Interest Rates Banks offer many different services, including savings accounts and loans. If you have a savings account with a bank, the bank pays you interest on the money in the account. If you take out a loan, you pay interest to the bank on the money you owe. Which will have the higher rate of interest, a savings account or an auto loan? Why?

Transcript

Interest Rates

Banks offer many different services, including savings accounts and loans. If you have a savings account with a bank, the bank pays you interest on the money in the account. If you take out a loan, you pay interest to the bank on the money you owe.

Which will have the higher rate of interest, a savings account or an auto loan?

Why?

Monday – Section 5-1 Tuesday ◦ Vocabulary Quiz, beginning of class ◦ Section 5-2

Wednesday – Section 5-3 & 5-4 Thursday ◦ Study Guide ◦ Audit your understanding quiz, end of class

Friday ◦ Chapter 5 test ◦ Chapter 6 – Read chapter, vocabulary, & audit your

understandings

Cash Control Systems

1. Define accounting terms related to using a checking account and a petty cash fund.

2. Identify accounting concepts and practices related to using a checking account.

3. Prepare business papers related to using a checking account.

4. Reconcile a bank statement.

5. Journalize dishonored checks and electronic banking transactions.

6. Establish and replenish a petty cash fund.

1. Code of conduct

2. Checking account

3. Endorsement

4. Blank endorsement

5. Special endorsement

6. Restrictive endorsement

7. Postdated check

8. Bank statement

9. Dishonored check

10. Electronic funds transfer

11. Debit card

12. Petty cash

13. Petty cash slip

Sections 5-1 thru 5-4

Quiz on Thursday!

A statement that guides the ethical behavior of a company and its employees

Focuses on the relationships with customers, employees, shareholders, suppliers, and community.

When in doubt, seek guidance from upper level management.

Not always the best advice…Enron.

"Respect: We treat others as we would like to be treated ourselves. Ruthlessness, callousness and arrogance don't belong here.”

"Integrity: We work with customers and prospects openly, honestly and sincerely. When we say we will do something, we will do it.”

"Communication: We believe that information is meant to move and that information moves people.”

"Excellence: We are satisfied with nothing less than the very best. We will continue to raise the bar for everyone."

Raise the bar, live behind bars,

it's all semantics.

In accounting money is referred to as cash. ◦ Most businesses make major cash payments by

cash.

◦ Small cash payments may be made from a cash fund kept at the place of business.

◦ Examples: Postage, supplies

Due to the frequency of cash payments: ◦ Greater risk for making recording errors

Transfer of cash from one person to another without question of ownership

Cash may be lost as it is moved from one place to another

Most companies keep most of its cash in the bank. ◦ Safety

◦ Deposits provide written evidence to support accounting records

◦ Checks written provide documentation of payments

◦ Greater control

◦ Accuracy

Check ◦ Business form ordering a bank to pay cash from a

bank account.

Checking Account ◦ A bank account from which payments can be

ordered by a depositor is called a checking account.

Signature Cards A signature card is a document that a bank keeps

on file with the signatures of all the authorized people on that account.

The bank employees can use this card to verify

signatures on checks to make sure the proper people sign them.

In other words, a signature card is a fraud prevention tool that a bank uses to make sure unauthorized people aren’t forging checks in the company’s name.

Deposit Slips

Each time cash or checks are placed into a bank account, a deposit slip is filled out.

Designs may vary from bank to bank, but all contain the same basic information: 1. Date 2. Currency amount 3. Coin amount 4. Checks – checks are listed on a deposit slip

according to the bank routing number on each check.

5. Total amount 6. Account name and number

Deposit receipts ◦ Copy of the printed receipt

◦ Stamped verification

Page 119 Printed verification

Date

D5000.00 – means $5000 was deposited

RDS – initials of the bank employee

After the deposit is recorded on the check stub, a checkbook subtotal is calculated.

The balance brought forward on Check Stub No. 1 is zero.

Previous balance + Deposit = Subtotal

Page 119 Balance Brought Forward + Deposit Subtotal +/- Other Subtotal - Amount of this check Balance Carried Forward

This should look familiar.

A signature or stamp on the back of a check transferring ownership

Federal regulations require that an endorsement be confined to a limited amount of space on the back of a check.

An endorsement should be signed exactly as the person’s name on the front of the check.

Ownership of a check may be transferred multiple times, resulting in several endorsements.

Each endorser guarantees payment of the check. If the bank does not receive payment from the person who signed the check, each endorser is individually liable for payment

3 types of endorsements:

1. Blank Endorsement

2. Special Endorsement

3. Restrictive Endorsement

Page 120

1. Blank Endorsement ◦ Consists only of the endorser’s signature ◦ A blank endorsement indicates that the

subsequent owner is whoever has the check

What are some cons with blank endorsements? ◦ If the check is lost or stolen, the check can be

cashed by anyone who has possession of it. ◦ Ownership may be transferred without further

endorsement. When should you use blank endorsement? ◦ Use only when a person is at the bank ready to

cash or deposit a check.

2. Special Endorsement ◦ An endorsement indicating a new owner of a

check.

◦ Known as endorsements in full.

◦ Include the words Pay to the order of and the name of the new check owner.

◦ Only the person or business named in a special endorsement can cash, deposit, or further transfer ownership of the check.

3. Restrictive Endorsement ◦ Restricts further transfer of a check’s ownership

◦ Limits use of the check to whatever purpose is stated on the endorsement.

◦ Many businesses have stamps prepared with a restrictive endorsement. Checks are immediately stamped upon receipt.

◦ Prevents unauthorized persons from cashing the check if it is lost or stolen.

Most businesses will use preprinted checks with check stubs attached.

Consecutive numbers are preprinted on the checks. ◦ Allows for an easy way of identifying each check. ◦ Keep track of all checks to assure that none are lost or

misplaced.

Check stub –

Business’s record of each check written for a cash payment transaction. (Objective evidence)

Complete check stub first to avoid forgetting to prepare it later.

Check is written after the check stub has been completed

1. Write the amount of the check in the space after the dollar sign at the top of the stub.

2. Write the date of the check on the Date line at the top of the stub.

3. Write to whom the check is to be paid on the To line at the top of the stub.

4. Record the purpose of the check on the For line.

5. Write the amount of the check in the amount column at the bottom of the stub on the line with the words “Amt. This Check.”

6. Calculate the new checking account balance and record the new balance in the amount column on the last line of the stub.

7. Write the date in the space provided. ◦ The date should be the month, day and year on

which the check is issued.

◦ Postdated check – a check with a future date. Most banks will not accept a postdated check.

8. Write to whom the check is to be paid following the words “Pay to the order of.”

◦ Business Entity (Accounting Concept) - if the person to whom a check is to be paid is a business, use the business’s name rather than the owner’s name. If the person to whom a check is to be paid is an individual, use that person’s name.

9. Write the amount in figures following the dollar sign.

◦ Write the figures close to the printed dollar sign.

◦ Prevents anyone from writing another digit in front of the amount to change the amount of the check.

10. Write the amount of the check in words on the line with the word “Dollars.”

◦ This amount verifies the amount written in figures after the dollar sign.

◦ Begin the words at the extreme left.

◦ Draw a line through the unused space up to the word “Dollars.”

Prevents anyone from using from writing additional words to change the amount.

If the amounts in words and in figures are not the same, a bank may only pay the amount in words.

Often, when the amounts do not agree, the bank will refuse the check.

11. Write the purpose of the check on the line labeled “For.”

◦ On some checks this space may be labeled “Memo.”

◦ Some checks do not have a line for writing the purpose of the check.

12. Sign the check. ◦ A check should not be signed until each item on the

check and its stub has been verified for accuracy.

Do you ever want to sign a blank check? Why?

1. Record the date in the date column

2. Write the word VOID in the Account Title column.

3. Write the check number in the Doc. No. column.

4. Place a check mark in the Post. Ref. column.

5. Place a dash in the Cash Credit column.

1 2 3 4 5

DOC. POST

NO. REF.

20 15 VOID C20

21

Date VOID Source Check Mark Dash in Credit column

Document

CREDITDATE ACCOUNT TITLE

GENERAL SALES CASH

DEBIT CREDIT CREDIT DEBIT

1. List the three types of endorsements.

3 types of endorsements:

1. Blank Endorsement

2. Special Endorsement

3. Restrictive Endorsement

2. List the steps for preparing a check stub.

1. Write the amount of the check in the space after the dollar sign at the top of the stub.

2. Write the date of the check on the Date line at the top of the stub.

3. Write to whom the check is to be paid on the To line at the top of the stub.

4. Record the purpose of the check on the For line. 5. Write the amount of the check in the amount

column at the bottom of the stub on the line with the words “Amt. This Check.”

6. Calculate the new checking account balance and record the new balance in the amount column on the last line of the stub.

3. List the steps for preparing a check.

Study Vocabulary Terms!

Quiz at the beginning of class.

Review Chapter 4 Test

On your Own, Section 5.1

NO. $

DATE 20 CHECK NO. ____________

TO DATE

FOR

$

BAL.BRO'T FOR'D . . . . . . . . . . . . .

AMT. DEPOSITED DOLLARS

SUBTOTAL . . . . . . . . . . . . . . . . . . . FOR CLASSROOM USE ONLY

A report of deposits, withdrawals, and bank balances sent to a depositor by a bank.

Account service charges are also listed on the bank statement.

When a bank receives a check:

The amount of each check is deducted from the depositor’s account.

The bank stamps the checks to indicate that the checks are canceled and are not to be transferred further.

Canceled checks may be returned to a depositor with a bank statement or may be kept on record by the bank.

Reasons bank records and depositor records may differ: A service charge may not have been charged

in the depositor’s business records Outstanding deposits may be recorded in the

depositor’s records but not on a bank statement

Outstanding checks may be recorded in the depositor’s records but not on a bank statement

A depositor may have made math or recording errors

The bank seldom makes errors but when errors are found, notify the bank immediately.

Example of a bank error:

Check or deposit recorded to the wrong account.

Bank statement is reconciled by verifying that information on a bank statement and a checkbook are in agreement.

Reconciling immediately is an important aspect of cash control.

For canceled checks listed on the bank statement, a check mark is placed on the corresponding check stub.

Check stubs without check marks indicate that they are still outstanding.

Outstanding checks ◦ Checks that have been issued by the depositor but

not yet reported on the bank statement.

Outstanding deposits ◦ Deposits made at the bank but not yet shown on a

bank statement.

1. Write the date on which the reconciliation is prepared

2. In the left amount column, list the balance brought forward on the next unused check stub.

3. In the space for bank charges, list any charges.

4. Write the adjusted check stub balance in the space provided at the bottom of the left amount column.

5. Write the ending balance shown on the bank statement in the right column.

6. Write the date and the amount of any outstanding deposits in the space provided. Add the outstanding deposits. Write the total outstanding deposits in the right column.

7. Add the ending bank statement balance to the total outstanding deposits. Write the total in the space for the subtotal.

8. List the outstanding checks and their amounts in the space provided. Add the amounts of the outstanding checks and write the total in the right column.

9. Calculate the adjusted bank balance, and write the amount in the space provided at the bottom of the right amount column. The subtotal minus the total outstanding checks equals the adjusted bank balance.

10. Compare adjusted balances. The adjusted balances must be the same. The adjusted check stub balance is the same as the adjusted bank balance. Because the two amounts are the same, the bank statement is reconciled. If the two adjusted balances are not the same, the error must be found and corrected before any more work is done.

Balance on check stub

-Bank service charge

-Bank fees

= Adjusted check stub balance

Balance on Bank Statement + Outstanding deposits - Outstanding checks =Adjusted bank balance

Steps:

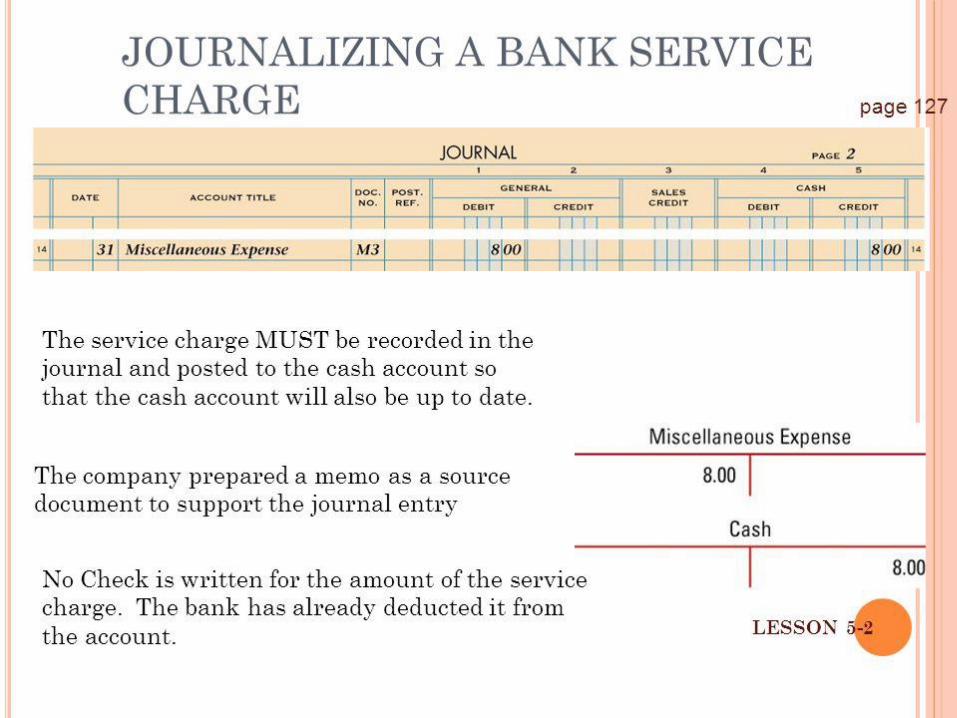

1. Write service charge on the check stub under the heading “Other.”

2. Write the amount of the service charge in the amount column.

3. Calculate and record the new subtotal on the Subtotal line. A new Balance Carried Forward is not calculated until check is written.

2. Debit. Write the title of the account to be debited, Miscellaneous Expense, in the account title column. Record the amount debited in the General Debit column.

3. Credit. Record the amount credited in the Cash Credit column.

4. Source Document. Write the source document number in the Doc. No. column.

1. List four reasons why a depositor’s records and a bank’s records may differ.

◦ A service charge may not have been charged in the

depositor’s business records

◦ Outstanding deposits may be recorded in the depositor’s records but not on a bank statement

◦ Outstanding checks may be recorded in the depositor’s records but not on a bank statement

◦ A depositor may have made math or recording errors

2. If a check mark is placed on the check stub of each canceled check, what does a check stub with no check mark indicate?

◦ That the check is outstanding.

Balance on check stub

-Bank service charge

-Bank fees

= Adjusted check stub balance

Balance on Bank Statement + Outstanding deposits - Outstanding check total =Adjusted bank balance

Reconciliation of Bank Statement Date:

Balance on Check Stub No. . . . . . . . . Balance on Bank Statement . . . . . . .

Have you seen “Returned Check Fee” signs posted by check out registers? What is the usual penalty? What are the results for not keeping track of how much money is in a checking account? What do you know about balancing a check register? List your answers.

Complete sentences – to be turned in.

Dishonored Checks –

A check that a bank refuses to pay.

Banks dishonor when the account of the person who wrote the check has insufficient funds to pay the check.

Other reasons banks dishonor checks:

1. The check appears to be altered.

2. The signature of the person who signed the check does not match the one on the signature card at the bank.

3. The amounts written in figures and in words do not agree.

4. The check is postdated.

5. The person who wrote the check has stopped payment on the check.

Issuing a check on an account with insufficient funds is illegal.

Altering or forging a check is also illegal.

A dishonored check may affect the credit rating of the person or business that issued the check.

The depositor’s bank will charge the depositor a fee for handling the check. The person who wrote the check will also have a fee charged to them by their bank.

State Return Check Fees

Alabama Return Check Fee 30.00$

Arkansas Return Check Fee 25.00$

Florida Return Check Fee 25.00$

Georgia Return Check Fee 30.00$

Louisiana Return Check Fee 25.00$

Mississippi Return Check Fee 40.00$

Missouri Return Check Fee 25.00$

Tennessee Return Check Fee 30.00$

But most penalties for forgery will include a combination of restitution and jail time, the length of which depends on the severity of the crime. First offenses for smaller amounts of money will receive the more lenient sentencing. No matter how small the crime, though, a person convicted of forgery will have felony criminal record.

A bounced check does not directly affect your credit score, but it could have an indirect effect on it.

Banks do not report bounced checks to the major credit bureaus - Experian, Equifax and Transunion - so a bounced check won’t show up on your credit report and won’t impact your credit score.

But, the person to whom you wrote the bad check to can report your bad check to a collection agency if not paid. The collection agency can in turn report your bad check to the credit bureaus.

1. Write dishonored check on the line heading “Other.” The amount is the amount of the dishonored check plus the service fee.

2. Write the total of the dishonored check in the amount column.

3. Calculate and record the new subtotal on the Subtotal line.

2. Debit – Write the title of the account to be debited in the account title column. Record the amount debited in the General Debit column. Example: Accounts Receivable - Name

3. Credit – Write the amount credited in the Cash Credit column.

4. Source Document – Write the source document number in the Doc. No. column

2. Debit – Write the title of the account to be debited in the account title column. Record the amount debited in the General Debit column. Example: Accounts Payable - Name

3. Credit – Write the amount credited in the Cash Credit column.

4. Source Document – Write the source document number in the Doc. No. column

2. Debit – Write the title of the account to be debited in the account title column. Record the amount debited in the General Debit column. Example: Supplies

3. Credit – Write the amount credited in the Cash Credit column.

4. Source Document – Write the source document number in the Doc. No. column

JOURNAL PAGE 17

1 2 3 4 5

DOC. POST

NO. REF.

12 5 Supplies M12 2 4 00 2 4 00

DATE ACCOUNT TITLEGENERAL SALES CASH

DEBIT CREDIT CREDIT DEBIT CREDIT

List six reasons why a bank may dishonor a check.

1. Banks dishonor when the account of the person who wrote the check has insufficient funds to pay the check.

2. The check appears to be altered. 3. The signature of the person who signed the

check does not match the one on the signature card at the bank.

4. The amounts written in figures and in words do not agree.

5. The check is postdated. 6. The person who wrote the check has stopped

payment on the check.

2. What account is credited when electronic funds transfer is used to pay cash on account?

Answer: Cash

3. What account is credited when a debit card is used to purchase supplies?

Answer: Cash

JOURNAL PAGE

1 2 3 4 5

DOC. POST

NO. REF.DATE ACCOUNT TITLE

GENERAL SALES CASH

DEBIT CREDIT CREDIT DEBIT CREDIT

Petty Cash

An amount of cash kept on hand and used for making small payments.

Used for small payments when writing a check is not time or cost efficient.

Small payment amount differs from company to company.

Petty cash is considered an asset and has a normal debit balance.

Online banking has become very popular.

How is your identity protected when you use this banking option?

What would be your concerns?

What are the advantages of using the online banking services?

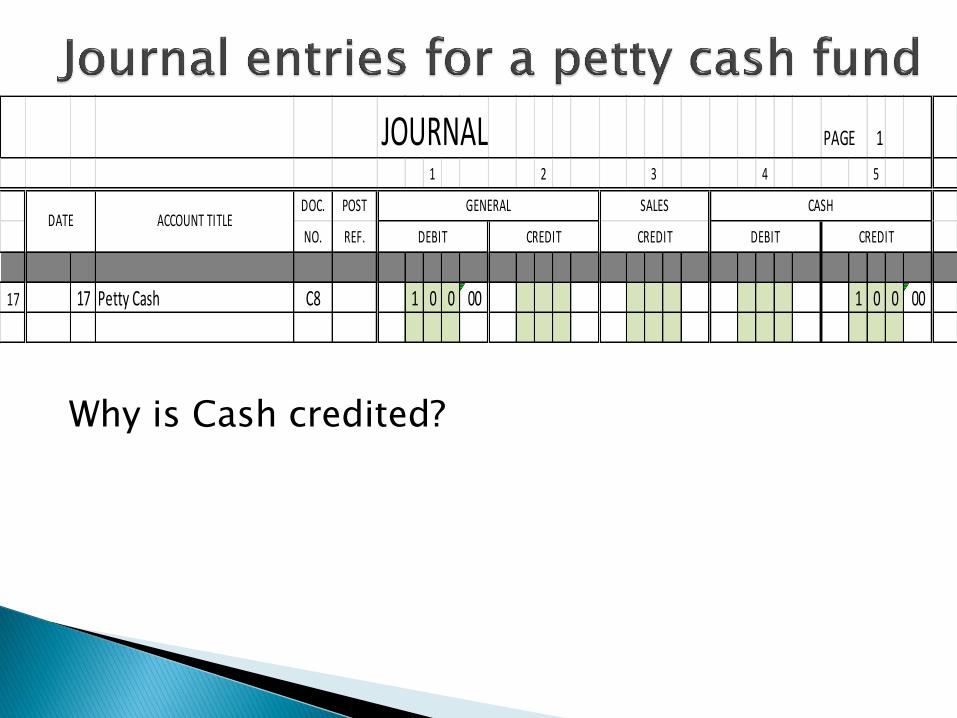

1. Date – Write the date in the date column.

2. Debit – Write the title of the account to be debited, Petty Cash, in the account title column. Record the amount debited in the General Debit column.

3. Credit – Write the amount credited in the Cash Credit column.

4. Source Document – Write the source document number in the Doc. No. column. Source document will be a check.

Why is Cash credited?

JOURNAL PAGE 1

1 2 3 4 5

DOC. POST

NO. REF.

17 17 Petty Cash C8 1 0 0 00 1 0 0 00

DATE ACCOUNT TITLEGENERAL SALES CASH

DEBIT CREDIT CREDIT DEBIT CREDIT

Petty Cash Slip – A form showing proof of a petty cash payment

Shows the following information: 1. Petty cash slip number 2. Date of petty cash payment 3. To whom paid 4. Reason for payment 5. Amount paid 6. Account in which the amount is to be recorded 7. Signature of the person approving the petty

cash payment

Petty cash slips are kept in the petty cash box until the fund is replenished.

No entries are made in the journal for the individual petty cash payments.

As petty cash is paid out, the amount in the petty cash box decreases.

Eventually the petty cash fund must be replenished & petty cash payments recorded.

Petty cash fund can be replenished at any time but must be replenished at the end of the month so that all of the expenses are recorded in the month they are incurred.

Proof of Fund Must be completed before petty cash is

replenished. The last line of the proof must show the same

total as the original balance of the petty cash fund.

If the petty cash does not prove, the errors must be found and corrected before any more work is done.

Petty cash remaining in the petty cash fund 70.00$

Plus total of petty cash slips . . . . . . . . . . . . . . . + 30.00