23

Marko Bogoievski March 2010 Infratil Investor Day CEO Presentation 2010

Marko Bogoievski

March 2010

Infratil Investor DayCEO Presentation 2010

2

Infratil Investor Day 2010 – Agenda

Time Presenter

8.00 - 8.30 Registration

8.30 - 9.30 IFT Overview Marko Bogoievski

9.30 – 10.30 Australian Energy Simon Draper

10.30 - 10.45 Break

10.45 - 11.30 TrustPower Chris O’Hara

11.30 – 12.15 Shell NZ Mike Bennetts

12.15 – 12.45 Wrap-upMarko Bogoievski

Lloyd Morrison

12.45 Lunch

3

Objectives for the day

• Principal objectives:

- Introduce the team

- Update the facts

- Highlight the challenges and the opportunities

- Lay out the plan

- Get your perspective

• Focus is on material businesses with significant sector developments and key

choices

- Shell NZ deal pending completion, but good example of current focus

• WIAL, NZ Bus, European airports, Infratil property, Snapper – all have

significant plans and opportunities, but unlikely to materially impact the

overall view on IFT valuation in the short-term

4

Infratil – well placed for the future

The importance of infrastructure investment in the local and global

economy only continues to grow …

• Our approach to investment has performed well during market cycles and

changing investment trends

• Deleveraging and capital constraints have created significant opportunities

for experienced and well capitalised infrastructure investors

• Our operational capability and comfort with demand and price risk further

differentiates IFT from other infrastructure investors

• The core Infratil assets are very good businesses in the right sectors, with

significant re-investment potential

5

Key investor questions

• What is the investment proposition?

• Does IFT represent value?

• Does recent activity make sense?

• What’s the plan from here?

• Is the model right?

6

Infratil investment proposition

Equity exposure to growth infrastructure with significant optionality

• Specialist infrastructure investor targeting high total returns to shareholders

over the long-term

• Actively managed portfolio of high quality core assets and early stage

investments offering significant capital growth

• Dynamic capital allocation to high return projects through controlling stakes

in key investments

• Ongoing origination activity and new business development

• Financial flexibility and risk management complemented by unique vantage

point in Australasian investment markets

• Management team and track record

7

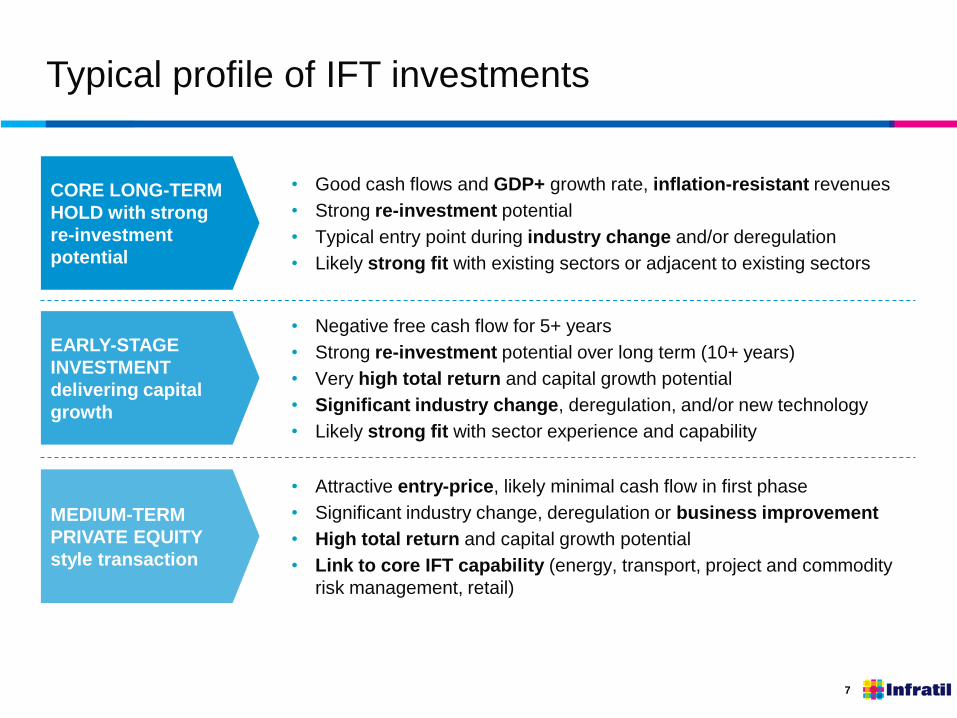

Typical profile of IFT investments

CORE LONG-TERM

HOLD with strong

re-investment

potential

• Good cash flows and GDP+ growth rate, inflation-resistant revenues

• Strong re-investment potential

• Typical entry point during industry change and/or deregulation

• Likely strong fit with existing sectors or adjacent to existing sectors

EARLY-STAGE

INVESTMENT

delivering capital

growth

MEDIUM-TERM

PRIVATE EQUITY

style transaction

• Negative free cash flow for 5+ years

• Strong re-investment potential over long term (10+ years)

• Very high total return and capital growth potential

• Significant industry change, deregulation, and/or new technology

• Likely strong fit with sector experience and capability

• Attractive entry-price, likely minimal cash flow in first phase

• Significant industry change, deregulation or business improvement

• High total return and capital growth potential

• Link to core IFT capability (energy, transport, project and commodity

risk management, retail)

8

Getting the balance right is critical …

IFT Portfolio Mix (illustration only)

CORE Cash Flow +

CORE Capital Growth

SUPP Private Equity

Other

9

Key investor questions

• What is the investment proposition?

• Does IFT represent value?

• Does recent activity make sense?

• What’s the plan from here?

• Is the model right?

10

IFT total returns peaked at 26% p.a. in 2007 …

$100 invested in IFT on 1 April 1994 would have accumulated to $1,312 by 7 March

2010 (17.5% p.a. compound)

-1000

-500

0

500

1000

1500

2000

-40%

-20%

0%

20%

40%

60%

80%

1994 1996 1998 2000 2002 2004 2006 2008 2010

Accumulation Index

Annual Return

Annual Return Annual Dividend Return Infratil Accumulation Index

11

A view from the analysts …

$M

Infratil

March 2010

Average Broker

Valuation 17/11/09

TrustPower $1,153 $1,309

Infratil Energy Australia $207 $284

Wellington Airport $285 $306

Infratil Airports Europe $146 $151

NZ Bus $212 $209

Other $54 $40

Total Assets $2,057 $2,299

Debt ($810) ($810)

Management contract - ($107)

NTA $1,247 $1,382

IFTWB Proceeds $43 $43

NTA/Share $2.13 $2.36

Gap at $1.66 29% 42%

12

Allocating the NTA discount isn’t easy

• TPW, WIAL trade on a multiple to sustainable

earnings

• NZ Bus, VEL/IEA at book value

• IAE at negative free cash flow valuation

• IFT Property probably ignored

Considerations:

1. VEL – potential for re-rating when retail profitability

is sustained (currently just valuing customer base)

2. NZ Bus – uncertainty over appropriate multiple and

future free cash flow

3. Shell NZ – question mark over whether it is a PE

deal or long-term asset with decent reinvestment

potential?

POTENTIAL DISCOUNT

FACTORS:

- Performance

- Outlook

- Management model

- Absolute gearing and

leverage

- Holdco structure and

parent company debt

- Reinvestment risk / or

lack of growth?

- Lack of marginal buyers

Focus always comes back to performance

13

Key investor questions

• What is the investment proposition?

• Does IFT represent value?

• Does recent activity make sense?

• What’s the plan from here?

• Is the model right?

14

2009/10 – a productive 12 months

The investment approach has remained constant and focused

• Operational results

- Strong TPW and WIAL earnings (about 70% of assets), respectable NZ Bus result

- Started next phase of investment and growth in IEA/VEL

- Disciplined approach to containing Glasgow and Kent airport negatives

• Portfolio activity

- $393m realised since March 31, 2009 across 5 properties

- $16m EBITDA leakage in divested assets ($133m in excess of BV)

- Over $230m of new capex deployed in high-return internal projects

- Close to major Shell NZ transaction (although not complete)

• $425m debt reduction – debt reduced to $810m from $1,210m

• $100m raised in new equity, and $43m more scheduled for May 2010

15

Forecast performance to March 31, 2010

• Second half NPAT will

benefit from $100m gains

on sale of ENE and AIA

• Negative mark to market

movements on forward

energy hedges in Australia

likely to drive Group

derivative losses to around

$40m – but dependent on

prices in March

2010 operating earnings (EBITDAF) and capital expenditure consistent

with half year guidance (after adjusting for divestments)

0

500

1,000

1,500

2,000

2,500

0

50

100

150

200

250

300

350

400

1998 2000 2003 2006 2009

IndexEBITDAF ($M)

EBITDAF Year End

IFT Accumulation Index

16

Shell NZ – how does downstream oil fit with IFT?

• Potential CORE+ asset with significant business

improvement opportunity in a rapidly changing

industry

• Market leader in most segments with very

competitive cost base and access to critical

energy-related infrastructure

• Quality portfolio of commercial customers and

retail sites

• Should respond well to selective investment

after many years of limited available capital

• IFT familiarity with energy and transport

supplemented by industry hires and third-party

advisors where necessary

• Opportunity to create a substantial NZ business

17

Key investor questions

• What is the investment proposition?

• Does IFT represent value?

• Does recent activity make sense?

• What’s the plan from here?

• Is the model right?

18

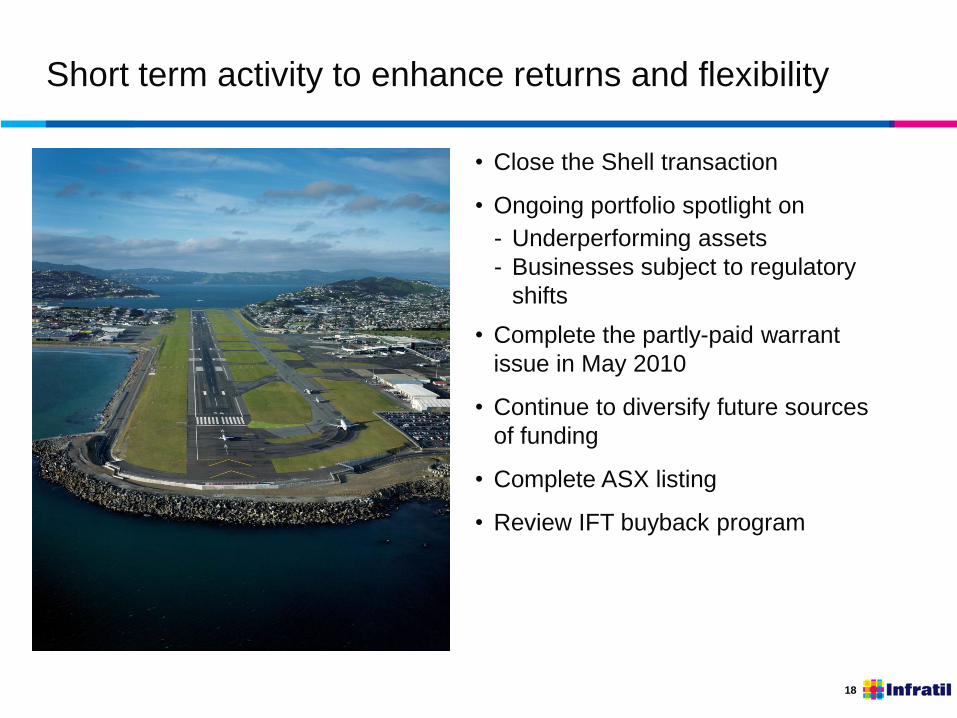

Short term activity to enhance returns and flexibility

• Close the Shell transaction

• Ongoing portfolio spotlight on

- Underperforming assets

- Businesses subject to regulatory

shifts

• Complete the partly-paid warrant

issue in May 2010

• Continue to diversify future sources

of funding

• Complete ASX listing

• Review IFT buyback program

19

Medium term investment program and outlook

• Group capex depends on TPW (wind

and irrigation) options and Australian

energy (generation and retail)

• Discretionary capex continues to be

carefully controlled – particularly in

sectors undergoing regulatory

reviews (public transport and airports)

• Origination activity is largely focused

on energy and transport opportunities

in Australia and NZ, although:

- Market scans are constantly conducted

across a broad range of infrastructure

sectors, and

- IFT has the ability to respond to

opportunistic situations

Projected IFT asset mix March 31, 2010

TrustPower

Infratil Energy Australia

Wellington Airport

European Airports

Public Transport/Property

20

Key investor questions

• What is the investment proposition?

• Does IFT represent value?

• Does recent activity make sense?

• What’s the plan from here?

• Is the model right?

21

Clarifying the investment story

Question Clarification

1 Is Infratil a specialist infrastructure investor or an

absolute return investment manager with a broad

infrastructure mandate?

Infratil is a specialist infrastructure

manager targeting investments benefiting

from long-term trends or industry change

2 Should Infratil have a tighter sector focus? Increasing energy bias

3 Should Infratil have a tighter geographic focus? Increasingly focused on investment

opportunities in Australia and NZ

4 What is the appropriate absolute level of

indebtedness?

Medium term metrics consistent with the

bottom end of investment grade credit

5 What is the appropriate capital structure? Debt next to cash flows where possible

6 Is Infratil an active manager? Active manager with influential stakes

7 What is the appropriate targeted return profile?

(and related dividend yield)

Maintain high absolute return targets over

the long-run, although this will be harder

given reduced leverage

22

Infratil – the bottom line

• Investment approach has withstood the test of time

• Operational capability enables IFT to pursue more difficult but rewarding

growth infrastructure opportunities

• Last 12 months of activity will improve performance and considerably

tighten the focus of IFT

• Internal pipeline of projects provides good visibility about future capex

opportunities and projected returns

• Pace of origination improving as second-order effects of financial crisis

result in dislocation and less competition for attractive assets

• Financial flexibility and co-investment model enables IFT to be a player

in material opportunities in Australia and NZ

www.infratil.com