Integrating Corporate Social Responsibility and Other Strategic Foci in a Distributed Production System A Transaction Cost Perspective on the North Sea Offshore Petroleum Industry Atle Midttun, Tore Dirdal, Kristian Gautesen, Terje Omland, Søren Wenstøp Research Report 11/2005 BI Norwegian School of Management Departement of Innovation and Economic Organization

Transcript

Integrating Corporate Social Responsibility and Other Strategic Foci in a Distributed

Production System

A Transaction Cost Perspective on the North Sea Offshore Petroleum Industry

Atle Midttun, Tore Dirdal, Kristian Gautesen, Terje Omland, Søren Wenstøp

Research Report 11/2005

BI Norwegian School of Management Departement of Innovation and Economic Organization

The paper explores the challenges of integrating CSR with other strategic foci into the supply/contractor chain, both conceptually and empirically, with a focus on one sectorial case: the Norwegian upstream petroleum industry. It compares contradictory theories of strategic focus and explores their implications for the organisation of the supply chain and discusses challenges and solutions for operative CSR oriented supply chain manage-ment Design/methodology/approach The empirical analysis, inspired by the cognitive mapping approach, seeks to elicit the strategic profiles of the oil majors and suppliers/contractors in the petroleum industry. This is based on textual analysis of core statements of overall business strategy such as the CEO’s and the Chairman’s statement letter to the shareholders.

The paper also draws on research and workshops with petroleum companies and their suppliers in the North Sea, as well as contracting experts and researchers taking part in the EU-TRENDS project which focused on satisfying Europe’s future demands and needs for sustainable, secure, safe and clean energy supplies.

Findings The strategic profiles of the petroleum companies and their suppliers/ contractors indicate that, while they coincide on many points, there is considerable discrepancy as far as CSR and HSE is concerned. The suppliers/contractors tend to emphasise the technology dimension more strongly than the petroleum companies. HSE and CSR are, on average, strategically under-communicated within the supply industry compared to the petroleum companies, but there is also considerable variation within each group. Research limitations/implications The paper explores how transaction cost theory may help frame managerial challenges and approaches in integrating CSR consistently throughout supply chains. It shows some of the limitations of the “rationalist” model of industrial organisation both at the firm level and at the supply chain level and discusses possible expansions into broader managerial approaches. Practical implications The paper highlights some of the managerial challenges and basic approaches for integrating CSR consistently throughout the value chain.

4

Originality/value The originality of the article lies conceptually in linking the CSR literature to transaction cost theory of industrial organisation. Empirically the article presents new insights into strategic foci of the petroleum companies and their supply chain Keywords CSR, Petroleum industry, supply chain, transaction cost Oslo, September 2005 Atle Midttun E-mail: [email protected] phone +4767557234

5

Introduction

Over the last decade Corporate Social Responsibility (CSR) has risen steadily higher on the international agenda. Extensive expectations of responsible corporate behaviour are also embedded in a number of initiatives from governments and global organisations1.

Large West European and North American multinational companies are now, in particular, finding it necessary to develop CSR programmes and initiatives to comply with societal expectations, voiced by sophisticated interest groups often backed up by media.

In an increasingly media-driven society, the concern with brand profiling and reputation effects, are seen to demand corporate responsibility at a new level. This trend has been backed up by several analytical arguments, including Edward Freeman’s (1999) argument for the benefits of broad stakeholder engagement, Charles Fombrun’s (2000) argument for CSR as a part of reputation building and John Elkington’s (1998) argument for CSR as a contribution to long-term commercial, ecological and social sustainability.

However, while the engagement of firms in CSR and stakeholdership has received extensive support in business practice as well as in parts of the management literature, other parts of the literature have raised serious concerns about the consequences of extensive CSR engagement for competitiveness and strategic focus. Notably, Jensen (2001) has argued that, in a world where firms must serve multiple stakeholders, each with their own claims as to what the legitimate goals of the firms should be, firms are left without a focus, and without a benchmark against which their managers can be held accountable. In Jensen’s own words “Because the advocates of stakeholder theory refuse to specify how to make the necessary tradeoffs among these competing interests, they leave managers with a theory that makes it impossible for them to make purposeful decisions, with no way to keep score, stakeholder theory makes managers unaccountable for their actions.” Adding CSR to other more

1 These include, the OECD guidelines for multinational companies, which give them an expanded responsibility for their global operations; the UN’s Global Compact whereby Kofi Annan has taken an initiative to strengthen the responsibility of industry for human rights, working conditions and the environment; new legislation at the national level being established in an increasing number of industrial countries which mandates reporting on social and environmental impacts of their activities. Socially responsible investment initiatives in the financial markets, increasingly supported by pension funds and other institutional investors, that have raised investor-pressure on companies to take social responsibility

6

conventional business concerns, in other words, introduces, for Jensen, a critical governance problem.

With increasing outsourcing of industrial production (Sturgeon 2002; Langlois 2003) the controversy of CSR engagement also spills over to management of the extended supply chain. In the view of the CSR proponents, a credible CSR policy must also include the extended supply chain. Initiatives like the Ethical Trading Initiative and the Forest Stewardship Council have thus sensitised public opinion, media and companies to corporate responsibility far beyond the boundaries of the firm. For instance, acceptable labour conditions in the textile industry in Asia, that supplies West European and North American retailers, is seen to be a necessary element of a credible CSR policy for the retailers. Likewise, acceptable forest management from raw material suppliers is seen to be a necessary part of CSR policy not only for paper manufacturers, but even for printers. However, from the perspective of Jensen’s governance critique, the adoption of CSR policies across the value chain is just as problematic as the adoption of CSR in an individual firm. In this context the governance problem translates into contractual challenges between the core brand-carrying company and its suppliers. Just as the lack of a single objective function in the case of a firm, according to Jensen, leaves it without guidance in setting priorities between conflicting interests, the lack of a concerted focus leaves the members of the distributed production system with potential competition between CSR and traditional business goals when it comes to optimising their contractual and organisational ties.

A Transaction Cost Perspective The conceptual apparatus of transaction cost theory allows us to formulate the challenge of integrating CSR in a distributed supply chain more precisely: The original transaction cost argument, as formulated by Coase in 1937 argued that the selection of market contracts versus hierarchic, integrated organisation of a production system is driven by an attempt to minimise transaction costs. Further development of this paradigm, notably by Williamson (1975, 1979, 1985, 1993a, 1993b) as a synthesis of economics, law and organisation theory, has developed a framework for classification and prediction of a number of mixed governance forms which are seen as intermediary forms between markets and hierarchy. Transaction cost theory postulates that, in essence, the choice of economic organisation of interfacing complementary processes in a production system is primarily determined by asset specificity, but also by uncertainty and the frequency of transactions. By asset specificity Williamson means the degree to which the transaction is dependent on

7

durable transaction-specific investments, particularly seen from the point of view of the supplier. With low asset specificity, the parties can easily integrate the supply chain/ system via market-contracts. With high asset specificity, the parties are better advised to integrate under common governance within the unitary firm.

In the setting of a distributed production system the challenge of multiple strategic foci is, in other words, turned into a challenge of competing models of economic organisation. On the one hand CSR seems to be increasingly demanded by interest groups and public opinion. On the other hand it may create difficult trade-offs in contracting and economic organisation.

The challenge may be how to organise the production system when one focus dictates loose coupling and another focus dictates integration. For example, static efficiency considerations may, by transaction cost standards, indicate market based commercial contracting as an optimal organisational strategy, whereas social and/or environmental concerns may dictate hierarchic integration or long-term alliances because of stronger asset specificity along this dimension. In such a case the chain would forsake efficiency by integrating the supply chain to accommodate the CSR focus. On the other hand, by increasing competitive market exposure to accommodate efficiency, it might undermine its CSR credibility.

An even more challenging situation is when a CSR and an efficiency perspective dictate two different sets of suppliers. This creates trade-offs also in the prioritisation between alternative partnership sets, one presumably with optimal efficiency capabilities and the other with CSR strengths, leading to obvious business dilemmas.

The Case of Petroleum Industry The paper explores the challenges of integrating CSR with other strategic foci into the supply/contractor chain, with an empirical focus on one a sectorial case: the Norwegian upstream petroleum industry. The upstream petroleum industry is extensively outsourced, with the petroleum companies sometimes providing as little as 20% of the total value creation. Norway is the world’s third largest exporter of petroleum after Saudi Arabia and Russia and hosts many of the largest players in the petroleum field both among the petroleum companies and the supplier industry. Figure 1 gives an overview of the main elements of the petroleum value chain. Key tasks in the upstream petroleum sector are: exploration, engineering and project management, construction of production facilities, subsea construction, pipelaying and fabrication of subsea equipment, installations and operations (production of oil).

8

Figure 1 The value system in petroleum industry

These tasks are performed by a host of suppliers and their sub-suppliers under the control of the petroleum companies, who hold the licences for exploration and production, To reflect this industrial configuration, the company sample in this analysis includes petroleum companies, operative on the Nordic Continental Shelf including five of the largest petroleum companies globally2: BP, Shell, Exxon Mobil, Total and Chevron Texaco, and two much smaller Norwegian companies, Statoil and Norsk Hydro. With respect to the supply/contractor industry, we have included some of the largest companies operating on the NCS, as well as some smaller ones, to capture a wide spectrum of activities in the NCS upstream petroleum sector3. This includes global suppliers such as, Halliburton, Baker Hughes, ABB, Schlumberger and FMC Technologies but also Norwegian suppliers such as the Kongsberg group, Corrocean, Aker Maritime, Stolt Offshore, Oddfjell Drilling, Petroleum Geo Services and Prosafe.

From a CSR perspective, the Norwegian continental shelf provides a context with considerable focus on social responsibility and thus an area where there is a strong likelihood that the challenge of reconciling efficiency and responsibility would be present. The strong Norwegian tradition of

2 based on data provided by Petroleum Intelligence Weekly 3 As a starting point for selection we used a list that presented the various suppliers of products and services that do business in relation to the Norwegian oil and gas industry. This list (published in 2001) was compiled by The Norwegian Trade Council (NTC) in collaboration with The Confederation of Norwegian Business and Industry (NHO) and The Norwegian Industrial and Regional Development Fund (SND). We then restricted our selection according to the preference stated above.

Platform andsubsea equipment

ExplorationField

DevelopmentProduction Exploitation Refining Distribution Consumer

Seismic data

Gas in pipesReservoirtechnology

Engineeringand projectmanagementsystems

Build-out consepts

Maritimeservices

Drilling rigs andships

Securitycertification

Drillingequipment- andsystems

Pipes

Platforms andproductionvessels

Oil on shipsSupply shipsand supplybases

Upstream Downstream

Platform andsubsea equipment

ExplorationField

DevelopmentProduction Exploitation Refining Distribution Consumer

Seismic data

Gas in pipesReservoirtechnology

Engineeringand projectmanagementsystems

Build-out consepts

Maritimeservices

Drilling rigs andships

Securitycertification

Drillingequipment- andsystems

Pipes

Platforms andproductionvessels

Oil on shipsSupply shipsand supplybases

Upstream Downstream

ExplorationField

DevelopmentProduction Exploitation Refining Distribution Consumer

unionisation and social and environmental concerns are important underlying factors. The focus on Core Strategy Statements Defining integration of CSR into core strategy as the prime responsibility of top management, we have concentrated the empirical analysis of CSR in the companies’ strategic profiles on core statements of over all business strategy such as the CEO’s and Chairman’s statement letter to the shareholders. These letters/statements represent high-level strategy statements, signalled at the top level of the firm and appear in all companies, thereby providing a general basis for comparative analysis across companies. Each sentence in the letters/statements containing a strategic orientation was analysed and sorted into one of the seven categories. The scores in each category was then normalised to a % share of the total number of sentences in the letter/statement. The scoring was undertaken by a team of three coders, who coded the sentences independently and then settled disagreements through discussion.

The analysis is inspired by the cognitive mapping approach (Eden et al 1992, Bonham 1993, Fuglseth 1989) as it seeks to elicit the strategic profiles of the oil majors and suppliers/contractors in the petroleum industry. However, instead of conducting interviews, a characteristic feature of this approach, we have based the discussion on textual analysis.

To condense the conceptual discussion the strategic foci that appear in the statements have been grouped into 7 dimensions or orientations:

1. technological performance 2. operational efficiency 3. financial performance 4. market position 5. human resources 6. health, safety and environment 7. CSR

Splitting the social/environmental dimension into two parts is a result of the fact that bordering on, and partly overlapping with the broad CSR agenda is a more focused “Health, safety and environment” agenda which the petroleum industry must relate to through mandatory legal requirements. Norway has, for instance, established a legal framework for Systematic Health, Environmental and Safety (HSE) activities in Enterprises, effective as of 1991. These regulations apply to managers, employees and employee

10

representatives in both public and private enterprises, when their products or services may harm customers or users4.

The HSE regulations resemble the CSR agenda as they relate not only to performance, but also to internal environmental and social practices. They require that all enterprises establish systems for the follow-up of HSE legislation through systematic measures, so that their activities are planned, organised, carried out, maintained and integrated through internal controls. The CSR focus, on the other hand, tends to be more directed towards issues of concern to particular external stakeholders or the public at large.

The traditional commercial dimensions such as technological and financial performance, operational efficiency and market positioning should be self-explanatory.

Besides the analysis of strategic statements in annual reports, the paper also draws on research and workshops with petroleum companies and their suppliers in the North Sea, as well as contracting experts and researchers. The workshops were conducted within the EU-TRENDS project, which focused on satisfying Europe’s future demands and needs for sustainable, secure, safe and clean energy supplies.

Strategic Profiles of Petroleum Industry and Suppliers/ Contractors The strategic profiles of the petroleum companies and their suppliers/ contractors indicate that, while they coincide on many points, there is considerable discrepancy as far as CSR and HSE is concerned (figure 2). Based on our qualitative content analysis we find that, on average, the petroleum majors and their suppliers/contractors agree on strong prioritising of market positioning (39% and 40%). They also agree on medium prioritising of operational efficiency (16% and 16%) and human resources (10 % and 9 %) However, the suppliers/contractors tend to emphasise the technology dimension more strongly (14%) than their contract partners, the oil companies (4%) do. HSE and CSR are, however, on average strategically under-communicated with the supply industry, whereas both issues receive medium attention with the petroleum companies. For CSR the share of strategic focus from the suppliers was 4.% while it was 14% with the

4 The purpose of the regulations is the promotion of continuous improvements in enterprises in the following areas: (1) working environment and safety, (2), protection of the environment from pollution (3), prevention of damage to health or environmental disturbances from products or consumer services, and finally (4) treatment of waste.

11

petroleum industry. For HMS, the share of strategic focus from the suppliers was 8% while it was 10% with the petroleum industry. Figure 2 Comparative strategic profiling of average petroleum majors and suppliers/contractors

One of the most striking findings was the large variation within each group. We found petroleum companies flagging CSR in up to 14% of their statements, while we found suppliers for whom CSR was not part of their strategic positioning at all. CSR engagement, therefore, seems to be fairly mixed in petroleum industry and even more mixed across the supply chain. This implies that one may find petroleum companies with a high CSR profile supplied by companies where CSR is strategically non-existent.

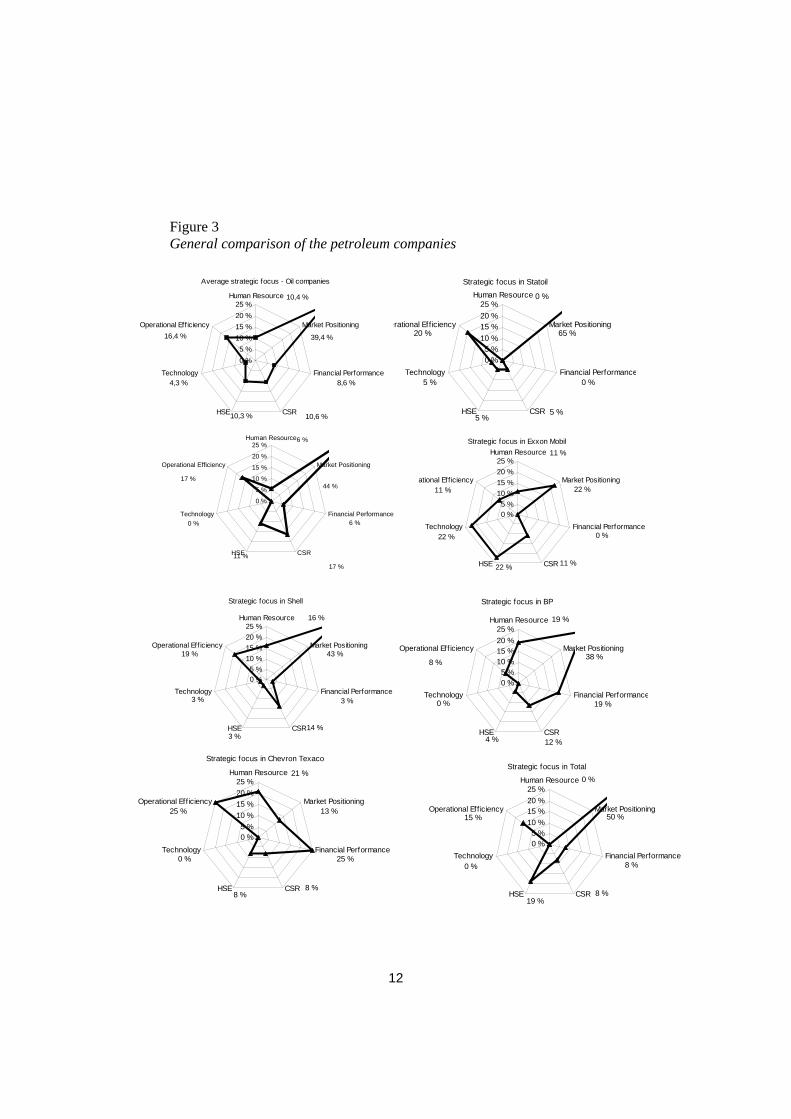

Individual Petroleum Companies The mixed picture of the petroleum company profile comes across in a more disaggregated display of individual company profiles. (Figure 3).

0,0 %5,0 %

10,0 %15,0 %20,0 %25,0 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Efficiency

Oil companiesSuppliers

12

Strategic focus in BP

12 %4 %

0 % 19 %

38 %

19 %

8 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in Exxon Mobil

22 %

11 %

11 %

22 %

22 % 11 %

0 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Figure 3 General comparison of the petroleum companies

Strategic focus in Statoil

20 %

5 %

5 %5 %

0 %

0 %

65 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in Shell

43 %

3 %

14 %3 %

3 %

19 %

16 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in Chevron Texaco

21 %

13 %

25 %

8 %8 %

0 %

25 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in Total

50 %

19 %

0 %

8 %

15 %

8 %

0 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in Hydro

17 %

6 %

44 %

6 %

17 %

0 %

11 %

0 %

5 %

10 %

15 %

20 %

25 %Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Efficiency

Average strategic focus - Oil companies

8,6 %

10,4 %

39,4 %

10,6 %10,3 %

4,3 %

16,4 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Efficiency

13

Among the petroleum companies we find Shell and British petroleum leading in incorporating CSR in their strategic outlook. Shell is obviously a forerunner when it comes to CSR policy and soft values in their strategic focus. Compared to the oil companies average, Shell has more focus on Human Resource and CSR, as indicated in the statement: “We believe that long term competitive success depends on being trusted to meet society’s expectations”. On the other hand, Shell has little focus on HSE and Financial Performance.

BP has likewise deliberately chosen a soft strategy, with higher focus on Human Resources and CSR. This is profiled in core strategic statements such as “We have to see too that our activities are conducted in line with high ethical standards, and that we are contributing to human progress in the communities in which we work.” Exxon Mobil, Total and to some extent Norsk Hydro convey strong HSE commitment in their top level strategic positioning.

The HSE orientation in Exxon Mobil comes across clearly in the following statement: “Exxon Mobil has shown that we can produce energy and chemical products while protecting the safety and health of people and safeguarding the environment. Our goal is no injuries, illnesses or operational incidents”. Exxon Mobil is, however, the most technology focused petroleum company, according to their top level strategic profiling. This comes clearly across in statements such as: “Technology has played – and will continue to play – an important role in our environmental performance, in our improvements in product quality and in our production of cleaner fuels, as well as in resource development”.

Total also has a more than average focus on HSE, as illustrated in the following statement: “Our goals are to set the standard not only with our financial performance, but also with our stringent requirements for operational safety, environmental protection and stronger ties with all parties that have a stake in our activities”. In addition, Total has an extensive focus on market positioning and operational efficiency.

Norsk Hydro is also concerned about CSR, HSE and operational efficiency to a greater degree than average: “Hydros purpose is to create a more vigorous community through innovation and efficient exploitation of natural recources and products. There is little focus on technology in the CEO letter. The main strategic focus in Norsk Hydro is on market positioning.

In its CEO letter, Statoil focuses most on its market positioning strategies, as indicated by the statement: “We are investing in the future on the NCS” Compared to the average of oil companies, Statoil has slightly more focus on operational efficiency, but no focus on Human Resources and Financial Performance. The CSR focus in Statoil is less than average for oil companies.

14

Chevron Texaco differs from the average in hat very little focus is placed on Market Positioning. Instead, most of the company’s strategic attention is paid to Operational Efficiency, Human Resources and Financial Performance. The financial performance focus comes across clearly in statements such as: “And we are focused on our most important financial objective – to be No. 1 among our largest global competitors in total stockholder return for the period 2000 through 2004”.

To sum up, there seems to be no simple industry standard, and the over all focus on CSR is obviously open to extensive strategic variation among petroleum companies.

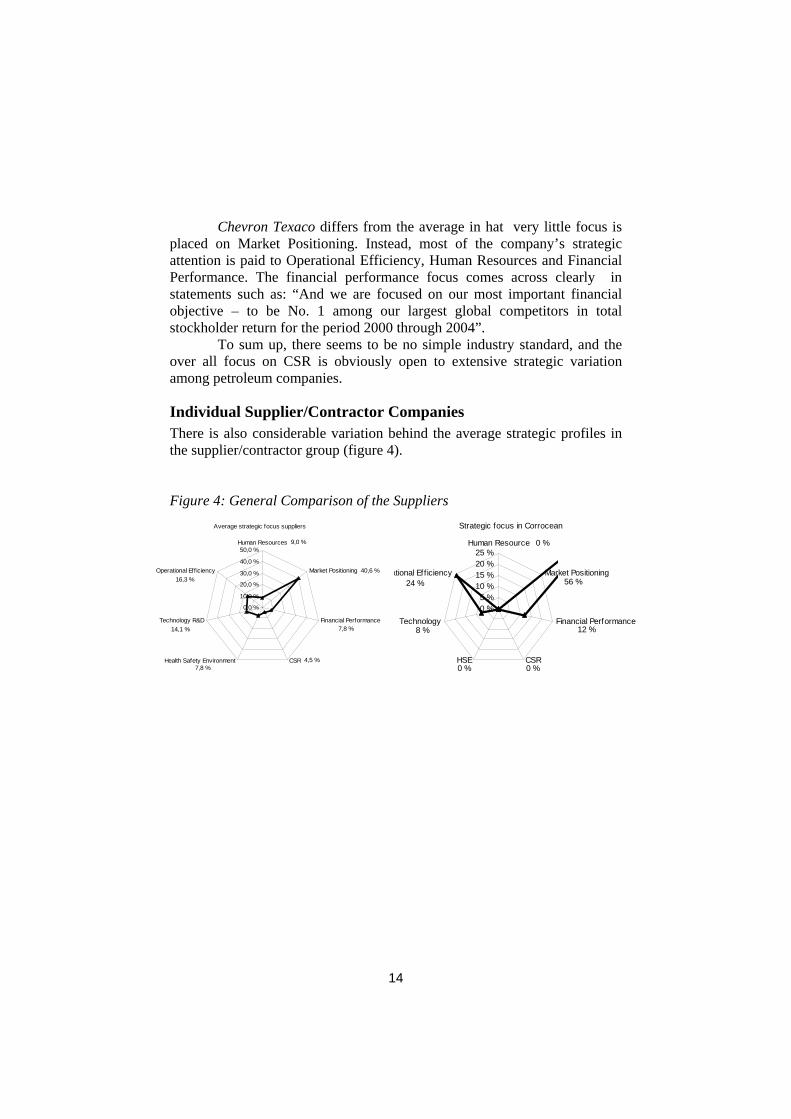

Individual Supplier/Contractor Companies There is also considerable variation behind the average strategic profiles in the supplier/contractor group (figure 4). Figure 4: General Comparison of the Suppliers

Strategic focus in Corrocean

56 %

12 %

0 %0 %

8 %

24 %

0 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Efficiency

Average strategic focus suppliers

4,5 %

7,8 %

40,6 %

9,0 %

16,3 %

14,1 %

7,8 %

0,0 %

10,0 %

20,0 %

30,0 %

40,0 %

50,0 %Human Resources

Market Positioning

Financial Performance

CSRHealth Safety Environment

Technology R&D

Operational Efficiency

15

Strategic focus in Kongsberg Gruppen

45 %

27 %

0 %

0 %0 %

27 %

0 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in ABB

14 %

32 %

0 %

0 % 9 %

14 %

32 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in Aker Maritime

64 %

5 %

0 %5 %

5 %

18 %

5 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in PGS

52,4 %

19,0 %

0,0 %0,0 %

0,0 %

14,3 %

14,3 %

0 %5 %

10 %15 %20 %25 %

Human Resource

Market Positioning

Financial Performance

CSRHSE

Technology

Operational Eff iciency

Strategic focus in Baker Hughes

3,1 %

15,6 %

18,8 %

9,4 %

34,4 %

12,5 %

6,3 %

0,0 %

5,0 %

10,0 %

15,0 %

20,0 %

25,0 %Human Resources

Market Positioning

Financial Performance

CSRHealth Safety Environment

Technology R&D

Operational Efficiency

Strategic focus in FMC Technologies

14,8 %

3,7 %

25,9 %

14,8 %

0,0 %

29,6 %

11,1 %

0,0 %

5,0 %

10,0 %

15,0 %

20,0 %

25,0 %Human Resources

Market Positioning

Financial Performance

CSRHealth Safety Environment

Technology R&D

Operational Efficiency

16

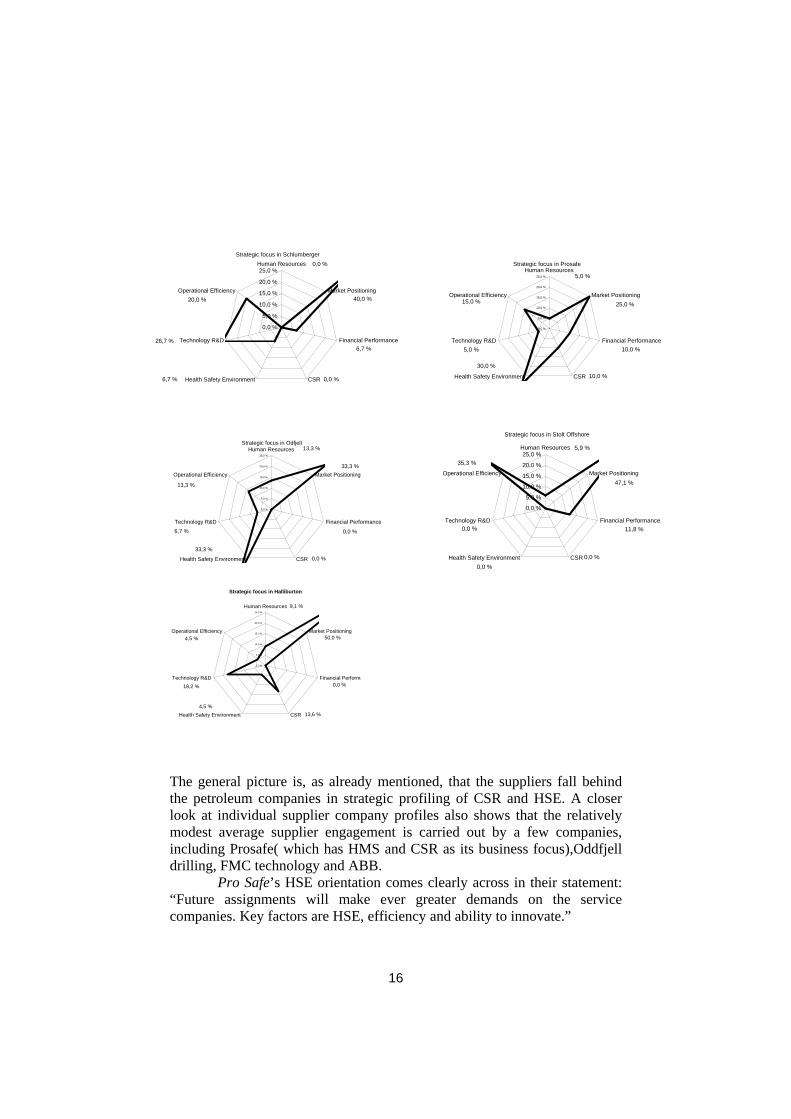

The general picture is, as already mentioned, that the suppliers fall behind the petroleum companies in strategic profiling of CSR and HSE. A closer look at individual supplier company profiles also shows that the relatively modest average supplier engagement is carried out by a few companies, including Prosafe( which has HMS and CSR as its business focus),Oddfjell drilling, FMC technology and ABB.

Pro Safe’s HSE orientation comes clearly across in their statement: “Future assignments will make ever greater demands on the service companies. Key factors are HSE, efficiency and ability to innovate.”

Strategic focus in Schlumberger0,0 %

40,0 %

6,7 %

0,0 %6,7 %

26,7 %

20,0 %

0,0 %

5,0 %

10,0 %

15,0 %

20,0 %

25,0 %Human Resources

Market Positioning

Financial Performance

CSRHealth Safety Environment

Technology R&D

Operational Efficiency

Strategic focus in Prosafe

10,0 %

10,0 %

25,0 %

5,0 %

15,0 %

5,0 %

30,0 %

0,0 %

5,0 %

10,0 %

15,0 %

20,0 %

25,0 %

Human Resources

Market Positioning

Financial Performance

CSRHealth Safety Environment

Technology R&D

Operational Efficiency

Strategic focus in Odfjell

0,0 %

33,3 %

0,0 %

33,3 %

6,7 %

13,3 %

13,3 %

0,0 %

5,0 %

10,0 %

15,0 %

20,0 %

25,0 %

Human Resources

Market Positioning

Financial Performance

CSRHealth Safety Environment

Technology R&D

Operational Efficiency

Strategic focus in Stolt Offshore

5,9 %

47,1 %

0,0 %

11,8 %

0,0 %

0,0 %

35,3 %

0,0 %

5,0 %

10,0 %

15,0 %

20,0 %

25,0 %Human Resources

Market Positioning

Financial Performance

CSRHealth Safety Environment

Technology R&D

Operational Efficiency

Strategic focus in Halliburton

9,1 %

4,5 %

18,2 %

4,5 %13,6 %

0,0 %

50,0 %

0,0 %

5,0 %

10,0 %

15,0 %

20,0 %

25,0 %

Human Resources

Market Positioning

Financial Performa

CSRHealth Safety Environment

Technology R&D

Operational Efficiency

17

Odfjell Drilling signals a strong HSE Orientation, following a period of setbacks: “The company suffered a setback to its continual improvement objective in 2003 and has implemented means to further strengthen training and safety management with particular emphasis being put on human behaviour.”

FMC signals its HMS and CSR orientations in statements such as: “Our success is ultimately determined by our people and their commitment to customer support, quality, environmental protection and employee safety.” And: “Although mindful of the risks presented by an organisation with thousands of employees and a global reach, we believe that through leadership, training, vigilance and a strong ethical compass, we can preserve the trust we have worked so hard to earn among all of our stakeholders.”

Similarly, ABB signals its CSR orientation in statements like: “Our strengths are in technology and our pioneering spirit. We contribute to economic, environmental and social development wherever we do business. Measuring our performance on the so-called triple bottom line, we are putting ABB back on the path to profitable, sustainable growth.”

Many of the suppliers follow the petroleum companies in their strong focus on market positioning. As indicated in figure 4, this includes companies such as Corrocean, Aker Maritime, Bakher Hughes, Haliburton and Schlumberger.

Like average suppliers (and oil companies), Corrocean also has it main strategic focus on Market Positioning. But unlike the average of suppliers, Corrocean has no focus on either Human Resource, HSE or CSR. Instead they focus more on operational efficiency: “Looking ahead, it is crucial to improve cost controls and implement initiatives geared towards becoming more competitive”.

Aker Maritime is a highly Market Positioning oriented company: “We are directing our activities towards three market segments; technology and products, field development and service and operations”. The company equals the suppliers’ average on Operational Efficiency focus, and all other dimensions, except HSE, are less important.

Stolt Offshore is also strongly oriented towards market positioning, as indicated by the statement: “We have aggressively refocused the Company on the markets where we have the most to offer, restructured the business so that it can more efficiently address these markets and reinforced the procedures that will deliver quality project management.” However, the company also has a strong focus on operational efficiency.

Baker Hughes has a strong orientation towards market positioning and a strong technological orientation, as is made clear by the following statement: “Baker Hughes has been a leader among the major oilfield service companies in focusing on our industry. Our six product line focused

18

divisions deliver best-in-class technology and are leaders in their chosen market segments.” A similar profile characterises Halliburton, as indicated by the statement: “One day, I believe, we will look back on 2003 as a watershed year when we took steps to become a leaner, tougher organisation and continued to put ourselves in position to win in the years ahead.”

Schlumberger also resembles Baker Hughes and Halliburton, with a strong emphasis on market positioning, but also with a strong technological focus. The markets positioning focus is evident in the statement: “The markets for oilfield services are changing, and the way in which oilfield services companies respond is also changing. The growing markets of Russia, some of the former Soviet republics, and more gradually China require a new approach, and nowhere is this more evident than in the operations of Integrated Project Management.” A distinguishing feature with many supplier companies is their strong focus on technology. This is very clearly displayed by the Kongsberg group, FMC, as well as by Schlumberger.

In the Kongsberg Group’s strategic profiling this clearly comes across in the following statement: “At Kongsberg, technology is not merely a tool for product development, but a sort of “religion”, something in which we believe and use actively, all the time”. Kongsberg has no focus on Operational Efficiency, HSE, CSR or Financial Performance.

In FMC Technologies technology is similarly stressed in statements like: “In 2003, we continued to invest in the acquisition and development of technologies that will help build our future. Our technology development is driven by the needs of our customers and our commitment to provide them with the most effective solutions for their challenges.”

As already mentioned, Schlumberger also has a strong technological dimension in its strategic profiling. This comes across in statements such as “Schlumberger, through its people and its technology, strives to provide global leadership and innovation within the energy services industry.” Finally, PGS stands out with a strong financial focus, as indicated by the statement: “As announced in the beginning of the fiscal year 2001, PGS embarked on an ambitious program of initiatives to return the Company to profitability and improve the return on our shareholder’s investment”.

Discussion and Normative Implications The analysis of top-level strategy statements indicates that there is room for concern about the compatibility of strategic foci amongst the contracting partners in the petroleum industry supply chain/system. Judging from the top level strategy formulations of the companies analysed, there seems to be a

19

credibility gap when it comes to having CSR and HSE (as profiled by the most advanced petroleum companies) trickling down in the strategic profiling of their supply chain, The suppliers/contractors seem, on average, more concerned with strategically profiling their technology orientations. Traditional economic foci and market positioning, in particular, prevail as dominant orientations for most supplier companies. Furthermore, their CSR profiles varies extensively, with many suppliers not focusing on CSR at a strategic level at all.

Given that as much as 80% of upstream petroleum activities may be outsourced to the supply industry, the CSR gap may threaten the credibility of the oil majors. Their size and dominant bargaining positions may easily lead to expectations of more concerted action throughout their supply chains. However, such integrated control strategies may come into conflict with bargaining strategies aimed at cost-efficient performance.

As a result, they may wish maximum competitive exposure of their suppliers, which, in turn, makes a more integrated CSR alignment difficult. They may hence experience tension between competing modes of industrial organisation in line with predictions from transaction cost theory. However, while Jensen (2001) is obviously right in pointing out dilemmas facing firms with multiple strategic foci, our analysis shows that such discrepancies do not only arise with CSR issues. Our material documents extensive divergence in prioritising between the different commercial dimensions as well as between static and dynamic efficiency. The static versus dynamic efficiency challenge has been very interestingly described by March (1991) among others as a tension between exploration and exploitation and indicates that firms have considerable experience in living with incommensurable strategic concerns.

The CSR issue is, therefore, hardly unique in posing challenges of a difficult judgmental character. Such judgmental evaluation must also be carried out in the case of static versus dynamic efficiency, where there is no simple formula to translate priorities in one sphere to priorities in another, as is the case for many other sub-goals in the traditional business repertoire.

A possible explanation of the divide between the CSR orientation of the petroleum companies and the more technologically and economically oriented strategic focus of their suppliers may be that the two orientations respond to different needs. The new CSR agenda has possibly come in response to increasing demands from the public and new stakeholders, directed primarily at the more visible petroleum companies. The traditional technically and economically related strategic focus might have survived better in the less exposed internal contracting in the supply chain.

CSR, may therefore have been flagged by some the petroleum companies as an up-front showpiece to meet increasing demands from their stakeholders, which they may even have seriously implemented in their own

20

organisation. At the same time they seem to have, de facto, prioritised technology and efficiency in their contracts with the suppliers. In this way the supply industry is responding adequately to what the petroleum companies are looking for, as far as this particular contractual specification is concerned. However this strategy may pose a credibility gap when CSR oriented stakeholders start inspecting the supply chain.

The transaction cost framework indicates several ways to meet the CSR dilemma and its challenge to industrial organisation. As pointed out in (table 1), there are at least three basic ways to organise the petroleum company/supplier interface with respect to CSR: strategic alignment, operative implementation and externalisation to Government. Table 1 Three basic ways to organise interfaces between petroleum company and suppliers with respect to CSR Strategic alignment Operative

implementation Externalisation to Government

Organisation of the Interface petro-co/ suppliers

Strategic integration

Contractual Specification

Taken for granted

Focus of petroleum company

Strategic focus on CSR

Strategic CSR focus

Non-strategic CSR compliance

Focus of suppliers Strategic focus on CSR

Operative CSR implementation

Non-strategic CSR compliance

Focus of public authorities

Disengaged or facilitating

Disengaged or facilitating

Regulative engagement

The first and most demanding solution, Strategic Alignment, would be to streamline the strategic profile of the value chain to systematically include a CSR agenda/focus. This would imply considerable strategic integration of the supply chain, and the system could add on costs due to the limited market exposure.

A second way to handle discrepancies in strategic foci would be to maintain highly profiled strategic flagging by the petroleum companies, but only operative implementation throughout the supplier system. The petroleum major can then leave the suppliers to flag their own strategies, but must specify operative criteria for CSR implementation and implement these criteria in the supplier contracts. A third way would be to externalise environmental and social responsibility to the public authorities. CSR would then become standardised

21

practice, mandated by law. In this case, strategic profiling of CSR would give no extra image-effect and the firm would leave both the operative and strategic tuning of its suppliers to the state.

Perspectives From Working Group With Petroleum Industry Three workshops were held throughout 2003 and 2004 with petroleum companies under the UE financed TRENDS project including Shell, Total, Norsk Hydro and Statoil, and suppliers including ABB, Aker Kværner, Schlumberger and Tess. Discussions in these workshops indicate that all three approaches presented above are relevant and being discussed in the industry.

Strategic alignment Expanding on the strategic alignment approach, petroleum companies emphasised the need to raise the awareness of CSR issues in the supply chain in their own organisation and in the industry in general. There was agreement among the petroleum companies that sustainable value propositions need to build on important and credible relationships. The vehicle for achieving this was seen to be the development of partnerships with efficient suppliers to secure CSR alignment and enhanced reputation throughout the value chain. Petroleum companies also saw the need to subsequently align their rewards system with enhanced social performance and to embed CSR issues in supplier evaluation and purchasing practices in order to give credibility to the strategic alignment strategy and to be able to influence suppliers to adopt their standards.

Certain petroleum companies also regretted going too far in their market orientation, dismantling their contract procurement some time ago and decentralising supplier contracts, to the extent of losing necessary strategic control. One of these companies is now in the process of re-centralising, to achieve greater strategic alignment. The positions of the supplier industry on strategic alignment varied somewhat. While one of the suppliers, which profiled itself as transferring advanced eco-efficiency, welcomed it, another supplier kept a low public profile on CSR because it was exposed to different clients with different needs and profiles. While this supplier saw itself as a relatively high performer in CSR, it was not valued by its customers in this respect. Yet a third supplier took an intermediary position by seeking to integrate CSR into the regular business process, without profiling it specifically. Contractual strategy The operative implementation of CSR, primarily based on contractual arrangements, was also discussed in the working group. As pointed out by the legal representative in the group, CSR could be included in new clauses

22

in the supplier’s contract, supported by both negative and positive incentives. The positive incentive could be an increased price to ensure CSR issues were complied with, while the negative incentive could be an indemnity clause providing petroleum company with compensation if suppliers failed to comply. The positive incentive approach obviously resonated better with the supply companies, while the negative incentive met some of the risk concerns of the petroleum companies..

More specifically, a contractual approach would require the petroleum company to define the required level of CSR and include this in a section of the supply contract. As well as references to licence conditions or governmental/local regulations, the petroleum company’s real understanding of the content of the CSR and systems implemented to manage CSR issues would be specified. The relationship between the petroleum company and its supplier would also have to be defined with respect to CSR and how this would be developed and controlled/managed. As pointed out by a contract expert in the work group, a contractual strategy would also have to point out procedures to determine the consequence under a breach, define arbitration procedures and specify economic losses to the petroleum company. A particular challenge to a contractual strategy would be the determination of non- economic losses. Such losses could be compensated by a standard fee to be paid by the supplier if damage was caused by the supplier or the supplier’s employees. Regulation The regulation approach was by many companies seen as a fallback position. In the view of most of the petroleum companies, the petroleum industry and its suppliers should develop a contractual arrangement to manage CSR issues and be ahead of governmental bodies Particular emphasis was placed on the ability of the petroleum industry to take strategic CSR initiatives when operating in weak state contexts such as in Angola, where the company has to step in for the state to build decent framework conditions. Nevertheless, many companies saw the need to set minimum level requirements by regulation and then increased levels through company strategy. Furthermore, suppliers intrigued by the different standards set by different customers, were attracted to the standardisation that government regulation might imply. In principle, CSR regulation would allow companies to optimise industrial organisation with a focus on traditional business factors and thereby potentially harvest efficiency gains as CSR would be maintained by government standards. On the other hand, government regulation might also introduce costs in the form of regulatory barriers and neglect of possibly

23

more efficient industrial implementation, particularly in a globalising economy, given the weakness of international regulatory organisations.

Conclusion Arguments can be put forward for developing CSR in the petroleum industry through various approaches. While there is good reason to expect that present discrepancies in the supply chain will be further challenged by engaged stakeholders, it is harder to define optimal solutions. While strategic alignment may appear an attractive tool for implementation, it would go against a powerful trend of outsourcing and market exposure that presumably carries efficiency gains. Furthermore, advances in regulatory theory and practice presents us with interesting bridges between government and self-regulation (Ayres & Braithwate 1992; Brown Weiss 1999, Baldwin et al 1998, Fox et al 2002). Most probably we will therefore see changes based on mixed approaches where advanced contracting also plays a central role. To optimise industrial organisation along one dimension remains an interesting heuristic idea in neoclassical economic theory of organisation, which, will inevitably be blurred by the real world multidimensionality of business, In this context, CSR is only one among a number of dimensions not always pointing in the same direction.

24

References: Ayres, I & Braithwaite, J (1992) Responsive Regulation: transcending the deregulation debate. Oxford University Press. Oxford Baldwin, Robert; Scott, Colin and Hood, Christopher (1998): A Reader on Regulation. Oxford University Press. Oxford Brown Weiss, E (1999) “The Emerging Structure of International Environmental Law” in Vig, Norman J. and Axelrod, R.S (eds) The Global Environment. CQ press Washington Bonham, Matthew, G (1993) “Cognitive Mapping as a Technique for Supporting International Negotiation” Theory and Decision vol 34 Bromley, D. (2002) “Comparing corporate reputations; League tables, quotients, benchmarks or case studies?” Corporate Reputation Review, 5, 1, 35-50. Coase, R. H. (1937), “The Nature of the Firm”, Economica, 4, 386-405. Eden, Colin, Ackerman, Fran and Cropper, Steve (1992): “The Analysis of Cause Maps” Journal of Management Studies vol 29 no 3 Elkington, J: 1998, Cannibals With Forks: The Triple Bottom Line of 21st Century Business, New Society Publishing Fombrun, C.J., Gardberg, N.A. and Sever, J.M. (2000) “The Reputation Quotient: A multistakeholder measure of corporate reputation”, The Journal of Business Management, 7, 4, 241-255. Fox, T; Ward, H and Howard, B (2002): “Public Sector Roles in Strenghening Corporate social Responsibility: A Baseline Study” World Bank Report October 2002 Fuglseth, Anna Mette (1989): Beslutningsstøtte: metode for diagnose av lederes informasjons- og situasjonsoppfatninger. Phd dissertation, Norwegian School of Economis and Business Administration Freeman, R. E. & J. S. Harrison: 1999, ‘Stakeholders, Social Responsibility, and Performance: Empirical Evidence and Theoretical Perspectives’, Academy of Management Journal, Vol. 42, No. 5

25

Friedman, M.: 1970, ‘The Social Responsibility of Business Is to Increase Its Profits’, New York Sunday Times Magazine, 13 Sept. Jensen, M.: 2001, ‘Value Maximization, Stakeholder Theory, and the Corporate Objective Function’, Journal of Applied Corporate Finance, Fall 2001 Moss Kanter, Rosabeth (2001) “From Spare Change to Real Change: The Social Sector as Beta Site for Business Innovation” Harvard Business Review on Innovation. Harvard Business School Press. Langlois, Richard, N (2003): “The vanishing hand: the changing dynamics of industrial capitalism” Industrial and Corporate Change vol 12 no 2 Larkin, J. (2002) Strategic Reputation Risk Management, London. Porter, Michael and Kramer (2001): The Competitive Advantage of Philantrophy Stabell, C.: 2001, ‘New Models for Value Creation and Competitive Advantage in the Petroleum Industry’, Research Report 1/2001, The Norwegian School of Management Sturgeon, Timothy J. (2002) “Modular production networks: a new American model of industrial organization” Industrial & Corporate Change vol 11 no 3 Weiss, E. B.: 1999, ‘The Emerging Structure of International Environmental Law’ in Norman & Axelrod (eds) The Global Environment, Congressional Quarterly Press Williamson, O. E. (1975), Markets and Hierarchies: Analysis and Antitrust Implications, New York, Free Press.

Williamson, O. E. (1979), “Transaction Cost Economics: The Governance of Contractual Relations”, Journal of Law and Economics, 7, 233-261.

Williamson, O. E. (1985), Economic Institutions of Capitalism, New York, Free Press.

Williamson, O. E. (1993), “Calculativeness, Trust, and Economic Organization, Journal of Law and Economics, 36, 453-486.

26

Williamson, O. E. (1993a), “The Evolving Science of Organization”, Journal of Institutional and Theoretical Economics, 149(1), 36-63. Zadek, S.: 2001, The Civil Corporation: The New Economy of Corporate Citizenship, Earthscan Reports: Products & Services for the Oil & Gas Industry, 2001, Norwegian Trade Council, Index Publishing AS