The world has changed in the midstream and pipelines must adapt

Pre-shale world

B Interstate system: Long-haul pipelines to connect supply in the Gulf, Rockies and Midcontinent to the consuming Northeast, Midwest and West

Interstate pipeline grid has been “built out;”regional pipelines to support dramatic increases in production close to market areas – especially Marcellus with volumes to the Northeast, Upper Midwest, eventually GoM

C Contracting for delivered supply: 15-20+ year contracts for Firm Transport –driven by Local Distribution Companies (LDC’s)

Most FT contracts expiring by 2020 (85%) with most recent renewals of 5 years or less, as LDC’s expect to reconfigure gas sources.Customer balance changing from LDC’s to Marketers/Producer Marketers and Producers; pipelines must reconfigure systems and redesign rates/offerings

A Basis: Wide basis, especially between the Gulf and Northeast

Collapsed basis, with new pipeline builds; erosion in NE bases with regional builds

New paradigm

D Midstream opportunities:Predominantly centered on natural gas, and long-haul pipeline focused

NGL and oil represent a large (60%+) and growing fraction of total opportunity; much greater competition for infrastructure including MLP’s, producers, and utilities

McKinsey & Company 2|

Significant midstream gas opportunity – But, who benefits?

2SOURCE: McKinsey North America Gas Model; McKinsey North American Basis and Flow mode; team analysis

ESTIMATES

~$150 Billion investment required

Will the interstatesbe able to benefit

significantly?

Discussion▪ Supply trends▪ Demand from industrial

projects▪ Resulting

infrastructure needs

Infrastructure area

80

10

Gathering, processing,and NGL’s

Laterals

27

Total

13

Interstate gas pipelines

146-154

Storage

Light Tight Oil (LTO)

4

Intrastate gas pipelines(pipes & compression)

12

Investment required thru 2020

18

McKinsey & Company 3|1 Excludes finding and land costs2 Associated gas plays and predominantly oil basins excluded from this chart

2000 1,800400 1,000

0

1,400

2

1,200 1,600

16

14

12

10

8

6

800600

4

NORTH AMERICAN SUPPLY TRENDS

Tight

Shale

Conventional

CBM

Gas production can yield ~10% returns in the $4-6/MMBturange, setting a “ceiling” for US gas prices

Technically Recoverable resources2, Tcf

Full cost Breakeven for gas basins1 2, $/MMBtu

2011 Prod. = 24 Tcf

SOURCE: McKinsey Supply Model

PRELIMINARY

McKinsey & Company 4|

Niobrara

Cody

Mowry

Gammon

Excello-Mulky

Marcellus (256)

Devonian

Chattanooga

Conasauga

Floyd-Neal

Fayetteville (20)

Haynesville/Bossier (251)

Woodford/Caney

Barnett (118)

Pearsall/Eagle Ford (>100)

Woodford (42)

Barnett and Woodford

Bend

PierreLewis

Hermosa

Mancos

Hilliard-Baxter-Mancos

Antrim

New Albany

Utica

Horn River Shale (40)

Montney (152)

ExplorationDevelopingProducing

Bakken

Incremental production – Bcfd growth vs. 2012

0

1

2

20172016201520142013 20202018 2019

Southern Supply

Appalachia Area

Rockies Area

Midcon Area

WCSB

MODELED

-2

0

20202017 2018 20192016201520142013

0

2

4

6

8

10

2018 2019 202020172016201520142013

-1

0

1

20192018 202020172016201520142013

-2

0

2

2018 2019 202020172016201520142013

SOURCE: McKinsey North American Supply Model; McKinsey analysis

NORTH AMERICAN SUPPLY TRENDS

Most incremental production expected out of Appalachia

1 Rig count updated until March 17, 2011; 2 Based on STEO (monthly); 3 Based on AEO (Annual)

With this much excess supply, prices will likely remain low

With this much excess supply, prices will likely remain low

McKinsey & Company 6|1 Pipeline to Mont Belvieu

U.S. (lower 48 states) production Natural gas liquids

US shales will drive a 58% increase in US L48 NGL production over the this decade and require ~$80B in capex – which is most of the opportunity

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

+58%

Refining

US Base NGLProduction

Barnett

Eagle Ford

Marcellus

Avalon

Bakken

Niobrara

Granite Wash

Woodford

2020181614121008062004

SOURCE: McKinsey North America Gas Model; Government and company reports; team analysis

Thousand bpd

Capital requirement

$ Billion incremental capital

5

3

3

9OtherShales

2813

Bakken 93

Niobrara 106

Eagle Ford 136

Marcellus 2411 51

NGLs Pipelines

Fractionation

Gathering

Processing

Total >$80B

RESULTING INFRASTRUCTURE NEEDS

McKinsey & Company 7|

Southwest to Southeastern

Southwest toNortheastern

Southwest toMidwestern

Southwest Panhandleto Midwestern

Southwest to Western

Western Canada toMidwestern

Rocky MountainArea to Midwest Rocky Mountain

Area to West

Canada to West

Eastern CanadaNortheast

Western Canada to Northeast

1

3

2

9

8

7

10 11

4

6

5

SOURCE: EIA, Office of Oil and Gas, Natural Gas Division, GasTran – Gas Transportation Information System; McKinsey modeling and analysis

Additional peak capacity needed (Bcfd)

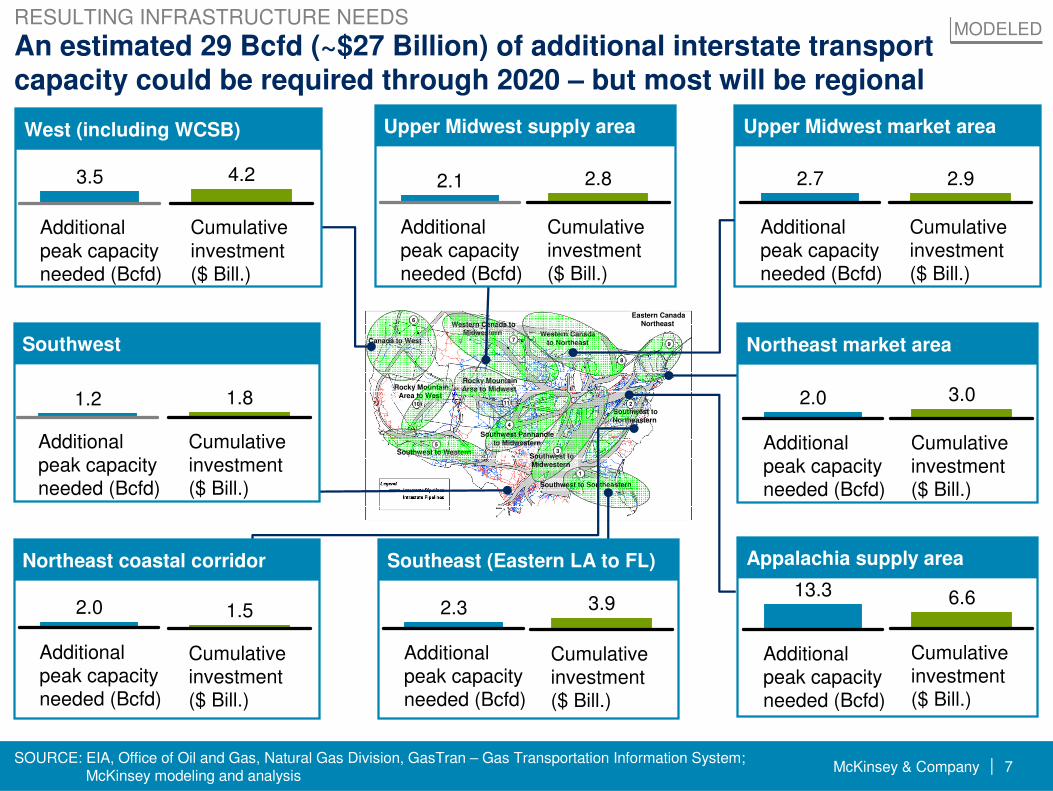

2.7

Upper Midwest market areaUpper Midwest supply area

Southwest Northeast market area

Northeast coastal corridor Southeast (Eastern LA to FL) Appalachia supply area

Cumulative investment ($ Bill.)

2.9

Additional peak capacity needed (Bcfd)

1.2

Cumulative investment ($ Bill.)

1.8

Additional peak capacity needed (Bcfd)

2.1

Cumulative investment ($ Bill.)

2.8

Additional peak capacity needed (Bcfd)

2.0

Additional peak capacity needed (Bcfd)

2.3

Cumulative investment ($ Bill.)

3.9

Additional peak capacity needed (Bcfd)

13.3

Cumulative investment ($ Bill.)

6.6

Additional peak capacity needed (Bcfd)

2.0

Cumulative investment ($ Bill.)

3.0

Cumulative investment ($ Bill.)

1.5

MODELEDAn estimated 29 Bcfd (~$27 Billion) of additional interstate transport capacity could be required through 2020 – but most will be regional

RESULTING INFRASTRUCTURE NEEDS

West (including WCSB)

Additional peak capacity needed (Bcfd)

3.5

Cumulative investment ($ Bill.)

4.2

McKinsey & Company 8|

Proposed1 natural gas, interstate pipeline projects – are all regional pipelines, expansions or laterals

SOURCE: Ventyx Energy Velocity, EIA; Company websites and presentations; Trade press

1 Includes projects under construction, approved, filed and proposed in all regions. Does not include two oil pipeline conversion projects (limited data); 8/122 Laterals to storage, LNG, power plants

RESULTING INFRASTRUCTURE NEEDS

Areas of concern▪ Appalachian

supply▪ Routes to

NE/Midwest

44

34

180

Laterals2

Expansion

Regional

Trunklines

Number of projects

96

Proposed1 natural gas pipelines

Miles

3,983.4

599.7

922.5

2,461.2

0

Bcfd

46.6

9.9

22.9

13.9

0

McKinsey & Company 9|

Marcellus production is displacing imports – pipes will eventually reverse

SOURCE: Ventyx Energy Velocity; team analysis

16

14

12

10

8

6

4

2

0

Ju

l 20

12

Jan

20

12

Ju

l 20

11

Jan

20

11

Ju

l 20

10

Jan

20

10

Ju

l 20

09

Jan

20

09

Ju

l 20

08

Jan

20

08

Ju

l 20

07

Jan

20

07

Production

REX

Canada2

MA LNG

TGP (Tenn.)

Transco

TETCO

Col. Gulf

TGT (Tx. Gas)

1 Production estimated based on processing plant data, and McKinsey supply model after 1/1/112 Canada includes Canadian imports, M&NE, Canaport LNG and Sable Island

Northeastern supply1

Million Dth/day

A

C

B

D

E

Declining flows from the Gulf – 28% decline in cumulative flows from 1/2010 to 1/2012 (Bcfd)

![BASIL INFRASTRUCTURE PROJECTS LIMITED vbcflcs@gmail.com BASIL INFRASTRUCTURE PROJECTS LIMITED [Formerly known as VBC Finance & Leasing Limited] BASIL INFRASTRUCTURE PROJECTS LIMITED](https://static.documents.pub/doc/80x56/5aa7aaa87f8b9a50528cae5d/basil-infrastructure-projects-limited-vbcflcsgmailcom-basil-infrastructure-projects.jpg)