24

Infrastructure investments An attractive option to help deliver a prosperous and sustainable economy

Infrastructure investments An attractive option to help deliver a prosperous and sustainable economy

C ontentsE xecuti v e summary0 3

Introducti on0 4

C urrent state of the i nfrastructure i nv estments market0 7

T he ev olv i ng reg ulatory cli mate — current req ui rements and Solv ency II1 2

O perati onal manag ement of i nfrastructure assets1 7

Appendi x2 1

C onclusi on2 2

3Infrastructure investments

In today’s low-yield environment, insurers are under increasing pressure to source additional investment return. Infrastructure investments may present an opportunity for insurers to achieve the required yields to cover future liabilities and provide competitively priced products. This is due to the fact that typical loans have historically outperformed comparative traditional investments.

In particular, the treatment of infrastructure loans under risk-based capital regulatory regimes, such as Solvency II, could be attractive relative to more traditional institutional investments. However, one should note that, although the capital charge may not necessarily inhibit this investment, a treatment that reflects the underlying economic risk of the asset class will likely enable insurers to commit more money to the sector.

Infrastructure investments are an interesting option for an insurer’s portfolio, as they provide:

• Potentially lucrative risk-adjusted return on equity

• Long-term risk exposure, which may provide a good match for long-term liabilities

• Illiquidity and sector-diversity, which could increase portfolio diversification

• An opportunity to lend money to sectors in need of funding, leading to social and potentially reputational benefits

There are practical issues, however, which an insurer should consider prior to investment, including:

• Determining whether margins are sufficient to cover the costs and risks associated with operational complexities, such as sourcing, managing and pricing infrastructure investments

• Putting in place suitable processes to assess and manage infrastructure debt investment

• Investing in infrastructure that is best suited to their balance sheet and risk profile (these opportunities have been limited because issuances have historically been influenced by banking requirements)

As a result of these considerations, the insurance industry has made only a marginal investment in the infrastructure sector in recent years. However, there is increasing interest as insurers find that the benefits of infrastructure assets outweigh the apparent costs relative to the low yields available on more traditional investments.

The typical annual benchmark spread achieved by infrastructure investments is comparable to A- and BBB-rated corporate bonds of a similar duration (as indicated by our analysis in this paper) with spreads ranging from 125–160bps for non-publicly rated private finance initiative (PFI)/public private partnership (PPP) infrastructure considered of A to BBB

Executive summary

credit quality by lenders. These relatively competitive spreads may be seen as attractive, with our analysis indicating that the achievable return on equity may be greater than that for A- or BBB-rated corporate bonds of a comparable duration under the Solvency II regulatory regime.

However, the source of preferred insurer investments has been limited. Increased interest in a concentrated sub-sector of the market has contributed to tightening margins on the most attractive investment opportunities. Therefore, insurers should understand the requirements of the infrastructure market to suitably influence the availability and attractiveness of investments.

In this paper, we have identified a selection of historic deals and pipeline opportunities which may be well suited to an insurance investor. We explore the operational complexity of such an investment, and analyze the materiality of such risks, including the possible mitigation options available to insurers.

4 Infrastructure investments

The definition of the infrastructure asset class can be very broad. One definition is “facilities or structures required for the effective operation of a business, state or economy.” In this paper, we define i nfrastructure to i nclude roads, rai lw ay s, ai rports, pow er g enerati on and transmi ssi on, ports, communi cati ons, w ater and w aste, tog ether w i th soci al i nfrastructure, such as hospi tals, schools

I ntro duc tio n

T y pes o f inf rastruc ture

D esc riptio n Ex ampl es

Greenfield or brownfield

Greenfield projects involve an asset or structure that needs to be designed and constructed, w here no i nfrastructure or bui ldi ng prev i ously exi sted. Inv estors fund the bui ldi ng of the i nfrastructure asset and the mai ntenance w hen i t i s operati onal.

T he G emi ni offshore w i nd farm proj ect i nv olv es the constructi on of tw o w i nd farms w i th a combi ned capaci ty of 6 00MW i n the N orth Sea, off the coast of the N etherlands. It has an esti mated completi on date of Q 4 2016 and a v alue of $ 3. 35b. 1

Brownfield projects involve an existing asset or structure that requires improvement, repair or expansion (i.e., land where a building or construction already exi sts). T he i nfrastructure asset or structure i s usually parti ally operati onal and may already be g enerati ng i ncome.

T he 7 . 5km road i mprov ement of the A556 trunk road betw een K nutsford and Bow don i n the U K , creati ng a modern dual carri ag ew ay road. T he i mprov ement w orks are expected to be completed by 2017 at a cost of betw een £ 16 5m and £ 221m. 2

C onstructi on (primary) or operati onal (secondary) phase

P ri mary i nfrastructure i nv estments are those made at the pre-operati onal or constructi on phase, before most rev enue i s g enerated. H i g her ri sk i s associ ated w i th constructi on-phase proj ects due to completi on and usag e ri sks.

The risk-return profile of infrastructure, which is complex to construct, is similar to hi g h-ri sk v enture capi tal proj ects. H ow ev er, the ri sks i nv olv ed i n proj ects w i th a more typical construction phase (such as schools and hospitals) are often bank-debt funded, and are low er ri sk than speculati v e constructi on proj ects g i v en that they are subj ect to g reater controls. N ote that a pri mary i nv estment could be either greenfield or brownfield.

The Johan Sverdrup Oil Field Development in Norway, w hi ch i s expected to be completed i n Q 4 2019 . T he cost of the dev elopment i s $ 28 . 6 b and i nv olv es installation of four fixed platforms and infrastructure to export oi l and g as. 3

Secondary i nfrastructure i nv estments apply to the operati onal stag e of a proj ect. T here i s a low er ri sk as constructi on has been completed and usag e lev els hav e been establi shed; the ri sk also reduces ov er ti me i f the proj ect has prov en to be rev enue g enerati ng . T hi s phase offers reli able long -term returns, althoug h i t still carries significant ongoing management challenges. Note that a secondary investment could be either greenfield or brownfield.

T he Marmaray P roj ect i s a 7 6 km subterranean rai lw ay dev elopment under the Bosporus Strai t i n T urkey . T he proj ect beg an i n 2004, w i th the i ni ti al phase completed i n 2013, follow i ng multi ple delay s due to archaeolog i cal sensi ti v i ty . 4

Av ai labi li ty - or demand-based

Av ai labi li ty -based proj ects are ty pi cally w here the g ov ernment, or some other sponsor, procures essenti al faci li ti es or serv i ces i n return for pay ments li nked to availability rather than usage levels (this obligation is defined in the terms of the i nv estment contract).

Av ai labi li ty -based i nv estments are ty pi cally low er-ri sk i nv estments w hereby eq ui ty cash flows can be debt like in their certainty and timing given that the exposure is to the sponsor rather than the profitability of the project. There is often an element of performance risk in the cash flows of availability-based projects, ty pi cally v i a performance-related deducti ons from the composi te pay ment. P roj ects usually i nclude schools, hospi tals and g ov ernment accommodati on.

T he G y stadmarka Secondary School P P P proj ect i n the U llensaker Muni ci pali ty , N orw ay , i s an example of a greenfield availability-based project.5

Demand-based proj ects are w here the i nv estor bears the rev enue ri sk of the project (i.e., the investor’s income relies on the ability of the project to generate cash). These projects vary widely in risk profile; often they have inflation-linked returns w i th g reater exposure to economi c ri sk and tend to be long term, hence uncertai n i n the future.

T he P edemontana L ombarda H i g hw ay i n Italy i s a demand-based proj ect and i s under the manag ement of Itali an concessi on company Autostrada P edemontana Lombarda. It is a brownfield project with an estimated v alue of $ 6 . 3b. 6

and housi ng . T here are a number of di fferent ty pes and common characteri sti cs of i nfrastructure i nv estments, w i th opportuni ti es i n the pi peli ne that may be attracti v e to an i nsurer.

Sev eral common di sti ncti ons w i thi n the i nfrastructure asset class are highlighted in Figure 1.

F ig ure 1 : D if f erent ty pes o f inf rastruc ture asset c l asses

T y pes o f inf rastruc ture

D esc riptio n Ex ampl es

C orporate enti ti es or concessi on structures

C orporate enti ti es i nclude uti li ty compani es, toll road operators and ai rport compani es, w hose rev enues are ei ther economi c or reg ulated. Many i nfrastructure corporate entities generate revenues that are broadly linked to inflation. C orporate enti ti es tend to be less lev erag ed than concessi on structures and debt i s typically more liquid (due to higher volumes of debt issuance in the market).

T he M6 toll road i n the U K w as opened i n December 2003. Midland Expressway Limited (MEL) is a private company w i th a g ov ernment concessi on to desi g n, bui ld, operate and mai ntai n the 27 mi les of the M6 toll road unti l 2054. 7

C oncessi on structures i nv olv e debt w hi ch i s ty pi cally secured on phy si cal assets or contracts. Some concessi on structures also prov i de for i ndex-li nked cash flows, which can be financed by index-linked bonds. Included within concession structures are government initiatives, such as PPPs and PFIs:

• PPPs help transfer financing risk of major infrastructure developments from the publi c to the pri v ate sector. Infrastructure has been dev eloped throug h P P P models w orldw i de.

• The PFI method is a form of PPP initially developed by Australia and the UK and adopted i n a number of E uropean countri es. It i s the most common method of using private capital to finance public infrastructure projects. The sectors within the infrastructure portfolio that fall under the UK Government’s PFI regime are educati on, healthcare, soci al housi ng and the Mi ni stry of Defence.

Such proj ects are characteri zed by a long -term commi tment from the publi c sector to pay a pre-ag reed i ncome, so long as a certai n publi c serv i ce i s deli v ered according to specification. This service is typically delivered by a private sector operator and, as such, pay ments made may be affected subj ect to operator performance.

Accordi ng to 2014 g ov ernment summary data, 8 there are 728 PFI projects in the UK, of which 671 are operational. The capital value of these PFI deals totals £ 56 . 6 b, an i ncrease of £ 2. 4b from 2013. An example of a PFI project currently in operation is the Oldham Sheltered Housing PFI Project, worth £400m over a 30-y ear concessi on peri od.

An example of a P P P proj ect i n E urope i s the Marsei lle L2 Motorways project in France. The financing for this availability-based PPP was confirmed in October 2013 and was the largest infrastructure financing in France i n 2013. 9

Debt or eq ui ty i nv estment

Debt is usually secured on physical assets and/or contracts and as such the cash flows are generally stable and secure. Debt will typically make up 80%–90% of a proj ect’ s capi tal req ui rement. T here are ty pi cally a number of borrow er opti ons embedded i n proj ects w hi ch add to the operati onal complexi ty of these investments. For example, prepayment risk exists with debt investments, which can be mi ti g ated v i a a sui table Spens clause.

T he 8 0MW K i zi ldere III G eothermal P lant proj ect i n Turkey has a debt to equity financing ratio of 89:11. Equity financing of $30m is to be provided by the Zorlu Group, with $250m of debt financing to be sourced.10

Equity investors receive the remaining cash flows from projects after deducting operati ng costs and i ncome used to serv i ce debt i nv estors. T hus, eq ui ty i nv estors have a leveraged exposure and are subject to more volatile cash flows and asset v aluati ons.

Equity will typically comprise 10%–20% of a project’s capital requirement. Equity is frequently structured as subordinated debt and may be provided by a financial i nv estor, as opposed to an operator or sponsor.

T he 22. 6 6 MW R eckahn 1 Solar P V P lant i n G ermany has a debt to equity ratio of 90:10. Debt financing of $ 6 3m i s to be prov i ded by Bay ernL B, w i th $ 8 m of equity financing from Commerz Real AG.11

5Infrastructure investments

Despi te the di v ersi ty w i thi n thi s asset class, there are a number of key characteri sti cs w hi ch are present i n most i nfrastructure investments (see Figure 2). As these features are fundamental,

T y pic al c h arac teristic s C o nseq uenc es f o r an insuranc e inv esto r

R eq ui re a larg e i ni ti al capi tal outlay or hav e materi al ong oi ng capi tal expendi ture needs

Insurers need to have sufficient funds available to meet the initial demands of investment, together with prov i si ons throug hout the proj ect to meet ong oi ng capi tal expendi ture demands.

Inv olv e long durati on contracts of v ary i ng complexi ty T he long durati on of contracts i s a natural match for the long -term nature of the li abi li ti es of li fe i nsurance and pensi ons. T he complexi ty of contracts req ui res dev elopment of an opti mal operati onal manag ement strateg y .

Yield stable, predictable, long-term cash flows (up to 35 years or more) which may be inflation-linked

Stabi li ty and long -term predi ctabi li ty makes i nfrastructure a potenti ally attracti v e proposi ti on for i nsurers, parti cularly should such assets sui tably match thei r li abi li ti es and help to opti mi ze the matchi ng adjustment. Debt cash flows are often not linked to inflation due to poor correlation between prevailing inflation and risk-free benchmarks (e.g., London Interbank Offered Rate (LIBOR)). Despite this, many projects (in theory) have inflation-linked cash flows.

Cash flows are often influenced by a regulatory regime set by a government or sponsored/subsidized by a g ov ernmental or q uasi -g ov ernmental body

T he long -term nature of contracts i ncreases the probabi li ty of exposure to a maj or chang e i n reg ulati on. Insurers should consi der mi ti g ati ng such ri sks accordi ng ly throug h careful contract neg oti ati ons before committing to invest. For example, in 2013, the Spanish Government cut subsidies for renewable energy i n i ts recent w av e of austeri ty measures, fundamentally affecti ng the returns av ai lable on renew able i nv estments. 12

Returns should, with some exceptions (e.g., toll roads), be relati v ely uncorrelated to the busi ness cy cle

V ari ati ons i n the busi ness cy cle should not materi ally i mpact expected returns on i nv estments.

Frequently monopolistic or quasi-monopolistic This makes such investments difficult to source but potentially lucrative once secured.

E IO P A hav e proposed a number of characteri sti cs w hi ch i nfrastructure debt and eq ui ty must sati sfy i n order to benefit from a reduced standard formula risk charg e. T hese characteri sti cs are explored further i n thi s paper.

An i nsurance i nv estor may be i ncli ned to focus on i nfrastructure i nv estments w hi ch sati sfy E IO P A’ s proposed qualifying criteria due to the material benefit it may yield under the standard formula. However, note that a g ood supply of such i nfrastructure i nv estments i s req ui red to mai ntai n competi ti v eness w i th other asset classes.

F ig ure 2 : T y pic al c h arac teristic s o f inf rastruc ture and th e c o nseq uenc es f o r an insuranc e inv esto r

6 Infrastructure investments

i t i s cruci al to assess the relati v e adv antag es and di sadv antag es for each characteri sti c from an i nv estor’ s perspecti v e.

7Infrastructure investments

C urrent state o f th e inf rastruc ture

inv estments mark et

Insurers hav e become more w i lli ng to take on new i nv estment ri sks and are li kely to consi der percei v ed low er-ri sk av ai labi li ty -based (or social) senior infrastructure debt assets. In particular, they are attracted to i nfrastructure assets prov i ded throug h P P P and PFI models, as these are issued by sub-sovereign entities and prov i de i mpli ci t g ov ernment support. T he relati v e securi ty of these i nv estments i s somew hat dependent on the sub-sov erei g n entity, with certain sectors (e.g., school and hospital trusts) faci ng substanti al poli ti cal pressure not to fai l. T he safety of such investments under a stressed scenario is difficult to determine, as i t i s partly reli ant on the acti ons and pri ori ti es of the relev ant g ov ernment.

UK insurers intend (and have already begun) to invest approxi mately £ 25b i n i nfrastructure i nv estments betw een 2013 and 2018 . 13 A recent example i s the £ 200m C onsumer P ri ce Index (CPI)-linked bond purchased from the Greater London Authority by Rothesay Life, which is the UK’s first CPI-linked sterling bond.14 T hi s deal demonstrates how i nfrastructure i nv estments can prov i de natural inflation hedges, which could be attractive for insurers wishing to match inflation-linked liabilities.

As the demand for i nfrastructure loans has i ncreased, how ev er, the available yield has narrowed significantly. This has led some i nsurers to consi der i nv estment i n i nfrastructure loans that carry greater risk. For example, insurers have started to fund i nfrastructure loans duri ng both pri mary and secondary phases of proj ects; i n parti cular, thei r preference for long -term lendi ng encourag es prov i di ng funds throug h both phases.

L oans are ty pi cally i ssued for the enti re term of a proj ect; thoug h, it is often the case that private equity companies (or the equivalent)

provide financing for the primary phase and capital markets finance the secondary phase. C api tal markets are comfortable accepti ng the project risk during this phase because of the collateral (i.e., the underly i ng i nfrastructure asset).

A compari son to tradi ti onal assetsThe Infrastructure Index (produced through EY proprietary analysis of Reuters data) shown in Figure 3 has been constructed as the average spread of five infrastructure bonds across different sectors. It i s i ndi cati v e of the performance of a ty pi cal i nfrastructure asset that an insurer may invest in, specifically PFI/PPP infrastructure assets rated A to BBB. T he av erag e term of the Infrastructure Index i s 20 y ears. It i s i mportant to note the challeng es i n constructi ng such an i ndex due to the li mi ted av ai labi li ty of data. T hi s i s relev ant to i nv estors, as they may be faced w i th li mi ted i nformati on w hen commi tti ng to i nfrastructure i nv estments.

Figure 3 shows the available spread for typical assets which an i nsurance company may hold. It i s i nteresti ng to note that the spread of the Infrastructure Index at 1 March 2015, constructed from a number of i nfrastructure bonds, falls betw een the annual benchmark spread av ai lable on A- and BBB-rated corporate bonds for terms of 10– 15 y ears. 15 T hi s sug g ests that the spread av ai lable from i nfrastructure i nv estment i s competi ti v e w hen compared to other more tradi ti onal assets despi te the narrow i ng of spreads si nce the beg i nni ng of 2014.

T he compari son i s w i th respect to i nfrastructure bonds, as opposed to i nfrastructure loans. It i s li kely that i nv estments i n i nfrastructure loans w ould be rew arded w i th an addi ti onal i lli q ui di ty premi um, g i v en that loans are not publi cly li sted, so less i nformati on i s readi ly

8 Infrastructure investments

av ai lable to prospecti v e i nv estors. T hi s addi ti onal premi um may reflect the fact that infrastructure loans may be structured in a more flexible way as they do not have to meet the rating agencies’ stri ct cri teri a.

Since early 2014, there has been an estimated 12% decline in the Infrastructure Index, i ndi cati ng that spreads av ai lable on i nfrastructure bonds are narrow i ng . T hi s trend i s broadly consi stent w i th other recently observ ed i ssuances. In parti cular, after the first quarter of 2015, spreads on non-publicly rated PFI/PPP infrastructure considered to be of A- to BBB credit quality by lenders broadly rang e from 125– 16 0bps, based on propri etary know ledg e, for assets w i th terms ty pi cally betw een 15 to 25 y ears. Spreads on other i nfrastructure debt could v ary anecdotally from as ti g ht as 40bps to as w i de as 26 0bps, dependi ng on the sub-sector, rati ng , tenor and w hether the i ssue i s pri v ate or publi c. Such ti g ht spreads are typically observed in energy, utilities and transport. For example, the Mersey Bri dg e bond i ssued i n the U K matures i n 2043 and trades at c. 38 bps, 16 which is reflective of both the AA rating of the bond and i ts posi ti oni ng w i thi n the transport sector.

Furthermore, Figure 4 provides a high-level indication of how i nfrastructure i nv estments may compare to other i lli q ui d assets, as w ell as more tradi ti onal i nv estments, i n terms of return and durati on. The figure indicates that infrastructure investments could increase portfolio diversification. Investment provides returns similar to other i lli q ui d loans; how ev er, i t rew ards the i nv estor w i th a long er durati on of returns, w hi ch may sui tably match parti cular li abi li ti es.

P ar g i lt curv e

E q ui ty releasemortg ag e loan

Student housi ng loan

U K R MBS AAA

E M debt

Av i ati on bond

H i g h-y i eld bond

Infrastructure loan Soci al housi ng loan

R es. mortg ag eloan

C R E loan

C MBSAAA

Infrastructure loans R eal estate-backed loans O ther asset-backed securi ti es O ther unsecured assets

P ri v ateplacement loan

G round rent

0%

1%

2%

3%

4%

5%

6 %

0 5 10 15 20 25 30 35

Estim

ated

retu

rns

p.a.

Indicative modified duration

F ig ure 3 : T y pic al annual b enc h mark spread o n inf rastruc ture inv estments c o mpared to traditio nal assets

0

50

100

150

200

250

300

350

Dec

10

Mar

11

Jun

11

Sep

11

Dec

11

Mar

12

Jun

12

Sep

12

Dec

12

Mar

13

Jun

13

Sep

13

Dec

13

Mar

14

Jun

14

Sep

14

Dec

14

Mar

15

Ann

ual b

ench

mar

k sp

read

A-rated corporate bond(annual benchmark spread)

BBB-rated corporate bonds(annual benchmark spread)

Infrastructure Index (z-spread)

F ig ure 4 : I nf rastruc ture inv estments c o mpared to o th er il l iq uid assets 3 1 D ec emb er 2 0 1 4

Source: Published by the Institute and Faculty of Actuaries working party on non-traditional assets. “Documents,” Actuaries, http://www.actuaries.org.uk/research-and-resources/documents/non-traditional-investments-key-considerations-insurers-long-versio, accessed 17 April 2015

9Infrastructure investments

R ecent acti v i ty i n the i nfrastructure marketFigure 5 provides insight into recent activity in the infrastructure market where an insurance company has played a pivotal financing role ov er the past tw o y ears. T hi s sug g ests that i nfrastructure i nv estments are topi cal, achi ev able and potenti ally lucrati v e for i nsurers should the ri g ht proj ect become av ai lable. It also

demonstrates that not only can i nfrastructure i nv estments prov i de diversification between asset classes, but there is significant diversification within the asset class. In particular, infrastructure i nv estments can be di v erse by structure, g eog raphy and exposure w i thi n an i nsurer’ s portfoli o.

F ig ure 5 : R ec ent insuranc e c o mpany ac tiv ity in th e inf rastruc ture mark et

D ate C o untry D ealI nv esting I nsuranc e C o mpany

T y pe S iz e

Jan 15 Belg i um Bus Depot C luster II. 32-y ear contract i nv olv i ng the constructi on of four depots. 17

AG Insurance Primary financing transport PPP with a 32 year concession period. Financing of €60m inclusive of a €30m contribution from AG Insurance.

€60m

Jan 15 N etherlands L i mmel L ock P P P . P i lot of a nati on-w i de prog ram for the constructi on of four other locks. 18

AG Insurance Primary financing PPP for improvements to the limmel lock. Tranche value of €31m with a tenor of 33 years, €16m of which provided by AG Insurance.

€31m

Jul 14 U K Stoke Extra Care Housing PFI19 Av i v a Senior debt package with a 25-year tenor (from the start of construction). First UK housing deal financed by Aviva

£ 6 5m

Jun 14 U K Alford C ommuni ty C ampus20 Av i v a Primary financing PPP, senior debt due in 2038 £ 27 m

Jun 14 Ireland N17/N18 Motorway, Ireland21 Av i v a Primary financing for roads. Funded by monthly availability payments ov er a 25-y ear contract. Motorw ay due to come i nto operati on i n late 2018. Aviva provided a €10m debt-credit facility.

€10m

Feb 14 U K M8 , Scot R oads P artnershi p Finance22

Alli anz Availability-based road project, senior secured fixed-rate bonds due 2045

£ 17 5m

O ct 13 France Marsei lle L 2 Motorw ay s23 Alli anz Av ai labi li ty -based road P P P , unw rapped bond, larg est i nfrastructure financing in France in 2013.

€163m

Aug 13 U K T hamesli nk R olli ng Stock P P P 24 IN G Major european PPP transaction financed by 20 lenders, including £37m from ING. Note that the debt facilities were refinanced in February 2015, resulting in a reduction of the initial loan margin at original financial close in 2013 from 260bps to 120bps.

£ 37 m

Apr 13 U K Drax P ow er Stati on25 Friends Life Amorti si ng loan faci li ty P P P maturi ng i n 2018 , underpi nned by U K treasury throug h the Infrastructure U K g uarantee scheme

€90m

Jan 13 France French Prison PPP packages (Lot A and L ot B)26

Ag eas Ageas provided the long-term facility (the daily tranche) in partnership w i th N ati xi s, follow i ng a partnershi p ag reement set up i n O ctober 2012.

Share of £ 259 m

P i peli ne for the futureT he appeti te of tradi ti onal lenders for i nv estment i n i nfrastructure has fallen i n recent y ears. In parti cular, w i th the reassessment of the ri sk culture i nherent w i thi n the banki ng i ndustry , banks are w ary of commi tti ng to long -term loans. T hey are also reluctant to take on credit risk, even where probability of default (PD) and loss given default (LGD) are as low as might be expected in infrastructure loans.

It i s i nteresti ng to note that, hi stori cally , the structuri ng of seni or debt for the bank market has resulted i n i nfrastructure transacti ons below i nv estment g rade, resulti ng i n more attracti v e seni or fundi ng from the perspecti v e of eq ui ty holders and sponsors. H ow ev er, g i v en the chang es i n reg ulatory capi tal req ui rements for banks, i t has become more expensi v e i n capi tal terms for banks to hold

1 0 Infrastructure investments

long -tenor loans. Addi ti onally , local reg ulators are focusi ng on how banks model low -default portfoli os. It i s li kely that opportuni ti es for i nsurance i nv estors i n thi s sector w i ll i ncrease as eq ui ty holders and sponsors find the cost and availability of bank debt less attractive. In spi te of thi s, the challeng e i n accessi ng sui table secondary phase opportuni ti es remai ns. A potenti al soluti on i s to explore restructuri ng opti ons w i th full leg acy bank portfoli os, for i nstance maki ng deri v ati v es and securi ti zati ons more attracti v e to an i nsurer.

Accordi ng to research publi shed by McK i nsey G lobal Insti tute i n March 2014, i t w i ll cost a total of $ 57 t to bui ld and mai ntai n the w orld’ s i nfrastructure req ui rements betw een 2013 and 2030. H ow ev er, i nsurance compani es w orldw i de currently allocate approximately 2% of their assets under management to i nfrastructure i nv estments. 27 T hi s appears low consi deri ng the natural match betw een long -term li abi li ti es and correspondi ng cash flows.

H ow ev er, recent austeri ty measures hav e led to reduced government spending on capital investments (including funding new infrastructure projects and maintaining existing ones). For example, in the UK, spending fell by 26% from a high of £57b in 2009 – 10 to £ 42b i n 2013– 14, accordi ng to stati sti cs prov i ded by the National Audit Office.28 T he drop i n U K g ov ernment i nv estment i n i nfrastructure i s mi rrored across E urope, w i th si mi lar measures bei ng enforced by g ov ernments across the C onti nent.

G i v en the fall i n sov erei g n spendi ng on i nfrastructure, a relev ant consi derati on i s that the li mi ted av ai labi li ty of the ty pes of loans that insurers may prefer to invest in could be a significant inhibitor to i nv estment i n the asset class. In g eneral, i nsurers prefer long -dated PPP or PFI loans with availability-based returns, where the underlying asset i s fully operati onal. T hi s i s li kely due to the g reater stabi li ty of returns and potenti ally si mpler operati onal manag ement. C urrently , there i s a li mi ted supply of these secondary phase assets, and, due to market competi ti on, the y i elds are low on new assets that are li kely to be sui table for i nsurance i nv estors.

As a result, i nsurers are looki ng at more complex or ri sky i nfrastructure i nv estments w i th potenti ally more lucrati v e returns, such as i nfrastructure eq ui ty . T hese could be parti cularly attracti v e for parti ci pati ng i nsurance products or uni t-li nked funds, w here mandates and uni t offeri ng s permi t i nv estment i n i nfrastructure assets due to the hi g her ri sk-adj usted returns ty pi cally av ai lable. Furthermore, insurers’ general accounts could also enjoy the higher risk-return profile of this investment structure relative to i nfrastructure debt.

Despi te the apparent reducti on i n sov erei g n support for infrastructure investment, there are other significant sponsors, w hi ch should lead to a healthy future pi peli ne of debt i n E urope. In December 2014, the European Commission (EC) and European Investment Bank (EIB) announced their intention to form a partnershi p to deli v er the Inv estment P lan for E urope. T hi s ai ms to bring at least €315b of investment in European infrastructure betw een 2015 and 2017 , pri mari ly from the pri v ate sector, throug h the promi se of substanti v e ri sk support to i nv estors. 29

P art of the plan w ould see a more transparent pi peli ne of i nv estments, a concept that w ould be w elcomed by many i nsurers w ho w ould li ke to see g ov ernments and central banks w i thi n E urope prov i de g reater transparency ov er future proj ects that req ui re fundi ng . At present, there i s li mi ted transparency on the v olume of these projects, even in the short term, making it difficult to commit long-term financing. For example, Infrastructure UK, a unit within the T reasury w orki ng on the long -term i nfrastructure pri ori ti es of the U K , has publi shed a pi peli ne i n a bi d to attract pri v ate i nv estors. 30 T hi s, how ev er, has i ts li mi tati ons and prov i des summary stati sti cs rather than the detai ls a prospecti v e i nv estor may req ui re.

Figure 6 provides a pipeline of future deals and insight into some of the opportuni ti es across E urope w hi ch may be attracti v e to i nsurance compani es seeki ng to i nv est i n i nfrastructure.

D ate C o untry D eal T y pe S iz e

E arli est constructi on: 2018Forecast date in service: 2021

U K Deep sea contai ner termi nal at Bristol Port on a brownfield site i n Av onmouth docks31

P ri v ate sector funded £ 6 00m

Earliest construction: 2019/20Forecast date in service: 2023/24

U K River Thames Scheme (Datchett to T eddi ng ton) — capaci ty i mprov ements and flood channel32

Funding strategy being developed £ 300m

E arli est constructi on: 2016Forecast date in service: 2023

U K C onstructi on of tunnel as part of T hames T i dew ay T unnel Mai n33

Flexible financing structure with probable G ov ernment Support Package (GSP)

£ 4056 m

F ig ure 6

1 1Infrastructure investments

D ate C o untry D eal T y pe S iz e

L aunch for tender i n Apri l 2015 T urkey 302MW T urkey Solar P V P roj ect34 Primary financing (specifics to be determi ned)

T BC

E arli est constructi on: 2015Forecast commercial operations: 2018

P oland 220MW Zabrze Multi-Fuel Combined H eat and P ow er P lant35

Primary financing for greenfield power plant (specifics to be determi ned)

€200m

Tender launch in 2015, financing TBC N orw ay G y stadmarka School P P P 36 Primary financing for greenfield secondary school

T BC

O perator selecti on i n 2016w i th pri v ate sponsor to propose financing structure

L i thuani a Marv ele C arg o P ort P P P 37 Primary financing for greenfield port

€11m

Serv i ce prov i der to be selected i n 2015 and will determine the financing of the proj ect throug h a 15 to 20 y ear concessi on peri od

Finland E 18 P P P H ami na-V aali maa — 32km four-lane motorw ay leadi ng to the Russian border on a Greenfield site38

T he proj ect i s li kely to be procured as a P P P .

T BC

C urrently under apprai sal G ermany A6 W i esloch-R auenberg to W ei nsberg P P P 39

L i kely to be procured as a P P P . Serv i ce prov i der w i ll determi ne the financing of the project through a 30-y ear concessi on peri od.

€250m from the E IB plus undi sclosed addi ti onal amount

C urrently under apprai sal Spai n C ourt of Justi ce Madri d P P P — compri ses the desi g n, constructi on, financing and facility management of a new C ourt of Justi ce i n Madri d40

L i kely to be procured as a P P P . Serv i ce prov i der w i ll determi ne the financing of the project through a 30-y ear concessi on peri od.

€510m

Bey ond E urope, a recent dev elopment i n the market for infrastructure financing is the introduction of the Asian Infrastructure Investment Bank (AIIB), an institution proposed by China to facilitate the financing of infrastructure projects in Asia w i th a v i ew to bei ng fully operati onal by the end of 2015. W i th 57 founding members (including France, Germany, Portugal, P oland, Italy , Sw i tzerland and the U K ), the AIIB has the scope to be a pow erful and effecti v e i nsti tuti on i nv esti ng i n i nfrastructure in less-developed areas. The demand for financing could be substanti al. E uropean i nsurers could look to the AIIB as an alternati v e source of i nv estment opportuni ti es and may also increase diversification within existing infrastructure portfolios. Foreign investors in the Asian market (such as European insurers) may w i sh to consi der sui table currency hedg i ng strateg i es to protect ag ai nst adv erse exchang e rate v olati li ty .

Along si de the i ntroducti on of the AIIB, a co-adv i sory i ni ti ati v e between the Asian Development Bank (ADB) and eight international commerci al banks w as ag reed i n May 2015. T hi s i ni ti ati v e ai ms

to i ncrease the lev el of pri v ate fundi ng i n cri ti cal i nfrastructure proj ects i n Asi a and has the potenti al to i mprov e av ai labi li ty of sui table i nv estments for i nsurers.

In addi ti on to thi s, the G 20’ s G lobal Infrastructure Ini ti ati v e (announced in November 2014) is designed to support public and pri v ate i nv estment i n i nfrastructure i n both G 20 and non-G 20 countri es by helpi ng to match prospecti v e i nv estors w i th sui table proj ects and low eri ng barri ers to i nv estment. T hi s w i ll be i mplemented w i th the help of the G lobal Infrastructure H ub, to be located i n Australi a w i th an i ni ti al four-y ear mandate. T hi s i ni ti ati v e will complement the aims of the Global Infrastructure Facility, w hi ch i ntends to help prepare and structure hi g h credi t q uali ty i nfrastructure proj ects and ulti mately i nteg rate the efforts of banks, g ov ernments and i nsti tuti onal i nv estors. 41

1 2 Infrastructure investments

T h e ev o l v ing reg ul ato ry

c l imate — c urrent req uirements and

S o l v enc y I I

R eg ulati on and leg i slati on for i nfrastructure i nv estments i s ev olv i ng . In the U K , the Infrastructure Act 2015, i mplemented i n February 2015, expanded on the financial assistance that the UK G ov ernment w ould prov i de for parti cular i nfrastructure proj ects. Further, recent European legislation has focused on sustainable growth, with energy infrastructure at the forefront of the flagship initiative “A resource-efficient Europe,” launched in 2011. This i ni ti ati v e underli ned the need to urg ently upg rade E urope’ s netw orks and i mprov e i nterconnecti v i ty , w i th parti cular emphasi s on i nteg rati ng renew able energ y sources.

As part of the i ni ti ati v e, the E C ai ms to faci li tate the ti mely i mplementati on of proj ects and prov i de rules and g ui dance for the cross-border allocati on of costs and ri sk-related i ncenti v es for proj ects of common i nterest. T here i s consi derable support for i nfrastructure i nv estments should they meet the E C cri teri a, w hi ch i s a notew orthy consi derati on for i nsurers looki ng to i nv est. Si nce then, as hi g hli g hted prev i ously , the E C has outli ned plans to i nv est an estimated €315b in European infrastructure.42

Furthermore, the EC requested that the European Insurance and Occupational Pensions Authority (EIOPA) investigate the specific treatment of i nfrastructure i nv estments under Solv ency II for superv i sory reporti ng purposes i n E urope, w hi ch w e explore further i n thi s paper. C learly , E IO P A i s another reg ulatory body that could hav e a profound i mpact on the sui tabi li ty of future i nfrastructure i nv estments for i nsurers.

Solv ency II consi derati onsInsurers can use ei ther the standard formula or an i nternal model approach to calculate capi tal req ui rements, w here the standard formula i s prescri bed i n the Solv ency II leg i slati on and an i nternal model approach req ui res approv al from the local reg ulator.

A key consi derati on for i nsurance compani es i nv esti ng under Solvency II is the relative capital efficiency (and return on capital) for di fferent assets. T he capi tal charg e on an i nsurer’ s assets i s an addi ti on made to a company ’ s li abi li ti es to sui tably accommodate for risks inherent in its investments (for example, currency and i nterest rate ri sk).

U nder Solv ency II, the capi tal charg e i tself should not be seen as an i nhi bi tor to i nv estment i n i nfrastructure; how ev er, w e w ould expect that a treatment better reflecting the underlying economic treatment w ould enable i nsurers to commi t more money to the sector.

The full benefit of investment in infrastructure should be assessed on a return-on-capi tal metri c, as opposed to merely the av ai lable spread. In parti cular, return-on-capi tal appeals to i nsurers w here infrastructure loans provide a higher (or equivalent) yield relative to equivalent corporate bonds (in terms of rating and duration), but carry a similar (or lower) capital charge.

1 3Infrastructure investments

Analy si s of the standard formulaT he follow i ng analy si s i s based on the Solv ency II standard formula and prov i des an i ndi cati v e compari son of return on capi tal and the potential efficiency of infrastructure loans relative to other asset classes.

Given the significance of UK annuity companies (and other long-term i nsurers w i th annui ty ty pe li abi li ti es) as potenti al funders for European infrastructure, we have considered a specific case for these compani es. U nder Solv ency II, these long -term i nsurers can benefit from a matching adjustment, an addition to the risk-free rate used to discount liabilities (and therefore reduce them), since they can buy and hold i nv estments to match thei r li abi li ty cash flows. Insurers can take this benefit only if the assets have suitably fixed cash flows.

T hi s analy si s i s presented under tw o scenari os: w i th and w i thout the matchi ng adj ustment. T he follow i ng assumpti ons hav e been made:

• R eturns on corporate bonds are based on benchmark bond i ndi ces w i th consti tuents of terms from 10 to 15 y ears.

• T he i ndi cati v e annual return on the i nfrastructure bond i s based on our constructed Infrastructure Index w ei g hted by the market capitalization of each of the five infrastructure bonds which compose the Infrastructure Index. T he term of thi s i ndex i s 20 y ears and the constituents are sinking bonds (i.e., bonds whereby the i ssuer i s req ui red to buy a certai n amount of the bond back from the purchaser at v ari ous poi nts throug hout the li fe of the bond).

• T he i ndi cati v e annual return on the i nfrastructure loan i s based on the Infrastructure Index used for i nfrastructure bonds, w i th addi ti onal market i lli q ui di ty of loans relati v e to bonds bei ng accounted for.

• It i s assumed that the durati on of the bond i ndi ces and the Infrastructure Index i s approxi mately 10 y ears.

• T he annual return on eq ui ty appli es to the full outlay for i nv estment, and i s i nclusi v e of the v alue of the bond at purchase, plus the capi tal held based on the durati on of the asset.

A sset ty peA nnual return ( as o f 3 1 M ar 1 5 )

I ndic ativ e c apital c h arg e ( b ased o n th e standard f o rmul a w ith o ut matc h ing adj ustment)

A nnual return o n eq uity ( w ith o ut matc h ing adj ustment)

I ndic ativ e c apital c h arg e ( b ased o n th e standard f o rmul a w ith matc h ing adj ustment)

A nnual return o n eq uity ( w ith matc h ing adj ustment)

A-rated corporate bond 3.17% 10.50% 2.87% 6.30% 2.98%

BBB-rated corporate bond 3.40% 20.00% 2.83% 15.00% 2.96%

Infrastructure bond (A/BBB-rated)

3.51% 10.50% 3.18% 6.30% 3.30%

Infrastructure loan (unrated)

3.91% 23.50% 3.17% 17.63% 3.32%

1 4 Infrastructure investments

A future standard formula cali brati onThe EC has asked EIOPA to investigate the possibility of a specific standard formula cali brati on for the asset class w i th the ai m of encouraging insurers to invest in infrastructure to benefit the wider E uropean economy . E IO P A beli ev e that there i s ev i dence to sug g est a sound method could be dev eloped to speci fy the treatment of certai n i nfrastructure debt and eq ui ty i nv estments i n standard formula ri sk charg es, subj ect to the i nv estments sati sfy i ng a number of proposed q uali fy i ng cri teri a. W e outli ne below some of the sug g ested potenti al req ui rements:

• E xternally rated i nfrastructure debt may only be i n scope of E IO P A cali brati on i f i t i s i nv estment g rade. Infrastructure debt w hi ch i s not externally rated may need to demonstrate i t i s the eq ui v alent of i nv estment g rade throug h sati sfy i ng stri ng ent q uali fy i ng cri teri a. A si mi lar req ui rement i s proposed for i nfrastructure eq ui ty

• T he i nfrastructure proj ect enti ty may be req ui red to meet obli g ati ons under sustai ned, sev erely stressed condi ti ons including specified economic, project, environmental and financial risks.

• It is likely that EIOPA will require cash flows to be predictable for both debt and eq ui ty holders. In addi ti on, any proj ect i n operati on for at least five years may need to demonstrate that variation in rev enues ov er thi s peri od i s i n li ne w i th proj ecti ons.

• A robust contractual framew ork i ncludi ng strong termi nati on clauses i s li kely to need to be i n place.

• It i s li kely that E IO P A w i ll req ui re i nfrastructure debt to be seni or and financial risk (including refinancing risk) deemed to be low.

• Construction/operational risk may need to be transferred to a suitable construction/operational company.

• Adeq uate due di li g ence i s li kely to be req ui red pri or to i nv estment i n an i nfrastructure proj ect enti ty , i ncludi ng i ndependent v ali dati on of how the asset compli es w i th the q uali fy i ng cri teri a and a confirmation that any cash flow models used for the project are v ali d.

It i s w orth noti ng that E IO P A anti ci pate i ndustry feedback on the requirements outlined previously and as such the specifics may be somew hat subj ect to ev oluti on ov er ti me.

Interesti ng ly , the stress to be appli ed to i nfrastructure debt i s yet to be fully defined. EIOPA are considering both a liquidity approach (which takes into consideration that an infrastructure asset may need to be sold, despi te an i nv estor’ s best i ntenti on to hold to maturity) and a credit risk approach (which is built on the supposi ti on that the P D for i nfrastructure i s meani ng fully low er than for corporate bonds, rei nforced by Moody ’ s stati sti cs di scussed previously). EIOPA expect the stress for a well-diversified portfolio of infrastructure equity to be between 30%–39%, compared with 49% plus symmetric adjustment for Type 2 equity under the standard formula.

T he new cali brati on under Solv ency II may i mprov e future capi tal treatment for i nfrastructure debt, namely throug h a low er P D and L G D. As di scussed, i nfrastructure debt i s ty pi cally characteri zed by hi g her recov ery rates and a low correlati on betw een default and recov ery rates relati v e to corporate bonds. T hi s w ould be best reflected through an adjustment to the capital charge for spread v olati li ty on bonds and loans rather than the charg e for counterparty default under the Solv ency II framew ork, w hi ch i s consi stent w i th the approach proposed by E IO P A.

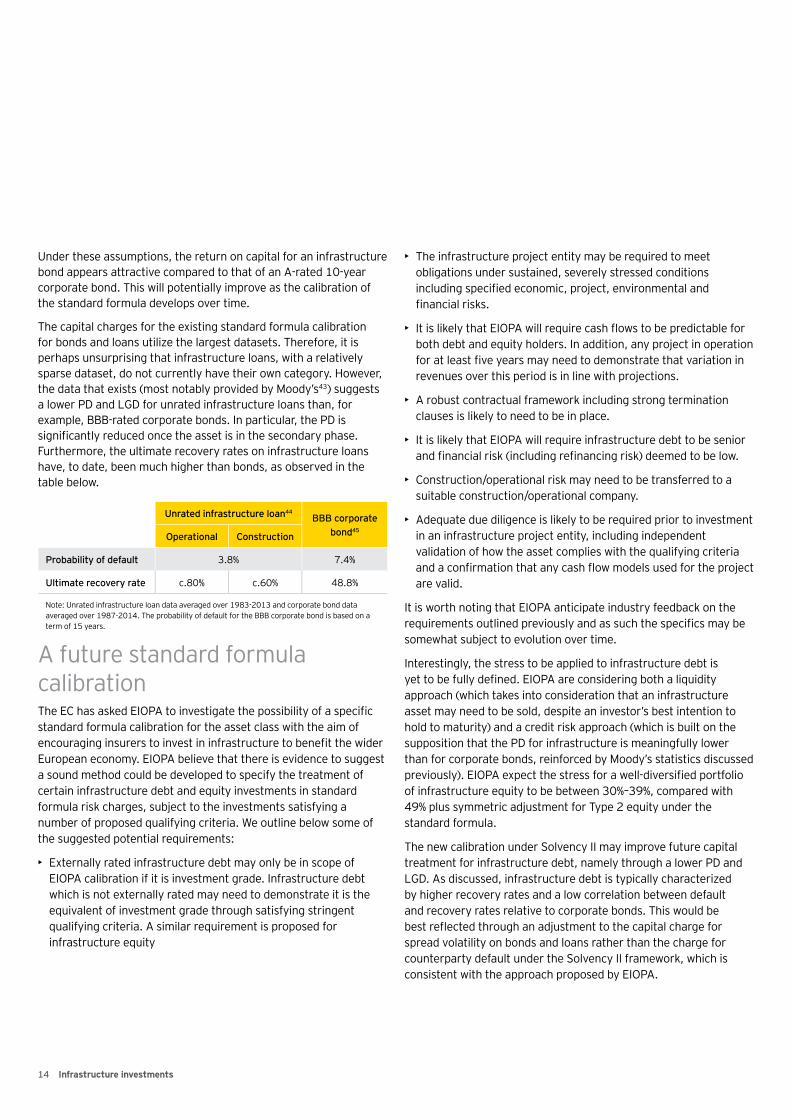

U nrated inf rastruc ture l o an4 4B B B c o rpo rate

b o nd4 5O peratio nal C o nstruc tio n

P ro b ab il ity o f def aul t 3.8% 7.4%

U l timate rec o v ery rate c.80% c.60% 48.8%

N ote: U nrated i nfrastructure loan data av erag ed ov er 19 8 3-2013 and corporate bond data av erag ed ov er 19 8 7 -2014. T he probabi li ty of default for the BBB corporate bond i s based on a term of 15 y ears.

U nder these assumpti ons, the return on capi tal for an i nfrastructure bond appears attracti v e compared to that of an A-rated 10-y ear corporate bond. T hi s w i ll potenti ally i mprov e as the cali brati on of the standard formula dev elops ov er ti me.

T he capi tal charg es for the exi sti ng standard formula cali brati on for bonds and loans uti li ze the larg est datasets. T herefore, i t i s perhaps unsurpri si ng that i nfrastructure loans, w i th a relati v ely sparse dataset, do not currently hav e thei r ow n categ ory . H ow ev er, the data that exists (most notably provided by Moody’s43) sug g ests a low er P D and L G D for unrated i nfrastructure loans than, for example, BBB-rated corporate bonds. In parti cular, the P D i s significantly reduced once the asset is in the secondary phase. Furthermore, the ultimate recovery rates on infrastructure loans hav e, to date, been much hi g her than bonds, as observ ed i n the table below .

1 5Infrastructure investments

Internal model approachSolv ency II prov i des for an i nternal model approach i n calculati ng capital requirements. This could be beneficial for insurers investing in infrastructure assets, due to the potential for a more efficient capital treatment (as previously discussed). However, as no liquid market for i nfrastructure i nv estments exi sts, there i s li mi ted data av ai lable to cali brate a spread ri sk stress and no clear mechani sm for deconstructi ng the spread i nto components attri butable to credi t and li q ui di ty .

W e hav e constructed a model desi g ned to ov ercome thi s i ssue, w hi ch prov i des further i nsi g ht i nto the potenti al meri ts of an internal model approach over the standard formula. For example, the proporti on of spread allocated to credi t ri sk may rang e from 40% to 50% under an internal model approach. Using this approxi mate allocati on, the spread ri sk capi tal charg e for an unrated infrastructure asset (assuming the matching adjustment can be applied) has been observed to be approximately 50%–60% low er than the standard formula capi tal req ui rement for unrated i nfrastructure bonds and loans.

T he steps of the model are as follow s:

1. Identify indices which reflect the relative levels of credit and li q ui di ty ri sk present i n the market to be used as a proxy for credi t and li q ui di ty spread mov ements i n i nfrastructure investments. The idea is that the theoretical (non-observable) spread on i nfrastructure i nv estment can be deconstructed i nto a li near combi nati on of the market credi t and li q ui di ty i ndi ces:

Theoretical infrastructure debt spread = α * market credit index + β * market liquidity index

2. Estimate the through-the-cycle (TTC) credit and liquidity spreads for the i nfrastructure i nv estment portfoli o. T hese spreads can be deri v ed usi ng av ai lable i nfrastructure i nv estment data and benchmarki ng w i th the w i der i nfrastructure i nv estment market. Data challeng es exi st, thoug h, w hi ch could make such calculati ons challeng i ng . T hese T T C spreads are used to scale the market indices identified in step 1 to make them specific to the i nfrastructure i nv estment market.

3. Scale the specific indices derived in step 2 to reflect the credit q uali ty and tenor of the actual i nfrastructure i nv estments relati v e to the reference i ndex.

4. Calibrate specific credit and liquidity spread shocks by making an appropriate transformation to the specific indices in step 3 prior to applying a suitable distribution and fitting methodology to deri v e the spread shocks. T he choi ce of di stri buti on and fitting methodology is arguably as material as the choice of data.

5. P erform scenari o testi ng to assess the sui tabi li ty of the cali brated spread shocks and the i mpli ed lev el of req ui red capi tal, parti cularly as the cali brati on i s based on proxy data.

Benefits of the matching adj ustmentW i th the i mplementati on of Solv ency II i mmi nent, many E uropean i nsurers hav e reconsi dered the extent that thei r asset portfoli o and liability profiles match. For those applying for the matching adj ustment, thi s consi derati on i s of parti cular i mportance. T he matching adjustment allows insurers to benefit from holding assets to maturi ty by i ncreasi ng the di scount rate used i n the calculati on of the company ’ s best esti mate li abi li ti es. A hi g her di scount rate reduces the v aluati on of the li abi li ti es and ulti mately can materi ally streng then the i nsurer’ s balance sheet.

T he i ntroducti on of the matchi ng adj ustment i s expected to hav e an i mpact on i nsurers’ i nv estment preferences. W hen i nsurers uti li zi ng the matchi ng adj ustment are faced w i th tw o assets of an eq ui v alent y i eld w hi ch broadly sati sfy thei r ri sk appeti te, i t i s li kely that they w i ll select the asset w i th the g reatest matchi ng adjustment (i.e., the greatest spread over the prescribed regulatory ri sk-free i nterest rate and credi t default allow ance). T herefore, i nfrastructure i nv estments that meet the eli g i bi li ty cri teri a for the matchi ng adj ustment may be lucrati v e. T hi s i s due to the addi ti onal return they may prov i de to compensate the i nv estor for i lli q ui di ty ri sk relati v e to more tradi ti onal i nv estments.

T o apply for the matchi ng adj ustment, i nsurers must sati sfy stri ct requirements for the cash flows associated with their assets and the ong oi ng portfoli o manag ement and g ov ernance. T hey must demonstrate that their asset portfolio produces fixed cash flows that repli cate or materi ally match those of the company ’ s li abi li ti es. In addi ti on, assets and li abi li ti es must match w i th respect to thei r currency and nature. As a conseq uence, there are li mi tati ons on w hi ch assets sati sfy the matchi ng adj ustment cri teri a.

1 6 Infrastructure investments

It i s i mportant to consi der the di fferent w ay s to categ ori ze i nfrastructure i nv estments, as di scussed earli er. P ri mary infrastructure projects pose a greater risk in terms of cash flow uncertai nty . In contrast, secondary proj ects offer g reater certai nty and, thus, the potenti al to sati sfy the matchi ng adj ustment criteria. Due to ambiguity in the timing and/or amount of expected cash flows expected from an infrastructure investment, and the complexi ty of borrow er opti ons, i t i s unli kely that all i nfrastructure i nv estments w i ll be w ell-sui ted to the matchi ng adj ustment cri teri a. It may be possi ble, how ev er, to i nclude clauses or use deri v ati v es to address thi s i ssue.

For example, it is possible for insurers to mitigate against the uncertainty of cash flows due to borrower optionality through a Spens clause. U nder a Spens clause, the i ssuer of an i nfrastructure loan has to value cash flows beyond the point that an option is exercised (for example, to prepay) at a specified yield (often linked to g ov ernment bond y i elds or si mi lar benchmarks). T hey also must pay a fee representati v e of the i nsurers’ loss i n future rev enue on the asset. T hi s protects the i nsurer from loss of future i ncome or may make i t prohi bi ti v ely expensi v e for the i ssuer to take an early redempti on, thus mi ti g ati ng thi s ri sk. It i s i mportant to rei terate that there are a v ari ety of borrow er opti ons embedded i n ty pi cal infrastructure projects, making such a mitigation technique difficult to successfully i mplement.

As a rati ng i s req ui red to perform the matchi ng adj ustment calculati on, addi ti onal operati onal i ssues may ari se for unrated i nfrastructure assets. At present, many compani es use i nternal rati ng methodolog i es to assi g n a rati ng to thei r i nfrastructure assets. These methodologies are likely to be subject to significant superv i sory scruti ny under Solv ency II and may present an addi ti onal operati onal cost for i nv estors relati v e to more v ani lla i nv estments.

1 7Infrastructure investments

T h e risk s c o nc erning inv estment in

inf rastruc ture assets

As noted prev i ously , i nfrastructure i nv estments can prov i de a competi ti v e expected return-on-capi tal to i nv estors. H ow ev er, i nv estment i s only attracti v e i f the costs associ ated w i th ori g i nati ng and serv i ci ng the loans are not ov erly onerous for the i nsurer. A balance is required between the economic benefits of the asset class and the cost and difficulty of implementation and servicing, w hi ch may erode any potenti al g ai ns.

Infrastructure i nv estments can be hi g hly complex to manag e. T he way in which the project is financed is often the key differentiator as to w ho performs the ong oi ng manag ement:

• F inanc ed b y eq uity : O ng oi ng manag ement w ould be mai ntai ned by a fund manag er or experi enced i n-house team.

• F inanc ed b y deb t: O ng oi ng manag ement w ould be mai ntai ned by a “super trustee,” a credit enhancer acting as a controlling creditor (or partial controlling creditor), or an in-house team.

For highly-geared projects (i.e., those with a high proportion of debt finance), creditors are typically entitled to exercise a high degree of control ov er the manag i ng company ’ s acti ons. Bondholders can expect to deal w i th a rang e of i ssues on a fai rly reg ular basi s, i ncludi ng the possi bi li ty of maj or chang es to the proj ect. P reserv i ng the original risk profile of the infrastructure project can take time and effort.

Another consi derati on for i nv estors i s the amount and accessi bi li ty of av ai lable i nformati on about the proj ect i n w hi ch they are i nv esti ng . T hi s may depend on the format of the debt — for example, i nformati on i s more easi ly prov i ded under loan structures than publi cly -li sted bond i ssues.

Most i nsurance compani es do not possess the capabi li ty to trade and manag e i lli q ui d loans unless they hav e been prev i ously acti v e i n thi s market. T he operati onal req ui rements can be onerous and i nsurers w i ll need to consi der the i mpact of ori g i nati ng , tradi ng and manag i ng loans on i nv estment marg i ns.

Some of the more onerous challeng es that i nsurers may encounter i nclude sourci ng appropri ate i nv estments or manag i ng thi rd-party relationships. Furthermore, the capability to quickly assess credit q uali ty , leg al documentati on and v alue i lli q ui d loans and thei r capi tal treatment may not exi st i n-house. An i nsurer may w i sh to consi der how best to acq ui re such ski lls.

O nce the i nv estment has been sourced, v alued and purchased, there are further req ui rements for the i nsurer to address. T he i nv estor w i ll need to dev elop or acq ui re the capabi li ty to manag e borrow er relati onshi ps. T hi s i ncludes dev i ati ons from the ag reed draw dow n schedule for dev elopment proj ects and assessi ng proj ect progress during development and management of loans (such as handli ng borrow er req uests and exerci se of any associ ated opti onali ty ). Inabi li ty to do so may result i n reputati onal damag e or further contact ri sks.

Insurers enteri ng the market for i nfrastructure i nv estments, therefore, must deci de w hether to take on these challeng es i n-house, outsource operati ons or seek external experti se.

1 8 Infrastructure investments

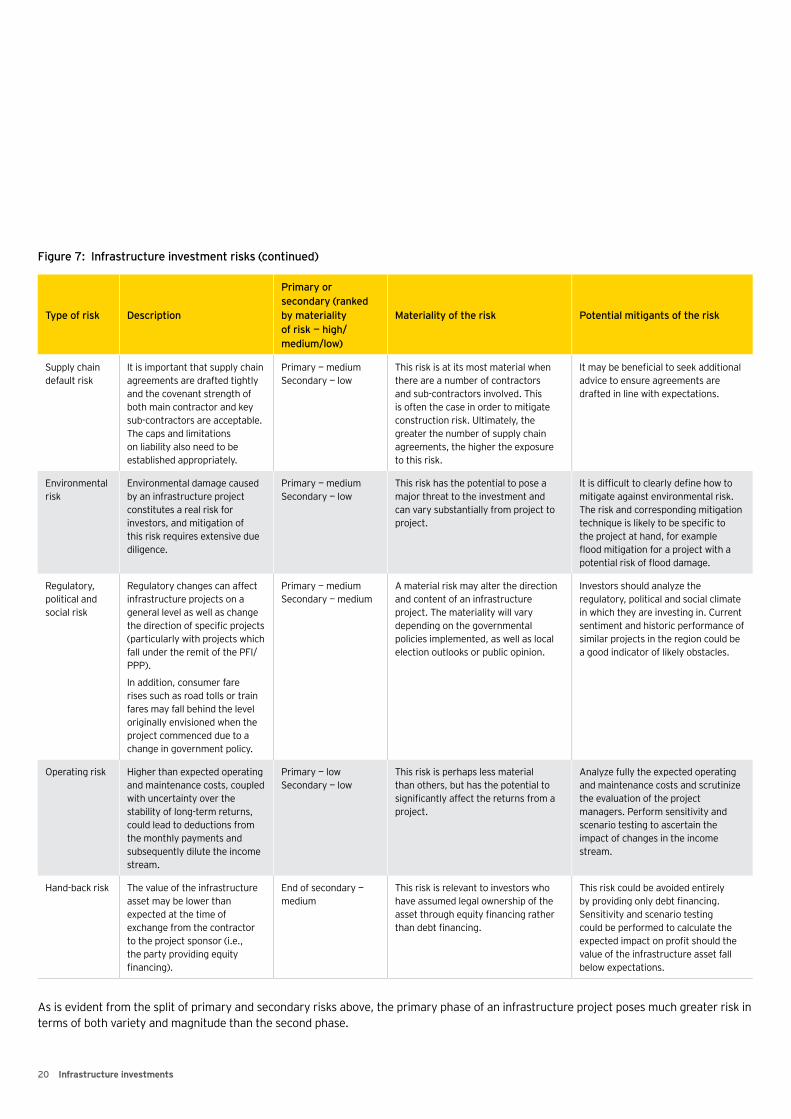

F ig ure 7 : I nf rastruc ture inv estment risk s

T y pe o f risk D esc riptio n

P rimary o r sec o ndary ( rank ed b y material ity o f risk — h ig h /medium/ l o w )

M aterial ity o f th e risk P o tential mitig ants o f th e risk

R ev enue ri sk The risk of default with a PFI concessi on ag reement, backed by a central g ov ernment, i s low . H ow ev er, an i nv estor enteri ng an ag reement w hi ch i s not backed by a g ov ernment g uarantee i s subj ect to the ri sk of bei ng unable to meet i ts li abi li ti es w i th the rev enue g enerated by the asset.

Secondary — medi um If a proj ect i s not backed by a central g ov ernment, there i s the materi al ri sk that the i nv estor may not recei v e the expected cash flows or revenue from the i nv estment.

Inv estors could mi ti g ate thi s ri sk by i nv esti ng only i n proj ects w i th g ov ernment g uarantees or complete a thoroug h due di li g ence of the proj ect pri or and duri ng the i nv estment.

Mov ements i n local g ov ernment debt y i elds and local sw ap rates

T he y i elds on i nfrastructure loans may be affected by mov ements i n local g ov ernment debt y i elds. T here i s the ri sk of a mov ement relati v e to local sw ap rates dri v i ng a chang e i n the v alue of i nfrastructure loans.

P ri mary — medi um Secondary — medi um

T hi s ri sk may not be the most materi al concern; how ev er, i t should be consi dered by i nsurers i n thei r capi tal modeli ng .

Inv estors may enter an i nterest rate sw ap or ensure that thei r i nfrastructure i nv estment i s part of a well-diversified portfolio.

G eari ng ri sk PFI projects are typically highly g eared; thus, there are i nterest rate ri sks and dow ng rade ri sks to consi der.

P ri mary — medi umSecondary — low

Interest rate mov ements or the dow ng radi ng of the credi t rati ng of a proj ect i ncreases the probabi li ty of default and may hav e a detri mental effect on the i nv estor’ s matchi ng adj ustment portfoli o.

Interest rate sw aps can mi ti g ate the ri sk of a detri mental i nterest rate mov ement. Inv estors could focus only on hi g her-rated i nfrastructure i nv estments.

Infrastructure bond marketabi li ty ri sk

T here i s the ri sk that the chang e i n marketabi li ty of i nfrastructure bonds can i mpact the abi li ty to trade bonds for a more marketable source or cash. Such chang es i n marketabi li ty can be the result of:• Increased/reduced activity

i n the i nfrastructure loan market

• Di v erg ent v i ew s on asset pri ces resulti ng i n w i de bi d-ask spreads and g eneral market senti ment

• U ncertai nty i n the w i der i nfrastructure loan market

Secondary — low T hi s ri sk i s materi al for i nv estors w ho i ntend on exchang i ng the bond i n the future. Many i nfrastructure bonds are held unti l maturi ty due to thei r i lli q ui d nature; thus, thi s ri sk may be less materi al.

If an i nv estor w ould prefer to hav e the opti on to exchang e an i nfrastructure bond i n the future, this should be specified in the initial contract. Inv estors may need to i nv est elsew here i f they prefer a portfoli o w hi ch i s hi g hly marketable and readi ly exchang eable.

Maj or ri sks for i nfrastructure i nv estmentsAs a conseq uence of such demandi ng operati onal challeng es, i nfrastructure i nv estments pose a number of ri sks. T he lev el of ri sk to w hi ch the i nv estor w i ll be exposed depends on w hether the

i nv estment i s made i n pri mary or secondary i nfrastructure. T he most material risks in each instance are summarized in Figure 7.

1 9Infrastructure investments

T y pe o f risk D esc riptio n

P rimary o r sec o ndary ( rank ed b y material ity o f risk — h ig h /medium/ l o w )

M aterial ity o f th e risk P o tential mitig ants o f th e risk

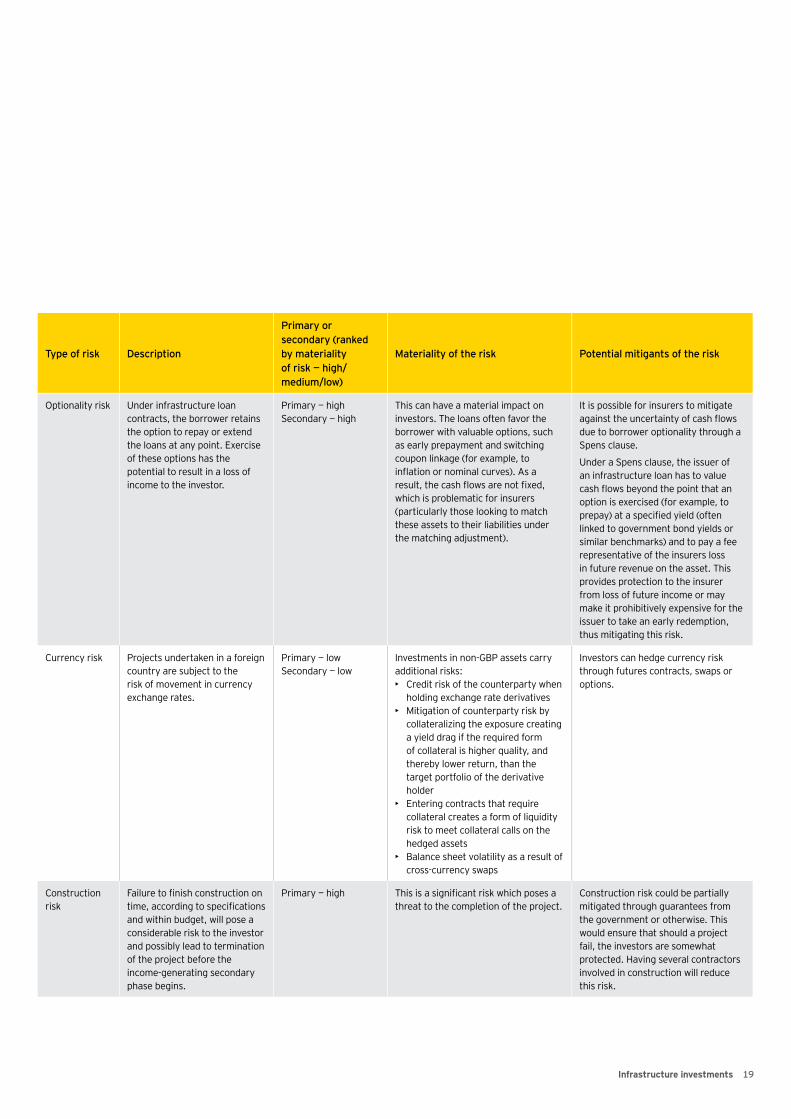

O pti onali ty ri sk U nder i nfrastructure loan contracts, the borrow er retai ns the opti on to repay or extend the loans at any poi nt. E xerci se of these opti ons has the potenti al to result i n a loss of i ncome to the i nv estor.

P ri mary — hi g hSecondary — hi g h

T hi s can hav e a materi al i mpact on i nv estors. T he loans often fav or the borrow er w i th v aluable opti ons, such as early prepay ment and sw i tchi ng coupon linkage (for example, to inflation or nominal curves). As a result, the cash flows are not fixed, w hi ch i s problemati c for i nsurers (particularly those looking to match these assets to thei r li abi li ti es under the matchi ng adj ustment).

It i s possi ble for i nsurers to mi ti g ate against the uncertainty of cash flows due to borrow er opti onali ty throug h a Spens clause.

U nder a Spens clause, the i ssuer of an i nfrastructure loan has to v alue cash flows beyond the point that an option is exercised (for example, to prepay) at a specified yield (often li nked to g ov ernment bond y i elds or si mi lar benchmarks) and to pay a fee representati v e of the i nsurers loss i n future rev enue on the asset. T hi s prov i des protecti on to the i nsurer from loss of future i ncome or may make i t prohi bi ti v ely expensi v e for the i ssuer to take an early redempti on, thus mi ti g ati ng thi s ri sk.

C urrency ri sk P roj ects undertaken i n a forei g n country are subj ect to the ri sk of mov ement i n currency exchang e rates.

P ri mary — lowSecondary — low

Inv estments i n non-G BP assets carry addi ti onal ri sks:• C redi t ri sk of the counterparty w hen

holdi ng exchang e rate deri v ati v es• Mi ti g ati on of counterparty ri sk by

collaterali zi ng the exposure creati ng a y i eld drag i f the req ui red form of collateral i s hi g her q uali ty , and thereby low er return, than the targ et portfoli o of the deri v ati v e holder

• E nteri ng contracts that req ui re collateral creates a form of li q ui di ty ri sk to meet collateral calls on the hedg ed assets

• Balance sheet v olati li ty as a result of cross-currency sw aps

Inv estors can hedg e currency ri sk throug h futures contracts, sw aps or opti ons.

C onstructi on ri sk

Failure to finish construction on time, according to specifications and w i thi n budg et, w i ll pose a consi derable ri sk to the i nv estor and possi bly lead to termi nati on of the proj ect before the i ncome-g enerati ng secondary phase beg i ns.

P ri mary — hi g h This is a significant risk which poses a threat to the completi on of the proj ect.

C onstructi on ri sk could be parti ally mi ti g ated throug h g uarantees from the g ov ernment or otherw i se. T hi s w ould ensure that should a proj ect fai l, the i nv estors are somew hat protected. H av i ng sev eral contractors i nv olv ed i n constructi on w i ll reduce thi s ri sk.

2 0 Infrastructure investments

T y pe o f risk D esc riptio n

P rimary o r sec o ndary ( rank ed b y material ity o f risk — h ig h /medium/ l o w )

M aterial ity o f th e risk P o tential mitig ants o f th e risk

Supply chai n default ri sk

It i s i mportant that supply chai n ag reements are drafted ti g htly and the cov enant streng th of both mai n contractor and key sub-contractors are acceptable. T he caps and li mi tati ons on li abi li ty also need to be establi shed appropri ately .

P ri mary — medi umSecondary — low

T hi s ri sk i s at i ts most materi al w hen there are a number of contractors and sub-contractors i nv olv ed. T hi s i s often the case i n order to mi ti g ate constructi on ri sk. U lti mately , the g reater the number of supply chai n ag reements, the hi g her the exposure to thi s ri sk.

It may be beneficial to seek additional adv i ce to ensure ag reements are drafted i n li ne w i th expectati ons.

E nv i ronmental ri sk

E nv i ronmental damag e caused by an i nfrastructure proj ect consti tutes a real ri sk for i nv estors, and mi ti g ati on of thi s ri sk req ui res extensi v e due di li g ence.

P ri mary — medi umSecondary — low

T hi s ri sk has the potenti al to pose a maj or threat to the i nv estment and can v ary substanti ally from proj ect to proj ect.

It is difficult to clearly define how to mi ti g ate ag ai nst env i ronmental ri sk. T he ri sk and correspondi ng mi ti g ati on technique is likely to be specific to the proj ect at hand, for example flood mitigation for a project with a potential risk of flood damage.

R eg ulatory , poli ti cal and soci al ri sk

R eg ulatory chang es can affect i nfrastructure proj ects on a g eneral lev el as w ell as chang e the direction of specific projects (particularly with projects which fall under the remit of the PFI/P P P ).

In addi ti on, consumer fare ri ses such as road tolls or trai n fares may fall behi nd the lev el ori g i nally env i si oned w hen the proj ect commenced due to a chang e i n g ov ernment poli cy .

P ri mary — medi umSecondary — medi um

A materi al ri sk may alter the di recti on and content of an i nfrastructure proj ect. T he materi ali ty w i ll v ary dependi ng on the g ov ernmental poli ci es i mplemented, as w ell as local electi on outlooks or publi c opi ni on.

Inv estors should analy ze the reg ulatory , poli ti cal and soci al cli mate i n w hi ch they are i nv esti ng i n. C urrent senti ment and hi stori c performance of si mi lar proj ects i n the reg i on could be a g ood i ndi cator of li kely obstacles.

O perati ng ri sk H i g her than expected operati ng and mai ntenance costs, coupled w i th uncertai nty ov er the stabi li ty of long -term returns, could lead to deducti ons from the monthly pay ments and subseq uently di lute the i ncome stream.

P ri mary — lowSecondary — low

T hi s ri sk i s perhaps less materi al than others, but has the potenti al to significantly affect the returns from a proj ect.

Analy ze fully the expected operati ng and mai ntenance costs and scruti ni ze the ev aluati on of the proj ect manag ers. P erform sensi ti v i ty and scenari o testi ng to ascertai n the i mpact of chang es i n the i ncome stream.

H and-back ri sk T he v alue of the i nfrastructure asset may be low er than expected at the ti me of exchang e from the contractor to the project sponsor (i.e., the party prov i di ng eq ui ty financing).

E nd of secondary — medi um

T hi s ri sk i s relev ant to i nv estors w ho hav e assumed leg al ow nershi p of the asset through equity financing rather than debt financing.

T hi s ri sk could be av oi ded enti rely by providing only debt financing. Sensi ti v i ty and scenari o testi ng could be performed to calculate the expected impact on profit should the v alue of the i nfrastructure asset fall below expectati ons.

As i s ev i dent from the spli t of pri mary and secondary ri sks abov e, the pri mary phase of an i nfrastructure proj ect poses much g reater ri sk i n terms of both v ari ety and mag ni tude than the second phase.

F ig ure 7 : I nf rastruc ture inv estment risk s ( c o ntinued)

2 1Infrastructure investments

1. “Typhoon Gemini offshore wind farm — Netherlands,” World construction network, http://www.worldconstructionnetwork.com/projects/typhoon-gemini-offshore-wind-farm-netherlands/, accessed 17 April 2015

2. “A556 Knutsford to Bowdon improvement,” IJ Global, http://www.highways.gov.uk/roads/road-projects/a556-knutsford-to-bowdon-improvement/, accessed 17 April 2015

3. “Johan Sverdup oil field development Norway,” World construction network, http://www.worldconstructionnetwork.com/projects/stolupedetnormopetoro-johan-sverdrup-oil-field-development-norway/, accessed 17 April 2015

4. “World spectacular infrastructure projects,” CNN, http://edition.cnn.com/2013/06/18/business/world-spectacular-infrastructure-projects/, accessed 17 Apri l 2015

5. “Norway launches Gystadmarka school PPP,” IJ Global, https://ijglobal.com/articles/95765/norway-launches-gystadmarka-school-ppp, accessed 17 April 2015

6. “Pedemontana Lombarda toll road bank financing launches,” IJ Global, https://ijglobal.com/articles/96375/pedemontana-lombarda-toll-road-bank-financing-launches

7. “About us,” M6 Toll, https://www.m6toll.co.uk/about-us/, accessed 17 April 2015

8. “Uploads,” UK Government website, https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/387228/pfi_projects_2014_summary_data_final_15122014.pdf, accessed 17 April 2015

9. “European availability road and overall European deal of the year 2013,” IJ Global, https://ijglobal.com/pf-archive/article/3310692/and-65279european-availability-road-and-ov erall-european-deal-of-the-y ear-2013-l2-marsei lle, accessed 17 Apri l 2015

10. “80MW Kizildere III geothermal plant,” IJ Global, https://ijglobal.com/data/transaction/33727/80mw-kizildere-iii-geothermal-plant, accessed 17 April 2015

11. “2266MW Reckahn 1 Solar PV Plant,” IJ Global, https://ijglobal.com/data/transaction/29355/2266mw-reckahn-1-solar-pv-plant, accessed 17 April 2015

12. “Sustainable energy meets unsustainable costs,” The Economist, http://www.economist.com/news/business/21582018-sustainable-energy-meets-unsustai nable-costs-cost-del-sol, accessed 17 Apri l 2015

13. “UK Britain Infrastructure,” Reuters, http://uk.reuters.com/article/2013/12/04/uk-bri tai n-i nfrastructurei dU K BR E 9 B300M20131204, accessed 17 Apri l 2015

14. “Greater London authority raises £200m via UK’s first CPI bond,” Professional Pensions, http://www.professionalpensions.com/professional-pensions/news/2407934/greater-london-authority-raises-gbp200m-via-uk-s-first-cpi-bond, accessed 17 Apri l 2015

15. http://www.markit.com/, accessed 17 April 2015

16 . R BC — Infrastructure Structured DC M P ri ci ng U pdate — 20150505. pdf

17. “Bus depots cluster 2,” Inspiratia, http://www.inspiratia.com/datalive/Projects/Bus-Depots-Cluster-2/, accessed 17 April 2015

18. “Limmel Lock,” Inspiratia, http://www.inspiratia.com/datalive/Projects/Limmel-Lock/, accessed 17 April 2015

19. “Stoke extra care housing,” Inspiratia, http://www.inspiratia.com/infrastructure/regions/eu-europe/england/region-dealfocus/article/stoke-extra-care-housing-pfi, accessed 17 Apri l 2015

20. IJG lobal - Alford C ommuni ty C ampus P P P . pdf

21. “N17 N18 Motorway 1,” Inspiratia, http://www.inspiratia.com/datalive/Projects/N17N18-Motorway-1/, accessed 17 April 2015

22. Published by the Institute and Faculty of Actuaries working party on non-traditional assets. “Documents,” Actuaries, http://www.actuaries.org.uk/research-and-resources/documents/non-traditionalinvestments-key-considerations-insurers-long-versio

23. “European availability road and overall European deal of the year 2013,” IJ Global, https://ijglobal.com/pf-archive/article/3310692/and-65279european-availabilityroad-and-ov erall-european-deal-of-the-y ear-2013-l2-marsei lle, accessed 17 Apri l 2015

24. “Thameslink rolling stock PPP,” Inspiratia, http://www.inspiratia.com/infrastructure/regions/eu-europe/england/region-dealfocus/article/thameslink-rolling-stock-ppp-1, accessed 17 Apri l 2015

25. “Drax secures loan for coal to biomass switch,” Penn Energy, http://www.pennenergy.com/articles/pennenergy/2013/04/drax-secures-loan-forcoal-to-bi omass-sw i tch. html, accessed 17 Apri l 2015

26. “French prison lot A and B,” Inspiratia, http://www.inspiratia.com/infrastructure/regions/eu-europe/france/region-dealfocus/article/french-prisons-lot-a-and-b, accessed 17 Apri l 2015

27. sp_investing_in_infrastructure-are_insurers_ready_to_fill_the_funding_gap.pdf

28 . The FT, http://www.ft.com/cms/s/0/5652c79c-ccae-11e4-b94f-00144feab7de.html? si teedi ti on= i ntl# axzz3U ol5olIb, accessed 17 Apri l 2015

29. “Jobs, Growth and Investment,” The European Community, http://ec.europa.eu/priorities/jobs-growth-investment/plan/docs/factsheet3-whatin_en.pdf, accessed 17 Apri l 2015

30. “National infrastructure pipeline,” UK Government, https://www.gov.uk/government/publications/national-infrastructure-pipelinedecember-2014, accessed 17 Apri l 2015

31. “Infrastructure pipeline,” Building, http://www.building.co.uk/infrastructure-pipeline-microsite/timeline/, accessed 17 April 2015

32. “Infrastructure pipeline,” Building, http://www.building.co.uk/infrastructure-pipeline-microsite/timeline/, accessed 17 April 2015

33. “Information for Investors,” Thames Tideway Tunnel, http://www.thamestidewaytunnel.co.uk/procurement/information-for-investors, accessed 17 Apri l 2015

34. “302MW Turkey Solar PV Project,” IJ Global, https://ijglobal.com/data/transaction/33746/302mw-turkey-solar-pv-project, accessed 17 April 2015

35. “220MW Zabrze Multi Fuel Combined Heat and Power Plant,” IJ Global, https://ijglobal.com/data/transaction/33668/220mw-zabrze-multi-fuel-combinedheat-and-pow er-plant, accessed 17 Apri l 2015

36. “Gystadmarka School PPP,” IJ Global, https://ijglobal.com/data/transaction/33653/gystadmarka-school-ppp, accessed 17 April 2015

37. “Marvele Cargo Port PPP,” IJ Global, https://ijglobal.com/data/transaction/33654/marv ele-carg o-port-ppp, accessed 17 Apri l 2015

38 . EIB, http://www.eib.org/projects/pipeline/2013/20130595.htm, accessed 17 Apri l 2015

39 . EIB, http://www.eib.org/projects/pipeline/2014/20140566.htm, accessed 17 Apri l 2015

40. EIB, http://www.eib.org/projects/pipeline/2015/20150058.htm, accessed 17 Apri l 2015

41. “Despite wave of infrastructure capital investment opportunities remain scarce,” Moodys, https://www.moodys.com/research/Moodys-Despite-wave-of-infrastructure-capitalinvestment-opportunities-remain-scarce--PR_326366, accessed 17 April 2015

42. “Jobs, Growth and Investment,” The European Community, http://ec.europa.eu/priorities/jobs-growth-investment/plan/docs/factsheet3-whatin_en.pdf, accessed 17 Apri l 2015

43. “Infrastructure project finance,” Moodys, https://www.moodys.com/researchandratings/market-segment/infrastructureproject-finance/005008/4294966386/4294966623/0/0/-/0/rr, accessed 17 April 2015

44. Moodys, https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBC_179524, accessed 17 April 2015

45. Moodys, https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBC_179348, accessed 17 April 2015

A ppendix

22 Infrastructure investments

ConclusionInfrastructure investments are an interesting option for an insurer’s portfolio. There are considerable benefits to such an investment, notably the competitive expected return (and return on capital under Solvency II) which could be achieved. Although not as inviting as a couple of years ago, spreads on infrastructure investments continue to lie within a range that would be of interest to insurers. In addition, the fact that certain infrastructure investments may provide real returns to match inflation-linked or real liabilities and the possibility that some assets could be eligible for the matching adjustment further demonstrate the range of potential benefits that an infrastructure investment portfolio could offer an insurer.

But despite these advantages, there remain ongoing managerial challenges and difficulty in sourcing such infrastructure assets. This scarcity, coupled with high demand, has a detrimental effect on the benefits and may erode advantages that infrastructure investments hold over more traditional assets. Insurers appear willing to invest and plan to continue doing so, at least while the apparent benefits seem to outweigh the costs.

2 3Infrastructure investments