Vol.25 No10 January 2012 In this issue 4 President’s message 4 Chamber’s Activities • Municipalika 2012 – Making Cities Work • MCCI-MMA Video Discussion on “The Point of Impact” • FFT on Nuclear Power – To be or Not to be • Seminar on Exim Trade Facilitation 4 General Committee 4 Expert Committees 4 SPOT LIGHT Foreign Direct Investment 4 Policy Watch 4 Reflections 4 Additions to Library 4 Representations 4 Trade Fairs & Exhibitions 4 Economic Review

SAFE DRINKING WATER@ 1 Paisa per liter for Preventive Healthcare

GRE

EN TECHNOLO

GY

DE NORA IS A PIONEER IN ELECTRO-CHLORINATION

SYSTEMS BRANDED AS SEACLOR MAC®.

DE NORA HAS DEVELOPED SOLAR OPERATED EC

MODELS USING GREEN TECHNOLOGY.

ALL MAC MODELS ARE MANUFACTURED IN INDIA.

MORE THAN 900 INSTALLATIONS.

Typical Continuous Type

WORKS ONSOLAR ENERGY

De Nora Solution for SAFE WATER• 80% diseases are Water Borne• De Nora Proprietary processes destroy most of the

Bacteria & many Harmful Virus to make Water Safe• Muncipality & Community Water Treatment• Safe Water for Drinking, Cooking & Bathing• Removal of Algae in cooling water circuits• Disinfection of Water for Swimming pools• Pollution Control - Special Applications

Capacity of SAFE WATER per day• SOLAR unit: 54 CubM• BATCH processes: 600 CubM to 7,200 CubM• Continuous Processes: 12,000 CubM to 72,000 CubM

KEY FEATURES• Onsite generation of Chlorine as Hypo Solution• Uses only SALT & WATER• Environmentally friendly & replaces Hazardous Chemicals• Easy to Transport, Install, Operate & Maintenance• Works with MICROPROCESSOR• Salinity check with REFERENCE cell• Better SALT & POWER Efficiency• All India Sales & Services

MAIN CUSTOMERS• Railways• PHED's like Jaipur & Nagpur etc.• PSU's like Refineries, SAIL, BHEL & BEL etc.• WHO approved vendors & NGO

SOLAR SYSTEMS• No Electricity required, Works with SOLAR Energy• SAFE drinking WATER to isolated villages• Produces 54,000 liters of SAFE drinking WATER everyday• Safe drinking water for 12,000 peoples everyday• Easy to Operate, Environmentally friendly & Economic• Can be operated by VILLAGERS themselves• Less Operating Cost and Negligible Maintenance

Typical Batch Type

Solar Mac unit

3

PRESIDENT’S MESSAGE

Economy & Business - in mystified state?

Dear Members,

In the year 2011 which passed by and also the beginning of 2012 till now, there are mixed feelings about how our economy and businesses are doing.

Indian economy, undoubtedly, was steered by a series of downbeat economic and political events last year. The global turmoil and uncertainties did cause an impact on our economy too.

The decelerating GDP growth rate has made our aim of achieving double digit growth, a thing of the past, and today we are struggling to maintain a 7.5% to 8% growth while the projections are no better than 7% ( India's economy may grow only by 6% in 2012, according to report by Moody's Analytics).The IIP dip added its own woes to the existing industrial gloom.

Rising Inflation took everyone by surprise and has had a cascading effect on many sectors, adversely affecting almost every section of people. Food inflation touched a record high. The Reserve Bank of India lifted interest rates 13 times within a period of 18 months to tame the inflation bug, but the effort did not yield necessary results. This, as many feel, has produced the worst of both worlds: Growth has been hit while there was less impact on inflation or expectations!

Financial markets tell a similar story. The Sensex fell 25% in 2011, while the rupee fell a dramatic 16% in 2011, making it the worst performing major Asian currency and resulted in portfolio investors actively withdrawing funds.In fact 2011 was full of signs of an economy decelerating - high inflation, a slowdown in manufacturing, exports losing momentum, and so on.

Also on the business front, nothing of the much talked about reforms or initiatives moved ahead - The GST, DTC, Companies Bill, none of them saw the light of the day. There is no sign of most of them coming through even in the current budget session too.

The mood is somber among the policy makers and the business community with regard to the short-term aspects of the economy and the outlook for 2012. India's corporate sector looks particularly vulnerable. Production of capital goods, considered as a gauge of investment intentions, plunged. Infrastructure, particularly power, has been a major concern and the current plight of industries in Tamil Nadu needs no elaboration. All these and more do present a very bleak picture.

However, there are strong arguments that we should not confuse a short-run cyclical dip with a permanent de-rating of long-term structural potential.

The usual consolation is that our growth rate, though not matching our ambition, is still better off than many other countries, since most of them have negative or zero growth rate. The other silver lines are softening of inflation, including food inflation, a bit in the last few months. Headline inflation has particularly shown a decline in January 2012.

In an environment in which global growth is likely to be weak, economies like India that have a powerful domestic consumption dynamic, should lead; specifically for India, a fall in the exchange rate could also play a positive role. Indian exporters can gain market

share even if global trade remains depressed. Recovery in the US which is India’s biggest export market should help demand for manufactured goods.

With union budget around the corner, we should brain storm what really is required to get that magic growth rate of 9-10% which is said to be essential for a country of our size, to achieve many of our objectives and attain inclusive growth.

Reforms are going slow, but I recall what the IIM professor stated. Reforms need not be only in FDI & FII. These will automatically happen when the economic momentum picks up, with or without reforms. The reforms that we need are the ones that can actually raise our sustainable long-term growth rate. These have to come in areas like better targeting of subsidies, making projects in infrastructure viable so that they attract capital, raising the productivity of agriculture, improving healthcare and education, focusing on skill development, implementing fundamental reforms in taxation like GST and finally easing the countless rules and regulations that make doing business in India such a nightmare. Tackling corruption and ensuring good governance has to top the agenda.

If the government can get even a minimalist agenda out of the above going, while improving its governance and management of infrastructure, and if the Reserve Bank of India can cut interest rates quickly, the Indian script for 2012 could change. A number of these things do not require new legislation and can be done through executive procedure. What is required is the will to find the way.

To assist and promote a business casefor Sustainable Development andevolve a congenial policy and actionoriented environment for the sustainabledevelopmentoftheChennaimetropolitanregion in collaboration with like-mindedinstitutions.

The Sustainable Chennai Forum (SCF)will work closely with like-mindedorganizations like Madras University,Athena Infonomics, Anna University,Citizens alliance for Sustainable livingSUSTAIN,UNHabitat,BritishDeputyHighCommission andUS agencies andothersinthesector.

5

25thJanuary2012:

MCCI-MMAVideoDiscussionon“ThePointofImpact”

ThePointofImpactwasthetopicforthe

monthly video discussion being jointly

organizedbytheChamberandMMA.Mr

SKRaja,TrainerandFacilitator,conducted

theprogramme.

Mr Raja explained that Point of Impact

betweenacustomerandapersoninan

organization or a retail shop is nothing

but communication between the two.

Hesaidcustomerserviceissoimportant

as the customer forms opinions about

one’s organization at the first point of

contact.Hesaidcustomerserviceisgood

common sense and the three keys for

this are – attitude, communication and

effort. Create a positive attitude with

the customer; attitude comes from the

thoughtwhichiscontrolledbyus.

He said the good traits of a positive

person are – they smile, they do not

wastetimeandtheyareproblemsolvers.

Smile even when you are on the

phone. Have good eye contact with

the customer; great service iswhat the

customerwants.Createatrustwiththe

customerandconvincehimhesaid.

Explaining further he said, the threeelementsofcommunicationare–words,voicetoneandbodylanguage.Useopenended questions with the customer –rather than saying “yes/no”. Move tomore specific questions and encourageconversation;makethemfeelimportant.Bea listener– listen to the customeratleast80%.

Asyouwouldhaveseenfromthenewspapers,beginning15th February 2012, major shipping lines and feederoperatorshavedecidedtowithdrawtheChennaiTradeRecoveryleviedontheEximtradeattheChennaiPort.

Irked by the delay, the representatives of various tradebodies including the Madras Chamber took up theissuewiththeMinistryofShippingandtheMinistryofCommercetoresolvethisissue.

SMEdelegationtoJapan–May2012

Indo-JapanChamberofCommerce&Industrywill be taking a 20-membermulti-sector SMEdelegation to Japan between May 14-18,2012.

ThedelegationwillbevisitingTokyo,Yokohama,Osaka, Hiroshima, Fukuoka and Saga. Theprogramme primarily comprises B2B seminarswith Japanese counterparts and leadingChambersofCommerceintheseplaces.

Members of MCCI are invited to join thisdelegation.Forfurtherdetailspleasecontact:

At the start, the Burrah Sahibsfirst thought of the Port and otherinfrastructure like the Railways, Postsand Telegraphs and the Chamber sawto it they happened for the benefit ofimperial trade and commerce. Benefitsof British Rule was a stock questionstudents had to answer. However, itcan'tbedeniedthatpost-independencethosebenefits (most of all, the Englishlanguage which has given us the lift-off to cyberspace to reap the rewardsof a preferred destination for IT andoutsourcing) proved useful startingblocksforfreeIndiatogetstartedonitseconomicdevelopmentmission.

It is remarkable that for nearly 25years after Independence, there wasan amicable co-existence of the Britishfirms and the newly emerging Indianentrepreneurs and their companiessharing the seats in the ChamberCommittee equally almost till the mid70s.Theprimeinterestoftheexpatriatesin thatperiodwas taxationbearingonrepatriationandrestrictionsimposedbythe Foreign Exchange Regulation Actwhich one Assocham President called'FerociousFERA'.

IndianbusinesscameintoitsownintheChamber with a strong leadership ofsenior aswell as youngentrepreneurs.Theyhadtograpplewiththechallengesof a planned and controlled economy.Forquiteafewyearsthekeyquestionofstrategydebatedwas"tobereactiveor proactive". Reactive representationshadtobemadeoutofnecessityintheinterests of the membership, but loudaffirmationsofcommitmenttoproactiveactionweremadeateveryopportunity.Chambers, including MCCI, undertookeducational and trainingprojects, ruraldevelopmentprogrammesetc.

Allthetimethepitchwasraisedatannualmeetings and in representations for

liberalisation and freeing the economyfrom the shackles of controls andlicensingandregressivetaxation.Loandbehold,theeconomywasprogressivelydecontrolled and liberalized from theearlypartofthe1990s.

The gradual globalization of theeconomy with the emergence of theage of technology spurring the newknowledge based IT industries hasmarked a sea change in the industrialand commercial scene. They had theirimpact on older business modelswith the consequence that businessorganizations like the Chamber havebegun to reflect a new spirit of takingresponsibility for initiating positiveprogrammes on their own, apart fromcooperating with public bodies andgovernment to promote developmentforthegreatergoodofthecommunityand the nation. MCCI's thoughtfulproject of a Skill Development CentrenearChennaiisaninstanceinpoint.Themanystudies,seminarsandworkshopson a wide variety of subjects leaveno doubt that the Chamber is on aproactivetrajectoryevenasitdischargesitstraditionalrepresentationalfunctions.

Onecanseethenewcamaraderieonanequalbasisamongmembersatmeetings,quiteincontrastwiththestuffinessandhierarchical conservatism of the past.Theatmosphereisinformalandrelaxed.This spirit has also been carried downtothedaytodayadministrationoftheChamber with notable delegation ofresponsibility to the Secretary-Generalandallocationoffunctionstomembersofherteamtoofficiateatmeetingsandevents. In the old days, the Secretariatwas appreciated for its silent behind-the-sceneperformance.

Back to the November-December IN-TOUCH which set off these train ofthoughts, the cover page carries thephotograph of the Central MinisterreleasingtheMCCIStudyonPortSectorinTamilnadu.So,ithascomefullcircle.At its very start, the Chamber got theMadrasPortestablished.Now175yearslater,ithasenlargeditslogisticshorizonpushingforthedevelopmentofportsin

Tamilnadu to launcha thousand ships.Fullsteamaheadtothebicentenary!

(Mr C S Krishnaswami is the formerSecretary of The Madras Chamber ofCommerce&Industry)

OBJECTIVES: To awaken the peopleon the serious problem of hungeramong the poorest of the poor andinitiateactiontofeedthemostneedy,toprovide safewater, clothes, education,withparticularreferencetochildrenwithmalnutrition,undernourishedwomen

GOAL: To make India hunger free by2020

MOTTO: Concern, care, compassion,commitment and cooperation to servethehungriestcitizens

VISION:Tolightthelampofhopeandconfidence in themindsof thehungrypeople to leadnormal lifewithhumandignity

MISSION: ‘Care the uncared’, ‘Reachtheunreached’, ‘Feed theunfed’, Savetheunsaved’

SLOGAN: “SAVE THE FOOD ANDFEED THE POOR” , “MAKING INDIAHUNGER FREE IS THE SOCIAL ANDMORAL RESPONSIBILITY OF EVERYCITIZENWITHDIVINEBLESSINGS”

SHEhumblyappealstoallthecelebritiesin film, sports, music sectors andindustrialandcorporateestablishmentsto join handswith the society to lightthe lampofhopeand lifewithhumandignity among the poorest citizens.PleasecontactDr.V.RajagopalPresident,Tirupati phone number 0877-2287083mobile number 094412 00217 [email protected]

“Ifyoucannotfeedonehundredpersonsper day, feed at leastONE person perday”–MotherTeresa,NobelLaureate.

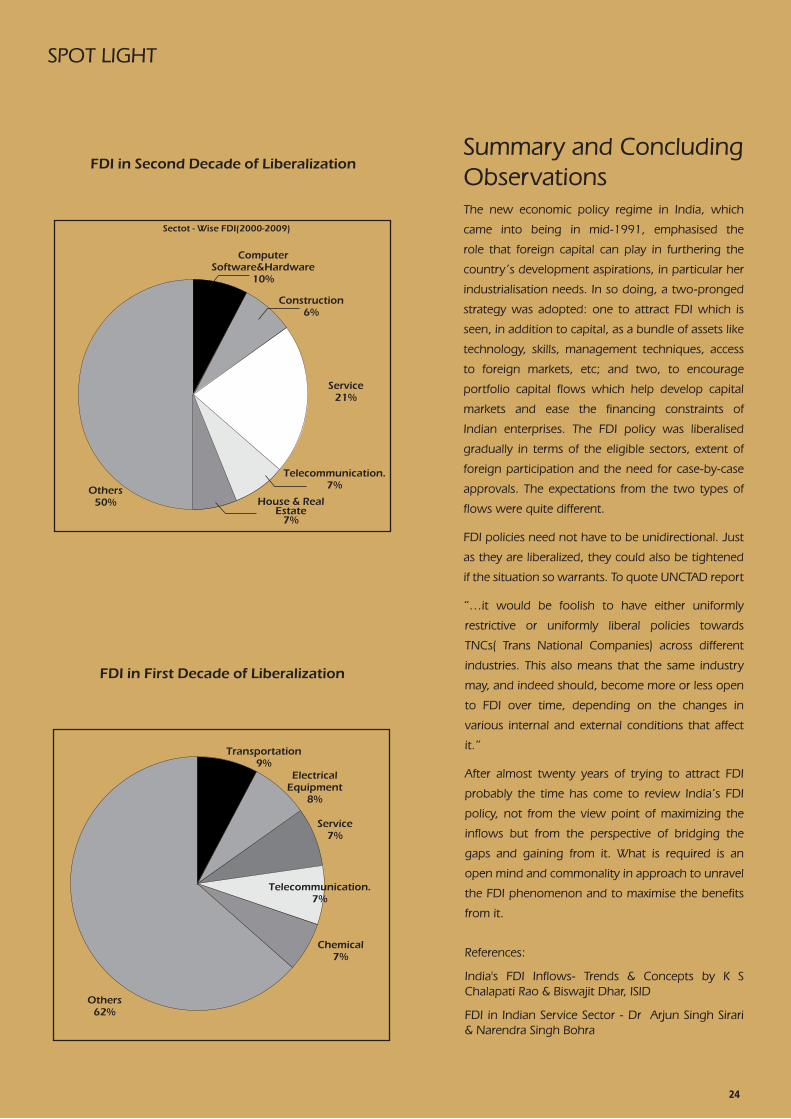

1.Macroeconomy1.1 Advance Estimation of Gross Domestic Product for 2011-12

Gross Domestic Product (GDP) at factorcost at constant (2004-05) prices in theyear2011-12is likelytoattaina levelofRs.52,22,027crore,asagainsttheQuickEstimatesofGDPfortheyear2010-11ofRs.48,85,954crore.ThegrowthinGDPduring 2011-12 is estimated at 6.9 percentascomparedtothegrowthrateof8.4percentin2010-11.

The growth rate of 6.9 per cent inGDP during 2011-12 has been due tothe growth rates of over 8 per centin the sectors of ‘electricity, gas andwater supply’, 'trade, hotels, transportand communication', and 'financing,insurance, real estate and businessservices'. Theremay be slow growth inthesectorsof‘agriculture,forestryandfishing’ (2.5%), manufacturing (3.9%)and construction (4.8%). The growthin the mining and quarrying sector isestimatedtobenegative(-2.2%).

Agriculture

The ‘agriculture, forestry and fishing’sector is likely to show a growth 2.5percent in itsGDPduring 2011-12,asagainstthepreviousyear’sgrowthrateof7.0percent.Productionoffoodgrainsis expected to grow by 2.3 per cent ascomparedto12.2percentgrowthinthepreviousagricultureyear.Theproductionofcottonandsugarcaneisalsoexpectedtoriseby3.3percentand1.6percent,respectively, in 2011-12. Among the

Themanufacturingsectorislikelytoshowagrowthof3.9percent inGDPduring2011-12asagainstthegrowthof7.6percent during 2010-11. According to thelatestestimatesavailableontheIndexofIndustrial Production (IIP), the index ofmanufacturingandelectricityregisteredgrowthratesof4.1percentand9.5percent,respectivelyduringApril-November,2011-12, as compared to the growthrates of 9.0 per cent and 4.5 per centinthesesectorsduringApril-November,2010-11.Theminingsectorislikelytoshow a negative growth of 2.2 percent in2011-12asagainstgrowthof5percentduring2010-11.TheIIPminingregisteredadeclineof2.5percent.Theconstruction sector is likely to show agrowthrateof4.8percentduring2011-12 as against growth of 8 per cent inthe previous year. The key indicatorsof construction sector, namely, cementproduction and steel consumptionhave registered growth rates of 5.3 percentand4.4percent,respectivelyduringApril-December,2011-12.

Services

The estimated growth in GDP forthe trade, hotels, transport andcommunication sectors during 2011-12 isplacedat11.2per centasagainstgrowth of 11.1 percent in the previousyear. This is mainly on account of

growthduringApril-November,2011-12of15.5percentinpassengershandledincivilaviation.Further,privatecorporatesector registered significant growth intrade,hotelsandrestaurantandbusinessservicesduringfirsthalfof2011-12.Therehasbeenanincreaseof28.0percentinstock of telephone connections as onDecember2011.Thesalesofcommercialvehicleswitnessedan increase of 19.2per cent per cent in April-December2011. The sector, 'financing, insurance,real estate and business services', isexpected to show a growth rate of 9.1per cent during 2011-12, on accountof 16.9 per cent growth in aggregatedeposits and 15.9 per cent growth inbankcreditduringApril-December2011(against the respective growth rates of28.0 per cent and 19.2 per cent in thecorresponding period of previous year).The growth rate of 'community, socialand personal services' during 2011-12 is estimated to be 5.9 per cent.

1.2 Export Growth in January 2012

India’sexportsforthemonthofJanuary2012 have registered a growth of10.1%, at US$ 25.4 billion. Imports fortheJanuary2012wereUS$40.1billionwith a growth of 20.3%. Balance ofTradestoodatUS$(-)14.7billionduringJanuary2012.April2011-January2012the export stood at 242.8 billion US $withagrowthof23.5%,ImportsfortheApril2011-January2012stoodat391.5billion US $ with the growth of 29.4%andApril2011toJanuary2012stoodat

26

ECONOMICREVIEW

(-)US$148.7billion.

During April 2011-January 2012, thefollowing sectors have done well viz.,engineering, (US $ 49.7 billion) whichregisteredthegrowthof21%,petroleum&oilproducts(48.9US$billion),50.1%,Gems&Jewelleryregisteredthegrowthof 33% (US $ 37 billion), Drugs andpharmaceuticals 21.1% (US $ 10.20billion US $), leather 23.4% (US $ 3.8billion)Cotton yarn and fabricmade-up14.7%(US$5.59billion),electronics(7.3billionUS$)13.4%,Readymadegarments21.5% ( US $ 10.9 billion), other basicchemicalsgrowsby29.6%withthe(US$8.8billion).

As regards to imports during April2011-January 2012, the growthestimates on the following sectors are:POL38.8%(US$117.9billion),Goldandsilver 46.6% (US 50 billion), machinery25.8% (US $ 28.8 billion), electronics22.9% (US $ 27.8 billion), Organic &inorganic chemicals23.6% (US $ 15.8billion)andcoal69%(US$14.1billion).

1.3 Industrial Production and use-based Index for December, 2011

IndexofIndustrialProduction(IIP)GeneralIndexforthemonthofDecember2011stands at 178.8,which is 1.8% higherascomparedtothelevelinthemonthofDecember2010.ThecumulativegrowthfortheperiodApril-December2011-12standsat3.6%overthecorrespondingperiodofthepreviousyear.

The Indices of Industrial Production fortheMining,ManufacturingandElectricitysectors for the month of December2011 stand at 136.2, 190.7 and 149.8respectively, with the correspondinggrowthratesof(-)3.7%,1.8%and9.1%as compared to December 2010. Thecumulativegrowth

inthethreesectorsduringApril-December,2011-12 over the corresponding periodof2010-11hasbeen (-)2.7%,3.9%and9.4% respectively, which moved theoverall growth in the General Index to3.6%.

As per Use-based classification, thegrowth rates in December 2011 over

December2010are4.0%inBasicgoods,(-) 16.5% inCapital goods and (-) 2.8%inIntermediategoods(StatementIII).TheConsumerdurablesandConsumernon-durableshaverecordedgrowthof5.3%and13.4% respectively,with theoverallgrowthinConsumergoodsbeing10.0%.

1.4 Tax Collection during April-January

Gross direct tax collection during April-January of the current fiscalwas up by14.57percent at Rs.4, 25,274 crore asagainstRs.3,71,188croreinthesameperiod last fiscal.While gross collectionofcorporatetaxeswasup11.87percent(Rs.2,85,837croreagainstRs.2,55,514crore last year), gross collection ofpersonal income tax was up by 20.43percent(Rs.1,38,730croreagainstRs.1,15,192 crore last year). Net direct taxcollections stood at Rs.3, 46,959 crore,upfromRs.3,17,500croreinthesameperiodlastfiscal,registeringagrowthof9.28percent.

Growthinwealthtaxwas45.11percent(Rs.682 crore against Rs.470 crore),whilegrowthinsecuritiestransactiontax(STT)was-27.19percent(Rs.4,145croreagainstRs.5,693crore).

2.CorporateSector

2.1 Revenue collection in the Current Fiscal

TheCentralBoardofExciseandCustoms(CBEC) has been able to achieve nearly80.74% of Budget Estimate up-to themonth of January, 2012 in the currentfiscalyear.Atthepresentrateofgrowth,CBECisoptimistictoachievethebudgettargets(Rs.3,92,908crore).

PleasereferTable5forrelevantfigures

The overall growth in indirect taxrevenuecollectionsduringthe monthof January, 2012 is around 7.2%.HowevertheprogressivegrowthduringApril-January of current fiscalyearhasshown 15.1% over the correspondingperiodoflastfinancialyear.ThegrowthinCentralExciserevenuehasbeennegativeforJanuary,2012.However,theoverallgrowth in Central Excise Revenue up

to January, 2012 is 6.8% showing apositivetrend.TheServiceTaxrevenuecollection continues to be buoyantand has shown 34.2% growth duringJanuary,2012.TheCustomsgrowthhasbeen2.5%duringthemonthofJanuary,2012, though the overall growth up toJanuary,2012hasbeen12.7%.

2.2 Railways Revenue Earnings up by 10.41 per cent during April 2011- January 2012

ThetotalapproximateearningsofIndianRailwaysonoriginatingbasisduring1stApril 2011-31st January 2012 wereRs. 84155.40 crore compared to Rs.76223.07croreduringthesameperiodlastyear,registeringanincreaseof10.41percent.

ThetotalgoodsearningshavegoneupfromRs.50916.21croreduring1stApril2010-31stJanuary2011toRs.56247.30crore during 1st April 2011 – 31stJanuary2012,registeringanincreaseof10.47percent.

The total passenger revenue earningsduring first ten months of the financialyear 2011-12 were Rs. 23345.48 crorecompared to Rs. 21336.88 croreduringthe same period last year, registeringanincreaseof9.41percent.

The revenue earnings from othercoaching amounted to Rs. 2353.55croreduringApril2011-January2012compared to Rs. 2093.62 crore duringthesameperiodlastyear,anincreaseof

12.42percent.

The total approximate numbersof passengers booked during April2011-January2012were6911.69millioncompared to 6577.15 million duringthe same period last year, showing anincreaseof5.09percent.Inthesuburbanandnon-suburbansectors, thenumbersofpassengersbookedduringApril2011-January2012were3651.87millionand3259.82 million compared to 3524.86million and 3052.29 million duringthe same period last year, showing anincrease of3.60per centand6.80percentrespectively.

![MCCI IN AN HOMOGENEOUS POOL: LESSONS LEARNT FROM …...benchmark [10] and from updated data presented in the final MCCI program report [4]. The temperature of upper walls receiving](https://static.documents.pub/doc/80x56/6075f4cd6c570d27650ff55a/mcci-in-an-homogeneous-pool-lessons-learnt-from-benchmark-10-and-from-updated.jpg)