34

International Policy Update & Producer Opportunities Parr Rosson Professor & Director Center for North American Studies Department of Agricultural Economics Texas A&M University C NAS

International Policy Update &

Producer Opportunities

Parr Rosson

Professor & Director

Center for North American Studies

Department of Agricultural Economics

Texas A&M University

CNAS

Overview

Trade Trends

International Institutions

Trade Agreements

Conclusions & Implications

Trade Trends &

International Setting

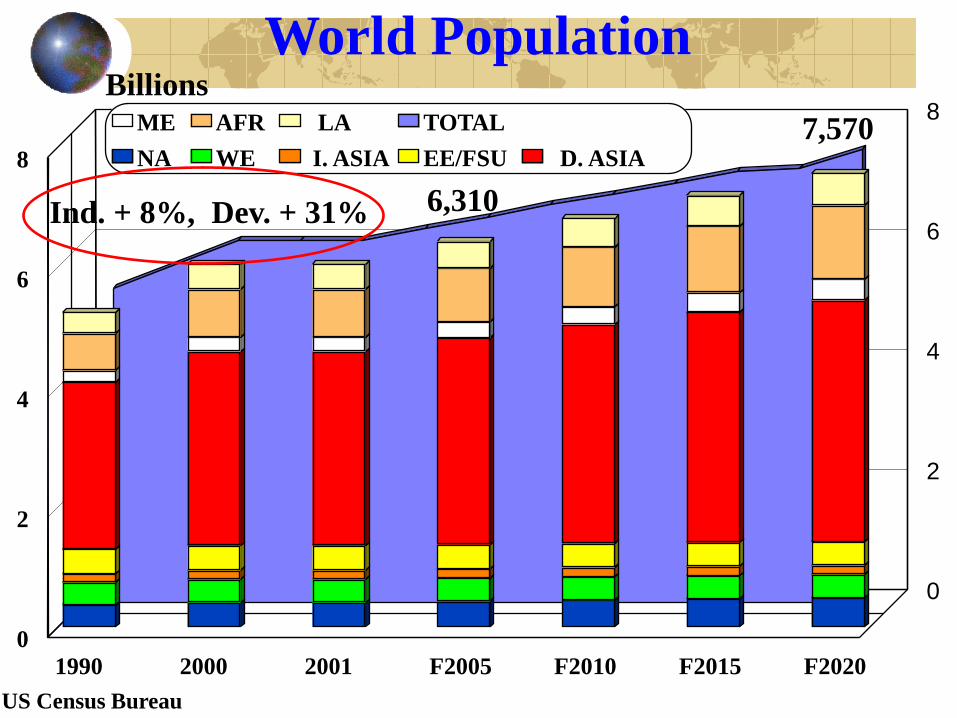

World Population

US Census Bureau

1990 2000 2001 F2005 F2010 F2015 F2020 0

2

4

6

8

0

2

4

6

8

NA WE I. ASIA EE/FSU D. ASIA

ME AFR LA TOTAL

Billions

6,310

7,570

Ind. + 8%, Dev. + 31%

World Economic Output

Global Insight, Inc., World Economic Outlook, 2002.

1990 2000 2001 F2005 F2010 F2015 F2020 $0

$10

$20

$30

$40

$50

$60

$70

NA WE I. ASIA EE/FSU

D. ASIA ME AFR CSA

GDP, Trillion 1997 Dollars

Ind. + 64%, Developing + 140%

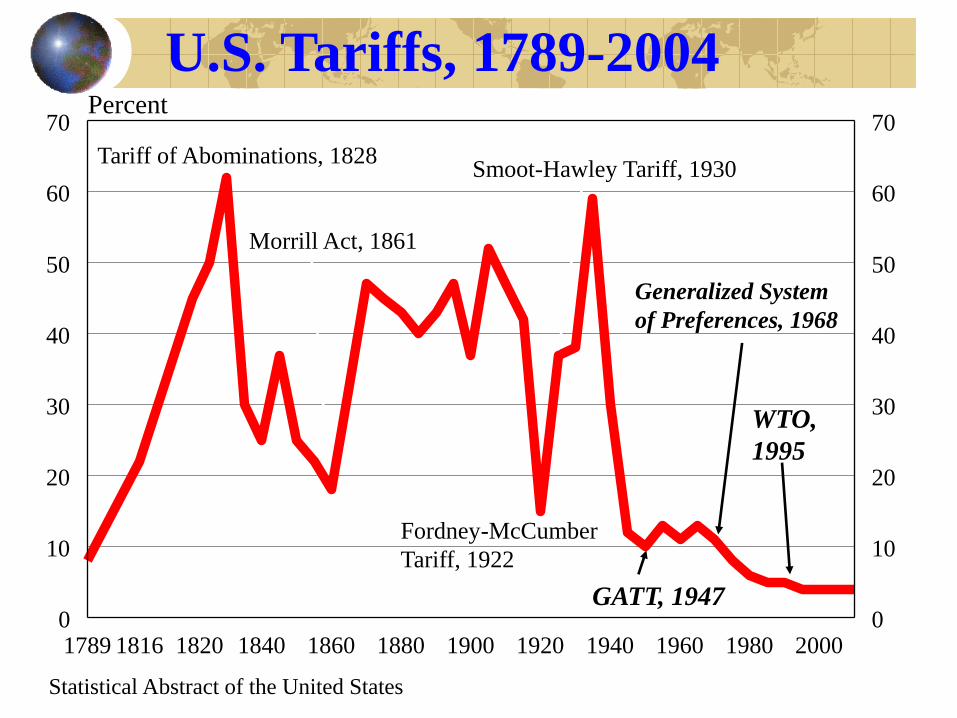

U.S. Tariffs, 1789-2004

Statistical Abstract of the United States

1789 1816 1820 1840 1860 1880 1900 1920 1940 1960 1980 2000 0

10

20

30

40

50

60

70 Percent

0

10

20

30

40

50

60

70

Tariff of Abominations, 1828

Morrill Act, 1861

Smoot-Hawley Tariff, 1930

Generalized System

of Preferences, 1968

Fordney-McCumber

Tariff, 1922

GATT, 1947

WTO,

1995

World Average Agricultural Tariffs, 2002

Source: WTO & ERS/USDA

115

85

55

40 30 25

10

0

20

40

60

80

100

120

140

Percent

Region Average

World Average

62%

Source: U.S. Trade Internet System, www.fas.usda.gov/ustrade

2000 2001 2002 2003 2001 2005

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

Billion Dollars

Canada Mexico Japan EU-25 China/HK

Taiwan Korea Turkey Indonesia Russia

Top 10 U.S. Ag Export Markets

U.S. Agricultural Trade, 1970-2006F

Source: U.S. Trade Internet System, www.fas.usda.gov/ustrade

2006 Forcast for Fiscal Year f rom USDA/FAS (Feb 06 Forecast)

19701975

19801985

19901995

20002005

2006F

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0Billion Dollars

Exports Imports

Since 2000:

Exports + 25%

Imports + 50%

Trade Surplus Vanishes

Observations

Disparity in Population & Income

Growth

Disparity in Use of Trade Barriers

Disparity in Agricultural Trade Growth

Finally Seeing China Emerge as

Market, Cuba Growing

Questions About Role & Future

Importance of Trade

International Institutions &

Trade Strategies

U.S. Trade Strategy

Unilateral

Generalized System of Preferences (GSP)

CBI/CBERA

African Growth Opportunities Act (AGOA)

Regional/Bilateral

NAFTA, CAFTA-DR, Others

Multilateral

World Trade Organization

Only Forum Where All 150 Member Countries Are Present & Farm Policy Is Negotiated

Concurrent

Initiatives

Doha Development Agenda in the

World Trade Organization (2001-6?)

The Hong Kong

Ministerial

December 13-18, 2005

Agreement on Reductions by April 30, 2006

Draft Schedules Due July 31, 2006

Conclude Negotiations December 31, 2006

Three Pillars for Negotiations in

Agriculture

Market Access

Export Competition

Domestic Support

Negotiations Under Tight Timeline

Due to Expiration of TPA July

2007

Hong Kong, December 2005

Little Progress Made in Hong Kong

EU Trade Commissioner said state of negotiations was “serious but not desperate.”

Agreement to Eliminate Export Subsidies by 2013

Greater “Quota-Free, Duty-Free” Access Granted LDCs, Up to 97% of Products

LDC’s want it above 99% and Prepared to Veto

While Many Fundamental Issues Remain Unresolved, Deadlines Have Been Set

Hong Kong, December 2005 (continued)

Agreement on Degree of Tariff Cuts by April 30, 2006 EU Wants to Reduce by 39% (They Claim 46%) while U.S.

and Others Think EU Needs to Reduce by about 60%

Each Country to Submit Tariff Schedules by July 30

While Export Subsidies Addressed, More work on STE’s and Export Credit Guarantees Needed

Agreement Still Needed on Cuts in Trade Distorting Domestic Support (Amber/Blue) U.S. Wants about 53%, Pushing EU and Japan Towards 80%

This Does Not Address Green Box Programs

U.S. wants “New” Blue Box for CCPs

Other Negotiating/Related Issues

NAMA (Non-Ag Market Access)

The Cotton Case (DS 267)

U.S. Budget Situation

Dissension within EU (France vs.

Everyone Else)

Observations

WTO Could Result in No Substantial

Agreement

Future of WTO May Be On the Line

Agreement Important to U.S.

Open Markets

Get Rid of Export Subsidy Distortions

Minimize Litigation Over Farm Policy

Role of Trade Agreements

Why Regional Agreements?

2d Best After MTN

WTO Has Been Slower than Desired

Outcome is Uncertain

Economic Incentives

Open Markets

Increase Business Efficiency

Keep Pressure on MTN to Perform

Strategic Considerations

Secure Strategic Materials

Oil, Fertilizer, Natural Gas

Stem Illegal Immigration by Creating

Economic Opportunity in Other

Countries

Create ‘Buffer Zone’ Against

Terrorism (9/11 Commission Report)

Australia ‘05

Bahrain ‘05 CAFTA-DR

‘05

Chile ‘04

FTAA ‘06

Morocco ‘04

Southern African

Customs Union ‘06

Singapore ‘03

Jordan ‘01

U.S. Trade Agreements

NAFTA ‘94 Israel ‘85

CUSTA, ‘89

Andean FTA

‘06

Panama ‘06

Thailand ‘06

MEFTA

‘06

S. Korea

Trade Agreements In-Place (7)

Israel-1985-1994

Canada-US

(CUSTA)-1989-1998

North America

(NAFTA)-1994-2008

US-Mexico

US-Canada

Canada-Mexico

Jordan-December

17, 2001-2010

Chile-January 1,

2004-2015

Singapore-May 6

2003-2012

Australia-January 1,

2005-2022

Trade Agreements-Pending (10)

Morocco-President

Signed 8/17/04, Pending

Signature, King of

Morocco

CAFTA-DR-Signed by

President, (20 Years to

Full Implementation)

Bahrain-Pending

Submission to Congress

Panama-Nine

Negotiating Sessions

Held, Panama Delays

Colombia, Ecuador,

Peru (ANDEAN)-

Nine Rounds,

Negotiations Continue

Thailand-Three

Rounds Held

S. Korea - 2007

Trade Agreements-Pending (10)

Southern African Customs Union

(SACU): Botswana, Namibia, Lesotho,

Swaziland, South Africa-Six Rounds

Held

MEFTA: Oman & United Arab

Emirates

Under Negotiation: Egypt, Others??

Dominican

Republic,

800 Miles

NE

North

Houston,

1,300 Miles

NW

Mexico

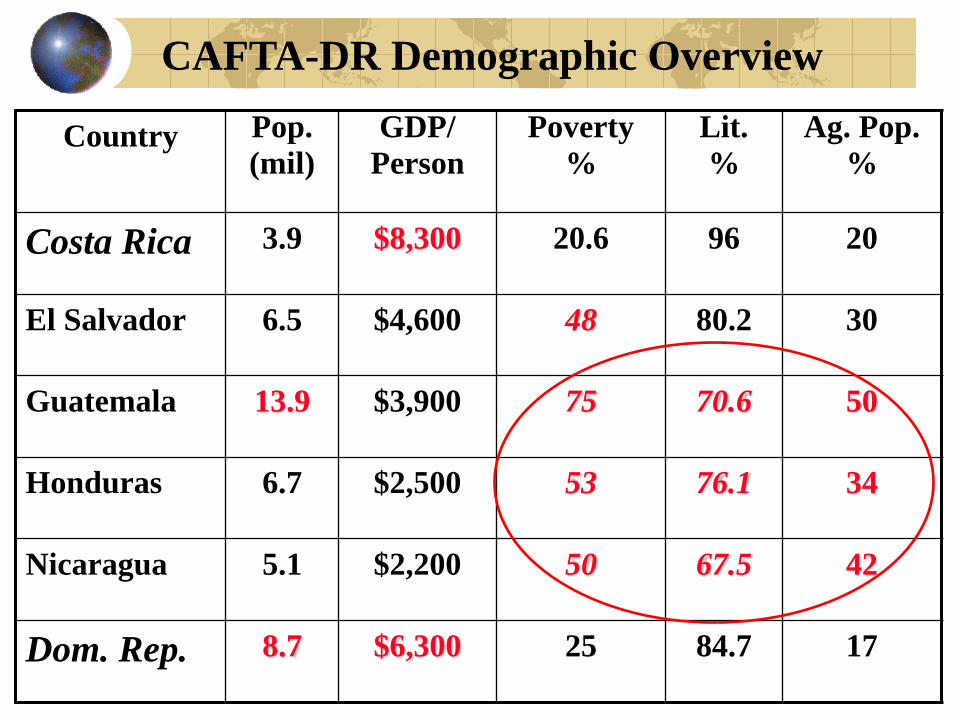

Country Pop.

(mil)

GDP/

Person

Poverty

%

Lit.

%

Ag. Pop.

%

Costa Rica 3.9 $8,300 20.6 96 20

El Salvador 6.5 $4,600 48 80.2 30

Guatemala 13.9 $3,900 75 70.6 50

Honduras 6.7 $2,500 53 76.1 34

Nicaragua 5.1 $2,200 50 67.5 42

Dom. Rep. 8.7 $6,300 25 84.7 17

CAFTA-DR Demographic Overview

CAFTA-DR Prospects

U.S. Ag. Export Gains of $1.5 Billion Annually

Near Term: HQ Beef, Cotton, Wheat & Soybeans

Long Term: Rice, Dairy, Pork, Poultry & Corn

Challenges: Sugar, Cantaloupe, Honeydew

Limitations: Infrastructure, Income Growth/Distribution, Plant & Animal Health

Other Opportunities: Investment

CAFTA-DR Ag. Trade, 2003

USDA, FATUS.

Grains & Feeds

43.5%

Oilseeds

19.4%

Meats

15.2% Veg/Fruit

8.7%

Cotton

3.5%

Other

9.6%

Bananas

25.4%

Fruit/Veg

19.9%

Fish

18.0%

Coffee

17.3%

Sugar

7.1% Other

12.4%

US Exports: $1,339 million US Imports: $2,654 million

Observations

Agreements May Be Necessary Condition for Opening New Markets for Agriculture

Time is Crucial Due to Expiration of TPA

Some Agreements Easier than Others

Future of Free Trade of the Americas in Serious Doubt

Conclusions and Implications

Conclusions & Implications

U.S. Market Is Open, Rest of World Is Not

U.S. Export Growth Lags Import Growth

If Trade Growth is Important, Disparities Must

Be Addressed

Progress in WTO Important to U.S. & Texas

for at Least 2 Reasons:

Markets

Farm Policy

Conclusions & Implications

Reductions in Trade Distorting Domestic

Support Likely Substantial Some Adjustment for U.S. Producers

Absent WTO Progress, Expect More

Litigation in WTO Aimed at Farm U.S. Policy

Trade Reform is at a Crossroads: Protection or

Progress? If Export Markets Are Important, Trade Agreements &

WTO Progress Are Necessary, But Not Sufficient

Thank You!

Questions?

Parr Rosson

Department of Agricultural Economics

Texas A&M University

College Station, TX 77843-2124

E-mail: [email protected]

Telephone: 979-845-3070