Page 1

Wahyu Winardi

Seventh High Level Tax Conference For Asian Countries

Tokyo, 5-7 April 2016

Directorate General of Tax (DGT) – Ministry of Finance of Republic of IndonesiaDeputy Director of VAT Regulation -Directorate of Tax Regulation I

Challenge and Solution

Page 3

3

Indonesia’s Tax Ratio

Tax Ratio

Relatively

Stagnant 12%

2,296

2,774

3,339

3,951

4,949

5,606

6,447

7,419

8,229

9,084

10,543

281 347 409 491 659 620 723

874 981 1,075 1,307

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

(Trillion Rupiah)

GDP (Curent LCU)

Tax Revenues (Inc. Customs &

Excise)

12% 13% 12%

12% 13%11% 11%

12% 12%12% 12%

Tax Ratio

Sources: Statistics Indonesia & Directorate General of Taxes

Page 4

4

Indonesia’s Tax Ratio

Source: World Bank

2007 2008 2009 2010 2011 2012

Cambodia 9.70 10.56 9.65 10.00 10.15 11.61

Indonesia 12.43 13.04 11.43 11.21 11.77 11.90

Lao PDR 11.59 12.10 12.76 12.93 13.68 14.83

Malaysia 14.30 14.66 14.94 13.33 14.79 15.61

Philippines 13.54 13.59 12.23 12.15 12.38 12.89

Singapore 12.89 13.85 13.07 12.97 13.30 13.82

Thailand 15.14 15.38 14.20 14.94 16.37 15.19

Average 12.80 13.31 12.61 12.51 13.21 13.69

0

2

4

6

8

10

12

14

16

18

Tax R

ati

o (

%)

Among ASEAN Countries

Sources: World Bank

Page 5

5

Indonesia’s Tax Structure

Sources: Statistics Indonesia & Directorate General of Taxes

-

500

1,000

1,500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Tri

llio

n R

up

iah

Share of Tax Revenue By DGT

Tax Revenues (Inc. Customs & Excise) Tax Revenue by DGT

Average 85% of Total

Tax Revenue

140

166

194

250

268

298

358

382

418

459

101

123

155

210 193

230

278

338

385

409

35 43 44

77

50 59

73 83 89 87

20 24 30 31 31 37 30 29 25 24

2 2 3 3 3 4 4 4 5 6

-

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Tri

llio

n R

up

iah

Structure of Tax Revenue (By DGT)

Non Oil & Gas Income Tax VAT & Luxury Sales Tax Oil & Gas Income Tax Land & Building Tax Other Tax

Page 6

6

Indonesia’s VAT Structure

Sources: Statistics Indonesia & Directorate General of Taxes

42%

0

50

100

150

200

250

300

350

400

2014 2015

Tri

llio

n R

up

iah

VAT Structure

Domestic VAT

Import VAT

Luxury Sales tax

Import Luxury Sales Tax

Other VAT

59%

59%

37%

36%

2% 3%

-

500

1,000

1,500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Tri

llio

n R

p

Share of VAT Revenue

Tax Revenues by DGT

VAT Revenues

42%

Page 7

7

Indonesia’s VAT Efficiency Ratio

33%

Sources: Statistics Indonesia & Directorate General of Taxes

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

GDP (Curent LCU) 2,774 3,339 3,951 4,949 5,606 6,447 7,419 8,229 9,084 10,543

VAT Revenues 101 123 155 210 193 230 278 338 385 409

VAT Efficiency Ratio 37% 37% 39% 42% 34% 36% 37% 41% 47% 51%

37% 37%39%

42%

34%36%

37%

41%

47%

51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

2,000

4,000

6,000

8,000

10,000

12,000

Tri

llio

n R

up

iah

VAT Efficiency Ratio

Page 8

8

33%

INDONESIA & DEVELOPING COUNTRIES

0,0 0,1 0,2 0,3 0,4 0,5 0,6 0,7 0,8

Madagascar

Zambia

Gabon

Guinea

Congo Republic

Uganda

Burkina Faso

Togo

Mauritania

Czech Republic

Slovak Republic

Poland

Indonesia

Romania

Sri Lanka

Nigeria

Bulgaria

Ghana

Paraguay

Thailand

Venezuela

Barbados

Mongolia

Croatia

Singapura

Source: OECD Factbook 2010: Economic,

Environmental and Social Statistics (2011), Revenue

statistics: Comparative tables, OECD Tax Statistics

(database) and Rate of VAT/GST from “The Modern

VAT”

Indonesia’s VAT Efficiency Ratio

Page 9

9

33%

INDONESIA & OECD COUNTRIES

0,0 0,2 0,4 0,6 0,8 1,0 1,2 1,4 1,6

Indonesia

Spain

Iceland

Norway

Ireland

Belgium

Italy

Poland

Chile

Sweden

France

Mexico

Slovak Republic

Greece

United Kingdom

Portugal

Czech Republic

Germany

Austria

Finland

Denmark

Netherlands

Turkey

Hungary

Luxembourg

Slovenia

Estonia

Australia

Israel

Korea

Switzerland

New Zealand

Japan

Canada

Source: OECD Factbook 2010: Economic,

Environmental and Social Statistics (2011), Revenue

statistics: Comparative tables, OECD Tax Statistics

(database) and Rate of VAT/GST from “The Modern

VAT”

Indonesia’s VAT Efficiency Ratio

Page 10

10

VAT Revenue - History

0

50

100

150

200

250

300

350

400

450

500

196

91

97

01

97

11972

197

31

97

41

97

51

97

61

97

71

97

81

97

91

98

01

98

11

98

21

98

31

98

41

98

51

98

61

98

71

98

81989

199

01

99

11

99

21

99

31

99

41

99

51

99

61

99

71

99

81

99

92

00

02

00

12

00

22

00

32

00

42005

200

62

00

72

00

82

00

92

01

02

01

12

01

22

01

32

01

4

TR

ILL

ION

RU

PIA

H

VAT

Regime

Sales Tax

Regime

Political Reform

1998

DGT

Modernization

2002VAT Law

Amandement-3

2009

Revamp

VAT Administration

2011 2019

Tax Reform 1985

VAT Law-

Amandement -2

2000

Page 11

11

Shadow Economy

No CountryCountry Average

1999/2007

1 Australia 14.6

2 China 13.5

3 Hong Kong 17.2

4 India 24.0

5 Indonesia 19.9

6 Japan 11.4

7 Korea, Rep. 28.2

8 Malaysia 31.3

9 New Zealand 13.2

10 The Philippines 45.1

11 Singapore 13.3

12 Srilanka 45.3

13 Taiwan 25.8

14 Thailand 54.7

Size of Shadow Economy in Asia-Pacific Countries

(% of GDP)

Source: New Estimates for the Shadow Economies all over

the World, Friedrich Schneider, Andreas Buehn, and

Claudio E. Montenegro, 2010

0 10 20 30 40 50 60

Australia

China

Hong Kong

India

Indonesia

Japan

Korea, Rep.

Malaysia

New Zealand

The Philippines

Singapore

Srilanka

Taiwan

Thailand

% (Percentage)

VAT Efficiency Ratio (Average 1999-2007)

Page 12

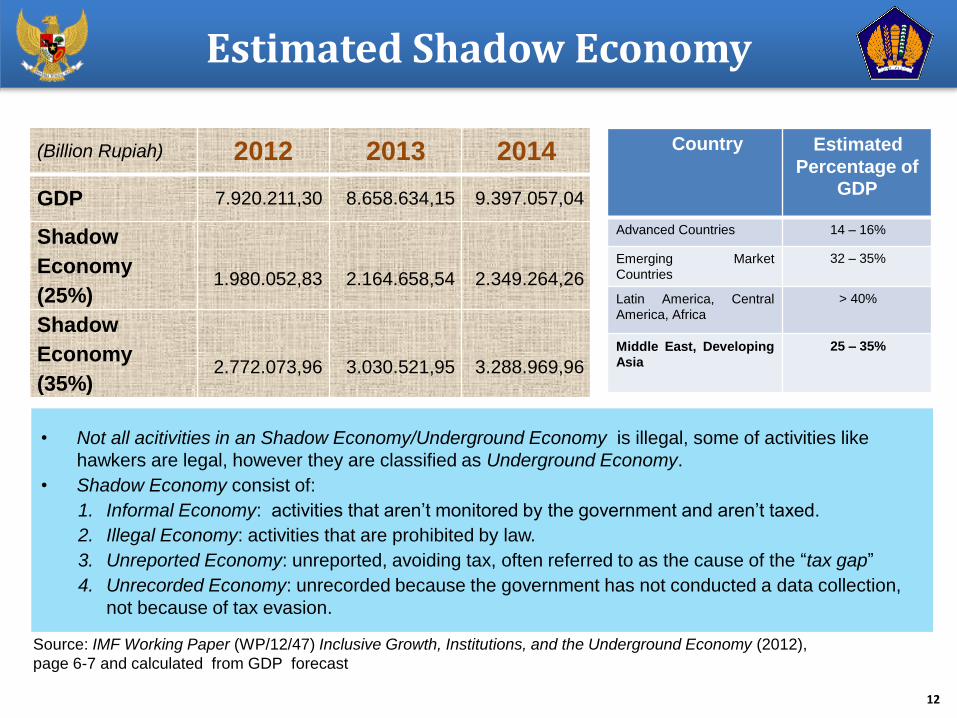

12

Estimated Shadow Economy

Source: IMF Working Paper (WP/12/47) Inclusive Growth, Institutions, and the Underground Economy (2012),

page 6-7 and calculated from GDP forecast

(Billion Rupiah) 2012 2013 2014

GDP 7.920.211,30 8.658.634,15 9.397.057,04

Shadow

Economy

(25%) 1.980.052,83 2.164.658,54 2.349.264,26

Shadow

Economy

(35%) 2.772.073,96 3.030.521,95 3.288.969,96

• Not all acitivities in an Shadow Economy/Underground Economy is illegal, some of activities like

hawkers are legal, however they are classified as Underground Economy.

• Shadow Economy consist of:

1. Informal Economy: activities that aren’t monitored by the government and aren’t taxed.

2. Illegal Economy: activities that are prohibited by law.

3. Unreported Economy: unreported, avoiding tax, often referred to as the cause of the “tax gap”

4. Unrecorded Economy: unrecorded because the government has not conducted a data collection,

not because of tax evasion.

Country Estimated

Percentage of GDP

Advanced Countries 14 – 16%

Emerging Market

Countries

32 – 35%

Latin America, Central

America, Africa

> 40%

Middle East, Developing

Asia

25 – 35%

Page 13

13

0 10 20 30 40

VA

T R

ate

Co

rpora

te

Inco

me T

ax

Ra

te

Pers

onal

Inco

me T

ax

Ra

te

VAT RateCorporate Income

Tax Rate

Personal Income

Tax Rate

Average 11.33 23.11 26.89

Vietnam 10 22 35

Thailand 7 20 35

Singapore 7 17 20

Philippines 12 30 32

Myanmar 30 25 20

Malaysia 6 25 26

Laos 10 24 24

Indonesia 10 25 30

Cambodia 10 20 20

Tax Rate Comparison - ASEAN

Risk to Tax Evasion

A distinct type of VAT evasion in

Indonesia is crediting VAT from

fictitious transaction.

In ASEAN, Indonesia’s tax rate is

considered moderate.

The tax regime and type of tax

administration influence the

decision of taxpayers to work in

formal or informal sectors

Page 14

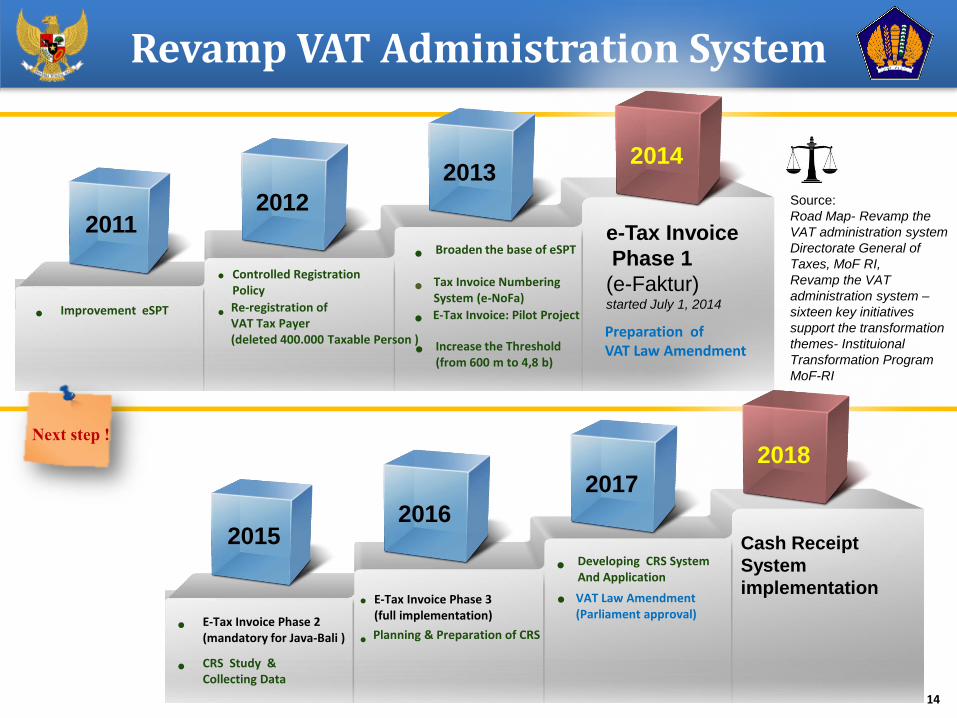

14

20122011

20142013

e-Tax Invoice

Phase 1

(e-Faktur)started July 1, 2014

• Improvement eSPT

• Controlled Registration Policy

• Re-registration of VAT Tax Payer(deleted 400.000 Taxable Person )

• Broaden the base of eSPT

• Tax Invoice Numbering System (e-NoFa)

• E-Tax Invoice: Pilot Project

• Increase the Threshold (from 600 m to 4,8 b)

20162015

2018

2017

Cash Receipt

System

implementation

• E-Tax Invoice Phase 2(mandatory for Java-Bali )

• CRS Study & Collecting Data

•

• Planning & Preparation of CRS

• Developing CRS System And Application

Source:

Road Map- Revamp the

VAT administration system

Directorate General of

Taxes, MoF RI,

Revamp the VAT

administration system –

sixteen key initiatives

support the transformation

themes- Instituional

Transformation Program

MoF-RI

• VAT Law Amendment(Parliament approval)

Next step !

E-Tax Invoice Phase 3(full implementation)

Preparation of VAT Law Amendment

Revamp VAT Administration System

Page 15

15

Implementation of e-Tax Invoice

Manual E-NoFa

Client Application

Web Application

ERP/ASP

2014 2015 2016

E-NoFa online via Web

2013

Development

Public announcement &education

Certain Taxable person LTO, Jakarta Special Regional TO,

Medium TOTaxable personJawa,Bali

All taxable personmandatory

Development

Development

Tax

Invoice

serial

number

Phase 1

Phase 2

Phase 3

Selection

method

for

taxable

person

obliged to

use e-tax

invoice

E-Tax Invoice Data Base Management

Channel

novJulima

r

Juli Juli JuliJan Jan JanJanJan

Procedures:

Regulation of

MoF,

Decision of

DGT

Test

Piloting / Trial Application

Page 16

16

Taxable Person Monitoring Program

Improve VAT

Administration SystemAn Early Warning

System of VAT Fraud

Maintain Taxable Person

Validity

Taxable Person Monitoring Program is an

application aimed to:

Page 17

17

Cash Receipt System (CRS)

1611, 85%

142, 8%138, 7%

Transaksi Tunai

Transaksi Kartu Kredit

Transaksi Kartu Debit

Cash Transaction

Credit Card Transaction

Debit Card Transaction

Source: Bank of Indonesia Year 2012

Total credit card and debit card

transactions in 2012 is Rp 280 trillion

Background to implement CRS:

to capture cash economy

Page 18

18

Summary of VAT Administration Improvement

RUU PPN

• Limiting or Getting

rate of exemption

• Broadening the

base(revised law and

regulation)

Improving

VAT Administration(e-administration)

•Audit

•E-Tax Invoice

Improving

VAT Monitoring

System(e-monitoring)

• Increase the

treshold of Rp 4,8 b(ensure only large

business with better

accounting system need

to register)

Implement

Cash Register

System

Increasing

VAT rate?How to increase revenue?

Page 19

19

Conclusion

Indonesia’s Tax Ratio is still considered

low compared to other ASEAN

countries

Indonesian Government have to deal

with Shadow Economy and VAT Fraud

to increase tax revenue, reduce tax

gap, as well as increase tax ratio

Page 20

Thanks For Your Attention

![Indonesia's Water Sector[1]](https://static.documents.pub/doc/80x56/55cf8ac255034654898d86fc/indonesias-water-sector1.jpg)