www.imrg.org IMRG Capgemini Sales Index Report March 2017 (reporting February 2017 results) What is the IMRG Capgemini e-Retail Sales Index? The IMRG Capgemini e-Retail Sales Index is the primary performance indicator of the UK online shopping industry, tracking 'hard' sales data from reputable e-retailers since April 2000. The participating merchants represent a significant proportion of the UK internet shopping market.

Transcript

www.imrg.org

IMRG Capgemini

Sales Index Report March 2017 (reporting February 2017 results)

What is the IMRG Capgemini e-Retail Sales Index? The IMRG Capgemini e-Retail Sales Index is the primary performance indicator of the UK online

shopping industry, tracking 'hard' sales data from reputable e-retailers since April 2000. The

participating merchants represent a significant proportion of the UK internet shopping market.

*ABV excludes travel **m-Retail includes sales via smartphone and tablets combined

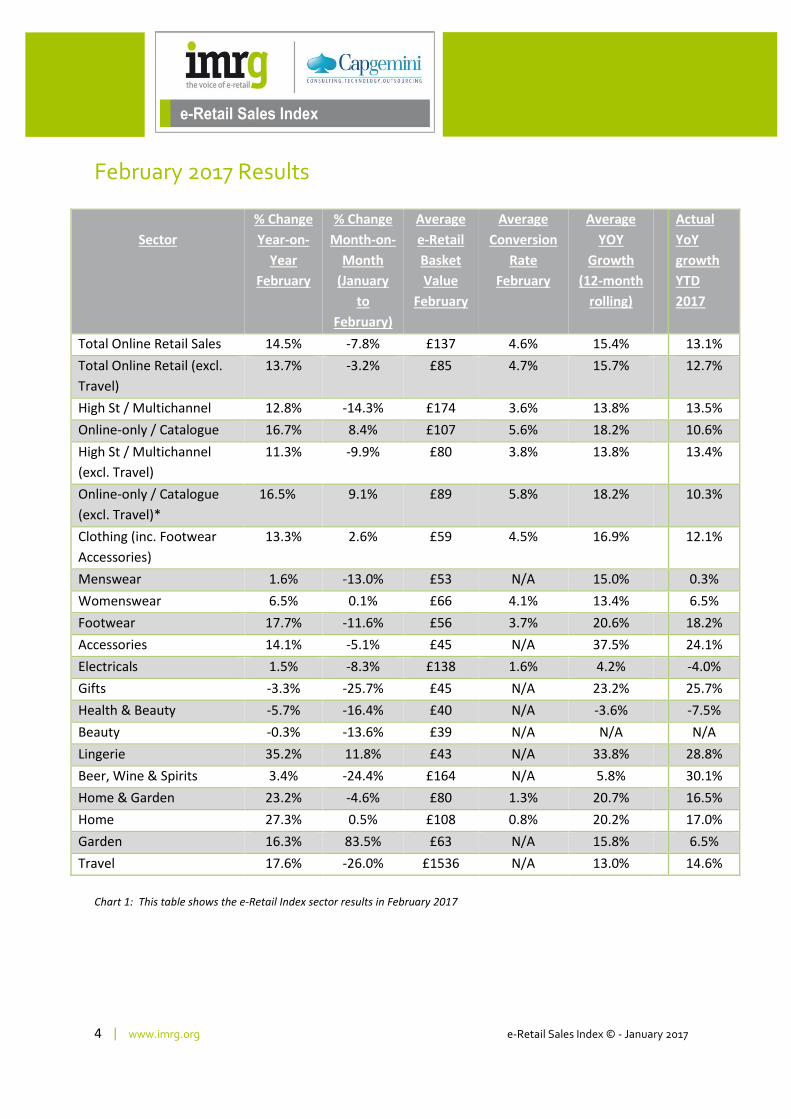

KEY HIGHLIGHTS:

• UK mobile retail sales (including smartphones and tablets) grew 12.1% year-on-year in February and declined 15.1% from January.

• Sales via smartphones reported a year on year growth of 57.0%. February 2016 was 92.4%

• Tablets returned to positive growth with 3.5% year on year in February. The rolling 12 months growth for tablets is 5.0%.

• The share of mobile retail sales for smartphones reached 48% in February (tablets 52%) — an increase from January 2017 at 46%.

• Average basket values (excl. Travel) for total mobile retail was £79. During the same period in 2016 it was £72.

COMMENT: UK mobile retail sales recorded annual growth of 12.1% during February, and decreased 15.1% from January. This compares with 33.3% year-on-year growth in February last year, and a monthly decrease of 15.3% from January 2015. Smartphones continue to outperform tablet year on year growth, with 57.0% and 35% respectively.

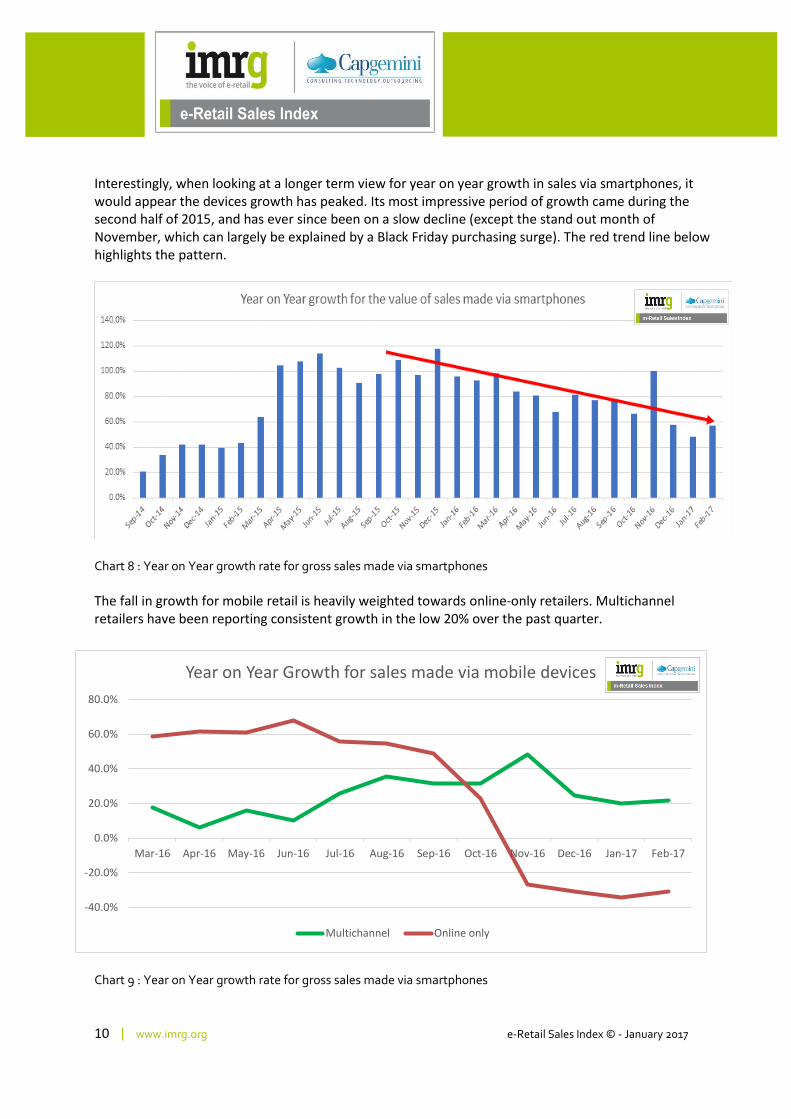

Interestingly, when looking at a longer term view for year on year growth in sales via smartphones, it would appear the devices growth has peaked. Its most impressive period of growth came during the second half of 2015, and has ever since been on a slow decline (except the stand out month of November, which can largely be explained by a Black Friday purchasing surge). The red trend line below highlights the pattern.

Chart 8 : Year on Year growth rate for gross sales made via smartphones

The fall in growth for mobile retail is heavily weighted towards online-only retailers. Multichannel retailers have been reporting consistent growth in the low 20% over the past quarter.

Chart 9 : Year on Year growth rate for gross sales made via smartphones

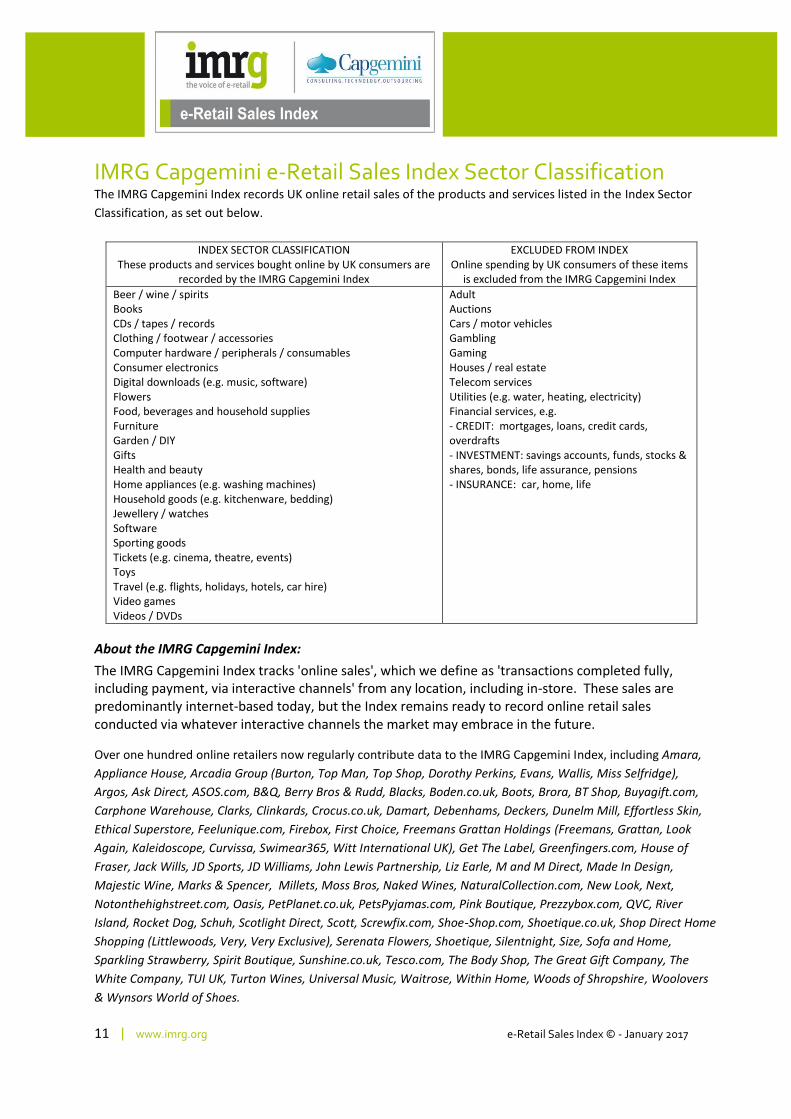

IMRG Capgemini e-Retail Sales Index Sector Classification The IMRG Capgemini Index records UK online retail sales of the products and services listed in the Index Sector

Classification, as set out below.

INDEX SECTOR CLASSIFICATION These products and services bought online by UK consumers are

recorded by the IMRG Capgemini Index

EXCLUDED FROM INDEX Online spending by UK consumers of these items

is excluded from the IMRG Capgemini Index

Beer / wine / spirits Books CDs / tapes / records Clothing / footwear / accessories Computer hardware / peripherals / consumables Consumer electronics Digital downloads (e.g. music, software) Flowers Food, beverages and household supplies Furniture Garden / DIY Gifts Health and beauty Home appliances (e.g. washing machines) Household goods (e.g. kitchenware, bedding) Jewellery / watches Software Sporting goods Tickets (e.g. cinema, theatre, events) Toys Travel (e.g. flights, holidays, hotels, car hire) Video games Videos / DVDs

Adult Auctions Cars / motor vehicles Gambling Gaming Houses / real estate Telecom services Utilities (e.g. water, heating, electricity) Financial services, e.g. - CREDIT: mortgages, loans, credit cards, overdrafts - INVESTMENT: savings accounts, funds, stocks & shares, bonds, life assurance, pensions - INSURANCE: car, home, life

About the IMRG Capgemini Index:

The IMRG Capgemini Index tracks 'online sales', which we define as 'transactions completed fully, including payment, via interactive channels' from any location, including in-store. These sales are predominantly internet-based today, but the Index remains ready to record online retail sales conducted via whatever interactive channels the market may embrace in the future.

Over one hundred online retailers now regularly contribute data to the IMRG Capgemini Index, including Amara,

Appliance House, Arcadia Group (Burton, Top Man, Top Shop, Dorothy Perkins, Evans, Wallis, Miss Selfridge),

Participation in the IMRG Capgemini Index is available to reputable online retailers of all sizes. For further details, or to participate in the survey, please contact:

Matthew Walsh IMRG Tel : +44 (0)203 696 0990 Email: [email protected]

*Estimate of Market Cash Value: 1 Index point currently = GBP £0.77 million

Please note that IMRG has rebased its Index-linked estimates of the UK online retail market size downwards by 24.9%, and will no longer use Forrester Research’s IMRG Capgemini E-retail Sales Index Multiplier, which we have previously used to estimate the size of the UK online retail market. IMRG’s own extensive research now provides the basis for the IMRG Index Multiplier, which has been rebased to: - 1 Index point = GBP 0.77 million.

The IMRG Capgemini Index is a trend line that represents the collective gross sales value of participating merchants. We attribute a cash value to an Index point — i.e. a 'multiplier', with which we estimate the market's cash value, month by month. To accommodate the fact that the overall internet shopping market's growth is greater than that of the Index group, as more merchants trade online, we have rebased the multiplier value from time to time:

- November 2008: 1 point = £0.77 million (IMRG) - May 2006: 1 point = £1.02 million (Forrester Research) - January 2005: 1 point = £0.87 million (Forrester Research) - February 2003: 1 point = £0.82 million (Forrester Research) - April 2000: 1 point = £0.8 million (Forrester Research)

We do not recalculate Index cash value estimates retrospectively, as this would skew the historical data.

About IMRG: IMRG (Interactive Media in Retail Group) is the UK’s industry association for online retail. Formed in 1990, IMRG is setting and maintaining pragmatic and robust online retail standards to enable fast-track industry growth, and facilitates its community of members with practical help, information, tools, guidance and networking. Consumers can be confident when dealing with IMRG Members because all interact in an environment where they are encouraged to operate using methods that are Honest, Decent, Legal, Truthful and Fair, and have undertaken to not bring the industry into disrepute. The strength of IMRG is the collective and cooperative power of its members. For more information please visit http://www.imrg.org/ or email [email protected].

About Capgemini: With around 120,000 people in 40 countries, Capgemini is one of the world's foremost providers of consulting, technology and outsourcing services. The Group reported 2011 global revenues of EUR 9.7 billion. Together with its clients, Capgemini creates and delivers business and technology solutions that fit their needs and drive the results they want. A deeply multicultural organization, Capgemini has developed its own way of working, the Collaborative Business ExperienceTM, and draws on Rightshore®, its worldwide delivery model. Learn more about us at www.capgemini.com. Rightshore® is a trademark belonging to Capgemini.