25 CHAPTER - 2 PROFILE OF INTERNATIONAL MONETARY FUND (IMF) 2 . 1 INTRODUCTION This second Chapter of the Thesis presents the profile of the International Monetary Fund (IMF) as in 2006 AD. Having come into being in 1944, in the post-World War-II devastated world, with just 44 member countries, the IMF in 2007 had 185 member countries, bailed so many countries out of the balance of payment crises (including India), trained an army of financial bureaucrats worldwide in detecting the looming crises and avoiding them, and done so many other things for maintaining international liquidity and international financial flows from one country to another, and has done remarkable work in helping highly indebted poor countries to bring about their dilapidated economies to the world level. The IMF’s celebrated motto is “Making the Global Economy Work for All”. The following pages present a brief profile of the IMF, the organization whose performance is being studied under this work. 2. 2 HOW THE IMF IS RUN The highest decision-making body of the IMF is the Board of Governors, which is appointed by the member countries. Some of the Board of Governor’s powers are delegated to the Fund’s Executive Board, which is composed of 24 Executive Directors, who are appointed or elected by the member countries. The Board of Governors consists of one governor and one alternate governor from each of the IMF’s 185 member countries. The governor is usually the member country’s minister of finance or the head of its central bank. All governors meet once a year at the IMF-World Bank Annual Meetings. There are two committees of governors that represent the whole membership. The International Monetary and Financial Committee (IMFC) is an advisory body composed of 24 IMF governors (or their alternates) representing the same countries or constituencies (groups of countries) as the 24 Executive Directors. The IMFC normally meets twice a year, in March or April and at the time of the Annual Meetings in September or October. Its responsibilities include providing guidance to the Executive Board and advising and reporting to the Board of Governors on issues related to the management of the international monetary system. The current Chairman of the IMFC was Gordon Brown, the then Chancellor of the Exchequer of United Kingdom. The Development

Transcript

25

CHAPTER - 2

PROFILE OF INTERNATIONAL MONETARY FUND (IMF)

2 . 1 INTRODUCTION

This second Chapter of the Thesis presents the profile of the International Monetary

Fund (IMF) as in 2006 AD.

Having come into being in 1944, in the post-World War-II devastated world,

with just 44 member countries, the IMF in 2007 had 185 member countries, bailed so

many countries out of the balance of payment crises (including India), trained an army of

financial bureaucrats worldwide in detecting the looming crises and avoiding them, and

done so many other things for maintaining international liquidity and international financial

flows from one country to another, and has done remarkable work in helping highly

indebted poor countries to bring about their dilapidated economies to the world level.

The IMF’s celebrated motto is “Making the Global Economy Work for All”.

The following pages present a brief profile of the IMF, the organization whose

performance is being studied under this work.

2. 2 HOW THE IMF IS RUN

The highest decision-making body of the IMF is the Board of Governors, which is

appointed by the member countries. Some of the Board of Governor’s powers are

delegated to the Fund’s Executive Board, which is composed of 24 Executive Directors,

who are appointed or elected by the member countries.

The Board of Governors consists of one governor and one alternate governor

from each of the IMF’s 185 member countries. The governor is usually the member

country’s minister of finance or the head of its central bank. All governors meet once a

year at the IMF-World Bank Annual Meetings.

There are two committees of governors that represent the whole membership.

The International Monetary and Financial Committee (IMFC) is an advisory body

composed of 24 IMF governors (or their alternates) representing the same countries or

constituencies (groups of countries) as the 24 Executive Directors. The IMFC normally

meets twice a year, in March or April and at the time of the Annual Meetings in September

or October. Its responsibilities include providing guidance to the Executive Board and

advising and reporting to the Board of Governors on issues related to the management

of the international monetary system. The current Chairman of the IMFC was Gordon

Brown, the then Chancellor of the Exchequer of United Kingdom. The Development

26

Committee (formally, the Joint Ministerial Committee of the Boards of Governors of the

World Bank and the IMF on the Transfer of Real Resources to Developing Countries) is

a joint World Bank-IMF body composed of 24 World Bank or IMF governors or their

alternates. The Committee serves as a forum that helps build intergovernmental consensus

on development issues. It also normally meets twice a year, following the IMFC meetings.

Both committees summarize their meetings in communiqués, which are published on the

IMF’s Web site and in its Annual Reports.

Executive Board Standing Committees

In 2007 AD, there were 10 Standing Committees on which Executive Directors

served:

1. The Committee on Administrative Policies considers and makes recommenda-

tions to the Executive Board on matters of administrative policy requiring

action by the Board that are referred to it by the Chairman, the Board, or

individual Executive Directors.

2. The Committee on the Budget considers the Managing Director’s budget

proposals and other material circulated by the Managing Director regarding

the Fund’s administrative and capital budgets. It makes its views on the

budget proposals known to the Executive Board and meets as needed to

consider budget implementation.

3. The Committee on Executive Board Administrative Matters considers and

reports to the Executive Board on aspects of administrative policy relating

to the Executive Directors and their Alternates or senior advisors, advisors,

and assistants referred to it by the Executive Board or by an Executive

Director.

4. The Agenda and Procedures Committee contributes to the development and

smooth implementation of the Executive Board’s work program.

5. The Committee on Liaison with the World Trade Organization considers

and makes recommendations to the Executive Board on issues that arise

concerning the Fund’s relationship with the WTO or in connection with

matters of common interest to the Fund and the WTO.

6. The Evaluation Committee follows closely the evaluation function in the Fund

and advises the Executive Board on matters relating to evaluations.

7. The Committee on Interpretation considers and makes reports and recommen-

dations to the Executive Board on questions of interpretation. Legal

questions are sent to the Committee by the Executive Board at the request

of an Executive Director.

8. The Pension Committee decides matters of a general policy nature arising under

the Staff Retirement Plan.

27

World (Political) : IMF’s Domain

Source: Readers’ Digest Association Limited (RDAL): 2002 :

“Countries of the World”, New York: RDAL, p.7.

28

29

30

31

32

33

9. The Ethics Committee considers matters relating to the Code of Conduct for

IMF staff and may also provide guidance to Executive Directors, at their

request, on ethical aspects of the conduct of their Alternates, advisors,

and assistants.

10. The Committee on the Annual Report reviews and makes recommendations to

the Executive Board on the format and content of the Fund’s Annual Report

in line with the provisions of the Fund’s Articles of Agreement and By-

Laws, as well as with the Fund’s commitment to transparency and role in

the international monetary system. The Committee aims to ensure that

the Annual Report helps promote the Fund’s accountability.

The Board Standing Committees are reconstituted by decisions of the Executive

Board following the regular election every two years of Executive Directors, on the

basis of a proposal by the Managing Director following consultation with the Dean of

the Board. Several long-standing principles have guided the proposals for constituting

the membership of Board committees: the desirability of a reasonable geographical balance

in the composition of each committee; a need for rotation, with some continuity; and

maintenance of a reasonable distribution of the burden of committee work among

Executive Directors. There are formal requirements for some committees concerning

the number of members. In addition, account is taken, to the extent possible, of the

preferences of individual Executive Directors.

Executive Directors hold the chairmanship of all but three Board committees,

namely, the Committee on Administrative Policies, the Committee on the Budget, and

the Pension Committee, which are chaired by the Managing Director or one of his

representatives. The Secretary of the Fund, or his representative, serves as the Secretary

of every Committee except the Ethics Committee. Executive Directors may participate

in all regular meetings of the Executive Board’s committees.

The day-to-day work of the IMF is conducted at its Washington, D.C.,

headquarters by its Executive Board; this work is guided by the IMFC and supported by

the IMF’s staff. The Managing Director is Chair of the Executive Board and head of the

IMF staff; he is assisted by a First Deputy Managing Director and two other Deputy

Managing Directors. The Executive Board has a central role in policy formulation and

decision making in the IMF, and exercises all the powers for conducting the institution’s

business, except those that the Articles of Agreement reserve for the Board of Governors

or the Managing Director. The Board meets in “continuous session, ” that is, as often as

the business at hand requires, usually for three full days each week.

In calendar year 2005, total Board meeting time amounted to about 462 hours.

The Board held 266 formal meetings (including those in which decisions were made), 10

informal seminars, and 92 other informal meetings, including committee meetings. It

spent 42 percent of its time on member country matters (mainly Article IV consultations

and reviews and approvals of IMF financing arrangements); 28 percent of its time on

global and regional surveillance and general policy issues (such as the World Economic

Outlook, Global Financial Stability Report, IMF financial resources, the international

34

Table 2.1

Executive Directors of IMF and their Voting Powers (as of April 30, 2007)

Director Votes by Total Percent of

Alternate Casting Votes of country votes1 total2

Appointed

Meg Lundsager United States 371,743 371,743 16.83

Vacant

Shigeo Kashiwagi Japan 133,378 133,378 6.04

Michio Kitahara

Klaus D.Stein Germany 130,332 130,332 5.90

Stephan von Stenglin

PierreD uquesne France 107,635 107,635 4.87

Bertrand Dumont

Tom Scholar United Kingdom 107,635 107,635 4.87

Jens Larsen

Elected

Willy Kiekens Austria 18,973

(Belgium) Belarus 4,114

Johann Prader Belgium 46,302

(Austria) Czech Republic 8,443

Hungary 10,634

Kazakhstan 3,907

Luxembourg 3,041

Slovak Republic 3,825

Slovenia 2,567

Turkey 12,163 113,969 5.16

Jeroen Kremers Armenia 1,170

(Netherlands) Bosnia and Herzegovina 1,941

Yuriy G. Yakusha Bulgaria 6,652

(Ukraine) Croatia 3,901

Cyprus 1,646

Georgia 1,753

Israel 9,532

Macedonia 939

Moldova 1,482

Netherlands 51,874

Romania 10,552

Ukraine 13,970 105,412 4.77

Roberto Guarnieri Costa Rica 1,891

(República Bolivariana El Salvador 1,963

de Venezuela) Guatemala 2,352

Ramón Guzmán Honduras 1,545

(Spain) Mexico 26,108

Nicaragua 2,550

Spain 30,739

Venezuela 26,841 92,989 4.21

35

Arrigo adun Albania 737

(Italy) Greece 8,480

Miranda Xafa Italy 70,805

(Greece) Malta 1,270

Portugal 8,924

San Marino 420

Timor-Leste 432 90,968 4.12

Richard Murray Australia 32,614

(Australia) Kiribati 306

Wilhemina C.Mañalac Korea 16,586

(Philippines) Marshall Islands 285

Micronesia 301

Mongolia 761

New Zealand 9,196

Palau 281

Papua New Guinea 1,566

Philippines 9,049

Samoa 366

Seychelles 338

Solomon Islands 354

Vanuatu 420 85,360 3.86

GE Huayong China 81,151 81,151 3.67

(China)

HE Jianxiong

(China)

Jonathan Fried Antigua and Barbuda 385

(Canada) Bahamas,The 1,553

Peter Charleton Barbados 925

(Ireland) Belize 438

Canada 63,942

Dominica 332

Grenada 367

Ireland 8,634

Jamaica 2,985

St.Kitts and Nevis 339

St.Lucia 403

St.Vincent & Grenadines 333 80,636 3.65

Tuomas Saarenheimo Denmark 16,678

(Finland) Estonia 902

Jon T. Sigurgeirsson Finland 12,888

(Iceland) Iceland 1,426

Table 2.1 (contd.)

Director Votes by Total Percent of

Alternate Casting Votes of country votes1 total2

36

Latvia 1,518

Lithuania 1,692

Norway 16,967

Sweden 24,205 76,276 3.51

Jong Nam Oh Australia 32,614

(Korea) Kiribati 306

Richard Murray Korea 16,586

(Australia) Marshall Islands 285

Micronesia 301

Mongolia 761

New Zealand 9,196

Palau 281

Papua New Guinea 1,566

Philippines 9,049

Samoa 366

Seychelles 338

Solomon Islands 354

Vanuatu 420 72,423 3.33

A.Shakour Shaalan Bahrain 1,600

(Egypt) Egypt 9,687

Samir El-Khouri Iraq 12,134

(Lebanon) Jordan 1,955

Kuwait 14,061

Lebanon 2,280

Libyan Arab Jamahiriya 11,487

Maldives 332

Oman 2,190

Qatar 2,888

Syrian Arab Republic 3,186

United Arab Emirates 6,367

Yemen,Republic of 2,685 70,852 3.26

Sulaiman M.Al-Turki Saudi Arabia 70,105 70,105 3.22

(Saudi Arabia)

Abdallah S.Alazzaz

(Saudi Arabia)

Hooi Eng Phang Brunei Darussalam 2,402

(Malaysia) Cambodia 1,125

Made Sukada Fiji 953

(Indonesia) Indonesia 21,043

Lao People ’s Demo.Republic 779

Malaysia 15,116

Myanmar 2,834

Table 2.1 (contd.)

Director Votes by Total Percent of

Alternate Casting Votes of country votes1 total2

37

Nepal 963

Singapore 8,875

Thailand 11,069

Tonga 319

Vietnam 3,541 69,019 3.17

Peter J.Ngumbullu Angola 3,113

(Tanzania) Botswana 880

Peter Gakunu Burundi 1,020

(Kenya) Eritrea 409

Ethiopia 1,587

Gambia,The 561

Kenya 2,964

Lesotho 599

Malawi 944

Mozambique 1,386

Namibia 1,615

Nigeria 17,782

Sierra Leone 1,287

South Africa 18,935

Sudan 1,947

Swaziland 757

Tanzania 2,239

Uganda 2,055

Zambia 5,141 65,221 3.00

WANG Xiaoyi China 63,942 63,942 2.94

(China)

GE Huayong

(China)

Fritz Zurbrügg Azerbaijan 1,859

(Switzerland) Kyrgyz Republic 1,138

Andrzej Raczko Poland 13,940

(Poland) Serbia and Montenegro 4,927

Switzerland 34,835

Tajikistan 1,120

Turkmenistan 1,002

Uzbekistan 3,006 61,827 2.84

Aleksei V.Mozhin Russian Federation 59,704 59,704 2.74

(Russian Federation)

Andrei Lushin

(Russian Federation)

Table 2.1 (contd.)

Director Votes by Total Percent of

Alternate Casting Votes of country votes1 total2

38

Abbas Mirakhor Afghanistan,Islamic Republic of 1,869

(Islamic Republic of Iran)Algeria 12,797

Mohammed Daïri Ghana 3,940

(Morocco) Iran,Islamic Republic of 15,222

Morocco 6,132

Pakistan 10,587

Tunisia 3,115 53,662 2.47

Eduardo Loyo Brazil 30,611

(Brazil) Colombia 7,990

Roberto Steiner Dominican Republic 2,439

(Colombia) Ecuador 3,273

Guyana 1,159

Haiti 1,069

Panama 2,316

Suriname 1,171

Trinidad and Tobago 3,606 53,634 2.46

B.P.Misra Bangladesh 5,583

(India) Bhutan 313

Amal Uthum Herat India 41,832

(Sri Lanka) Sri Lanka 4,384 52,112 2.39

Héctor R.Torres Argentina 21,421

(Argentina) Bolivia 1,965

Javier Silva-Ruete Chile 8,811

(Peru) Paraguay 1,249

Peru 6,634

Uruguay 3,315 43,395 1.99

Damian Ondo Mañe Benin 869

(Equatorial Guinea) Burkina Faso 852

Laurean W.Rutayisire Cameroon 2,107

(Rwanda) Cape Verde 346

Central African Republic 807

Chad 810

Comoros 339

Congo,Democratic 5,580

Congo,Republic of 1,096

Côte d ’Ivoire 3,502

Djibouti 409

Equatorial Guinea 576

Gabon 1,793

Guinea 1,321

Guinea-Bissau 392

Table 2.1 (contd.)

Director Votes by Total Percent of

Alternate Casting Votes of country votes1 total2

39

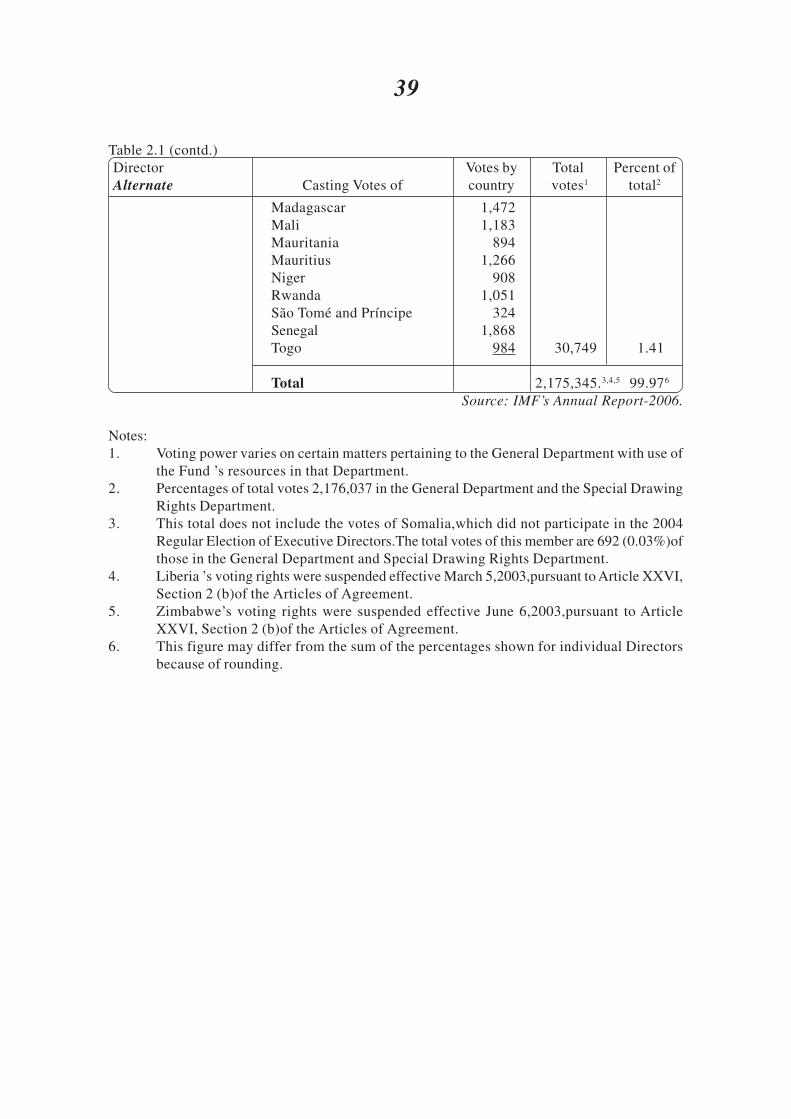

Madagascar 1,472

Mali 1,183

Mauritania 894

Mauritius 1,266

Niger 908

Rwanda 1,051

São Tomé and Príncipe 324

Senegal 1,868

Togo 984 30,749 1.41

Total 2,175,345.3,4,5 99.976

Source: IMF’s Annual Report-2006.

Notes:

1. Voting power varies on certain matters pertaining to the General Department with use of

the Fund ’s resources in that Department.

2. Percentages of total votes 2,176,037 in the General Department and the Special Drawing

Rights Department.

3. This total does not include the votes of Somalia,which did not participate in the 2004

Regular Election of Executive Directors.The total votes of this member are 692 (0.03%)of

those in the General Department and Special Drawing Rights Department.

4. Liberia ’s voting rights were suspended effective March 5,2003,pursuant to Article XXVI,

Section 2 (b)of the Articles of Agreement.

5. Zimbabwe’s voting rights were suspended effective June 6,2003,pursuant to Article

XXVI, Section 2 (b)of the Articles of Agreement.

6. This figure may differ from the sum of the percentages shown for individual Directors

because of rounding.

Table 2.1 (contd.)

Director Votes by Total Percent of

Alternate Casting Votes of country votes1 total2

40

financial system, the debt situation, low-income countries, and issues related to IMF

lending facilities and program design); and the remaining time on committees and

administrative and other matters.

2.3 IMF’S ORGANIZATION

The IMF staff is organized mainly into departments with regional (or area), functional,

information and liaison, and support responsibilities. These departments are headed by

directors who report to the Managing Director. The IMF’s organization chart appears

on the next page.

2.3.1 Area Departments

The five area departments - African, Asia and Pacific, European, Middle East

and Central Asia , and Western Hemisphere - advise management and the Executive

Board on economic developments and policies in countries in their regions. Their staff is

also responsible for putting together financial arrangements to support members’

economic reform programs and for reviewing performance under these IMF-supported

programs. Together with relevant functional departments, they provide member countries

with policy advice and technical assistance, and maintain contact with regional

organizations and multilateral institutions in their geographic areas. Supplemented by

staff in functional departments, area departments carry out much of the IMF’s country

surveillance work through direct contact with member countries. In addition, 87 area

department staff are assigned to members as IMF resident representatives.

2.3.2 Resident Representatives

At the end of April 2006, the IMF had 87 resident representative positions covering

92 member countries in Africa, Asia, Europe, the Middle East, and the Western Hemi-

sphere. New offices were opened in Burundi,Liberia,Paraguay,the Republic of Congo,

Sierra Leone, and Sudan. These posts, usually filled by one IMF employee supported by

local staff, enhance IMF policy advice and are often set up in conjunction with a reform

program. The representatives, who typically have good access to key national

policymakers, can bring major benefits to the quality of IMF country work.In particular,

through their professional expertise and deeper familiarity with local conditions, resident

representatives contribute to the formulation of IMF policy advice, monitor performance,

especially under IMF-supported programs, and coordinate technical assistance. They

can also alert the IMF and the host country to potential policy slippages, provide on-site

program support,and play an active role in IMF outreach in member countries. Since the

advent of enhanced initiatives for low-income countries, resident representatives have

helped members develop their Poverty Reduction Strategies by taking part in country-

led discussions on the strategy and by presenting IMF perspectives. They also support

monitoring of program implementation and institution building, working with different

branches of government, civil society organizations,donors, and other stakeholders.

2.3.3 Functional and Special Services Departments

The Finance Department is responsible for mobilizing, managing, and

safeguarding the IMF’s financial resources to ensure that they are deployed in a manner

41

consistent with the Fund’s mandate. This entails major responsibilities for the institution’s

financial policies and for the conduct, accounting, and control of all financial transactions.

In addition, the department helps safeguard the IMF’s financial position by assessing the

adequacy of the Fund’s capital base (quotas), net income targets, precautionary balances,

and the rates of charge and remuneration. Other responsibilities include investing funds

in support of assistance to low-income countries and conducting assessments of financial

control systems in borrowing members ’ central banks.

The Fiscal Affairs Department is responsible for activities involving public finance

in member countries. It participates in area department missions, particularly with respect

to the analysis of fiscal issues; reviews the fiscal content of IMF policy advice, including

in the context of IMF-supported adjustment programs; helps countries draw up and

implement fiscal programs; and provides technical assistance in public finance. It also

conducts research and policy studies on fiscal issues, including tax policy and revenue

administration, as well as on income distribution and poverty, social safety nets, public

expenditure policy issues, and the environment.

As part of the IMF’s efforts under the Medium-Term Strategy to strengthen its

work on financial surveillance, the International Capital Markets Department is being

merged with the Monetary and Financial Systems Department early in FY 2007. During

FY 2006, the department assisted the Executive Board and management in overseeing

the international monetary and financial system and enhanced the IMF’s crisis prevention

and crisis management activities. It also prepared the semiannual Global Financial

Stability Report, assessing developments in international capital markets. Staff members

liaised with private capital market participants, national authorities, and official forums

dealing with the international financial system. In addition, the department played a

leading role in the IMF’s analytical work and advice to members on access to international

capital markets and on strategies for external debt management.

The IMF Institute provides training for officials of member countries, particularly

developing countries, in such areas as financial programming and policy, external sector

policies, balance of payments methodology, national accounts and government finance

statistics, and public finance. The Institute also conducts an active program of courses

and seminars in economics, finance, and econometrics for IMF economists.

The Legal Department advises management, the Executive Board, and the staff

on the applicable rules of law. It prepares most of the decisions and other legal instruments

necessary for the IMF’s activities. The department serves as counsel to the IMF in

litigation and arbitration cases, provides technical assistance on legislative reform,

assesses the consistency of laws and regulations with selected international standards

and codes, responds to inquiries from national authorities and international organizations

on the laws of the IMF, and arrives at legal findings regarding IMF jurisdiction on exchange

measures and restrictions.

As mentioned above, the Monetary and Financial Systems Department and the

International Capital Markets Department are being merged in early FY 2007 to

strengthen the IMF’s work on financial surveillance. During FY 2006, the department

42

engaged in four operational areas, financial system surveillance (including the Financial

Sector Assessment Program and Article IV consultations), banking supervision and crisis

resolution, monetary and exchange rate infrastructure and operations, and technical

assistance. It provided analytical, operational, and technical support to member countries

and area departments, including development and dissemination of good policies and

best practices. An important role was coordinating with collaborating central banks,

supervisory agencies, and other international organizations.

The Policy Development and Review Department (PDR) plays a central role in

the design and implementation of the IMF’s policies related to surveillance and the use

of the IMF’s financial resources. Through its review of country and policy work, PDR

seeks to ensure the consistent application of IMF policies throughout the institution. In

recent years, the department has spearheaded the IMF’s work in strengthening the

international financial system, streamlining and focusing conditionality, and developing

the Poverty Reduction and Growth Facility (PRGF) and the Heavily Indebted Poor

Countries (HIPC) Initiative. PDR economists participate in country missions with area

department staff, typically covering 80-90 countries a year, and assist member countries

that are making use of IMF resources to mobilize other financial resources.

The Research Department conducts policy analysis and research in areas relating

to the IMF’s work. The department plays a prominent role in global surveillance and in

developing IMF policy concerning the international monetary system. It cooperates with

other departments in formulating IMF policy advice to member countries. It coordinates

the semiannual World Economic Outlook exercise and prepares analysis for the

surveillance discussions of the Group of Seven, the Group of Twenty, and such regional

groupings as the Asia Pacific Economic Cooperation (APEC) forum, and the Executive

Board’s discussions of world economic and market developments. The department also

maintains contacts with the academic community and with other research organizations.

The Statistics Department maintains databases of country, regional, and global

economic and financial statistics, and reviews country data in support of the IMF’s

surveillance role. It is also responsible for developing statistical concepts in external

sector, government finance, and monetary and financial statistics, as well as for producing

methodological manuals. The department provides technical assistance and training to

help members develop statistical systems and produces the IMF’s statistical publications.

In addition, it is responsible for developing and maintaining standards for the dissemination

of data by member countries.

2.3.4 Information and Liaison

The External Relations Department works to promote public understanding of

and support for the IMF and its policies. It aims to make the IMF’s policies understandable

through many activities aimed at transparency, communication, and engagement with a

wide range of stakeholders. It prepares, edits, and distributes most IMF publications

and other material, promotes contacts with the press and other external groups, such as

civil society organizations and parliamentarians, and manages the IMF’s Web site.

43

The IMF’s offices in Asia and Europe and at the United Nations maintain close

contacts with other international and regional institutions. The UN Office also makes a

substantive contribution to the Financing for Development process, while the offices in

Asia and Europe contribute to bilateral and regional surveillance and are a major part of

the IMF’s outreach effort.

2.3.5 Support Services

The Human Resources Department helps ensure that the IMF has the right mix

of staff skills, experience, and diversity to meet the changing needs of the organization,

and that human resources are managed, organized, and deployed in a manner that

maximizes their effectiveness, moderates costs, and keeps the workload and stress at

acceptable levels. The department develops policies and procedures that help the IMF

achieve its work objectives, manages compensation and benefits, recruitment, and career

planning programs, and supports organizational effectiveness by assisting departments

with their human resource-management goals.

The Secretary’s Department organizes and reports on the activities of the IMF’s

governing bodies and provides secretariat services to them, as well as to the Group of

Twenty-four. In particular, it assists management in preparing and coordinating the work

programme of the Executive Board and other official bodies, including by scheduling

and helping ensure the effective conduct of Board meetings. In carrying out these tasks,

the department helps promote open and efficient channels of communication between

the governing bodies, management, and staff. The department, in cooperation with its

counterpart office in the World Bank, also organizes the arrangements for the Annual

Meetings.

The Technology and General Services Department manages and delivers services

essential for the IMF’s operation. These include information services (information

technology, library services, multimedia services, records and archives management,

and telecommunications); facilities services (building projects and facilities management);

general administrative services (travel management, conference and catering services,

and procurement services); language services (translation, interpretation, and preparation

of publications in languages other than English); and a broad range of security and business

continuity services (covering headquarters security, field security, and information

technology security).

The IMF also has offices responsible for internal auditing and review of work

practices, budget matters, technical assistance, and investments under the staff retirement

plan.

2.3.6 Office of Internal Audit and Inspection

The Office of Internal Audit and Inspection (OIA) contributes to the internal

governance of the IMF by providing independent examinations of the effectiveness of

the risk management, control, and governance processes of the IMF. To meet this

objective, OIA conducts about 25 audits and reviews per year. These audits and reviews

include examining the adequacy of controls and procedures to safeguard and administer

44

Fund assets and financial accounts, assessing the efficiency and effectiveness with which

internal resources are being used, evaluating the adequacy of the management of

information technology, and ensuring that adequate physical and information security

measures are in place. Under its multi-year program of reviews, OIA subjects IMF

departments to comprehensive reviews that assess whether their activities are aligned

with the overall goals of the Fund, whether resources dedicated to low-priority activities

can be reallocated, and whether the work is conducted in an efficient and effective fashion.

In line with best practices, OIA reports to IMF management and to the External

Audit Committee, thus assuring its independence. In addition, the Executive Board is

briefed annually on OIA’s work program and the major findings of its audits and reviews.

2.3.7 Independent Evaluation Office

The Independent Evaluation Office (IEO) was established in 2001 with a view

to increasing transparency and accountability and strengthening the learning culture of

the IMF. The IEO is independent of IMF management and staff and operates at arm’s

length from the Executive Board, to which it reports on its findings.

During FY 2006, the IEO completed three evaluations: the Financial Sector

Assessment Program, multilateral surveillance, and IMF support to Jordan in 1989-2004.

A fourth evaluation, on the IMF’s advice on capital account liberalization, was completed

in FY 2005 but discussed by the IMF’s Executive Board in FY 2006. Formal outreach

seminars were held in Asia, Europe, and the Middle East. Currently ongoing evaluations

relate to structural conditionality in IMF-supported programs, the IMF’s role in the

determination of the external resource envelope in sub-Saharan African countries, and

the IMF’s advice on exchange rate policy.

To help prepare additions to its work program in FY 2007, the IEO has published

a broad list of possible topics for evaluation over the medium term, reflecting the many

suggestions received from outside stakeholders as well as IMF Executive Directors,

management, and staff.

2.3.8 External Evaluation of the IEO

The IEO itself underwent an external evaluation in early 2006. The resulting

report confirmed that the IEO is an important part of good governance at the IMF, and

made several recommendations to further strengthen the work of the office.

In April 2006, the IMF Executive Directors met to discuss the report on the IEO

prepared by an External Evaluation Panel. It was agreed that the IEO had served the

IMF well and earned strong support across a broad range of stakeholders. It was also

agreed that the IMF continued to need an independent evaluation office to contribute to

the institution’s learning culture and facilitate oversight and governance by the Executive

Board. In this connection, the Panel’s observation that the IEO had acted independently

was welcomed.

The weaknesses highlighted in the report were noted and welcomed the analysis

and recommendations for further strengthening the IEO’s effectiveness. In particular,

45

Directors concurred that a more focused and strategic orientation, together with strong

support from the Board and management, would help ensure the IEO’s continued

usefulness and relevance.

To maintain the high quality of IEO reports, Directors called for them to be

shorter, with more focused assessments and recommendations. Many Directors

emphasized that IEO reports should look beyond process to substance, including

judgments on the theoretical foundations and analytical frameworks underlying the Fund’s

advice. Directors generally agreed with the Panel’s recommendation that IEO outreach

activities should be intensified.

Directors generally welcomed the Panel’s suggestions for strengthening follow-

up to the IEO’s recommendations, including more Board involvement. They considered

that the Panel’s call for a more systematic approach for following up on and monitoring

the implementation of IEO recommendations approved by the Board should be further

examined. The IEO had also been taking lead in reviewing its existing publications

policy to ensure that it reflected evolving best practice. Changes in the IEO’s publications

policy were consistent with ensuring its independence.

2.4 TRANSPARENCY POLICY OF THE IMF

The IMF’s transparency policy stems from an Executive Board decision in January 2001

to allow the voluntary publication of country documents and systematic publication of

policy papers and associated Public Information Notices (PINs). The decision followed

steps that had been taken since 1994 to enhance the transparency of the IMF and to

increase the availability of information about its members’ policies. It also defined the

key elements of the IMF’s publication policy, including safeguards to maintain the

frankness of the Fund’s policy discussions with members by striking the right balance

between transparency and confidentiality. Under these safeguards,which were revisited

in the June 2005 review of transparency, members may request deletions of information

not already in the public domain that constitutes either highly market-sensitive material

or premature disclosure of policy intentions.

Disseminating Information : IMF’s Publications and Website

The IMF publishes a wide variety of material targeted at a broad range of

readerships. Many of the Fund’s publications are available both in print and on its Web

site (www. imf. org). The World Economic Outlook (WEO) and the Global Financial

Stability Report (GFSR) are the main vehicles through which the IMF publicizes its

global surveillance findings and some of its most significant analytical work.

Ø The IMF releases a large number of reports and other country documents covering

economic and financial developments and trends in member countries. Each

report, based on the staff’s analytical work and meetings with country officials,

is prepared independently by a staff team and published at the option of the

members. This series includes Article IV Reports, Reports Related to Use of

IMF Resources, Selected Issues papers, and Statistical Appendices. In almost

all cases, Executive Board discussions on these papers are summarized in

46

Public Information Notices (PINS), which are available on IMF’s Website.

Ø The IMF’s Annual Report provides a comprehensive look at the IMF’s activities

in each financial year and is designed to be used as a reference tool.

Ø The Annual Report on Exchange Arrangements and Exchange Restrictions

presents information on the exchange and trade systems of the IMF’s member

countries in a tabular format.

Ø Staff research on the international monetary system and other topical subjects is

published in IMF Staff Papers, a quarterly journal; the quarterly newsletter

IMF Research Bulletin; the IMF Working Papers series; the Occasional Papers

series; books; and various other publications.

Ø The Fund’s Dissemination Standards Bulletin Board on its Internet Website

provides links to the data and statistical Web sites of subscribers to the Special

Data Dissemination Standard (SDDS) and partici-pants in the General Data

Dissemination System (GDDS) and presents comprehensive information on

the methods and practices behind the compilation and dissemination of such

data in a user-friendly format comparable across countries.

Ø International Financial Statistics (IFS), produced monthly, provides updated

financial information from countries around the world; the IMF’s Statistics

Department also produces a yearbook containing annual data over 12 years

for the countries covered in the monthly publication. The IFS database is

available online to subscribers. Other statistical publications include the

Balance of Payments Statistics Yearbook, Government Finance Statistics

Yearbook, and Direction of Trade Statistics (quarterly, yearbook, and CD-

ROM issues).

Ø Guides and manuals published by the Fund cover a variety of subjects, such as

balance of payments statistics and compilation, external debt statistics, foreign

direct investment trends, monetary and financial statistics, the producer price

index, and financial soundness indicators.

Ø The biweekly newsletter IMF Survey reports on current IMF policies and activities,

and its annual companion, IMF In Focus, offers a clear, concise picture of

IMF policies and operations.

Ø Pamphlets such as What Is the IMF? and IMF Technical Assistance are written

for the nonspecialist, as are factsheets and issues briefs posted on the IMF’s

Web site, which aim to explain key aspects of IMF operations and policies.

Ø The quarterly magazine Finance and Development (F&D) and the Economic Issues

series (pamphlets on broad economic subjects related to the Fund’s areas of

expertise) are written in nontechnical language and aimed at disseminating

information on topical subjects to nonspecialists.

47

Ø An on-line, quarterly Civil Society Newsletter covers IMF activities and issues

of particular interest to civil society organizations.

Ø Videos about the work of the IMF are available to interested media, educational

institutions, and social organizations, and are also used in recruitment activities.

Ø Educational material is available from the IMF Center and at www. imf. org/

econed. The IMF Center hosts a permanent exhibition on the international

monetary system, offers book and economic forums and tours of the institution,

and includes a bookstore and giftshop. The IMF Center is open to the general

public daily, from Monday to Friday.

Ø Selected Fund publications are also available in languages other than English.

Communications and Outreach

The IMF communicates with the public at large and a wide range of more specific

nonofficial audiences. These communications activities are led by the IMFC management

and External Relations Department (EXR). But, in recent years, staff throughout the

organization, together with Executive Directors, have increasingly recognized the need

for and value of communication with external audiences as an integral component of the

Fund’s operational work. The relative strength of economic and financial systems during

FY 2006 meant that the Fund was able to focus its communications on a few strategically

important issues and, at the same time, to extend its outreach activities to selected non-

official audiences, especially parliamentary organizations.

2.5 AN OVERVIEW OF IMF’S FUNCTIONING

The following itemized text offers an overview of the IMF’s functioning in a typical

year.

2.5.1 Purpose and Organization

The IMF is an international organization of 185 member countries. It was

established to promote international monetary cooperation and exchange stability and

to maintain orderly exchange arrangements among members; to facilitate the expansion

and balanced growth of international trade, and contribute thereby to the promotion and

maintenance of high levels of employment; and to provide temporary financial assistance

to member countries under adequate safeguards to assist in solving their balance of

payments problems in a manner consistent with the provisions of the IMF’s Articles of

Agreement.

The IMF conducts its operations and transactions through the General Department

and the Special Drawing Rights Department (the SDR Department). The General

Department consists of the General Resources Account (GRA), the Special Disbursement

Account (SDA), including the Multilateral Debt Relief Initiative-I Trust (MDRI-I Trust),

over which the SDA has substantial control, and the Investment Account.

The IMF also administers trusts and accounts established to perform financial

and technical services and financial operations consistent with the purposes of the IMF.

48

The resources of these trusts and accounts are contributed by members or the IMF

through the SDA. With the exception of the MDRI-I Trust, whose financial statements

are consolidated with those of the General Department, the financial statements of the

SDR Department and these trusts and accounts are presented separately.

General Resources Account

The GRA holds the general resources of the IMF. Its resources reflect the payment

of quota subscriptions, use and repayment of IMF credit, collection of charges on the

use of credit, payment of remuneration on creditor positions, borrowings, and payment

of interest and repayment of borrowings.

Special Disbursement Account

The assets and resources of the SDA are held separately from the GRA and the

Investment Account of the General Department. The SDA is the vehicle for receiving

and investing profits from the sale of the IMF’s gold and for making transfers to other

accounts for special purposes authorized in the Articles, in particular for financial

assistance on special terms to low-income members of the IMF. Resources of the SDA

included proceeds from the sales of the IMF’s gold in the past, including income from

the investment of gold profits.

The SDA holds claims receivable from outstanding loans extended under the

Structural Adjustment Facility (SAF), and repayments of Trust Fund loans to the Trust

Fund (in liquidation) are transferred to the SDA Repayments of principal and interest

from SAF loans and resources derived from the termination of the Trust Fund are

transferred from the SDA to the Reserve Account of the Poverty Reduction and Growth

Facility and Exogenous Shocks Facility Trust (PRGF-ESF Trust), which is administered

separately by the IMF as Trustee.

Effective January 5, 2006, the IMF adopted the legal framework applicable to

the Multilateral Debt Relief Initiative (MDRI) to provide full debt relief to low- income

member countries. For this purpose, the MDRI-I and MDRI-II Trusts were established

to provide grant assistance under the MDRI. Subsequent to the adoption of the MDRI,

the resources held in the SDA were transferred to the MDRI-I Trust, the PRGF-HIPC

Trust, and the PRGF-ESF Trust Subsidy Account.

Investment Account

On April 28, 2006, the Executive Board of the IMF approved the establishment

of the Investment Account within the General Department and authorized the transfer

of currencies from the GRA in an amount equivalent to the total amount of the General

and Special Reserves of the GRA on April 30, 2006. The transfers to the Investment

Account were made subsequent to the financial year ended April 30, 2006.

2.5.2 Accounting Policies

Basis of Accounting

The consolidated financial statements of the General Department are prepared in

49

accordance with International Financial Reporting Standards (IFRS). The consolidated

financial statements include the accounts of the GRA, the SDA, the Investment Account

(inactive in financial year ended April 30, 2006), and the MDRI-I Trust, an entity that is

determined to be substantially controlled by the SDA owing primarily to the existence of

the Trustee’s power to terminate the Trust and the SDA’s claim to the Trust’s entire

residual assets upon termination as long as there are no contributor resources in the

MDRI-I Trust. All transactions and balances between these entities have been eliminated

during the consolidation. Specific accounting principles and disclosure practices are

explained further below.

Use of Estimates

The preparation of consolidated financial statements in conformity with IFRS

requires management to make estimates and assumptions that affect the reported amounts

of assets and liabilities and disclosure of contingent assets and liabilities at the date of

the financial statements and the reported amounts of revenue and expenses during the

reporting period. Actual results could differ from those estimates.

Unit of Account

The consolidated financial statements are expressed in terms of SDRs. The value

of the SDR is determined by the IMF each day by summing the values in U.S.dollars,

based on market exchange rates, of the currencies in the SDR valuation basket. The IMF

reviews the SDR valuation basket every five years. The latest review was completed in

November 2005, and the new composition of the SDR valuation basket became effective

on January 1, 2006. The currencies in the basket as of April 30, 2006, and 2005 and their

amounts were as follows:

Table 2.2

IMF’s SDR Valuation Basket (as of April 30, 2006)

Currency Amounts

2006 2005

Euro 0.4100 0.4260

Japanese yen 18.4000 2.0000

Pound sterling 0.0903 0.0984

U.S.dollar 0.6320 0.5770As of April 30, 2006, one SDR was equal to 1.47106 U.S.dollars

(one SDR was equal to 1.51678 U.S.dollars as of April 30, 2005).

Source: IMF’s Annual Reports for the respective years.

Currencies

Currencies consist of members’ currencies and securities held by the IMF. Each

member has the option of substituting non-negotiable and non-interest-bearing securities

for the IMF’s holdings of its currency that exceed ¼ of 1 percent of the member’s quota.

These securities are encashable by the IMF on demand.

Each member is required to pay to the IMF its initial quota and subsequent quota

increases partly in its own currency, with the remainder to be paid in usable currencies

50

prescribed by the IMF, or SDRs. The only exception was the quota increase of 1978,

which was paid entirely in members’ own currencies.

Usable currencies consist of currencies of member countries considered by the

IMF to have strong balance of payments and reserve positions. These currencies are

included in the IMF’s Financial Transactions Plan to finance purchases and other transfers

of the IMF. Participation in the Financial Transactions Plan is reviewed on a quarterly

basis. Usable currencies and SDR holdings readily available to finance IMF operations

and transactions are considered cash equivalents. The changes in non-usable currencies

result from the IMF’s transactions (purchases and repurchases) where a member’s

currency is exchanged for another member’s currency, or from the inclusion/exclusion

of a member’s currency in the IMF’s Financial Transactions Plan.

Currencies, including securities, are valued in terms of the SDR on the basis of

the currency/SDR exchange rate determined for each currency. Securities can be

substituted by members for currencies at their option. These securities are not marketable

but can be converted into currencies on demand. Each member is obligated to maintain,

in terms of the SDR, the value of the balances of its currency, including its securities,

held by the IMF in the GRA. This requirement is referred to as the maintenance-of-value

obligation. Whenever the IMF revalues its holdings of a member’s currency, a receivable

or a payable is established for the amount required to maintain the SDR value of the

IMF’s holdings of that currency. The currency balances in the balance sheet include

these receivables and payables. All currencies are revalued periodically in terms of the

SDR, including at each financial year end.

Credit Outstanding

The IMF provides balance of payments assistance in accordance with established

policies by selling to members, in exchange for their own currencies, SDRs or currencies

of other members. When members make purchases, they incur obligations to repurchase

the IMF’s holdings of their currencies arising from the purchases within specified periods

by payments in SDRs or other currencies, as determined by the IMF. The IMF credit is

subject to specific repayment schedules over periods that vary depending on the type of

facility used. Members are entitled to repurchase, at any time, the IMF’s holdings of

their currencies on which charges are levied and are expected to make repurchases as

and when their balance of payments and reserve position improve.

The repurchase policies of the IMF are intended to ensure the revolving character

of its resources. Purchases of currencies from the GRA are subject to repurchase

obligations, which can differ depending on the policy or facility under which purchases

are made. In keeping with a long-standing principle of the IMF that its resources should

be repaid as soon as the balance of payments and reserve position improve, members in

a position to do so are expected to make repurchases under predetermined time-based

expectation schedules. However, if a member’s external position is not sufficiently strong,

it may request that repurchases on the expectation schedule be extended to the original

obligation schedule. A member is considered overdue only after failure to make a payment

on the repurchase obligation schedule.

51

Overdue Obligations and Burden-sharing Mechanism

It is the policy of the IMF to exclude from current income charges due from

members that are six months or more overdue in meeting any financial obligation to the

IMF. The IMF fully recovers this lost income from the burden-sharing mechanism, through

adjustments, in the current period, to therates of charge and remuneration. Members

that have borne the financial consequences of overdue charges receive refunds to the

extent that overdue charges that had given rise to burden-sharing adjustments are

subsequently settled.

An impairment loss would be recognized if there is objective evidence of

impairment as a result of a past event that occurred after initial recognition, and is

determined as the difference between the outstanding credit’s carrying value and the

present value of the estimated future cash flows. No impairment losses have been

recognized.

First Special Contingent Account

In view of the risk resulting from overdue obligations, the IMF accumulates

balances in the first Special Contingent Account (SCA-1) by collecting resources under

the burden-sharing mechanism. Losses arising from overdue principal, if realized, would

be charged against the SCA-1. The IMF has not realized any losses on overdue financial

obligations. However, the IMF considers it prudent to maintain the SCA-1 as an added

protection until all arrears are fully settled. Balances in the SCA-1 are refundable to the

members that shared the cost of its financing in proportion to their contributions when

there are no outstanding overdue repurchases and charges, or at such earlier time as the

IMF may decide.

IMF’s SDR Holdings

Although SDRs are not allocated to the IMF, the IMF may acquire, hold, and

dispose of SDRs through the GRA. The IMF receives SDRs from members in the

settlement of their financial obligations to the IMF and uses SDRs in transactions and

operations with members. The IMF earns interest on its SDR holdings at the same rate

as all other holders of SDRs.

Gold Holdings

The Articles of Agreement limit the use of gold in the IMF’s operations and

transactions. Any use provided for in the Articles requires a decision adopted by an 85

percent majority of the total voting power. Under the Articles, the IMF may sell gold

outright on the basis of prevailing market prices but cannot engage in any other gold

transactions, such as loans, leases, swaps, or the use of gold as collateral. In addition,

the IMF does not have the authority to buy gold, but it may accept payments from a

member in gold instead of SDRs or currencies in any operation or transaction under the

IMF’s Articles at prevailing market prices.

In accordance with the provisions of the Articles, whenever the IMF sells gold

held on the date of the Second Amendment of the IMF’s Articles of Agreement (April 1,

52

1978), the portion of the proceeds equal to the historical cost must be placed in the

GRA. Any portion of the proceeds in excess of the historical cost will be held in the

SDA or transferred to the Investment Account. The IMF may also sell gold held on the

date of the Second Amendment to those mem- bers that were members on August 31,

1975, in proportion to their quotas on that date, in exchange for their own currencies at

the historical cost. The IMF values its gold holdings at historical cost using the specific

identification method. The carrying value of the Fund’s gold holdings is derived from

quota subscriptions prior to the Second Amendment and the settlement of financial

obligations by members in 1992 and 1999.

2.5.3 Financial Risk Management

In providing financial assistance to member countries and conducting its

operations, the IMF is exposed to various types of risks, including credit, interest rate,

exchange rate, liquidity, and operational risks. Because of its unique role in the

international monetary system, the principal risk facing the IMF is credit risk.

Credit Risk

Credit risk refers to potential losses on the credit outstanding owing to the inability,

or unwillingness, of member countries to make repurchases. While the IMF is accorded

preferred creditor status, i.e., the claims of other creditors are subordinate to those of

the IMF, credit risk is inherent since the IMF generally provides financing when other

sources are not available to a member and has limited ability to diversify its loan portfolio.

As a result, credit concentration is high.

The IMF’s credit-risk-mitigating measures comprise policies on access limits;

program design and monitoring, including conditionality attached to its financing; early

repurchase policies; and preventative, precautionary, and remedial measures to cope

with the financial consequences of protracted arrears.

Interest Rate Risk

Interest rate risk is the risk that future cash flows will fluctuate because of changes

in market interest rates. The IMF’s cost structure and its income position are interest-

rate driven. Fluctuations in interest rates could widen or narrow the spread between the

rate of charge on credit outstanding and the rate of remuneration paid to member countries

with remunerated reserve tranche positions. To minimize the effect of interest rate

fluctuations on income, the IMF links the rate of charge directly to the SDR interest rate

(which is equal to the rate of remuneration).

Exchange Rate Risk

Exchange rate risk is the exposure to the effects of fluctuations in the prevailing

foreign currency exchange rates on an entity’s financial position and cash flows. The

IMF uses the SDR as the unit of account and conducts its transactions in terms of the

SDR. It has no exchange rate risk exposure on its holdings of members’ currencies

since, under the Articles of Agreement, members are required to maintain the value of

such holdings in terms of the SDR. Any depreciation/appreciation in their currency vis-

53

à-vis the SDR gives rise to a currency valuation adjustment receivable or payable that

must be settled on an annual basis and that is included in the stock of the IMF’s currency

holdings. Therefore, the value of the IMF’s currency holdings does not fluctuate in SDR

terms. Exchange rate risk on IMF investments is managed by investing in securities

denominated in SDRs or in the constituent currencies of the SDR valuation basket. The

IMF also has other assets and liabilities, such as trade receivables and payables,

denominated in currencies other than SDRs and makes administrative payments largely

in U.S.dollars, but the exchange rate risk exposure is very limited.

Liquidity Risk

Liquidity risk is the risk of non-availability of resources to meet the IMF’s financing

needs and obligations. The IMF must have usable resources available to meet members’

demand for credit. While the IMF’s sources are revolving, uncertainties in timing and

amount of credit extended to members during financial crises expose the IMF to liquidity

risk. Moreover, the IMF must also stand ready to meet the potential demands from

members drawing upon their reserve tranche positions, which have no fixed maturity

and are part of members’ reserves.

The IMF manages its liquidity risk not by matching the maturity of assets and

liabilities but by closely scrutinizing developments in its liquidity position, especially as

they relate to the adequacy of quota-based resources to meet liquidity needs. The Articles

of Agreement require the IMF to conduct a general review of members’ quotas at intervals

of no more than five years in order to assess the adequacy of quota-based resources to

meet members’ demand for IMF financing. There have been eight quota increases,

including an ad hoc increase, as a result of the reviews. The last general review (the

twelfth) was completed in January 2003 with no proposed quota increase. Should the

available quota-based resources be inadequate to meet financing needs, the IMF may

activate its standing credit lines totaling SDR 34 billion under the General Arrangements

to Borrow and the New Arrangements to Borrow, and its associated agreement with

Saudi Arabia for an additional SDR 1.5 billion. The IMF also monitors its liquidity

position over a shorter term, using objective criteria such as the forward commitment

capacity for the next twelve-month period.

Operational Risk

Operational risk includes risk of loss attributable to errors or omissions because

of failures in executing or processing transactions, inadequate controls, human factors,

and/or failures in underlying support systems.

The IMF mitigates operational risk by (i) identifying key operational risks, (ii)

maintaining a system of internal controls, (iii) documenting policies and procedures on

administrative and accounting and reporting processes, and (iv) conducting internal audits

to ensure accurate processing of transactions and minimize the possibility of undetected

errors. The design and effectiveness of controls are evaluated continuously and

improvements are implemented on a timely basis. The results of the internal evaluation

of the effectiveness of internal controls are reported by the Office of Internal Audit and

Inspection to the External Audit Committee, which also exercises oversight over the

54

external audit of the IMF’s accounts and its controls.

The IMF has adopted a Code of Ethics to promote the highest standards of ethics

among its staff, including senior management and members of the Executive Board. The

enforcement of the Code of Ethics is supplemented by procedures for the reporting and

investigation of irregularities and improprieties, including fraudulent acts.

2.5.4 Multilateral Debt Relief Initiative

Under the MDRI, debt relief is provided to Heavily Indebted Poor Countries

(HIPCs) and non-HIPCs with annual per capita income of $380 or less, and to HIPCs

with an annual per capita income of more than $380. Grant assistance from the MDRI

Trusts (together with assistance under the HIPC Initiative) provides debt relief to cover

the full stock of debt owed to the IMF as of December 31, 2004, that remains outstanding

at the time the member qualifies for such relief.

During the financial year ended April 30, 2006, debt relief under the MDRI was

granted to 20 members amounting to SDR 2,503 million, consisting of outstanding credit

in the GRA of SDR 90 million and PRGF-ESF Trust loans of SDR 2, 413 million. MDRI

grant assistance provided from resources held in the MDRI-I Trust amounted to SDR 1,

120 million. All HIPCs will receive MDRI assistance upon reaching the completion point

under the HIPC Initiative. Since the stock of debt owed to the IMF as of December 31,

2004, decreases over time, the actual debt eligible for MDRI assistance for the remaining

members depends on the timing of their completion points. The IMF periodically reviews

the qualification of members for MDRI debt relief as these members make progress

toward reaching the completion point under the HIPC Initiative.

MDRI grant assistance to the remaining eligible members is subject to the

availability of resources and is accrued when it is probable that a liability has been incurred

and the amount of such grant assistance can be reasonably estimated. The liability recorded

in the MDRI-I Trust amounted to SDR 380 million as of April 30, 2006, and is based on

the evaluation of currently available facts with respect to each individual eligible member

and includes factors such as progress made toward reaching the completion point under

the HIPC Initiative and the capacity to meet the macroeconomic performance and other

objective criteria after reaching the completion point. As the qualification of members

for MDRI debt relief is assessed, the amounts recorded are reviewed periodically and

adjusted to reflect additional information that becomes available.

2.5.5 Special Disbursement Account

Investments

As at April 30, 2006, there were no investments in the SDA. Investments in the

MDRI-I Trust consisted of short-term fixed-term deposits with maturities of less than

one year and amounted to SDR 384 million. As at April 30, 2005, the investments in the

SDA consisted of short-term fixed-term deposits with maturities of less than one year

and amounted to SDR 2,519 million.

55

Investment income of the SDA and the MDRI-I Trust for the years ended April

30, 2006, and 2005 was SDR 49 million and SDR 52 million, respectively.

Contributions to Administered Accounts

Assets in the SDA can be used for special purposes authorized in the Articles,

including providing financial assistance on special terms to low-income member countries.

Proceeds from the repayment of SAF loans are transferred from the SDA to the Reserve

Account of the PRGF-ESF Trust as contributions. During the financial years ended April

30, 2006, and 2005, such contributions amounted to SDR 37 million and SDR 41 million,

respectively.

In addition, the accumulated investment earnings in the SDA are available for

financing the PRGF-HIPC Trust on an as-needed basis. During the financial year ended

April 30, 2006, the SDA contributed SDR 63 million to the PRGF-HIPC Trust (SDR

164 million during the financial year ended April 30, 2005).

Trust Fund

The IMF is the Trustee of the Trust Fund, which was established in 1976 to

provide balance of payments assistance on concessional terms to eligible members that

qualify for assistance. The Trust Fund is in liquidation.

In 1980, the IMF, as a Trustee, decided that, upon the completion of the final

loan disbursements, the Trust Fund would be terminated as of April 30, 1981. Since that

date, the activities of the Trust Fund have been confined to the conclusion of its affairs.

The Trust Fund has no assets other than claims receivable, including interest and special

charges, from Liberia, Somalia, and Sudan amounting to SDR 118 million at April 30,

2006, and 2005. All interest is deferred. Cash receipts on these loans are to be transferred

to the Special Disbursement Account.

2.5.6 Borrowings

Under the General Arrangements to Borrow (GAB) and an associated agreement

with Saudi Arabia, the IMF may borrow up to SDR 18.5 billion when supplementary

resources are needed, in particular, to forestall or to cope with an impairment of the

international monetary system. The GAB became effective on October 24, 1962, and

has been renewed through December 25, 2008. Interest on borrowings under the GAB

is set at a rate equal to the SDR interest rate.

Under the New Arrangements to Borrow (NAB), the IMF may borrow up to

SDR 34 billion of supplementary resources. The NAB is the facility of first and principal

recourse, but it does not replace the GAB, which will remain in force. Outstanding

drawings and commitments under these two borrowing arrangements are limited to a

combined total of SDR 34 billion. The NAB became effective for a five-year period on

November 17, 1998, and has been renewed through November 16, 2008. Interest on

borrowings under the NAB is payable to the participants at the SDR interest rate or any

such higher rate as may be agreed between the IMF and participants representing 80

percent of the total credit arrangements. There was no balance outstanding as at April

56

30, 2006, and 2005 under the GAB or the NAB.

2.5.7 Arrangements

An arrangement is a decision of the IMF that gives a member the assurance that

the IMF stands ready to provide SDRs or usable currencies during a specified period

and up to a specified amount, in accordance with the terms of the arrangement. At April

30, 2006, the undrawn balances under the 11 arrangements that were in effect in the

GRA amounted to SDR 7,539 million (SDR 7,927 million under 12 arrangements at

April 30, 2005).

2.5.8 Burden-sharing and Special Contingent Account

Under the burden-sharing mechanism, the basic rate of charge is increased and

the rate of remuneration is adjusted downward to offset the effect on the IMF’s income

of the nonpayment of charges and also to finance the additions to the SCA-1. Cumulative

charges, net of settlements, that have resulted in adjustments to charges and remuneration

since May 1,1986 (the date the burden-sharing mechanism was adopted) amounted to

SDR 859 million at April 30, 2006, (SDR 848 million at April 30, 2005). The cumulative

refunds for the same period, resulting from the settlements of overdue charges for which

burden-sharing adjustments have been made, amounted to SDR 1, 080 million and SDR

1,073 million, at April 30, 2006, and 2005, respectively.

The SCA-1 is financed by adjustments to the rate of charge and the rate of

remuneration. Balances in the SCA-1 are to be distributed to the members that shared

the cost of its financing when there are no outstanding overdue repurchases and charges,

or at such earlier time as the IMF may decide. Amounts collected from members for the

SCA-1 are akin to refundable cash deposits and are recorded as collections of cash and

as a liability to those who paid it. Losses arising from overdue obligations, if realized,

would be shared by members in proportion to their cumulative contributions to the SCA-

1. For the financial years ended April 30, 2006, and 2005, the annual addition to the

SCA-1 amounted to SDR 94 million.

2.5.9 Technical Assistance and Training

The IMF complements its surveillance operations and its lending in support of

member countries' policy programmes with technical assistance and training. The goal is

to help member countries strengthen their human and institutional capacity to design

and implement macroeconomic and structural policies that promote macroeconomic and

financial stability, economic growth, and poverty reduction.

The IMF offers technical assistance and training mainly in its core areas of its

expertise, such as macroeconomic policy, tax and revenue administration, public