REVIEW OF OPERATIONS ING BELGIUM WITHIN ING GROUP ING Group ranks among the leading financial institutions in Europe and worldwide. Its management structure is divided into business lines. Even though it separates banking and insurance, this structure retains the integrated services model in countries such as Belgium, where it has been successfully developed. Following the example of its parent company, ING Belgium has organised its structure along two business lines: Retail & Private Banking and Wholesale Banking. 12 ANNUAL REVIEW 2005 ING BELGIUM

Transcript

R E V I E W O F O P E R A T I O N S

ING BELGIUM WITHIN ING GROUPING Group ranks among the leading financial institutions in Europe

and worldwide. Its management structure is divided into business lines.

Even though it separates banking and insurance, this structure retains

the integrated services model in countries such as Belgium, where it

has been successfully developed. Following the example of its parent

company, ING Belgium has organised its structure along two business

lines: Retail & Private Banking and Wholesale Banking.

12 ANNUAL REVIEW 2005 ING BELGIUM

ING BELGIUM ANNUAL REVIEW 2005 13

BRIEF HISTORY OF ING GROUP

ING Group is an international financial institution of Dutch ori-

gin whose main components can be traced back 150 years. The

Group was created in 1991 by merging the insurance comp-

any Nationale-Nederlanden and the banking group NMB

Postbank Groep, both formed out of previous mergers. Since

then, ING Group has seen steady expansion, driven by major

acquisitions and by the organic growth of its component com-

panies.

ING Group operates in the fields of banking, insurance and

asset management. It currently employs over 115,000 staff,

servicing more than 60 million customers in some 50 coun-

tries spread across five continents. In terms of market

capitalisation, ING Group ranks among the top ten financial

groups in Europe and among the top 20 worldwide.

Its strategy has a two-pronged approach:

• quality of execution, the main underlying concepts of which

include creating value, aiming for customer satisfaction, cost

and risk management, and generating a performance-led

culture;

• growth, which is sought simultaneously via expansion in

emerging markets and by upholding excellent performances

in mature markets.

ING GROUP STRUCTURES

Legal structureThe ING Group legal structure is formed by a holding com-

pany, ING Groep N.V., which owns and controls two other

holding companies:

• ING Bank N.V., covering all its banking and financial-

services companies;

• ING Verzekeringen N.V., grouping together insurance com-

panies.

In accordance with Dutch company law, the strategy and

day-to-day management of ING Groep N.V. is handled and

defined by an Executive Board (Raad van Bestuur). The

Executive Board is overseen by a Supervisory Board (Raad van

Commissarissen), exclusively composed of independent mem-

bers, as required by the Dutch Code of Corporate Governance.

The Executive Board currently comprises Michel Tilmant (Chief

Executive Officer and Chairman of ING Groep N.V.), Cees Maas

(Chief Financial Officer and Vice-Chairman of ING Groep N.V.),

Eric Boyer de la Giroday, Fred Hubbell, Eli Leenaars, Alexander

Rinnooy Kan, and Hans Verkoren (Executive Board members).

Fred Hubbell, Alexander Rinnooy Kan and Hans Verkoren have

given notice that they intend to resign at the end of the Annual

General Meeting of Shareholders of 25 April 2006.

The Supervisory Board will propose to the Annual General

Meeting to appoint Tom McInerney, Chief Executive Officer

of ING US Financial Services, Jacques de Vaucleroy, Group

Chairman of ING Retail within ING US Financial Services, Hans

van der Noordaa, Chief Executive of ING Retail in the

Netherlands, and Dick Harryvan, Chief Financial Officer and

Chief Risk Officer of ING Direct, to the Executive Board.

Management structureThe Group's management structure complements its legal

structure. It is centred on six business lines, each operating

under the direct responsibility of an Executive Board member 1.

A geographic breakdown has been favoured for insurance and

asset management 2:

• Insurance Americas covers life and non-life insurance busi-

ness and asset management in North and Latin America;

• Insurance Europe is responsible for life and non-life

insurance business and asset management in Europe;

• Insurance Asia/Pacific covers life insurance business and

asset management in the Asia-Pacific region.

Banking, on the other hand, is broken down by business:

• Wholesale Banking covers investment banking and finan-

cial markets activities exercised in the Benelux countries and

in the main international centres;

• Retail Banking combines retail banking in the Netherlands,

Belgium, Luxembourg, Poland, Romania and India; Retail

Banking also covers life and non-life insurance business in

Belgium and Luxembourg, owing to close links with the

banking network in these countries; Retail Banking also

covers private banking in selected markets such as the

Benelux countries, Switzerland, and some Asian countries;

• ING Direct covers direct banking business in France, the

United Kingdom, Germany, Austria, Italy, Spain, the United

States, Canada, and Australia. ING Direct currently focuses

its action on savings and mortgage products. It also manages

a credit cards portfolio in the Benelux countries via ING Card.

ING BANK N.V.

BANKING SUBSIDIARIES

ING VERZEKERINGEN N.V.

INSURANCE SUBSIDIARIES

ING Group legal structure

ING GROEP N.V.

1 See p.14 / 2 A central entity co-ordinates international asset management. It is headed by Tom McInerney.

ING BELGIUM WITHIN ING GROUP

14 ANNUAL REVIEW 2005 ING BELGIUM

ING BELGIUM: FINANCIAL AND MANAGERIAL SCOPE

The primary objective of the present Annual Review is to

describe the activities and analyse the results of a vast ensem-

ble consisting of ING Belgium SA/NV and the principal business

units consolidated by the former.

It will also allude to the banks’ managerial responsibilities,

entrusted by ING Group, in six countries: - Luxembourg, France,

Switzerland, Italy, Spain, and Portugal- that, with Belgium,

make up the South West Europe region. In some cases, this

managerial responsibility is exercised in towards companies

outside the ING Belgium consolidation scope.

In each of the six countries, a Country Management

Committee, headed by a Country General Manager, is

responsible for co-ordinating local activities. The Country

General Manager also has the task of representing ING Group

to national authorities and regulatory bodies.

Within ING Belgium, a co-ordination office assists the Executive

Committee with carrying out its regional responsibilities.

At the beginning of April 2006, the insurance company, ING

Nationale-Nederlanden Spain was removed from the manage-

rial responsibility of ING Belgium and placed with Insurance

Central Europe, part of Insurance Europe. This decision trans-

lates the desire to place the company in a portfolio specifically

dedicated to insurance activities; in addition, the companies

regrouped within Insurance Central Europe all work with tied

agents, which simplifies management.

* Subject to approval by the Annual General Meeting.

INSURANCE AMERICASFred Hubbell

INSURANCE EUROPEFred Hubbell -

Alexander Rinnooy Kan

INSURANCEASIA/PACIFIC

Alexander Rinnooy Kan

WHOLESALE BANKINGEric Boyer

de la Giroday

RETAIL BANKINGEli Leenaars

ING DIRECTHans Verkoren

EXECUTIVE BOARD

INSURANCE AMERICASTom McInerney

INSURANCE EUROPEJacques de Vaucleroy

INSURANCEASIA/PACIFIC

Hans van der Noordaa

WHOLESALE BANKINGEric Boyer

de la Giroday

RETAIL BANKINGEli Leenaars

ING DIRECTDick Harryvan

EXECUTIVE BOARD

Until 25 April 2006

From 25 April 2006*

ING Group management structure

R E V I E W O F O P E R A T I O N S

RETAIL & PRIVATE BANKING ING Belgium has grouped retail and private banking together in the same

business line. This structure, served by a unique product management unit,

allows the bank to maximise synergy between the two types of activity, via its

branches and alternative channels. ING’s second Belgian retail network, Record

Group, a subsidiary of the bank, continued to expand as a result of organic

growth and acquisitions. Following the takeover of Eural, it now ranks as the

third-largest savings bank in Belgium.

ING BELGIUM ANNUAL REVIEW 2005 15

16 ANNUAL REVIEW 2005 ING BELGIUM

RETAIL & PRIVATE BANKING

ING BELGIUM RETAIL & PRIVATEBANKING

ING Belgium's Retail & Private Banking business line is centred

on three main fields nation-wide:

• Retail Distribution;

• Private Banking;

• Product Management.

Retail DistributionThe Retail Distribution line determines the sales policy

applicable to individuals, professionals and small firms. It is

also responsible for the branch network.

Highlights of the year under reviewThe year was marked by the success of sales campaigns con-

ducted with a view to acquiring new customers. These took

the form of either promotional campaigns targeting one pro-

duct, or initiatives intended to highlight the proximity of the

bank:

• ING Belgium capitalised on its shrewd positioning with regard

to mortgage loans, with annual production exceeding 30,000

transactions;

• the same also applied to the launch, in March 2005, of the

ING Card, more than 72,000 of which were sold during the

nine months that followed;

• campaigns targeted at young people were a runaway success

among children of customers and non-customers; the bank

observed a significant increase of more than 25,000 customers

in this segment;

• finally, "open door days" organised in September attracted

some 100,000 visitors, including 25,000 prospects; they also

significantly raised the bank's public profile.

In net figures, ING Belgium boosted its sales portfolio by 58,000

personal and business customers in 2005.

Deposit accounts outstanding, opened in the name of retail

customers, rose year on year from EUR 14.7 billion to EUR

15.1 billion (up 3%), as a result of campaigns targeted at the

temporary increase in the growth premium.

The take-up of financial products posted a further increase. The

main driving forces behind this increase were structured notes,

the Optima insurance account, and mutual funds adopting the

most efficient investment strategy 1.

With regard to recurring savings, the year-end pension cam-

paign allowed the bank to reinforce its positions.

It was also an excellent year for the non-life insurance sector,

which posted 15% growth in sales of the Global Home and

Family Insurance, Assistance and Motor policy.

Network structureThe Belgian network comprises nine Retail & Private Banking

regions: Antwerp, North Brussels, South Brussels, Hainaut,

At the end of 2005, the bank had a total of 807 branches,

compared with 819 the previous year. 234 branches were run

by self-employed agents, compared with 225 at the end of

2004.

Direct bankingFor many years, ING Belgium has continuously implemented

a multichannel distribution strategy. The direct banking solu-

tions developed have a common denominator: optimising the

day-to-day account management and carrying out main

banking transactions, which allows traditional branches to

focus on personalised advice. Direct banking is included, there-

fore, in a consistent, integrated sales approach, which

enables customers to choose, at any time, the channel that

best matches their needs.

ING Belgium has more than 830 Self’Bank sites accessible

seven days a week between 5 am and 11.30 pm. Most of these

sites are adjacent to a traditional branch. Three quarters of the

bank's customers actively use the some 2,700 machines avail-

able: more than 96 million transactions were recorded in 2005.

The bank continued the installation of "Cash in/Cash out"

machines at its Self'Bank sites allowing euro banknotes to be

deposited, counted and immediately credited to the account:

87 such machines are currently in operation. In July 2005, the

bank also took over some 110 Banksys ATMs installed in the

front of its branches. On 3 February 2006, the Self'Bank net-

work became accessible to all holders of bank cards issued in

Belgium for cash withdrawals and loading the Proton function.

The number of active users of online Home’Bank has

increased, year on year, from 209,000 to 270,000 (up

29.2%) 2. At the same time, the number of sessions jumped

from 36 million to 46 million (up 27.8%), while the number

of payment transactions rose from 21 million to 26 million (up

23.8%).

There was a 37% increase in the total number of transactions

using the online secure payment system, Home’Pay.

1 See the section, "Third-party asset management", in the chapter "Specialised products and services" / 2 As the bank has toughened up the criteria defining the concept of active user, thestatistics are not comparable with those of the 2004 report.

ING BELGIUM ANNUAL REVIEW 2005 17

The SMS service for sending account balances, available

credit-card limits, and estimated securities account balances con-

tinued to be a genuine success, with over 800,000 messages.

Depending on callers' requirements, Phone’Bank gives access

either to an interactive voice server for obtaining quick infor-

mation or for carrying out main transactions on an account,

or to one of the 150 ING Contact Centre specialist advisers

for one-to-one assistance. The centre fields around 600,000

calls and replies to 120,000 e-mails every year. The team pro-

vides advice and offers a sales and after-sales service on the

telephone for ING Belgium's products. It is responsible for

answering customers and non-customers using the bank's

information lines and conducts telemarketing campaigns. Help-

desk technicians field queries relating to the installation and

use of Home’Bank.

The bank promotes its products and services on the website.

Thanks to its interactive nature, this also contributes to acquir-

ing new customers. Numerous simulators, linked to reply forms,

allow the public to contact the bank. Following up these leads

is coordinated by ING Contact Centre.

In 2005, the bank mainly worked on improving the presen-

tation and layout of its website. The home page 1 has a series

of coloured boxes, and each sales campaign now has a devot-

ed promotional sub-site. The tracking statistics confirm the

validity of these options: the number of visitors almost

doubled during the second half year (up 87%), while 135,000

people were interested in the promotional sites.

The site also contains an e-commerce platform, ING Shop, giv-

ing access to a number of online stores and where tickets can

be ordered for various events 2. Payment is carried out com-

pletely securely via Home'Pay.

Private BankingHighlights of the year under reviewFollowing the excellent performance posted in 2003 and 2004,

ING Private Banking continued its expansion at a significant

rate. Total assets under management stood at EUR 12.4 bil-

lion at the close of 2005, a rise of 19%. For the last two

financial years, cumulative growth was 51% 3.

This rise can be attributed to several factors:

• the scale of commercial synergies with the Retail and

Wholesale business lines;

• the repatriation of capital following the Belgian Tax

Amnesty ("DLU/EBA");

• intense M&A activity in the SMEs segment, with each trans-

action generating significant funds for the vendor(s);

• bullish stock markets for most of the year.

Network structureThe structure of the Private Banking network has been worked

out so that it maximises the obvious synergies existing with

Retail Banking.

The National Private Banking Manager has the dual role, there-

fore, of line manager for his entire line, while maintaining a

functional link with each Retail & Private Banking Regional

Manager.

He, in turn, is supported by:

• two Private Banking Regional Managers, one in charge of

Flanders, the other responsible for Brussels and Wallonia,

who have a functional authority over the Private & Personal

Banking Managers in their areas;

• the portfolio management teams at ING Private Portfolio

Management SA/NV;

• a Private Trading Desk, dedicated to customers who are par-

ticularly active in financial markets.

Product ManagementThis department is responsible for developing products

aimed at retail, professional, corporate 4 and domestic private

banking customers, and for managing these products for their

entire life cycle. It is organised into four main divisions: invest-

ments, loans, insurance products and "convenience" products,

such as accounts, payment methods and cards 5.

The department also assumes overall responsibility for the

effectiveness of the value chain, i.e. the entire product devel-

opment and marketing process. To do this, it joins forces with

specialist entities, including Business Information Systems and

operational departments 6. Against this backdrop, nine value

1 www.ing.be / 2 www.ingshop.be / 3 Non-consolidated data relating to ING Belgium SA/NV / 4 This comprises small and medium-sized enterprises whose annual turnover does not exceedEUR 4 million. Over this limit, companies fall under Wholesale Banking / 5 A considerable portion of these products, most notably convenience products, are also marketed to WholesaleBanking customers / 6 See the chapter, "Operations & Information Technology".

18 ANNUAL REVIEW 2005 ING BELGIUM

chain teams were set up in 2005. Under the aegis of Product

Management, they are responsible for managing the differ-

ent value chains, in collaboration with all the parties

concerned within the bank. Their area of competence relates

to savings, investment, standard loans, “tailor made” loans,

healthcare, loss insurance, accounts, payments, and customer

databases. This modus operandi allows the processes to be

managed in an effective and co-ordinated manner.

An in-depth analysis has been conducted within ING Group

with a view to harmonising the range of products and pro-

cesses offered in Belgium and in the Netherlands. The aim is

not to integrate the existing entities, but to entrust them with

the task of jointly building the retail bank of the future for

the Benelux. A certain number of external events that promote

European-wide harmonisation of the retail market are per-

ceived as opportunities by ING. The most noticeable example

in this respect is the setting up of a Single European

Payment Area (SEPA), planned for 2008-2010.

The Product Management Department was set up in the

autumn of 2004. Its first financial year over, it has already com-

pleted a number of projects, mainly including:

• rationalisation of the range of short-term notes and sub-

ordinated bank savings certificates;

• rationalisation of the range of credit facilities for retail cus-

tomers;

• successful rollout of the ING Card, a credit card with revolv-

ing credit;

• launch of an automated tool for assessing medical risks,

authorising online acceptance of an insurance file handled

in a branch 1;

• scrutiny of procedures relating to mortgage and consumer

loans, short-term notes, and subordinated bank savings cer-

tificates in the context of the Sarbanes-Oxley law.

SECOND BELGIAN RETAIL NETWORK:RECORD GROUP

Record Group, second ING banking network in Belgium, com-

prises three entities:

• Record Bank SA/NV, whose business is described in more

detail below;

• Record Credit Services SCRL/CVBA, which manages credit

portfolios;

• Fiducré SA/NV, a subsidiary of Record Bank SA/NV, which

acts as a debt-recovery specialist on behalf of ING Group

or non-affiliated companies.

Record Bank SA/NV is a wholly-owned subsidiary of ING

Belgium. It has a two-fold remit:

• developing a retail bank targeted at retail customers, the

self-employed, professionals, and family-run businesses; it

fulfils this remit via a network of self-employed banking

agents; it offers a range of savings, investment, credit and

insurance products;

• the sale of consumer loans, home and business loans

through various distribution channels, such as lending inter-

mediaries and vendors 2.

Following the absorption of Westkrediet (2002), AGF Belgium

Bank (2003), and Mercator Bank (2004), the next phase of

external growth was achieved in 2005 with the takeover of

Eural from the Dexia Group. This was concluded by ING

Belgium on 1 December 2005, with the aim of integrating the

new acquisition in Record Bank during 2006. Record Bank now

has a network of some 900 professional banking agents

throughout Belgium, serving over 500,000 customers.

External growth was again underpinned by significant organic

growth. These combined resulted in Record Bank becoming the

third largest savings bank in Belgium, with total deposits of EUR

8.5 billion and credits outstanding verging on EUR 5 billion.

Highlights of 2005 included the growth in mortgage loans,

which passed the EUR 1 billion mark for the first time. It was

also a good year for consumer loans.

The operational integration of Mercator Bank proved to be

trickier than expected, which put staff and Record Bank agents

under considerable pressure during the months that followed

the merger. The situation has stabilised since then. The opti-

misation of processes will be continued during the first few

months of 2006.

1 See the section "Insurance", in the chapter, "Specialised products and services” / 2 Mostly affiliated garages and franchised traders.

RETAIL & PRIVATE BANKING

ING BELGIUM ANNUAL REVIEW 2005 19

A new generation of “package” applications will be installed

with a view to the operational merger with Eural, planned for

next autumn.

In terms of product development, Record Bank launched its

own structured notes. It expanded its range to include the

Record Top Pension Fund. It also developed a range of busi-

ness loans, for which it worked out a specific acceptance policy.

From 2006 onwards, Record Bank will sell insurance products

alongside its banking products, such as mortgage protection

and investment insurance. The groundwork for rolling out this

new activity was carried out in 2005.

The advertising campaign launched in 2004 based on the slo-

gans "My own bank", "My own loan", "My own broker" was

resumed in 2005. A more assertive presence, coupled with a

more pro-active policy with regard to advertisements in the

national press and local media, should continue to increase

Record Bank's profile.

As already mentioned, Record Credit Services SCRL/CVBA

is specialised, within Record Group, in credit portfolio man-

agement, of which the large majority originate from Record

Bank. The company's financial year was in line with previous

years. It will be able, therefore, to pay out an attractive divi-

dend to its co-operators in 2006.

Fiducré SA/NV also boosted its outstanding recoverable debts

thanks to the purchase of a number of major portfolios.

R E V I E W O F O P E R A T I O N S

WHOLESALE BANKINGThe Wholesale Banking business line combines two major contributors

to ING Belgium's income: firstly, the departments servicing corporate

and institutional customers, and secondly, financial markets. In line with

ING Group's "volume to value" strategy, the overall economic return of

a relationship is favoured, rather than its mere book profitability.

20 ANNUAL REVIEW 2005 ING BELGIUM

ING BELGIUM ANNUAL REVIEW 2005 21

The structure of ING Belgium Wholesale Banking business line

is identical to that of the Group.

CORPORATE AND INSTITUTIONAL CUSTOMERS

Four main entities are dedicated to the corporate and insti-

tutional customer segment:

• as its name suggests, Wholesale Banking Clients is respon-

sible for forging relationships with customers; it comprises

the Corporate Banking and F inanc ia l Inst i tut ions

Departments;

• Wholesale Banking Network coordinates the operational

models applicable in the seven countries making up the

South West Europe region;

• Wholesale Banking Products is responsible for devising and

managing products and, as for Retail & Private Banking, is

kept separate from the relationship aspect;

• a fourth entity combines the Corporate Finance and Equity

Markets Departments.

Wholesale Banking ClientsCorporate BankingThe Corporate Banking Department, which is part of Wholesale

Banking Clients, is responsible for corporate customers in the

South West Europe region, with an annual turnover in excess

of EUR 4 million 1.

In Belgium, the Corporate Banking Department heads up a

Domestic Wholesale Division, which targets:

• medium-sized companies with a turnover of between

EUR 4 million and EUR 250 million; it also co-ordinates a

network of seven Domestic Wholesale regions 2, relayed by

14 local business centres, for effective national coverage;

the bank's aim, with regard to this segment, is to become

the leading bank servicing its customers;

• institutional customers such as supranational organisations,

local authorities, hospitals, convalescent homes, congrega-

tions, insurance companies, universities and colleges,

labour unions, and pension funds; in this segment, the bank

stands out as a "challenger".

The Corporate Banking Department is also directly responsible

for large corporates with turnover in excess of EUR 250 mil-

lion. The relationship is managed on two levels:

• parent account managers (PAMs) liaise with the parent com-

pany and are the preferred point of contact of its senior

management; they are mainly called on to resolve strategic

problems;

• for day-to-day and local matters, the senior managers are

assisted by a team of local account managers (LAMs) as well

as product specialists, according to requirements.

Financial InstitutionsTogether with ING Bank Nederland, ING Belgium's Financial

Institutions Department has set up a joint platform dividing

geographical responsibilities. As such, ING Belgium is respon-

sible for Southern Europe, Germany, Switzerland, Austria,

Africa, and most Far Eastern countries.

Its customers include retail, merchant and savings banks, leas-

ing and factoring companies, insurers, investment funds and fund

managers, and international and supranational organisations.

To this diverse customer target, the department offers an

extensive range of products and services, some of which, such

as clearing, payments, and credit facilities, come under its

direct responsibility. Otherwise the sales approach is carried

out jointly with specialist departments.

Clearing and payments services have been one of the depart-

ment's long-standing strong points. They act as the focal point

for many other relationships. ING Group, for which ING

Belgium is designated as a centre of excellence in this field,

owes its prime position in the restricted circle of internation-

al financial institutions operating in the market to the major

efforts made in recent years in terms of human resources and

investment. Its offer is in line with the aim of banks to limit

the number of counterparts in international accounts and pay-

ment flows.

ING Belgium continues to be involved with the confirmation

of documentary credits covering its corporate customers'

exports to emerging markets. It also continues to provide

dynamic management of its international trade risk portfolio,

by maintaining an active presence in the secondary market for

this type of transaction.

The range of services promoted by the Financial Institutions

Department is regularly expanded: at present, it integrates cap-

insurance, employee benefits, M&A, and consultancy to gov-

ernments and financial institutions in emerging countries.

1 Below this limit, companies come under Retail & Private Banking / 2 Antwerp, Brussels, Hainaut-Namur, Liège, Limburg-Leuven, Oost-Vlaanderen and West-Vlaanderen.

22 ANNUAL REVIEW 2005 ING BELGIUM

WHOLESALE BANKING

Counterpart risks are managed in close collaboration with the

Risk Management Department. In addition to setting up and

monitoring credit lines to cover short-, medium- and long-term

financial markets transactions, we should highlight individual

and bilateral credits, as well as syndicated deals regularly led

by the bank. Risk selection, which calls into play the sales

teams' excellent know-how of their counterparts, and the

rigour that prevails during analyses and decisions, have kept

the total loss rate at an extremely low level in recent years.

Wholesale Banking ProductsThe devising and management of products is deliberately kept

separate from the relationship aspect.

However, the complex nature of problems arising for corpor-

ate and institutional customers often results in tailor-made

solutions. Once the requirement has been identified by the rela-

tionship manager and forwarded to the specialist, they join

forces to resolve the problem. However, the relationship

manager will assume the responsibility for determining

whether the worked-out solution responds effectively to the

customer's requirements and, if it does not, will ask the spe-

cialist to modify it.

Specialists are based in the actual business centres, at close

proximity to customers, for standard products, such as treas-

ury management, arbitrage and insurance.

The need for more specific expertise is, by definition, more

infrequent. This is why it is focused in Brussels, where it is

made available to the business centres. Apart from this respon-

sibility, the staff in question regularly receives international

assignments.

Corporate Finance & Equity MarketsOwing to their complementary nature, both businesses have

been combined in the same line so that customers are offered

a complete service covering the primary and secondary markets,

while adhering to local regulatory restrictions. Synergies are in

place with the Financial Markets and Private Banking lines.

Corporate FinanceThis department had an excellent year.

It acted as a consultant for fourteen mergers and acquisitions.

For the third year running, it came top of the "Mergermarket"

professional ranking for the number of takeovers involving a

Belgian company. This mainly included the sale of Aviapartner

to a joint venture formed from some of the company's man-

agement and 3i.

In the traditional capital markets, ING Belgium acted as a joint

global coordinator during the reinvestment of GIMV shares by

the Vlaamse Participatiemaatschappij (VPM), and Arcelor shares

by Société de gestion des participations de la Région wallonne

(SOGEPA). ING Belgium was also the joint book-runner for the

flotation of BioAlliance Pharma on the Paris-based Euronext

Stock Exchange and was part of the placement syndicate for

Elia's flotation on the Brussels Stock Exchange.

As in 2004, the bank acted as trustee on behalf of the

European Commission, as part of the major merger between

Group4Falck and Securicor.

The collaboration with Corporate Banking resulted in another

record year for the department as regards funding acquisitions

and mezzanine financing.

The department also made three private equity disinvestments

and carried out a series of new and additional investments.

Equity MarketsEquity Markets, which employs more than 100 staff through-

out the South West Europe region, carries on its activity from

a functional platform set up in 2003. Operating in eight major

European cities, including London, Amsterdam, Paris, and

Brussels, this structure targets institutional customers in

Western and Eastern Europe, approached via sales teams and

specialist analysts.

With a strong presence in ING Group's two main domestic mar-

kets, it focuses on the quality of its Benelux product. The

appreciation shown by its major international customers is a

direct result of the investment that has been made in terms

of research, distribution, and trading during the last 18 months.

The Equity Markets teams have set themselves the target of

ranking among the European top ten, and the Benelux top

three.

ING BELGIUM ANNUAL REVIEW 2005 23

FINANCIAL MARKETS

The Financial Markets Department has a three-pronged

structure: Assets and Liabilities Management, the Strategic

Trading Platform, and the Customers & Products line. The first

two entities carry out their activities on behalf of the bank.

The Customers & Products line is mainly, but not exclusively,

targeted at customers.

In 2005, Financial Markets was among the departments apply-

ing the "value chain management" concept, which gauges the

impact of support activities and IT costs in particular for each

product 1.

The Financial Markets Department has always been a substan-

tial contributor to the bank's income. Although the year under

review was remarkable, it was not able, however, to repeat

the outstanding performance posted in 2004.

Assets and Liabilities ManagementThis ad hoc division oversees the bank's liquidity and the bal-

ance sheet management policy decided by the Executive

Commitee.

Strategic TradingThis entity takes care of the bank's strategic positioning.

Customers & ProductsGeneral overview This division offers corporate and institutional customers and

other Group entities, including the retail network, unrestrict-

ed access to the main financial markets, developed and

emerging.

The product range includes credit and equity derivatives, li-

quidity products, interest rate and exchange rate derivatives,

structured products, financing of security issues, and the issue

of company and government bonds.

ING Group's financial markets activity is carried on in Western

and Eastern Europe, Asia, the USA and Latin America. It is assist-

ed by teams on the ground that have a thorough knowledge

of their local market, in addition to a top-level research depart-

ment that is highly specialised in the emerging markets.

Debt MarketsING Belgium's Debt Markets Division reports to the Customers

& Products line of the Financial Markets Department.

Integrated in the ING Debt Markets platform, it finalises bond

issues on behalf of companies and government and quasi-

government organisations.

In 2005, the total issued volume represented the exchange

value of USD 2,821 billion, compared with USD 2,151 billion

in 2004 and USD 1,713 billion in 2003.

The volume issued in euros for companies continued to drop,

from EUR 161 billion in 2003 to EUR 102 billion in 2004, and

to EUR 95 billion in 2005. The main trends included the

increased number of telecoms issuers, which jumped from 14%

in 2004 to 21% in 2005, and the reduced number of auto-

motive manufacturers, which fell from 30% to 19%. The latter

trend is explained by the downgrading of General Motors and

Ford to speculative investment status (junk bonds) in the first

quarter of 2005. In the euro-denominated “corporate”

issues compartment, the ING Debt Markets platform took the

lead management for companies such as KPN and General

Electric. It also managed a large number of loans for emerg-

ing issuers in Eastern Europe, such as Evraz Steel, JSC Open

Investments, and Central European Distribution Corporation

(CEDC).

INTERNATIONAL BOND MARKET - BREAKDOWN BY TYPE OF ISSUERFor all currencies, as %

2005 2004 2003 2002 2001

Corporates 12 14 21 23 32

Financial institutions 58 56 46 42 37

Governments 9 9 8 7 5

Regions 1 1 2 2 2

Other public issuers 16 17 20 22 21

Supranational organisations 4 3 3 4 3

1 See the section, "Product Management", in the chapter, "Retail & Private Banking".

24 ANNUAL REVIEW 2005 ING BELGIUM

The year was also marked by a large number of long-term debt

issues on behalf of sovereign and quasi-sovereign issuers, and

by numerous inflation-linked bonds. Poland, Austria, and

Hungary rose 15-year funding; the Netherlands, Spain,

Greece, and the European Investment Bank opted for the

30-year segment, whereas France managed to raise 50-year

funding. The ING Debt Markets platform remained active

in the sovereign bonds segment: it was appointed by the

Dutch and Greek governments to manage large-scale euro-

denominated bonds.

WHOLESALE BANKING

INTERNATIONAL BOND MARKETTotal issued volume Exchange value in USD billions

1,84

0

1,58

0

1,71

3 2,15

1

2,82

1

2001 2002 2003 2004 2005

R E V I E W O F O P E R A T I O N S

INTERNATIONAL NETWORKMost of ING Belgium's international network is focused on the

South West Europe region. The main entities are located in France,

Luxembourg and Switzerland. The international network makes a

substantial contribution to the bank's consolidated net profit.

ING BELGIUM ANNUAL REVIEW 2005 25

26 ANNUAL REVIEW 2005 ING BELGIUM

INTERNATIONAL NETWORK

PROFILE OF MAJOR INTERNATIONALSUBSIDIARIES 1

ING Bank (France)On 20 January 2005, ING Group and Barclays Bank PLC

announced in simultaneous press releases that they had

entered into talks concerning the takeover of the personal and

private banking business of ING Securities Bank (France) by

Barclays Bank PLC. The signature of the agreement was

announced early June 2005, with transfer of ownership on

1 July. The sales teams of the ING Ferri branches and of Private

banking, as well as the support teams directly dedicated to

these activities joined Barclays Bank PLC.

Since then, ING Bank (France), a wholly-owned subsidiary of

ING Belgium, has concentrated its development in two areas:

• wholesale banking;

• the marketing of undertakings for collective investment in

transferable secur i t ies (UCITS) of ING Investment

Management 2.

A "new foundation plan" was conceived, in accord with the

labour unions, with a view to adapting the structure to the new

scope of activities. It foresees the suppression of 181 workplaces

net, solely situated within support functions. The implementa-

tion of the plan will take place during 2006.

ING Bank (France) posted consolidated net profit of EUR 26.5

million for 2005, compared with EUR 23.9 million for the pre-

vious year. Recurring business suffered from a reduced

operating result, due to the drop in income related to the sale

of the retail arm and the termination of certain activities, which

temporarily exceeded the savings made in overheads arising

from these decisions.

Wholesale bankingThe wholesale business was characterised in particular by the

continued refinancing of companies' cash lines and by the

participation in local stock market transactions resulting from

privatisations and acquisition projects of certain customers.

With regard to the former, it should be noted that margins

and commissions seem to have bottomed out, achieving their

lowest rate of the decade, while maturities are at seven years

almost across the board. As for the latter, the quality of the

relationships forged by the bank has enabled it to be selected

at the highest level to refinance nearly all of the major acquisition

deals initiated by French companies.

Commission linked to cash-management transactions rose con-

siderably year on year. Significant increases occurred as new

agreements gained clout.

The bank was involved in a number of structured export financ-

ing deals, mainly in the aeronautical sector. It also considerably

developed its short-term export finance business.

Forex and interest rate dealing-room activity was upbeat in

2005 and managed to turn basic trends to good account: the

depreciation of the euro against the dollar, the anticipated hike

of the European Central Bank (ECB) key rate, and the correc-

tion of the euro interest rate curve. Derivatives and structured

products were also popular with corporates and new institu-

tional customers.

With regard to equities and derivatives business, the approach

made to institutional customers was stepped up. The integra-

tion of the business line into the European Equities platform

and the synergies between the teams operating on this plat-

form are proving successful.

Finally, financial engineering carried out a number of deals on

the Euronext primary markets, in concert with its counterparts

in London and Amsterdam.

Investment managementING Investment Management (France) strengthened its ties with

strategic consultants. Several of them benefited from up-to-date

analyses and a presentation of new investment strategies. The

aim of this approach is to be included in calls for tenders launched

by pension funds, insurers and mutual insurance companies.

The entity also bolstered its presence among institutional cus-

tomers. Investment strategies such as Emerging Markets Debt

or High Dividend were successfully unveiled to those customers

which have the option of investing in these assets.

The profitability of the business rose favourably.

CONSOLIDATED ITEMS In EUR millions

2005* 2004 2003

Total assets 3,353.57 4,510.26 4,702.13

Shareholders' funds (before result for the period) 492.50 468.57 486.68

Customer loans and advances 1,281.89 1,056.45 1,284.49

Deposits by customers 983.93 1,015.17 1,163.36

Net profit (loss) 26.51 23.92 (18.11)

Staff (in units) 399 598 678

* Unaudited data.

1 Information based on the annual report of the companies concerned / 2 See the section, "Third-party asset management", in the chapter, "Specialised products & services".

ING BELGIUM ANNUAL REVIEW 2005 27

ING Luxembourg SAA wholly-owned subsidiary of ING Belgium, ING Luxembourg

has a network of sixteen branches throughout Luxembourg.

This physical presence is complemented by a transactional web-

site which maintains its popularity.

Against a difficult economic backdrop, the bank posted after-

tax profit of almost EUR 129 million. Excluding non-recurring

items, the year-on-year increase exceeds 15%. This is the result

of performances posted by the various lines of business, boost-

ed by rigorous cost-control measures.

Retail income, which groups domestic and private banking, rose

by some 10%, with deposit and lending volumes posting a sub-

stantial rise. The implementation of the European Directive on

savings taxation did not cause an outflow of funds. It did, how-

ever, accelerate the drop in the physical payment of coupons,

which has been constant since 2002.

The three areas of the wholesale business were also on the up.

In the institutionals sector, there was a substantial increase in

outstandings of insurance companies. A number of major finan-

cial-engineering transactions were also completed with

multinationals. At the same time, provisions for defaulting loans

on big local companies were at an all-time low. Finally, the

dealing-room result rose for the third year running, mainly

thanks to the excellent forex performance and to the efforts

made in the sale of the group's products.

Most of ING Luxembourg's income is traditionally generated

by activities linked to collective investment undertakings. At

EUR 27.01 billion, total outstanding administered funds rose

by EUR 4.21 billion during the financial year.

Customer loans and advances remained stable compared with

the previous year. Historically low interest rates were behind

the 10% rise in the demand for mortgage loans.

Deposits by customers posted a similar rise, for both current

and fixed-term accounts.

As mentioned above, non-recurring items limited the increase

in net profit to 3.5%, compared with that for 2004. Excluding

these items for both financial years, the net operating result

rose by 15%.

ING Bank (Switzerland) SAING Bank (Switzerland) is owned by ING Luxembourg, a wholly-

owned subsidiary of ING Belgium.

With a staff of 311, the company mainly concentrates on pri-

vate fund management. In addition to its central office in

Geneva, it has branches in Zurich, Basle, Lugano, Lausanne

and Crans Montana. It also operates banking and trust com-

pany subsidiaries in Jersey, and a bank in Monaco.

One of the 150 foreign banks in Switzerland, its ambition today

is to rank among the market leaders. The private fund man-

agement business is conducted under the ING Private Banking

label, while representation and marketing of the group's mu-

tual funds are handled by ING Investment Management.

Total assets increased by 21%. This growth was mainly

explained on the liabilities side by an increase in deposits by

customers, and on the assets side by a rise in fixed-term loans

and advances.

Income before depreciation, provisions and taxes rose over-

all by EUR 1.65 million. The rise results from the 4.9% increase

in interest income and the 5.1% rise in fee income. Costs rose

by 2.3% compared with 2004, but were kept under control.

At EUR 32.74 million, compared with EUR 30.75 million the

previous year, net profit rose by EUR 1.99 million, or 6.5%,

owing to the combined effect of the increased operating result

Published shareholders' equity, after appropriation 350.78 348.47 438.75

Customer loans and advances 588.76 535.08 587.73

Deposits by customers 1,205.45 1,064.51 1,174.49

Income before depreciation, provisions, extraordinary items and taxes 45.11 43.46 38.14

Net profit 32.74 30.75 30.05

Staff (in units) 311 308 304

* 1 CHF = 0.6428 EUR 0.6472 EUR 0.6415 EURCONSOLIDATED ITEMS In EUR millions

2005 2004 2003

Total assets 11,988.79 8,967.46 8,985.20

Shareholders' funds 1,260.94 1,176.58 1,140.92

Customer loans and advances 2,052.93 2,068.10 1,827.56

Deposits by customers 6,981.48 6,254.74 6,688.75

Net profit 128.93 124.52 93.63

Staff (in units) 833 878 916

28 ANNUAL REVIEW 2005 ING BELGIUM

The rise was mainly due to profit carried forward following

payment of the dividend.

OTHER INTERNATIONAL OPERATIONS

SwitzerlandING Belgium's Geneva branch was granted a licence to deal

in transferable securities at the end of 2004. The branch took

over all dealing-room activities from ING Bank (Switzerland)

as from 1 January 2005. The Equity Sales desk was transferred

on 1 January 2006.

SpainAll the ING Group entities in Madrid have been accommodated

at “ING House”, located in the city centre. The move was

completed mid-April 2005

PortugalDuring mid-2005, a new activity was rolled out at the Lisbon

branch, with the setting up of a commercial bridgehead placed

under the functional authority of ING Investment Management

Belgium. The aim of this entity is to promote ING Investment

Management products to local institutional clients.

United KingdomING Belgium remains the representative shareholder of the

stockbroker Williams de Broë. The bank strengthened its man-

agerial control over the company, which it also recapitalised:

these measures follow on from operational losses incurred in

the past.

IrelandING Belgium retained its Irish branch (ING Belgium, Dublin

Branch) and subsidiary (ING Belgium Ireland).

The NetherlandsThe Breda branch, an operational arm for international cash

management, had a favourable year.

GermanyThe business of the Cologne branch will be transferred to ING

Bank Deutschland during 2006.

USAING Belgium wound up two of its US operations, BBL (USA)

Holdings, Inc. and its subsidiary BBL (USA) Capital Corporation.

INTERNATIONAL NETWORK

R E V I E W O F O P E R A T I O N S

SPECIALISED PRODUCTS AND SERVICES The bank markets a range of products and services developed by

separate legal entities, subsidiaries and sister companies. For those

activities that do not form a direct part of its core business, such as

insurance, leasing and factoring, ING Belgium chooses to use the

services of specialist companies, which have their own customer base.

With regard to asset management, these concerns are coupled with a

concern for effective corporate governance.

ING BELGIUM ANNUAL REVIEW 2005 29

30 ANNUAL REVIEW 2005 ING BELGIUM

THIRD-PARTY ASSET MANAGEMENT

ING Investment Management (ING IM)With total outstandings in excess of EUR 350 billion, and a

workforce of some 700 investment professionals, ING IM is

ING Group's principal asset manager. The company manages

customer assets within geographical centres of expertise

(Europe, USA, Asia), while capitalising on a direct commercial

presence in more than 30 countries worldwide. Close collab-

oration between the three regions gives all its customers

permanent access to the Group's entire expertise.

Designed to match the profile and expectations of each

investor category, the aim of the developed strategies is to cre-

ate long-lasting performance that is completely transparent

for customers. For each investment style, the keywords are pro-

active management, the importance of fundamental analysis,

a medium-term investment horizon, rigorous risk monitoring,

the systematic implementation of strategies via standard port-

folios 1, and teamwork 2.

ING IM's commercial development is underpinned by a

three-pronged strategy:

• the main focus obviously relates to ING customers who are

approached via local sales outlets;

• distribution, via ING Direct or third parties, of the Group's

undertakings for collective investment in countries where

ING is not present with a physical distribution network;

• perfection of specific solutions, such as ALM 3 services, tar-

geted at institutional clients.

Undertakings for collective investment (UCI’s)Investor behaviourLow-risk products, preferably accompanied by a capital pro-

tection mechanism, continued to be popular with Belgian retail

customers. Thanks to the improved situation on the stock

exchange, however, investors have been displaying increas-

ing interest in products invested in or linked to equities, albeit

without capital protection. These trends explained the success:

• in the first category, of the ING (L) Selectis Short Term

Growth and ING (L) Protected Equifix Callable 1 sub-funds;

• in the second, of the ING (L) Invest Euro Income and ING

(L) Invest Europe High Dividend subfunds.

Against a backdrop of historically low interest rates and of infla-

tionary fears, the new Euro Inflation Linked subfund of the ING (L)

Renta Fund bond market fund was positively received by cus-

tomers, owing to its defensive character and the benefits displayed

in terms of diversification. During the whole of the financial year,

however, the basic trend seemed to be a shying away from bond

products and the reallocation of portfolios towards more trad-

itional savings vehicles and capital protection products. Irrespective

of interest rate levels, the decline was favoured by the end-of-year

announcement of a tax levy on mutual funds invested more than

40% in fixed-income securities.

Product performanceThe combination of marked economic growth and a notable

appreciation of the dollar was especially profitable for assets

invested in the emerging countries. This was illustrated by the

performance posted for ING (L) Invest Latin America (up 78.0%

in euros) and ING (L) Invest Emerging Europe (up 68.7% in

euros). Rising oil prices resulted in a significant increase for

ING (L) Invest Energy (up 56.0% in euros). The subfunds ING

(L) Invest Japan (up 53.0% in euros) and ING (L) Invest Japanese

Small and Mid Caps (up 63.6% in euros) both fully benefit-

ed from the revived interest in the Japanese stock exchange.

Conversely, the relatively substandard performance of telecoms

was reflected in the modest rise (up 3.5% in euros) in the sub-

funds covering this sector.

Of the bond subfunds, ING (L) Renta Fund Asian Debt post-

ed the biggest rise (up 22.8% in euros), owing to the combined

effect of reduced credit spreads, falling interest rates, and the

appreciating currencies concerned. The subfunds invested in

dollars or in the dollar zone did not lag behind, namely ING

(L) Renta Fund II Canadian dollar (up 21.6% in euros), ING (L)

Renta Cash CAD (up 20.9% in euros), and ING (L) Renta Cash

USD (up 18.2% in euros).

In the mixed products range, outstanding performances were

displayed by ING (L) Patrimonial Aggressive (up 20.6% in euros)

and ING (L) Patrimonial Balanced (up 15.3% in euros). The Star

Fund pension fund also fared very well (up 16.2% in euros).

In the protected capital products range, the subfunds invest-

ed in equities posted a return that outstripped that for

sub-funds invested in bonds: ING (L) Protected Equi-Fix

Netherlands 2 (up 19.7% in euros), ING (L) Selectis Flanders

(up 18.4% in euros), and ING (L) Selectis Belgium Fix 1 (up

13.6% in euros).

SPECIALISED PRODUCTS AND SERVICES

1 To guarantee a similar level of return to all customers opting for the same investment strategy / 2 To ensure continued management on a lasting basis. / 3 Asset & Liability Management.

ING BELGIUM ANNUAL REVIEW 2005 31

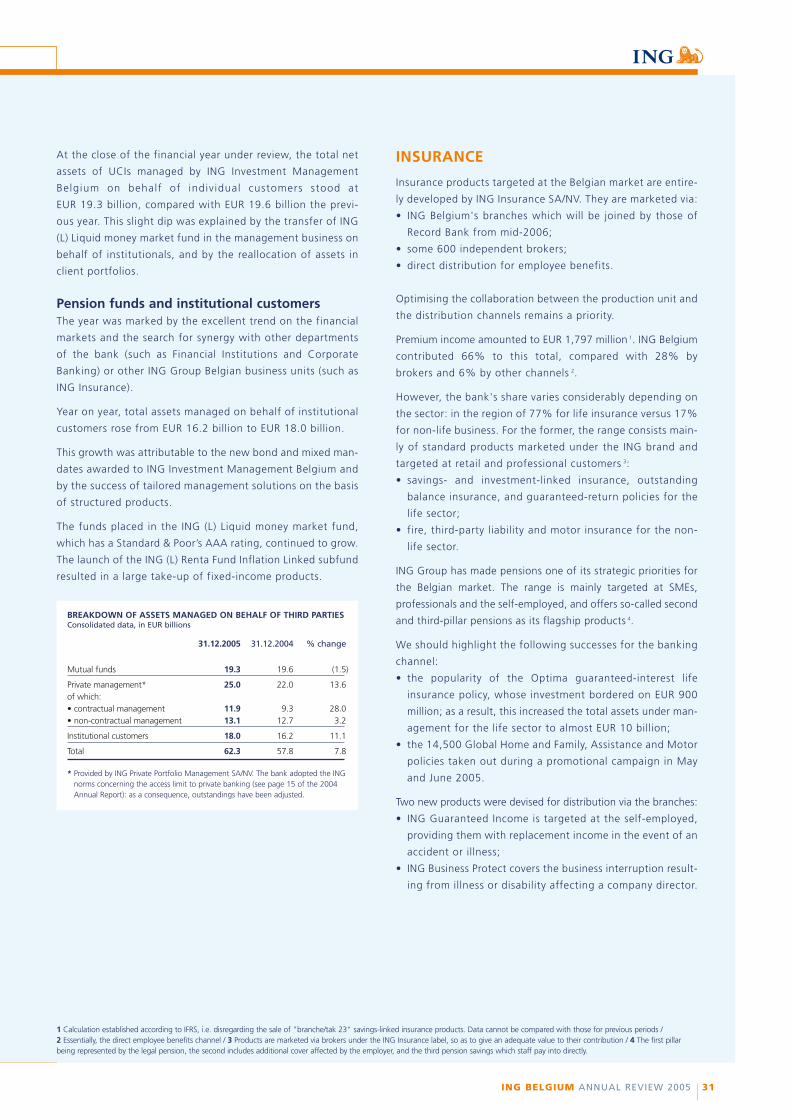

At the close of the financial year under review, the total net

assets of UCIs managed by ING Investment Management

Belgium on behalf of individual customers stood at

EUR 19.3 billion, compared with EUR 19.6 billion the previ-

ous year. This slight dip was explained by the transfer of ING

(L) Liquid money market fund in the management business on

behalf of institutionals, and by the reallocation of assets in

client portfolios.

Pension funds and institutional customersThe year was marked by the excellent trend on the financial

markets and the search for synergy with other departments

of the bank (such as Financial Institutions and Corporate

Banking) or other ING Group Belgian business units (such as

ING Insurance).

Year on year, total assets managed on behalf of institutional

customers rose from EUR 16.2 billion to EUR 18.0 billion.

This growth was attributable to the new bond and mixed man-

dates awarded to ING Investment Management Belgium and

by the success of tailored management solutions on the basis

of structured products.

The funds placed in the ING (L) Liquid money market fund,

which has a Standard & Poor’s AAA rating, continued to grow.

The launch of the ING (L) Renta Fund Inflation Linked subfund

resulted in a large take-up of fixed-income products.

INSURANCE

Insurance products targeted at the Belgian market are entire-

ly developed by ING Insurance SA/NV. They are marketed via:

• ING Belgium's branches which will be joined by those of

Record Bank from mid-2006;

• some 600 independent brokers;

• direct distribution for employee benefits.

Optimising the collaboration between the production unit and

the distribution channels remains a priority.

Premium income amounted to EUR 1,797 million 1. ING Belgium

contributed 66% to this total, compared with 28% by

brokers and 6% by other channels 2.

However, the bank's share varies considerably depending on

the sector: in the region of 77% for life insurance versus 17%

for non-life business. For the former, the range consists main-

ly of standard products marketed under the ING brand and

targeted at retail and professional customers 3:

• savings- and investment-linked insurance, outstanding

balance insurance, and guaranteed-return policies for the

life sector;

• fire, third-party liability and motor insurance for the non-

life sector.

ING Group has made pensions one of its strategic priorities for

the Belgian market. The range is mainly targeted at SMEs,

professionals and the self-employed, and offers so-called second

and third-pillar pensions as its flagship products 4.

We should highlight the following successes for the banking

channel:

• the popularity of the Optima guaranteed-interest life

insurance policy, whose investment bordered on EUR 900

million; as a result, this increased the total assets under man-

agement for the life sector to almost EUR 10 billion;

• the 14,500 Global Home and Family, Assistance and Motor

policies taken out during a promotional campaign in May

and June 2005.

Two new products were devised for distribution via the branches:

• ING Guaranteed Income is targeted at the self-employed,

providing them with replacement income in the event of an

accident or illness;

• ING Business Protect covers the business interruption result-

ing from illness or disability affecting a company director.

BREAKDOWN OF ASSETS MANAGED ON BEHALF OF THIRD PARTIES Consolidated data, in EUR billions

* Provided by ING Private Portfolio Management SA/NV. The bank adopted the INGnorms concerning the access limit to private banking (see page 15 of the 2004Annual Report): as a consequence, outstandings have been adjusted.

1 Calculation established according to IFRS, i.e. disregarding the sale of "branche/tak 23" savings-linked insurance products. Data cannot be compared with those for previous periods / 2 Essentially, the direct employee benefits channel / 3 Products are marketed via brokers under the ING Insurance label, so as to give an adequate value to their contribution / 4 The first pillarbeing represented by the legal pension, the second includes additional cover affected by the employer, and the third pension savings which staff pay into directly.

32 ANNUAL REVIEW 2005 ING BELGIUM

To this should be added the electronic tool which, thanks to

an automated assessment of medical risks, makes it extreme-

ly easy to take out a life insurance policy, thereby reducing

costs while at the same time increasing customer satisfaction.

In the area of group insurance, ING Insurance launched EB

Connect, a secure on-line application that allows employers

to consult their policies on-line, make any necessary changes,

and keep track of processing.

ING Insurance's operating profit, before tax and excluding cap-

ital gains and losses on the investment portfolio, increased by

24% to reach EUR 147 million. Net profit stood at EUR 131

million, up 114% 1.

LEASING

Leasing activities are carried out via two companies with a com-

mon single shareholder, ING Lease Holding, in which ING

Belgium holds a 30% share:

• ING Lease Belgium takes care of the finance leasing of all

property and equipment;

• ING Car Lease Belgium handles the operational leasing of

cars and light commercial vehicles.

Finance leasing: ING Lease BelgiumOverall, ING Lease Belgium is ranked third in the Belgian

finance leasing market.

Sales figures At EUR 656 million, production for the period posted its sec-

ond-best ever performance, following the all-time high of EUR

692 million achieved in 2004. The biggest increases related

to heavy goods vehicles (up 35%), cars and light commercial

vehicles (up 18%), and property (up 16%).

At the end of 2005, the financial value of the portfolio was

EUR 1,677 million, compared with EUR 1,614 million the pre-

vious year.

Financial resultsThe two main items in ING Lease Belgium's key figures posted

significant increases:

• at EUR 26.1 million, compared with EUR 20.0 million, the

group operating result before taxes and charges rose by 31%;

• the cost/income ratio dipped from 40.6% to 38.3%.

These results were influenced favourably by the low level of

the credit risk cost and by the adoption of an internal rating

system for the calculation of write-downs.

SynergiesING Lease Holding stepped up its European operations. With

a presence in 12 countries and a highly diverse asset portfolio,

it is in a position to help ING Group customers develop local-

ly. ING Lease Belgium meshes fully with this strategy, with

regard to both its "vendors" and its international customers.

In 2005, the quality of the business synergies forged with ING

Belgium translated into 16% growth in the value of leasing

contracts concluded with the bank's customers.

SPECIALISED PRODUCTS AND SERVICES

1 Data calculated according to ING Group's accounting standards (IFRS).

ING INSURANCE - PREMIUM INCOMEBreakdown of premium income by distribution channel (for 2005 as %)

ING Belgium66

Brokers28

Others6

ING BELGIUM ANNUAL REVIEW 2005 33

Highlights of the year under reviewING Lease Belgium vacated its premises on avenue de

Cortenbergh in Brussels to take up occupancy in a new com-

plex located in rue Colonel Bourg in Evere. Apart from the

major added-value generated by the sale of the former prop-

erty 1, the new head office provides ING Lease Belgium staff

with a better working environment and increased comfort. It

uses efficient energy-saving and environmentally-friendly tech-

nology. It also means that the company will avoid future

renovation costs.

An ambitious IT drive was launched aimed at boosting oper-

ational efficiency through increased productivity, combined

with cost cutting. Alongside this, the organisation will be over-

hauled to standardise procedures and to encourage a

pro-active attitude. All this should improve both the company's

performance and the level of customer satisfaction.

Operational leasing: ING Car Lease BelgiumING Car Lease Belgium specialises in the operational leasing

of cars and light commercial vehicles 2 of all makes. It also offers

short-term rental of these types of vehicles. Its products, com-

bined with those of ING Lease Belg ium, prov ide a

comprehensive solution with regards to vehicle leasing and

fleet management in Belgium.

ING Car Lease Belgium also assists companies with defining their

company-car policy, building up their fleet in an economically-

balanced way, and managing the tax aspects.

Thanks to the Fleet Agent application, customers also have

access to an on-line module offering vehicles and detailed

reports for managing their fleet.

ING Car Lease in the Belgian operational leasingmarketIn 2005, 480,088 new cars and 59,593 light commercial vehicles

were registered in Belgium. Compared with corresponding fig-

ures for 2004, this translates into a 1% drop for cars and a

5.3% rise for light commercial vehicles. As in the past, almost

half of the cars were registered in the name of a company.

Orders for new cars used for long-term leasing rose by 5.7%,

totalling 88,077 vehicles. Prices are under extreme pressure

in this highly competitive market, which has practically reached

maturity and seen numerous mergers.

With a fleet of 18,129 vehicles 3, ING Car Lease Belgium has

an 8% market share. The company bases its strategy on the

continued growth of a segmented portfolio of customers with

a high satisfaction level. These features also ensure a substan-

tial return.

Highlights of the year under reviewAs part of the "TOPpING" project, the development of an IT

platform for the Benelux countries was continued during 2005.

Successfully rolled out in early 2006, the tool will act as a

springboard for further expansion of the vehicle fleet,

accompanied by increased operational efficiency.

ING Car Lease Belgium bolstered its business synergies with

ING Belgium, by promoting the cross-selling of operational

leasing within the bank's retail and wholesale segments.

Operating under the slogan "Think Wheels", the tie-up result-

ed in a total of 792 new contracts, a rise of 86.8% on 2004.

The banking channel contributed 15.2% to total production.

Since 1991, ING Car Lease Belgium has awarded the "Leasing

Car of the Year" prize: in 2005, it went to the BMW Series 3.

Financial resultsAt the end of 2005, the total value of ING Car Lease Belgium's

portfolio stood at EUR 268 million. Profit before tax was EUR

10.6 million and EUR 6.8 million after tax.

The value of the ING Car Lease Luxembourg portfolio was EUR

11.9 million at 31 December 2005.

Both entities combined employ 129.1 full-time equivalents.

Outlook for 2006ING Car Lease Belgium's main priority remains the continued

development of business synergies with the other ING Group

entities.

The company will continue to develop its business in the light

commercial vehicles sector.

According to its forecasts, the growth of its vehicle fleet is like-

ly to exceed market expectations.

1 This capital gain is not entered in the above results / 2 Weighing 3.5 tons or less / 3 This figure does not include the Luxembourg fleet, comprising 695 vehicles.

34 ANNUAL REVIEW 2005 ING BELGIUM

FACTORING

The bank's factoring business is conducted in cooperation with

IFB SA/NV International Factors, a joint subsidiary of ING

Belgium and KBC. Established in 1963, IFB is Belgium's old-

est factoring company and holds a 24% market share.

Its commercial department comprises two separate business

units, responsible for maintaining the relationship with the KBC

and ING Belgium networks respectively.

In addition to its main factoring business, IFB operates as a

credit insurance broker and as a commercial information and

debt-collection agent. It is able, therefore, to offer global solu-

tions to companies for the management of their “loans and

advances to customers” balance-sheet item.

The total volume of receivables rose by 14.6%, thanks to a

series of new contracts of which several exceeded EUR 25 mil-

lion. ING Belgium accounted for 16.72% of the year's new

business in this area.

Following the implementation of Basle II, which weights finan-

cing in the form of factoring more favourably than

conventional loans, IFB conducted various campaigns aimed

at promoting factoring at ING Belgium. The outcome of these

campaigns should be reflected in the production of 2006.

In credit insurance, turnover stood at EUR 5,413 million at the

year-end.

Operating profit at the close of 2005 was comparable to that

for 2004. A noticeable reduction in write-downs on receivables

offset the rise in write-downs on the company's current major

IT investment.

The forecast for 2006 estimates growth in business volume

of about 15%. Owing to write-downs on current investment,

however, net profit is likely to be down 10% on 2005.

SPECIALISED PRODUCTS AND SERVICES

In EUR millions

2005 2004 2003

Total business volume 3,181.20 2,779.00 2,467.49

Total income 21.81 20.89 19.17

Overheads 10.81 11.03 11.00

Operating profit, before write-downs and provisions 11.00 9.86 8.17

Write-downs on receivables 1.54 2.24 2.08

Write-downs on fixed assets 1.15 0.63 0.44

Net profit 4.72 5.15 4.41

Staff (in units) 93 90 95

R E V I E W O F O P E R A T I O N S

OPERATIONS & INFORMATIONTECHNOLOGYThe structure of ING Belgium's Operations and IT entities has been

adapted to the Group's management organisation. Efforts have been

continued as part of the plan to improve operational efficiency, with

ING Group management announcing that this will be implemented in

the Benelux countries.

ING BELGIUM ANNUAL REVIEW 2005 35

36 ANNUAL REVIEW 2005 ING BELGIUM

OPERATIONS & INFORMATION TECHNOLOGY

IMPROVEMENT IN OPERATIONAL EFFICIENCY

On 13 July 2005, ING announced a large-scale efficiency pro-

gramme for its Operations & Information Technology Division.

This programme meshes with the Group's ongoing cost-cutting

drive, with a view to preserving its competitive edge, especial-

ly in mature markets such as the Benelux countries. It includes

the option of redistributing certain activities within the group

or outsourcing them, provided that the outside supplier is able

to carry out these activities at least at an identical level of qual-

ity, with more flexibility and at a lower cost.

The scope of the plan was laid down on 2 November 2005.

At ING Belgium, this will concern a total of 550 jobs, includ-

ing 320 as part of streamlining and 230 as a result of

outsourcing. Most of these jobs are located in the General

Banking Operations, Securities, and Business Information

Systems Departments. Initial concrete decisions are expected

in 2006.

OPERATIONS

General Banking OperationsAs part of the bank's reorganisation into business lines, the

department has transferred its Product Management and Sales

Support sections, which have been allocated to Retail and

Wholesale Banking.

Conversely, but using similar logic, the department has

resumed the handling of successions and standard credit facil-

ities, which had been localised in the regional sales offices 1.

Adopting the name General Banking Operations, which is more

in line with its new brief 2, the department has opted for a

twofold structure, each headed by a national manager:

• International Payments, which also includes documen-

tary transactions and cross-border cheques;

• Convenience & Retail Loans, which covers accounts and

As things currently stand, some of these activities are carried

out by all three processing sites, Brussels, Namur and Gent,

while some activities have been refocused at one or two sites.

In addition to this dual operational approach, the department

has three support entities:

• Business & Project Support Management manages the

projects portfolio; the unit is also responsible for manage-

ment control and operational risk management.

• Programme Manager is responsible for implementing the

"Lean" methodology in the operational entities 3;

• Business Excellence & Communication is responsible for

the department's internal communications and imple-

menting quality control plans.

The department aims to offer its customers high-quality ser-

vices in line with demand, at a transparent cost, and with an

acceptable level of operational risk.

For 2006, its priorities concern:

• continuing the centralisation of activities;

• systematically implementing the "Lean" methodology.

Concrete decisions are also expected in 2006 on the outsour-

cing of scanning and encoding activities.

Securities Department The Securities Department executes all stock market orders

issued by ING Belgium's retail, professional and institutional

customers. It also executes buying and selling orders relating

to mutual funds, savings certificates, bonds, and other finan-

cial instruments that come in via the various distribution

channels. The department executes the payment of coupons

and the redemption of matured securities.

Within the department, five divisions carry out an essential-

ly operational activity:

• the first four relate to securities placed with ING Belgium;

as its name suggests, Order Management processes orders;

Safekeeping includes holding, reconciliation, customer

reporting, proxy services, and tax rebates; this division also

includes a unit that is responsible for the issue, via Sogès-

Fiducem, of bearer certificates representing foreign equities;

the Corporate Actions entity handles all securities trans-

actions such as the payment of coupons, optional dividends;

the mission of the Clearing & Settlement division is self-

explanatory;

• the processing of securities issued in physical form is dealt

with by the Physical Securities & Coupons division; it also

acts as a depository and a paying agent.

Two divisions fulfil briefs that exceed the operational dimen-

sion:

• Retail Support acts as a single point of contact for the

branch network; this entity fields network queries concern-

ing securities held by retail customers, via a call centre and

a dedicated site; it also handles complaints and carries out

research;

• Wholesale Support provides direct support to profession-

al and institutional customers.

1 Recovery operations have been centralised for the same reasons: processing has been entrusted to the Credit Policy & Decision Department / 2 Instead of Payments & Accounts Department /3 This methodology aims to increase the department's level of customer satisfaction, via an accompanying improvement in processes and quality in terms of performing tasks.

ING BELGIUM ANNUAL REVIEW 2005 37

Business Support & Finance is responsible for managing

projects, processes and risks, and for management control.

ING Belgium's Securities Department forms part of ING Group's

Ops & IT line. This cross-border organisation allows operat-

ing costs to be kept to a minimum and a high-quality service

to be offered to customers.

BUSINESS INFORMATION SYSTEMS

Since the beginning of 2005, ING Belgium's IT activities have

been completely integrated into ING Group's Ops & IT Banking

division. The structure and priorities of the Business Information

Systems Department therefore perfectly match those of ING

Group's IT business line.

Structure of the departmentThe department is organised into three main functional lines:

• Wholesale Banking Applications manages the needs of

Securities, International Payments & Cash Management,

International Network, Transactional Services, Support

Services, Finance, and Risk & Business Intelligence;

• Retail Banking Applications looks after the distribution

channel applications ("click", "call" and "face"), customer

and product referentials, domestic payments, payment cards,

and credit facilities;

• Infrastructure is responsible for the operational manage-

ment of all computer installations and database systems.

Five support entities cover specific needs:

• IT Management Support is responsible for the IT corpor-

ate governance process and project management;

• as its name suggests, the Information Risk Management

entity manages the information risk;

• Finance allocates resources and manages purchases and the

budget;

• Special Studies is responsible for special problems of para-

mount importance, which are studied by the IT Department;

the Disaster Recovery Plan and the removal of obsolete IT

applications and infrastructures were included in the 2005

programme;