RMB Internationalization RMB Internationalization For French Chamber of Commerce and Industry in Hong Kong For French Chamber of Commerce and Industry in Hong Kong December 1 December 1 st st , 2010 , 2010 Eddie Ching Chief Operating Officer, Financial Institutions Group, Asia Pacific

Transcript

RMB InternationalizationRMB InternationalizationFor French Chamber of Commerce and Industry in Hong KongFor French Chamber of Commerce and Industry in Hong Kong

December 1December 1stst, 2010, 2010

Eddie Ching

Chief Operating Officer, Financial Institutions Group, Asia Pacific

1. Offshore RMB - Overview

2. China and RMB

3. RMB Trade Settlement

4. RMB Opportunities

5. Offshore RMB Market

6. Offshore RMB – Other Considerations

7. HSBC RMB Product Capability & Experience

Page 3

Page 4

Page 9

Page 15

Page 19

Page 33

Page 36

Agenda

3

Offshore RMB - Overview

No change to onshore RMB within mainland China

Recent development centers around offshore RMB sinc e July 2009

Objective is to facilitate interaction and transact ion between Chinese enterprises and foreign companies

Primarily focused on import/export trade, extending into FDI and ODI i.e. real economy activities

Since July 2010, foreign companies are allowed to purchase, borrow and transfer offshore RMB freely outside China , creating a more active and liquid FX, MM and investment market

China and RMB

5

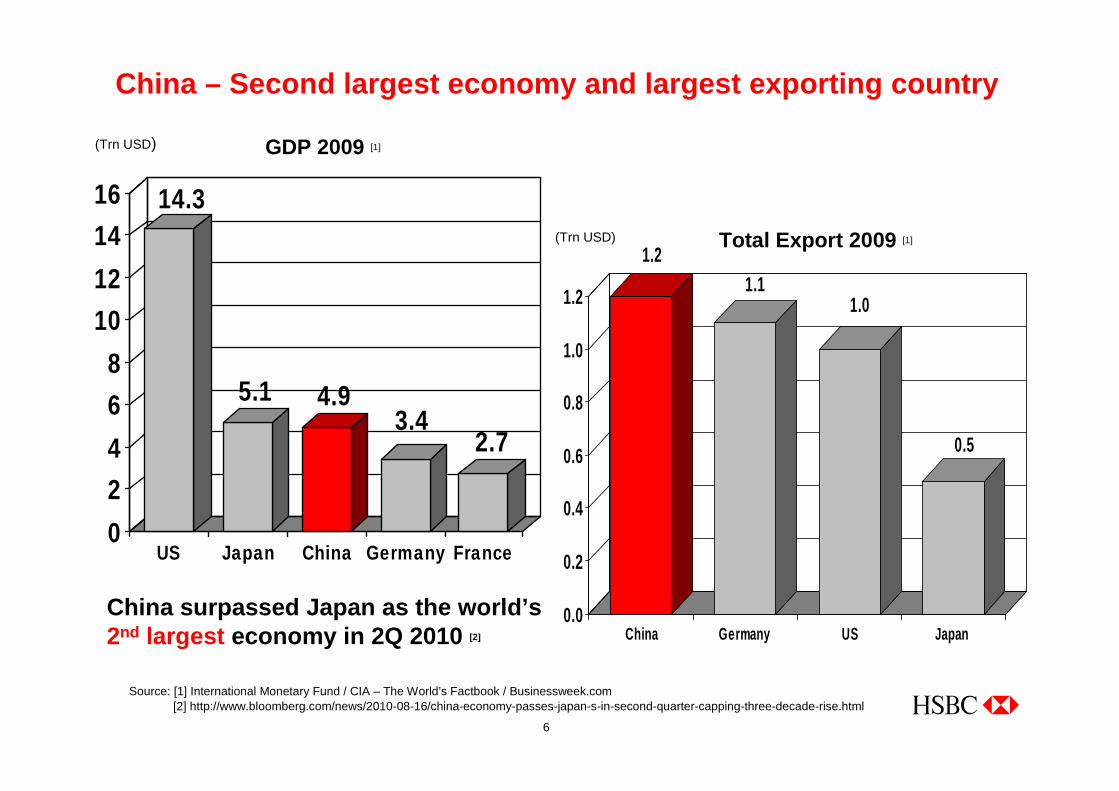

1.3 Billion people [1]

2nd Largest Economy [2]

1st Largest Exporter

USD 1.2 Trillion [1]

Source: [1] China Popin, http://www.cpirc.org.cn/en/eindex.htm[2] http://www.bloomberg.com/news/2010-08-16/china-economy-passes-japan-s-in-second-quarter-capping-three-decade-rise.html

China

6

14.3

5.1 4.93.4

2.7

0

2

4

6

8

10

12

14

16

US Japan China Germany France

Source: [1] International Monetary Fund / CIA – The World’s Factbook / Businessweek.com[2] http://www.bloomberg.com/news/2010-08-16/china-economy-passes-japan-s-in-second-quarter-capping-three-decade-rise.html

1.21.1

1.0

0.5

0.0

0.2

0.4

0.6

0.8

1.0

1.2

China Germany US Japan

(Trn USD)

GDP 2009 [1]

Total Export 2009 [1]

(Trn USD)

China surpassed Japan as the world’s2nd largest economy in 2Q 2010 [2]

China – Second largest economy and largest exporting country

7

Source: CIA – World Factbook 2010

Gross Domestic Product (GDP) of China grows by 11.1% y-o-y in 1H 2010

China – GDP Growth Rate

8

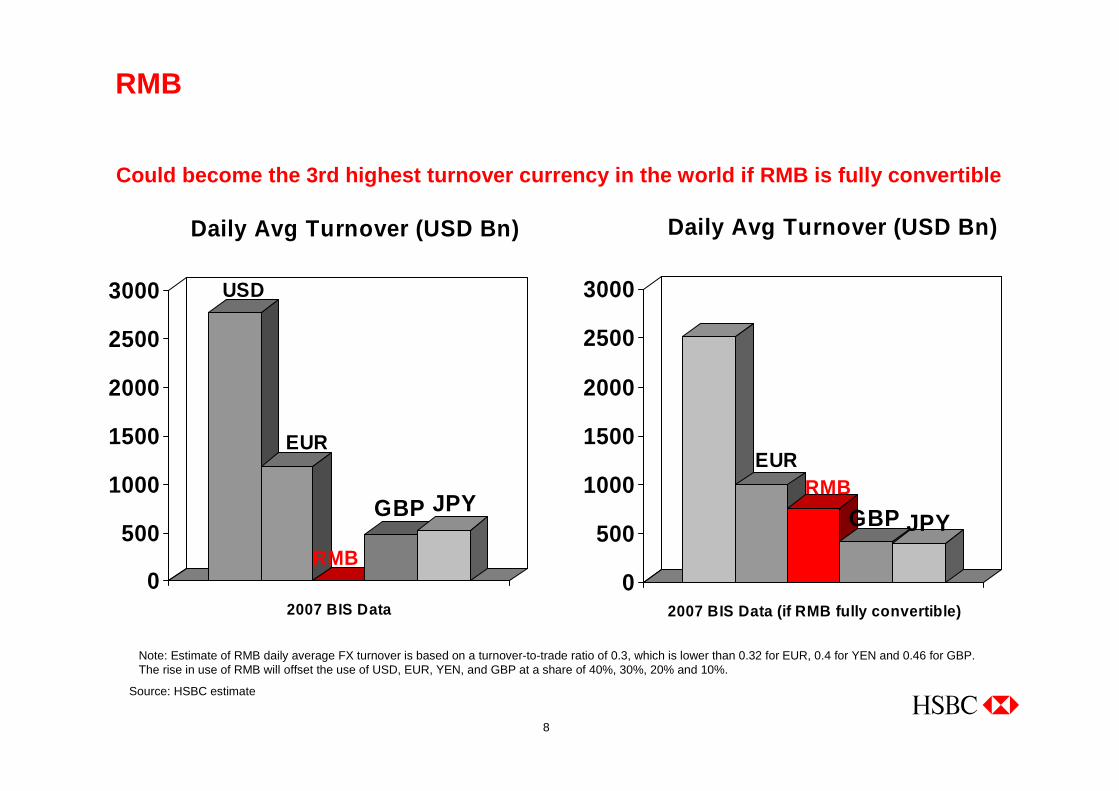

USD

EUR

RMB

GBP JPY

0

500

1000

1500

2000

2500

3000

2007 BIS Data

Daily Avg Turnover (USD Bn)

EURRMB

GBP JPY

0

500

1000

1500

2000

2500

3000

2007 BIS Data (if RMB fully convertible)

Daily Avg Turnover (USD Bn)

Note: Estimate of RMB daily average FX turnover is based on a turnover-to-trade ratio of 0.3, which is lower than 0.32 for EUR, 0.4 for YEN and 0.46 for GBP. The rise in use of RMB will offset the use of USD, EUR, YEN, and GBP at a share of 40%, 30%, 20% and 10%.

Source: HSBC estimate

Could become the 3rd highest turnover currency in t he world if RMB is fully convertible

RMB

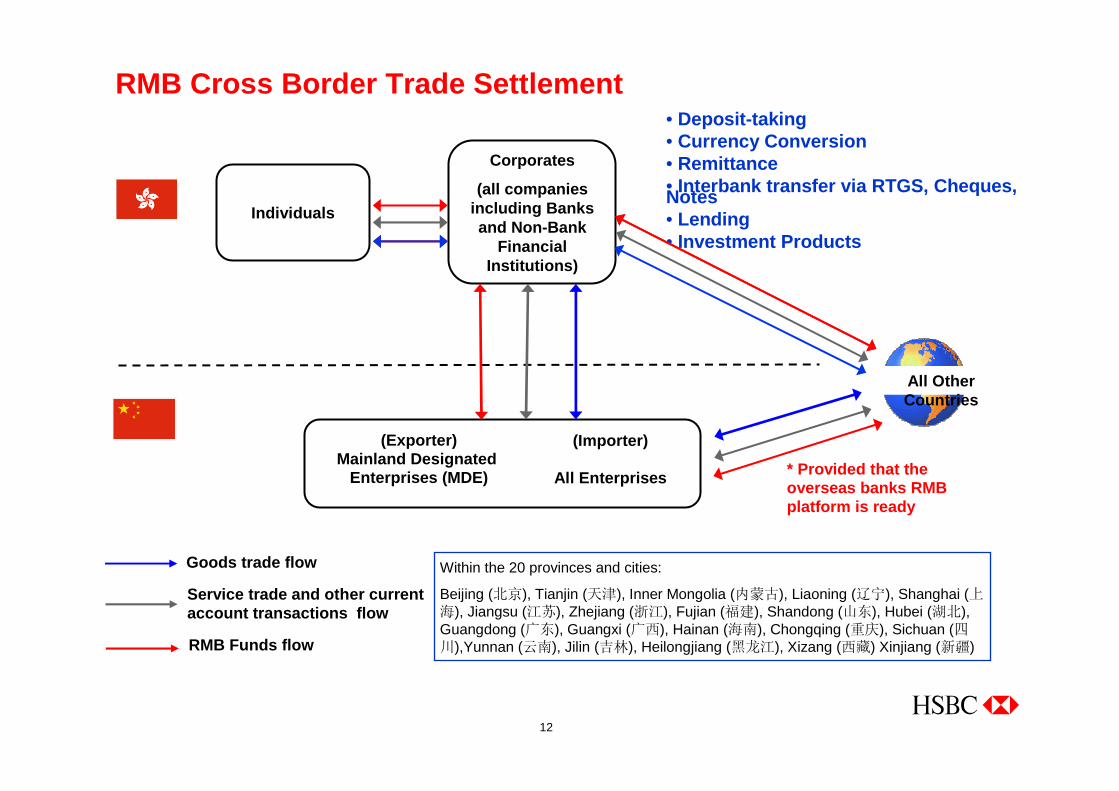

RMB Trade Settlement

10

Total value of Mainland China’s import and export w as US$2,207 billion in 2009

Source: China Customs

1430.7

USD bn 2008

Of which:

US 252.4

Total 1201.7

2009

Hong Kong 190.7

Japan 116.1

Korea 73.9

Germany 59.2

Netherland 45.9

UK 36.1

Singapore 32.3

India 31.6

France 23.3

EXPORT by Mainland China

1,133.1

USD bn 2008

Of which:

Japan 150.7

Total 1,005.6

2009

Korea 112.1

Taiwan 103.3

US

Germany 55.8

Australia 37.4

Malaysia 32.1

Brazil 29.7

Thailand 25.6

Russia 23.8

IMPORT by Mainland China

Canada 21.8 UK 9.6

220.8

166.2

97.9

53.7

49.9

36.7

31.3

30.1

29.7

21.5

17.7

130.9

102.6

85.7

55.8

39.4

32.3

28.3

24.9

21.3

7.9

81.4 77.4

China International Trade

11

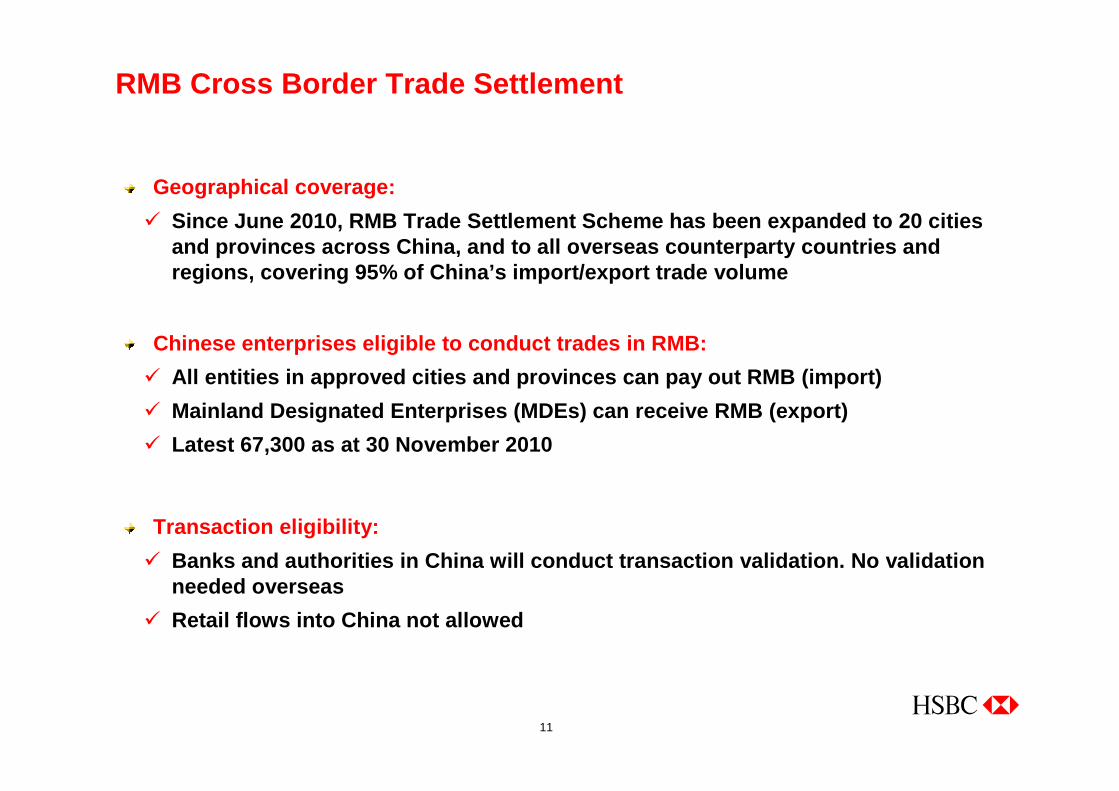

Geographical coverage:

� Since June 2010, RMB Trade Settlement Scheme has be en expanded to 20 cities and provinces across China, and to all overseas cou nterparty countries and regions, covering 95% of China’s import/export trad e volume

Chinese enterprises eligible to conduct trades in R MB:

� All entities in approved cities and provinces can p ay out RMB (import)

� Mainland Designated Enterprises (MDEs) can receive RMB (export)

� Latest 67,300 as at 30 November 2010

Transaction eligibility:

� Banks and authorities in China will conduct transac tion validation. No validation needed overseas

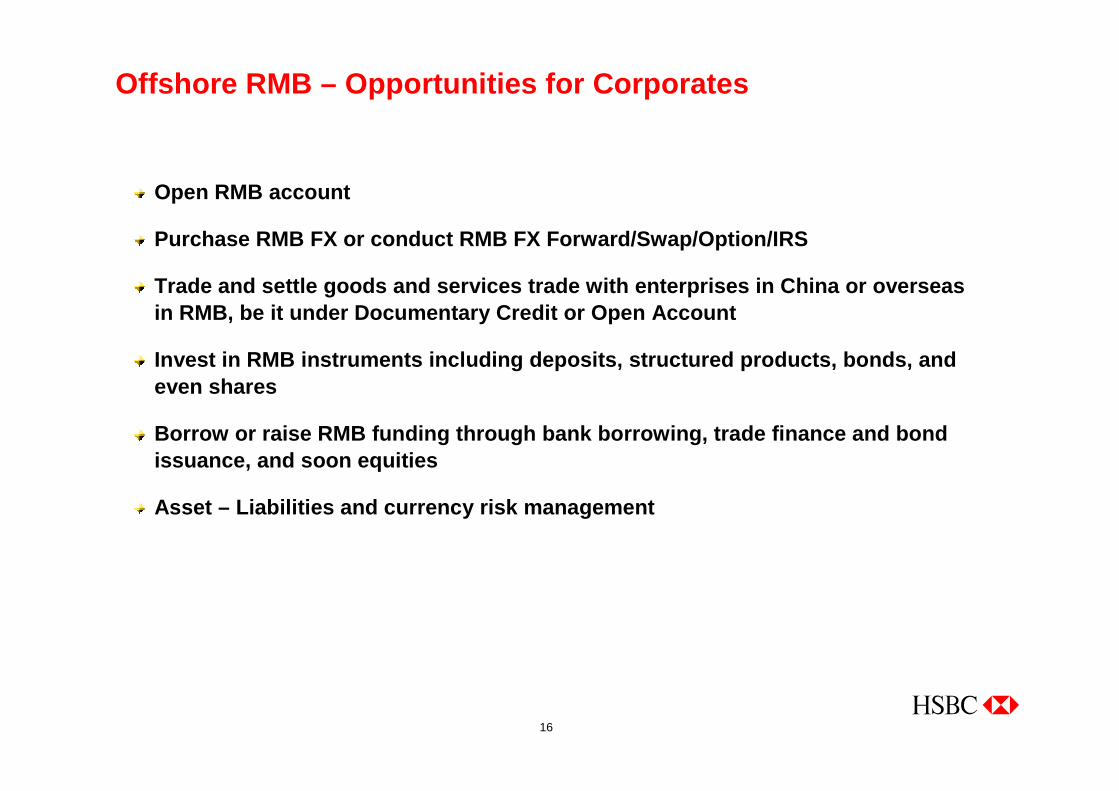

Purchase RMB FX or conduct RMB FX Forward/Swap/Opti on/IRS

Trade and settle goods and services trade with ente rprises in China or overseas in RMB, be it under Documentary Credit or Open Acco unt

Invest in RMB instruments including deposits, struc tured products, bonds, and even shares

Borrow or raise RMB funding through bank borrowing, trade finance and bond issuance, and soon equities

Asset – Liabilities and currency risk management

17

Offshore RMB – Opportunities for Banks and Broker De alers

Account and payment services

Trade and trade financing for corporate

CNH FX sales and trading

CNH bond sales and trading

Balance sheet management via CNY bond investment (i n Hong Kong and/or China)

Debt capital raising – issuance of CNH bond in Hong Kong

CNH bond custodian services

18

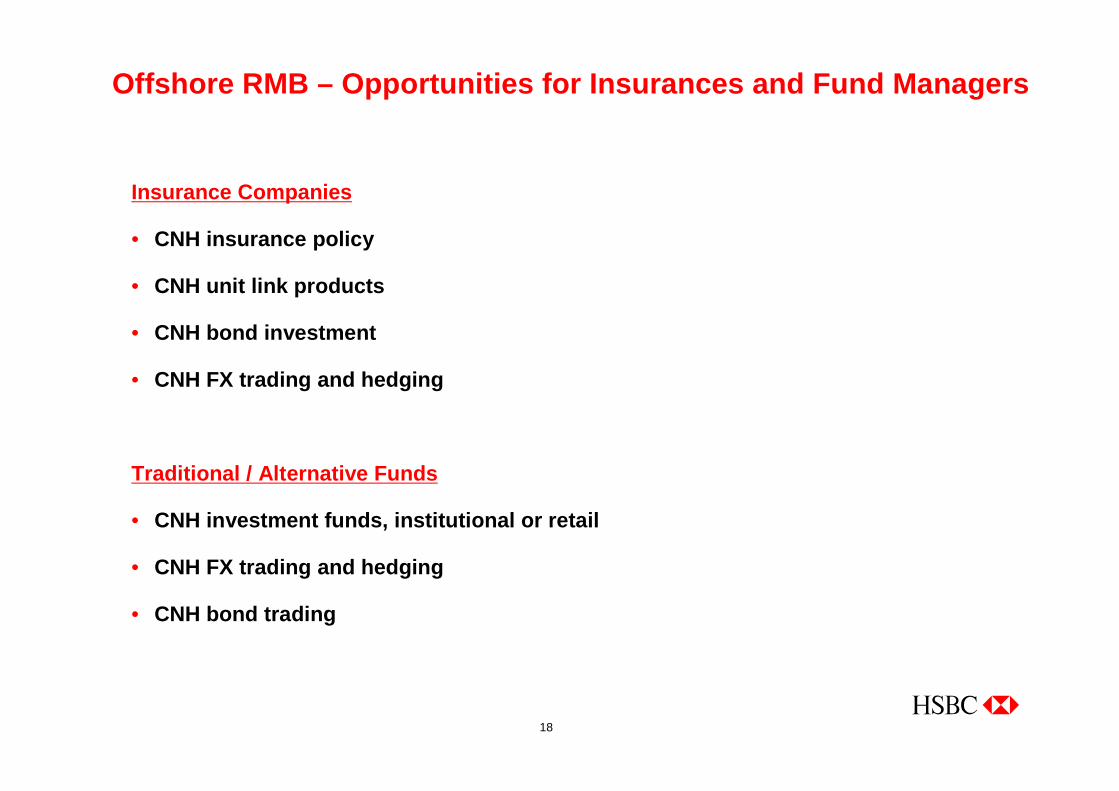

Offshore RMB – Opportunities for Insurances and Fund Managers

Insurance Companies

• CNH insurance policy

• CNH unit link products

• CNH bond investment

• CNH FX trading and hedging

Traditional / Alternative Funds

• CNH investment funds, institutional or retail

• CNH FX trading and hedging

• CNH bond trading

Offshore RMB Market

� CNY – onshore currency used and traded in mainland China

� NDF CNY – offshore non-deliverable forward rate available to corporate and

institution internationally

� CNH Trade – offshore deliverable forward rate provided by the RMB Clearing

Bank in Hong Kong referencing onshore CNY rate for corporate engaged in

cross border China import/export trade settlement

� CNH General – offshore deliverable forward rate openly traded an d available to

corporate and institution internationally

Type of RMB

20

21

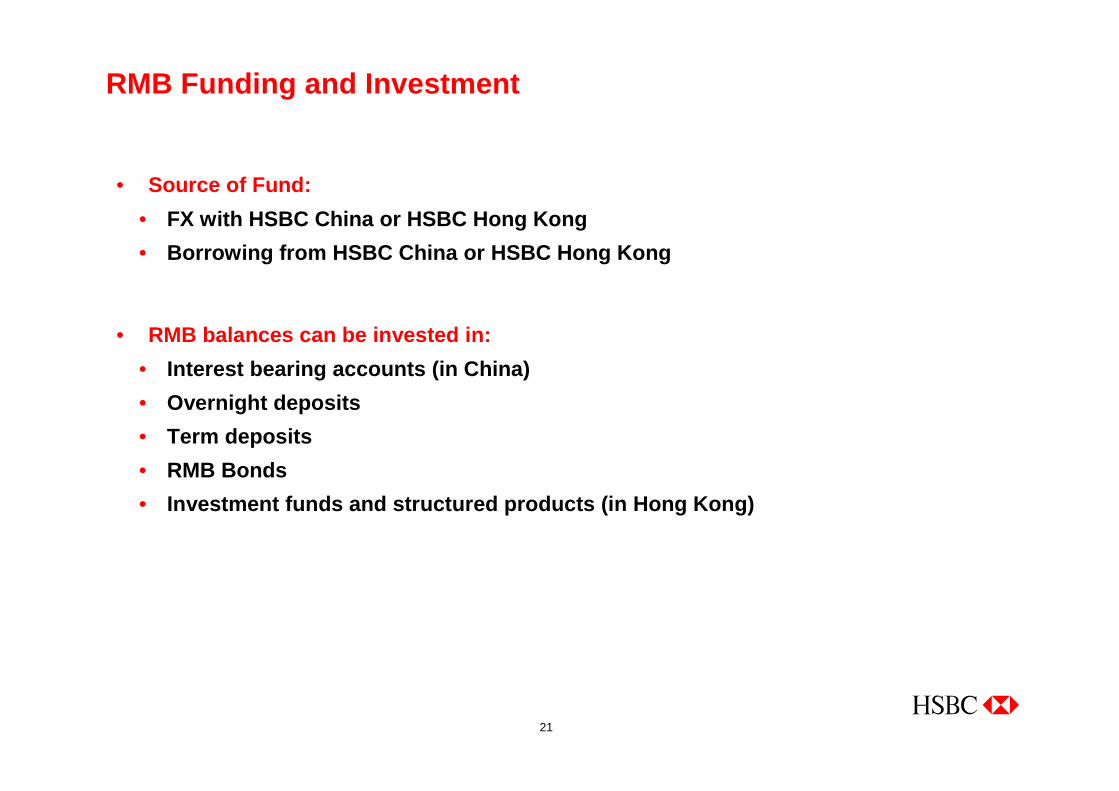

RMB Funding and Investment

• Source of Fund:

• FX with HSBC China or HSBC Hong Kong

• Borrowing from HSBC China or HSBC Hong Kong

• RMB balances can be invested in:

• Interest bearing accounts (in China)

• Overnight deposits

• Term deposits

• RMB Bonds

• Investment funds and structured products (in Hong K ong)

22

RMB Funding Options – HSBC China – For Banks

• FX Trades:

• RMB spot with HSBC China

• Forwards not available to offshore counterparty

• After hours trades possible via email, with SWIFT c onfirmation on next business day

• Subject to the quota assigns to HSBC China by PBOC

• Borrowing:

• Can borrow RMB from HSBC China

• Limited up to 1 month in tenor by regulations

• Subject to the quota assigned to HSBC China by PBOC

• RMB balances can be converted back to other currenc ies

23

RMB Funding Options - HSBC Hong Kong – For All

• FX Trades:

• RMB spot with HSBC Hong Kong

• Forwards, Options and Swap available

• During RMB Spot Market Trading hours deals can be b ooked through Reuters or directly with our HSBC FX Desk

• No regulatory quota but subject to availability in interbank market

• Borrowing:

• Can borrow RMB from HSBC Hong Kong

• No limit in tenor or size but subject to liquidity conditions in market

• RMB balances can be converted back to other currenc ies

24

RMB Money Market in Hong Kong

• Money market rate for RMB obtained from Trade purposes and another for General purposes

• Money market rate for General purpose is around 50- 75bps lower than that of Trade purposes

• A good indication of the rates can be found on HSBC ’s Reuters page “ HSBCRMB”

• Free transfer of RMB funds across different account s

- Any payment, for goods/service, investment products , or even salary can be effected in RMB

- Banks become more active in managing RMB funding. I nterbank wholesale money market liquidity gradually develops to cope w ith funding demands. The offshore RMB interest rate should evolve to become more market-based

Source: HKMA, Bloomberg, HSBC

25

RMB FX in Hong Kong

• Two tier market now exists, Participating Banks in Hong Kong quote 2 types of RMB exchange rate as follow:

- Exchange rate for Trade purposes

- Exchange rate for General purposes

HK Spot market

- Daily volume of USD300–400m, and growing weekly

- Transaction size of USD1–10m

HK Forwards

- Daily volume of USD250m, average ticket size USD2-3 m, Bid-Offer Spread

narrows to 50bps

- Tenor of upto 2 years is actively traded in the mar ket

- Offshore USD/RMB Forward is quoted at premium and o nshore Forward is at

discount

26

RMB Bond Market in Hong Kong - Snapshot

First and only offshore RMB bond market

First issue launched in 2007 by China Development B ank

In 2009, foreign banks’ China incorporated entities can also issue RMB bonds in HK

First Sovereign Bond issued in 2009

First Offshore RMB CD issued by Citic Bank Internat ional in Jul 2010

First Offshore RMB bond issued by Hopewell in Jul 2 010

First Multinational Corporation Offshore RMB bond i ssued by McDonald’s in Aug 2010

47 RMB bonds/CD issued in Hong Kong so far

A total of RMB/CD 75bn has been issued

Outstanding RMB bonds/CD amounts to RMB 57bn

HSBC is engaged with 32 out of 42 RMB Bond/CD issue s in Hong Kong since 2007

27

RMB Bond Market in Hong Kong - Outstanding

The offshore RMB bond market started in 2007

with China Development Bank as the first issuer.

In 2007-2008, the market was dominated by

Chinese banks as they were the only entities

allowed to issue offshore RMB bonds

In 2009, HSBC (China) became the first foreign

bank to issue offshore RMB bonds and the Ministry of Finance completed RMB6bn

debut issuance in Oct 2009

In 2010, the offshore RMB bond market

developed rapidly on the back of PBOC and

HKMA’s supplement regarding expansion of

offshore RMB businesses

Source: Bloomberg, HSBC

HSBC-led deals in red

Pricing Issuer Rating Am ount Coupon Matur ityDate Issuer Moody's S&P (RMB m n) (%) Date

25-Nov-10 The Export - Import Bank of China Aa3 A+ 1,000 1.950 2-Dec-1222-Nov-10 Ministry of Finance of China Aa3 A+ 1,000 2.480 1-Dec-2022-Nov-10 Ministry of Finance of China Aa3 A+ 2,000 1.800 1-Dec-1522-Nov-10 Ministry of Finance of China Aa3 A+ 2,000 1.000 1-Dec-1322-Nov-10 Ministry of Finance of China Aa3 A+ 3,000 TBA 2YR24-Nov-10 Caterpillar Financial A2 A 1,000 2.000 1-Dec-1215-Nov-10 The Export - Import Bank of China Aa3 A+ 4,000 2.650 2-Dec-1315-Nov-10 China Merchants Holding HK - - 700 2.900 19-Nov-139-Nov-10 China Resources Pow er - - 1,000 2.900 12-Nov-139-Nov-10 China Resources Pow er - - 1,000 3.750 12-Nov-1522-Oct-10 Sinotruk - - 2,700 2.950 22-Oct-1218-Oct-10 Asian Development Bank Aaa AAA 1,200 2.850 21-Oct-2015-Oct-10 China Development Bank - - 3,000 2.700 11-Nov-1311-Oct-10 China Development Bank - - 2,000 3mSHIBOR+10bps 14-Oct-138-Oct-10 ICBC (Asia) - - 117 2.300 22-Oct-128-Oct-10 ICBC (Asia) - - 47 2.650 22-Dec-13

17-Sep-10 Deutsche Bank - - 200 2.000 28-Sep-1216-Sep-10 Bank of Tokyo-Mitsubishi - - 20 1.980 26-Sep-1116-Sep-10 ICBC (Asia) - - 1,000 2.250 24-Sep-1216-Sep-10 ICBC (Asia) - - 1,000 2.250 24-Sep-127-Sep-10 Bank of China - A- 2,200 2.650 30-Sep-127-Sep-10 Bank of China - A- 2,800 2.900 30-Sep-132-Sep-10 China Development Bank - - 500 2.100 13-Sep-122-Sep-10 China Development Bank - - 1,000 2.100 13-Sep-121-Sep-10 China Development Bank - - 100 1.950 12-Sep-11

7-Jul-10 Hopew ell Highw ay Inf rastructure - - 1,380 2.980 13-Jul-126-Jul-10 Citic Bank International - - 500 2.680 20-Jul-11

28-Sep-09 Ministry of Finance of China A1 A+ 3,000 2.250 27-Oct-1128-Sep-09 Ministry of Finance of China A1 A+ 2,500 2.700 27-Oct-1228-Sep-09 Ministry of Finance of China A1 A+ 500 3.300 27-Oct-147-Sep-09 HSBC Bank (China) A1 / Prime-1 - 2,000 2.600 14-Sep-11

14-Aug-09 China Development Bank A1 A+ 2,000 2.450 20-Aug-1110-Aug-09 China Development Bank A1 A+ 1,000 3mSHIBOR+30bps 20-Aug-1129-Jun-09 Bank of East Asia (China) - A- 4,000 2.800 23-Jul-1125-Jun-09 HSBC Bank (China) A1 / Prime-1 - 1,000 3mSHIBOR+38bps 13-Jul-11

28

RMB Bond Market in Hong Kong - Growing

In the year 2010 YTD, we saw 29 new RMB

Bond/CD issuance in offshore RMB Market,

which is more than the total number of

issuances from 2007-2009.

Moreover, more than half of the volume is

contributed by offshore issuer so far.

Recently, Export and Import Bank of China

announced the decision to issue no larger than

5bn RMB bond in Hong Kong. We are expecting there is still more room

to grow for the Offshore RMB Market in 2010.

In sum, the Offshore RMB market is growing

rapidly.

Source: Bloomberg, HSBC

Offshore RMB Bonds/CD Issuance

0

5

10

15

20

25

2007 2008 2009 2010 YTD0

5

10

15

20

25

30

Issue Amt by Offshore EntityIssue Amt by Onshore Entity# of Issues

RMB (Bn) # Of Issues

29

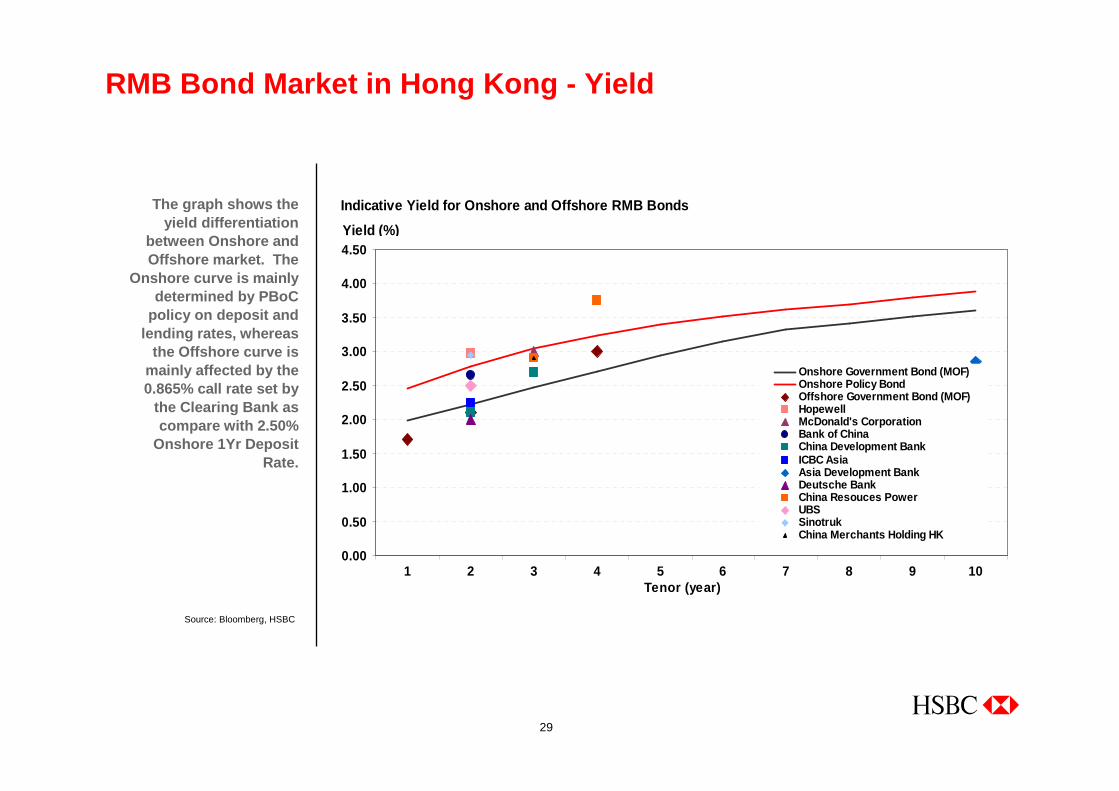

RMB Bond Market in Hong Kong - Yield

The graph shows the yield differentiation

between Onshore and Offshore market. The

Onshore curve is mainly determined by PBoC

policy on deposit and lending rates, whereas

the Offshore curve is mainly affected by the 0.865% call rate set by

the Clearing Bank as compare with 2.50%

Onshore 1Yr Deposit Rate.

Source: Bloomberg, HSBC

Indicative Yield for Onshore and Offshore RMB Bonds

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

1 2 3 4 5 6 7 8 9 10Tenor (year)

Onshore Government Bond (MOF) Onshore Policy Bond Offshore Government Bond (MOF) HopewellMcDonald's CorporationBank of ChinaChina Development BankICBC AsiaAsia Development BankDeutsche BankChina Resouces PowerUBSSinotrukChina Merchants Holding HK

Yield (%)

30

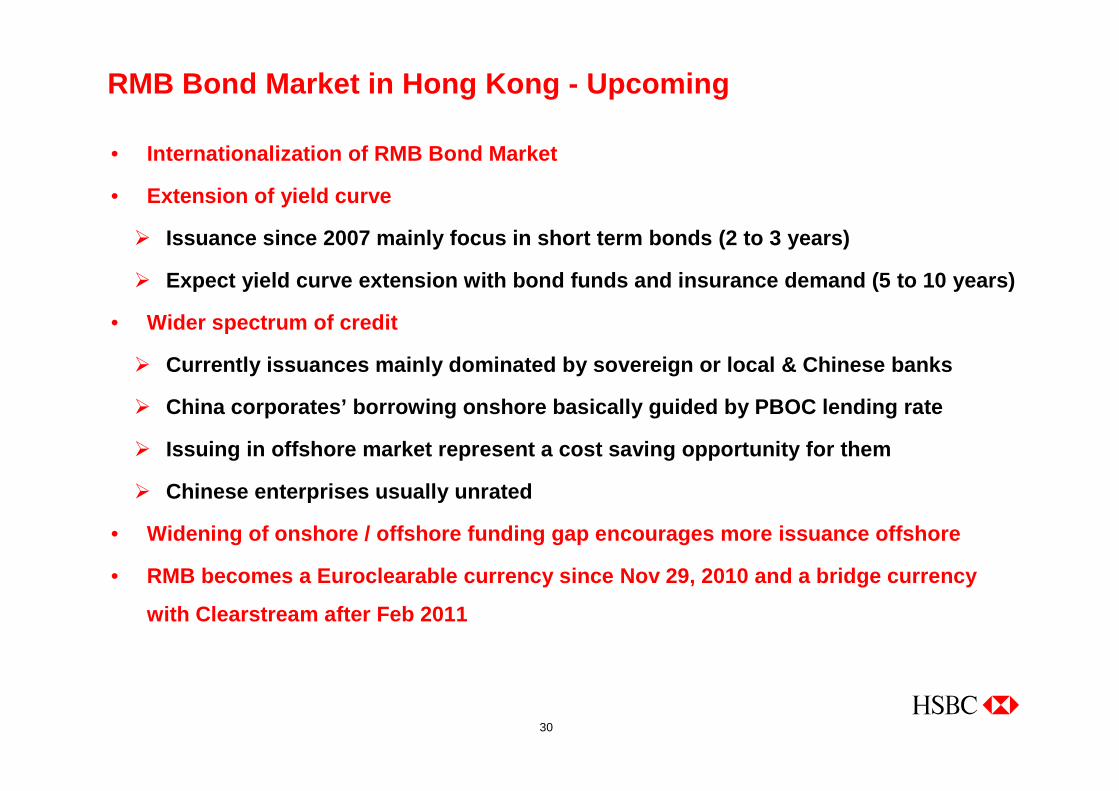

RMB Bond Market in Hong Kong - Upcoming

• Internationalization of RMB Bond Market

• Extension of yield curve

� Issuance since 2007 mainly focus in short term bond s (2 to 3 years)

� Expect yield curve extension with bond funds and in surance demand (5 to 10 years)

• Wider spectrum of credit

� Currently issuances mainly dominated by sovereign o r local & Chinese banks

� China corporates’ borrowing onshore basically guided by PBOC lending rate

� Issuing in offshore market represent a cost saving opportunity for them

� Chinese enterprises usually unrated

• Widening of onshore / offshore funding gap encourag es more issuance offshore

• RMB becomes a Euroclearable currency since Nov 29, 2010 and a bridge currency

with Clearstream after Feb 2011

31

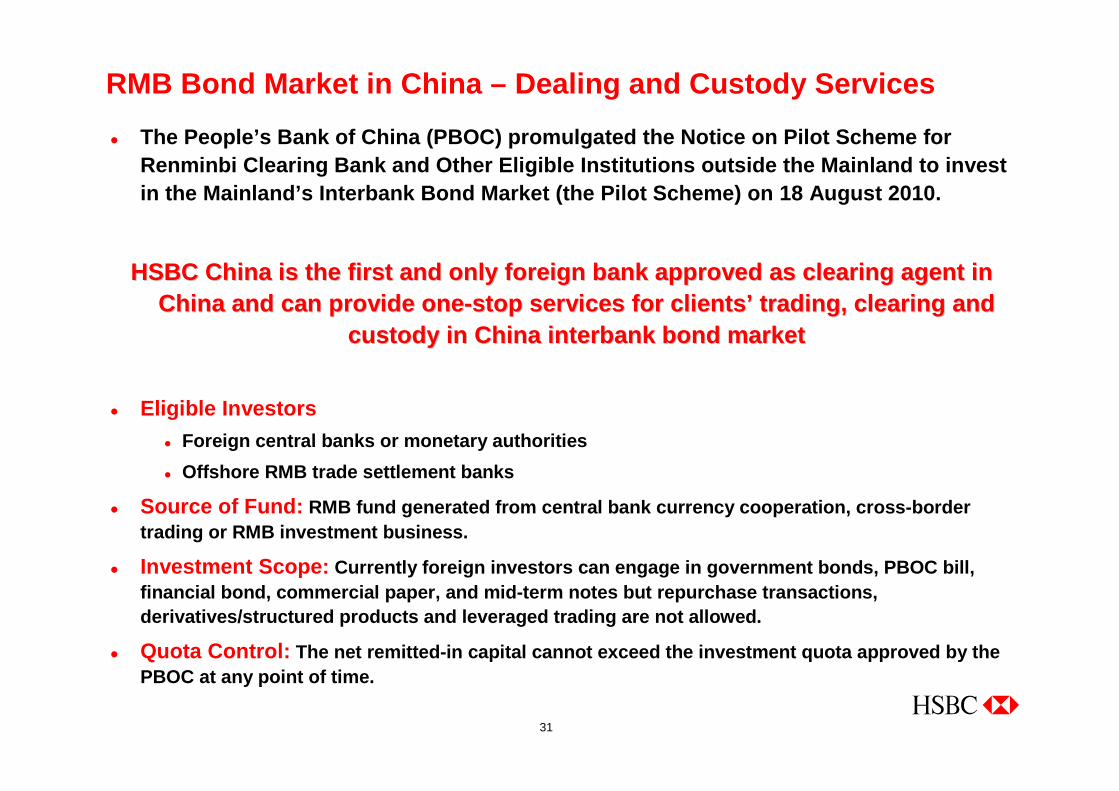

� The People’s Bank of China (PBOC) promulgated the N otice on Pilot Scheme for Renminbi Clearing Bank and Other Eligible Instituti ons outside the Mainland to invest in the Mainland’s Interbank Bond Market (the Pilot Scheme) on 18 August 2010.

HSBC China is the first and only foreign bank appro ved as cleariHSBC China is the first and only foreign bank appro ved as cleari ng agent in ng agent in China and can provide oneChina and can provide one --stop services for clientsstop services for clients ’’ trading, clearing and trading, clearing and

custody in China interbank bond marketcustody in China interbank bond market

� Eligible Investors

� Foreign central banks or monetary authorities

� Offshore RMB trade settlement banks

� Source of Fund: RMB fund generated from central bank currency coope ration, cross-border trading or RMB investment business.

� Investment Scope: Currently foreign investors can engage in governmen t bonds, PBOC bill, financial bond, commercial paper, and mid-term note s but repurchase transactions, derivatives/structured products and leveraged tradi ng are not allowed.

� Quota Control: The net remitted-in capital cannot exceed the inves tment quota approved by the PBOC at any point of time.

RMB Bond Market in China – Dealing and Custody Servi ces

32

RMB Bond Market in China - Application Process

1. Apply for investment quota approval from PBOC

2. Open a bond account with China Government Securities Depository Trust & Clearing Co. Ltd (CDC) and file with PBOC Shanghai

3. Apply to PBOC Shanghai for opening a special RMB cash settlement account

4. Open a securities account and a special RMB cash settlement account with HSBC

5. Apply for trading with interbank trading centre (CFETS)

PBOCPBOC

Starts Trading

HSBCHSBCPBOC SHHPBOC SHH

CDCCDC

CFETSCFETS

PBOC SHHPBOC SHH

Offshore RMB – Other Considerations

34

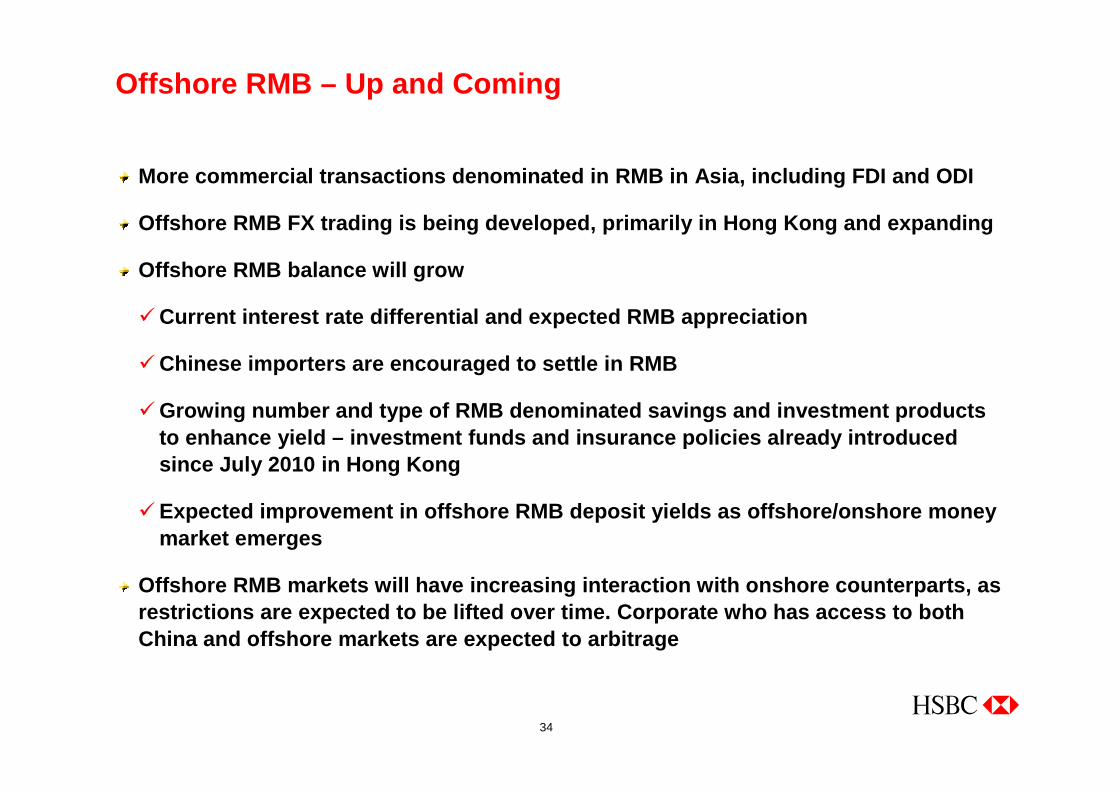

Offshore RMB – Up and Coming

More commercial transactions denominated in RMB in Asia, including FDI and ODI

Offshore RMB FX trading is being developed, primari ly in Hong Kong and expanding

Offshore RMB balance will grow

�Current interest rate differential and expected RMB appreciation

�Chinese importers are encouraged to settle in RMB

�Growing number and type of RMB denominated savings and investment products to enhance yield – investment funds and insurance po licies already introduced since July 2010 in Hong Kong

�Expected improvement in offshore RMB deposit yields as offshore/onshore money market emerges

Offshore RMB markets will have increasing interacti on with onshore counterparts, as restrictions are expected to be lifted over time. C orporate who has access to both China and offshore markets are expected to arbitrag e

35

Offshore RMB – What is missing

Movement of RMB crossing China border must be suppo rted by an underlying commercial transactions, between two companies

RMB capital account movement, e.g. capital injectio n or shareholder’s loan into China, requires one more PBOC approval on top of us ual regulatory approval

Specifically for Hong Kong Only

No RMB lending to individuals

Personal RMB conversion remains at CNY20,000 per da y

HSBC RMB Capability & Experience

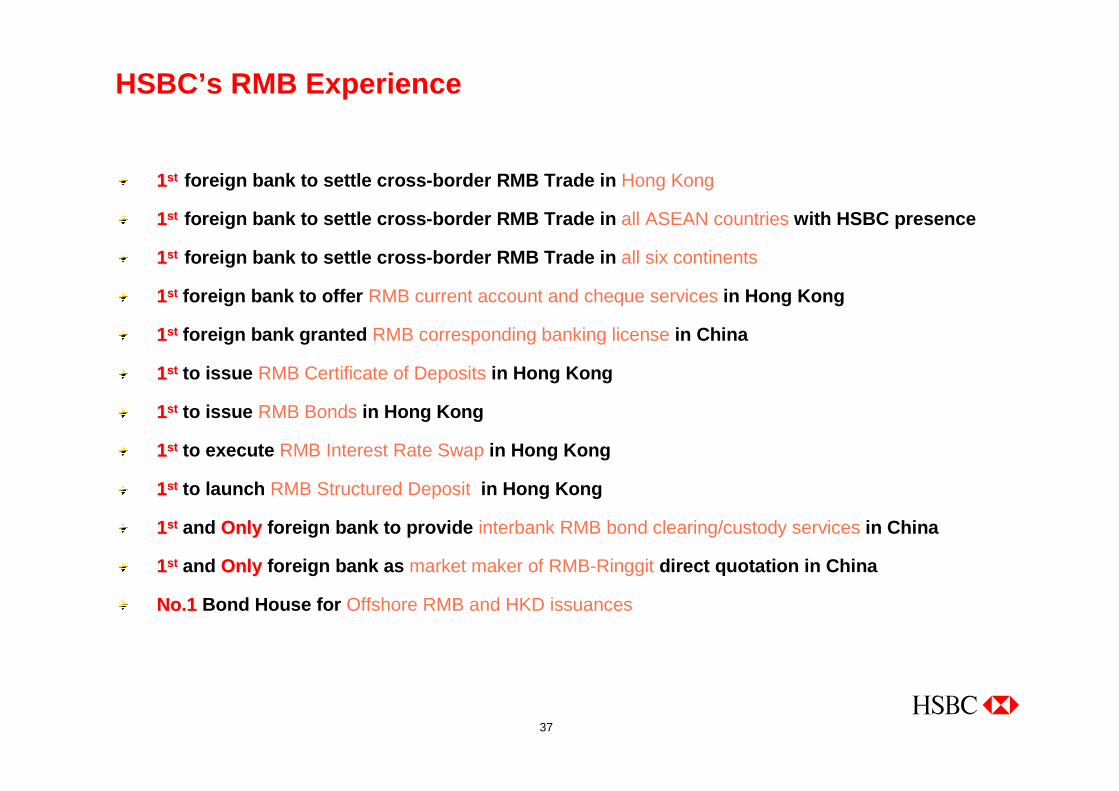

37

11stst foreign bank to settle cross-border RMB Trade in Hong Kong

11stst foreign bank to settle cross-border RMB Trade in all ASEAN countries with HSBC presence

11stst foreign bank to settle cross-border RMB Trade in all six continents

11stst foreign bank to offer RMB current account and cheque services in Hong Kong

11stst foreign bank granted RMB corresponding banking license in China

11stst to issue RMB Certificate of Deposits in Hong Kong

11stst to issue RMB Bonds in Hong Kong

11stst to execute RMB Interest Rate Swap in Hong Kong

11stst to launch RMB Structured Deposit in Hong Kong

11stst and OnlyOnly foreign bank to provide interbank RMB bond clearing/custody services in China

11stst and OnlyOnly foreign bank as market maker of RMB-Ringgit direct quotation in China

No.1No.1 Bond House for Offshore RMB and HKD issuances

• No Restriction on Account Opening • No Restriction on Account Opening

Custody • RMB Custody and Funds Administration Services • RMB Custody and Clearing

Exchange Services and Risk Management Products

• Spot FX (for trade / general purposes)

• Deliverable FX Forward

• Deliverable FX Option

• Deliverable FX Swap

• Deliverable Interest Rate Swap

• Non Deliverable Forward

• Spot FX

Borrowing / Financing Products

• Trade financing facilities and commercial loans

• Issuance of offshore RMB bonds/CDs

• Money Market

• Trade financing facilities and commercial loans

• Money Market

Investment Products

• Time deposit, certificate of deposit

• Primary and secondary RMB bonds trading

• FX linked structured deposit

• Interest rate linked structured deposit

• Equity linked structured deposit

• Gold linked structured deposit

• RMB investment funds

• Time deposit

• Call deposit

• Interbank bond trading (for banks only)

HSBC – your bank of choice in international RMB busi ness

HSBC - First International Bank to settle cross border trade in RMB July 2009

Structured and traded FX neutral collateralised USD loan in HK

April 2010

Structured and traded FX linked RMB Structured Deposit in HK

July 2010

Structured and traded equity linked RMB structured deposit in HK

July 2010

Structured and traded Libor linked RMB structured deposit in HK

Aug 2010

One of the pioneer banks to sell large size general purpose RMB FX to corporate customerJuly 2010

First bank to execute RMB Interest Rate Swap

Oct 2010

HSBC’s RMB Capability

39

Disclaimer

This document is issued by The Hongkong and Shanghai Banking Corporation Limited (HSBC). The information contained herein is derived from sources we believe to be reliable, but

which we have not independently verified. HSBC makes no representation or warranty (express or implied) of any nature nor is any responsibility of any kind accepted with respect to the

completeness or accuracy of any information, projection, representation or warranty (expressed or implied) in, or omission from, this document. No liability is accepted whatsoever for

any direct, indirect or consequential loss arising from the use of or reliance on this document or any information contained herein by the recipient or any third party.

Any examples given are for the purposes of illustration only. The opinions in this document constitute our present judgement, which is subject to change without notice. This document

does not constitute an offer or solicitation for, or advice that you should enter into, the purchase or sale of any security, commodity or other investment product or investment agreement,

or any other contract, agreement or structure whatsoever and is intended for institutional, professional or sophisticated customers and is not intended for the use of private individual or

retail customers. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. Recipients should not rely on this

document in making any investment decision and should make their own independent appraisal of and investigations into the information and any investment, product or transaction

described in this document. Unless governing law permits otherwise, you must contact a HSBC Group member in your home jurisdiction if you wish to use HSBC Group services in

effecting a transaction in any investment mentioned in this document. This document, which is confidential and not for public circulation, must not be copied, transferred or the content

disclosed, in whole or in part, to any third party. The document should be read in its entirety.

Copyright. The Hongkong and Shanghai Banking Corporation Limited 2010. ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or

transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the Hongkong and Shanghai Banking

Corporation Limited.

References to HSBC Research are to opinions held by HSBC Global Research in previously published research reports and do not represent an endorsement by HSBC Global

Research or any product or strategy referred to herein. HSBC Global Research is not under any duty to update any such opinions.

All the information set out in this presentation is provided on the best of the Bank's current knowledge and understanding of the relevant law, rules, regulations, directions and guidelines

governing or otherwise applicable to RMB trade services but the Bank makes no guarantee, representation or warranty and accepts no liability as to its accuracy or completeness.

Please refer to any updates that shall be published or issued by our Bank from time to time including notices that we place at our HSBC branches.