25

Inception Workshop on Mainstreaming Gender into Trade Policy 21-22 April 2009, Addis Ababa Overview of Intra-African Trade By Daniel A. Tanoe NEPAD & Regional Integration Division, ECA

Inception Workshop onMainstreaming Gender into Trade Policy

21-22 April 2009, Addis Ababa

Overview of Intra-African Trade

By Daniel A. Tanoe

NEPAD & Regional Integration Division, ECA

Introduction

OUTLINE

Importance of Intra-African trade Africa’s export and import patterns Challenges of intra-African trade Some basic facts on Informal sector trade in

Africa

Why intra-African trade is important

AU vision - A common continental market for goods and services.

Common Market makes sense for Africa’s 53 mostly small economies.

Trade as an engine of growth

More trade within Africa – Retention of wealth

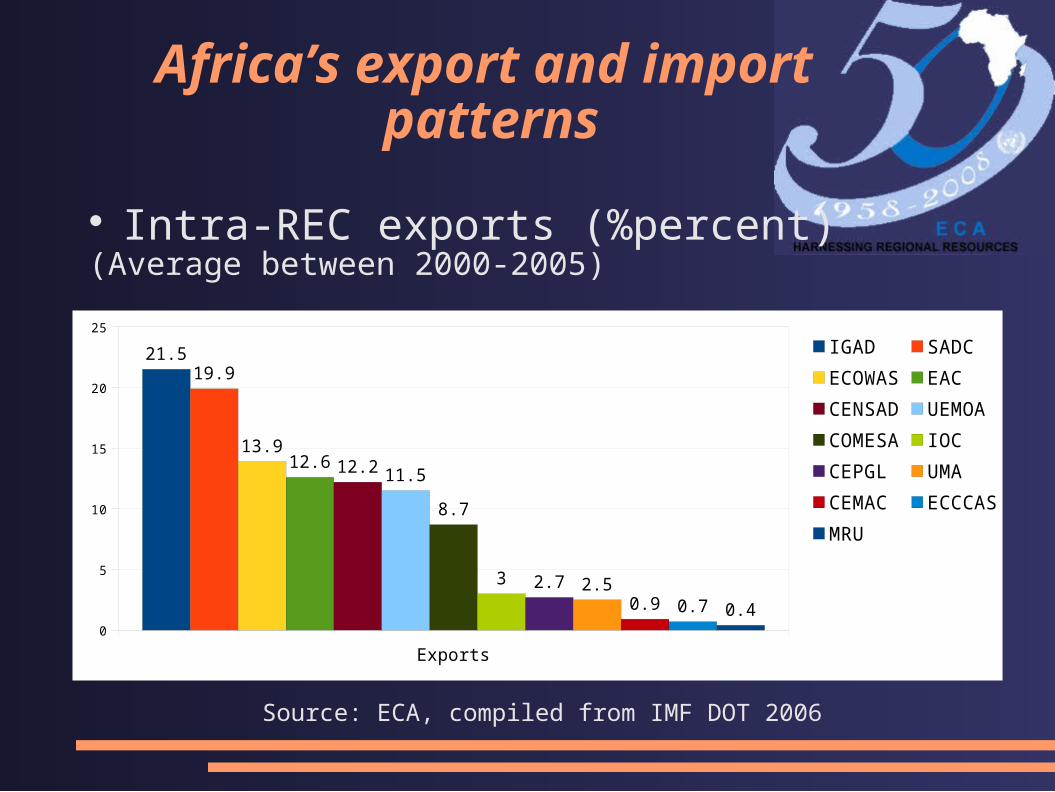

Africa’s export and import patterns

Africa's export and import patterns by RECs (Regional Economic

Communities)

Africa’s export and import patterns

Exports0

5

10

15

20

25

21.519.9

13.912.6 12.2 11.5

8.7

3 2.7 2.50.9 0.7 0.4

IGADSADCECOWASEACCENSADUEMOACOMESAIOCCEPGLUMACEMACECCCASMRU

Intra-REC exports (%percent)(Average between 2000-2005)

Source: ECA, compiled from IMF DOT 2006

Exports to the rest of Africa (%)((Average between 2000-2005))

Source: ECA, compiled from IMF DOT 2006

Exports0

2

4

6

8

10

12

14

16

18

2018.6

8.6

7.2

5.8 5.54.7 4.5 4.5

3.9

2.7 2.3 2.2 1.8

UEMOACOMESAEACIGADECOWASCEPGLUMACENSADMRUCEMACSADCECCCASIOC

Africa’s export and import patterns

Intra-REC imports (%)(Average between 2000-2005)

Source: ECA, compiled from IMF DOT 2006

Imports0

5

10

15

20

25

30

35 33.1

18.7

15.8 15.2 14.913

11.1

5.23.8 3.6 3.1

1.6 1.3

SADCEACECOWASIGADUEMOACENSADCOMESACEMACECCCASIOCUMACEPGLMRU

Africa’s export and import patterns

Imports from Rest of Africa (%)(Average between 2000-2005))

Source: ECA, compiled from IMF DOT 2006

Imports0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

35.5

17.215.1

14 13.7

9.9 9.4 8.9

6.45.2

3.62.6 1.7

CEPGLCOMESAIOCECCCASUEMOAEACMRUCEMACCENSADECOWASIGADSADCUMA

Africa’s export and import patterns

Africa’s export and import patternsGrowth trends

2000 2001 2002 2003 2004 2005

75

100

125

150

175

200

225

Intra-REC indices of export trends(base year = 2000)

CEMACCEPGLCOMESACENSADUEMOAIGADIOCECOWASSADCUMAEACECCASMRU

Africa’s export and import patterns

Intra-REC indices of export trends(base year = 2000)

REC 2000 2001 2002 2003 2004 2005CEMAC 100 121.88 139.34 152.07 181.15 206.98 150.24CEPGL 100 106.73 127.42 142.86 187.62 214.37 146.50COMESA 100 115.74 124.40 146.12 173.44 205.13 144.14CENSAD 100 100.20 132.67 140.09 171.83 212.30 142.85UEMOA 100 104.66 115.74 145.30 166.50 187.71 136.65IGAD 100 128.63 125.56 150.77 142.58 167.00 135.76IOC 100 126.66 99.43 169.01 146.22 150.14 131.91ECOWAS 100 81.93 114.31 109.74 157.13 196.99 126.68SADC 100 89.31 100.26 128.02 150.35 173.06 123.50UMA 100 103.89 109.88 122.29 125.61 172.31 122.33EAC 100 111.67 115.25 118.78 126.05 144.02 119.30ECCAS 100 106.63 104.26 103.66 124.93 142.74 113.70MRU 100 82.34 89.36 104.65 108.18 123.60 101.35

AverageGrowth

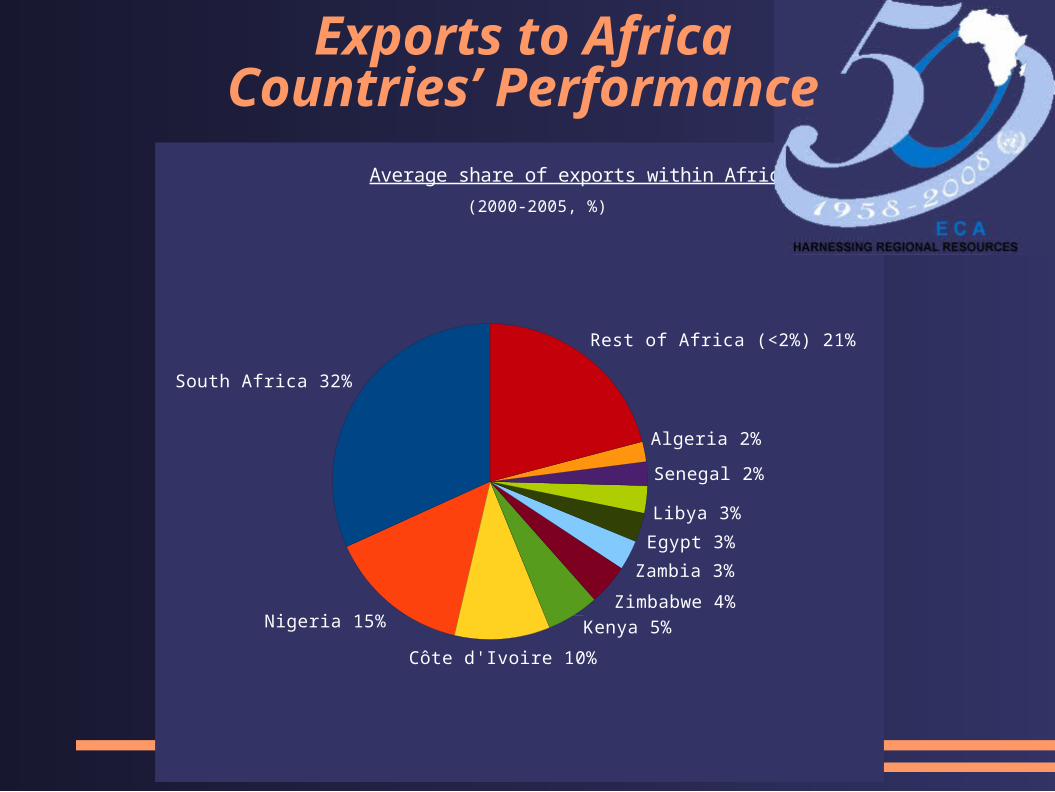

South Africa 32%

Nigeria 15%

Côte d'Ivoire 10%

Kenya 5%

Zimbabwe 4%

Zambia 3%

Egypt 3%

Libya 3%

Senegal 2%

Algeria 2%

Rest of Africa (<2%) 21%

Average share of exports within Africa

(2000-2005, %)

Exports to AfricaCountries’ Performance

Exports to Africa

Countries’ Performance Share of exports within Africa (%)(Average between 2000-2005

Country Exports Country Exports Country Exports Country ExportsSouth Africa 31.79 Togo 1.21 Congo, Rep. 0.37 Sierra Leone 0.05Nigeria 14.56 Tanzania 1.17 Congo, DR 0.34 Burundi 0.04Côte d'Ivoire 9.86 Uganda 1.1 Guinea 0.28 Rwanda 0.04Kenya 5.36 Djibouti 1.09 Burkina Faso 0.27 C.A.R. 0.04Zimbabwe 4.19 Mauritius 0.98 Madagascar 0.23 Cape Verde 0.00Zambia 3.07 Ghana 0.94 Sudan 0.18 Comoros 0.00Egypt 2.97 SACCA 0.92 Mali 0.11 São Tomé&P. 0.00Libya 2.79 Benin 0.8 Equatorial Guinea 0.08 Total 100Senegal 2.45 Gabon 0.8 Liberia 0.08Algeria 2.05 Mauritania 0.75 Seychelles 0.07 Source: ECA, compiledMorocco 1.86 Angola 0.69 Gambia 0.06 from IMF DOT 2006Tunisia 1.58 Malawi 0.58 Guinea-Bissau 0.06Cameroon 1.55 Ethiopia 0.51 Somalia 0.05Mozambique 1.49 Niger 0.5 Chad 0.05

South Africa 8%

Zimbabwe 7%

Zambia 6%

Ghana 6%

Côte d'Ivoire 6%

Nigeria 5%

Mali 5%

Mozambique 4%Morocco 3%Angola 3%

Kenya 3%Egypt 3%

Tanzania 3%

Uganda 3%

Libya 3%

Congo, DR. 3%

Senegal 3%

Cameroon 2%

Malawi 2%

Mauritius 2%

Rest of Africa (<2%) 18%

Average share of imports within Africa

(2000-2005, %)

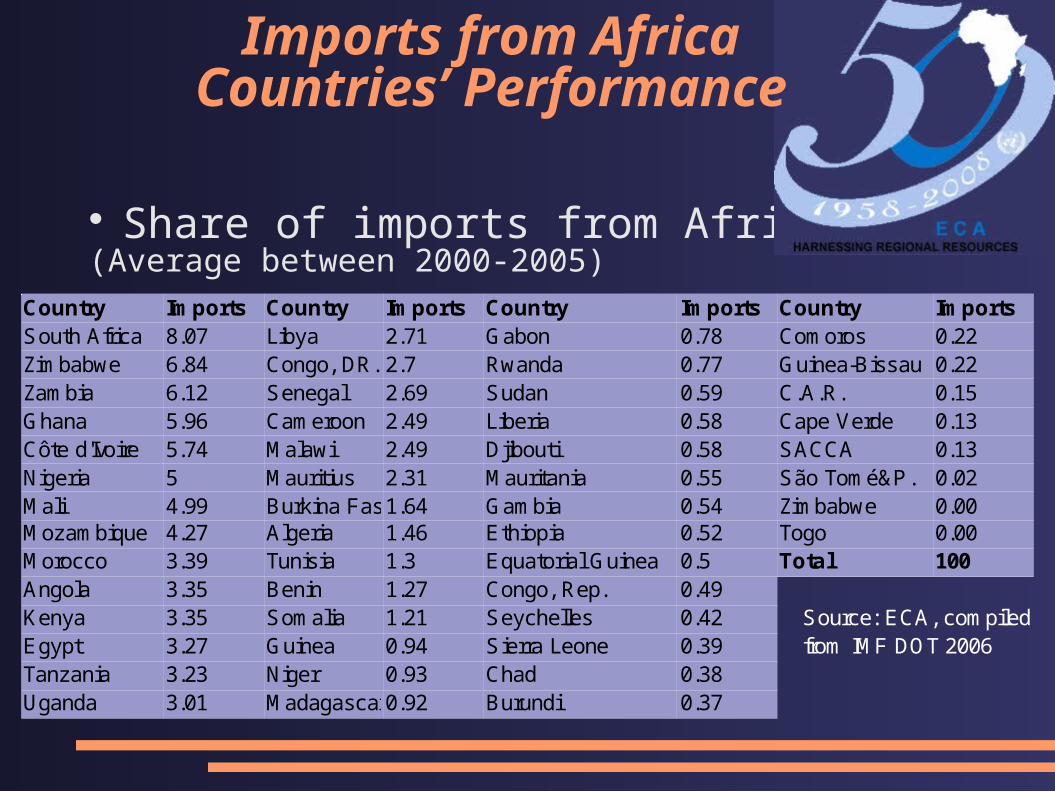

Imports from AfricaCountries’ Performance

Share of imports from Africa (%)(Average between 2000-2005)

Country Imports Country Imports Country Imports Country ImportsSouth Africa 8.07 Libya 2.71 Gabon 0.78 Comoros 0.22Zimbabwe 6.84 Congo, DR. 2.7 Rwanda 0.77 Guinea-Bissau 0.22Zambia 6.12 Senegal 2.69 Sudan 0.59 C.A.R. 0.15Ghana 5.96 Cameroon 2.49 Liberia 0.58 Cape Verde 0.13Côte d'Ivoire 5.74 Malawi 2.49 Djibouti 0.58 SACCA 0.13Nigeria 5 Mauritius 2.31 Mauritania 0.55 São Tomé&P. 0.02Mali 4.99 Burkina Faso1.64 Gambia 0.54 Zimbabwe 0.00Mozambique 4.27 Algeria 1.46 Ethiopia 0.52 Togo 0.00Morocco 3.39 Tunisia 1.3 Equatorial Guinea 0.5 Total 100Angola 3.35 Benin 1.27 Congo, Rep. 0.49Kenya 3.35 Somalia 1.21 Seychelles 0.42 Source: ECA, compiledEgypt 3.27 Guinea 0.94 Sierra Leone 0.39 from IMF DOT 2006Tanzania 3.23 Niger 0.93 Chad 0.38Uganda 3.01 Madagascar0.92 Burundi 0.37

Imports from AfricaCountries’ Performance

Africa’s export and import patterns

Africa’s merchandise exports

43%

20%

16%

9%

12%

Total merchandise(2005)

To EuropeTo N. AmericaTo AsiaTo AfricaTo ROW

Total Merchandise

From Africa Share2005 2000 2005

To World 297.7 100.00% 100.00%To Europe 127.8 50.30% 42.90%To N. America 60.2 17.30% 20.20%To Asia 48.6 16.40% 16.30%To Africa 26.5 9.80% 8.90%

ValueIn Billion $

Fuels and Mining Products Manufactured Products Agricultural Products

From Africa Share Share Share2005 2000 2005 2005 2000 2005 2005 2000 2005

To World 194.2 100.00% 100.00% 63 100.00% 100.00% 32.3 100.00% 100.00%To Europe 74.2 45.70% 38.20% 34.5 60.10% 54.70% 15.2 50.00% 47.20%To N. America 52.9 24.70% 27.20% 5.1 8.60% 8.10% 0.02 5.00% 6.30%To Asia 33.4 18.30% 17.20% 7.7 9.80% 12.20% 0.05 18.20% 15.30%To Africa 9.4 5.10% 4.80% 11.4 16.20% 18.10% 0.06 18.70% 17.10%

ValueIn Billion $

ValueIn Billion $

ValueIn Billion $

African merchandise exports

38%

27%

17%

5%13%

Fuels and Mining Products(2005)

To Europe

To N. America

To Asia

To Africa

To ROW55%

8%

12%

18%

7%

Manufactured Products(2005)

To Europe

To N. America

To Asia

To Africa

To ROW

47%

0%

53%

Agricultural Products(2005)

To Europe

To others

To ROW

Africa’s export and import patterns

Overall Intra-African Trade Picture

Persistently small intra-African trade, consistently under 15 per cent.

Dependence on developed countries

Heavy export reliance on fuels and minerals

Challenges of intra-African trade

Highlights

African countries desirous to encourage trade among themselves;

However, on the whole, with a few exceptions, not much progress has been made on intra-African trade;

Challenges of intra-African trade

Nature of African economies /Supply side

Inadequate trade related infrastructure

Trade facilitation challenges

Challenges of intra-African trade

Informal Sector tradein Africa: Some basic facts

Mainly unregistered trade across borders based on popular demand and supply

Often referred to as illicit trade or classified as smugglers Participants and beneficiaries are usually people and communities along

border lines and adjacent areas It terms of gender, it includes both female and men of all ages Large numbers of women are often observed transporting goods on their

backs and heads across borders Such unregistered trade is often not reported in national accounts and does

not pay tax Goods traded “informally” once in the country sometimes find

themselves in licensed/registered shops by registered traders Goods traded include agricultural products, clothing, shoes, electronics Informal sector traders are often subjected to harassment by customs

officers and police, and seizure of goods Financing of informal trade is mostly through own savings and credits

from friends and relatives as bank loans are not easily accessible to small traders.

Informal sector trade (Basic Facts contd)

Century-old practice People and communities of regions want to interact and trade without

governmental interference or requirement for formal registration for such trade

Informal trade sustains livelihoods and meets basic needs Failure of state in fulfilling the needs of the poor and border communities

compels informal trade Long distances from national central markets Alternate market outlets for better prices Avoidance of heavy taxes, customs duties, levies and other charges

including solicitation of bribery by Government officials Avoidance of stoppages and searches at several road blocs that may

involve unloading and loading even of people, causing waste of time.

Magnitudes of informal sector trade:

Difficult to give exact magnitudes because of its unrecorded nature

Available data mostly based on sample case studies & estimates from particular short periods, and thus the picture is mostly incomplete.

Some estimates suggest that the value of unrecorded/informal exports could be as high as 25% of total formal exports. (e.g. Informal cross-border trade survey report by Uganda Bureau of Statistics, June 2006.

Informal sector trade (contd)

Lessons

Lower customs duties and taxes on essential commodities

Improve customs procedures and remove non-tariff barriers

Systematically include issue of informal trade in bilateral and multilateral trade discussions/forums in RECs

Bring socio-economic development to border areas and rural communities

Remove frequent road blocs

THANK YOU