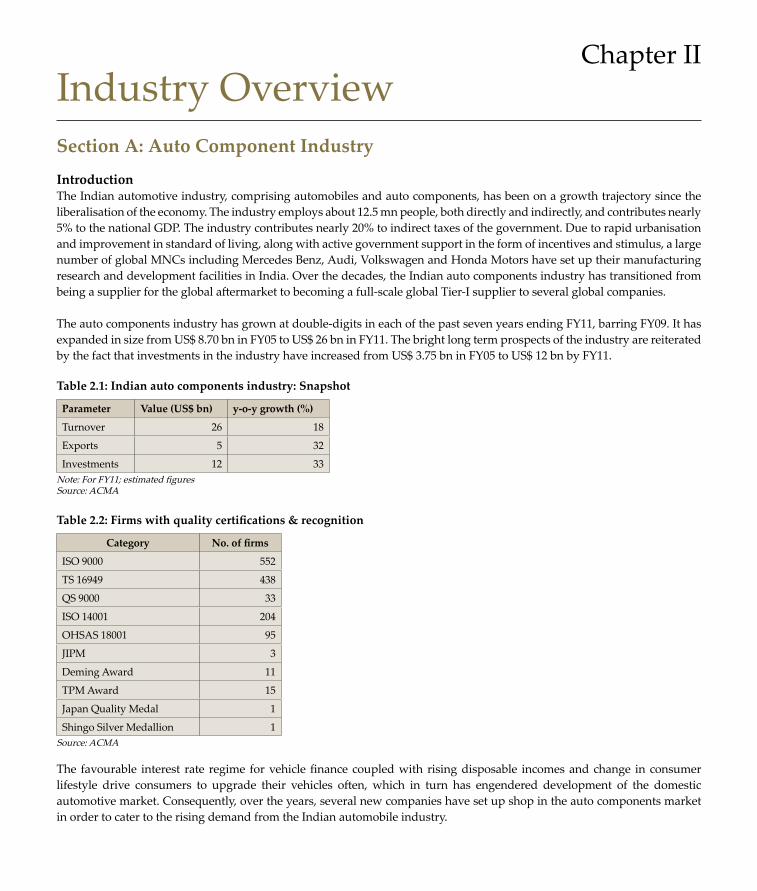

Industry Overview Section A: Auto Component Industry Introduction The Indian automotive industry, comprising automobiles and auto components, has been on a growth trajectory since the liberalisation of the economy. The industry employs about 12.5 mn people, both directly and indirectly, and contributes nearly 5% to the national GDP. The industry contributes nearly 20% to indirect taxes of the government. Due to rapid urbanisation and improvement in standard of living, along with active government support in the form of incentives and stimulus, a large number of global MNCs including Mercedes Benz, Audi, Volkswagen and Honda Motors have set up their manufacturing research and development facilities in India. Over the decades, the Indian auto components industry has transitioned from being a supplier for the global aſtermarket to becoming a full-scale global Tier-I supplier to several global companies. The auto components industry has grown at double-digits in each of the past seven years ending FY11, barring FY09. It has expanded in size from US$ 8.70 bn in FY05 to US$ 26 bn in FY11. The bright long term prospects of the industry are reiterated by the fact that investments in the industry have increased from US$ 3.75 bn in FY05 to US$ 12 bn by FY11. Table 2.1: Indian auto components industry: Snapshot Parameter Value (uS$ bn) y-o-y growth (%) Turnover 26 18 Exports 5 32 Investments 12 33 Note: For FY11; estimated figures Source: ACMA Table 2.2: Firms with quality certifications & recognition Category No. of firms ISO 9000 552 TS 16949 438 QS 9000 33 ISO 14001 204 OHSAS 18001 95 JIPM 3 Deming Award 11 TPM Award 15 Japan Quality Medal 1 Shingo Silver Medallion 1 Source: ACMA The favourable interest rate regime for vehicle finance coupled with rising disposable incomes and change in consumer lifestyle drive consumers to upgrade their vehicles oſten, which in turn has engendered development of the domestic automotive market. Consequently, over the years, several new companies have set up shop in the auto components market in order to cater to the rising demand from the Indian automobile industry. Chapter II

Transcript

7

Industry OverviewSection A: Auto Component Industry

IntroductionThe Indian automotive industry, comprising automobiles and auto components, has been on a growth trajectory since the liberalisation of the economy. The industry employs about 12.5 mn people, both directly and indirectly, and contributes nearly 5% to the national GDP. The industry contributes nearly 20% to indirect taxes of the government. Due to rapid urbanisation and improvement in standard of living, along with active government support in the form of incentives and stimulus, a large number of global MNCs including Mercedes Benz, Audi, Volkswagen and Honda Motors have set up their manufacturing research and development facilities in India. Over the decades, the Indian auto components industry has transitioned from being a supplier for the global aftermarket to becoming a full-scale global Tier-I supplier to several global companies.

The auto components industry has grown at double-digits in each of the past seven years ending FY11, barring FY09. It has expanded in size from US$ 8.70 bn in FY05 to US$ 26 bn in FY11. The bright long term prospects of the industry are reiterated by the fact that investments in the industry have increased from US$ 3.75 bn in FY05 to US$ 12 bn by FY11.

Table 2.1: Indian auto components industry: Snapshot

Parameter Value (uS$ bn) y-o-y growth (%)

Turnover 26 18

Exports 5 32

Investments 12 33Note: For FY11; estimated figuresSource: ACMA

Table 2.2: Firms with quality certifications & recognition

Category No. of firms

ISO 9000 552

TS 16949 438

QS 9000 33

ISO 14001 204

OHSAS 18001 95

JIPM 3

Deming Award 11

TPM Award 15

Japan Quality Medal 1

Shingo Silver Medallion 1Source: ACMA

The favourable interest rate regime for vehicle finance coupled with rising disposable incomes and change in consumer lifestyle drive consumers to upgrade their vehicles often, which in turn has engendered development of the domestic automotive market. Consequently, over the years, several new companies have set up shop in the auto components market in order to cater to the rising demand from the Indian automobile industry.

Chapter II

8

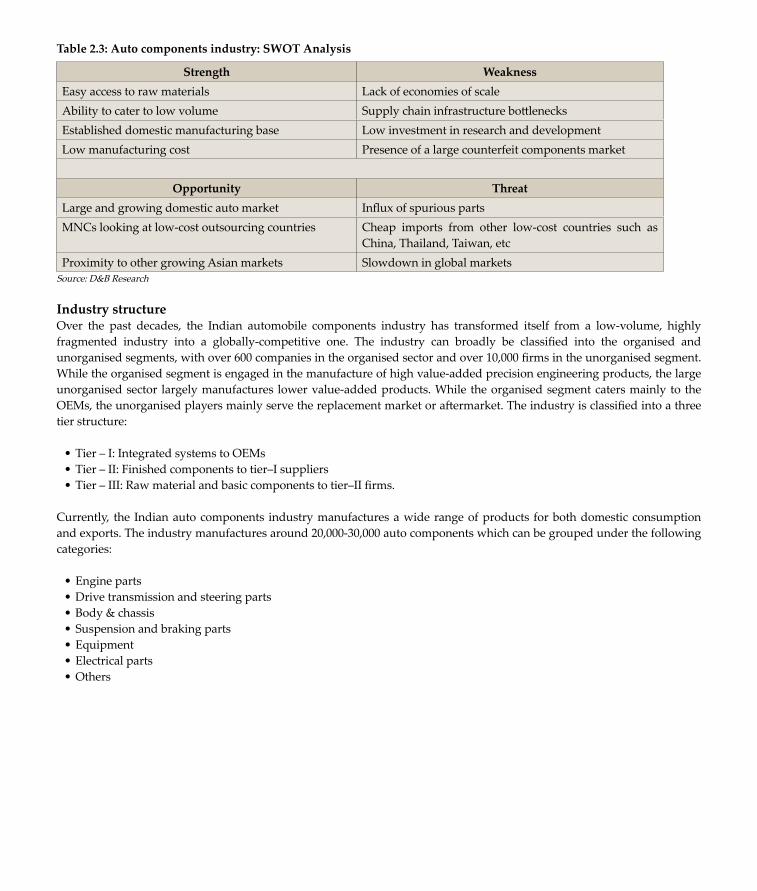

Table 2.3: Auto components industry: SwOT Analysis

Strength WeaknessEasy access to raw materials Lack of economies of scaleAbility to cater to low volume Supply chain infrastructure bottlenecksEstablished domestic manufacturing base Low investment in research and development Low manufacturing cost Presence of a large counterfeit components market

Opportunity ThreatLarge and growing domestic auto market Influx of spurious partsMNCs looking at low-cost outsourcing countries Cheap imports from other low-cost countries such as

China, Thailand, Taiwan, etcProximity to other growing Asian markets Slowdown in global markets

Source: D&B Research

Industry structureOver the past decades, the Indian automobile components industry has transformed itself from a low-volume, highly fragmented industry into a globally-competitive one. The industry can broadly be classified into the organised and unorganised segments, with over 600 companies in the organised sector and over 10,000 firms in the unorganised segment. While the organised segment is engaged in the manufacture of high value-added precision engineering products, the large unorganised sector largely manufactures lower value-added products. While the organised segment caters mainly to the OEMs, the unorganised players mainly serve the replacement market or aftermarket. The industry is classified into a three tier structure:

• Tier – I: Integrated systems to OEMs • Tier – II: Finished components to tier–I suppliers • Tier – III: Raw material and basic components to tier–II firms.

Currently, the Indian auto components industry manufactures a wide range of products for both domestic consumption and exports. The industry manufactures around 20,000-30,000 auto components which can be grouped under the following categories:

• Engine parts • Drive transmission and steering parts • Body & chassis• Suspension and braking parts • Equipment • Electrical parts • Others

9

The chart below depicts the composition of products manufactured by the industry.

Chart 2.1: Auto components industry: product composition (%)

Source: ACMA

Auto components manufacturers mostly form clusters around a few major OEMs in different parts of the country. Pune, Chennai, National Capital Region and Pithampur (Rajasthan) are emerging as major auto component clusters in India.

Table 2.4: Auto components: Regional clusters

Cluster Cities

Western cluster Pune, Aurangabad, Nashik (Maharashtra)

Southern cluster Chennai & Coimbatore (Tamil Nadu); Bengaluru (Karnataka)

Central cluster Pithampur, Dewas, Indore (Madhya Pradesh)

Eastern cluster Jamshedpur & Guptamani near Kharagpur; Singur (West Bengal)Source: D&B Research

Table 2.5: Auto component clusters in India

State number

Andhra Pradesh 1

Delhi 1

Gujarat 5

Haryana 3

Jharkhand 1

Karnataka 2

Maharashtra 5

Madhya Pradesh 1

Punjab 4

Tamil Nadu 1Source: D&B Research

Demand dynamicsThe domestic auto components industry’s market size is estimated to be US$ 26 bn in FY11. The industry’s turnover grew at a CAGR of 20.0% during FY05-FY11 due to robust growth in the domestic automobile sector and surge in exports.

10

Chart 2.2: Trend in industry turnover

*EstimatedSource: ACMA

The global economic slowdown had adversely affected the demand for auto components in FY09. Major automotive companies cancelled or postponed their orders due to lack of sales owing to the economic uncertainty. As a result, the industry’s growth slowed down to a meagre 2% during FY09, after posting double-digit growth in the preceding four years. Nevertheless, the industry started witnessing signs of recovery during FY10 due to some stability returning in the global economy. Moreover, the government’s stimulus packages announced in the wake of the recession also began to yield results with increase in domestic consumption levels. Consequently, the Indian auto components industry ended FY10 with sales growth of 20%. The growth momentum was maintained in FY11 as well, with industry turnover growing at a respectable 18%.

Demand for auto components is directly related to that for automobiles; hence, demand drivers for automobiles indirectly influence those for auto components. Factors that influence OEM demand for auto components differ from those that influence replacement demand for components. The key demand drivers are listed below:

Demand drivers for OEMs:• Economic growth • Infrastructure development • Easy availability of finance and sales promotion offers • Inadequate public transport • Freight rates.

Demand drivers for the replacement market:Automobiles

• Rising penetration of personal vehicles • Vehicle life • Usage of automobiles.

Auto components• Growing market for used vehicles • Overloading of vehicles • Deteriorating road infrastructure • Up-gradation of emission standards.

Exports scenarioExports constitute about 15% of the Indian auto components industry’s total turnover. Exports of auto components from India grew from US$ 1.69 bn in FY05 to US$ 5 bn by FY11, registering a healthy CAGR of 19.8%. Export figures remained stagnant in FY10 and stood at US$ 3.8 bn. Exports once again bounced back in FY11, registering sharp growth of 32%. During

11

FY11, global OEMs/tier-I manufacturers accounted for 80% share in the Indian auto component industry’s exports, while the global aftermarket accounted for the rest. Europe accounted for nearly 37% of India’s exports and continues to be one of the major export destinations followed by Asia.

Chart 2.3: Auto components: Composition of export destinations (%)

Source: ACMA

Supply dynamics Raw materials constitute a major cost component in the auto components industry, accounting for around 60% of total expenses, followed by labour charges at close to 10%.

Indian auto components manufacturers have been focusing on R&D activities — innovation, design, and engineering activities — to meet global quality standards and emerge as full-service providers to OEMs.

Notwithstanding the slowdown in the global economy in the recent years, the Indian auto components industry continues to attract investments and the industry continues to add new capacities.

Investments in the industry increased from US$ 3.10 bn in FY04 to US$ 9 bn in FY10, growing at a CAGR of 19.4%. Investments are estimated to have increased to US$ 12.0 bn in FY11. Major foreign companies have been investing in the domestic industry through joint ventures/partnerships or by setting up their own production plants. Domestic components players are also investing heavily in the industry to reap benefits of the bright long term growth prospects.

Chart 2.4: Auto components industry: Investments snapshot

*EstimatedSource: ACMA

12

Challenges faced by the industryThe auto components industry is in a robust growth phase. However, the industry faces certain critical challenges that could hamper its growth going forward. Some of the major challenges faced by the industry are listed below:

• Technological capability not enough to match global standards • Surging raw material prices putting pressure on profit margins• Slowdown in the global economy affecting exports• Players are losing bargaining power against buyers as industry size is larger than OEMs • Increasing rivalry among players with numerous small similar firms targeting same customer segments • Players have low bargaining power with raw material suppliers, especially steel suppliers due to increasing demand for steel • FTAs signed with other developing countries may increase bulk imports of relatively cheaper auto components.

The way ForwardGoing forward, the Indian auto components industry is well poised to achieve strong growth owing to rising domestic demand in the OEM market and expanding replacement market. The export market for auto components is likely to see strong traction once the global market stabilises and the economic uncertainty fades away. According to the ACMA, the domestic auto components industry is likely to grow to US$ 110 bn by 2020, with the domestic market at around US$ 80 bn. The share of the auto components industry in the country’s GDP is likely to increase to 3.6% by 2020, up from 2.1% in FY10. Given the bright long term demand prospects in the domestic market and with India emerging as a favoured low-cost sourcing destination, auto component manufacturers are likely to invest in increasing production capacities and technological capabilities. Further, companies would continue de-risking their business by entering other industries. However, market competition is expected to intensify. Further, prices of raw material would maintain an upward trend. This is expected to exert pressure on the industry’s profit margins. In such a scenario, cost control programmes would assume greater significance for the industry players, both big and small.

Section B: Electronic Goods industryThe Indian electronic goods industry forms a small part of the global electronics industry. However, in the recent years, the domestic market has witnessed a robust growth driven by several factors such as manufacturing growth, ICT penetration, rising disposable income, retail boom and attractive finance schemes. Production grew at an impressive CAGR of 18.3% during FY06-FY10. In FY11, production is estimated to have increased by around 10.0% (y-o-y) at ` 1,217.6 bn. However there exists a huge gap in demand and supply in this sector. Domestic production constitutes less than 45% of domestic consumption (FY09). As most of the raw material required for manufacturing electronic goods is not available domestically, manufacturers need to import materials from countries such as China, Taiwan and Korea.

Chart 2.5: Trend in production of electronic goods

*EstimatesSource: Department of Information Technology

13

Industry StructureThe Indian electronics industry is broadly divided into consumer electronics, industrial electronics, computer hardware, strategic electronics, communication and broadcasting and electronic components. As per FY11 estimates, consumer electronics and the communication & broadcast equipment segments have the largest share comprising of 28% and 27% of the total production, respectively. While the consumer electronic segment has always held the dominant share, the share of the communication & broadcast equipment segment has increased during the recent years.

Chart 2.6: Indian electronic goods industry

Note: For FY11; estimatedSource: Department of Information Technology

Consumer electronicsThe consumer electronics segment includes products that can be directly used by the end-users; for instance, television sets, DVD/MP3 players and microwave ovens. India has a large manufacturing base for this segment and it is a highly competitive market. Currently, the Indian consumer electronics market is dominated by the MNCs. Growing middle class, demand for premium and luxury products in the urban markets due to changing consumer lifestyle and low- end affordable products are driving the demand for this segment.

Production of consumer electronics is estimated to have increased by 15.2% at ` 334.0 bn in FY11, as against production of ` 290.0 bn in FY10. According to the Department of Information Technology, within this segment, colour TVs has the largest revenue share. The domestic market for colour TVs is estimated to have been around 16.1 mn units in FY11, a growth of 5.5% over FY10. The market for colour TV is being driven by the robust sales of LCD TVs. The market for LCD TV has increased from 1.5 mn units in FY10 to 2.8 mn units in FY11 primarily owing to declining prices and low penetration levels.

Going forward, higher disposable income and availability of finance, increase in digitisation, affordable products in most categories, establishment of retail chains and growing organised retail will continue to be the growth drivers for consumer electronic goods.

Industrial electronicsIndustrial electronics comprises of critical hardware technologies and systems with built-in software. The important devices used in this segment relate to power electronics, medical electronics and other intermediates like semiconductor. It is one of the challenging areas which require high level of technical skill in designing systems for applications in a variety of industrial sectors. India has expertise in conceptualising such systems and erecting and commissioning them. However, this sector largely depends on import of critical hardware and associated software. Large projects are implemented with C&I packages, which are imported from abroad, without any knowledge of design. Thus, this, in most cases, leads to higher initial cost and maintenance cost in the long run.

The Department of Electronics is trying to support this segment, especially the SME sector, through its Industrial Application Programme, by providing proven indigenous technologies wherever possible. A large collaborative programme on Intelligent

14

Transportation System, which includes various technology modules for application in the road transportation sector, was launched during FY10. In FY11, production in this segment was an estimated ` 181.9 bn, as against ` 151.60 bn in FY10, a growth of 20.0%.

Computer hardwareIndia is one of the fastest growing hardware markets in the Asia-Pacific region. Most of the prominent global vendors have strong presence in the Indian market. The BFSI (Banking, Financial Services and Insurance), telecom, ITeS (Information Technology enabled Services), manufacturing verticals, Small & Medium Enterprises (SMEs), e-Governance and households are the key demand verticals for this segment. Domestic production in the computer hardware segment for FY11 is estimated to have remained almost unchanged at ` 149.70 bn as compared to FY10. According to the Department of Electronics, this could be attributed to decelerating growth in exports, substitution of domestic production by cheaper imports and rising input cost. However, within this segment, domestic sales of PCs are estimated to have recorded a growth of 12% in FY11 to touch 9.7 mn units, with notebook sales estimated to have grown by 40% and desktop sales by 12.7%. Going forward, expanding e-governance and social programs, rise in PC sales owing to increased access and broadband penetration, awareness and affordability of technology and increasing notebook sales are expected to drive the growth of this segment. With significant IT adoption plans on the anvil by the government as well as the corporate sector, the IT systems and hardware market is expected to expand rapidly in the coming years.

Strategic electronicsThe strategic electronics segment includes satellite-based communications, navigation and surveillance, underwater electronic system, infra-red based detection and ranging system, disaster management, internal security system and GPS-based vehicle tracking system etc. The estimated production figure for this segment for FY11 is ` 76.80 bn, a growth of about 10% as compared to FY10.

Strategic electronics goods are often used by the defence and paramilitary forces. Owing to the need to maintain national and energy security and growth in the domestic economy, India’s defence, aerospace and nuclear sectors are expected to grow substantially. According to the report of the Task Force for the IT, ITES and Electronics Hardware Manufacturing Industry, India is expected to be one of the top five markets for defense equipment by 2015, driven by geo-political considerations. Moreover, focus by commercial aircraft manufacturers on low-cost countries are expected to generate growth in the aerospace market in emerging markets in general and India in particular. The civilian nuclear agreement between the US and India will enable commerce and cooperation, in particular allowing India to collaborate with global companies on nuclear projects, thereby driving the growth of this segment.

Communication and broadcasting equipmentCommunication technology is increasingly being recognised as a key driver for economic development. Digital exchanges, transmission equipment, microwave transreceivers, satellite communication terminals, optical fibre communication equipment, and two-way radio communication equipment come under the purview of this segment. India has also emerged as the fastest growing telecom services markets in the world which has boosted the telecom electronics and equipment manufacturing segment. Moreover, India is considered to be one of the fastest growing markets for global telecom electronics and equipment and vendors such as Alcatel-Lucent, Ericsson, Motorola and Nokia have established their operations in India. In the coming years, growing need for telecommunication market as evidenced in the increasing subscriber base, growth in rural mobile telephony and increasing broadband penetration and connectivity will drive the growth of this segment.

Box 2.1: Key highlightsTotal subscriber base at the end of Mar-11 has reached 846.32 millionWireless subscription base at the end of Mar-11 stands at 811.59 millionWireline subscription base stands at 34.73 million at the end of Mar-11New additions in the wireless segment for the quarter ending Mar-11 is 59.40 million Total tele-density has touched 70.89% as at the end of Mar-11Broadband subscription base is 11.89 million as at the end of Mar-11

During FY11, the communication and broadcasting equipment segment is estimated to have grown by 5% on a y-o-y basis to ` 325.50 mn.

15

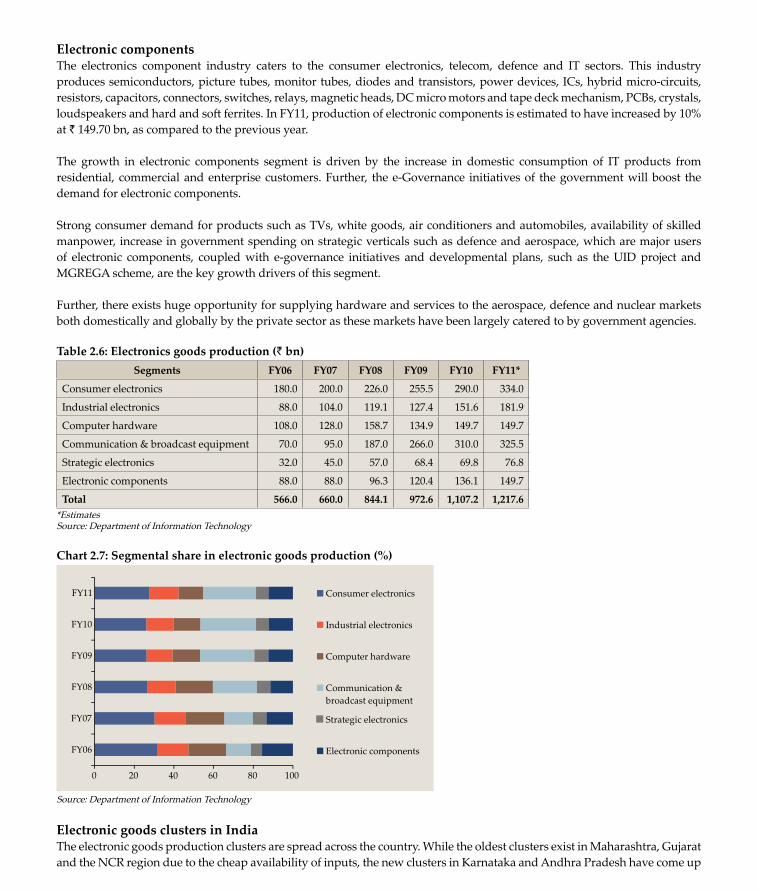

Electronic componentsThe electronics component industry caters to the consumer electronics, telecom, defence and IT sectors. This industry produces semiconductors, picture tubes, monitor tubes, diodes and transistors, power devices, ICs, hybrid micro-circuits, resistors, capacitors, connectors, switches, relays, magnetic heads, DC micro motors and tape deck mechanism, PCBs, crystals, loudspeakers and hard and soft ferrites. In FY11, production of electronic components is estimated to have increased by 10% at ` 149.70 bn, as compared to the previous year.

The growth in electronic components segment is driven by the increase in domestic consumption of IT products from residential, commercial and enterprise customers. Further, the e-Governance initiatives of the government will boost the demand for electronic components.

Strong consumer demand for products such as TVs, white goods, air conditioners and automobiles, availability of skilled manpower, increase in government spending on strategic verticals such as defence and aerospace, which are major users of electronic components, coupled with e-governance initiatives and developmental plans, such as the UID project and MGREGA scheme, are the key growth drivers of this segment.

Further, there exists huge opportunity for supplying hardware and services to the aerospace, defence and nuclear markets both domestically and globally by the private sector as these markets have been largely catered to by government agencies.

Total 566.0 660.0 844.1 972.6 1,107.2 1,217.6*EstimatesSource: Department of Information Technology

Chart 2.7: Segmental share in electronic goods production (%)

Source: Department of Information Technology

Electronic goods clusters in IndiaThe electronic goods production clusters are spread across the country. While the oldest clusters exist in Maharashtra, Gujarat and the NCR region due to the cheap availability of inputs, the new clusters in Karnataka and Andhra Pradesh have come up

16

to meet the demand for electronics from the IT/ ITeS industry in these regions. India has created a world class manufacturing ecosystem in Sriperumbudur, Chennai. The key production clusters are as follows:

Table 2.7: Key production clusters

Ahmedabad, GujaratBengaluru, KarnatakaGurgaon, HaryanaHyderabad, Andhra PradeshMumbai, MaharashtraAbdasa, GujaratAgartala, TripuraNoida, Uttar PradeshPune, MaharashtraChennai, Tamil Nadu

Source: UNIDO

Strong growth in exportsA significant portion of domestic production of electronic goods is consumed in the Indian market while only a small part of it is exported. Exports from the electronic goods industry in India constitutes around 21% (average share during FY06-FY11) of the production. Exports of electronic goods used to be meager, but has picked up during the past few years. The surge in exports of communication and broadcasting equipment had contributed to the recent growth in exports. The Asian (excluding Middle East) and the European markets are the largest export destinations for the electronic goods industry while the share of America, which used to hold a significant share of exports (around 29% during FY06), has come down over the years. Africa and Middle East have garnered an increasing share in exports since the past two to three years.

Major growth drivers of the Indian electronic goods sector• Growth in per capita income and corporate spend on electronics• Government’s focus on infrastructure • Transformation of electronics goods from an aspiration to a utilitarian need • Quick rate of obsolescence in technology• Availability of affordable products for lower income groups as well

Key challenges in the electronic goods sector • Inadequate infrastructure viz power, transportation and land• Limited preferential market access for local companies resulting in excessive import of low-cost products• Limited R&D focus• Unfavourable tax structure• Inflexible labour laws• Limited focus on value addition and exports

Government initiativesThe Government has identified electronics hardware as a thrust area and has been taking a number of steps regularly to promote this industry. It introduced a Special Incentive Package Scheme (SIPS), in 2007, to attract investments for setting up semiconductor fabrication and other micro and nanotechnology manufacturing industries in India. Under SIPS, the Department of Electronics had received twenty six applications (as of Mar 10) seeking financial assistance.

Various initiatives towards promotion of technology innovation and commercialisation of electronics and IT have been undertaken. In 2008, the Department of Electronics had launched a scheme for Technology Incubation and Development of Entrepreneurs (TIDE) in the area of Electronics & ICT to provide financial support for nurturing the techno-entrepreneurs as well as for strengthening the technology incubation activity. Currently 17 institutions are being supported under the TIDE scheme.

OutlookThis industry has significant potential to develop and manufacture electronics hardware for the global market and increase its global share. According to the Report of the Task Force for IT, ITES and Electronics Hardware Manufacturing Industry, electronics hardware production for domestic consumption is estimated to increase from US$ 16 bn in 2009 to US$ 85 bn in 2014 and further to US$ 320 bn in 2020.

Electronics hardware exports are estimated to increase from US$ 4.4 bn in 2009 to US$ 15 bn by 2014 and US$ 80 bn by 2020. However, in order to achieve this export growth it has been recommended by the Government that India needs to focus more on designing and manufacturing global products, then reach out to the rural areas in the domestic market and then the emerging export markets. Moreover, given the growing demand for electronics in the country and the fact that most of it is currently being met through imports, there is a huge economic opportunity in developing the Electronics System and Design Manufacturing (ESDM) industry in India.

There is also greater need for India to focus on research & development, giving more thrust to the semiconductor industry, cluster development, effective supply chain and logistics system and focus on inventing mass-products that matter to rural and bottom of the pyramid segments. Going forward, the demand for appliances and energy efficient consumer electronics is going to be high and the domestic producers should leverage the opportunity to enhance growth.

![[MS-IPHTTPS]: IP over HTTPS (IP-HTTPS) Tunneling Protocol€¦ · IP over HTTPS (IP-HTTPS) Tunneling Protocol Intellectual Property Rights Notice for Open Specifications Documentation](https://static.documents.pub/doc/80x56/5f5d18b22a82be0e3640e86d/ms-iphttps-ip-over-https-ip-https-tunneling-protocol-ip-over-https-ip-https.jpg)