 0

What is the consequence of a rising housing expenditure share with respect to the landprice pZ The answer is provided by

Proposition 1 The equilibrium land price pZ reads as follows18One can easily modify this simplifying assumption without major implications19Due to Walrasrsquo law the market for manufacturing goods clears as well

5

pZ = Y [( crarr) + crarr]

Proof Solving Y = pMM + pHH Equations 15 16 and ZM +ZH = 1 with respect to ZH pM

and pH gives

ZH =

( crarr) + crarr (17)

pH = Y

H (18)

pM = (1 )Y

M (19)

Combining pZ = pMcrarr M1ZH with Equations 17 and 19 proves proposition 1 The same result

is of course obtained if one alternatively combines pZ = pH HZH with Equation 17 and 18

If gt crarr then an increase in the demand for housing services as captured by an increasing leads to a higher land price The reason is simple The production of housing services reliesmore heavily on land compared to manufacturing in the sense that the cost share of land inthe production of housing services = pZZH

pHHexceeds the cost share of land in manufacturing

crarr = pZZM

pMM An increase in means that the demand for housing services rises while the demand

for manufacturing goods falls Because land is more important in housing services productionthan in manufacturing the aggregate demand for land goes up Given that the land supply isfixed the land price increases

A back-of-the-envelope calculation may be instructive Real (mean) GDP grew by a factorof 72 from 1950 to 2012 For the expenditure share we employ a factor of 16520 The landshare in the housing sector is set to = 05 (see Table 5) Unfortunately long run data on thecost share of land in manufacturing crarr are not available Nonetheless it is instructive to noticethat Equation 1 implies that pZ should grow by a factor of 114 if crarr = 005 whereas pZ shouldgrow by a factor of 91 if crarr = 03 That is the differential impact of a rising on the land priceranges between 26 percent (9172 1) and 58 percent (11472 1) the reported 42 percent increasein the main text represents an intermediate value Notice that for = const the land price

20The expenditure share droped remarkably in the aftermath of World War I and World War II by much morethan GDP and then recovered quickly within a couple of years back to its respective pre-war levels cf Figure31 The value in 1950 marks the lower turning point after World War II and hence represents an unusuallylow number We therefore consider the proportional increase between the expenditure share in 2012 and theaverage value before 1950

6

increases by a factor of 72 due to GDP growth Recall also that our imputed land price asdisplayed in Figure 26 grew by a factor of 113

A4 Figures and tables

Figure 32 Imputed land prices - sensitivity analysis

Figure 33 Imputed land prices - individual countries

7

AUS CAN CHE DEU DNK FRA GBR ITA JPN NLD NOR SWE USA18701880 075 013 052 025 074 020 0301890 0401900 054 070 018 051 062 023 040 029 04819131914 043 073 020 052 030 040 028 043 031 0511920 0511930 040 061 017 046 030 023 031 052 034 0491940 054 017 045 019 033 046 033 0431950 049 056 017 028 032 017 025 065 015 0291960 040 052 017 032 030 012 026 085 031 0461970 048 048 025 038 030 015 028 086 038 031 0471980 040 052 048 030 041 011 026 081 038 032 0471990 062 047 036 042 0902000 063 049 032 039 081 0572010 071 053 037 059 077 053Note Dates are approximate Sources See Appendix B

Table 5 Share of land in total housing value

B Data appendix

This data appendix supplements our working paper No Price Like Home Global HousePrices 1870ndash2012 The main purpose of this appendix is to provide an overview about thedata sources we had at our disposal and discuss all relevant details of the sources we finallyused for constructing our long-run house price indices We present residential house priceindices for 14 advanced economies that cover the years 1870 to 2012

A large number of researchers and statisticians offered advice helped in locating data andshared their data sources We wish to thank Paul de Wael Christopher Warisse Willy Biese-mann Guy Lambrechts Els Demuynck and Erik Vloeberghs (Belgium) Debra Conner Gre-gory Klump Marvin McInnis (Canada) Kim Abildgren Finn Oslashstrup and Tina Saaby Hvolboslashl(Denmark) Riitta Hjerppe Kari Levaumlinen Juhani Vaumlaumlnaumlnen and Petri Kettunen (Finland)Jacques Friggit (France) Carl-Ludwig Holtfrerich Petra Hauck Alexander Nuumltzenadel Ul-rich Weber and Nikolaus Wolf (Germany) Alfredo Gigliobianco (Italy) Makoto Kasuya andRyoji Koike (Japan) Alfred Moest (The Netherlands) Roger Bjornstad and Trond AmundSteinset (Norway) Daniel Waldenstroumlm (Sweden) Annika Steiner Robert Weinert Joel FlorisFranz Murbach Iso Schmid and Christoph Enzler (Switzerland) Peter Mayer Neil MonneryJoshua Miller Amanda Bell Colin Beattie and Niels Krieghoff (United Kingdom) JonathanD Rose Kenneth Snowden and Alan M Taylor (United States) Magdalena Korb helped withtranslation

B1 Description of the methodological approach

Data sources

Most countriesrsquo statistical offices or central banks began only recently to collect data on houseprices For the 14 countries covered in our sample data from the early 1970s to the present

8

can be accessed through three principal internationally recognized repositories the databasesmaintained by the Bank for International Settlements (2013) the OECD and the FederalReserve Bank of Dallas (2013) To extend these back to the 19th century we used threeprincipal types of country specific data

First we turn to national official statistical publications such as the Helsinki StatisticalYearbook or the annual publications of the Swiss Federal Statistical office and collectionsof data based on official statistical abstracts Typically such official statistics publicationscontained raw data on the number and value of real estate transactions and in some casesprice indices A second key source are published and unpublished data gathered by legal or taxauthorities (eg the UK Land Registry ) or national real estate associations (eg the CanadianReal Estate Association) Third we can also draw on the previous work of financial historiansand commercial data providers

Selection of house price series

Constructing long-run data series usually involves a good many compromises between the idealand the available data This is also true for each of our 14 house price indices Typicallywe found series for shorter periods and had to splice them to arrive at a long-run indexThe historical data we have at our disposal vary across countries and time with respect tokey characteristics (area covered property type frequency etc) and in the method used forindex construction In choosing the best available country-year-series we follow three guidingprinciples constant quality longitudinal consistency and historical plausibility

We select a primary series that is available up to 2012 refers to existing dwellings andis constructed using a method that reflects the pure price change ie controls for changesin composition and quality When extending the series we concentrate on within-countryconsistency to avoid principal structural breaks that may arise from changes in the marketsegment a country index covers We therefore while aiming to ensure the broadest geographicalcoverage for each of the 14 country indices wherever possible and reasonable maintain thegeographical coverage of the indices Likewise we try to keep the type of house covered constantover time be it single-family houses terraced houses or apartments We examine the historicalplausibility of our long-run indices We heavily draw on country specific economic and socialhistory literature as well as primary sources such as newspaper accounts or contemporarystudies on the housing market to scrutinize the general trends and short-term fluctuations inthe indices Based on extensive historical research we are confident that the indices offer areasonably time-consistent picture of house price developments in each of our 14 countries

9

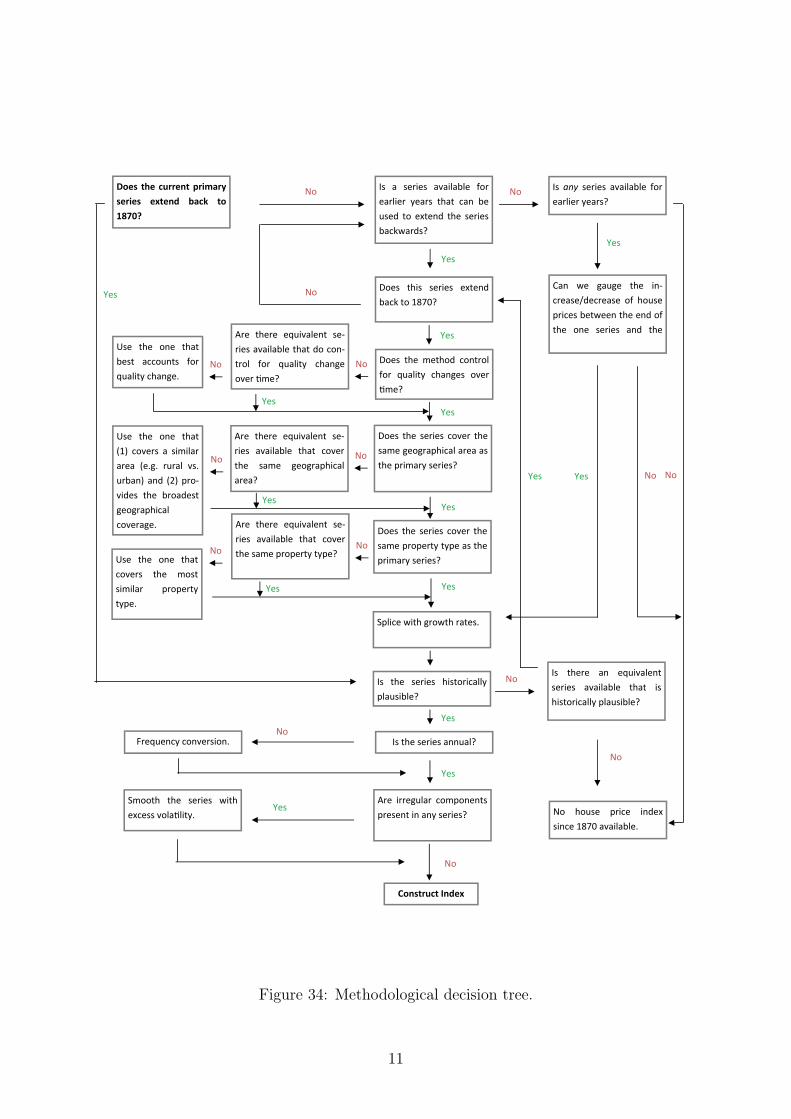

Construct the country indices step by step

The methodological decision tree in Figure 34 describes the steps we follow to construct consis-tent series by combining the available sources for each country in the panel By following thisprocedure we aim to maintain consistency within countries while limiting data distortions Inall cases the primary series does not extend back to 1870 but has to be complemented withother series

Other housing statistics

We complement the house price data with three additional housing related data series prices offarmland construction costs and estimates for the total value of the housing stock For pricesof farmland we again rely on official statistical publications and series constructed by otherresearchers For benchmark data on the total market value of housing and its components(ie structures and land) we turn to the OECD database of national account statistics forthe most recent period (with different starting points depending on the country) We consultthe work of Goldsmith (1981 1985) and also build on more recent contributions such asPiketty and Zucman (2014) (for Australia Canada France Germany Italy Japan the USand UK) and Davis and Heathcote (2007) (for the US) to cover earlier years For dataon construction costs we mostly draw on publications by national statistical offices In somecases we also rely on the work of other scholars such as Stapledon (2012a) Maiwald (1954) andFleming (1966) national associations of builders or surveyors (Belgian Association of Surveyors2013) or journals specializing in the building industry (Engineering News Record 2013) Formacroeconomic and financial variables we rely on the long-run macroeconomic dataset fromSchularick and Taylor (2012) and the update presented in Jordagrave et al (2013)

B2 Australia

House price data

Historical data on house prices in Australia is available for 1870ndash2012

The most comprehensive source for house prices for the Sydney and Melbourne area isStapledon (2012b) His indices cover the years 1880ndash2011 For the sub-period 1880ndash1943 theyare computed from the median asking price for all residential buildings indiscriminate of theircharacteristics and specifics for 1943ndash1949 Stapledon (2012b) estimates a fixed prices21 for1950ndash1970 he uses the median sales price22 For the sub-period 1970ndash1985 Stapledon (2012b)

21Price controls on houses and land were imposed in 1942 and were only removed in 1948 (Stapledon 200723 f)

22The ask price series for residential houses (1880ndash1943) and the sales price series (1948ndash1970) are compiled

10

Does thecurrentprimaryseries extend back to1870

ConstructIndex

Are there equivalent seͲriesavailablethatdoconͲtrol for quality changeoverƟme

Is the series historicallyplausible

IstheseriesannualFrequencyconversion

Are irregular componentspresentinanyseries

Smooth the series withexcessvolaƟlity

YesNo

Yes

Yes

No

Is a series available forearlier years that can beused toextend the seriesbackwards

Is any series available forearlieryears

No No

Does this series extendbackto1870

Can we gauge the inͲcreasedecrease of housepricesbetweentheendofthe one series and the

Does themethod controlfor quality changes overƟme

Does the series cover thesamegeographicalareaastheprimaryseries

Splicewithgrowthrates

Yes

Yes

Yes

Yes

Yes

No

Is there an equivalentseries available that ishistoricallyplausible

No

No

NoDoes the series cover thesamepropertytypeastheprimaryseries

No

Yes

Yes

Use the one thatbest accounts forqualitychange

Use the one that(1) covers a similararea (eg rural vsurban)and (2)proͲvides the broadestgeographicalcoverage

No

No

Use the one thatcovers the mostsimilar propertytype

No

No house price indexsince1870available

No

No

Yes No

Yes

Yes

Yes

Are there equivalent seͲries available that coverthesamepropertytype

Yes

Are there equivalent seͲries available that coverthe same geographicalarea

Figure 34 Methodological decision tree

11

relies on estimates of median house prices by Abelson and Chung (2004) (see below) for 1986ndash2011 he uses the Australian Bureau of Statistics (2013b) (see below) index for establishedhouses

The median house price series compiled by Abelson and Chung (2004)23 for Sydney andMelbourne are constructed from various data sources for the Sydney series they rely on i) a1991 study by Applied Economics and Travers Morgan which draws on sales price data from theLand Title Offices (for 1970ndash1989) and ii) on sales price data from the Department of Housingie the North South Wales Valuer-General Office (for 1990ndash2003) For the Melbourne seriesthe authors rely on previously unpublished sales price data from the Productivity Commissiondrawing in turn on Valuer-General Office (for 1970ndash1979) and Victorian Valuer-General Officesales price data (for 1980ndash2003)

Besides the Sydney and Melbourne house price indices (see above) Stapledon (2007 64 ff)provides aggregate median price series for detached houses for the six Australian state capitals(Adelaide Brisbane Hobart Melbourne Perth Sydney) for the years 1880ndash2006 As houseprice data is ndash with the exception of Melbourne and Sydney ndash not available for the time priorto 1973 the author uses census data on weekly average rents to estimate rent-to-rent ratios24

The rent-to-rent-ratios are then used to estimate mean and median price data for detachedhouses in the four state capitals (Adelaide Brisbane Hobart Perth) based on the weightedmean price series for SydneyndashMelbourne for the time 1901ndash197325 For the years after 1972Stapledon (2007 234 f) uses the Abelson and Chung (2004) series for the period 1973ndash1985and the Australian Bureau of Statistics (2013b) series for 1986ndash2006 (see below)

In addition to Stapledon (2012b 2007) and Abelson and Chung (2004) four early additionalhouse price data series and indices for Sydney and Melbourne are available i) Abelson (1985)provides an index for Sydney for 1925ndash197026 ii) Neutze (1972) presents house price indicesfor four areas in Sydney (1949ndash1967)27 iii) Butlin (1964) presents data for Melbourne (1861ndash

from weekly property market reports in the Sydney Morning Herald and the Melbourne Age The reports arefor auction sales and private treaty sales

23Abelson and Chung (2004) also present series for Brisbane (1973ndash2003) Adelaide (1971ndash2003) Perth (1970ndash2003) Hobart (1971ndash2003) Darwin (1986ndash2003) and Canberra (1971ndash2003) For details on the data sourcesused for these cities see Abelson and Chung (2004 10)

24The ratios are computed from average weekly rents for detached houses in the four state capitals (numer-ators) and a weighted weekly rent calculated from data for Sydney and Melbourne (denominators) Data isavailable for the years 1911 1921 1933 1947 and 1954

25The same method is applied to extend the series backwards ie to the period 1880ndash1900 Each cityrsquos shareof houses is applied for weighting

26Abelson (1985) collects sales and valuation prices from the NSW Valuer-Generalrsquos records for about 200residential lots in each of the 23 local government areas He calculates a mean a median and a repeat valuationindex

27These areas are Redfern (1949ndash1969) Randwick (1948ndash1967) Bankstown (1948ndash1967) and Liverpool (1952ndash1967) He also calculates an average of these four for 1952ndash1967 (Neutze 1972 361) These areas are low tomedium income areas He relies on sales prices In none of the years there are less than ten sales in most yearshe includes data on more than 40 sales (Neutze 1972 363) Neutze does not further discuss the method heused He argues however that his price series can be taken as being typical of all housing

12

1890)28 and iv) Fisher and Kent (1999) compute series of the aggregate capital value of ratableproperties covering the 1880s and 1890s for Melbourne and Sydney

For 1986ndash2012 the Australian Bureau of Statistics (2013b) publishes quarterly indices foreight cities for i) established detached dwellings and ii) project homes The indices are calcu-lated using a mix-adjusted method29 Sales price data comes from the State Valuer-Generaloffices and is supplemented by data on property loan applications from major mortgage lenders(Australian Bureau of Statistics 2009)30

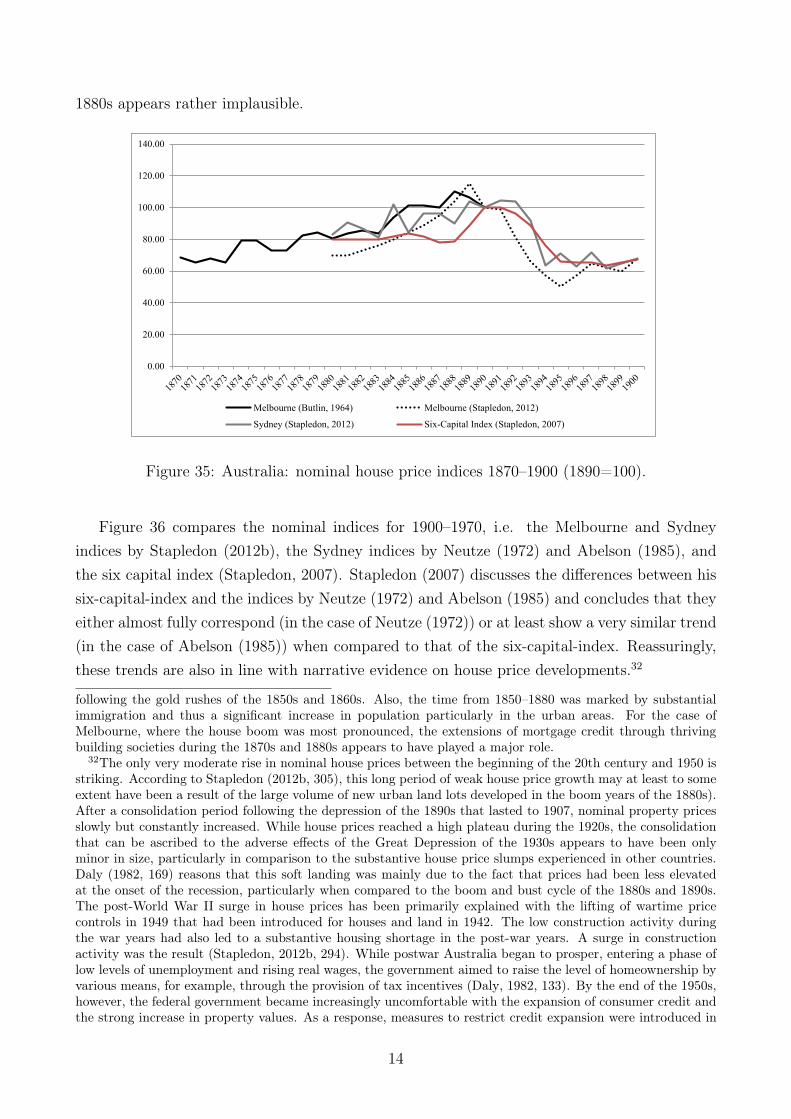

Figure 35 compares the nominal indices for 1860ndash1900 ie an index for Melbourne calcu-lated from Butlin (1964) the Melbourne and Sydney indices by Stapledon (2012b) and thesix capital index (Stapledon 2007) For the years they overlap (1880ndash1890) the four indicesprovide considerable indication of a boom-bust scenario albeit with peaks and troughs stag-gered between two to three years For the 1890s the indices generally show a positive trendwhich culminates between 1888 (Butlin 1964 Melbourne) and 1891 (Stapledon 2012b Syd-ney) The six-capitals-index follows a pattern that is somewhat disjoint and inconsistent withthat picture While from 1880 to 1887 prices are stagnant the boom period is limited to merethree years (1888ndash1891) during which the index reports a nominal increase of house prices inthe six capitals amounting to 25 percent This trajectory however not only differs from theMelbourne and Sydney indices but is also at odds with various accounts (Daly 1982 Stapledon2012b)31 Against this background the stagnation of the six-capital-index during most of the

28According to Stapledon (2007) this series gives a general impression of house price movements after 1860The series is based on advertisements of houses for sale in the newspapers Melbourne Age and Argus Stapledon(2007 16) reasons that by measuring the asking price in terms of rooms rather than houses Butlin partiallyadjusted for quality changes and differences as the average amount of rooms per dwelling rose considerablybetween 1861 and 1890

29The eight cities are Sydney Melbourne Brisbane Adelaide Perth Hobart Darwin Canberra rsquoProjecthomesrsquo are dwellings that are not yet completed In contrast the concept of rsquoestablished dwellingsrsquo refers toboth new and existing dwellings Locational structural and neighborhood characteristics are used to mix-adjust the index ie to control for compositional change in the sample of houses The series are constructedas Laspeyre-type indices The ABS commenced a review of its house price indices in 2004 and 2007 Priorto the 2004 review the index was designed as a price measure for mortgage interest charges to be included inthe CPI The weights used to calculate the index were thus housing finance commitments As part of the 2004review the pricing point has been changed the stratification method improved and the relative value of eachcapital cityrsquos housing stock used as weights In 2007 the stratification was again refined and the housing stockweights were updated Due to the substantive methodological changes of 2004 the ABS publishes two separatesets of indices 1986ndash2005 and 2002ndash2012 (Australian Bureau of Statistics 2009) They move however closelytogether in the years they overlap

30For 1960ndash2004 there also exists an unpublished index calculated by the Australian Treasury (Abelsonand Chung 2004) The index moves closely together with the one calculated by Abelson and Chung (2004)(correlation coefficient of 0995 for the period 1986ndash2003 and 0774 for 1970ndash1985) For the period 1970ndash2012an index is available from the OECD based on the house price index covering eight capital cities publishedby the Australian Bureau of Statistics For the period 1975ndash2012 the Federal Reserve Bank of Dallas splicestogether the index published by the Australian Bureau of Statistics (2013b) and the Treasury house price index

31Daly (1982) provides a graphical analysis of land and housing prices in Sydney for the period 1860ndash1940drawing on data from business records by Richardson and Wrench (at the time one of the largest real estateagents in Sydney) newspaper reports of sales and advertisements Daly (1982 150) and Stapledon (2012b)describe a pronounced property price boom during the 1880s followed by a bust in the 1890s The surge inreal estate prices was primarily spurred by a prolonged period of economic growth during the 1870s and 1880s

13

1880s appears rather implausible

000

2000

4000

6000

8000

10000

12000

14000

Melbourne (Butlin 1964) Melbourne (Stapledon 2012)

Sydney (Stapledon 2012) Six-Capital Index (Stapledon 2007)

Figure 35 Australia nominal house price indices 1870ndash1900 (1890=100)

Figure 36 compares the nominal indices for 1900ndash1970 ie the Melbourne and Sydneyindices by Stapledon (2012b) the Sydney indices by Neutze (1972) and Abelson (1985) andthe six capital index (Stapledon 2007) Stapledon (2007) discusses the differences between hissix-capital-index and the indices by Neutze (1972) and Abelson (1985) and concludes that theyeither almost fully correspond (in the case of Neutze (1972)) or at least show a very similar trend(in the case of Abelson (1985)) when compared to that of the six-capital-index Reassuringlythese trends are also in line with narrative evidence on house price developments32

following the gold rushes of the 1850s and 1860s Also the time from 1850ndash1880 was marked by substantialimmigration and thus a significant increase in population particularly in the urban areas For the case ofMelbourne where the house boom was most pronounced the extensions of mortgage credit through thrivingbuilding societies during the 1870s and 1880s appears to have played a major role

32The only very moderate rise in nominal house prices between the beginning of the 20th century and 1950 isstriking According to Stapledon (2012b 305) this long period of weak house price growth may at least to someextent have been a result of the large volume of new urban land lots developed in the boom years of the 1880s)After a consolidation period following the depression of the 1890s that lasted to 1907 nominal property pricesslowly but constantly increased While house prices reached a high plateau during the 1920s the consolidationthat can be ascribed to the adverse effects of the Great Depression of the 1930s appears to have been onlyminor in size particularly in comparison to the substantive house price slumps experienced in other countriesDaly (1982 169) reasons that this soft landing was mainly due to the fact that prices had been less elevatedat the onset of the recession particularly when compared to the boom and bust cycle of the 1880s and 1890sThe post-World War II surge in house prices has been primarily explained with the lifting of wartime pricecontrols in 1949 that had been introduced for houses and land in 1942 The low construction activity duringthe war years had also led to a substantive housing shortage in the post-war years A surge in constructionactivity was the result (Stapledon 2012b 294) While postwar Australia began to prosper entering a phase oflow levels of unemployment and rising real wages the government aimed to raise the level of homeownership byvarious means for example through the provision of tax incentives (Daly 1982 133) By the end of the 1950showever the federal government became increasingly uncomfortable with the expansion of consumer credit andthe strong increase in property values As a response measures to restrict credit expansion were introduced in

14

0

50

100

150

200

250

1900

1902

1904

1906

1908

1910

1912

1914

1916

1918

1920

1922

1924

1926

1928

1930

1932

1934

1936

1938

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

Sydney (Stapledon 2012) Melbourne (Stapledon 2012)

Sydney (Neutze 1972) Sydney (Abelson 1985)

Six Capital Cities (Stapledon 2007)

Figure 36 Australia nominal house price indices 1900ndash1970 (1960=100)

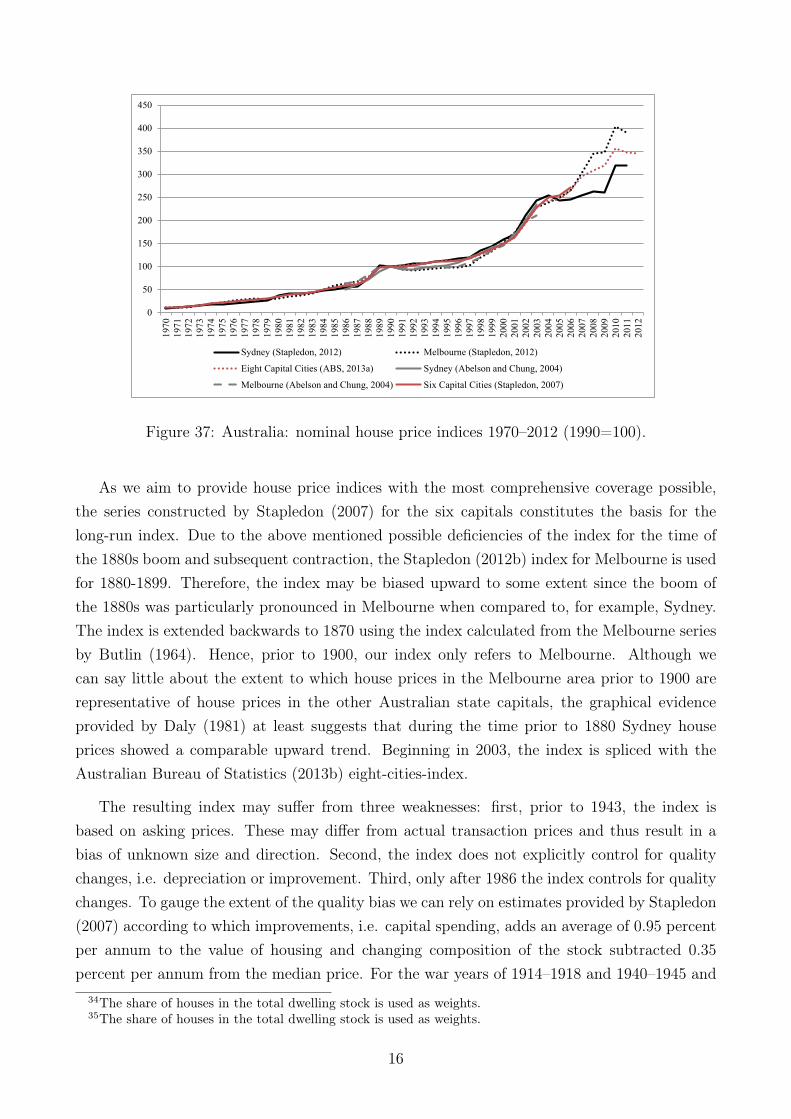

Figure 37 shows the indices which are available for the period 1970ndash2012 the Sydney andMelbourne indices by Stapledon (2012b) indices calculated from the Sydney and Melbourne se-ries by Abelson and Chung (2004) the six-capitals-index by Stapledon (2007) and the weightedindex for eight cities for 1986ndash2012 by the Australian Bureau of Statistics (2013b)33 Despitetheir different geographical coverage all indices for the years from 1970ndash2012 follow a jointalmost identical path It is only after 2004 that the increase in Melbourne property pricesshows to be more pronounced compared to Sydney or the Eight Capital Index

1960 The resulting credit squeeze had an immediate and sizable impact on both the real estate market andthe economy as whole (Stapledon 2007 56) The recovery from this brief interruption was rapid and propertyprices continued to boom

33The ABS series is spliced in 2003 As Stapledon (2012b) draws upon Abelson and Chung (2004) for 1970ndash1985 these series should therefore be identical for this period As Stapledon (2012b) uses the Australian Bureauof Statistics (2013b) series for Sydney and Melbourne for 1986ndash2012 these again should be identical for thisperiod In addition since Stapledon (2007) uses the Australian Bureau of Statistics (2013b) series for eightcapital cities these two indices are identical for post-1986 The Australian Bureau of Statistics (2013b) indexonly starts in 1986

15

0

50

100

150

200

250

300

350

400

450

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Sydney (Stapledon 2012) Melbourne (Stapledon 2012)

Eight Capital Cities (ABS 2013a) Sydney (Abelson and Chung 2004)

Melbourne (Abelson and Chung 2004) Six Capital Cities (Stapledon 2007)

Figure 37 Australia nominal house price indices 1970ndash2012 (1990=100)

As we aim to provide house price indices with the most comprehensive coverage possiblethe series constructed by Stapledon (2007) for the six capitals constitutes the basis for thelong-run index Due to the above mentioned possible deficiencies of the index for the time ofthe 1880s boom and subsequent contraction the Stapledon (2012b) index for Melbourne is usedfor 1880-1899 Therefore the index may be biased upward to some extent since the boom ofthe 1880s was particularly pronounced in Melbourne when compared to for example SydneyThe index is extended backwards to 1870 using the index calculated from the Melbourne seriesby Butlin (1964) Hence prior to 1900 our index only refers to Melbourne Although wecan say little about the extent to which house prices in the Melbourne area prior to 1900 arerepresentative of house prices in the other Australian state capitals the graphical evidenceprovided by Daly (1981) at least suggests that during the time prior to 1880 Sydney houseprices showed a comparable upward trend Beginning in 2003 the index is spliced with theAustralian Bureau of Statistics (2013b) eight-cities-index

The resulting index may suffer from three weaknesses first prior to 1943 the index isbased on asking prices These may differ from actual transaction prices and thus result in abias of unknown size and direction Second the index does not explicitly control for qualitychanges ie depreciation or improvement Third only after 1986 the index controls for qualitychanges To gauge the extent of the quality bias we can rely on estimates provided by Stapledon(2007) according to which improvements ie capital spending adds an average of 095 percentper annum to the value of housing and changing composition of the stock subtracted 035percent per annum from the median price For the war years of 1914ndash1918 and 1940ndash1945 and

34The share of houses in the total dwelling stock is used as weights35The share of houses in the total dwelling stock is used as weights

16

Period Series

ID

Source Details

1870ndash1880 AUS1 Butlin (1964) Geographic Coverage Melbourne Type(s) ofDwellings All kinds of existing dwellings DataAdvertisements in newspapers Method Medianasking prices

1881ndash1899 AUS2 Stapledon (2012b) Geographic Coverage Melbourne Type(s) ofDwellings All kinds of existing dwellings DataAdvertisements in newspapers Method Medianasking prices

1900ndash1942 AUS3 Stapledon (2007) Geographic Coverage Six capital cities Type(s)of Dwellings All kinds of existing dwellingsData Advertisements in newspapers and Cen-sus estimates of average rents Method Medianasking prices

1943ndash1949 AUS4 Stapledon (2007) Geographic Coverage Six capital cities Type(s)of Dwellings All kinds of existing dwellingsData Estimate of the fixed price Method Es-timate of fixed price

1950-1972 AUS5 Stapledon (2007) Geographic Coverage Six capital cities Type(s)of Dwellings All kinds of existing dwellingsData Weekly property reports in newspapersand Census estimates of average rents Method Median sales prices

1973ndash1985 AUS6 Abelson and Chung(2004) as used inStapledon (2007)

Geographic Coverage Six capital cities Type(s)of Dwellings All kinds of existing dwellingsData Data from Land Title Offices (LTOs)Productivity Commission data Valuer-GeneralOffices Method Weighted average of medianprices34

1986ndash2002 AUS7 Australian Bureauof Statistics (2013b)as used in Stapledon(2007)

Geographic Coverage Six capital cities Type(s)of Dwellings New and existing detached housesData Data from State Valuer-General Officessupplemented by data on property loan appli-cations from major mortgage lenders Method Weighted average of mix-adjusted house priceindices35

2003ndash2012 AUS8 Australian Bureau ofStatistics (2013b)

Geographic Coverage Eight capital citiesType(s) of Dwellings New and existing de-tached houses Data Data from State Valuer-General Offices supplemented by data on prop-erty loan applications from major mortgagelenders Method Mix adjustment

Table 6 Australia sources of house price index 1870ndash2012

17

the depression periods 1891ndash1895 and 1930ndash1935 Stapledon (2007) assumes 055 percent perannum These estimates are in line with Abelson and Chung (2004) If we adjust the growthrates of our long-run series downward accordingly the average annual real growth rate over theperiod 1870ndash2012 of 168 percent becomes 111 percent in constant quality terms As this is arather crude adjustment we use the unadjusted index (see Table 6) for our analysis

Housing related data

Construction costs 1881ndash2012 Stapledon (2012a Table 2) - Construction costs of new dwellingsand alterations and additions

Residential land prices 1880sndash2005 Stapledon (2007 29 ff) - Real price series of lots atthe urban fringe period averages

Building activity 1956ndash2012 Australian Bureau of Statistics (2013a)

Homeownership rates 1911ndash2006 (benchmark dates) Australian Bureau of Statistics (var-ious years)

Value of housing stock Goldsmith (1985) and Garland and Goldsmith (1959) provide es-timates of the value of total housing stock dwellings and land for the following benchmarkyears 1903 1915 1929 1947 1956 1978 Data for 1988ndash2011 is drawn from OECD (2013)Piketty and Zucman (2014) present data on the value of household wealth in land and dwellingsfor 1959ndash2011

Household consumption expenditure on housing 1870ndash1939 Butlin (1985 Table 8) 1960ndash2012 Australian Bureau of Statistics (2014)

B3 Belgium

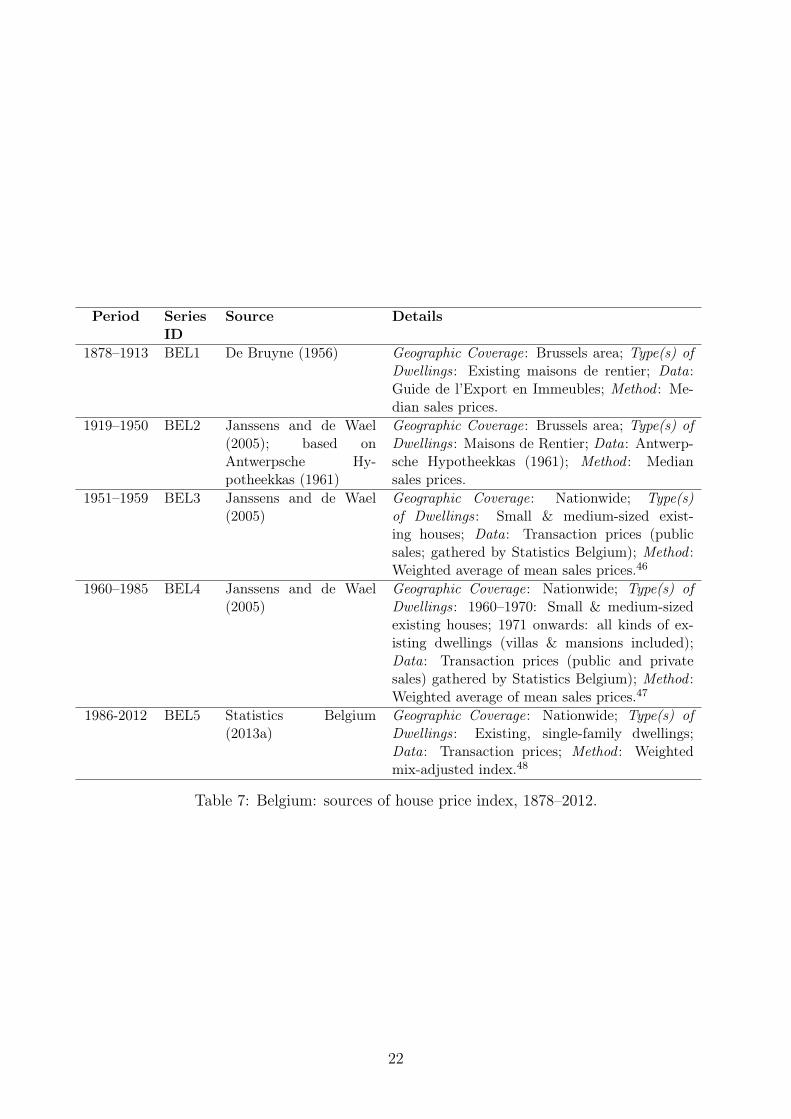

House price data

Historical data on house prices in Belgium is available for 1878ndash2012

The earliest available data on house prices in Belgium is provided by De Bruyne (1956) Itcovers the greater Brussels area for the period 1878ndash1952 and is reported as the annual medianprice per square meter of the interquartile range for four real estate categories i) residentialproperty36 in the center of Brussels ii) maisons de rentier37 iii) building sites (since 1885) and

36rsquoMaisons drsquohabitationrsquo are defined as houses of rather inferior quality Some of them may be rsquomaisons derentierrsquo (see below) that have been downgraded because of the neighborhood or the age of the building Theyare usually inhabited by workers or employees small and do not have electricity central heating gas or water(De Bruyne 1956 62)

37rsquoMaisons de rentierrsquo are defined as properties that are located in a good neighborhood have usually morethan one story are well maintained and serve as a single-family dwelling (De Bruyne 1956 61 f)

18

iv) commercial properties38 (since 1879)39

A second extensive source comprising two house price indices - one for 1919ndash1960 and theother for 1960ndash2003 - is Janssens and de Wael (2005) The first index ie for 1919ndash1960 isbased on two data sources for 1919ndash1950 the index relies on a property price index for Brusselspublished by the Antwerpsche Hypotheekkas (1961) using sales price data for maisons de rentierThe AHK-index is computed as the annual median price of the interquartile range For 1950ndash1960 the index is based on nationwide data for all public housing sales subject to registrationrights gathered by Statistics Belgium For these years the index reflects the development of theweighted mean sales price weights are constructed from the share of total national sales in eachof the 43 Belgian arrondissements (districts) The computational method for the second indexfrom Janssens and de Wael (2005) covering the years 1960ndash2003 is identical to that appliedto the sub-period 1950ndash1960 The sole difference lies in the coverage of the data provided byStatistics Belgium While for the period 1950ndash1960 sales information is limited to public salesthe index for the time 1960ndash2003 is computed using price information for both public andprivate housing sales that were subject to registration rights

In addition to these two principal sources for the years since 1986 Statistics Belgium(2013a) on a quarterly basis publishes price indices for the following four types of real estatei) building lots ii) apartments iii) villas and iv) single-family dwellings The indices areconstructed using stratification and are available for the national regional district (arrondisse-ments) and communal level40

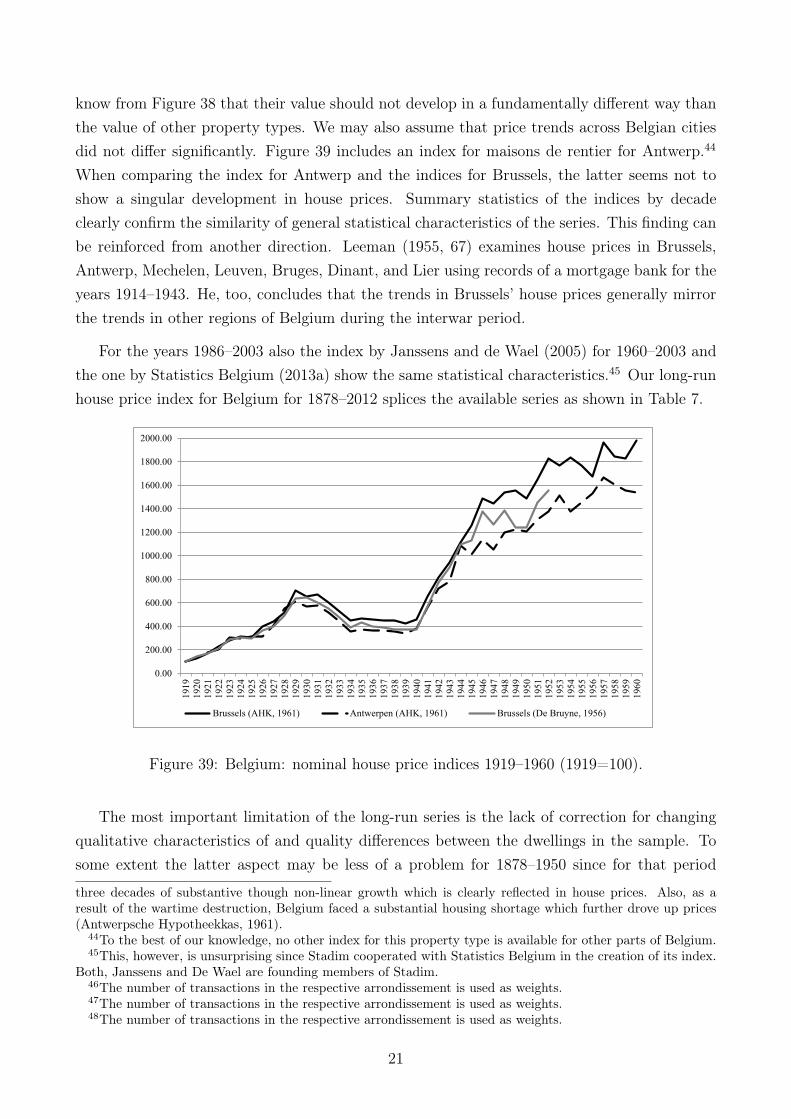

Figure 38 shows the nominal indices for the different property types (maisons drsquohabitationmaisons des rentier commercial buildings and building sites) based on the data from De Bruyne(1956) Three indices (maison drsquo habitation maison de rentier and maison de commerce)move closely together throughout the 1878ndash1913 period only the building sites index shows acomparably higher degree of volatility particularly during the 1880s and 1890s Neverthelessall four indices depict a similar trend nominal house prices trend downwards until the late

38Commercial properties are defined as all buildings for commercial use ie hotels restaurants retail storeswarehouses etc (De Bruyne 1956 63)

39The data is drawn from accounts of public real estate sales published in the Guide de lrsquoExpert en Immeubles(Real Estate Agentsrsquo Catalogue) a periodical of the Union des Geacuteomegravetres-Experts de Bruxelles (Union ofSurveyors of Brussels) The records include the more urban parts of the Brussels district such as Brusselsitself Etterbeek Ixelles Molenbeek Saint-Gilles Saint-Josse Schaerbeek Koekelberg and Laeken De Bruyne(1956) also publishes separate house price series for the more rural areas such as Anderlecht AuderghemForest Ganshoren Jette Uccle Watermael-Boitsfort Berchem-Ste-Agathe Woluwe-St-Lambert Woluwe-St-Pierre Evere Haeren Neder over-Heembeck