12

Case Analysis on India’s Insurance Industry A Financial Services Presentation By Group 5

| Date post: | 20-Aug-2015 |

| Category: |

Economy & Finance |

| Upload: | satyam-kumar |

| View: | 222 times |

| Download: | 2 times |

Case Analysis on India’s Insurance Industry

A Financial Services Presentation By Group 5

Insurance Industry: Overview

Premiu

m

•In the year 2006, the premium value worldwide was $3, 723 billion out of which 59% was in life insurance

•The CAGR of business premium in India between 2001-10 was 31%, however there was flat growth between 2010-12 with CAGR of around 2% in business premium.

Industrializ

ed Marke

tVS.

Emerging

Markets

•Penetration was 9.2% in industrialized nations and2.7% in emerging nations

•In India, the penetration was 4.1% in life and 0.6% in non-life

•Growth of insurance however in emerging nation is higher than that of industrialized nations.

Econom

ic Factors effectin

g Growth

•Economic growth

•Inflation•Interest

rates•Stock

market performance

•Government regulations and policies

Nationalization & its effects

Nationalization Effects Merits: • Penetration in rural areas increased

but the total value of rural policy declined

• Nationalization also helped in successful cutting of operating cost

• Channelized the resources into social infrastructure projects.

• High level of customer satisfaction• The GIC grew tenfold (approx. 1/4th

the size of life business)Shortfalls:• The invested funds however yielded

less returns because of a conservation approach in managing the portfolios.

• Invested more in non-convertible debentures rather than start-up projects.

• The main reason behind nationalization was malpractices by private firms

• Premiums were charged at inflated rates from Indians

• Bombay Mutual Life Assurance society, first to underwrite life policies for Indians at fair market rate.

• In 1956, the Government of India nationalized the life insurance sector with the passing of the LIC Act, 1956

• In 1972, the general insurance was nationalized as wholly state-owned General Insurance Company of India

Top Players in the Insurance Industry

• Indian insurance market is 19th largest globally and ranks 5th in Asia

• The public sector companies have continued to dominate the Indian market with private players rising to a market share of 48%

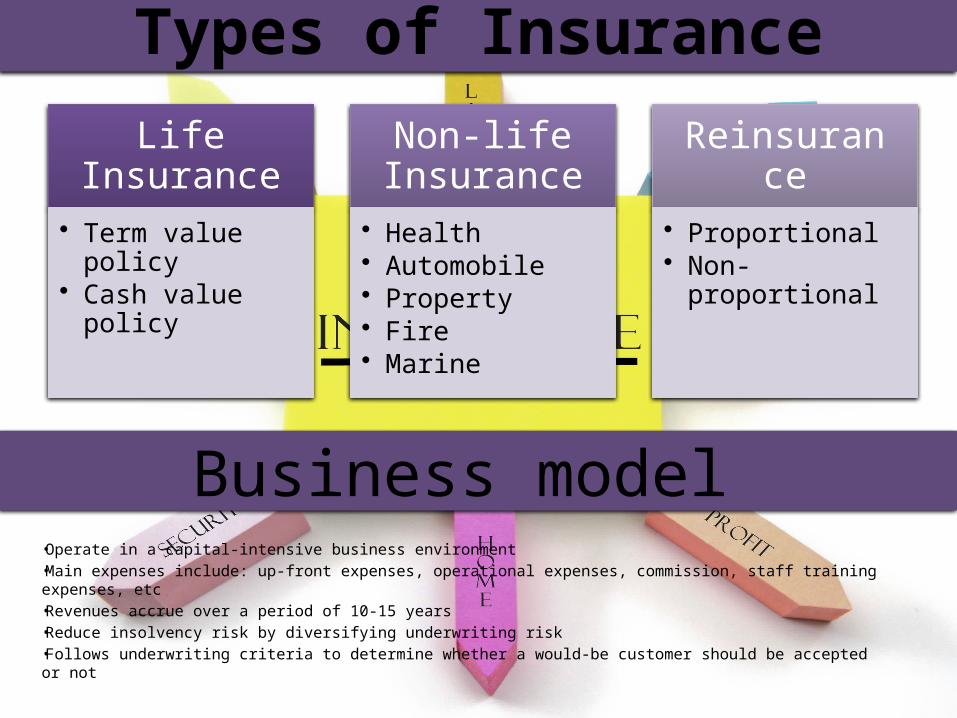

Types of Insurance

Life Insurance

• Term value policy

• Cash value policy

Non-life Insurance

• Health• Automobile • Property• Fire • Marine

Reinsurance

• Proportional • Non-

proportional

•Operate in a capital-intensive business environment•Main expenses include: up-front expenses, operational expenses, commission, staff training expenses, etc•Revenues accrue over a period of 10-15 years•Reduce insolvency risk by diversifying underwriting risk•Follows underwriting criteria to determine whether a would-be customer should be accepted or not

Business model

Continued…

Types of cost • Distribution expenses• Underwriting expenses• Loss adjustment expenses• Underwriting losses: claims

by policy holders when settled down

Ratios • Loss ratio• Expense ratio• Combined ratio- it is a

measure of an insurer’s underwriting performance

If combined ratio-<1= positive underwriting>1= negative underwriting

Insurer’s profit= premium earned+ investment income- operating

expenses

Distribution Channels

Source- handbook on Indian Insurance Statistics 2011-12 published by IRDA

-More amenable to the distribution of low complexity with low cost-Low value standardised product and cross selling

-High end specialise products

-Offer customize products

-Lowest potential reach-Have lower distribution or underwriting expense

Direct writers

Agents

Bancassurance

Retailers & Utility compani

es

Brokers &

Financial Advisors

Internet

Bancassurance Model

Referral Model•Pass on business leads to

insurers.•Receive referral fee•Undertake little risk•Actual transaction carried

out by insurer personnel.

Corporate Agency•Personnel are trained to sell

insurance products.•Undertake reputational risk

for marketing insurance products.

•Get commission in return

Fully integrated Financial Services •Forms wholly-owned

insurance subsidiaries/ JVs•Undertake most risk•Gains from synergy &

economies of scope

Insurance Tariffs

• In 1950, government of India established Tariff Committee, with power to set, amend and modify the premium rates of major lines of General Insurance.

• In 1968, it was changed to Tariff Advisory Committee with even broader powers.• Post Liberalization, in 1993 Malhotra Committee was set up which gave some

recommendations : Separation of Life and Non life sectors, Definition of Underwriting Standards and giving licenses to private insures.

• These recommendations were put into effect in 1999.• IRDA was set up as the industry regulator in 1996 and statuary authority in 2000. • Since October 2000, IRDA Issued 15 Private Life insurance licenses and 8 private

Non-Life insurance licenses. • New insurance companies must have capital of Rs. 1 billion and new reinsures

must have a capital of Rs. 2 billion.• Since the private sector was open for the industry Rs. 16.88 billion came as

foreign investment.

Detariffication

• On 1st January 2007, IRDA implemented the first phase of detariffing of India’s General Insurance business.

• General insurance companies were allowed a maximum of 20% discount on Fire and Engineering Policies. And up to 10 % discount on motor insurance.

• Further more reductions were not expected, but it fall down to 30%.• Without cross subsidizing, Health and Marine insurance premium rate was

risen by 20 to 25%.• IRDA freeze any product innovation till April 2008. It was to stabilize and get

the right price risk till the next phase of detariffication.• In India, Third party insurance became mandatory.• Low premium rates of fire and engineering insurance was compensated by

Third party insurance.• After detariffication, the revenues increased but showed a slow growth of the

industry that was from 22% to 18%.

Road Ahead…• It can be postulated that by 2014 the penetration of life

insurance in India will increase to 4.4% and that of non life insurance to 0.9%

• In the next three years, health insurance is poised to become the second largest business for non life insurers after motor insurance

• The Indian General Insurance industry has evolved significantly in the past few years

• Penetration and density levels are lower than the developed as well as comparable developing countries

• This is mainly driven by lack of financial awareness, lack of understanding of general insurance products, low perceived benefits and purchase decision based on insistence by financers, statutory requirements, etc

Projected growth of India’s General Insurance industry (Gross Direct Premium)(In INR Crore)

THANK YOU!

Group No. 5- . Yamini Sharma

• Satyam Kumar• Bhuwan Chopra• Ankit Garg• Richa Singhania