129

E C I F F O N O I T A U L A V E T N E D N E P E D N I International Monetary Fund Evaluation Report The IMF and Argentina, 1991–2001 The IMF and Argentina, 1991–2001 2004

| Date post: | 07-Sep-2018 |

| Category: |

Documents |

| Upload: | truongkhue |

| View: | 213 times |

| Download: | 0 times |

ECIFF

ON

OITA

ULAVETNEDNEPEDNI

I n t e r n a t i o n a l M o n e t a r y F u n d

Evaluation Report

The IMF and Argentina,1991–2001

The IMF and A

rgentina,1991–2001

IMF 20

04

The IMF and Argentina, 1991–2001

IEO

The IMF and Argentina,1991–2001

I n t e r n a t i o n a l M o n e t a r y F u n d • 2 0 0 4

Evaluation Report

ECIFF

ON

OITA

ULAVETNEDNEPEDNI

© 2004 International Monetary Fund

Production: IMF Multimedia Services DivisionFigures: Jorge A. Salazar

Typesetting: Alicia Etchebarne-Bourdin

Cataloging-in-Publication Data

Price: US$25.00

Please send orders to:International Monetary Fund, Publication Services

700 19th Street, N.W., Washington, D.C. 20431, U.S.A.Tel.: (202) 623-7430 Telefax: (202) 623-7201

E-mail: [email protected]: http://www.imf.org

recycled paper

The IMF and Argentina, 1991–2001 / [prepared by a team headed by ShinjiTakagi] — [Washington, D.C.] : International Monetary Fund, Indepen-dent Evaluation Office, 2004.

p. cm. — [Evaluation report]Includes bibliographical references.ISBN 1-58906-380-5

1. International Monetary Fund — Argentina. 2. Argentina — Economicpolicy. 3. Crisis management — Argentina. I. Takagi, Shinji, 1953– II. Evalu-ation report (International Monetary Fund. Independent Evaluation Office).

HC125.I53 2004

Preface vii

Abbreviations and Acronyms viii

THE IMF AND ARGENTINA, 1991–2001

Executive Summary 3

1 Introduction 8

Overview of Economic Developments, 1991–2001 11Factors Contributing to the Crisis 14

2 Surveillance and Program Design, 1991–2000 17

Exchange Rate Policy 17Fiscal Policy 23Structural Reforms in Macro-Critical Areas 29The Manner of Engagement with Argentina 36

3 Crisis Management, 2000–01 39

Second Review and Augmentation, January 2001 39Completion of Third Review, May 2001 46Fourth Review and Augmentation, September 2001 50Noncompletion of Fifth Review, December 2001 56The Decision-Making Process 58

4 Lessons from the Argentine Crisis 64

Major Findings 64Lessons for the IMF 68Recommendations 73

Boxes

1.1. The IMF and Argentina, 1991–2001 91.2. Was the Convertibility Regime Viable? 151.3. The Politics of the Convertibility Regime 162.1. Economic Characteristics of Hard Peg Economies 182.2. Measuring the Equilibrium Real Exchange Rate 233.1. Framework and Implementation of Private Sector Involvement 433.2. Financial Instruments Used During the Crisis 543.3. Measures Announced or Taken During 2001 Without Prior

Consultation With the IMF 614.1. How and When Could an Alternative Approach Have Been

Attempted? 694.2. Experience with Catalytic Finance 72

Contents

iii

CONTENTS

Figures

1.1. Inflation 111.2. Capital Flows 121.3. Real Quarterly GDP Growth 121.4. Interest Rate Spreads over U.S. Treasuries 132.1. Monthly Real Effective Exchange Rate 192.2. Trade and Current Account Balances 192.3. Comparison of Fiscal Targets and Actuals 242.4. Projected Overall Fiscal Balances and Their Outturns 252.5. Public Sector Debt Targets and Actuals 272.6. Public Sector Debt and General Government Overall Balances 282.7. Real GDP Growth and Unemployment 313.1. IMF and Private Sector (Consensus) Forecasts for Key Program

Variables 453.2. Bank Deposits, January 3, 2000–December 31, 2001 473.3. Evolution of Fiscal Deficit Targets and Outcomes 483.4. International Reserves, January 3, 2000–December 31, 2001 51

Tables

1.1. Key Economic Indicators 103.1. Program Projections and Targets for 2001 413.2. Fiscal Performance Under the Stand-By Arrangement in 2001 48

Appendixes

1 The IMF’s Financing Arrangements with Argentina, 1991–2002 772 Argentina and the IMF Prior to 1991 783 A Retrospective on Argentina’s Fiscal Policy, 1991–2001 804 Selected Program Conditionality, 1991–2001 835 Economic Characteristics of Major Emerging Market Economies 856 Debt Sustainability Analysis 877 A Preliminary Analysis of the 2001 Mega-Swap 908 Financial Instruments Used by Argentina During the Crisis 959 Timeline of Selected Events, 1991–2002 98

10 List of Interviewees 101

Appendix Figures

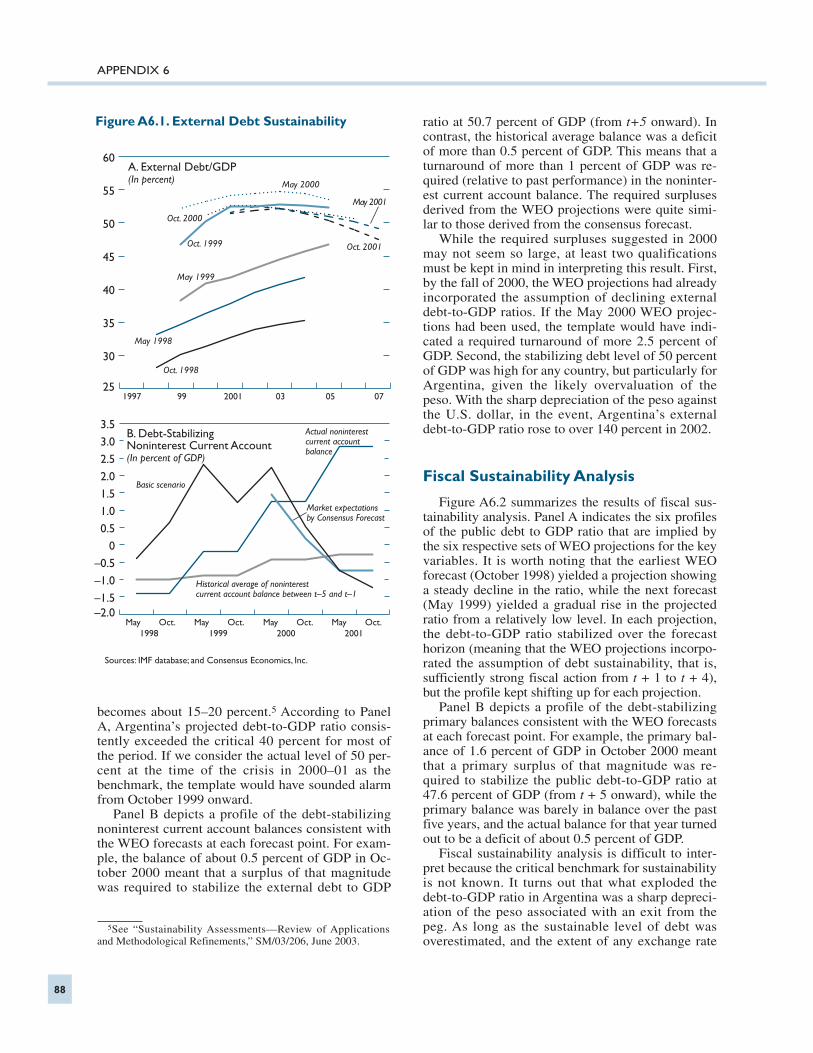

A5.1. General Government Fiscal Balance in Crisis Countries 85A6.1. External Debt Sustainability 88A6.2. Public Debt Sustainability 89A7.1. Exchange Options 90

Appendix Tables

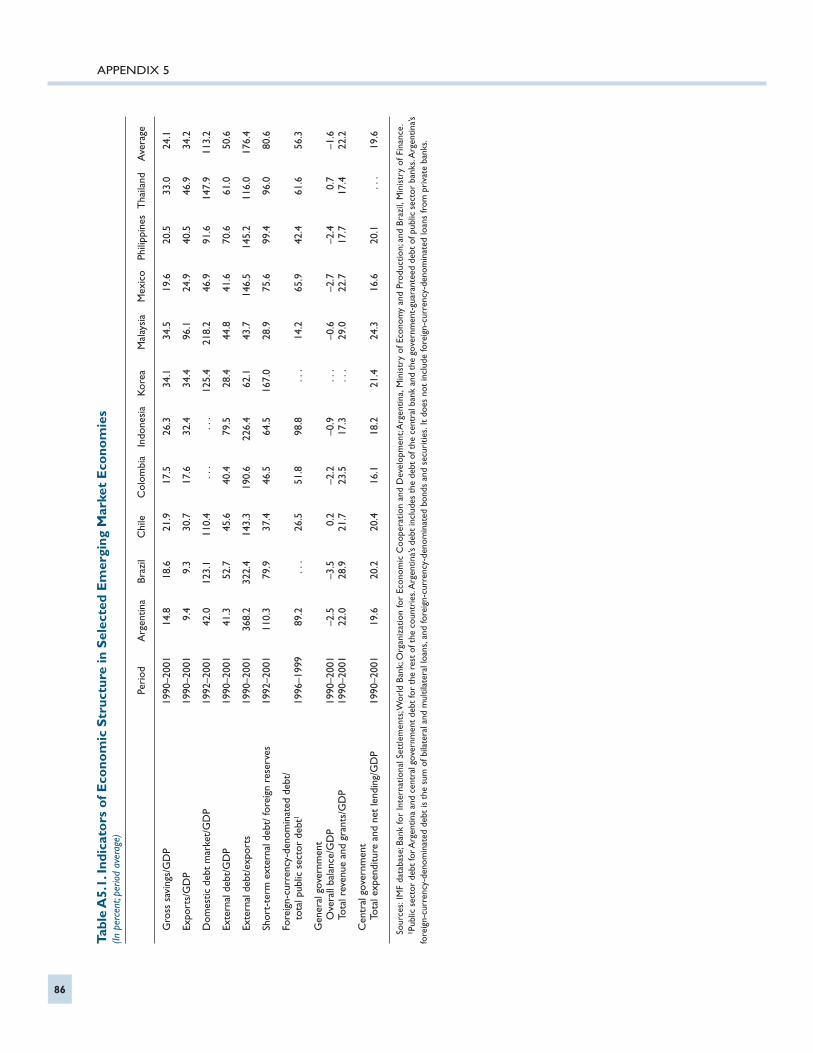

A3.1. Public Sector Balance, 1961–2000 81A3.2. Consolidated Public Sector 81A3.3. Adjusted Fiscal Balance 81A3.4. Social Security Balance 81A3.5. Federal and Provincial Fiscal Accounts 82A5.1. Indicators of Economic Structure in Selected Emerging Market

Economies 86A7.1. An Overview of the Mega-Swap 91A7.2. Details of Old and New Bonds 92

iv

Contents

Bibliography 103

STATEMENT BY THE MANAGING DIRECTOR, IMF STAFF RESPONSE,IEO COMMENTS ON MANAGEMENT/STAFF RESPONSE,STATEMENT BY THE GOVERNOR FOR ARGENTINA,ANDSUMMING UP OF IMF EXECUTIVE BOARD DISCUSSION

BY THE CHAIRMAN

Statement by the Managing Director 109

IMF Staff Response 110

IEO Comments on Management/Staff Response 114

Statement to Executive Board Members from the Governor for Argentina, His Excellency Roberto Lavagna 115

Summing Up of IMF Executive Board Discussion by the Chairman 120

v

The following symbols have been used throughout this report:

– between years or months (e.g. 2003–04 or January–June) to indicate the years ormonths covered, including the beginning and ending years or months;

/ between years (e.g. 2003/04) to indicate a fiscal (financial) year.

“Billion” means a thousand million.

Minor discrepancies between constituent figures and totals are due to rounding.

Some of the documents cited and referenced in this report were not available to the publicat the time of publication of this report. Under the current policy on public access to theIMF’s archives, some of these documents will become available five years after their is-suance. They may be referenced as EBS/YY/NN and SM/YY/NN, where EBS and SMindicate the series and YY indicates the year of issue. Certain other documents are to be-come available ten or twenty years after their issuance depending on the series.

This report evaluates the role of the IMF in Argentina during 1991–2001, focus-ing particularly on the period of crisis management from 2000 until early 2002. It was prepared by a team headed by Shinji Takagi and including Benjamin Cohen,Isabelle Mateos y Lago, Misa Takebe, and Ricardo Martin. It also benefited fromsubstantive contributions from Nouriel Roubini and Miguel Broda. The report wasapproved by Montek S. Ahluwalia, then Director of the Independent Evaluation Of-fice (IEO). Research assistance and logistical support in Argentina from Nicolas Arregui; administrative support by Annette Canizares, Arun Bhatnagar, MariaGutierrez, and Florence Conteh; and editorial work by Ian McDonald and Esha Rayare gratefully acknowledged.

In keeping with standard IEO procedures, parties whose actions and decisionswere evaluated, including IMF staff and previous Argentine authorities, were given achance to comment on a draft of the report, but the final judgments are the responsi-bility of the IEO alone. The final version of the report was submitted to IMF manage-ment for comments, and also circulated simultaneously to Executive Directors. Thereport, with management and staff comments and the IEO response, was discussed bythe Executive Board on July 26, 2004. The report is being published as discussed bythe Board, along with a statement to the Executive Board by the Governor of the IMFfor Argentina and the Chairman’s Summing Up of the Board discussion.

The IEO was created in 2001 to provide objective and independent evaluations onissues relevant to the IMF. It operates independently of IMF management, and atarms’ length from the IMF Executive Board.

Preface

vii

CBA Currency board arrangementCET Common external tariffDSA Debt sustainability analysisEFF Extended Fund Facility (IMF)FAD Fiscal Affairs Department (IMF)FIN Finance Department (IMF)G-7 Group of Seven countriesG-10 Group of Ten countriesICM International Capital Markets Department (IMF)IDB Inter-American Development BankIEO Independent Evaluation Office (IMF)IFI International financial institutionIMF International Monetary FundIMFC International Monetary and Financial Committee (IMF)LIBOR London interbank offered rateLOI Letter of intent (IMF)MAE Monetary and Exchange Affairs Department (IMF)1

MERCOSUR Mercado Común del SurNDA Net domestic assetsNFPS Nonfinancial public sectorNIR Net international reservesNPV Net present valuePAYG Pay-as-you-goPBG Policy-based guarantee (World Bank)PDR Policy Development and Review Department (IMF)PSI Private sector involvementREER Real effective exchange rateRES Research Department (IMF)SBA Stand-By Arrangement (IMF)SDR Special drawing right (IMF)SRF Supplemental Reserve Facility (IMF)TRE Treasurer’s Department (IMF)2

VAT Value-added taxWEO World Economic Outlook (IMF)WHD Western Hemisphere Department (IMF)

1Effective May 1, 2003, name was changed to Monetary and Financial Systems Department.2Effective May 1, 2003, name was changed to Finance Department.

Abbreviations and Acronyms

viii

The IMF and Argentina, 1991–2001

The Argentine crisis of 2000–02 was among themost severe of recent currency crises. With the

economy in a third year of recession, in December2001, Argentina defaulted on its sovereign debt and,in early January 2002, the government abandoned theconvertibility regime, under which the peso had beenpegged at parity with the U.S. dollar since 1991. Thecrisis had a devastating economic and social impact,causing many observers to question the role playedby the IMF over the preceding decade when it was al-most continuously engaged in the country throughfive successive financing arrangements.

Overview

The convertibility regime was a stabilization de-vice to deal with the hyperinflation that existed at thebeginning of the 1990s, and in this it was very suc-cessful. It was also part of a larger Convertibility Plan,which included a broader agenda of market-orientedstructural reforms designed to promote efficiency andproductivity in the economy. Under the ConvertibilityPlan, Argentina saw a marked improvement in its eco-nomic performance, particularly during the earlyyears. Inflation, which was raging at a monthly rate of27 percent in early 1991, declined to single digits in1993 and remained low. Growth was solid throughearly 1998, except for a brief setback associated withthe Mexican crisis, and averaged nearly 6 percent dur-ing 1991–98. Attracted by a more investment-friendlyclimate, there were large capital inflows in the form ofportfolio and direct investments.

These impressive gains, however, masked theemerging vulnerabilities, which came to the surfacewhen a series of external shocks began to hit Ar-gentina and caused growth to slow down in the sec-ond half of 1998. Fiscal policy, though much im-proved from the previous decades, remained weakand led to a steady increase in the stock of debt,much of which was foreign currency denominatedand externally held. The convertibility regime ruledout nominal depreciation when a depreciation of thereal exchange rate was warranted by, among otherthings, the sustained appreciation of the U.S. dollar

and the devaluation of the Brazilian real in early1999. Deflation and output contraction set in, whileArgentina faced increasingly tighter financing con-straints amid investor concerns over fiscal solvency.

The crisis resulted from the failure of Argentinepolicymakers to take necessary corrective measuressufficiently early, particularly in the consistency offiscal policy with their choice of exchange rateregime. The IMF on its part erred in the precrisis pe-riod by supporting the country’s weak policies toolong, even after it had become evident in the late1990s that the political ability to deliver the necessaryfiscal discipline and structural reforms was lacking.By the time the crisis hit Argentina in late 2000, therewere grave concerns about the country’s exchangerate and debt sustainability, but there was no easy so-lution. Given the extensive dollarization of the econ-omy, the costs of exiting the convertibility regimewere already very large. The IMF supported Ar-gentina’s efforts to preserve the exchange rate regimewith a substantial commitment of resources, whichwas subsequently augmented on two occasions. Thissupport was justifiable initially, but the IMF contin-ued to provide support through 2001 despite repeatedpolicy inadequacies. In retrospect, the resources usedin an attempt to preserve the existing policy regimeduring 2001 could have been better used to mitigateat least some of the inevitable costs of exit, if the IMFhad called an earlier halt to support for a strategy that,as implemented, was not sustainable and had pushedinstead for an alternative approach.

Surveillance and Program Design,1991–2000

Exchange rate policy

The convertibility regime was enormously suc-cessful in achieving price stability quickly. Althoughthe IMF was initially skeptical of its medium-term vi-ability, its internal views as well as public statementsbecame much more upbeat when Argentina—with fi-nancial support from the IMF—successfully weath-ered the aftermath of the Mexican crisis, endorsing

Executive Summary

3

EXECUTIVE SUMMARY

the convertibility regime as essential to price stabilityand fundamentally viable. Little substantive discus-sion took place with the authorities on whether or notthe exchange rate peg was appropriate for Argentinaover the medium term, and the issue received scantanalysis within the IMF.

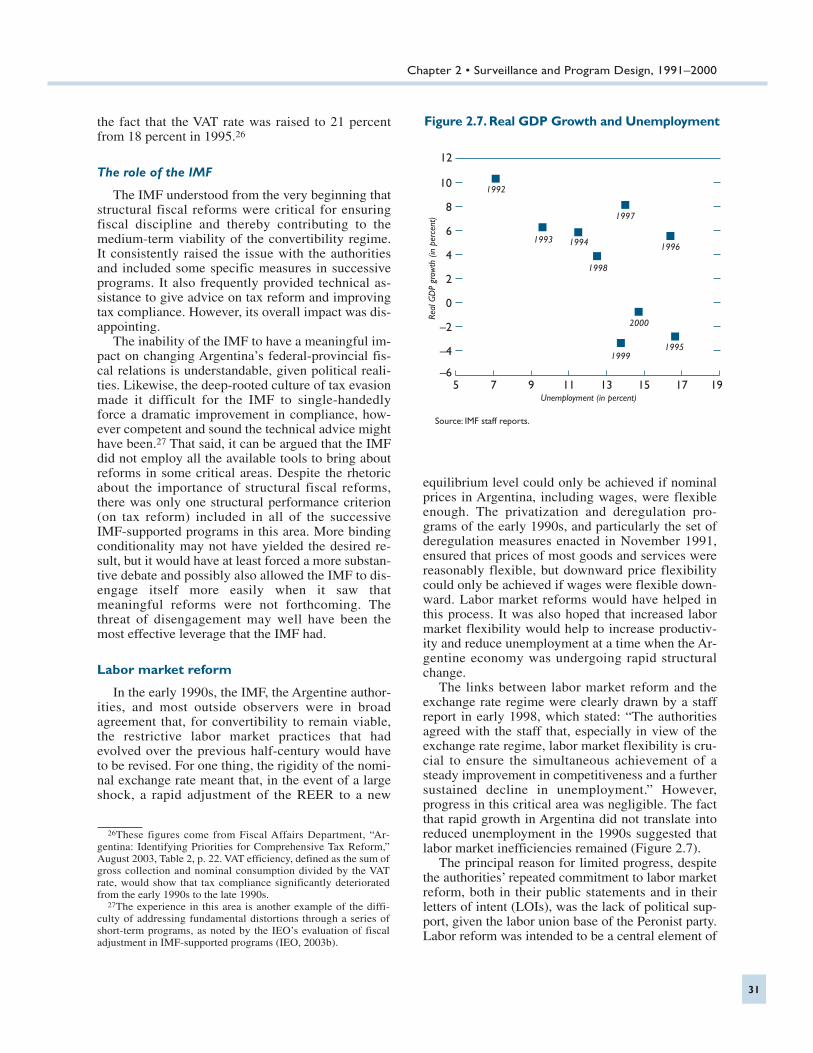

Following the devaluation of the Brazilian realin early 1999, IMF staff began to consider more se-riously the viability of the peg and possible exitstrategies. However, consistent with establishedpractice, but contrary to recent Executive Boardguidelines, the issue was not raised with the author-ities in deference to the country’s prerogative tochoose an exchange rate regime of its own liking.Neither was the issue brought to the attention of theExecutive Board. Not only was the staff concernedthat discussion of exchange rate policy, if leaked tothe public, might cause a self-fulfilling speculativeattack on the currency, but it also knew from its an-alytical work that the risks and costs associatedwith any exit from convertibility were already veryhigh.

Fiscal policy

The choice of the convertibility regime made fis-cal policy especially important. Given the restric-tions on use of monetary policy, debt needed to bekept sufficiently low in order to maintain the effec-tiveness of fiscal policy as the only tool of macro-economic management and the ability of the govern-ment to serve as the lender of last resort. Fiscaldiscipline was also essential to the credibility of theguarantee that pesos would be exchanged for U.S.dollars at par. Fiscal policy was thus rightly thefocus of discussion between the IMF and the author-ities throughout the period. While fiscal policy im-proved substantially from previous decades, the ini-tial gains were not sustained, and the election-drivenincrease in public spending led to a sharp deteriora-tion in fiscal discipline in 1999. As a result, the stockof public debt steadily increased, diminishing theability of the authorities to use countercyclical fiscalpolicy when the recession deepened.

The IMF’s surveillance and program condition-ality were handicapped by analytical weaknessesand data limitations. The IMF’s focus remained onannual fiscal deficits, when off-budget operations,notably the court-ordered recognition of old debt,were raising the stock of debt. Insufficient attentionwas paid to the provincial finances, the sustainablelevel of public debt for a country with Argentina’seconomic characteristics was overestimated, anddebt sustainability issues received limited attention.These deficiencies were understandable, given theexisting professional knowledge, available analyti-cal tools, and data limitations, but the IMF’s high

stake in Argentina should have prompted the staffto explore in greater depth the risks that might arisefrom considerably less favorable economic devel-opments. The more critical error of the IMF, how-ever, was its weak enforcement of fiscal condition-ality, which admittedly was inadequate. The deficittargets involved only moderate adjustments, evenwhen growth was higher than expected, while theywere eased to accommodate growth shortfalls.Even though the annual deficit targets were missedevery year from 1994, financing arrangements withArgentina were maintained by repeatedly grantingwaivers.

Structural reforms

The IMF correctly identified structural fiscal re-forms, social security reform, labor market reform,and financial sector reform as essential to enhancingthe medium-term viability of the convertibilityregime, by promoting fiscal discipline, flexibility,and investment. These views were broadly shared bythe authorities. In fact, most of the initiatives for re-form in these areas came from the authorities; therole of the IMF was largely limited to providingtechnical assistance in the fiscal areas, particularlytax administration. Some gains were made in theearly years, but the long-standing political obstaclesto deeper reforms proved formidable. Little progresswas made in later years, and the earlier reforms wereeven reversed in some cases.

The remarkable feature of the successive IMF-supported programs with Argentina was the paucityof formal structural conditionality. Despite therhetoric about the importance of structural reformsin program documents, only two performance crite-ria (covering tax and social security reforms) wereset in the first three IMF arrangements; in the subse-quent arrangements, not a single performance crite-rion was set, though a number of structural bench-marks were included. Staff consistently expressedreservations over the weak structural content of thesuccessive arrangements, but management, sup-ported by the Executive Board, overruled the staffobjections to approve programs with weak structuralconditionality. As it turned out, the lack of strongstructural conditionality had the unfortunate out-come of obliging the IMF to remain engaged withArgentina when the evident lack of substantiveprogress in structural reform should have called foran end to the program relationship.

Crisis Management, 2000–2001

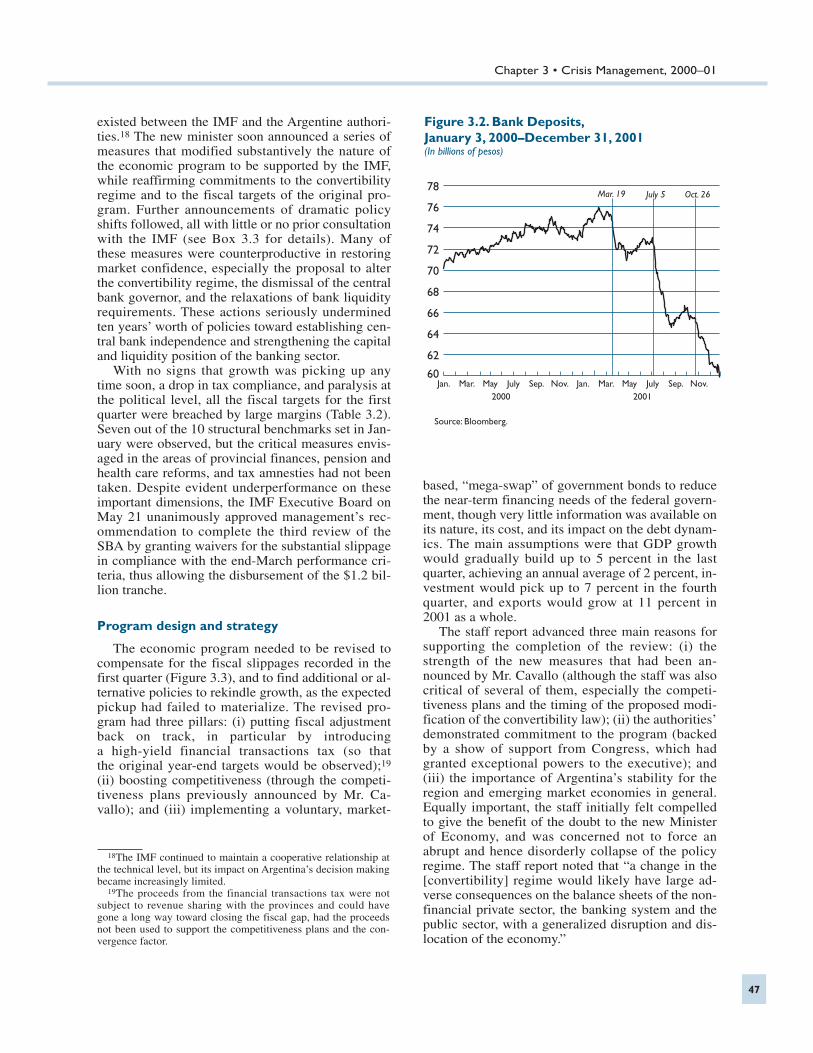

In the fall of 2000, Argentina effectively lost access to voluntary sources of financing. The authori-

4

Executive Summary

ties approached the IMF for a substantial augmenta-tion of financial support under the Stand-By Arrange-ment approved in March 2000, which up to that timehad been treated as precautionary. In response, fromJanuary to September 2001, the IMF made three de-cisions to provide exceptional financial support toArgentina, raising its total commitments to $22 bil-lion. In December, however, the fifth review of theprogram was not completed, which marked the effec-tive cutoff of IMF financial support.

The augmentation decision in January 2001

The decision to augment the existing arrange-ment, approved by the Executive Board in January2001, was based on the diagnosis that Argentinafaced primarily a liquidity crisis and that any ex-change rate or debt sustainability problem wasmanageable with strong action on the fiscal andstructural fronts. The protracted recession wasthought to have resulted from a combination of ad-verse but temporary shocks, and it was assumedthat external economic conditions would improvein 2001. The IMF was also well aware that thecosts of a fundamental change in the policy frame-work would be very large and wished to give theauthorities the benefit of the doubt, when they wereevidently committed to making strong policy cor-rections. Exceptional IMF financing was thusdeemed justified on catalytic grounds. Given theprobabilistic nature of any such decision, the cho-sen strategy may well have proved successful if theassumptions had turned out to be correct (whichthey were not) and if the agreed program had beenimpeccably executed by the authorities (which itwas not). The critical error was not so much withthe decision itself as with the failure to have an exitstrategy, including a contingency plan, in place,inasmuch as the strategy was known to be risky. Noserious discussion of alternative strategies tookplace, as the authorities refused to engage in suchdiscussions and the IMF did not insist.

The decisions to complete the third review inMay and to further augment the arrangementin September 2001

While these decisions still involved uncertainty,the weak implementation of the program in early2001 and the adoption—without consultation withthe IMF—of a series of controversial and market-shaking measures by the authorities after March2001 should have provided ample ground for con-cluding that the initial strategy had failed. In fact,even within the IMF, there was an increasing recog-nition that Argentina had an unsustainable debt pro-file, an unsustainable exchange rate peg, or both. Yet

no alternative course of action was presented to theBoard, and the decisions were made to continue dis-bursing funds to Argentina under the existing policyframework, on the basis of largely noneconomicconsiderations and in hopes of seeing a turnaroundin market confidence and buying time until the ex-ternal economic situation improved.

The decision not to complete the review inDecember 2001

After the September augmentation, economicactivity and market confidence continued to col-lapse, making the achievement of the program’stargets and the salvage of convertibility virtuallyimpossible. While aware of this predicament, theIMF did not press the authorities for a fundamentalchange in the policy regime and announced in earlyDecember that the pending review under the Stand-By Arrangement could not be completed under thecircumstances. Within a month of this announce-ment, economic, social, and political dislocationoccurred simultaneously, leading to the resignationof the President, default on Argentina’s sovereigndebt, and the abandonment of convertibility, soonfollowed by government decisions that further am-plified the costs of the collapse of convertibility. Inthose circumstances, the IMF was unable to pro-vide much help and largely stood by as the crisisunraveled.

The decision-making process

The IMF’s management of the Argentine crisisreveals several weaknesses in its decision-makingprocess. First, contingency planning efforts by thestaff were insufficient. Too much attention wasgiven to determining—inconclusively—which al-ternative policy framework should be recom-mended to the authorities, while little effort wasmade to determine what practical steps the IMFshould take if the chosen strategy failed. Second,from March 2001 on, the relationship between theIMF and the authorities became less cooperative,with the authorities taking multiple policy initia-tives that the IMF viewed as misguided but feltcompelled to endorse. Third, little attention waspaid to the risks of giving the authorities the benefitof the doubt beyond the point where sustainabilitywas clearly in question. Fourth, the ExecutiveBoard did not fully perform its oversight responsi-bility, exploring the potential trade-offs between al-ternative options. To some extent, this appears tohave reflected the fact that some key decisions tookplace outside the Board and that some critical is-sues were judged by management to be too sensi-tive for open discussion in the full Board.

5

EXECUTIVE SUMMARY

Lessons from the Argentine CrisisThe Argentine crisis yields a number of lessons

for the IMF, some of which have already beenlearned and incorporated into revised policies andprocedures. This evaluation suggests ten lessons, inthe areas of surveillance and program design, crisismanagement, and the decision-making process.

Surveillance and program design

• Lesson 1. While the choice of exchange rateregime is one that belongs to country authori-ties, the IMF must exercise firm surveillance toensure that the choice is consistent with otherpolicies and constraints. Candid discussion ofexchange rate policy, particularly when a fixedpeg is involved, must become a routine exerciseduring IMF surveillance.

• Lesson 2. The level of sustainable debt foremerging market economies may be lower thanhad been thought, depending on a country’s eco-nomic characteristics. The conduct of fiscal pol-icy should therefore be sensitive not only toyear-to-year fiscal imbalances, but also to theoverall stock of public debt.

• Lesson 3. The authorities’ decision to treat anarrangement as precautionary should not, but inpractice may, involve a risk of weakened stan-dards for IMF support. Weak program design andweak implementation in the context of arrange-ments being treated as precautionary do not helpa country address its potential vulnerabilities.When there is no balance of payments need, itmay be better not to agree to an arrangement,thus subjecting the country to market disciplinerather than to program reviews by the IMF.

• Lesson 4. Emphasis on country ownership inIMF-supported programs can lead to an undesir-able outcome, if ownership means misguided orexcessively weak policies. The IMF should beprepared not to support strongly owned policiesif it judges they are inadequate to generate a de-sired outcome, while providing the rationale andevidence behind such decisions.

• Lesson 5. Favorable macroeconomic perfor-mance, even if sustained over some period oftime, can mask underlying institutional weak-nesses that may become insuperable obstacles toany quick restoration of confidence, if growth isdisrupted by unfavorable external develop-ments. The IMF may have only a limited role toplay when institutional weaknesses are deeplyrooted in the political system, and structuralconditionality cannot substitute for domesticownership of the underlying reforms.

Crisis management

• Lesson 6. Decisions to support a given policyframework necessarily involve a probabilisticjudgment, but it is important to make this judg-ment as rigorously as possible, and to have afallback strategy in place from the outset in casesome critical assumptions do not materialize.

• Lesson 7. The catalytic approach to the resolu-tion of a capital account crisis works only underquite stringent conditions. When there are well-founded concerns over debt and exchange ratesustainability, it is unreasonable to expect a vol-untary reversal of capital flows.

• Lesson 8. Financial engineering in the form ofvoluntary, market-based debt restructuring iscostly and unlikely to improve debt sustainabil-ity if it is undertaken under crisis conditions andwithout a credible, comprehensive economicstrategy. Only a form of debt restructuring thatleads to a reduction of the net present value(NPV) of debt payments or, if the debt is be-lieved to be sustainable, a large financing pack-age by the official sector has a chance to reverseunfavorable debt dynamics.

• Lesson 9. Delaying the action required to re-solve a crisis can significantly raise its eventualcost, as delayed action can inevitably lead tofurther output loss, additional capital flight, anderosion of asset quality in the banking system.To minimize the costs of any crisis, the IMFmust take a proactive approach to crisis resolu-tion, including providing financial support to apolicy shift, which is bound to be costly regard-less of when it is made.

The decision-making process

• Lesson 10. In order to minimize error and in-crease effectiveness, the IMF’s decision-makingprocess must be improved in terms of riskanalysis, accountability, and predictability. Amore rule-based decision-making procedure,with greater ex ante specification of the circum-stances in which financial support will be avail-able, may facilitate a faster resolution of a crisis,though the outcome may not always be opti-mum. Recent modifications to the exceptionalaccess policy have already moved some way inthis direction.

Recommendations

On the basis of these lessons, the evaluation offers six sets of recommendations to improve

6

Executive Summary

the effectiveness of IMF policies and procedures,in the areas of crisis management, surveillance,program relationship, and the decision-makingprocess.

Crisis management

• Recommendation 1. The IMF should have acontingency strategy from the outset of a crisis,including in particular “stop-loss rules”—thatis, a set of criteria to determine if the initialstrategy is working and to guide the decisionon when a change in approach is needed.

• Recommendation 2. Where the sustainabilityof debt or the exchange rate is in question, theIMF should indicate that its support is condi-tional upon a meaningful shift in the country’spolicy while it remains actively engaged to fos-ter such a shift. High priority should be givento defining the role of the IMF when a countryseeking exceptional access has a solvencyproblem.

Surveillance

• Recommendation 3. Medium-term exchangerate and debt sustainability should form the corefocus of IMF surveillance. To fulfill these objec-tives (which are already current policy), the IMFneeds to improve tools for assessing the equilib-rium real exchange rate that are more forward-looking and rely on a variety of criteria, exam-ine debt profiles from the perspective of “debtintolerance,” and take a longer-term perspectiveon vulnerabilities that could surface over themedium term.

Program relationship

• Recommendation 4. The IMF should refrainfrom entering or maintaining a program rela-tionship with a member country when there isno immediate balance of payments need andthere are serious political obstacles to neededpolicy adjustment or structural reform.

• Recommendation 5. Exceptional access shouldentail a presumption of close cooperation be-tween the authorities and the IMF, and specialincentives to forge such close collaborationshould be adopted, including mandatory disclo-sure to the Board of any critical issue or infor-mation that the authorities refuse to discuss with(or disclose to) staff or management.

The decision-making process

• Recommendation 6. In order to strengthen therole of the Executive Board, procedures shouldbe adopted to encourage: (i) effective Boardoversight of decisions under management’spurview; (ii) provision of candid and full infor-mation to the Board on all issues relevant to de-cision making; and (iii) open exchanges of viewsbetween management and the Board on all top-ics, including the most sensitive ones. These ini-tiatives will be successful only insofar as IMFshareholders—especially the largest ones—col-lectively uphold the role of the Board as theprime locus of decision making in the IMF.While a number of approaches to modifyingBoard procedures to strengthen governance arepossible, and the issue goes beyond the scope ofthe evaluation, some possible steps are discussedin the concluding section of Chapter 4.

7

The Argentine crisis of 2000–02 was among the most severe of recent currency crises. The

currency-board-like arrangement, under which the peso had been pegged at parity with the U.S.dollar since 1991, collapsed in January 2002 and,by the end of 2002, the peso was trading at Arg$3.4to the U.S. dollar. Coming after three years of re-cession, the crisis had a devastating impact. Theeconomy contracted by 11 percent in 2002, bring-ing the cumulative output decline since 1998 tonearly 20 percent. Unemployment rose to over 20percent, and the incidence of poverty worseneddramatically.

The role played by the International MonetaryFund (IMF) deserves special attention for at leastthree reasons. First, unlike the cases of Indonesiaand Korea, where the IMF had no program involve-ment for several years preceding the crisis, in Ar-gentina the IMF had been almost continuously en-gaged through programs since 1991 (Box 1.1).Second, again unlike the other cases, the crisis inArgentina did not explode suddenly. Signs of possi-ble problems were evident at least by 1999, whichled the government to seek a new Stand-ByArrangement (SBA) with the IMF in early 2000.Third, IMF resources were provided in support ofArgentina’s fixed exchange rate regime, which hadlong been stated by the IMF as both essential toprice stability and fundamentally viable. Indeed, inthe debates on fixed versus flexible rates that fol-lowed the East Asian crisis, Argentina’s currency-board-like regime was often held up as an exampleof the kind of credible fixed rate regime that is fun-damentally viable.

This evaluation examines the role of the IMF inArgentina during 1991–2001, with a special focuson the period of crisis management from 2000 up tothe first few days of 2002.1 While the principal focus

of the evaluation is on the crisis period, it is neces-sary to review experience in the preceding decade inorder to shed light on why and how, despite its ex-tensive involvement with the country, the IMF wasnot able to help Argentina prevent and better managethe crisis.

In keeping with the terms of reference of the In-dependent Evaluation Office (IEO), the primary pur-pose of the evaluation is to draw lessons for the IMFin its future operational work. The following qualifi-cations apply:

(1) Any evaluation necessarily benefits fromhindsight. While hindsight can be useful indrawing lessons for the future, in evaluatingthe past, and especially in determining ac-countability, it must be kept in mind that muchof what we know now may not have beenknown to those who had to make the relevantdecisions.

(2) The behavior of an economy is always subjectto uncertainty, and uncertainties increase incrises. Decisions taken in the face of uncer-tainty cannot be judged to represent mistakenjudgment ex ante just because they failed toachieve the results envisaged. It is necessaryto take a probabilistic approach: were the exante probabilities of success high enough tojustify the decision, given the expected benefitof success and the potential costs of an evenmore aggravated crisis if the strategy eventu-ally failed?

(3) To be meaningful, evaluation of a particularstrategy must imply comparison with an alter-native that may have produced better results.However, it is extremely difficult rigorously toestablish such a counterfactual.

(4) The IMF is only one of the actors involved. Inpractice, the country itself is ultimately re-sponsible for its policy decisions. This is espe-cially important when the underlying policychoices are strongly owned by the country—as they were in Argentina.

Introduction

8

CHAPTER

1

1The choice of this period leaves out issues related to the role ofthe IMF in Argentina’s subsequent economic reconstruction andrecovery. The IEO’s terms of reference do not allow it to evaluateissues that have a direct bearing on the IMF’s ongoing operations.

Chapter 1 • Introduction

The evaluation makes extensive use of IMF doc-uments made available to the IEO.2 The IEO, how-ever, is not given automatic access to documentsthat are purely internal to management or thatcover management’s exchanges with national au-thorities, except when such documents were sharedwith staff.3 Since there is often close consultationbetween management and the IMF’s major share-holder governments, and the records available to us

do not cover these consultations, our judgments oncertain policy matters are based on limited infor-mation. This is acknowledged where relevant.

The evaluation team has extensively intervieweda number of those involved in decision making in theIMF as well as some current and former officials ofArgentina and other member countries. The teamhas also benefited from consulting with the exten-sive academic literature on the Argentine crisis andinteracted with a number of individuals who haveexpressed views on the IMF’s role in it.

The report is organized as follows. The rest ofthis chapter provides a brief overview of economicdevelopments from 1991 to early 2002 and dis-cusses factors that contributed to the crisis. Chap-ter 2 evaluates the content and effectiveness of sur-veillance and program design in the precrisis pe-riod, from 1991 to early 2000. The focus is placed on three areas of critical relevance to the IMF,namely (i) exchange rate policy, (ii) fiscal policy,and (iii) macro-critical structural reforms. Chap-ter 3 discusses major issues and procedures associ-ated with the key decisions made by the IMF

9

Box 1.1.The IMF and Argentina, 1991–2001

From 1991 through 2001, the IMF maintained fivesuccessive financing arrangements with Argentina.These included two extended arrangements under theExtended Fund Facility (EFF) approved in 1992 and1998, and three SBAs approved in 1991, 1996, and2000 (see Appendix 1 for details). Of these, the 1998extended arrangement was treated as precautionary,and no drawings were made under it. As a result, thebalance of outstanding IMF credit to Argentina actuallydeclined during 1997–99. It was only in late 2000 thatthe IMF’s exposure to Argentina rose sharply (see fig-ure). In addition, the IMF provided extensive technicalassistance to Argentina, dispatching some 50 missionsduring this period, mainly in the fiscal and bankingareas, in order to support the objectives of the IMF-sup-ported programs.

From early 2000 onward, the IMF-supported pro-grams attempted to address the worsening recession aswell as, from late 2000, Argentina’s inability to accessinternational capital markets. In March 2000, a three-year SBA for SDR 5.4 billion ($7.2 billion) was agreedto and, in January 2001, this was augmented by SDR 5.2billion to SDR 10.6 billion ($13.7 billion). At the sametime, additional financing was arranged from officialand private sources. The total amount of financing wasannounced to be $39 billion, prompting the governmentto use the word “blindaje” (shield) in characterizing thepackage. In September 2001, the arrangement was further augmented by SDR 6.4 billion ($8 billion) toSDR 17 billion ($22 billion), with up to $3 billion setaside to be used in support of a possible debt-restructur-

ing operation. In December 2001, with the hoped-for re-turn of confidence nowhere to be seen and the fiscal pro-gram seriously off track, the scheduled program reviewwas not completed, and IMF support of Argentina waseffectively cut off.

2They include staff reports for Article IV consultations and useof IMF resources, technical assistance reports, briefing papersand back-to-office reports for staff missions and visits, internalmemorandums and technical notes exchanged among staff or be-tween staff and management, minutes or summaries of formaland informal Executive Board meetings, comments by manage-ment and staff on briefing papers, and policy papers prepared bystaff for the Board. Some of these Board policy papers have beenpublished, including on the IMF’s website. Full citations for thesepapers are made in footnotes and not in the bibliography, exceptwhen they are available in print form.

3Management refers to the group of senior IMF officials con-sisting of the Managing Director, the First Deputy Managing Di-rector, and two Deputy Managing Directors.

Financial Transactions Between Argentina and the IMF(In millions of SDRs)

Source: IMF database.

1991 92 93 94 95 96 97 98 99 2000 01 02–2000

0

2000

4000

6000

8000

10000

12000Disbursements

Net flowCredit outstanding

Repayments and charges

CHAPTER 1 • INTRODUCTION

10

Tabl

e 1.

1.K

ey E

cono

mic

Ind

icat

ors

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Rea

l GD

P gr

owth

(pe

rcen

t)10

.510

.36.

35.

8–2

.85.

58.

13.

8–3

.4–0

.8–4

.4–1

0.9

Rea

l pri

vate

con

sum

ptio

n gr

owth

(pe

rcen

t)15

.012

.17.

15.

4–4

.07.

38.

72.

5–4

.00.

3–4

.9–1

3.3

Rea

l pub

lic c

onsu

mpt

ion

grow

th (

perc

ent)

–13.

122

.712

.12.

7–1

.6–0

.93.

87.

15.

6–0

.1–1

.9–1

3.5

Rea

l fix

ed in

vest

men

t gr

owth

(pe

rcen

t)31

.533

.516

.013

.7–1

3.0

8.8

17.7

6.5

–12.

6–6

.8–1

5.7

–36.

4

Infla

tion

(CPI

,Dec

./Dec

.,pe

rcen

t)84

.017

.57.

43.

91.

60.

10.

30.

7–1

.8–0

.7–1

.541

.0M

oney

(M

1,D

ec./D

ec.,

perc

ent,

in p

esos

)14

8.6

49.0

33.0

8.2

1.6

14.6

12.8

0.0

1.6

–9.1

–20.

178

.4Br

oad

mon

ey (

Dec

./Dec

.,pe

rcen

t,in

pes

os)

167.

963

.055

.914

.9–4

.320

.026

.910

.32.

34.

4–1

9.7

18.3

Cur

rent

acc

ount

bal

ance

(bi

llion

U.S

.dol

lars

)–0

.4–6

.5–8

.0–1

1.1

–5.2

–6.8

–12.

2–1

4.5

–11.

9–8

.8–4

.59.

6(In

per

cent

of G

DP)

–0.2

–2.9

–3.4

–4.3

–2.0

–2.5

–4.2

–4.9

–4.2

–3.1

–1.7

3.1

Expo

rt o

f goo

ds a

nd s

ervi

ces

(U.S

.dol

lars

,per

cent

gro

wth

)–2

.13.

48.

517

.828

.913

.69.

00.

7–1

0.5

11.6

–0.5

–7.4

Impo

rt o

f goo

ds a

nd s

ervi

ces

(U.S

.dol

lars

,per

cent

gro

wth

)68

.358

.830

.311

.3–4

.615

.824

.13.

4–1

5.3

0.5

–16.

6–5

2.6

Publ

ic s

ecto

r de

bt (

perc

ent

of G

DP)

34.8

28.3

30.6

33.7

36.7

39.1

37.7

40.9

47.6

50.9

62.2

...

Exte

rnal

deb

t (p

erce

nt o

f GD

P)34

.527

.730

.533

.338

.440

.642

.747

.551

.251

.652

.242

.9D

ebt

serv

ice

ratio

(pe

rcen

t)33

.627

.530

.925

.230

.239

.450

.057

.675

.470

.866

.3..

.

Inte

rnat

iona

l res

erve

s m

inus

gol

d (b

illio

n U

.S.d

olla

rs)

6.2

10.2

14.0

14.6

14.5

18.3

22.3

24.8

26.3

25.1

14.6

10.5

Exch

ange

rat

e (p

eso/

U.S

.dol

lar,

end-

peri

od)

1.0

1.0

1.0

1.0

1.0

1.0

1.0

1.0

1.0

1.0

1.0

3.4

Rea

l effe

ctiv

e ex

chan

ge r

ate

(end

-per

iod)

114

0.5

165.

417

7.8

169.

316

2.9

163.

317

5.8

170.

617

7.6

184.

818

4.7

71.6

Term

s of

tra

de (

good

s an

d se

rvic

es,

perc

ent

chan

ge)

7.6

6.1

–7.7

14.4

–4.5

9.9

0.2

–5.1

–8.4

7.2

–5.7

–10.

8

Cen

tral

gov

ernm

ent

prim

ary

bala

nce

(per

cent

of G

DP)

...

1.3

2.1

0.8

0.1

–0.5

0.4

0.9

0.4

1.0

0.1

0.7

Gen

eral

gov

ernm

ent

prim

ary

bala

nce

(per

cent

of G

DP)

...

1.3

1.5

0.1

–1.3

–0.7

0.3

0.5

–0.8

0.5

–1.4

0.3

Cen

tral

gov

ernm

ent

over

all b

alan

ce

(per

cent

of G

DP)

...

–0.2

0.9

–0.5

–1.5

–2.2

–1.6

–1.3

–2.5

–2.4

–3.8

–11.

9G

ener

al g

over

nmen

t ov

eral

l bal

ance

(p

erce

nt o

f GD

P)..

.–0

.40.

1–1

.4–3

.2–2

.9–2

.1–2

.1–4

.2–3

.6–6

.2–1

2.8

Sour

ces:

IMF

data

base

;and

Wor

ld B

ank,

Glo

bal D

evel

opm

ent F

inan

ce.

1 Ave

rage

of 1

990

= 1

00.

Chapter 1 • Introduction

during the crisis period, from late 2000 through theend of 2001. These decisions include (i) the com-pletion of the second review and augmentation ofthe SBA (January 2001); (ii) the completion of thethird review (May 2001); (iii) the completion of thefourth review and augmentation (September 2001);and (iv) the noncompletion of the fifth review (De-cember 2001), which was effectively the cutoff ofIMF financial support. Chapter 4 summarizesmajor findings of the evaluation, draws lessons forthe IMF from the Argentine experience, and pre-sents six sets of recommendations. Finally, ten ac-companying appendixes provide more detailed in-formation and analyses on some of the issuesdiscussed in the report, including a timeline ofmajor events and a list of interviewees.

Overview of Economic Developments, 1991–2001

The Convertibility Law, which pegged the Ar-gentine currency to the U.S. dollar in April 1991,was a response to Argentina’s dire economic situa-tion at the beginning of the 1990s. Following morethan a decade of high inflation and economic stag-nation, and after several failed attempts to stabilizethe economy, in late 1989 Argentina had fallen intohyperinflation and a virtual economic collapse (seeAppendix 2). The new exchange rate regime, whichoperated like a currency board, was designed to sta-bilize the economy by establishing a hard nominalpeg with credible assurances of nonreversibility.The new peso (set equal to 10,000 australes) wasfixed at par with the U.S. dollar and autonomousmoney creation by the central bank was severelyconstrained, though less rigidly than in a classicalcurrency board.4 The exchange rate arrangementwas part of a larger Convertibility Plan, which included a broader agenda of market-orientedstructural reforms to promote efficiency and pro-ductivity in the economy. Various service sectorswere deregulated, trade was liberalized, and anti-competitive price-fixing schemes were removed;privatization proceeded vigorously, notably in oil,

power, and telecommunications, yielding large cap-ital revenues.

There was a marked improvement in Argentina’seconomic performance under the ConvertibilityPlan, particularly during its early years (Table 1.1).Inflation, which was raging at a monthly rate of 27percent in February 1991, declined to 2.8 percent inMay 1991; on an annual basis, inflation fell to singledigits in the summer of 1993 and remained low (oreven negative) from 1994 to the end of the convert-ibility regime in early 2002 (Figure 1.1). The overallfiscal balance of the federal government improvedsignificantly from the previous years, with an aver-age budgeted deficit of less than 1 percent of GDPduring 1991–98.

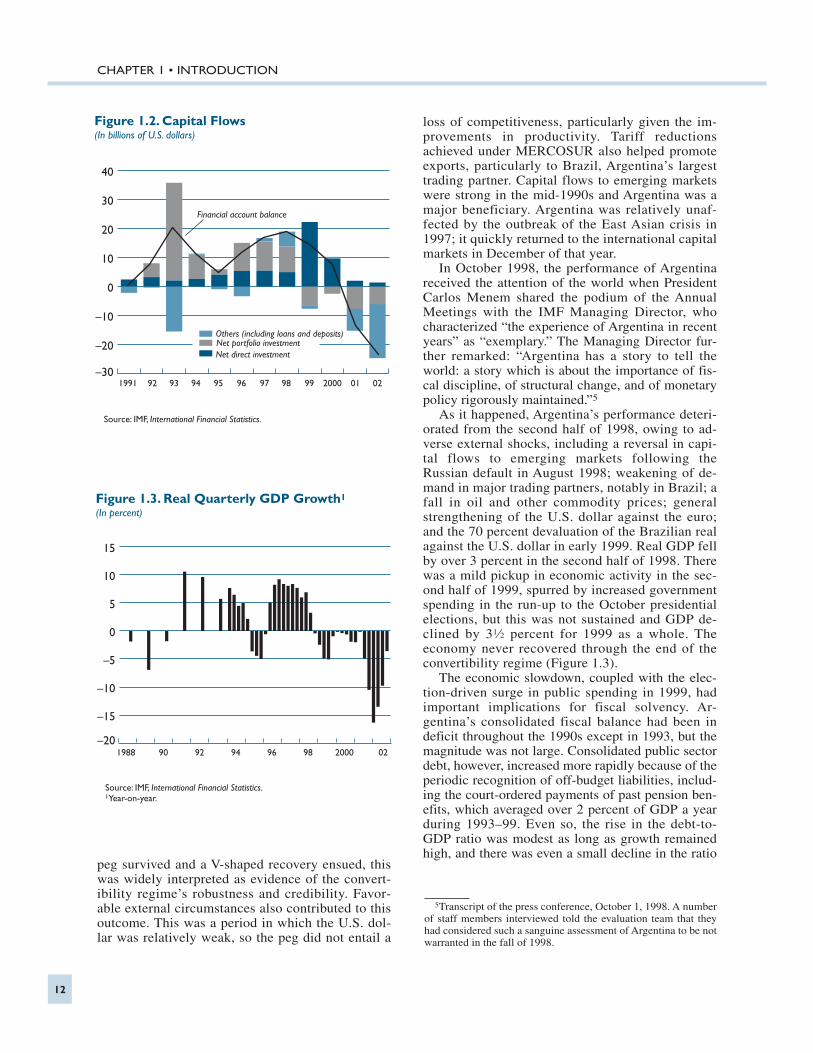

Growth performance was impressive throughearly 1998, except for a brief setback in 1995 whenArgentina was adversely affected by the Mexicancrisis. For 1991–98, GDP growth averaged nearly 6percent a year, vindicating the market-oriented re-forms introduced in the early 1990s. Attracted by amore investment-friendly climate, there were largecapital inflows in the form of portfolio and direct in-vestments. During 1992–99, Argentina receivedmore than $100 billion in net capital inflows, includ-ing over $60 billion in gross foreign direct invest-ments (Figure 1.2).

The resilience of the convertibility regime wasseverely tested by the Mexican crisis in 1995. In re-sponse, Argentina launched a rigorous adjustmentprogram under IMF financial support, consisting ofstrong fiscal action and structural reform. When the

11

4The Convertibility Law was approved by Congress on March27, 1991, establishing full convertibility of the austral at A10,000per U.S. dollar (or the new peso created in January 1992 at Arg$1per U.S. dollar), requiring the central bank in principle to backfully the monetary base with foreign exchange reserves, and pro-hibiting indexation of local-currency-denominated contracts. Un-like a “classical” currency board, however, the central bank wasallowed to hold U.S. dollar-denominated domestic debt as a coverfor part of base money, and was also not required to intervene tosupport the dollar (i.e., the peso technically could appreciateabove parity). See, for example, Baliño and others (1997) andHanke and Schuler (2002).

1992 93 94 95 96 97 98 99 2000 01 02–10

0

10

20

30

40

50

Figure 1.1. Inflation1

(In percent)

Source: IMF, International Financial Statistics.1Year-on-year change in CPI.

CHAPTER 1 • INTRODUCTION

peg survived and a V-shaped recovery ensued, thiswas widely interpreted as evidence of the convert-ibility regime’s robustness and credibility. Favor-able external circumstances also contributed to thisoutcome. This was a period in which the U.S. dol-lar was relatively weak, so the peg did not entail a

loss of competitiveness, particularly given the im-provements in productivity. Tariff reductionsachieved under MERCOSUR also helped promoteexports, particularly to Brazil, Argentina’s largesttrading partner. Capital flows to emerging marketswere strong in the mid-1990s and Argentina was amajor beneficiary. Argentina was relatively unaf-fected by the outbreak of the East Asian crisis in1997; it quickly returned to the international capitalmarkets in December of that year.

In October 1998, the performance of Argentinareceived the attention of the world when PresidentCarlos Menem shared the podium of the AnnualMeetings with the IMF Managing Director, whocharacterized “the experience of Argentina in recentyears” as “exemplary.” The Managing Director fur-ther remarked: “Argentina has a story to tell theworld: a story which is about the importance of fis-cal discipline, of structural change, and of monetarypolicy rigorously maintained.”5

As it happened, Argentina’s performance deteri-orated from the second half of 1998, owing to ad-verse external shocks, including a reversal in capi-tal flows to emerging markets following theRussian default in August 1998; weakening of de-mand in major trading partners, notably in Brazil; afall in oil and other commodity prices; generalstrengthening of the U.S. dollar against the euro;and the 70 percent devaluation of the Brazilian realagainst the U.S. dollar in early 1999. Real GDP fellby over 3 percent in the second half of 1998. Therewas a mild pickup in economic activity in the sec-ond half of 1999, spurred by increased governmentspending in the run-up to the October presidentialelections, but this was not sustained and GDP de-clined by 3!/2 percent for 1999 as a whole. Theeconomy never recovered through the end of theconvertibility regime (Figure 1.3).

The economic slowdown, coupled with the elec-tion-driven surge in public spending in 1999, hadimportant implications for fiscal solvency. Ar-gentina’s consolidated fiscal balance had been indeficit throughout the 1990s except in 1993, but themagnitude was not large. Consolidated public sectordebt, however, increased more rapidly because of theperiodic recognition of off-budget liabilities, includ-ing the court-ordered payments of past pension ben-efits, which averaged over 2 percent of GDP a yearduring 1993–99. Even so, the rise in the debt-to-GDP ratio was modest as long as growth remainedhigh, and there was even a small decline in the ratio

12

Figure 1.3. Real Quarterly GDP Growth1

(In percent)

Source: IMF, International Financial Statistics.1Year-on-year.

–20

–15

–10

–5

0

5

10

15

1988 90 92 94 96 98 2000 02

5Transcript of the press conference, October 1, 1998. A numberof staff members interviewed told the evaluation team that theyhad considered such a sanguine assessment of Argentina to be notwarranted in the fall of 1998.

Figure 1.2. Capital Flows(In billions of U.S. dollars)

Source: IMF, International Financial Statistics.

1991 92 93 94 95 96 97 98 99 2000 01 02–30

–20

–10

0

10

20

30

40

Others (including loans and deposits)Net portfolio investmentNet direct investment

Financial account balance

Chapter 1 • Introduction

from 1996 to 1997. The situation changed in 1999,when growth decelerated and the public finances de-teriorated sharply. The debt-to-GDP ratio rose from37.7 percent of GDP at end-1997 to 47.6 percent atend-1999, an increase of 10 percentage points in justtwo years. The ratio would eventually reach 62 per-cent at the end of 2001.

Argentina’s problems intensified in 2000, whengrowing solvency concerns over the cumulative in-crease in public debt were exacerbated by the con-tinued appreciation of the U.S. dollar and a furtherdrying up of capital flows to emerging marketeconomies. These developments would normally re-quire a smaller current account deficit and a depreci-ation of the real exchange rate, but the convertibilityregime placed severe limitations on the ability of Ar-gentina to achieve this adjustment in a manner thatcould avoid recession. Argentina initially sought torestore market confidence by negotiating an SBAwith the IMF, which it indicated would be treated asprecautionary.6

Market confidence did not recover as expectedand market access was effectively lost later in theyear, leading Argentina to seek an augmentation ofIMF support. From December 2000 to September2001, the IMF made a series of decisions to provideexceptional financial support to Argentina, whichultimately amounted to SDR 17 billion, includ-ing the undrawn balance under the existingarrangement (see Box 1.1 for details). However,stabilization proved elusive. The augmentation an-nounced in December 2000 and formally approvedin January 2001 had a favorable effect, but it wasshort-lived. Pressure built up again as it became ev-ident that political support for the agreed measureswas lacking and program targets were unlikely tobe met.

From the spring of 2001, the authorities took a se-ries of measures in quick succession, including: anannounced plan to change the anchor of the convert-ibility regime from the U.S. dollar to an equallyweighted basket of the dollar and the euro (theswitch to take effect only when the two currenciesreached parity); a series of heterodox industrial or protectionist policies (called “competitivenessplans”), involving various tax-exemption measuresin sectors most adversely affected by the recession;and an exchange of outstanding government bondstotaling $30 billion in face value for longer maturity

instruments (the so-called mega-swap).7 Many ofthese measures, which were taken without consulta-tion with the IMF, were perceived by the markets asdesperate or impractical, and served to damage mar-ket confidence.

Despite these initiatives and the financial supportof the IMF, market access could not be restored, andspreads on Argentine bonds rose sharply in the thirdquarter of 2001 (Figure 1.4). Amid intensified capi-tal flight and deposit runs, capital controls and a par-tial deposit freeze were introduced in December2001. With Argentina failing to comply with the fis-cal targets, the IMF indicated that it could not clearthe disbursement scheduled for December. At theend of December, following the resignation of Presi-dent Fernando De La Rúa, the country partially de-faulted on its international obligations. In early Janu-ary 2002, Argentina formally abandoned theconvertibility regime and replaced it with a dual ex-change rate system.

13

Figure 1.4. Interest Rate Spreads over U.S. Treasuries1

(In basis points)

Source: Datastream.1JP Morgan Emerging Market Bond Index (EMBI)—Global Stripped Spreads.

1994 95 96 97 98 99 2000 010

1000

2000

3000

4000

5000

6000EMBI Global Argentina

EMBI Global BradyEMBI Global Composite

6In IMF terminology, a financing arrangement is considered as“precautionary” if the authorities indicate an intention not to drawon the resources provided. However, there is no legal distinction between precautionary and regular arrangements, as the authori-ties have the right to use the resources made available under thearrangement, should circumstances change.

7Other measures included: (i) a transitional compensationmechanism (called the convergence factor) to mimic the basketpeg through fiscal means, by paying exporters a subsidy andcharging importers a duty equivalent to the difference between theprevailing exchange rate and the exchange rate calculated by thebasket; and (ii) the zero deficit plan (which subsequently becamelaw), mandating the government, in the event of a prospectivedeficit, to introduce across-the-board proportional cuts in primaryexpenditures, which revealed the dire liquidity position of thegovernment and was generally perceived as impractical. See Box3.3 for the chronology of these and other additional measures.

CHAPTER 1 • INTRODUCTION

Factors Contributing to the Crisis

The causes of the Argentine crisis have beenstudied extensively, and a considerable literaturehas emerged on the subject (see, for example,Mussa, 2002; Hausman and Velasco, 2002; de laTorre and others, 2002; and Perry and Servén,2002). The IMF also conducted its own internal re-view and drew a number of lessons from the crisis.8There is a general agreement that a combination ofdomestic and external factors contributed to the cri-sis, but different authors have emphasized differentfactors as relatively more important. Most have em-phasized one or more of the following three factorsas critically important: (i) weak fiscal policy(Mussa, 2002); (ii) the rigid exchange rate regime(Gonzales Fraga, 2002); and (iii) adverse externalshocks (Calvo and others, 2002). Some havestressed a combination of these factors as critical(Feldstein, 2002; Krueger, 2002).9

It is difficult to isolate, from the many factors in-volved, those that were fundamentally more impor-tant. It is possible, however, to distinguish betweenthe underlying factors that generated vulnerabilityand the immediate factors that triggered the crisis. Inthe absence of triggering events, a crisis may nothave occurred when it did, but the underlying vul-nerability would have continued and a crisis couldhave been triggered later by other adverse shocks. Inthe absence of the underlying vulnerability, however,the same adverse developments would not have hadthe catastrophic effects that were associated with thecrisis, though they may well have produced somenegative effects.

It is clear that Argentina’s vulnerability arosefrom the inconsistency between the weakness offiscal policy and its choice of the convertibilityregime. The weak fiscal policy created serious liq-uidity problems for the government when marketconditions tightened and led to the eruption of afunding crisis in early 2001. If Argentina’s publicsector had generated surpluses in its fiscal accountduring the precrisis years, it could have avoided thetightening liquidity constraints in 2000 and the all-out funding crisis of the public sector in 2001.

Argentina also would have enjoyed greater flexibil-ity in using fiscal policy to cope with the impact ofadverse shocks, and would have been spared fromthe need to contract fiscal policy when output wasalready declining.

Underlying this poor fiscal performance were Ar-gentina’s weak political institutions, which persis-tently pushed the political system to commit morefiscal resources than it was capable of mobilizing.Public expenditure could not be controlled becausespending was often used as an instrument of politicalfavor. Tax administration was also weak, leading towidespread tax avoidance and evasion, and efforts toimprove tax compliance were not successful. Furthercomplicating fiscal management were certain fea-tures of Argentina’s federal structure. The system ofrepresentation gave power to the provinces, which inturn relied on the federal government for much oftheir tax revenue. Provincial politicians enjoyed alarge share of the political benefit of spending withlittle of the cost of taxation, creating poor incentivesfor fiscal responsibility. On the federal level, the revenue-sharing (“coparticipation”) arrangements,under which the proceeds of some taxes (but not oth-ers) were shared with the provinces, led to highlydistortionary tax policies (by creating incentives touse nonshared taxes, such as payroll and financialtransactions taxes).10 Under these circumstances, in-centives to collect tax remained weak both in theprovinces and at the federal level (Tommasi, 2002;Spiller and Tommasi, 2003).

Though extremely effective initially as a stabi-lization tool, the convertibility regime was a riskychoice for Argentina over the medium term (Box1.2). By all but eliminating money creation as asource of revenue, it raised the required level of fis-cal discipline. While this was extremely positive interms of its impact on inflation, it also increased thepotential long-term disruptive effect if the fiscal dis-cipline was not fully delivered. It also made adjust-ment to adverse shocks more difficult by eliminatingnominal depreciation as an instrument of policy. Hadwages and prices been sufficiently flexible down-ward, the required real exchange rate depreciationcould have been achieved through price deflation. In

14

10As another aspect of the coparticipation scheme, there was atendency for excessive spending cuts to be made at the federallevel when fiscal adjustment was required, because any effort toincrease shared tax would lose a large share to the provinces. Itwas for this reason that Economy Minister José Luis Machinea in1999 negotiated a temporary arrangement with the provinces,whereby the federal government would transfer a fixed amount tothe provinces regardless of the amount of tax collected. SeeCuevas (2003). Coming at a time of deepening recession, how-ever, the fixed transfer scheme did not help the federal govern-ment improve its finances.

8Policy Development and Review Department, “Lessons fromthe Crisis in Argentina,” SM/03/345, October 2003. Henceforthreferred to as PDR (2003). See also Collyns and Kincaid (2003)for broader lessons on Latin America.

9There are studies that emphasize “structural” factors, such aseconomic liberalization and the volatility and procyclicality of in-ternational capital flows (Frenkel, 2003; Damill and Frenkel,2003) and political factors (Corrales, 2002). As early as 1997, theinsightful political analyses of Gibson (1997) and Starr (1997)predicted an eventual collapse of the convertibility regime basedon political factors existing at that time. For a more complete listof studies on the Argentine crisis, see the bibliography.

Chapter 1 • Introduction

the absence of downward wage flexibility, the im-provement in the current account required by the se-ries of adverse shocks that hit Argentina from late1998 could only be achieved through a prolongeddemand contraction.

Compounding these vulnerabilities was Argen-tina’s limited market for domestic borrowing andits limited ability to issue long-term debt denomi-nated in its own currency. As a result, the govern-ment relied heavily on external borrowing in for-eign currencies. The combination of a weak fiscalpolicy and heavy reliance on external borrowingwithin the constraint of the convertibility regimebecame a recipe for disaster, when the country washit by the prolonged adverse shocks. In particular, asharp reduction, or “sudden stop” in the terminol-

ogy of Calvo and others (2002), in global capitalflows to emerging market economies increasinglyraised the cost of external financing, and worsenedthe fiscal situation. Thanks to careful managementof maturity structure, the impact of the sudden stopon the public sector’s immediate financing needwas not as great as it would have been had more ofthe debt been contracted at shorter maturities, butthis only meant that the crisis took a few years todevelop.

Political factors also played a prominent role inArgentina (Box 1.3). The new government of Fer-nando De La Rúa, who took office in December1999 in the midst of growing signs of economic dif-ficulties, was a coalition (Alianza) of the centristRadical party and the center-left FREPASO party,

15

Box 1.2.Was the Convertibility Regime Viable?

Some authors have argued that the convertibilityregime (a hard peg to the U.S. dollar) was fundamen-tally unviable and thus doomed to fail from the incep-tion (Curia, 1999; and Gonzales Fraga, 2002). Issuesrelated to a choice of exchange rate regime are com-plex. Here, we will only consider one aspect of thechoice, namely, the ability of an exchange rate regimeto accommodate shocks that require a change in thereal exchange rate.

In considering the viability of the convertibilityregime for Argentina, there are three relevant questionsto ask:

• How frequent and large are required real exchangerate changes?

• How effectively can a required real exchange ratechange be accommodated in the absence of nomi-nal exchange rate flexibility?

• Assuming that the impact of a relevant shock is ad-verse and prolonged, how resilient is the economyagainst sustained deflation (when nominal flexibil-ity is sufficient) or sustained output contraction(when insufficient)?

Several of Argentina’s real characteristics were notideal for supporting a peg to the U.S. dollar: (i) exportswere predominantly homogeneous goods subject to fre-quent global shocks; (ii) Argentina’s small total trade-to-GDP ratio (about 16 percent) required a large real ex-change rate change to generate a given size of externaladjustment; (iii) the U.S. share of trade was relativelysmall (about 15 percent); and (iv) Argentina and theUnited States did not share closely correlated businesscycles. These were factors that could require frequentand possibly large real exchange rate changes, particu-larly with a fixed peg to the U.S. dollar, although there isno presumption that those changes would be necessarilylarge relative to the capacity of the country.

A country’s ability to respond to a required change inthe real exchange rate depends on the flexibility of itsmarkets and institutions. In Argentina, at the inceptionof the convertibility regime, its institutional rigidities inthe product and labor markets limited this ability. Butthese rigidities were an outcome of policy, and it wasfor this reason that a series of structural reforms werepursued in these areas in the early 1990s. Much rigidityremained, particularly in the labor market, but, giventhe magnitude and number of adverse shocks that hitArgentina in the late 1990s, it probably would havebeen unrealistic to expect that the country’s nominaland real flexibility alone could deliver the required ad-justment quickly.

Likewise, much of what makes up the resilience ofan economy—such as financial sector soundness andfiscal discipline—is also policy-driven. In terms of fi-nancial sector soundness, Argentina had a strong bank-ing system as measured by conventional prudential cri-teria, and the banking system did withstand the adverseimpact of the crisis for some time. What weakened theresilience of the Argentine economy was the lack of fis-cal discipline, in an environment where the public sec-tor relied on external borrowing. If Argentina had per-sistently generated fiscal surpluses throughout the1990s, the government would have retained capacity tofinance the economy out of recession; if it had less ex-ternal borrowing, the impact of the adverse shockswould have been less immediate. With a large real ex-change rate shock, prolonged output contraction mayhave been unavoidable, but the country could have usedits borrowing capacity to remain afloat until many ofthe shocks inevitably reversed themselves.

More fundamentally, the longer-term viability of anyfixed exchange rate regime depends on the degree ofpolitical support—in this case, the understanding of thetough policies needed to keep the convertibility regimeviable and the willingness to accept them.

CHAPTER 1 • INTRODUCTION

which represented divergent views of priorities ineconomic policy. The Alianza enjoyed a workingmajority in the Lower House of Congress, but theSenate and the majority of the provinces, includingthe three largest ones, remained under the control ofthe main Justicialist (Peronist) opposition. Internaldifferences within the government and its inability toreceive broad support within the larger political es-tablishment undermined the credibility of many gov-ernment initiatives. The fragile state of the coalition,as well as the lack of broader political support, led to

the resignation of Vice President Carlos Álvarez inOctober 2000 and the successive resignations of twoMinisters of Economy (José Luis Machinea and Ricardo López Murphy) within 20 days in March2001, with a devastating impact on market confi-dence at a critical stage. Political developments inthe later months of 2001, including the defeat of theruling coalition in congressional elections, also con-tributed to the perception that the government wouldnot be able to take the very difficult steps needed toresolve the crisis.

16

Box 1.3.The Politics of the Convertibility Regime

As with most major economic policy measures, theconvertibility regime had important political dimen-sions, including:

• With the early success of the Convertibility Plan,President Carlos Menem, who had been elected to asix-year term, decided to seek a second term bychanging the constitution. In January 1994, the twomain political parties agreed on a framework forconstitutional reform that would allow PresidentMenem to serve a second term of four years, withthe elections set for mid-1995. This led to politicaldeals with opposition, provincial, and labor leaders,which weakened commitment to fiscal disciplineand stalling—even rolling back in some cases—thepace of structural reforms. However, despite thepressure of the upcoming elections, the authoritieswere able to take decisive action on the fiscal andstructural fronts in response to the Mexican crisis inearly 1995.

• From early 1997, President Menem began to seeka third term, despite the constitutional injunction.His attempt was eventually not successful, but itcreated a prolonged period of political competi-tion in which Peronist leaders at the federal andprovincial levels tried to use public spending towin the nomination.

• Beset by bribery scandals, the Peronist party lost itsmajority in Congress after elections in October1997. This made it difficult for the executive to se-cure congressional approval for its fiscal and struc-tural policy agendas.

• In the presidential elections of 1999, the convert-ibility regime was so popular with the public thateven the main opposition Radical party ran on theplatform to maintain the fixed exchange rateregime. With the help of the FREPASO party, theRadical party won the elections and, on December10, 1999, the new coalition (Alianza) governmentof Fernando De La Rúa took office, with José LuisMachinea as Minister of Economy.

• There was some—though marginal— opposition tothe convertibility regime, because it was perceivedas a symbol of the economic dislocation and unem-ployment that accompanied the radical deregula-tion, liberalization, and privatization initiatives ofthe early 1990s. Once the vulnerabilities of the con-vertibility regime had become apparent after late1998, opposition became more vocal. During thepresidential elections of 1999, some major candi-dates made remarks suggesting the need for achange in the convertibility regime, but they failedto receive broad public support.

• The Alianza turned out to be fragile. In October2000, Vice President Carlos Álvarez resigned as aprotest over lack of action by the Cabinet on al-leged corruption charges. Lack of support withinthe coalition for strong fiscal adjustment led to theresignation of Minister Machinea on March 2, 2001and that of his successor Ricardo López Murphy inthe evening of March 19, the very day when he re-ceived public support from President De la Rúa andpresented his economic agenda to the Annual Meet-ings of the Inter-American Development Bank(IDB) in Santiago.

This chapter reviews the IMF’s prolonged in-volvement in Argentina from the introduction

of the convertibility regime in 1991 until the onset ofcrisis in late 2000. The purpose is to determine theextent to which IMF surveillance helped to identifythe vulnerabilities that led to the crisis and how ef-fectively the IMF used the program relationship withArgentina during much of the period to addressthese vulnerabilities. We focus on three areas of crit-ical relevance to the IMF: (i) exchange rate policy;(ii) fiscal policy; and (iii) macro-critical structuralreforms in the fiscal system, the labor market, the so-cial security system, and the financial system. Foreach of these areas, two sets of issues will be ad-dressed: first, whether the IMF’s diagnosis of whatneeded to be done at various stages was correct, andwhether it could have been improved; second, theIMF’s impact on the policies actually chosen, andwhat determined the strength or weakness of thatimpact.

Exchange Rate Policy

Argentina was one of the handful of countries thatmaintained a “hard peg” in the 1990s and early2000s (Box 2.1). It is well known that the sustain-ability of such an exchange rate regime critically de-pends on certain stringent conditions being fulfilled.One of the central issues in evaluating surveillanceand program design in this area during the precrisisphase is how the IMF perceived the convertibilityregime’s medium-term viability over time; how ef-fectively it advocated the requisite supporting poli-cies; and whether it provided timely advice on exitstrategy if and when supporting policies were judgedto be insufficient.

Early success of the convertibility regime

As pointed out in Chapter 1, the convertibilityregime, with a rigid peg to the U.S. dollar, was ini-tially adopted as an instrument of price stabilization,and this objective was achieved. The IMF was ini-tially reluctant to support the system (see Cavallo

and Cottani, 1997), and remained for some time con-cerned that it might not deliver the permanent stabi-lization that was needed. The staff report that accom-panied Argentina’s request for a new SBA in July1991 commented: “The convertibility scheme canassist the authorities in their search for a rapid decel-eration of inflation, but it is also evident that infla-tion must decline quickly and stay at very low levelsif the economy’s competitiveness is not to be im-paired. This in turn requires that the fiscal objectivesof the program be fully met.”

Because convertibility was initially viewed as astabilization device, little attention was paid towhether the arrangement was appropriate as a basisfor long-term growth. There was little analysis ofwhether the exchange rate regime was viable over themedium term, including the issue of whether theUnited States and Argentina formed an optimum cur-rency area in terms of synchronization of businesscycles, geographical trade structure, or common ex-posure to external shocks. Instead, attention was fo-cused on whether the fixed rate was overvalued at themoment the peg was introduced and whether the pegmight lead to a real appreciation in the near future.

Once the economy had stabilized and started togrow, the focus of the IMF shifted to the risk of over-heating. Partly because the rate of inflation initiallyremained higher than that in the United States, theArgentine currency appreciated in real effectiveterms by over 50 percent from March 1991 through1993 (Figure 2.1). Concerns were expressed over thecurrent account deficit, which widened to 3 percentof GDP in 1992 (Figure 2.2). Internal staff docu-ments occasionally expressed concern that the deteri-orating current account might undermine the sustain-ability of the exchange rate regime and suggestedthat fiscal policy be moved toward surplus and re-serve requirements on banks be tightened. The au-thorities generally disagreed with this assessment,though the fiscal balance improved in 1992–93 andreserve requirements were tightened somewhat inAugust 1993.

The worries over the current account deficit sub-sided in early 1994, as inflation continued to fall andthe real effective exchange rate (REER) began to de-

17

CHAPTER

2 Surveillance and ProgramDesign, 1991–2000

CHAPTER 2 • SURVEILLANCE AND PROGRAM DESIGN, 1991–2000

preciate, reflecting the U.S. dollar’s depreciationagainst Argentina’s main trading partners. The staff,while still advocating fiscal adjustment, no longerexpressed strong concerns over the sustainability ofthe exchange rate regime. In retrospect, this mighthave been an opportune time to exit the peg, al-though the memory of hyperinflation was still freshand argued against such a possibility at that time.Some Board members did raise the issue, but thestaff hardly discussed it with the authorities and ap-pears to have accepted their view that a significant