IAS 7 IAS-7 STATEMENT OF CASH FLOWS FEDERAL RESERVE NOTE THE UNITED STATES OF AMERICA THE UNITED STATES OF AMERICA THIS NOTE IS LEGAL TENDER A L70744629F 12 12 12 12 L70744629F ONE DOLLAR ONE DOLLAR WASHINGTON, D.C. FOR ALL DEBTS, PUBLIC AND PRIVATE SERIES 1985 H 293 ONE DOLLAR ONE DOLLAR h hi i ( i By Santosh Ghimire (CA, DipIFR)

Transcript

IAS 7IAS-7 STATEMENT OF CASH FLOWS

FEDERAL RESERVE NOTE

THE UNITED STATES OF AMERICATHE UNITED STATES OF AMERICA

THIS NOTE IS LEGAL TENDER

A

L70744629F

12

1212

12

L70744629F

ONE DOLLARONE DOLLAR

WASHINGTON, D.C.

FOR ALL DEBTS, PUBLIC AND PRIVATE

SERIES1985

H 293

ONE DOLLARONE DOLLAR

h hi i ( iBy Santosh Ghimire (CA, DipIFR)

Presentation OutlinePresentation Outline

• Introduction and Scope• Introduction and Scope

• Definitions of Key Terms

• Cash and cash equivalents

• Presentation and Format of Cash Flow

• Direct Vs Indirect Method

• Disclosures Requirements

Introduction and Scope

Applicability • An entity shall prepare a cash flow statement in accordance with the requirements ofAn entity shall prepare a cash flow statement in accordance with the requirements of

this Standard and shall present it as an integral part of its financial statements for each period for which financial statements are presented.

• Applies to all entities regardless of their size ownership Structure Industry etcApplies to all entities regardless of their size, ownership, Structure, Industry etc.

Importance and Scope

• Entities need cash for (i) Operation of business (ii) Pay obligation; and (iii)Provide• Entities need cash for (i) Operation of business (ii) Pay obligation; and (iii)Provide returns to investors.

• Preparation of cash flow is important ; (i) To show that profits are being realized (ii) To pay dividends; and (iii) To finance further investmentpay dividends; and (iii) To finance further investment

• Profits is not the same as cash …….and profitability does not mean liquidity. Even profitable company “crash”

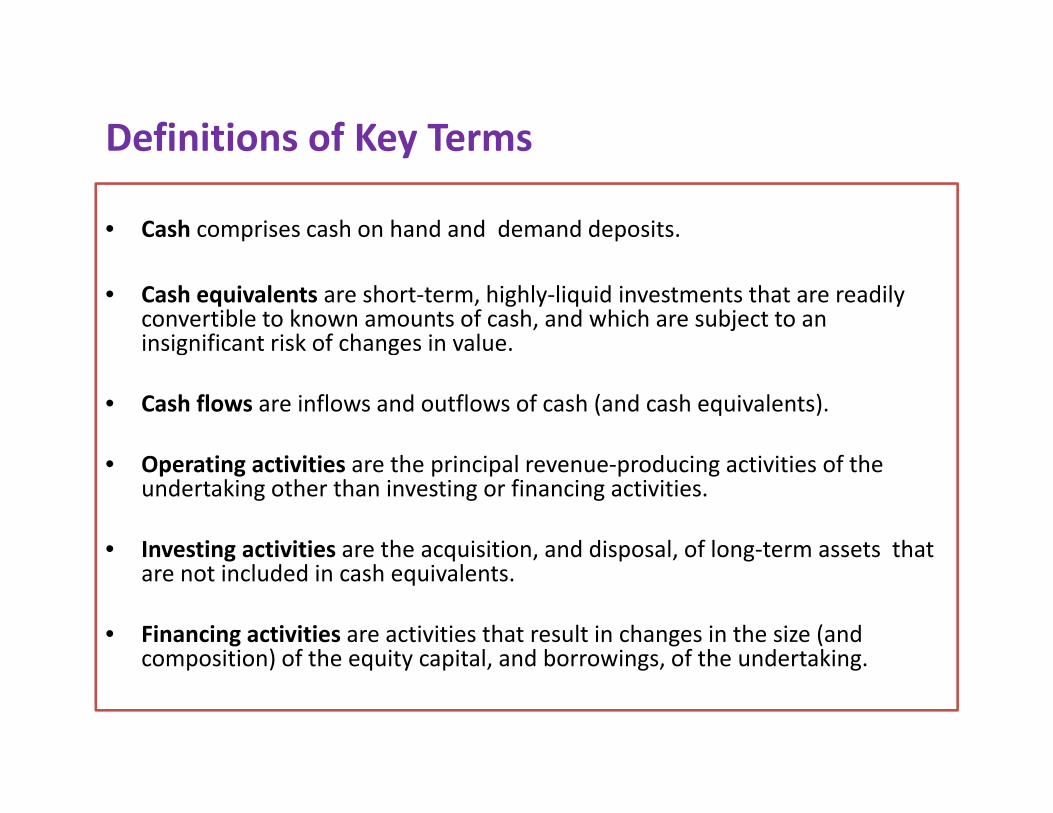

Definitions of Key TermsDefinitions of Key Terms

• Cash comprises cash on hand and demand deposits.

• Cash equivalents are short‐term, highly‐liquid investments that are readily convertible to known amounts of cash, and which are subject to an insignificant risk of changes in value.

• Cash flows are inflows and outflows of cash (and cash equivalents).

O ti ti iti th i i l d i ti iti f th• Operating activities are the principal revenue‐producing activities of the undertaking other than investing or financing activities.

• Investing activities are the acquisition, and disposal, of long‐term assets that g q p gare not included in cash equivalents.

• Financing activities are activities that result in changes in the size (and composition) of the equity capital and borrowings of the undertakingcomposition) of the equity capital, and borrowings, of the undertaking.

Cash and cash equivalents…..explanation

• Cash equivalents are held for the purpose of meeting short‐term cash commitments, rather than for investment.

• For an investment to qualify as a cash equivalent, it must be readily convertible to a known amount of cash, and be subject to an insignificant risk of changes in value.

• An investment normally qualifies as a cash equivalent only when it has a maturity of three months (or less), from the date of acquisition.

• Equity investments are excluded from cash equivalents unless they are inEquity investments are excluded from cash equivalents, unless they are, in substance, cash equivalents, for example in the case of preferred shares acquired within a short period of their maturity (and with a specified redemption date). EXAMPLE‐ Preferred shares acquired within a short period of their maturity

• Bank borrowings are generally considered to be financing activities. However, in some countries, bank overdrafts (which are repayable on demand) form an integral part of an undertaking's cash management.

Presentation and Format

Cash flows from Operating activities: XXX

Cash flows from Investing activities: XXX

Cash flows from Financing activities: XXX

Net increase (decrease) in Cash XXXCash and equivalents, beginning of year XXXq g g yCash and equivalents, end of year XXX

Cash flows from Operating Activities

The amount of cash flows arising from operating activities is a key indicator of the extent to which the operations have generated sufficient cash flows to repay loans, maintain the operating capability of the

d ki di id d ( d k i ) i hundertaking, pay dividends (and make new investments) without recourse to external sources of financing.

ExamplesExamples

• Cash receipt from sale of goods and rendering of services, royalty commission and other revenue

C h t t li f d d i• Cash payment to suppliers for goods and services

• Cash paid to and on behalf of the employees

• For Insurance Company: receipt and payment of claim and other policy benefits

• Income Tax receipt and payments

• Cash advance and loans made by the financial institutions

Operating Activities: A Review

Incur Employee Cash

transactions Sell Products Salaries and Wages

related withacquiring and

and Services q gselling

products and pservices

Make Inventory

Incur Utility andother OperatingMake Inventory

Purchases Costs

Cash flows from Investing Activities The separate disclosure of cash flows arising from investing activities represents the extent to which expenditures have been made for resources intended to generate future income and cash flows.

ExamplesExamples

• Payments/ receipts to acquire/from sales of property, plant and equipment, intangibles and other long‐term assets.

• payments to acquire shares or debt instruments of other undertakings, and interests in joint ventures (other than for instruments that are cash equivalents, or held for dealing (or trading purposes));

• receipts from sales of shares (or debt) instruments of other undertakings and interests in joint ventures (other than for instruments that are cash equivalents, or held for trading purposes); and

• Payments/ receipt for futures contracts, forward contracts, option contracts and swap contracts (except when the contracts are held for dealing or trading purposes, or the payments are classified as financing activities);

Investing Activities: A Review

Purchase/Sell

g

Cash transactions related with

Long‐term Investments

related withacquiring and

disposing of long‐disposing of long‐term assetsBuy/Sell

The separate disclosure of cash flows arising from financing activities is needed to predict claims on cash flows by providers of capital to the undertaking.

Examples• proceeds from issuing shares or other equity instruments;proceeds from issuing shares, or other equity instruments;

• payments to owners to acquire, or redeem the undertaking's shares;

• proceeds from issuing debentures, loans, notes, bonds, mortgages and other short or long‐term borrowings;

t f t b d d• repayments of amounts borrowed; and

• payments by a lessee for the reduction of the outstanding liability relating to a finance lease.relating to a finance lease.

Financing Activities: A Review

Sell/Repurchase Borrow/

g

Cash transactions

Sell/Repurchase Capital Stock

Borrow/ Repay Loans

related withinternal and A

FEDERAL RESERVE NOTE

THE UNITED STATES OF AMERICATHE UNITED STATES OF AMERICA

L70744629F

1212WASHINGTON, D.C.

THIS NOTE IS LEGAL TENDER

FOR ALL DEBTS, PUBLIC AND PRIVATE

H 293

external financing of

1212

L70744629F

ONE DOLLARONE DOLLAR

SERIES1985

the businessIssue/Retire L‐T Bonds Pay DividendsL T Bonds Pay Dividends

Direct Vs. Indirect Method• The choice of direct method vs indirect method is only for the cash

flow from operating activities. There is no difference in cash flow from Investing Activities and Financing Activities in any method.

• IFRS encourages the use of direct method but entity prefers indirect method.

a) The Direct Method: The major classes of gross cash receipts and gross payments are disclosed; and

b) The Indirect Method: The profit or loss is adjusted for the effects of transactions of a non‐cash nature, any deferrals or accruals of past or future operating cash receipts or payments, and items of income or expense associated with investing or financing cash flows.

Direct Method of Cash Flow Statement

+

‐+‐

‐

Direct Method of Cash Flow Statement

Direct Method ‐ Operating Activitiesirect Method Operating Activities

Example:

Accounts receivable, 1/1/10 90,000

p

Credit sales during year 900,000

Less: Accts. receivable, 12/31/10 ( 80,000)

Cash collections $910,000

Direct Method ‐ Operating Activitiesirect Method Operating Activities

Indirect Method of Cash Flow StatementIndirect Method of Cash Flow Statement

++‐+

Adjustment for changes in Working Capital(CA‐CL)

+‐

‐

Note: Cash from Investing and Cash flow from financing Activities are same as direct method.

Indirect Method:Adjustments to Net Income

• Accrual basis includes non‐cash expenses and revenues

Key adjustments:

– Deduct non cash expenses (e g Depreciation Bond– Deduct non‐cash expenses (e.g., Depreciation, Bond Discount Amortization)

– Deduct Gains (e.g., PP&E Disposals, Bond Retirements) *

– Add‐back Losses (e.g., PP&E Disposals, Bond Retirements) *

* Entire cash proceeds from LT asset disposals are shown as Investing Entire cash proceeds from LT asset disposals are shown as Investing activity and from LT debt retirement as Financing activity.

Adjustment for Changes in Balance SheetAdjustment for Changes in Balance Sheet

Some Useful Tips

Interest and Dividends• Cash flows arising from interest and dividends received and paid ( including g p ( g

capitalized) shall each be disclosed separately.

• Cash flows from interest and dividends received and paid shall each be classified in a consistent manner from period to period under appropriate activity heads.

T ITaxes on Income• Cash flows arising from taxes on income shall be separately disclosed.

C h fl i i f t i h ll b l ifi d h fl• Cash flows arising from taxes on income shall be classified as cash flows from operating activities unless they can be specifically identified with financing and investing activities.

Disclosure RequirementsDisclosure Requirements

• Components of Cash and Cash equivalents

• A reconciliation of the amounts for cash and cash equivalents in its statement of cash flows with the equivalent items reported in the statement of financial position.

• The policy that it adopts in determining the composition of cash and cash equivalents

• The effect of any change in the policy for determining the compositions of cash and cash equivalents.

• The amount of significant cash and cash equivalent balances held by the g q yentity that are not available for use by the group, with management comments.

• Any other voluntary disclosures• Any other voluntary disclosures.

![IAS 7 : STATEMENT OF CASH FLOWS - wirc-icai.org1].pdf · How Statement of Cash Flow is Important ? COMPILED BY: MR. YAGNESH DESAI. ... ELEMENTS OF FINANCING CASH FLOW COVERED IN PARA](https://static.documents.pub/doc/80x56/5b14a5fa7f8b9a257c8e3b05/ias-7-statement-of-cash-flows-wirc-icaiorg-1pdf-how-statement-of-cash.jpg)