Terms of Reference • Indian Maritime perspective 2020 • India’s Bunkering Prospects •International bunker calls on Indian Ports •Coastal Shipping – bunkering aspects • Implications of Deadline 2020 on Bunker grades fuels • Indian Bunkering system changes and its Govt support • Indian Oil bunkering presence

Transcript

Terms of Reference

• Indian Maritime perspective 2020

• India’s Bunkering Prospects•International bunker calls on Indian Ports•Coastal Shipping – bunkering aspects

• Implications of Deadline 2020 on Bunker grades fuels

• Indian Bunkering system changes and its Govt support

• Indian Oil bunkering presence

2

Indian Maritime Perspective 2020

3

• National Maritime Agenda 2010-20- an ambitious plan

• Increase Indian tonnage four fold to 43 million Gross Tonnage

• Enhance port capacity to 3130 MMT by 2020

More than 50 per cent of this capacity to be created in the non-major ports.The projected capacity enhancement at the Major ports in 2017-18 to 1230 MMT ( 22% enhancement)

• Promote Coastal Shipping and facilitate IWT transport route

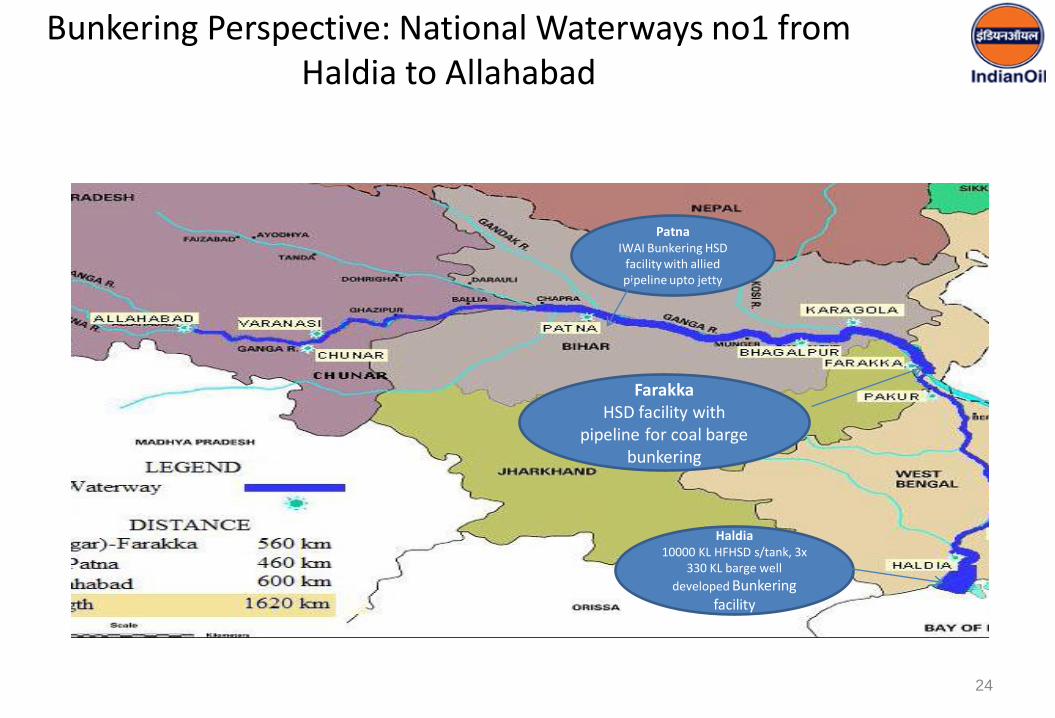

• For the development of inland waterways, an allocation of Rs.4,200 crore under a new project called Jal Marg Vikas (national waterways-I) on the Ganga river.

• The said project is expected to come up between Allahabad and Haldia to cover a distance of 1,620 km over a period of six years.

Shipping Corporation of India, Jindal,PSC, Allcargo, Essar Shipping,GESCO, Pratibha Shipping, etc.

ExplorationIn Rigs for powergeneration

HFHSDONGC, Reliance, Cairn Energy, AbanOffshore,

Vessels carrying rawmaterials

HFHSD ONGC, L&T, Punj Lloyd

Dredging In dredgersHFHSD, FO 380cst, FO 180cst, Lubes

DCI, Van Oord, ISDL, Mercator

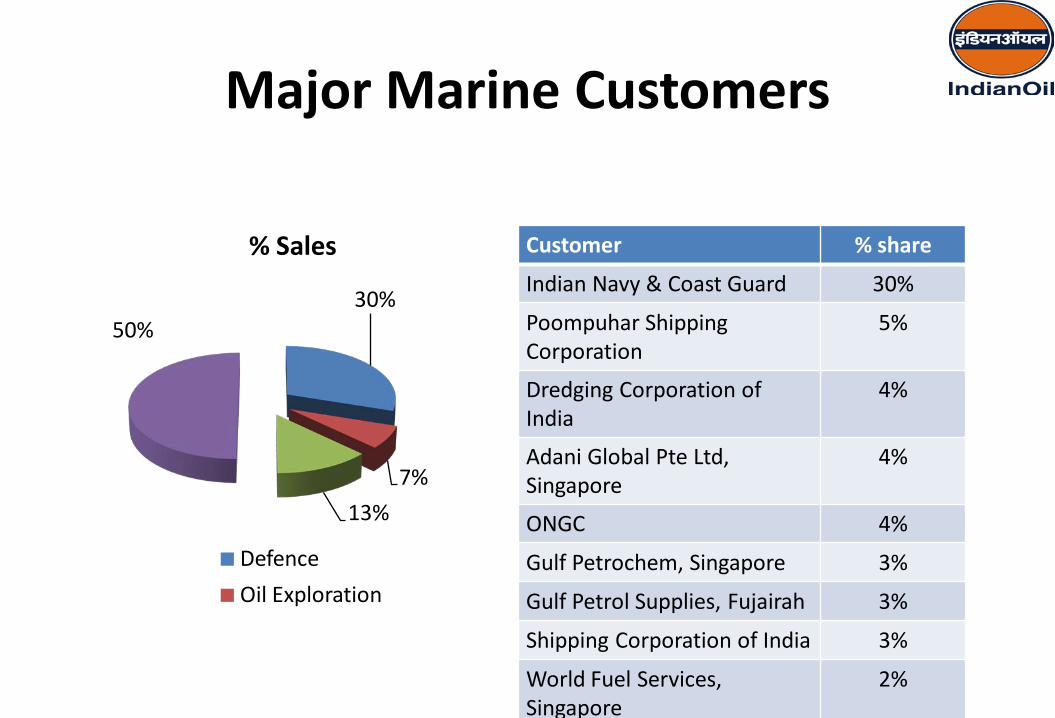

Major Marine Customers

30%

7%13%

50%

% Sales

DefenceOil Exploration

Customer % share

Indian Navy & Coast Guard 30%

Poompuhar Shipping Corporation

5%

Dredging Corporation of India

4%

Adani Global Pte Ltd, Singapore

4%

ONGC 4%

Gulf Petrochem, Singapore 3%

Gulf Petrol Supplies, Fujairah 3%

Shipping Corporation of India 3%

World Fuel Services, Singapore

2%

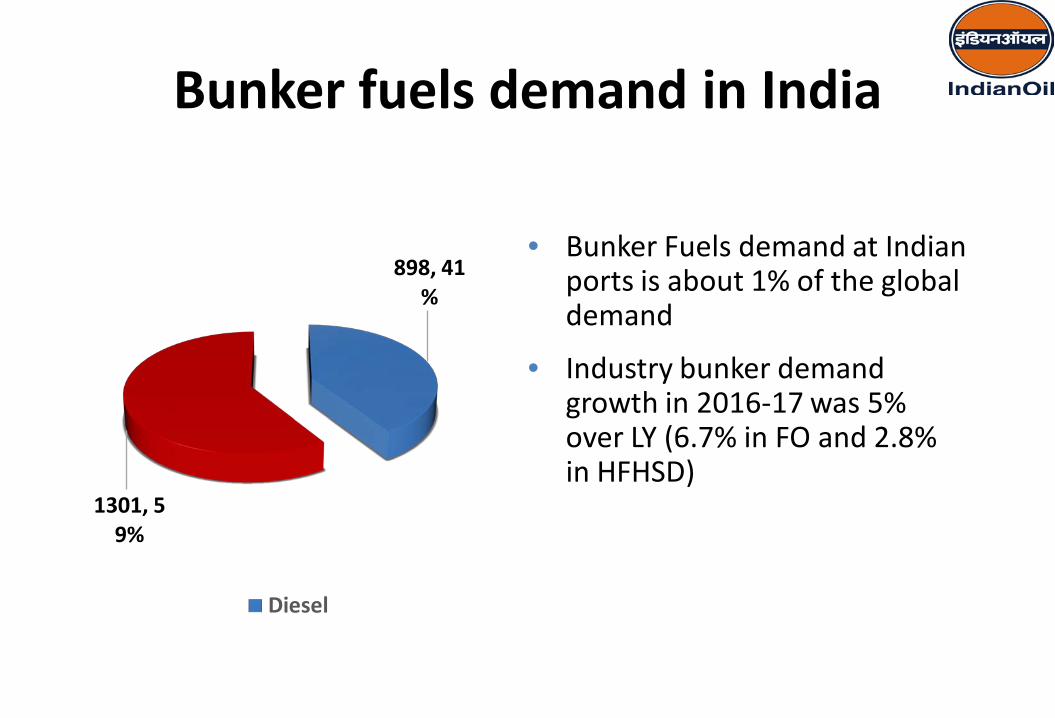

Bunker fuels demand in India

898, 41%

1301, 59%

Diesel

• Bunker Fuels demand at Indian ports is about 1% of the global demand

• Industry bunker demand growth in 2016-17 was 5% over LY (6.7% in FO and 2.8% in HFHSD)

Market share

41.6%

15.4%

10.1%

4.7%

2.2%1.1%

17.7%

2.9%4.2%

IOCHPCMXB/BPCMRPLRILEssarAdaniBharat Chemicals

• India : between two strong bunkering Hubs, Singapore and Fujiarah

• Distributed potential in India leading to multiple expenditure forcreating facilities for much lesser volume, whereas concentricpotential at Singapore & Fujiarah

•14

Indian Bunkering Challenges

IN D IAN OIL

15

Major Global Bunker Hubs : Singapore & Fujiarah

15Srilanka0.5 MMT

Singapore47 MMT

Fujairah24 MMT

INDIA2.1 MMT ( all types)

FO 380cst Price Compare 10.05.17

0

50

100

150

200

250

300

350

400

Singapore Fujairah Colombo Mumbai Cochin Haldia

FO 380cst USD per MT

Indian Maritime sector 2016-17• India has 7517 kms long

coastline with 12 major and about 200 minor ports

• During April – December 2016,– Major Ports registered a growth of

7.6%

– Minor Ports registered a growth of 14.8%

– Minor ports handled around 43% of the total maritime freight traffic of the country

Overall maritime traffic growth is

158.25

32.46

11.6

106.38

92.13

80.38

Cargo traffic (MMT)

POL Iron Ore F&RMCoal Container Other cargo

Market shift on cargo specific

IOC observed during 2016-17 that the bunker market in India shifted cautiously with bunkering interest at various ports .

Price , Quality , Quantity & Barging aspect –most important

With the introduction of FO 380cst at Haldia & Cochin, we have seen shift of Bunker Grade FO 380cst orders based on voyage pattern.

We have started FO 180 bunkering at Paradeepand Kakinada by barge.We have plans for finding ways thru import route at Managalore & TuticorinHence ….. Orders need to be converted through close assessment / follow up.

Major Cargo wise working and its overall business analysis will provide result . .

(source: world Port Source : http://www.worldportsource.com/ports/IND)

Indian Bunker Market Market Shift Impact

Major Cargo handled in Indian Ports

• Fertilizers, • Food Grain, • Sugar, • Paper And Newsprint, • Coking Coal, • Thermal coal• Petroleum Products• Metallurgical Coke, • Soda Ash, • Iron And Steel, • Limestone, • Machinery, • Scrap, • Vegetables Oil,• And General Cargoes.

• Food Grains, • Calcinated Petroleum Coke, • Jute And Jute Products, • Iron And Steel, • Pig Iron, • Tea,• Construction material• vehicles • Metal And Metal Products, • Machinery, • Mica, • And Other General Cargoes.

(source: world Port Source : http://www.worldportsource.com/ports/IND)

IMPORT EXPORT

Port-Kolkata : Study on Potential

(source: world Port Source : http://www.worldportsource.com/ports/IND)

Port Segment Description of Cargo Movement Expected Market(mainly of FO 380cst)

Coal Segment Thermal/Coking Coal coming mostlyfrom Australia & Indonesia which fallsenroute to Singapore (15-20 vsls permonth with average requirement pervsl per voyage 500 MT

8 TMT/month

POL Segment LPG Tanker 8-9 vsls per month 8 TMT/month

Port-Kolkata : Study on Potential

(source: world Port Source : http://www.worldportsource.com/ports/IND)

Port segment Description of cargo movement Expected market (mainly of FO 380

cst)Containersegment

operated between Chittagong,Kolkata/haldia,Colombo &Singapore 12 vsl/month averageon a regular basis. They are Pricesensitive having business shiftspread either toChittagong/Colombo/S’pore. Theyrequire credit of 30 days

3 TMT/month

Others segment At KoPT various types of cargomovement takes place being thelast port of call and impact ofcargoes movement to Nepal,Bhutan and some parts ofBangladesh through this port.

4 TMT per month

22

Coastal Shipping Penetration

23

Inland Waterways in India Cargo Movement only 0.5%

•National Waterway 1: Allahabad–Haldia stretch of the Ganga - Bhagirathi - Hooghly river system with a total length of 1,620 kilometers (1,010 mi) in October 1986.

•National Waterway 2: Saidiya–Dhubri stretch of the Brahmaputra river system with a total length of 891 kilometers (554 mi) in 1988.

•National Waterway 3: Kollam–Kottapuram stretch of the West Coast Canal along with Champakara and Udyogmandal canals, with a total length of 205 kilometers (127 mi) in 1993.

•National Waterway 4: Bhadrachalam–Rajahmundry and Wazirabad–Vijaywada stretch of the Krishna–Godavari river system along with theKakinada–Pondicherry canal network, with a total length of 1,095 km (680 mi) in 2007.

•National Waterway 5: Mangalgadi–Paradeep and Talcher–Dhamara stretch of the Mahanadi–Brahmani river system along with the East Coast Canal, with a total length of 623 km (387 mi) in 2007.

Implications of Deadline 2020 on Bunkergrades fuels

MARPOLAnnex VI Sulphur Regulations

• The IMO is enforcing a 0.50% limit on fuel sulphur content globally on 1 January2020, with a review in 2018 to decide if this deadline can be extended to 2025

Residual Max 1.5% Residual Max 1.0% Residual Max 4.5% Residual max 3.5%Distillate Max 0.1% Distillate Max 0.5% Distillate - Other 28

Source : Outlook for Marine Bunkers and Fuel Oil to 2025 by Marine & Energy Consulting and Energy Market Consultants

The World’s Bunker Market

Evolution of Marine Distillates

25.827.3

3032.2

8.2 7.8 7.1 6.6

2012 2015 2020 2025

Global Demand mb/d

Distillates Residual fuel

Marine Market -Demand shifting from Residual to Distillates

• Global Demand during 2012 to 2025: Distillates forecasted to increase by24%, while Residual fuel to decrease by 19%

• The demand for marine distillates will rise to 200- 250 million tons by 2020,versus today ‘s demand of about 30 million tons per yr

Global IMO -.5 % SulpurImplication

Source: OPEC

Source: OPEC

Implications of Deadline 2020

•Scrubbers•Exhaust Gas Recirculation (EGR)•Selective Catalytic Reactors (SCR)•Water injection – Humid Air Motors (HAM)/Water in Fuel (WIF)

Advance Technology / On board devices

•Decline in HFO consumption, Increase in Low Sulphur Distillates (<~ .5% ) - Price of Distillates expected to grow in future

Fuel Compliance

•LNG – expected share 11% by 2030 – 30% of New buildings with gas engine in 2020 – Price likely to be on high end of future projections •Bio-fuels•Methanol

Alternate Fuels

Three Scenarios for Compliance with the implications

Market information and implication of deadline 2020

•Certain alternate fuels are available for ECA areas(specs near to MDO)

•Cost benefit analysis to be evaluated from the suppliers/Market

•Number of days vessels trading in ECA area will also be governingfactors.

•Modification cost Vis a Vis alternate fuel cost will also be governingfactors .

•Do vessel need separate storage for alternate fuels?

32

Indian Bunkering system changes and itsGovt support

33

SuezHormuz

PanamaMalacca

Bosporus

Magellan

Good Hope

Gibraltar

Bab el-Mandab

Future of Bunkering in IndiaCochin on major vsl route – a strategic Location

Indian bunkering system –Changes in the concept• OPL bunker supply permission without callings charges –Cochin had

spearheaded and result is known

Floating permissions –an important step.

• Ports of respective State Governments will get additional wharfage on increased volume of supply.

• India will earn more foreign exchange as the payments are normally in term of US dollar.

• Subsidiary industries like barging cos/shipping agencies will increase which will result in more employment generation and more revenue to State Governments.

• Indian Ports will become the bunkering ports in international market, which will help to generate revenue to the port by way sales of fresh water/ship’s stores supplies etc.

35

Floating Bunker Station

Quantity as per Bunker Delivery Note

Capacity 5000-

8000 MT

Bunker FO 380cst HFHSD

Bonded & Duty Paid Supplies

Destination Cochin 0n the global traffic laneWorkability Diagram for Floating Bunker Station

Floating Bunker Station

Quantity as per Bunker Delivery Note

Capacity 5000-

8000 MT

Bunker FO 380cst HFHSD

Bonded & Duty Paid Supplies

West Bengal –Sand HeadWorkability Diagram for Floating Bunker Station

It is essential that bunker sales to foreign run vessels from indigenous production as well as imports –

a. Is treated as Export / Deemed Export under zero rated GST; orb. Provision in GST at a rate equivalent to Zero Excise Duties plus prevailing concessional VAT (i.e. Nil CGST/IGST plus concessional SGST)

B. Input Credit for GST on stock transfer

Stock transfer of products from one location to other, service tax is applicable on 30% of the transport cost. Application of GST rate on full transportation cost of product stock transfers would increase bunker prices considerably, again leading to foreign run vessels opting to take bunkers at other ports enroute in other countries, thus diminishing the marine bunker fuels demand at Indian ports.

Therefore in line with prevailing Service Tax regulations, GST input credit (equivalent to at least prevailing Service Tax rate on transportation) would be necessary on the stock transfer transportation in case of supplies to foreign run vessels.

C. Intermediate bonded storage

Under the present concept of intermediate bonded storage, product stock transfer from Refinery to the 1st transit storage location for onward positioning to various other ports coastally was permitted without payment of Excise Duties. GST implications on such stock transfers would increase bunker prices making them uncompetitive in the region.

Therefore in case of Bunker sale of products to foreign run vessels, 100% GST input credit is required for the products positioned from Refineries to the various port locations through such intermediate storage points.

GST in India -------- Impacts on Bunkering wef 01.07.2017

39

Indian Oil Bunkering Presence

• Indian Oil Corporation Ltd. is India's largest company by sales with a turnover of Rs. 3,99,601 crore (US$ 61 billion) and profits of Rs. 10,399 crore (US$ 1,589 million) for the year 2015-16..

• IndianOil is the highest ranked Indian company in the latest Fortune ‘Global 500’ listings, ranked at the 161th position.

• The IndianOil Group of companies owns and operates 11 of India's 23 refineries - with a combined refining capacity of 80.7 million metric tonnes per year

• IndianOil and its subsidiaries account for a 49% share in the petroleum products market, 35% share in refining capacity and 71% downstream sector pipelines capacity in India.

IN D IAN OIL

Indian Oil – At a Glance

Indian Oil – Bunkering Presence

Ports All India Bunkering ByIndian Oil

Bunkering ByOther Oil Co

Major National 12 12 8

Major Private 8 8 5

Other Minor 192 29 3

Port with bunker potential

212 49 16

42

IFO Bunkering by Barge started this month at Paradeep port

First IFO Bunkering to vessel MV Countess through Barge MT Dolphin.Bunkering operation was started in presence of Capt AK Mohapatra, Harbour Master PPT.

Shri. Pritish Bharat, GM IOC Odisha , Sti V Dhananjay, IOC DGM (CS), Bunker Order : 810 MTs of IFO180.

IFO & HFHSD Bunkering by Barge started this month at KAKINADA

Barge Bunkering for the first time ex.Kakinada Deep Water Port.

Marine Customer Segmentation

MGO (HFHSD) 530 TMT 2016-17

IFO384 TMT 2016-17

India’s Future

• Indian Refineries will have deficit situation for FO from 2018-19 onwards due to reduced production by Refineries

• Rationalization on product sharing can be carried out amongst Industry.

• Another option may be import of FO for supply to customers. Cost shall be the key deciding factor for the same.

• Indian Refineries will face a stiff challenge for production of 0.5% SulphurFO for Bunker grade as per MARPOL guidelines. Again cost shall be the major issue.

• Marine customers will slowly switch over to HFHSD from FO

Indian Oil aspire to work innovatively to emerge as amarket leader in bunkering, by maintaining highestcustomer service standards and committing to safeoperations to protect the environment through adedicated and empowered team in India